Global Soybean Meal Market Size, Share, Trends, COVID-19 Impact & Growth Forecast Report, Segmented By raw material (Organic and inorganic), process of production (normal soybean meal, De-hulled [min 50% protein] Hipro Soybean meal, Defatted soya flour toasted, and de-fatted soya flakes toasted), Application (food industry, beverage, dietary supplements, and healthcare products), distribution channel (supermarket, specialized stores, online stores, and retail stores), And Region (North America, Europe, Asia Pacific, Latin America, and Middle East - Africa), Industry Analysis From 2026 to 2034

Market Size, 2025

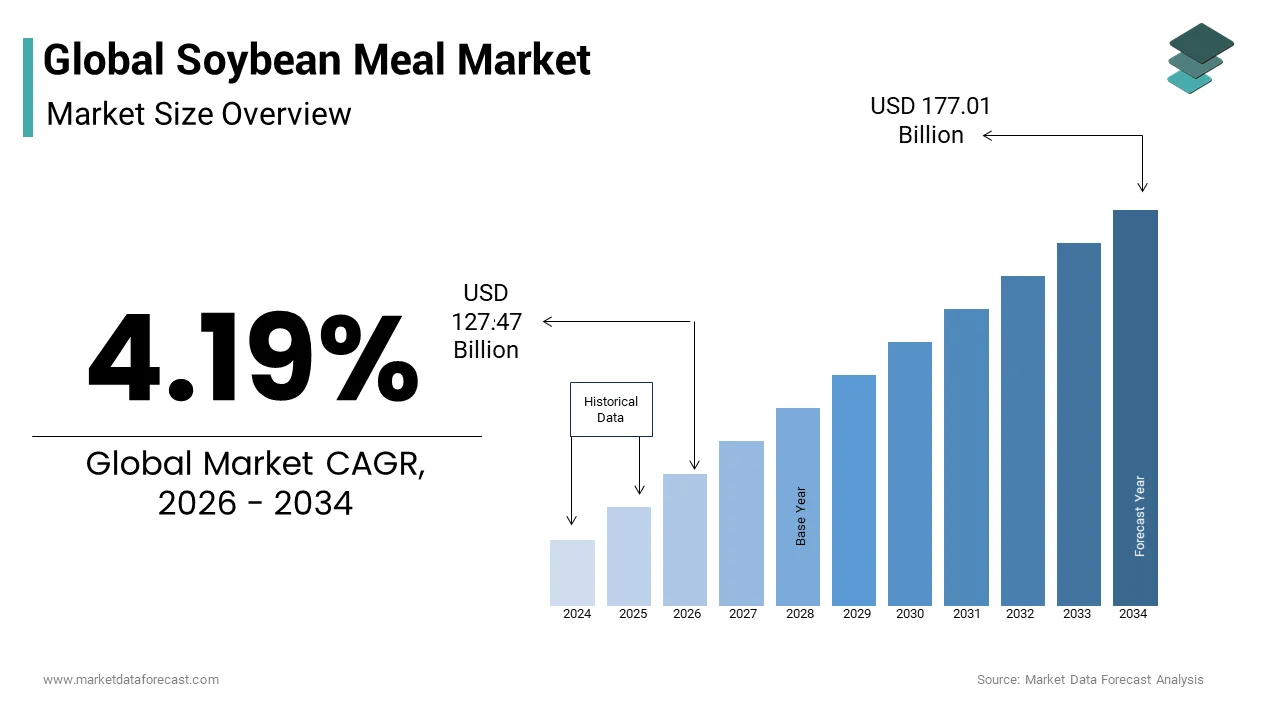

$122.34 BnMarket Estimate, 2026

$127.47 BnMarket Forecast, 2034

$177.01 BnCAGR, 2026–2034

4.19%Global Soybean Meal Market Size

The global soybean meal market size was valued at USD 122.34 billion in 2025 and is anticipated to reach USD 127.47 billion in 2026 and USD 177.01 billion by 2034, growing at a CAGR of 4.19% during the forecast period from 2026 to 2034.

Soybean meal is the main source of animal feed that improves the metabolism and the immune system of growing cattle. Soybean meal is a concentrated source of protein and energy and contains less fiber than most other oilseed meals available to the feed manufacturer. The higher protein, energy, and fiber content of soybean meal allows nutritionists to formulate more energy-efficient diets that are more efficient at turning food into meat.

Soybean meal is a by-product of soybean oil extraction. Soy flour is a rich source of protein that is used as food for humans and livestock. Soybean meal is mainly classified into two types: protein soybean meal, containing 47% -49% protein from shelled seed,s and conventional soybean meal containing 43% -44% protein in the shell. Soy flour is used in the widest variety of products, including animal feed, baked goods, health foods, cosmetics, and the manufacture of antibiotics.

MARKET DRIVERS AND RESTRAINTS

Soybean meal is expected to generate extremely good income in 2017-2027 because it is rich in protein. It can be used as food for humans and livestock, used in health products, and in the preparation of protein shakes. Due to the increasing demand for soybean meal for the manufacture of protein supplements and animal feed at a high rate, manufacturers are manufacturing and launching several new soybean meal products with improved protein content. These factors are the main drivers of this market, and demand is expected to increase year on year. To meet the growing demand, manufacturers are strategizing to remain the key player. The production of soybean meals at a high rate due to the increasing demand is a limitation for the soybean meal market because production is limited. The growing trend of the companion animal and pet health segment is another factor driving the market demand for soybean meals.

IMPACT OF COVID-19 ON THE SOYBEAN MEAL MARKET

The start of the coronavirus pandemic coincided with the peak harvest season. As markets are closed, there is a threat to the harvest on over 100 lakh hectares in the country.

Even between different segments, the impact varies considerably between different regions and between producers and salaried workers. This impact will reverberate throughout the economy and will last for more than a few months. Problems emerged after the COVID-19 pandemic. Despite all the measures and given the continued restrictions on the movement of people and the movement of vehicles, concerns have been expressed about the negative implications of the COVID-19 pandemic on the agricultural economy. Today's agriculture's immediate problems are classified mainly into two headings: For crop production, most of the planting process will be virtually unchanged in the summer. Therefore, there would be no impact as such on the availability of seeds at the moment. But if the same scenario continues until the end of the year, then seed availability can certainly be a problem. Due to the disruption of world trade, farmers face shortages of agricultural inputs such as fertilizers and pesticides. In a shorter period, there is little to wait. In the longer term, the delivery of fertilizers through international markets could become a problem, as some production plants in China have been closed.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.19% |

| Segments Covered | Raw Material, the Process of production, the Food industry, the Distribution channel |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Vippy Industries Ltd, Mukwano Group, Granol Industria, Zhongken Guobang (Tianjin) Co. Ltd., Gauri Agrotech Products Pvt. Ltd. |

SEGMENTAL ANALYSIS

By Raw Material Insights

The market segmentation for soybean meal can be divided into raw materials, the process of production, the food industry, and the distribution channel. Soybean meal is segmented on the basis of raw materials into organic and inorganic. Due to increasing health problems, people prefer organic soy flour because organic products are good for health.

The soybean meal market is segmented according to the process of production as normal soybean meal, shelled soybean meal,n meal [min. 50% protein] Hipro and shelled [min. 48% protein] Hipro soybean meal, toasted defatted soybean meal, and toasted defatted soybean flakes are commercially available. Regular soybean meal has a lower protein content than shelled soybean meal, which has about 45-46% crude protein content. Cockles are by-products that are eliminated because they have no place in human food, but are used for ruminants. According to its application in the food industry, Soy flour is segmented according to beverages, dietary supplements, and health products. In the food market segment, soybean meals can be used to make soybean chunks and soybean granules.

Deflated soy flour is used to make nutritious cookies. Soy flour protein isolates are used as protein shakes. Soy flour products are healthy and nutritious, so the market demand for the food and beverage market segments is high. In the health products market segment, soy flour is used to make products that contain isoflavones that have chemical similarities to estrogen. Demand from the dietary supplement market segment is higher as soy flour is used to make supplements rich in calcium, magnesium, iron, and folic acid. Soy flour is segmented according to the distribution channel: supermarkets, specialized stores, online stores, and retail stores. Online stores are the preferred mode of purchase for both consumers and manufacturers because they are convenient for both. Supermarkets have also acquired a good consumer base over the last ten years and are expected to grow at a significant rate.

REGIONAL ANALYSIS

North America Market Analysis

North America holds the dominant share of the market. Soy flour must be manufactured at a higher rate to meet the needs of the market. But with increasing harvests, there is a threat of disease. Soybean rust is a fungal disease that originated in Asia. It has spread to soybean fields in South American countries such as Brazil, Argentina, Chile, and finally to the US. The prevention and control of soybean rust requiresexpensive fungicidese, and the damage to yield is extreme. This disease represents a potential threat to the growth of the soybean meal market.

According to the Soybean Meal Information Center, almost 60% of the total soybean meal is consumed in China, the EU, and the United States together. China is the main producer of soybean meal, followed by the United States, while the main importers of soybean meal are Vietnam, Belgium, and Spain. Exports are dominated by the United States, Italy, and India. One of the biggest improvements in soybean cultivation is the rapid adoption of no-tillage technologies by farmers in South and North America. Although soy is produced mainly in a limited number of countries, it is widely traded, and soy flour is available in almost all countries.

LEADING COMPANY

Vippy Industries Ltd had the largest share of the Soybean Meal Market in terms of sales revenue in 2024.

KEY MARKET PLAYERS

The Soybean Meal Market is concentrated with well-established players. Key players in the Soybean Meal Market include

- Vippy Industries Ltd

- Mukwano Group

- Granola Industria

- Zhongken Guobang (Tianjin) Co., Ltd.

- Gauri Agrotech Products Pvt. Ltd.

- Bonne Vie Soybean Meal

- Gimatex Industries Pvt. Ltd.

- Eco Export

- Shafer Commodities Inc.

- Nordic Soya.

RECENT MARKET NEWS

- Bunge Netherlands B.V. and Bunge France SAS announced the successful completion of the acquisition of two crushing facilities from Cargill following the approval and closing of the transaction. The soybean and rapeseed crushing and soybean oil refining plant at the port of Amsterdam in the Netherlands,s and part of the bulk port terminal assets, ts have now been transferred to Bunge, and the soybean crushing plant and rapeseed located in the port of Brest, France. Both sites and their staff are now an integral part of Bunge's regional operations in Europe, the Middle East,ast and Africa (EMEA), and the global soybean crushing platform.

- Trade in 2018-19 was boosted after Iran began accepting post-US rupee sanctions.

- After the US sanctions, a sharp increase in demand from Iran's feed industry has improved the outlook for soybean meal exports from India. According to the latest data released by the Solvent Extractors Association of India (SEA), soybean meal exports to Iran for the year 2023-2029 amounted to 508,050 tons, much more than 22,910 tons last year.

- As the average price of a ton of soybean meal fell slightly in the first half of this month, some have said that the chicken farmer's purchasing power in relation to this raw material increased. However, this is only true compared to the previous month (in the first half of March, a drop of just over 1% compared to the average of last February). Because, until now, the price of soybean meal remains, monthly, at the second-highest level in history.

- Consolidated Grain and Barge Co. (CGB) acquired the food-grade soy division of Quality Technology International, Inc. (QTI). The new food-grade soy business will market, ship, and sell specialty feed soybeans through containers in Japan and domestically for processing and resale to Japanese food manufacturers.

MARKET SEGMENTATION

This research report on the global soya bean meal market is segmented and sub-segmented into the following categories.

By Raw Material

- Organic

- Inorganic

By Process of Production

- Normal Soya bean Meal

- De-hulled Hipro soya bean meal (min 50% protein)

- Defatted soya flour toasted

- De-fatted soya flake toasted

By Application

- Food Industry

- Beverage

- Dietary supplements

- Health care products

By Distribution Channel

- Supermarket

- Specialized Stores

- Online stores

- Retail Stores

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What is the soybean meal market?

The soybean meal market refers to the global industry involved in the production, trade, and consumption of soybean meal, a high-protein animal feed ingredient obtained after extracting oil from soybeans.

Why is soybean meal important in agriculture?

Soybean meal is a primary protein source in livestock, poultry, aquaculture, and pet feed, improving growth, feed efficiency, and overall animal health due to its high digestible protein content.

What drives growth in the soybean meal market?

Growth is driven by rising demand for meat and dairy products, expanding livestock and aquaculture sectors, population growth, and increasing animal feed consumption in developing and developed regions.

How is soybean meal produced?

Soybean meal is produced by cleaning, dehulling, flaking, and extracting oil from soybeans, after which the remaining defatted cake is processed into meal for feed use.

What are the common types of soybean meal?

Common types include high-protein soybean meal and dehulled soybean meal, differentiated by protein content, digestibility, and feed formulation requirements.

Which animals commonly consume soybean meal?

Soybean meal is widely used in poultry, swine, beef cattle, dairy cattle, aquaculture, and pet food diets due to its high protein and amino acid balance.

Which regions dominate the soybean meal market?

Key regions include North America, South America (especially Brazil and Argentina), Europe, and Asia-Pacific, driven by major soybean production and strong feed demand.

How do soybean meal prices affect the market?

Soybean meal prices are influenced by soybean crop yields, global supply and demand, weather conditions, oilseed processing capacity, and export dynamics.

What are the key trends in the soybean meal market?

Key trends include growth in aquaculture feed demand, sustainability and traceability efforts, alternative protein research, and premium feed formulation innovations.

Are there sustainable soybean meal options?

Yes. Sustainable practices include certified responsible sourcing, non-GMO meal, low-carbon footprint supply chains, and traceability initiatives for environmentally conscious feed buyers.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com