Sugar Market Size, Share, Trends & Growth Forecast Report – Segmented By Product Type (White Sugar, Brown Sugar, Liquid Sugar), Form, End-Use, Sector and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2025 to 2033

Global Sugar Market Summary

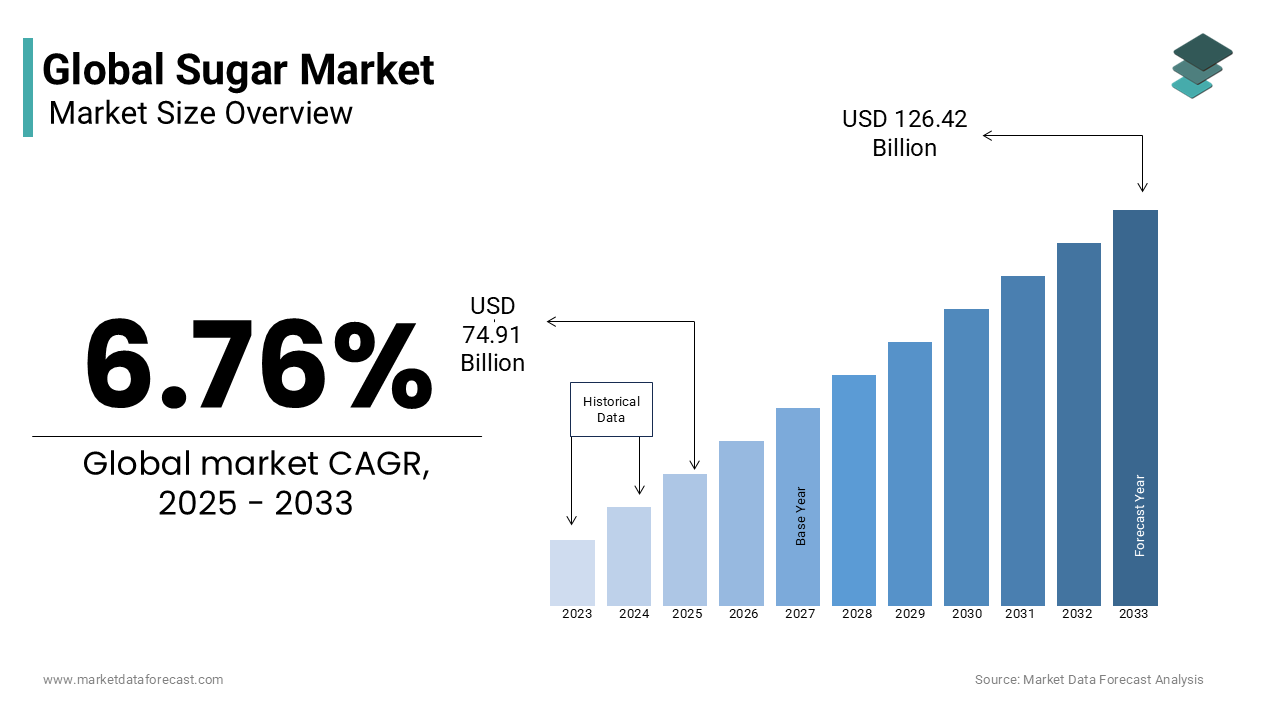

The global sugar market was valued at USD 70.16 billion in 2024, is estimated to reach USD 74.91 billion in 2025, and is projected to reach USD 126.42 billion by 2033, expanding at a CAGR of 6.76% from 2025 to 2033. The growth of the global sugar market is driven by rising consumption in the food and beverages sector, strong demand for confectionery and bakery products, and expanding use of sugar in processed foods and packaged drinks. Furthermore, population growth and increasing demand in emerging economies are accelerating market expansion.

Key Market Trends

- Growing demand for processed foods and beverages in developing countries.

- Increasing investments in sugar refining and production technologies.

- Rising consumption of confectionery and bakery items worldwide.

- Adoption of sugar in biofuel production as an alternative energy source.

- Expansion of Asia-Pacific sugar production and exports, particularly in India and Thailand.

Segmental Insights

- Based on product type, the white sugar segment dominated the global sugar market in 2024, supported by its wide use across food and beverage industries.

- Based on form, the granulated sugar segment accounted for a prominent share in 2024, driven by its versatility in industrial and household applications.

- Based on end-use sector, the food and beverages segment held a significant share of the sugar market in 2024, owing to its extensive utilization in packaged foods, soft drinks, and desserts.

Regional Insights

- Asia-Pacific was the top performer in the global sugar market, holding the largest share in 2024 due to high production and consumption in India, China, and Thailand.

- Europe contributed significantly, with strong demand for confectionery and bakery products.

- North America showed stable growth, supported by the food processing and beverage industries.

- Latin America emerged as a leading sugar producer, particularly Brazil, which plays a critical role in global sugar exports.

Competitive Landscape

Major players in the global sugar market include Südzucker AG (Germany), Raízen (Brazil), Tereos (France), Cosan S.A. (Brazil), Mitr Phol Group (Thailand), Associated British Foods plc (UK), Nordzucker AG (Germany), Louis Dreyfus Company (Netherlands), Wilmar International Ltd (Singapore), Thai Roong Ruang Sugar Group (Thailand), E.I.D.–Parry (India) Limited, Dalmia Bharat Sugar and Industries Limited, Balrampur Chini Mills Ltd, and Shree Renuka Sugars. These companies focus on the expansion of refining capacity, vertical integration, and global trade partnerships to strengthen their market presence.

Global Sugar Market Size

The sugar market was valued at USD 70.16 billion in 2024, is estimated to reach USD 74.91 billion in 2025, and is projected to reach USD 126.42 billion by 2033, growing at a CAGR of 6.76% from 2025 to 2033.

Sugar is the global production, trade, and utilization of sucrose derived primarily from sugarcane and sugar beet, serving as a fundamental caloric sweetener in food and beverage systems. The crop occupies over 26 million hectares worldwide, which is making it one of the most extensively grown tropical crops. Sugar beet, though less prevalent, contributes substantially in temperate zones, particularly in the European Union, where it represents about 80% of domestic sugar output. The World Health Organization notes that global per capita sugar consumption has plateaued at around 24 kilograms annually.

MARKET DRIVERS

The entrenched role in biofuel production in the form of sugarcane-based ethanol, which exerts significant influence on global supply dynamics is fuelling the growth of the Sugar market. This dual-use flexibility allows millers to shift output between sugar and ethanol based on international prices, creating a structural linkage between energy and agricultural markets. Ethanol accounted for 48% of Brazil’s road transport fuel mix in 2023, according to the Brazilian Ministry of Mines and Energy, reinforcing domestic demand for sugarcane. According to the European Commission, bioethanol from sugar beet contributed 1.7 million cubic meters to the EU’s renewable transport fuel supply in 2022, supporting climate targets under the Fit for 55 package.

The persistent demand for sugar in emerging-market processed food and beverage industries, where rising disposable incomes and urbanization fuel consumption of packaged goods is additionally fuelling the growth of the Sugar market. In Nigeria, the confectionery sector expanded by 11% in 2022, driven by local production of candies, baked goods, and dairy desserts, according to the National Bureau of Statistics. Sugar remains the preferred sweetener in these regions due to its cost-effectiveness, functional properties in texture and preservation, and consumer familiarity. As per the International Diabetes Federation, urban populations in Southeast Asia and West Africa are increasingly exposed to sugar-sweetened products through expanding retail networks.

MARKET RESTRAINTS

The escalating regulatory pressure on sugar consumption due to its association with non-communicable diseases, particularly obesity and type 2 diabetes is restricting the growth of Sugar market. As of 2023, 56 countries have implemented sugar-sweetened beverage taxes, according to the World Health Organization, including Mexico, South Africa, and Thailand, where such policies have led to measurable shifts in consumer behavior. Additionally, front-of-pack warning labels in Chile reduced the sales of high-sugar products by 24% between 2016 and 2020, as per the University of Chile’s Nutrition and Food Institute. These public health interventions not only dampen demand but also increase compliance costs for manufacturers reformulating products.

The vulnerability of sugar production to climate variability in tropical growing regions where sugarcane predominates is limiting the growth of the Sugar market. In 2023, India experienced a 14% reduction in sugar output compared to the previous year due to erratic monsoon patterns and prolonged drought in Maharashtra and Karnataka, as reported by the Indian Sugar Mills Association. Similarly, Thailand, the world’s third-largest sugar exporter, saw yields drop by 18% in the 2022–2023 season due to water shortages, according to the Office of the Cane and Sugar Board. The Intergovernmental Panel on Climate Change projects that climate change could reduce global sugarcane productivity by up to 13% by 2050 under high-emission scenarios, as outlined in its Sixth Assessment Report. These climatic pressures increase production uncertainty, elevate price volatility, and challenge the sustainability of large-scale monoculture systems in water-stressed regions.

MARKET OPPORTUNITIES

The development of high-intensity sweeteners and specialty sugars derived from sugarcane is likely to grow. In 2023, Brazil launched commercial production of rare sugars such as allulose and tagatose at pilot biorefineries operated by Biosev and Raízen, leveraging enzymatic conversion of sugarcane syrup, as confirmed by the São Paulo Research Foundation. These low-calorie monosaccharides exhibit 70–90% of sucrose’s sweetness but with minimal glycemic impact, making them attractive for diabetic and weight-management formulations. Additionally, unrefined specialty sugars like panela, jaggery, and muscovado are gaining premium positioning in organic and clean-label markets. According to the Organic Trade Association, U.S. retail sales of minimally processed cane sugars grew by 19% from 2020 to 2023.

The integration of circular economy principles in sugar production, where mills transform waste streams into energy, bioplastics, and agricultural inputs is also expected to elevate the growth of the Sugar market. Some facilities, such as those operated by EID Parry, have achieved energy self-sufficiency and export surplus power. Moreover, vinasse, a byproduct of ethanol fermentation, is being repurposed as a liquid fertilizer in Colombia, reducing synthetic nitrogen use by up to 30%, according to the Colombian Sugarcane Research Center (CENICAÑA).

MARKET CHALLENGES

The land-use competition between sugarcane cultivation and food security or conservation priorities is a challenging factor for the growth of the sugar market. In Indonesia, sugarcane expansion has contributed to the conversion of over 120,000 hectares of agricultural land between 2015 and 2022, according to the Ministry of Agriculture, often at the expense of rice paddies and smallholder farms. This shift has raised concerns about domestic food self-sufficiency, especially in regions already vulnerable to grain shortages. In Mozambique, large-scale sugar estates occupy fertile coastal zones that could otherwise support diversified farming, as noted in a 2023 land audit by the Center for African Studies at Eduardo Mondlane University.

The labor intensiveness and declining rural workforce availability in key sugar-producing regions is additionally hampering the growth of the sugar market. Sugarcane harvesting remains heavily reliant on manual labor in countries like India, Pakistan, and the Philippines, where mechanization rates are below 20%, as per the International Labour Organization. However, younger generations are increasingly migrating to urban centers, creating labor shortages during peak harvest seasons. In 2022, Maharashtra sugar mills reported a 30% deficit in available cutters, which is leading to delayed processing and sucrose loss, according to the Sugarcane Workers’ Welfare Board. Mechanization is hindered by small landholdings and hilly terrain, while rising wage demands increase production costs.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Type, Form, End-User and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Key Market Players | Südzucker AG from Germany, Raízen from Brazil, Tereos from France, Cosan S.A. from Brazil, Mitr Phol Group from Thailand, Associated British Foods plc from the UK, Nordzucker AG from Germany, Louis Dreyfus Company from the Netherlands, Wilmar International Ltd from Singapore, Thai Roong Ruang Sugar Group from Thailand, E.I.D. – Parry (India) Limited, Dalmia Bharat Sugar and Industries Limited, Balrampur Chini Mills Ltd, and Shree Renuka Sugars. |

SEGMENTAL ANALYSIS

By Product Type Insights

The white sugar segment dominated the global sugar market share in 2024 with its universal acceptance in industrial food and beverage manufacturing, where purity, consistency, and long shelf life are paramount. White sugar, with a sucrose content exceeding 99.8%, is the preferred sweetener for carbonated drinks, baked goods, and dairy products due to its neutral flavor and predictable crystallization behavior. In the United States, over 70% of commercially produced soft drinks rely exclusively on refined white sugar or high-purity sucrose blends, according to the American Beverage Association. Furthermore, its compatibility with automated production lines in large-scale facilities makes it indispensable in modern processing.

The liquid sugar segment is likely to grow with an emerging CAGR of 6.8% during the forecast period. This acceleration is fueled by its superior solubility and ease of integration in beverage production, particularly in ready-to-drink (RTD) formats. Liquid sugar, typically a 66% sucrose solution, eliminates the need for on-site dissolution, reducing energy consumption and processing time in bottling plants. In India, RTD tea and flavored water production increased by 15% in 2022, with manufacturers shifting from granulated to liquid sugar to improve efficiency, according to the Indian Bottlers’ Federation.

By Form Insights

The granulated sugar segment was accounted for a prominent share of the global sugar market in 2024 due to its versatility and widespread use across both industrial and household applications. Granulated sugar is the default form in bakery, confectionery, and dairy processing due to its controlled crystal size, flowability, and stability during storage. In the European Union, over 80% of industrial bakeries use granulated sugar as the primary sweetening agent, as confirmed by the European Confederation of Food Industries. Additionally, it remains the most accessible and affordable form for retail consumers, particularly in developing nations where bulk dry sugar is distributed through traditional supply chains.

The syrup sugar segment is likely to grow with an expected CAGR of 7.2% throughout the forecast period with its functional advantages in food manufacturing in texture modulation, moisture retention, and browning control. Syrup sugar often derived from inverted sucrose or high-maltose blends is increasingly used in premium bakery items, ice creams, and processed fruit products to enhance mouthfeel and extend shelf life. Moreover, the growth of plant-based and clean-label products has amplified demand for natural syrup-based sweeteners as alternatives to high-fructose corn syrup.

By End-Use Sector Insights

The food and beverages segment was accounted in holding a significant share of the sugar market in 2024 with sugar’s irreplaceable role in flavor enhancement, preservation, and texture development across a vast array of processed products. In India, the organized food processing sector consumed over 12 million tons of sugar in 2023 with rapid expansion in packaged snacks and dairy desserts, as reported by the Ministry of Food Processing Industries.

The pharma and personal care segment is anticipated to expand at a CAGR of 5.9% during the forecast period with the increasing use of sucrose and its derivatives as excipients in oral solid dosage forms, including tablets and syrups. Sucrose acts as a binder, filler, and flavor masker in pediatric and geriatric formulations, with over 40% of liquid pediatric medicines in Europe containing sucrose as a key ingredient, as confirmed by the European Medicines Agency. Additionally, in personal care, sugar-based surfactants such as alkyl polyglucosides are gaining traction in natural and eco-friendly skincare products due to their biodegradability and low irritation potential.

REGIONAL ANALYSIS

Asia Pacific Sugar Market Insights

Asia Pacific is the largest regional contributor to global sugar production and consumption and accounted for a very large share of white sugar volumes in 2024, with region-specific analyses putting Asia Pacific at roughly 38 percent of the white sugar market that year. The region combines heavy-producing countries such as India, Thailand and China with large industrial consumers in food processing and beverages. Asia Pacific’s dominance stems from extensive sugarcane area expansion and strong domestic demand for sweetened beverages and staples. The OECD and FAO project that Asia will supply an even larger share of global sugar output over the coming decade, driven by capacity growth in Southeast Asia and South Asia. Rapid urbanisation and rising processed food consumption across the region support structurally higher industrial sugar demand and frequent policy interventions on trade and export quotas from major producers such as India, further influencing global trade balances and prices.

North America Sugar Market Insights

North America occupies an important but not dominant position in global sugar supply and demand and serves as a large domestic industrial user and refined sugar markets. In 2024, the United States produced roughly 11.74 million metric tons of sugar, which represents about 6.45 percent of an approximate 182.11 million metric tons global market in 2024 based on production totals and published estimates. The United States concentrates much of the region’s refining capacity and the food processing industry in North America accounts for high industrial demand in confectionery beverages and baked goods, sustaining stable output even as public health campaigns pressure sugar use. The U.S. sugar sector is notable for heavy policy support, including import quotas and price supports, which shape trade flows and regional prices, and the country supplies refined sugar to Canada and Mexico under established trade patterns. The U.S. also leads in investment in alternative sweeteners and reformulation initiatives, which influence North American consumption trends. Production and supply projections are monitored closely by the USDA, which publishes seasonal production and supply outlooks that inform trading and industrial contracting decisions.

Europe Sugar Market Insights

Europe plays a specialist role in the global sugar market as the leading beet sugar-producing region and a sizable refined sugar consumer, representing roughly 8.8 percent of world sugar production in 2024 when measured against global tonnage estimates. The European Union remains the world’s principal producer of beet sugar and produced about 15 to 17 million tonnes in recent seasons, underpinning domestic food manufacturing and confectionery sectors. European production is under pressure from rising costs and regulatory and environmental constraints, which have driven consolidation of factories and intermittent reductions in beet area. At the same time, import flows into the EU have increased, especially from lower-cost exporters, which have pushed down domestic prices and prompted industry restructuring. Demand in Europe is gradually shifting because of public health initiatives that target sugar in beverages and processed food,s which is influencing reformulation efforts by major food manufacturers. The EU’s sugar policy changes and farmer responses therefor,e directly affect planting choices and seasonal supply profiles across the region.

Latin America Sugar Market Insights

Latin America stands as the single most influential sugar region globally, with a leading share of global trade and production and an estimated regional market share of approximately 38.3 percent in 2024, driven by Brazil’s very large output. Brazil alone accounts for a very large slice of world sugarcane and sugar output and is the largest exporter of both raw and refined sugar, supported by integrated mills that co-produce ethanol, which smooths industry economics. The region’s tropical climate, scale of cultivation and efficient milling technology enable low unit costs and large exportable surpluses that set global pricing benchmarks. Seasonal shifts in Brazil and policy choices on ethanol blending strongly affect world supply and price volatility. Latin America’s export orientation means that swings in Brazilian planting and cane yields translate quickly into international price movements and import demand shifts in consuming regions.

Middle East & Africa Sugar Market Insights

The Middle East and Africa together remain a smaller contributor to global sugar volumes relative to the other major regions, with combined production in the low single-digit share range of global output in 2024, roughly about six percent when Africa’s production of about 10.4 million tonnes is considered against global totals. Africa’s output is growing modestly with country-level expansions in South Africa, Egypt and a few others, but many countries still import significant quantities to meet domestic demand. The Middle East is principally an importer of sugar and a region where refinery capacity and sugar trade logistics matter for food security and industrial users. Growth constraints include water scarcity, limited irrigated cane area in many countries and infrastructure gaps, although targeted investments and public policy reforms in select nations aim to expand domestic processing and reduce import dependence. Health policy trends and subsidy regimes in several states also shape consumption and trade flows regionally.

COMPETETIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global sugar market include

- Südzucker AG (Germany)

- Raízen (Brazil)

- Tereos (France)

- Cosan S.A. (Brazil)

- Mitr Phol Group (Thailand)

- Associated British Foods plc (UK)

- Nordzucker AG (Germany)

- Louis Dreyfus Company (Netherlands)

- Wilmar International Ltd (Singapore)

- Thai Roong Ruang Sugar Group (Thailand)

- E.I.D. – Parry (India) Limited

- Dalmia Bharat Sugar and Industries Limited

- Balrampur Chini Mills Ltd

- Shree Renuka Sugars

The competitive landscape of the sugar market is shaped by a blend of state-influenced producers, multinational agribusinesses, and cooperatives by operating in a highly regulated and climate-sensitive environment. Unlike commoditized sectors, competition is not solely price-driven but increasingly defined by sustainability credentials, supply chain transparency, and value-added capabilities. Brazilian and Indian producers dominate volume, while European and Asian firms focus on quality and specialty applications. Technological differentiation in processing and co-product utilization is emerging as a key advantage.

Top Players in the Sugar Market

Wilmar International is a dominant agribusiness player in the Asia Pacific sugar sector, with integrated operations spanning cultivation, refining, and distribution across Indonesia, India, and China. The company operates large-scale sugar mills in Indonesia, particularly in Sumatra and Java, where it leverages vertically aligned supply chains to ensure consistent quality and traceability. In 2023, Wilmar expanded its specialty sugar portfolio by launching unrefined cane sugars under the “Sunny Gold” brand in Singapore and Malaysia, targeting health-conscious consumers seeking minimally processed alternatives. It has also strengthened partnerships with regional food manufacturers, supplying customized liquid and crystalline sugars for beverage and bakery applications.

Mitr Phol Group is headquartered in Thailand, stands as one of the largest sugar producers in Asia, with extensive operations in Thailand, Laos, and Australia. The company processes over 16 million tons of sugarcane annually and has strategically expanded its footprint in the Asia Pacific by exporting refined sugar to Japan, South Korea, and Taiwan under stringent food safety protocols. In 2022, Mitr Phol launched a bio-refinery initiative in Khon Kaen, Thailand, which is converting bagasse into renewable energy and developing pilot projects for sugar-based bioplastics in collaboration with Chulalongkorn University. The company has also invested in precision agriculture technologies to improve cane yield and water efficiency across its estates.

Shree Renuka Sugars is a major Indian sugar conglomerate that has significantly influenced the Asia Pacific market through its export activities and diversification into ethanol and renewable energy. The company operates multiple sugar mills in Maharashtra and Karnataka by producing both white and specialty sugars for domestic and international clients. Additionally, it has expanded ethanol production capacity to meet India’s national blending mandate, positioning sugar as a dual-output commodity.

Top Strategies Used by Key Market Participants

Key players in the sugar market are adopting vertical integration, product diversification, sustainability certification, technological modernization, and strategic export expansion to consolidate their positions. Companies are investing in end-to-end control from farm to refinery to ensure quality and traceability. Others are shifting toward high-value segments such as specialty sugars, ethanol, and bio-based materials. Precision agriculture and automation are being deployed to enhance yield and reduce environmental impact. Partnerships with research institutions are enabling innovation in bioproducts, while compliance with international sustainability standards strengthens market access.

MARKET SEGMENTATION

The research report on the Sugar Market has been segmented and sub-segmented based on categories.

By Product Type

- White Sugar

- Brown Sugar

- Liquid Sugar

By Form

- Granulated Sugar

- Powdered Sugar

- Syrup Sugar

By End-Use Sector

- Food and Beverages

- Pharma and Personal Care

- Household

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the sugar market?

The sugar market refers to the global industry involved in the production, processing, and distribution of sugar derived from sugarcane and sugar beet. It includes raw sugar, refined sugar, and value-added products.

Which countries are the largest producers of sugar?

Brazil, India, Thailand, the European Union, and the United States are the top sugar-producing countries globally.

What drives the growth of the sugar market?

Factors driving growth include increasing demand for sweeteners in food and beverages, rising population, urbanization, and growing consumption of processed foods and beverages globally.

What are the challenges in the sugar market?

Challenges include price volatility, climate-related production risks, changing regulations, and increasing health concerns related to sugar consumption.

What are the recent trends in the sugar market?

Recent trends include the rise of organic and specialty sugars, integration of sugar production with ethanol and bioenergy, and increased focus on sustainable and environmentally friendly cultivation practices.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com