- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$8,707 MnMarket Estimate, 2026

$8968.2 MnMarket Forecast, 2034

$11,361 MnCAGR, 2026–2034

3%Executive Summary: Global Tourism and Hospitality Market

- Market Scope: Comprehensive global tourism and hospitality market analysis covering travel types, service categories, travel models, regional leadership frameworks, and key strategic developments.

- Market Valuation: Valued at USD 8,707 million (2025), estimated at USD 8,968.2 million (2026), and projected to reach USD 11,361 million by 2034, registering a robust CAGR of 3% (2026–2034).

- Primary Growth Drivers: Resurgence of pent-up demand for cross-border leisure travel and the integration of artificial intelligence for hyper-personalized guest experiences. Opportunities include the expansion of regenerative tourism models and digital nomadism, balanced against restraints like geopolitical instability and acute labor shortages.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Type | Domestic tourism (constituted the largest share in 2025 due to resilience against external disruptions) | International tourism (projected to expand at a CAGR of 14.2% from 2026 to 2034) |

| By Services Provided | Lodging (represented the largest share at 34.3% in 2025) | Recreation (emerging as the fastest-growing category with a projected CAGR of 15.8%) |

| By Travel Model | Leisure tourism (dominated with 65.3% of global travel volume in 2025) | Business travel (experiencing the fastest recovery with a projected CAGR of 12.6%) |

| By Region / Country | North America (held the largest share at 26.3% in 2025, supported by high disposable income and air connectivity) | Asia-Pacific region (projected high-growth trajectory driven by expanding middle-class economies) |

Major Market Players & Market Structure

Market Structure: Highly competitive global travel and hospitality landscape featuring leading platforms, hospitality groups, and travel agencies competing on generative AI integrations, marketplace expansions, and sustainability initiatives.

Key Companies: TUI Group, TCS World Travel, Expedia Group, American Express Global Business Travel, Gray & Co, Booking Holdings, Air BnB, Trip.com Group Ltd., TripAdvisor, Inc., Royal Holdings Co., Ltd., Marriott International, Hilton Worldwide Holdings Inc., and Intercontinental Exchange Inc.

Global Tourism and Hospitality Market Size

The global tourism and hospitality market was valued at USD 8,707 million in 2025, is estimated to reach USD 8,968.2 million in 2026, and is projected to reach USD 11,361 million by 2034, growing at a CAGR of 3% from 2026 to 2034.

Tourism and Hospitality refer to the services and infrastructures designed to accommodate, transport, and engage individuals traveling for leisure, business, or cultural purposes. It includes lodging establishments such as hotels, resorts, and alternative accommodations, alongside transportation networks, food and beverage services, tour operations, and destination management. Unlike transactional industries, this sector thrives on experiential value, curating memorable interactions that reflect local culture, comfort, and personalized service. A defining characteristic of modern tourism is its deep interdependence with geopolitical stability, environmental conditions, and global mobility frameworks.

According to the World Meteorological Organization, extreme weather events have disrupted travel itineraries in several countries since 2020, affecting everything from coastal resort operations to mountain trekking routes. Urban centers like Barcelona and Bangkok have seen tourism, illustrating their economic centrality. With digital platforms now shaping traveler expectations emphasizing instant booking, real-time reviews, and hyper-local experiences the industry is undergoing a transformation where service agility and cultural authenticity are becoming as critical as infrastructure quality.

MARKET DRIVERS

Resurgence of Pent-Up Demand for Cross-Border Leisure Travel

The sustained release of pent-up demand following prolonged pandemic-related restrictions is a primary catalyst revitalizing the global tourism and hospitality market. The concept of "revenge travel" has emerged as a behavioral trend, particularly among millennials and high-income demographics, who are allocating significant portions of disposable income to international trips. This resurgence is amplified by flexible work arrangements; remote employment has enabled "workcations," where professionals extend business trips into leisure stays. Countries like Portugal and Thailand have introduced digital nomad visas, attracting a large number of long-term visitors in 2023 alone, as reported by their respective immigration authorities. Additionally, social media platforms such as Instagram and TikTok have intensified destination desirability through viral content, turning remote locations like the Azores and Bhutan into high-demand spots. This reawakening of global wanderlust, rooted in psychological recovery and digital connectivity, is driving unprecedented booking volumes and reshaping travel seasonality.

Integration of Artificial Intelligence in Guest Experience Personalization

The deployment of artificial intelligence to deliver hyper-personalized guest experiences, fundamentally altering service delivery across hotels, airlines, and tour operators, is another transformative driver. Leading hospitality chains are leveraging machine learning algorithms to analyze guest behavior, preferences, and historical data to anticipate needs before explicit requests are made. Chatbots and virtual concierges, such as those implemented by Hilton’s “Connie” and Accor’s “Ask A&O,” handle a significant portion of routine inquiries, freeing staff for high-touch engagements. Furthermore, AI is optimizing dynamic pricing models by assessing real-time demand signals, local events, and competitor rates, enabling more precise revenue management. In luxury resorts across the Maldives and Santorini, facial recognition and IoT-enabled rooms adjust lighting, temperature, and music playlists upon guest entry, creating seamless, intuitive environments. As consumer expectations evolve toward invisibility in service where needs are met without effort the integration of AI is no longer a competitive edge but a foundational requirement for operational excellence and emotional resonance in modern hospitality.

MARKET RESTRAINTS

Escalating Geopolitical Instability and Travel Disruptions

The growing frequency and impact of geopolitical conflicts and regional instability a significant impediments to the steady recovery of the tourism and hospitality market. Armed confrontations, civil unrest, and diplomatic tensions directly disrupt air connectivity, deter international arrivals, and trigger travel advisories that suppress consumer confidence. Beyond direct conflict zones, spillover effects influence neighboring regions. Additionally, political crackdowns on dissent or restrictive visa policies in countries like Belarus and Myanmar have led to sustained international isolation, limiting tourism inflows. These unpredictable disruptions not only cause immediate revenue loss but also erode long-term destination branding, making recovery difficult even after hostilities subside.

Labor Shortages and Workforce Sustainability in Hospitality Services

The acute shortage of skilled labor, particularly in frontline roles such as housekeeping, culinary services, and guest relations, is a persistent structural challenge confronting the tourism and hospitality market. This gap stems from long-standing issues, including low wage structures, seasonal employment, and physically demanding work environments, which have been exacerbated by pandemic-era job exits. European resorts in Spain and Greece have reported turning away bookings due to insufficient kitchen and cleaning staff, with some properties operating at notable capacity despite full reservation calendars. The problem is equally acute in Asia. Moreover, younger generations are increasingly reluctant to enter the industry due to a perceived lack of career progression and work-life imbalance. Without systemic reforms in wages, training, and employee well-being, the labor deficit threatens service quality, operational scalability, and the overall guest experience, undermining the sector’s ability to capitalize on renewed travel demand.

MARKET OPPORTUNITIES

Expansion of Regenerative Tourism and Community-Based Travel Models

The shift from sustainable tourism to regenerative tourism, a model that goes beyond minimizing harm to actively restoring ecosystems and empowering local communities, is a transformative opportunity. Unlike conventional tourism, which often extracts economic value without equitable distribution, regenerative approaches prioritize co-creation with indigenous populations, environmental rehabilitation, and cultural preservation. In Costa Rica, community-led eco-lodges in the OSA Peninsula have adopted regenerative practices such as reforestation, wildlife corridor restoration, and fair-trade artisan partnerships, increasing local income as reported by the Ministry of Environment and Energy. Similarly, Bhutan’s “high-value, low-impact” policy mandates a daily Sustainable Development Fee of $100, which funds conservation, healthcare, and education, ensuring tourism directly benefits national well-being. Luxury operators like &Beyond and Six Senses are embedding regenerative principles into their offerings, allowing guests to participate in coral planting, soil enrichment, and language preservation initiatives. This experiential reciprocity resonates with environmentally and socially conscious travelers, particularly Gen Z and affluent millennials. By transforming visitors into contributors, regenerative tourism redefines the industry’s role from passive service provider to active agent of positive change, unlocking new market differentiation and long-term destination resilience.

Digital Nomadism and the Rise of Long-Term Stay Ecosystems

The institutionalization of digital nomadism, driven by the permanence of remote work and the emergence of dedicated long-term stay infrastructures, is another pivotal opportunity. Unlike traditional tourists, digital nomads stay for weeks or months, generating sustained demand for mid-to-high-end accommodations, co-living spaces, high-speed internet, and hybrid work environments. Bali’s “Bali Digital Nomad Visa” initiative has spurred the development of integrated work-lifestyle hubs, combining boutique lodging with shared offices, wellness centers, and networking events. Real estate developers and hotel chains are adapting accordingly. By catering to this mobile, high-spending demographic, destinations can reduce seasonality, enhance occupancy rates, and foster innovation in service design, positioning themselves at the forefront of the post-industrial travel economy.

MARKET CHALLENGES

Climate-Induced Destination Vulnerability and Seasonal Volatility

The increasing vulnerability of key destinations to climate change, leading to unpredictable seasonality and long-term degradation of natural assets, is one of the most pressing challenges facing the tourism and hospitality market. Coastal resorts, mountain ski areas, and island nations are experiencing accelerated environmental deterioration that undermines their core appeal. The Intergovernmental Panel on Climate Change reports that global sea levels have risen by 3.7 mm per year since 2006, threatening low-lying tourist hotspots such as the Maldives, where 80% of land is less than one meter above sea level. In the Mediterranean, prolonged heatwaves have pushed summer temperatures beyond 40°C, prompting travelers to shift visits to shoulder seasons or alternative regions, disrupting revenue cycles. Similarly, ski resorts in the Alps have seen snow cover duration decline by 38 days per season since 1970, according to the Swiss Federal Institute for Forest, Snow and Landscape Research, forcing investments in artificial snowmaking at prohibitive costs. Coral bleaching in Southeast Asia and the Caribbean has diminished snorkeling and diving attractions, with Australia’s Great Barrier Reef losing 50% of its coral cover since 1995, as confirmed by the Australian Institute of Marine Science. These ecological shifts not only erode destination viability but also necessitate costly adaptation strategies, challenging the sustainability of traditional tourism models.

Over-Tourism and Erosion of Local Social Fabric

The phenomenon of over-tourism, where excessive visitor volumes overwhelm urban and cultural destinations, leading to resident displacement, infrastructure strain, and cultural commodification, is a growing challenge. Iconic cities such as Venice, Barcelona, and Kyoto have reached critical thresholds where tourism inflows exceed local carrying capacity, triggering public backlash and policy. Additionally, the commercialization of cultural rituals such as Bali’s sacred ceremonies being repackaged for tourist performances undermines authenticity and fosters resentment. Balancing economic benefits with community well-being has become a defining governance challenge, requiring innovative zoning, visitor management systems, and inclusive planning to ensure long-term coexistence.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3% |

| Segments Covered | By Type, Services Provided, Travel Model, and Region. |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | France, The UK, Spain, Germany, Italy, Rest of Europe. |

|

Market Leaders Profiled | TUI Group, TCS World Travel, Expedia Group, American Express Global Business Travel, Gray & Co, Booking Holdings, Air BnB, Trip.com Group Ltd., TripAdvisor, Inc., Royal Holdings Co., Ltd., Marriott International, Hilton Worldwide Holdings Inc., Intercontinental Exchange Inc, and Others. |

SEGMENTAL ANALYSIS

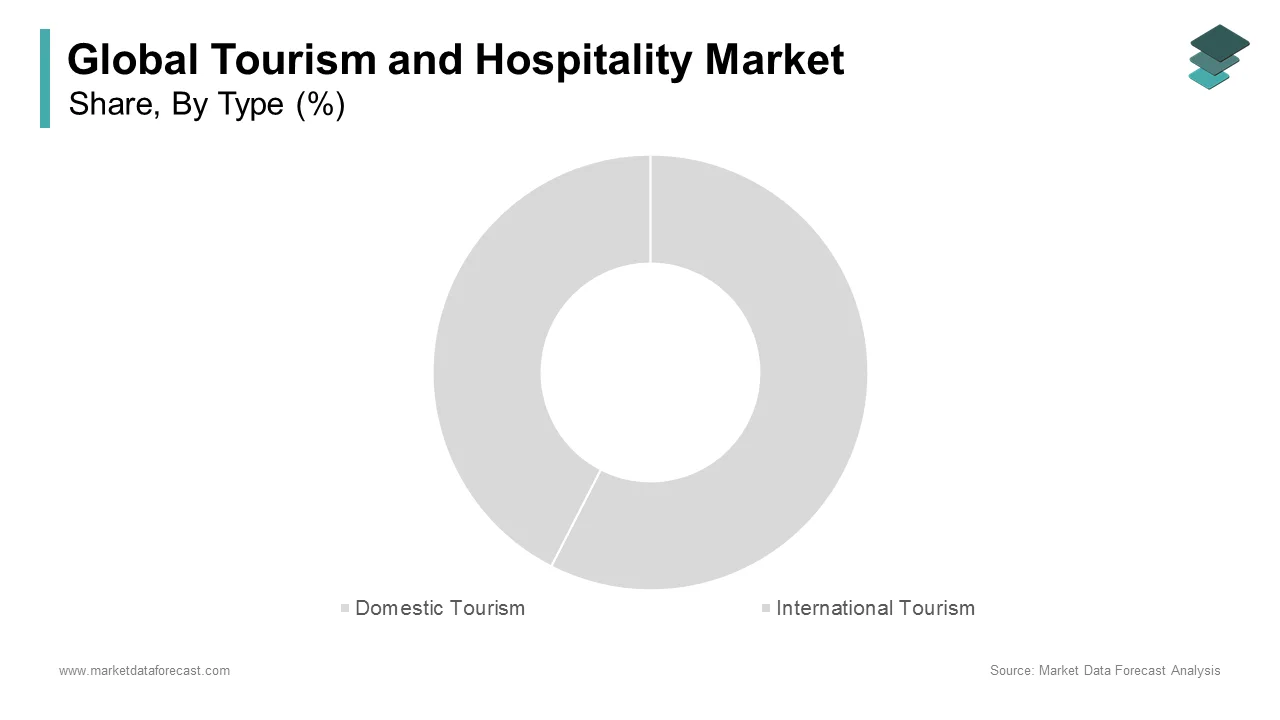

By Type Insights

The domestic tourism segment constituted the largest type of the global tourism and hospitality market by accounting for a substantial share of total travel activity in 2025. This dominance is primarily driven by its resilience to external disruptions such as border closures, visa restrictions, and geopolitical instability. During the pandemic, when international travel declined, domestic tourism remained a critical lifeline for national economies, sustaining hospitality operations and preserving employment. In countries like India and Indonesia, domestic travel is deeply embedded in cultural and religious practices, including pilgrimages and family reunions. A further key factor is affordability; domestic trips typically incur lower transportation and accommodation costs, making them accessible to middle- and lower-income populations. Additionally, governments have actively promoted domestic circuits through marketing campaigns. With rising road and rail infrastructure and the proliferation of regional getaways, domestic tourism continues to serve as the backbone of the sector’s recovery and stability.

The international tourism segment is the fastest-growing and is projected to expand at a CAGR of 14.2% from 2026 to 2034. This acceleration stems from the full reopening of global air networks and the resurgence of long-haul travel, particularly in premium segments. The normalization of visa policies and bilateral air service agreements is a major driver. Apart from these, the expansion of digital nomad visas in several countries, including Spain, Croatia, and Mauritius, has institutionalized medium-term international stays, blurring the line between tourism and relocation. Furthermore, the revival of international conferences and cultural events, such as Expo 2025 in Osaka and UEFA Euro 2025, has reignited business and leisure travel. As global confidence in mobility returns and airlines restore pre-pandemic capacity, international tourism is regaining its role as a high-value, economically transformative force.

By Services Provided Insights

The lodging segment representd the largest service by contributing 34.3% of total revenue in the global tourism and hospitality market in 2025. This lead position is anchored in its indispensability accommodation is a non-negotiable component of every trip, whether for leisure, business, or transit. The sector encompasses a wide spectrum, from luxury hotels and boutique inns to alternative stays like vacation rentals and hostels, allowing for scalability across income groups. The premium pricing power of high-end properties is a primary driver of its dominance. Institutional demand further reinforces growth; corporate contracts, government delegations, and event-based bookings ensure stable occupancy. The rise of hybrid accommodations, such as co-living spaces and workation resorts, has expanded the lodging model beyond traditional stays. With real estate developers and private equity firms increasingly investing in hospitality assets, lodging remains the financial cornerstone of the tourism ecosystem.

The recreation segment is emerging as the fastest-growing service category and is projected to grow at a CAGR of 15.8% in the coming years. This surge is fueled by the increasing demand for experiential travel, where participation in activities defines the trip’s value rather than passive sightseeing. Adventure tourism, cultural immersion, and wellness retreats are now central to travel itineraries. Wellness tourism, a subset of recreation, has seen exponential growth. Additionally, experiential offerings are increasingly personalized through AI and local partnerships; platforms like Withlocals and GetYourGuide enable travelers to book authentic, community-led experiences, from pottery workshops in Kyoto to coffee harvesting in Colombia. The rise of “transformational travel”, where journeys are designed for self-growth and emotional impact, further elevates recreation’s appeal. As travelers shift from consumption to participation, recreation is evolving into the most dynamic and emotionally resonant pillar of the hospitality value chain.

By Travel Model Insights

The leisure tourism segment dominated the travel model segment by capturing 65.3% of global travel volume in 2025. This preeminence is rooted in the fundamental human desire for relaxation, exploration, and personal enrichment, which has only intensified in the post-pandemic era. The psychological need for recovery from prolonged isolation and remote work has triggered a global surge in vacation planning, with families and individuals prioritizing trips that offer emotional restoration. Besides, social media has amplified destination aspiration, with platforms like TikTok generating viral trends that drive mass visitation to locations such as Santorini’s cliffside villages and Japan’s bamboo forests. The flexibility of remote work has further extended leisure trips into “workcations” and slow travel, where stays last weeks rather than days. With leisure travel increasingly viewed as essential to quality of life, it continues to define the rhythm and scale of global tourism demand.

The business travel segment is experiencing the fastest recovery and is projected to grow at a CAGR of 12.6% from 2026 to 2034. This resurgence is driven by the reactivation of in-person corporate engagements that digital platforms cannot fully replicate. While video conferencing reduced the need for routine meetings, high-stakes activities such as contract negotiations, investor roadshows, and team-building retreats require physical presence. Another factor is the strategic importance of face-to-face relationship building. Additionally, corporate travel policies are adapting to hybrid models, combining business trips with leisure extensions, known as “bleisure” travel. With multinational firms resuming global operations and supply chain coordination requiring on-site presence, business travel is regaining its role as a high-yield, structurally essential component of the tourism economy.

REGIONAL ANALYSIS

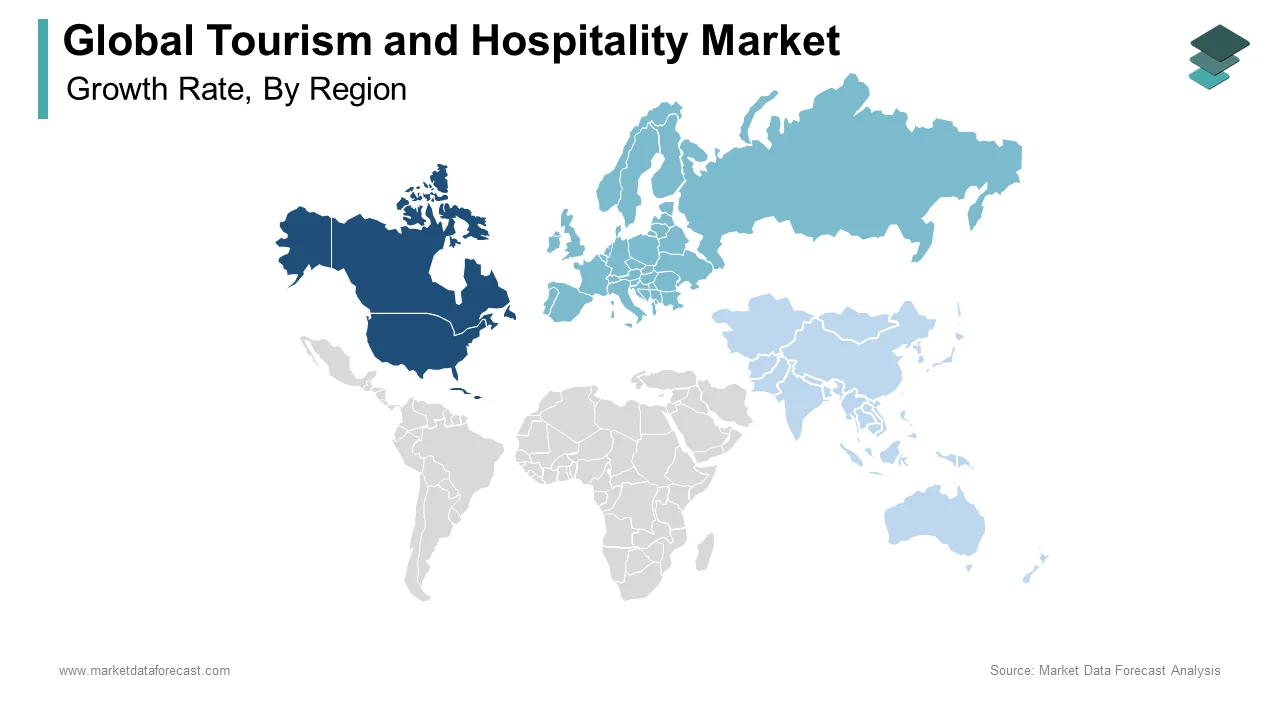

North America Tourism and Hospitality Market Insights

North America held the largest share of the global tourism and hospitality market at 26.3% in 2025. The region’s position is underpinned by high disposable income, extensive air connectivity, and a deeply ingrained travel culture. Domestic travel remains robust. The region’s hospitality infrastructure is highly diversified, ranging from luxury resorts in Florida to tech-integrated hotels in major urban centers. Las Vegas and Orlando continue to dominate leisure travel, while cities like New York and Chicago are key MICE destinations. The integration of digital payment systems, contactless check-ins, and AI concierges has elevated service standards. Moreover, the U.S. government’s expansion of the Visa Waiver Program to include additional European and Asian countries has facilitated inbound mobility. With strong consumer confidence and resilient corporate travel, North America remains a cornerstone of global tourism demand.

Europe Tourism and Hospitality Market Insights

Europe held a significant market share. The region benefits from dense cultural heritage, compact geography, and seamless intra-regional mobility enabled by the Schengen Area. France, Italy, and Spain are among the world’s most visited nations. Urban tourism thrives in cities like Paris, Barcelona, and Vienna, while rural and alpine destinations attract niche markets such as eco-tourism and winter sports. The region is also a leader in cultural tourism. Germany’s business tourism sector is particularly strong. With strong institutional support and a balanced mix of leisure and business travel, Europe maintains a dominant and diversified presence in the global market.

Asia-Pacific Tourism and Hospitality Market Insights

Asia-Pacific accounts for a notable share of the global tourism market. The region’s significance is amplified by its vast population, rapid urbanization, and growing middle class, particularly in China, India, and Southeast Asia. Domestic tourism in India reached a significant level in 2023, driven by festivals, religious circuits, and expanding rail connectivity. Japan’s tourism rebound has been remarkable, fueled by the weak yen and global interest in cultural experiences. Australia and New Zealand remain key destinations for long-haul leisure and adventure tourism, with the Great Barrier Reef and Fiordland National Park attracting millions. The rise of digital nomad visas in Thailand, Indonesia, and Malaysia is reshaping regional demand. With infrastructure investments in airports, hotels, and smart cities accelerating, the Asia-Pacific is poised for sustained growth, particularly as outbound mobility from emerging economies expands.

Latin America Tourism and Hospitality Market Insights

Latin America holds a descent share of the global market. The region’s appeal lies in its biodiversity, cultural richness, and affordable travel options. Mexico and Brazil are the leading destinations, with Cancun and Rio de Janeiro serving as major international gateways. Ecotourism is a key strength. Chile’s Patagonia region has become a global hub for adventure tourism, while Argentina’s wine routes and tango culture draw cultural travelers. However, infrastructure limitations and safety concerns in certain areas constrain growth. Despite this, digital platforms and low-cost carriers are improving access. The rise of experiential travel, such as Amazon river cruises and Andean treks, is driving premiumization. With increasing investment in sustainable tourism and regional air connectivity, Latin America is emerging as a high-potential destination for niche and experiential travelers.

Middle East and Africa Tourism and Hospitality Market Insights

Middle East and Africa collectively represent a key share of the global tourism market, with the Gulf Cooperation Council (GCC) countries driving much of the growth, according to Gulf Business Reports. The UAE, led by Dubai and Abu Dhabi, is the region’s tourism powerhouse. Saudi Arabia’s Vision 2030 includes a significant billion investment in tourism infrastructure, with projects like NEOM and the Red Sea Global developments targeting luxury and eco-tourism. Egypt has rebounded strongly. In Africa, South Africa remains the most visited nation. The region’s appeal is expanding beyond religious and heritage tourism to include wellness, adventure, and business events. With sovereign wealth funds backing mega-projects and digital nomad visas being introduced, the Middle East and Africa are transitioning from regional players to global tourism contenders.

KEY MARKET PLAYERS

Companies playing a prominent role in the global tourism and hospitality market include TUI Group, TCS World Travel, Expedia Group, American Express Global Business Travel, Gray & Co, Booking Holdings, Air BnB, Trip.com Group Ltd., TripAdvisor, Inc., Royal Holdings Co., Ltd., Marriott International, Hilton Worldwide Holdings Inc., Intercontinental Exchange Inc, and Others.

TOP LEADING PLAYERS IN THE MARKET

Marriott International stands as a defining force in the global hospitality landscape, renowned for its expansive portfolio spanning luxury, lifestyle, and extended-stay segments. Through brands like The Ritz-Carlton, St. Regis, and Courtyard by Marriott, the company has mastered the art of balancing operational consistency with localized authenticity. Its strength lies in a decentralized management model that empowers regional teams to adapt offerings to cultural nuances while maintaining global service standards. Marriott has pioneered digital transformation in guest experience, integrating mobile check-in, keyless entry, and AI-driven personalization across properties. The company’s loyalty program, Bonvoy, fosters deep customer engagement by offering curated experiences beyond mere stays, including culinary events and cultural immersions. By consistently investing in sustainable architecture and community integration, Marriott has positioned itself not just as a lodging provider but as a steward of responsible hospitality, influencing industry norms and shaping traveler expectations worldwide.

Booking Holdings Inc., the parent company of Booking.com, Agoda, and Priceline, has redefined how travelers access and book accommodations by creating a seamless, algorithm-driven digital marketplace. Its dominance stems from a frictionless user interface, vast inventory coverage, and dynamic pricing intelligence that connects millions of properties with global demand. Unlike traditional operators, Booking Holdings does not own physical assets, allowing unparalleled scalability and rapid market penetration across emerging economies. The company excels in localization, offering content in over 40 languages and tailoring search results to regional preferences, from payment methods to property types. Its data-centric approach enables predictive analytics that guide inventory recommendations and marketing strategies for partners. By empowering independent hotels, guesthouses, and alternative accommodations with visibility and booking infrastructure, Booking Holdings has democratized access to global tourism networks, making it an indispensable intermediary in the digital travel ecosystem.

Airbnb has revolutionized the tourism and hospitality sector by shifting the paradigm from institutional lodging to community-based, experiential stays. By enabling homeowners to monetize unused space, the platform has expanded accommodation supply in both urban and remote locations, often bypassing traditional zoning and regulatory frameworks. Airbnb’s success lies in its curation of unique, hyper-local experiences treehouses, houseboats, and heritage homes that appeal to travelers seeking authenticity over uniformity. The company has evolved beyond short-term rentals into a full-service travel platform, offering “Airbnb Experiences” led by locals, from cooking classes to guided foraging tours. This integration of lodging and activity has redefined trip planning, emphasizing immersion and connection. Airbnb’s decentralized model challenges conventional hospitality economics, fostering a peer-to-peer ecosystem that prioritizes personalization and cultural exchange, thereby reshaping consumer expectations and forcing legacy players to innovate.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

A pivotal strategy employed by leading players is the integration of end-to-end travel ecosystems that unify accommodation, transportation, activities, and dining within a single digital interface. Companies are moving beyond siloed services to offer seamless, itinerary-driven experiences that reduce planning friction and increase customer dependency. This holistic approach enhances user retention and enables cross-selling of high-margin services.

Another key tactic is the adoption of hyper-personalization through artificial intelligence and behavioral analytics. By leveraging vast datasets on user preferences, past bookings, and real-time context, companies tailor recommendations, pricing, and communication to individual travelers. This level of customization fosters emotional engagement and loyalty, transforming transactional interactions into curated journeys.

A third strategy involves strategic investment in sustainability and community-centric models. Leading firms are embedding regenerative practices, carbon offset programs, and local economic empowerment into their operations. By aligning with evolving consumer values around ethical travel, companies strengthen brand trust and secure long-term social license to operate in sensitive destinations.

COMPETITIVE LANDSCAPE

The competitive dynamics of the tourism and hospitality market are characterized by a constant tension between scale-driven consolidation and niche-driven differentiation. Global players leverage vast networks, technological infrastructure, and brand equity to dominate visibility and distribution, while boutique operators and regional platforms thrive by offering authenticity, cultural depth, and personalized service. The rise of digital intermediaries has shifted power toward platforms that control consumer access, compelling traditional hoteliers and tour operators to adapt or risk marginalization. Innovation is no longer confined to luxury amenities but extends to operational agility, sustainability credentials, and experiential design. Companies are increasingly competing on the quality of storytelling, the depth of local integration, and the ability to anticipate traveler emotions. The boundary between service provider and experience curator is blurring, with success hinging on creating memorable, shareable moments rather than merely functional stays. Trust, transparency, and ethical conduct have become decisive factors, especially as travelers scrutinize environmental impact and community equity. In this evolving landscape, competitiveness is determined not just by price or location, but by the ability to deliver meaning, connection, and resilience in an unpredictable world.

RECENT MARKET DEVELOPMENTS

- In February 2023, Marriott International launched the Travel Brilliantly initiative, integrating generative AI into its guest services platform to enable real-time, multilingual concierge support and personalized itinerary planning across its global property network.

- In July 2023, Booking Holdings acquired a strategic stake in Japan’s Rakuten Travel, enhancing its foothold in the Asia-Pacific market and enabling deeper integration with local payment systems and regional loyalty programs.

- In November 2023, Airbnb introduced the Experiences Marketplace, a curated global catalog of locally hosted activities, allowing hosts to monetize skills and cultural knowledge while enriching the traveler experience beyond accommodation.

- In January 2024, Accor partnered with the International Union for Conservation of Nature to implement biodiversity protection protocols across 100 of its eco-labeled properties in Africa and Southeast Asia, reinforcing its commitment to regenerative tourism.

- In March 2024, Hilton launched the Omni Journey platform, unifying its booking, stay, and post-travel engagement systems into a single AI-powered interface that anticipates guest preferences and automates service delivery across touchpoints.

MARKET SEGMENTATION

This research report on the global tourism and hospitality market has been segmented and sub-segmented based on type, services provided, travel model, and region.

By Type

- Domestic Tourism

- International Tourism

By Services Provided

- Accommodation

- Food & Beverages

- Recreation & Entertainment

- Transportation

- Travel

By Travel Model

- Business Travel

- Leisure Travel

- Other Activities

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa