Global Tracheostomy Tube Market Size, Share, Trends & Growth Forecast By Type (Silicone Rubber and PVC), Application (Emergency Treatment and Therapy) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

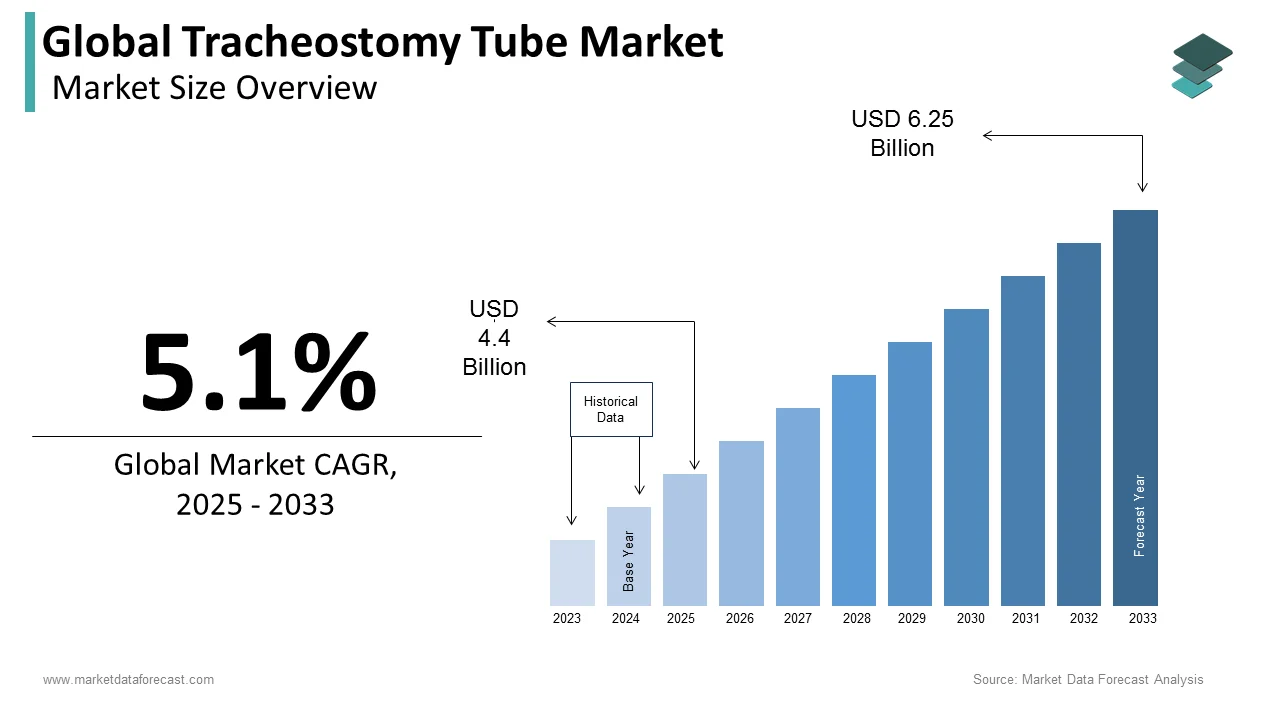

$4.4 BnMarket Estimate, 2026

$4.62 BnMarket Forecast, 2034

$6.88 BnCAGR, 2026–2034

5.1%Global Tracheostomy Tube Market Report Summary

The global tracheostomy tube market was valued at USD 4.4 billion in 2025 and is projected to grow from USD 4.62 billion in 2026 to USD 6.88 billion by 2034, registering a CAGR of 5.1% from 2026 to 2034. Market growth is driven by the increasing prevalence of respiratory disorders, rising demand for long-term airway management solutions, and growing numbers of critical care admissions worldwide. Tracheostomy tubes play a vital role in maintaining airway patency for patients requiring prolonged ventilation, respiratory support, or treatment of upper airway obstructions. Advancements in tracheostomy tube materials, increasing adoption of home healthcare services, and expanding critical care infrastructure are further supporting market growth.

Key Market Trends

- Rising prevalence of chronic respiratory diseases and critical care admissions.

- Increasing demand for long-term airway management and ventilatory support solutions.

- Growing adoption of home healthcare and post-acute respiratory care services.

- Advancements in biocompatible and patient-friendly tracheostomy tube designs.

- Expansion of healthcare infrastructure and intensive care unit capacities globally.

Segmental Insights

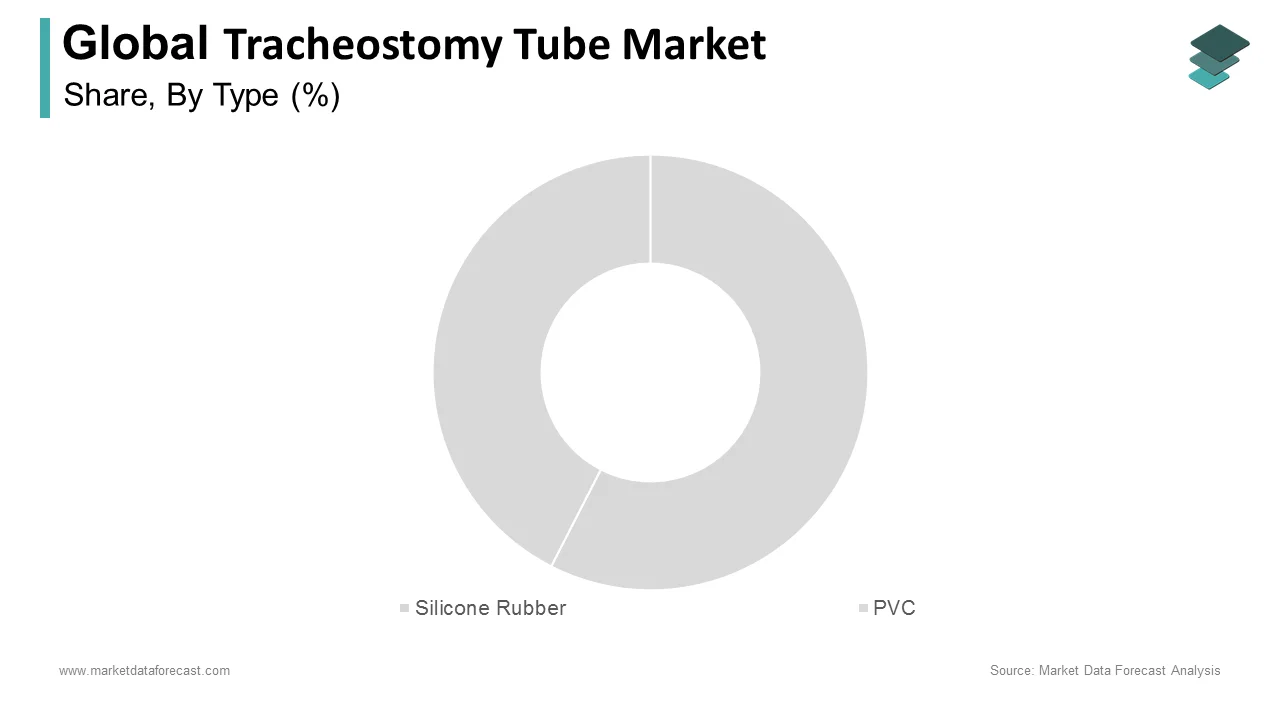

- Based on type, the polyvinyl chloride (PVC) tubes segment dominated the global tracheostomy tube market by accounting for 48.6% share in 2025, driven by their flexibility, affordability, durability, and widespread use in airway management procedures.

- Based on application, the therapy applications segment held the largest share of the market with 45.7% in 2025, supported by the extensive requirement for long-term airway support and respiratory management among patients requiring prolonged ventilation and critical care treatment.

Regional Insights

The global tracheostomy tube market is witnessing steady growth across major regions, supported by increasing respiratory disease prevalence, advancements in critical care services, and growing healthcare investments.

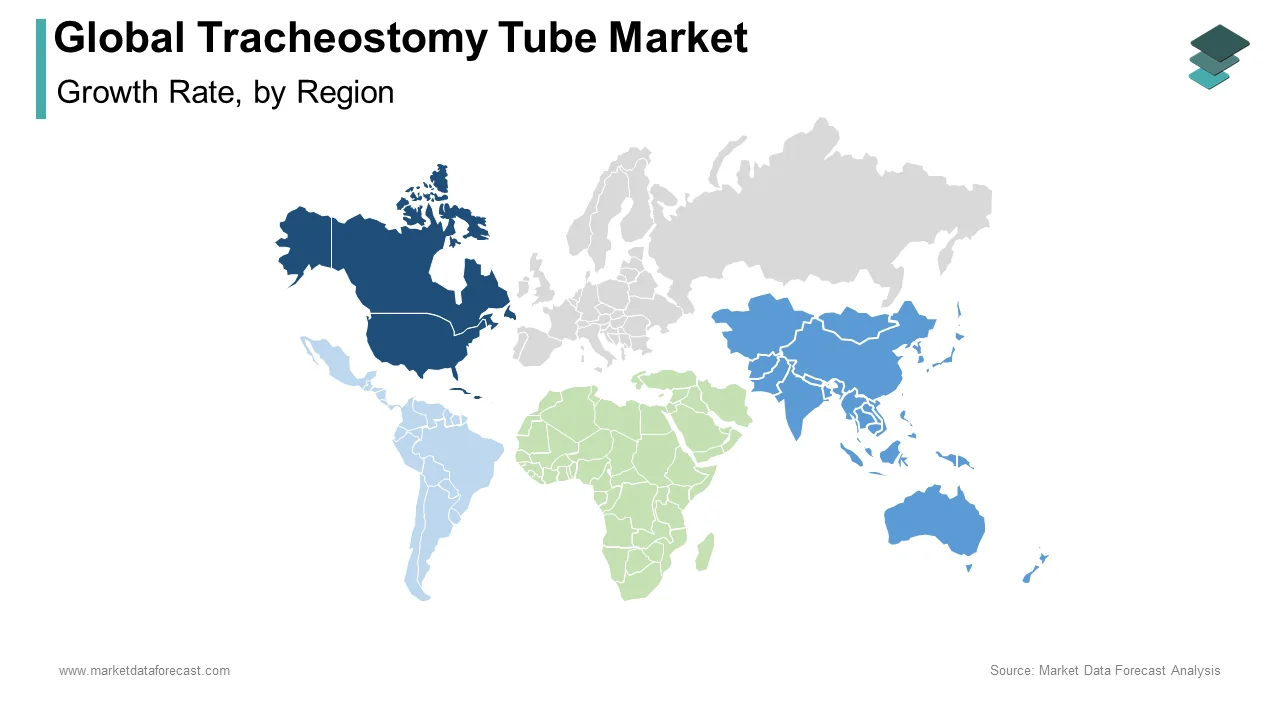

- North America dominated the global market in 2025 with 35.1% share, driven by advanced healthcare infrastructure, high critical care procedure volumes, and widespread adoption of innovative airway management technologies.

- Europe maintained a strong position in the global market by accounting for 28.3% share in 2025, supported by robust healthcare systems, increasing elderly populations, and growing demand for respiratory care solutions.

- Asia-Pacific is projected to register the fastest growth during the forecast period, driven by rapid healthcare infrastructure development, increasing prevalence of respiratory disorders, and expanding access to critical care services across emerging economies.

Competitive Landscape

The global tracheostomy tube market is characterized by the presence of established medical device manufacturers focusing on product innovation, patient safety, and advanced airway management solutions. Market participants are investing in the development of improved tracheostomy tube designs, enhanced biocompatible materials, and specialized products for critical care and home healthcare settings. Strategic collaborations, product launches, and geographic expansion initiatives are shaping competitive dynamics across the market.

Prominent companies operating in the global tracheostomy tube market include Medtronic, Teleflex Medical, Smiths Medical, TRACOE Medical, ConvaTec, Fuji Systems, Sewoon Medical, Boston Medical, Well Lead, TuoRen, and Pulmodyne.

Global Tracheostomy Tube Market Size

The global tracheostomy tube market was worth US$ 4.4 billion in 2025 and is anticipated to reach a valuation of US$ 6.88 billion by 2034 from US$ 4.62 billion in 2026, and it is predicted to register a CAGR of 5.1% during the forecast period 2026 to 2034.

A tracheostomy tube (often called a "trach tube") is a small, curved medical device placed directly into the windpipe (trachea) through a surgical opening in the front of the neck. These tubes are critical in intensive care units, home healthcare settings, and long-term care facilities serving individuals with chronic respiratory conditions, neurological disorders, or traumatic injuries. The market is characterized by a shift toward patient-centric designs that prioritize comfort, safety, and ease of use for both clinicians and caregivers. In Europe, the aging population significantly influences demand as per Eurostat data, which indicates that 21 percent of the European Union population was aged 65 or older in 2023, creating a substantial base for chronic respiratory care. The World Health Organization and global health studies indicate that Chronic Obstructive Pulmonary Disease (COPD) affects over 390 million people globally, underscoring the expanding need for airway management solutions. Furthermore, the rise in hospital-acquired infections has prompted stricter hygiene protocols, with the Centers for Disease Control and Prevention reporting that ventilator-associated events occur in 5 to 10 percent of mechanically ventilated patients. This statistic drives the adoption of advanced tracheostomy tubes with integrated suction ports and antimicrobial coatings. The integration of telemedicine and remote monitoring technologies also transforms post-discharge care, enabling better management of tracheostomy patients at home. These clinical and demographic factors collectively define the current landscape, emphasizing the vital role of tracheostomy tubes in sustaining life and improving quality of life for vulnerable patient populations across diverse healthcare environments.

MARKET DRIVERS

Rising Prevalence of Chronic Respiratory Diseases and Neurological Disorders Drives Demand

The escalating prevalence of chronic respiratory diseases and neurological disorders drives the growth of the tracheostomy tube market. This creates a sustained need for long-term airway management solutions. Conditions such as chronic obstructive pulmonary disease, asthma, and neuromuscular diseases like amyotrophic lateral sclerosis often lead to respiratory failure, necessitating tracheostomy for effective ventilation and secretion clearance. According to the Global Burden of Disease Study 2023, chronic respiratory diseases accounted for approximately 4.2 million deaths globally, highlighting the severity and widespread nature of these conditions. The aging population is particularly susceptible, with the United Nations Department of Economic and Social Affairs projecting that the number of people aged 60 years and older will reach 2.1 billion by 2050. This demographic shift increases the incidence of stroke and neurodegenerative diseases, which frequently result in bulbar dysfunction and the inability to protect the airway. Data from the American Stroke Association indicates that approximately 800000 people suffer a stroke each year in the United States alone, with many requiring temporary or permanent tracheostomy during recovery. Additionally, the rising incidence of spinal cord injuries due to accidents and trauma contributes to the demand, with the National Spinal Cord Injury Statistical Center reporting 17900 new cases annually in the US. These clinical realities ensure a steady influx of patients requiring tracheostomy tubes, thereby driving consistent demand for both disposable and reusable devices across acute and home care settings.

Advancements in Critical Care Infrastructure and Home Healthcare Services Expand Access

Improvements in critical care infrastructure and the expansion of home healthcare services significantly propel the tracheostomy tube market. This enhances patient access to specialized airway management and post-acute care. Hospitals worldwide are upgrading their intensive care units with advanced ventilation systems and monitoring technologies, which support longer survival rates for critically ill patients who subsequently require tracheostomy. According to the Society of Critical Care Medicine (SCCM) and other bodies, ICU capacity has expanded significantly (often cited as a steady pre-pandemic increase followed by a massive surge during COVID-19), facilitating better management of complex respiratory cases. Simultaneously, the shift toward home-based care reduces hospital stays and lowers healthcare costs while improving patient comfort. The National Association for Home Care and Hospice reports that home health services in the United States serve over 12 million patients annually, many of whom require skilled nursing for tracheostomy care. This transition is supported by government reimbursement policies that favor outpatient care and by technological innovations such as portable suction devices and humidification systems that make home management feasible. Training availability is improving, with the European Respiratory Society (ERS) providing certified training programmes and clinical guidelines to standardize airway management, though adoption rates among private home care agencies vary by region. These developments create a robust ecosystem that supports the continued use of tracheostomy tubes outside hospital walls, thereby expanding the market beyond acute care settings into the growing home healthcare sector.

MARKET RESTRAINTS

High Risk of Complications and Infections Deters Procedure Adoption

The high risk of complications and infections associated with tracheostomy procedures hampers the growth of the tracheostomy tube market. This causes hesitation among clinicians and patients regarding the necessity and timing of the intervention. Tracheostomy is an invasive procedure that carries risks such as bleeding, infection, stomal stenosis, and accidental decannulation, which can lead to severe morbidity or mortality. Reviews in journals such as the Journal of Intensive Care Medicine and Respiratory Care indicate that early complications (such as bleeding) occur in 5% to 10% of tracheostomies, while late complications (including tracheal stenosis) affect approximately 2% to 5% of patients, depending on the technique used. Ventilator-associated pneumonia remains a major concern, with the Centers for Disease Control and Prevention estimating that it extends hospital stays by an average of 7 to 9 days and increases treatment costs substantially. These adverse outcomes prompt healthcare providers to delay tracheostomy in favor of less invasive alternatives such as non-invasive ventilation when possible. Additionally, the psychological impact on patients, including anxiety and communication difficulties, further complicates recovery and acceptance of the device. Studies published in journals like Critical Care have found that up to 50% of patients report significant distress, primarily due to communication difficulties related to their tracheostomy tube, which significantly affects their quality of life. The need for rigorous sterile technique and specialized nursing care also limits the procedure's feasibility in resource-limited settings. These clinical risks will continue to constrain the broader adoption of tracheostomy tubes despite their life-saving potential. That limitation will hold true until safer techniques and better infection control measures are universally adopted.

Stringent Regulatory Requirements and Reimbursement Challenges Limit Market Growth

Stringent regulatory requirements and complex reimbursement landscapes are major restraints for the tracheostomy tube market. This imposes high compliance costs and limits financial accessibility for patients. Medical devices such as tracheostomy tubes are subject to rigorous approval processes by agencies like the Food and Drug Administration in the United States and the European Medicines Agency in Europe. Studies indicate that the implementation of the Medical Device Regulation (MDR) has doubled compliance costs and significantly extended certification timelines, leading manufacturers to withdraw approximately 20% of their legacy device portfolios from the market. Small and medium-sized manufacturers often struggle to meet these demanding standards, which require extensive clinical data and quality management systems. Furthermore, reimbursement policies vary significantly across regions and payers, creating uncertainty for healthcare providers and patients. In the United States, the Centers for Medicare and Medicaid Services periodically adjust reimbursement rates for durable medical equipment, which can impact the affordability of specialized tracheostomy supplies. A report by the Healthcare Financial Management Association indicated that 25 percent of claims for home respiratory equipment face initial denial due to documentation errors or policy restrictions. These administrative burdens discourage the adoption of premium products and limit patient access to advanced features such as speaking valves or customized fittings. Consequently, regulatory and financial barriers slow down market expansion and restrict the availability of innovative solutions to those who need them most.

MARKET OPPORTUNITIES

Integration of Smart Technologies and Remote Monitoring Creates New Value Propositions

The integration of smart technologies and remote monitoring capabilities offers substantial opportunities for the tracheostomy tube market. This enhances patient safety and enables proactive care management. Innovations such as sensors embedded in tracheostomy tubes can monitor airway pressure, humidity, and secretions in real time, transmitting data to healthcare providers via wireless networks. According to leading digital health analyses, the global landscape for IoT in healthcare and connected medical devices is projected to grow aggressively at a 23.4% CAGR, heavily driven by remote patient monitoring demands. This technology allows for early detection of blockages or dislodgement, reducing emergency interventions and hospital readmissions. Telehealth platforms further support this ecosystem by enabling virtual consultations where clinicians can assess stoma health and guide caregivers through maintenance procedures. American Telemedicine Association (ATA) data confirms that telehealth utilization stabilized at 38 times higher than pre-pandemic baselines, with chronic care management representing the single largest share at 30% of all virtual visits. Additionally, smart alarms and mobile applications provide caregivers with instant alerts and educational resources, improving confidence and competence in home care settings. Manufacturers partnering with technology firms can develop comprehensive solutions that combine hardware with software services, creating recurring revenue streams. These advancements not only improve clinical outcomes but also differentiate products in a competitive market, positioning smart tracheostomy systems as the next standard of care for respiratory support.

Expansion into Emerging Markets with Improving Healthcare Infrastructure Offers Untapped Potential

The expansion into emerging markets with improving healthcare infrastructure provides a clear path for manufacturers seeking to diversify their geographic footprint and capture growing patient populations, which is likely to boost the expansion of the tracheostomy tube market. Countries in the Asia Pacific, Latin America, and the Middle East are investing heavily in hospital construction and critical care capabilities, driven by urbanization and rising healthcare expenditures. World Bank health financing assessments warn that following a brief pandemic surge, public health spending per capita in low- and lower-middle-income countries has experienced a sustained decline, straining universal access goals. As ICU capacity expands in nations such as India, China, and Brazil, the demand for essential airway management devices, including tracheostomy tubes, rises correspondingly. Local manufacturing initiatives and government tenders often favor cost-effective solutions, creating opportunities for companies that can offer high-quality products at competitive prices. Additionally, increasing awareness of respiratory health and improved insurance coverage in these regions enhances patient access to specialized care. Partnerships with local distributors and training programs for healthcare professionals can facilitate market entry and build brand loyalty. Manufacturers can tap into a vast, untapped customer base by addressing the specific needs of these growing economies. Doing so allows them to achieve sustainable, long-term growth beyond saturated, mature markets.

MARKET CHALLENGES

Shortage of Skilled Healthcare Professionals Impacts Quality of Care and Device Utilization

The acute shortage of skilled healthcare professionals is a significant challenge for the tracheostomy tube market. This impacts the quality of care and proper utilization of devices. Tracheostomy care requires specialized knowledge and technical skills to prevent complications such as infection, obstruction, and accidental decannulation. According to the World Health Organization, there is a projected shortfall of 10 million health workers globally by 2030, with nursing shortages being particularly acute in critical care and home health settings. This labor gap leads to inadequate training for caregivers and family members who often assume responsibility for tracheostomy maintenance at home. Work published through the American Association of Critical-Care Nurses (AACN) emphasizes a growing practice-experience gap, where the surging volume of novice nurses faces systemic challenges in rapidly mastering complex ICU procedures. Lack of expertise results in higher rates of adverse events and increased burden on emergency services when complications arise. Furthermore, the turnover rate among respiratory therapists and critical care nurses exacerbates the problem, requiring continuous investment in training programs that strain hospital budgets. Without a competent workforce, the benefits of advanced tracheostomy technologies cannot be fully realized, leading to suboptimal patient outcomes. Addressing this challenge requires collaborative efforts between educational institutions, healthcare facilities, and manufacturers to develop standardized training curricula and simulation tools that enhance workforce readiness and ensure safe, effective device usage.

Supply Chain Vulnerabilities and Raw Material Costs Disrupt Production and Availability

Persistent supply chain vulnerabilities and fluctuating raw material costs are constraining the expansion of the tracheostomy tube market. This disrupts production schedules and affects product availability. The manufacturing of medical-grade plastics, silicones, and metals relies on global supply networks that are susceptible to geopolitical tensions, natural disasters, and logistical bottlenecks. Dependence on single-source suppliers for critical components such as medical-grade silicone exacerbates risk with any disruption, causing immediate production halts. The price volatility of petroleum-based raw materials used in plastic production further complicates cost management, with crude oil prices varying by 25 percent within short periods, as reported by the International Energy Agency. These fluctuations force manufacturers to either absorb losses or pass increased costs to healthcare providers, potentially limiting access to affordable devices. Additionally, stringent quality control requirements mean that alternative sourcing options require lengthy validation processes, delaying responsiveness to supply shocks. A survey by the Medical Device Manufacturers Association revealed that 60 percent of companies experienced material shortages in the past year, affecting their ability to meet demand. These operational challenges will continue to threaten market stability and hinder the consistent delivery of essential airway management solutions. This will persist until more resilient and localized supply chains are established.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Medtronic, Teleflex Medical, Smiths Medical, TRACOE Medical, ConvaTec, Fuji Systems, Sewoon Medical, Boston Medical, Well Lead, TuoRen, Pulmodyne, and others. |

SEGMENTAL ANALYSIS

By Type Insights

The polyvinyl chloride tubes segment was the largest in the tracheostomy tube market and occupied a 48.6% share in 2025. This prominence of the segment was supported by its cost-effectiveness, widespread availability, and suitability for short-term use in acute care settings. These tubes are primarily designed for single-use or temporary airway management, making them ideal for emergency departments, intensive care units, and operating rooms where infection control is paramount. Sources indicate that disposable single-use items account for over 75% of respiratory care consumables used in hospital settings, driven by a strict preference for sterile, single-patient workflows. The low manufacturing cost of PVC allows healthcare facilities to manage budgets effectively while maintaining high standards of hygiene. Clinical consensus and hospital procurement data show that thermoplastic PVC tubes are the standard choice for initial acute tracheostomies due to their temporary rigidity, which facilitates easier insertion during critical airway procedures. Additionally, the transparency of PVC material enables clinicians to visually monitor secretions and ensure proper placement without additional imaging. The prevalence of healthcare-associated infections drives single-use demand, with guidelines from the Centers for Disease Control and Prevention (CDC) emphasizing that using disposable devices eliminates patient-to-patient cross-contamination risks associated with inadequate reprocessing. Furthermore, the ease of disposal and compliance with biomedical waste regulations make PVC tubes a practical choice for large healthcare systems. These factors combined ensure that PVC remains the dominant material type, particularly in high-volume clinical environments where efficiency and safety are prioritized over long-term durability.

The silicone rubber tubes segment is predicted to witness the highest CAGR of 7.2% from 2026 to 2034 due to the increasing need for long-term airway management and superior patient comfort. Unlike rigid PVC, silicone is soft, flexible, and highly biocompatible, reducing the risk of tissue irritation, granulation formation, and pressure necrosis around the stoma site. According to the European Respiratory Society, patients requiring tracheostomy for more than four weeks benefit significantly from silicone tubes, which minimize trauma and enhance quality of life. The aging population and rising prevalence of chronic neurological conditions have increased the number of patients transitioning to home care, where comfort and ease of maintenance are critical. Studies in peer-reviewed journals, such as the Journal of Clinical Nursing, show that long-term home care patients report high satisfaction levels with silicone tubes because their flexible design reduces baseline discomfort during neck movement. Additionally, silicone tubes are often reusable after proper sterilization, offering economic benefits for long-term users despite higher initial costs. The development of advanced silicone formulations with antimicrobial properties accelerates adoption, with medical-grade silicone market analyses showing a strong shift toward coated devices to suppress bacterial biofilm formation. Manufacturers are also introducing customizable silicone options that fit diverse anatomical structures, addressing individual patient needs. These clinical advantages and patient-centric innovations position silicone rubber as the primary growth engine in the evolving tracheostomy tube landscape.

By Application Insights

In 2025, the therapy applications segment held the majority share of 45.7% of the tracheostomy tube market because of the extensive requirement for long-term airway support in patients with chronic respiratory failures, neurological impairments, and prolonged mechanical ventilation needs. This segment encompasses both hospital-based rehabilitation and home healthcare settings where patients require stable and secure airways for extended periods. Epidemiological data indicate that between 60,000 and 80,000 tracheostomies are performed annually in the United States, with the vast majority executed as scheduled, therapeutic interventions for prolonged mechanical ventilation rather than emergency airway rescues. The dominance of this segment is driven by the high survival rates of critically ill patients who survive initial acute phases but require ongoing respiratory support. Clinical tracking indicates that across a broad intensive care spectrum, approximately 7% to 15% of mechanically ventilated patients undergo a tracheostomy to facilitate weaning from the ventilator, though rates vary significantly by specific patient condition. Furthermore, the rise in home healthcare services supports this trend. These patients require durable and comfortable tubes that allow for speaking, swallowing, and pulmonary hygiene, thereby enhancing their overall quality of life. The integration of multidisciplinary care teams, including respiratory therapists, speech language pathologists, and nurses, ensures effective management of therapeutic tracheostomies. This comprehensive approach sustains steady demand for specialized tubes designed for long-term use, solidifying the therapy segment as the largest contributor to market revenue.

The emergency treatment applications segment is estimated to register the fastest CAGR of 6.5% during the forecast period, owing to increasing incidences of trauma road accidents and advancements in pre-hospital critical care. Emergency tracheostomies are life-saving procedures performed when upper airway obstruction prevents conventional intubation, necessitating immediate surgical or percutaneous access. According to the World Health Organization, road traffic injuries result in approximately 1.19 million deaths globally each year, with severe trauma survivors frequently requiring immediate emergency airway management. The growing prevalence of maxillofacial injuries and severe burns further amplifies the need for rapid deployment tracheostomy kits in emergency departments and ambulance services. Clinical standards from the American College of Surgeons Committee on Trauma emphasize that immediate, definitive airway stabilization is the critical priority for severe trauma management to halt preventable death from asphyxia. Additionally, the expansion of emergency medical services in developing regions enhances access to critical care procedures. Training programs for paramedics and emergency physicians have expanded. The National EMS Scope of Practice Model, maintained by NHTSA, designates emergency advanced airway management as a core competency required for all licensed paramedic-level providers nationwide, subject to state and local medical direction. Innovations such as portable suction integrated tubes and quick insert designs facilitate faster and safer procedures in chaotic environments. These factors collectively propel the emergency treatment segment to the forefront of growth as healthcare systems prioritize rapid response capabilities and trauma care infrastructure.

REGIONAL ANALYSIS

North America Tracheostomy Tube Market Analysis

North America was the top performer in the global tracheostomy tube market and accounted for a 35.1% share in 2025. This dominance of the regional market was driven by advanced healthcare infrastructure, high procedure volumes, and robust reimbursement policies. The United States serves as the primary contributor within this region with a well-established network of intensive care units and specialized respiratory care centers. According to the Agency for Healthcare Research and Quality, tracheostomy volume has fluctuated, with recent pre-pandemic estimates showing approximately 60,000 to 80,000 procedures annually in the US, though numbers surged temporarily during the COVID-19 pandemic. The presence of major medical device manufacturers and continuous innovation in airway management technologies further strengthen the market position. Reimbursement frameworks provided by Medicare and private insurers support the adoption of premium products, including silicone and speaking valve-equipped tubes. Data reflects that CMS has expanded coverage criteria for home respiratory equipment (such as non-invasive ventilation for COPD), contributing to a steady increase in beneficiary utilization and market growth in recent years. Additionally, the high prevalence of chronic diseases such as COPD and stroke drives consistent demand for therapeutic tracheostomy solutions. The region benefits from stringent regulatory standards that ensure product safety and quality, fostering trust among healthcare providers. Furthermore, the integration of telehealth and remote monitoring technologies enhances post-discharge management, improving patient outcomes and reducing readmission rates. These structural and economic factors consolidate North America’s leadership in the global tracheostomy tube market.

Europe Tracheostomy Tube Market Analysis

Europe maintained a strong position in the global tracheostomy tube market and captured a share of 28.3% in 2025. This growth of the European market was propelled by a rapidly aging population and stringent quality standards for medical devices. Countries such as Germany, France, and the United Kingdom have well-developed healthcare systems that prioritize patient safety and clinical outcomes. According to Eurostat, the proportion of people aged 65 and older in the EU reached 21 percent in 2023, creating a substantial demographic base for chronic respiratory care. The implementation of the European Medical Device Regulation has raised the bar for product certification, ensuring that only high-quality and safe tracheostomy tubes reach the market. This regulatory environment encourages innovation while protecting patients from substandard products. Additionally, strong public healthcare funding supports access to essential respiratory supplies for patients across socioeconomic groups. The region also sees significant investment in research and development, with academic institutions collaborating with industry leaders to develop next-generation airway solutions. Cultural emphasis on palliative care and quality of life further influences product preferences, favoring features that enable communication and mobility. These demographic, regulatory, and cultural factors ensure that Europe remains a key market for advanced and reliable tracheostomy care solutions.

Asia Pacific Tracheostomy Tube Market Analysis

Asia Pacific is the fastest-growing region in the global tracheostomy tube market due to rapid healthcare infrastructure expansion and a rising burden of respiratory diseases. Countries such as China, India, Japan, and South Korea are investing heavily in hospital construction and critical care capabilities to address growing health needs. World Bank data indicates that health expenditure in East Asia and the Pacific has risen steadily, with specific high-growth markets like Vietnam seeing per capita spending increase by approximately 8% annually, though regional public spending as a share of GDP varies widely. The high prevalence of smoking and air pollution contributes to elevated rates of chronic obstructive pulmonary disease and lung cancer, driving the need for airway management interventions. Data from the Global Burden of Disease Study indicates that Asia accounts for approximately 45% of global COPD cases (with over 95 million cases in East and South Asia alone), creating a vast patient pool for respiratory and tracheostomy services. Additionally, improving insurance coverage and medical tourism initiatives enhance access to specialized care in the region. Local manufacturing capabilities are expanding with companies producing cost-effective alternatives to imported brands. Infrastructure initiatives in India aim to add approximately 200,000 new hospital beds in the coming years to meet government targets, a figure often cited in market reports, while the Asian Development Bank funds broader health infrastructure upgrades across the region. Government initiatives to train healthcare professionals in critical care also support market growth. These dynamic economic and demographic trends position the Asia Pacific as the most influential region for future expansion in the tracheostomy tube industry.

Latin America Tracheostomy Tube Market Analysis

Latin America shows moderate growth in the tracheostomy tube market owing to economic volatility, yet sustained improvements in healthcare access and critical care capacity. Brazil, Mexico, and Argentina are the primary markets in the region, leveraging public health initiatives to expand ICU availability and respiratory care services. According to the Pan American Health Organization (PAHO), the capacity of intensive care beds in many Latin American countries doubled (increasing by nearly 100%) during the peak of the COVID-19 pandemic to address emergency demand, though significant urban-rural disparities remain. The rising incidence of trauma due to road accidents and violence drives demand for emergency airway management solutions. Data from the Inter-American Development Bank suggests that public investment is prioritizing broad emergency response systems and critical care infrastructure, which indirectly supports the availability of essential airway management supplies in hospitals. However, currency fluctuations and budget constraints limit the adoption of premium products, favoring cost-effective PVC tubes. Private healthcare sectors in major cities offer advanced care options, attracting patients who can afford higher-quality silicone tubes and accessories. The lack of standardized reimbursement policies across countries creates fragmentation, affecting market consistency. Despite these challenges, the growing middle class and increasing awareness of respiratory health contribute to steady demand. Partnerships with international manufacturers and local distributors help navigate logistical hurdles, ensuring product availability. These factors indicate a market with potential for gradual expansion as economic stability and healthcare infrastructure continue to improve.

Middle East and Africa Tracheostomy Tube Market Analysis

The Middle East and Africa present is likely to expand notably in the tracheostomy tube market during the forecast period due to medical tourism in Gulf States and gradual infrastructure development in emerging African economies. Countries such as Saudi Arabia, the United Arab Emirates, and South Africa are key contributors with investments in world-class hospitals and specialized respiratory care centers. Recent industry reports (e.g., Alpen Capital) estimate that GCC healthcare spending already exceeds $100 billion and is projected to reach approximately $135.5 billion by 2027, driven by an aging population and demand for advanced medical devices. Medical tourism attracts patients from neighboring regions seeking high-quality critical care, including complex airway management procedures. In Africa, the situation varies significantly, with South Africa having a relatively developed private healthcare sector, while other nations face resource constraints. The World Health Organization reports that access to essential surgical services, including tracheostomy, remains limited in many low-income African countries due to workforce shortages. However, initiatives by non-governmental organizations and international aid agencies are improving supply chains for basic medical supplies. The prevalence of infectious diseases such as tuberculosis also contributes to the need for airway interventions. As governments prioritize health system strengthening and local manufacturing capabilities emerge, the market is poised for incremental growth. These diverse dynamics make the region a frontier for strategic partnerships and targeted interventions to improve access to life-saving airway devices.

COMPETITIVE LANDSCAPE

The competition in the tracheostomy tube market is characterized by a mix of established multinational corporations and specialized niche manufacturers who compete on product quality, innovation, and clinical support. Major players leverage their extensive distribution networks and brand recognition to maintain dominance in hospital and home care settings. However, smaller companies often differentiate themselves through specialized designs such as pediatric tubes or custom-fitted options for complex anatomies. Price competition is moderate due to the critical nature of the device, but cost effectiveness remains a key factor for healthcare procurement departments. Regulatory barriers create high entry thresholds protecting incumbent firms from new competitors, yet encouraging continuous innovation to meet evolving standards. Intellectual property rights play a significant role with patents on specific cuff designs or materials, providing temporary monopolies. Collaborations with healthcare providers for clinical trials enhance credibility and drive adoption. The shift toward value-based care prompts companies to demonstrate superior patient outcomes and reduced complication rates. Ultimately, success depends on balancing technological advancement with reliable supply chain management and comprehensive customer support services.

KEY MARKET PARTICIPANTS

Some of the leading companies in the global tracheostomy tube market profiled in the report are

- Medtronic

- Teleflex Medical

- Smiths Medical

- TRACOE Medical

- ConvaTec

- Fuji Systems

- Sewoon Medical

- Boston Medical

- Well Lead

- TuoRen

- Pulmodyne

TOP PLAYERS IN THE MARKET

- Smiths Medical Inc is a prominent global player in the tracheostomy tube market, known for its innovative Portex brand, which offers a comprehensive range of cuffed and uncuffed tubes. The company focuses on enhancing patient safety through advanced design features such as high-volume, low-pressure cuffs that minimize tracheal damage. Smiths Medical has recently invested in digital health solutions to integrate remote monitoring capabilities with its respiratory products. Their commitment to clinical education ensures that healthcare professionals are well-trained in proper insertion and maintenance techniques. By expanding its manufacturing footprint and strengthening distribution networks in emerging markets, the company enhances accessibility to critical airway management devices. These strategic initiatives reinforce their reputation for quality and reliability while addressing the evolving needs of intensive care and home healthcare sectors globally.

- Teleflex Incorporated contributes significantly to the tracheostomy tube market through its diverse portfolio of airway management solutions, including the Shiley and Bivona brands. The company emphasizes product innovation by developing silicone tubes with adjustable flanges and speaking valves that improve patient communication and comfort. Teleflex has recently focused on sustainability initiatives by optimizing packaging materials and reducing waste in production processes. Strategic acquisitions of specialized medical device companies have allowed them to broaden their product offerings and enter new therapeutic areas. The corporation leverages robust regulatory expertise to navigate complex global compliance requirements, ensuring timely market entry for innovations. Teleflex strengthens its position as a trusted partner for hospitals and home care providers seeking reliable airway management solutions. This is achieved by actively prioritizing customer feedback and clinical outcomes.

- Medtronic plc plays a vital role in the tracheostomy tube market by leveraging its extensive global reach and strong research and development capabilities. The company offers a variety of disposable and reusable tubes designed to meet diverse clinical needs from emergency care to long-term therapy. Medtronic has recently integrated smart technologies into its respiratory care portfolio, enabling data-driven insights for better patient management. Collaborations with healthcare institutions facilitate clinical trials that validate the efficacy and safety of their products. The company also invests heavily in training programs for clinicians to ensure proper usage and reduce complication rates. By focusing on value-based healthcare models, Medtronic aims to improve patient outcomes while controlling costs. Their commitment to innovation and operational excellence ensures they remain a key contributor to the advancement of airway management technologies worldwide.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the tracheostomy tube market primarily focus on product innovation and strategic partnerships to maintain a competitive advantage. Companies invest heavily in research and development to create biocompatible materials such as silicone that reduce tissue irritation and enhance patient comfort. Expansion into emerging markets through local manufacturing and distribution agreements allows firms to tap into growing healthcare infrastructure. Digital integration is another critical strategy, with businesses developing smart devices that monitor airway parameters and transmit data to healthcare providers. Regulatory compliance and quality assurance remain paramount as firms navigate stringent approval processes in major markets. Educational initiatives targeting clinicians help build brand loyalty and ensure proper device usage. These combined strategies foster resilience, adaptability, and long-term growth in a specialized and highly regulated medical device environment.

MARKET SEGMENTATION

This research report on the global tracheostomy tube market has been segmented and sub-segmented based on the type, application, and region.

By Type

- Silicone Rubber

- PVC

By Application

- Emergency Treatment

- Therapy

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the global tracheostomy tube market?

The global tracheostomy tube market covers products for managing airway access in respiratory disorders, with growth driven by rising chronic respiratory diseases and surgical procedures

2. What are the major types in the global tracheostomy tube market?

Key types include cuffed, uncuffed, pediatric, and percutaneous tracheostomy tubes, each tailored for specific clinical airway management needs in the global tracheostomy tube market

3. What drives growth in the global tracheostomy tube market?

Growth is driven by increasing chronic respiratory disease prevalence, aging populations, and technological advances in tube design improving safety and comfort

4. What regions lead the global tracheostomy tube market?

North America and Asia-Pacific are major contributors, with Asia-Pacific growing fastest due to rising respiratory disease cases and expanding healthcare infrastructure

5. How important is technology in the global tracheostomy tube market?

Technology enhances tube features such as leak prevention, sensor integration, and improved materials, boosting product demand in the global tracheostomy tube market

6. What are common applications of products in the global tracheostomy tube market?

Applications include ICU care, long-term ventilation, emergency airway management, and treatment of chronic respiratory conditions

7. What challenges affect the global tracheostomy tube market?

Challenges include reimbursement issues, high device costs, risk of complications, and regulatory hurdles limiting access in some regions

8. How does the global tracheostomy tube market address safety?

Enhanced cuff designs reduce leakage and tissue damage, while innovations improve patient comfort and airway security in the global tracheostomy tube market

9. What role do hospitals play in the global tracheostomy tube market?

Hospitals are primary end-users, using tubes for surgeries, ICU management, and emergency care, driving demand in the global tracheostomy tube market

10. How is the global tracheostomy tube market affected by respiratory disease trends?

Rising COPD, lung cancer, and other respiratory disease cases increase demand for tracheostomy tubes worldwide, fueling market growth

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com