- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Global Transcatheter Heart Valve Market Report Summary

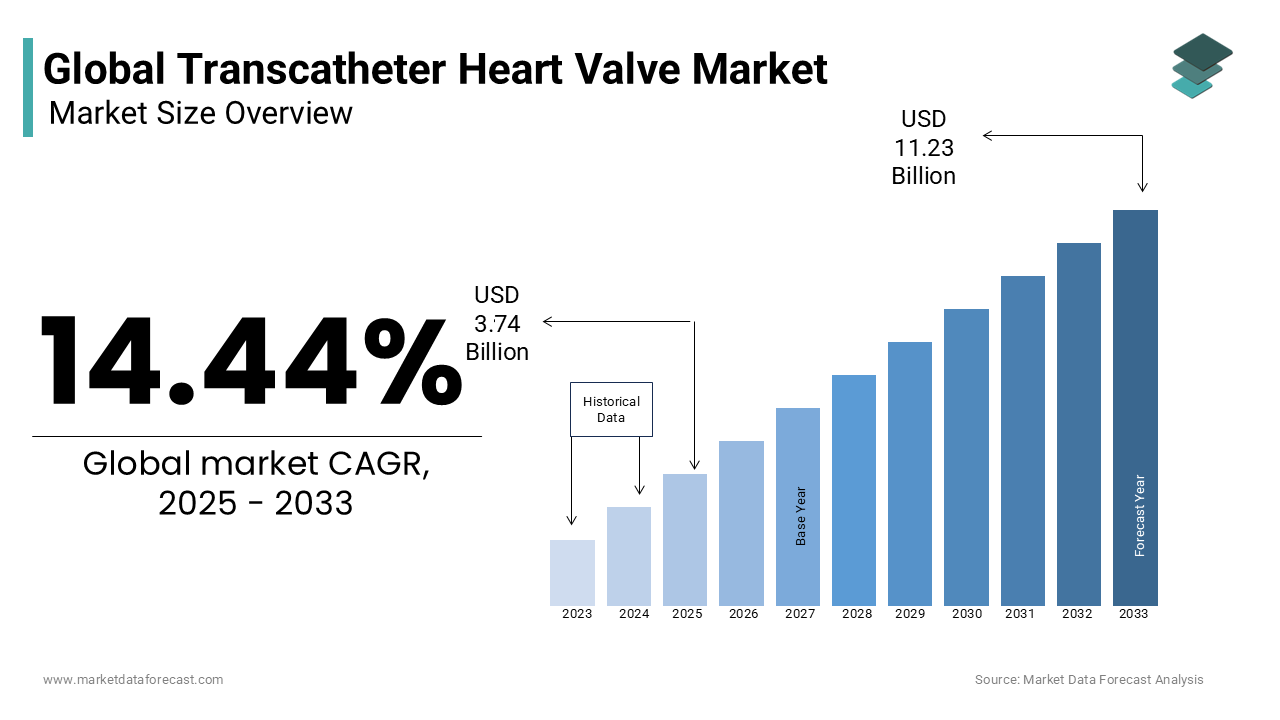

The global transcatheter heart valve market was valued at USD 3.27 billion in 2024, is estimated to reach USD 3.74 billion in 2025, and is projected to reach USD 11.23 billion by 2033, registering a CAGR of 14.44% from 2025 to 2033. The growth of the global transcatheter heart valve market is driven by an expanding elderly population with degenerative valvular disease, growing clinical evidence supporting transcatheter therapies across surgical risk profiles, and rising adoption of minimally invasive structural heart interventions. Technological advances in valve design, delivery systems, and imaging together with increasing use of AI-enabled pre-procedural planning are further fueling market growth. Moreover, expansion into mitral and tricuspid valve indications, coupled with improving reimbursement frameworks in key markets, is broadening the eligible patient pool and accelerating global uptake.

Key Market Trends

- Expanding indications for transcatheter therapies from high-risk to intermediate and low-risk patients driven by landmark randomized trials and updated guidelines.

- Rapid growth in transcatheter mitral and tricuspid interventions as device innovation addresses complex valve anatomies.

- Increasing adoption of transfemoral, minimalist TAVR pathways enabling shorter hospital stays and outpatient care models.

- Integration of advanced imaging and AI for precision sizing, reduced complications, and streamlined procedural planning.

- Movement toward service- and outcomes-based commercial models (including RaaS-like training and registry-linked reimbursement) to support broader market access.

Segmental Insights

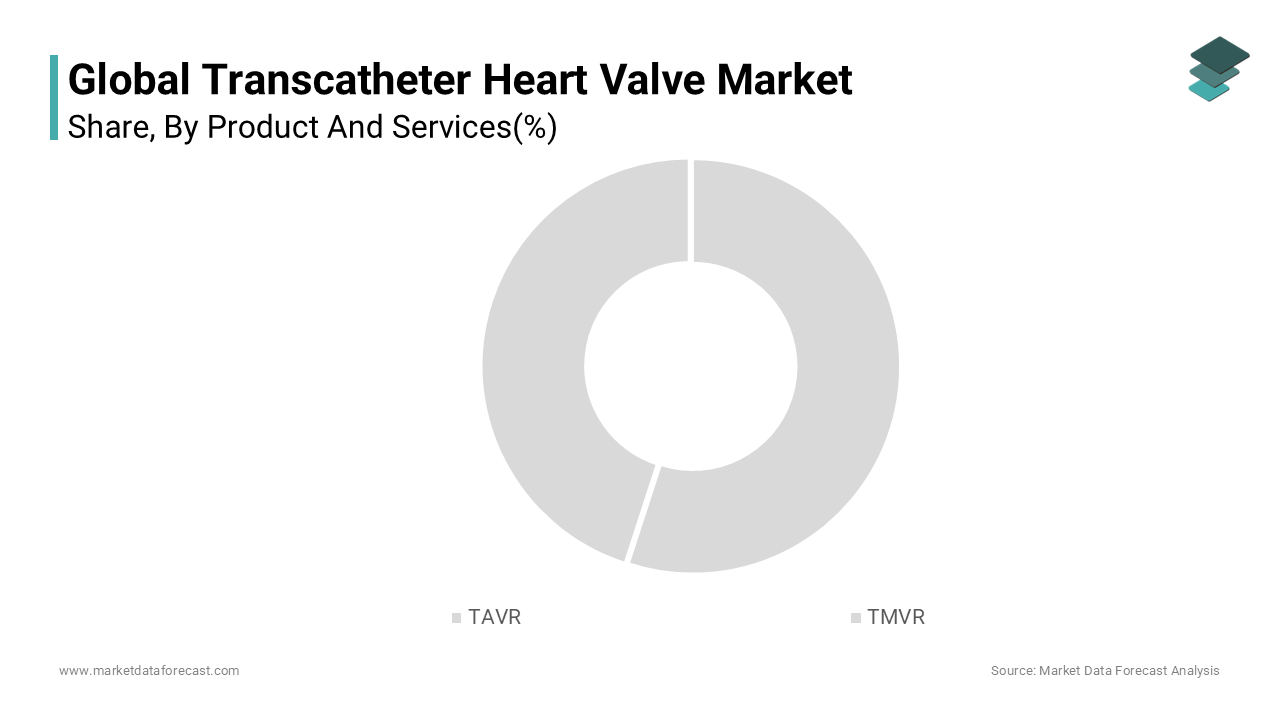

- Based on products and services, the TAVR (Transcatheter Aortic Valve Replacement) segment dominated the market in 2024, owing to mature clinical evidence, broad regulatory approvals, and clear diagnostic thresholds that create a large, addressable patient population for aortic stenosis.

- Based on product and services (growth segment), the TMVR (Transcatheter Mitral Valve Repair/Replacement) segment is projected to register the highest CAGR (~18.3% from 2025–2033), driven by unmet needs in heart-failure populations and emerging replacement systems that expand treatable indications.

- Based on delivery systems, the transfemoral approach was the leading delivery route in 2024, supported by lower invasiveness, smaller sheath profiles, faster recovery and widespread applicability in most patients.

- Based on end user, Hospitals accounted for the majority share in 2024, reflecting the need for multidisciplinary heart teams, hybrid catheterization/surgical suites, and critical-care backup for complex structural procedures.

Regional Insights

The global transcatheter heart valve market is expanding worldwide, with adoption driven by reimbursement clarity, clinical training programs, and demographic pressures in different regions.

- North America was the largest region, accounting for ~42.3% of the market in 2024, driven by early adoption, comprehensive reimbursement (notably CMS policies), extensive registry participation and high procedural volumes.

- Europe held ~31.6% share in 2024, supported by guideline alignment, public healthcare integration, and strong registry-driven quality improvement programs across major markets such as Germany, the UK and France.

- Asia-Pacific is a rapidly growing region, propelled by aging populations (notably Japan), expanding regulatory approvals, increased physician training, and growing procedure volumes in China, India and Australia.

- Latin America, Middle East & Africa are emerging markets with selective adoption concentrated in private and tertiary referral centers, medical-tourism hubs, and national centers of excellence as infrastructure and reimbursement mature.

Competitive Landscape

The global transcatheter heart valve market is oligopolistic and innovation-driven, dominated by companies with deep clinical evidence, large installed bases, and comprehensive training/regulatory programs. Competition centers on valve durability, deliverability, paravalvular seal, coronary access, and expansion into non-aortic valves. Companies pursue multicenter randomized trials, registry participation, and strategic partnerships to secure guideline inclusion and reimbursement. Price and value-based contracting, expansion into emerging markets, and development of lower-profile and specialty platforms (mitral/tricuspid) are key strategic priorities. Prominent players in the global transcatheter heart valve market include Edwards Lifesciences Corporation, Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, LivaNova PLC, JenaValve, Venus Medtech, Meril Life Sciences, CryoLife, and MicroPort Scientific Corporation.

Global Transcatheter Heart Valve Market Size

The global transcatheter heart valve market size was valued at USD 3.27 billion in 2024 and is estimated to reach USD 11.23 billion by 2033 from USD 3.74 billion in 2025, registering a CAGR of 14.44% from 2025 to 2033.

Transcatheter heart valves are implantable medical devices designed to replace or repair dysfunctional native heart valves, primarily the aortic and mitral valves, via minimally invasive catheter based delivery rather than open chest surgery. These prostheses typically consist of a bioprosthetic leaflet structure mounted on a self-expanding or balloon expandable metal stent frame, deployed through femoral or transapical access routes under fluoroscopic and echocardiographic guidance. The technology was initially developed for high risk or inoperable patients with severe aortic stenosis but has progressively expanded to intermediate and low risk populations as clinical evidence accumulates. The global volume of transcatheter aortic valve replacement (TAVR) procedures has shown significant growth trends. As per research, guidelines from major cardiology and surgical associations have expanded the indications for transcatheter valve therapy to include patients across various surgical risk profiles, moving beyond the initial high-risk population. The number of FDA-approved transcatheter heart valve technologies has expanded steadily since the initial approval, with ongoing innovation in device design. Furthermore, Valvular heart disease is a significant and growing public health concern, with the prevalence of conditions like aortic stenosis increasing notably in aging populations. This establishes a substantial and growing patient pool amenable to catheter based intervention.

MARKET DRIVERS

Aging Global Population Expands the Pool of Eligible Patients

The rising prevalence of degenerative valvular heart disease among elderly populations directly fuels the growth of the transcatheter heart valve market. This is because surgical risk increases with age. According to multiple sources, the global population of individuals aged 65 and over is rapidly expanding and is projected to more than double by mid-century. Moreover, as per a study, the prevalence of degenerative calcific aortic stenosis (AS) is strongly age-related, with a prevalence of approximately 0.2% among people in their 50s that increases significantly to about 9.8% among octogenarians (those aged 80-89 years). This has significant implications for the healthcare market in developed nations, where the condition is the most prevalent form of valvular heart disease, as increasing life spans are projected to more than double the burden of severe AS cases requiring intervention by 2050. The European Heart Journal published data showing that 78 percent of patients diagnosed with severe symptomatic aortic stenosis are aged 75 or older making them ideal candidates for transcatheter intervention. In addition, due to the nation's aging demographic, the median age in Japan reached approximately 49.0 years in 2023 (one of the highest globally, second only to Monaco). This trend, coupled with clinical guidelines recommending the procedure for elderly patients, has led to a significant increase in transcatheter aortic valve implantation (TAVI). This demographic inevitability ensures a sustained and expanding base of high need patients for whom transcatheter valves offer the only viable therapeutic option.

Robust Clinical Evidence Supporting Broader Indications

Landmark randomized trials have progressively validated the safety and efficacy of transcatheter valves in lower risk populations thereby expanding treatable indications and transcatheter heart valve market. Recent trials and guidelines indicate that transcatheter aortic valve replacement is superior or non-inferior to surgical replacement in low-risk patients, associated with reduced adverse events like death, stroke, rehospitalization, acute kidney injury, and atrial fibrillation. Transcatheter therapy is a recommended first-line option for all eligible patients with severe aortic stenosis and has been extended to include mitral valve interventions. These evidence-based guideline shifts have transformed transcatheter valves from rescue therapy to standard of care accelerating procedural volumes across diverse healthcare systems.

MARKET RESTRAINTS

High Procedure and Device Costs Limit Access in Resource Constrained Settings

The substantial expense associated with these systems, including the device delivery system imaging support and specialized personnel, restricts adoption in low- and middle-income countries and underfunded healthcare systems, which poses a major restraint to the transcatheter heart valve market. The average cost of a transcatheter aortic valve replacement (TAVR) often exceeds a significant dollar amount, with device costs comprising the majority of the expense, as per sources. A very low percentage of eligible patients in certain developing regions receive this therapy due to financial and infrastructural barriers. According to research, access to the procedure in one specific large country is limited to a small number of hospitals outside major metropolitan areas because the required hybrid operating rooms are exceptionally expensive. Public health systems in many Latin American countries cover transcatheter valves in fewer than a third of states. Hospital systems in another major country are experiencing negative financial margins on a large percentage of TAVR cases due to insufficient insurance reimbursement rates relative to actual costs. These economic constraints create significant disparities in access despite proven clinical benefit.

Risk of Long Term Durability and Reintervention Uncertainties

The long-term performance of transcatheter bioprosthetic valves beyond 10 to 15 years is unclear, which creates uncertainty about structural valve deterioration and the subsequent need for repeat procedures, and thereby hinders the expansion of the transcatheter heart valve market. Short- and mid-term outcomes, however, are well-established. Medical experts have observed a notable incidence of bioprosthetic heart valve failure within less than a decade following implantation. Younger individuals receiving bioprosthetic valves exhibit a higher rate of valve degradation compared to older patient groups. Due to limited information regarding long-term durability, professional medical bodies are advising caution against the standard use of these valves in certain younger patient demographics. Long-term studies following patients for a decade indicate that a percentage experience severe structural degeneration of their implanted valves. Furthermore, the feasibility of valve in valve procedures, while technically possible, carries higher risks of coronary obstruction and patient prosthesis mismatch. These uncertainties complicate decision making for younger patients and may delay adoption until more durable materials or regenerative technologies emerge creating a ceiling on market expansion in lower age cohorts.

MARKET OPPORTUNITIES

Expansion into Mitral and Tricuspid Valve Segments

The rapid advancement of transcatheter applications for the mitral and tricuspid valves is a major growth frontier in medical technology, which is setting up new opportunities for the growth of the transcatheter heart valve market. This development is building upon the established success of aortic valve replacement. According to research, a large population of individuals experiences significant mitral regurgitation, and many of these individuals are not suitable candidates for traditional surgical intervention. A new transcatheter mitral valve replacement system is now approved for use, demonstrating a significant reduction in mortality at one year compared to standard medical therapy alone. The use of transcatheter tricuspid interventions has experienced substantial growth in adoption. As per sources, severe tricuspid regurgitation impacts a significant number of patients, most of whom currently have no available surgical option. As imaging guidance and delivery systems improve these anatomically complex valves are becoming increasingly addressable creating a multi-billion dollar opportunity beyond the mature aortic segment.

Adoption of Artificial Intelligence and Advanced Imaging for Precision Implantation

Integration of artificial intelligence and real time multimodal imaging is enhancing procedural accuracy and reducing complications thereby broadening operator confidence and patient eligibility. This integration is creating potential prospects for the expansion of the transcatheter heart valve market. AI-powered pre-procedural planning tools are used to predict optimal valve sizing and landing zones, according to studies. An AI-based echocardiography analysis platform now automates annular measurements quickly. As per research, centers utilizing 3D fusion imaging of CT and fluoroscopy have reported reduced contrast volume usage and shorter procedure times. Machine learning algorithms are being implemented to predict post-implantation conduction disturbances, which enables preemptive pacemaker planning. These technological synergies not only improve outcomes but also shorten learning curves for new implanting centers accelerating global diffusion of transcatheter valve therapy beyond elite academic hospitals.

MARKET CHALLENGES

Complex Reimbursement Landscapes and Coverage Variability

Reimbursement policies for these valves vary significantly across countries and even within regions, which is one of the major challenges to the transcatheter heart valve market. This creates administrative and financial unpredictability for providers. Coverage for certain advanced medical procedures is not universally provided across all member countries of an organization. Prior authorization requirements frequently result in significant delays in patient care. Payer organizations in a specific large country enforce strict coverage criteria, requiring participation in registries. A significant percentage of rural healthcare facilities are unable to meet these registry participation requirements due to limitations in information technology. Moreover, a national regulatory body in another country mandates individual case-by-case approval for specific patient age groups. The national health system in a major South American country only partially reimburses the cost of medical devices. These fragmented and evolving payment models discourage investment in necessary infrastructure and trained personnel particularly in community hospitals thereby limiting equitable access despite clinical guidelines endorsing broad use.

Shortage of Trained Structural Heart Interventionalists

The successful deployment of transcatheter heart valves requires a multidisciplinary heart team including interventional cardiologists, imaging specialists, and cardiac surgeons with specialized training in structural heart disease, which poses a serious impediment to the transcatheter heart valve market. Globally, this specialized workforce remains insufficient. According to sources, there is a significant shortage of qualified professionals capable of performing structural heart procedures relative to the overall patient population size and the increasing demand for these interventions. In addition, as per studies, most nations lack formalized training pathways or accreditation programs for physicians to specialize in advanced transcatheter procedures like transcatheter valve implantation. Also, a substantial gap exists between the large number of patients eligible for specific structural heart interventions (e.g., TAVR) and the very limited number of physicians qualified to perform the procedure nationwide. The proficiency curve for these procedures is steep; a low annual operator volume is directly correlated with a significantly higher risk of adverse outcomes and mortality shortly after surgery. The continued shortage of skilled personnel will impede progress in procedural quality and growth, despite technological advances, if standardized credentialing and scalable simulation training pathways are not established.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Analysed | By Product and Services, Delivery System, End User and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Analysed | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Edwards Lifesciences Corporation, Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, LivaNova PLC, JenaValve Technology, Inc., Venus Medtech (Hangzhou) Inc., Meril Life Sciences Pvt. Ltd., CryoLife, Inc. and MicroPort Scientific Corporation are a few of the notable companies in the global transcatheter heart valve market. |

SEGMENTAL ANALYSIS

By Product and Services Insights

The Transcatheter Aortic Valve Replacement (TAVR) segment dominated the transcatheter heart valve market by capturing a substantial share in 2024. Its maturity, robust clinical validation, and broad regulatory approvals across risk strata have mainly contributed to the dominance of the TAVR segment. Major cardiology societies have uniformly adopted TAVR as first line therapy for severe aortic stenosis irrespective of surgical risk. Regulatory bodies continue to clear new generations of TAVR systems, which feature improvements such as enhanced repositionability and reduced paravalvular leak. Major clinical trials have demonstrated outcomes that are superior or non-inferior to traditional surgical options for low-risk patient groups, leading to rapid and widespread adoption in community hospitals. This evidence-based consensus has transformed TAVR from a niche rescue therapy to standard of care across the entire aortic stenosis spectrum. Degenerative calcific aortic stenosis is the most common valvular heart disease in developed nations with a well defined progression trajectory. Unlike mitral or tricuspid disease aortic stenosis has a clear hemodynamic threshold for intervention, valve area below 1.0 cm² or mean gradient above 40 mmHg, enabling straightforward patient identification. The high disease burden combined with unambiguous diagnostic criteria ensures a large and consistent patient pool for TAVR.

The Transcatheter Mitral Valve Repair/Replacement (TMVR) segment is predicted to witness the highest CAGR of 18.3% percent from 2025 to 2033, which is driven by unmet need in heart failure populations and recent regulatory milestones. Functional mitral regurgitation affects a significant share of patients with advanced heart failure creating a vast eligible population. According to sources, a notable number of individuals experience moderate to severe mitral regurgitation. Also, a proportion of these individuals may not be suitable candidates for conventional surgical intervention due to existing health conditions or impaired heart function. Transcatheter edge-to-edge repair has been studied in patients with secondary mitral regurgitation. Clinical trial evidence suggests that this transcatheter approach may lead to a reduction in heart failure hospitalizations and a decrease in the risk of mortality in a specific patient group. Current clinical practice guidelines include a recommendation for considering transcatheter mitral intervention in carefully selected patients. This clinical validation has unlocked a new patient cohort previously managed only with medical therapy. The initial adoption of repair devices paved the way for market acceleration, which is now driven by the introduction of true replacement systems. The technological advances address anatomical complexities that limited earlier repair only approaches thereby expanding treatable indications and driving exponential growth

By Delivery Systems Insights

The transfemoral approach segment led the transcatheter heart valve market by occupying a significant share in 2024. Factors such as its minimally invasive nature and compatibility with percutaneous techniques are attributed to the leading position of the transfemoral approach segment. Contemporary TAVR systems commonly use smaller access sheaths. Advancements allow for access through narrower iliofemoral arteries. A majority of TAVR procedures now utilize these reduced sheath sizes. Pre-procedural imaging is a common practice for evaluating vascular anatomy. This assessment helps in minimizing potential vascular complications. Systematic evaluation of vascular access is a routine part of the procedure guidelines. These innovations have made transfemoral access feasible in most of patients who previously required alternative routes due to peripheral artery disease. The percutaneous nature of transfemoral delivery enables same day ambulation and shorter hospitalization. As per sources, the average length of hospital stay following transfemoral TAVR procedures has decreased considerably over time. A growing number of cases involving this procedure are now managed in an outpatient setting or with a short observation period. Patients who undergo the transfemoral approach experience a faster recovery to their usual functional status compared to those undergoing the transapical method. This accelerated recovery reduces healthcare costs and aligns with value-based care models. These outcomes solidify transfemoral as the preferred route across all care settings.

The transapical approach segment is estimated to register the fastest CAGR of 9.7% during the forecast period. The rapid expansion of the transapical approach segment is fuelled by complex anatomies and mitral valve applications. A subset of individuals being evaluated for transcatheter aortic valve replacement (TAVR) may have vascular pathways in their iliofemoral region that are not suitable for the standard transfemoral approach. Certain patients in clinical studies have required alternative delivery methods due to these vascular challenges. For some replacement systems, particularly those for the mitral valve which require larger equipment, a specific alternative access point is often used. The shift in the demographic eligible for this procedure towards an older age bracket may correspond to a higher occurrence of peripheral vascular conditions. This anatomical reality ensures continued demand for transapical as a vital alternative access strategy. Several next generation transcatheter valves are specifically designed for transapical deployment due to coaxial alignment requirements. The expansion of structural heart interventions beyond the aortic valve means that transapical access is strategically relevant once more for challenging anatomical targets.

By End User Insights

In 2024, the hospitals segment remained the dominant segment in the transcatheter heart valve market and accounted for a majority share as transcatheter valve procedures require multidisciplinary teams and advanced infrastructure. Current guidelines from the American College of Cardiology and European Society of Cardiology require a formal heart team, including interventional cardiologists cardiac surgeons imaging specialists and anesthesiologists, for all transcatheter valve cases. "According to the Centers for Medicare and Medicaid Services (CMS) guidelines, TAVR reimbursement is tied to specific facility requirements that ensure safety and positive patient outcomes. The majority of TAVR procedures in the United States take place in hospital settings that meet these stringent infrastructure and accreditation standards. Hospitals also provide critical care support for potential complications such as annular rupture or conduction disturbances which occur in a portion of cases. This clinical and regulatory complexity confines the vast majority of procedures to acute care settings. Hospitals leverage established cardiac catheterization and surgical programs to streamline transcatheter valve workflows. Apart from these, hospital based programs participate in national registries like TVT which are required for regulatory compliance and quality benchmarking. This ecosystem of expertise infrastructure and data reporting creates a self-reinforcing advantage that community or outpatient settings cannot replicate.

The ambulatory surgical centers segment is anticipated to witness the fastest CAGR of 14.2% over the forecast period, as procedural safety improves and recovery times shorten. The significantly lower complication rates for low-risk TAVR have enhanced the feasibility of performing the procedure in an outpatient setting. A growing number of TAVR procedures are being performed in outpatient settings. Industry groups have established criteria for identifying patients suitable for ambulatory care, focusing on specific clinical characteristics. Data indicates that facilities performing TAVR on an ambulatory basis achieve comparable patient outcomes to traditional hospital settings. This clinical equivalence combined with 30 percent lower facility fees is driving payer and provider interest in decentralized care models. Government and private payers are incentivizing lower cost settings through site neutral payment adjustments. According to sources, reimbursement rates for facility-based TAVR procedures have remained consistent in certain contexts, while payments for ambulatory TAVR procedures have seen an increase. Ambulatory TAVR is included in a value-based care initiative framework that encourages risk sharing among providers. Private insurers cover outpatient TAVR at a percenatge of hospital rates provided quality metrics are met. This policy tailwind is accelerating the migration of select cases to specialized outpatient environments.

REGIONAL ANALYSIS

North America Transcatheter Heart Valve Market Analysis

North America was the top performer in the transcatheter heart valve market and accounted for a share of 42.3% in 2024. Factors like early adoption, robust reimbursement, and high disease awareness are primarily driving the domination of the North American market. The United States is the epicenter with the Centers for Medicare and Medicaid Services covering TAVR for risk categories. According to sources, the number of TAVR procedures performed has shown significant growth. A substantial portion of these procedures are now being performed in low-risk patients. Canada contributes through universal healthcare coverage. Annual TAVR volumes are indicating a consistent upward trend. Mexico’s growth stems from medical tourism with a notable number of international patients are seeking TAVR treatment in private healthcare facilities. The region’s combination of regulatory clarity payer support and specialized training programs sustains its leadership position.

Europe Transcatheter Heart Valve Market Analysis

Europe was the second-largest region in the transcatheter heart valve market and captured a share of 31.6% share in 2024. The expansion of the European market is propelled by standardized guidelines and public health system integration. Germany leads with the Federal Joint Committee emphasizing heart team evaluation for all cases and reimbursing TAVR significant euros per procedure. The volume of TAVR procedures performed across certain regions has been substantial, according to studies. Updated guidance in some healthcare systems supports TAVR as a primary treatment option for specific age groups. Also, there is an emerging trend toward pioneering outpatient models for TAVR, with a significant percentage of low-risk cases seeing rapid discharge. Europe’s strength lies in equitable access and data driven quality improvement through registries like EuroPCR.

Asia Pacific Transcatheter Heart Valve Market Analysis

Asia Pacific experienced rapid growth in the transcatheter heart valve market because of aging populations and healthcare investment. Japan is the regional leader with significant number of TAVR procedures in 2023 driven by the world’s highest median age. Australia has expanded its public funding for TAVR, with the Medicare Benefits Schedule now providing coverage for patients across all surgical risk categories, from high to low risk. China's transcatheter valve market is experiencing rapid expansion driven by increased regulatory approvals of innovative devices (both local and international) and substantial growth in physician training and procedure volume, reflecting an accelerating adoption of TAVR technology. India's TAVR market remains nascent but growing. The region’s vast untreated patient pool and rising medical infrastructure ensure sustained double digit growth.

Middle East and Africa Transcatheter Heart Valve Market Analysis

The Middle East and Africa region is an emerging transcatheter heart valve market, with growth centered on medical tourism and urban healthcare hubs. Saudi Arabia's healthcare system, supported by Vision 2030, is expanding its capacity in highly specialized fields like structural heart diseases, aiming to improve accessibility and quality of services across the Kingdom. The United Arab Emirates has a well-developed private and public healthcare infrastructure, including numerous advanced hospitals capable of performing complex TAVR procedures. South Africa's private healthcare sector plays a significant role in adopting advanced medical technologies and procedures. Egypt and Turkey are recognized for their established healthcare systems and capabilities, serving as key regional referral hubs for complex medical interventions, including advanced cardiac procedures, attracting both domestic and international patients. Despite low per capita penetration the concentration of high-net-worth patients and government investment in specialty care creates a distinct growth corridor.

Latin America Transcatheter Heart Valve Market Analysis

Latin America is predicted to grow notably in the transcatheter heart valve market during the forecast period, with Brazil and Mexico leading adoption through private healthcare systems. Brazil’s Ministry of Health reported 3200 TAVR procedures in 2023 with 85 percent performed in private hospitals in São Paulo and Rio de Janeiro. Mexico’s growth is fueled by medical tourism with considerable number of international patients received TAVR primarily from the United States and Canada. Chile and Colombia are emerging. Argentina’s public system remains limited. While constrained by public funding the region’s affluent urban populations and proximity to North America support steady expansion in specialized private centers.

COMPETITVE LANDSCAPE

The transcatheter heart valve market is characterized by intense competition among a few dominant players with high barriers to entry due to regulatory complexity clinical validation requirements and intellectual property density. Leadership is determined by clinical outcomes device reliability and physician preference rather than price. Edwards Lifesciences maintains first mover advantage with strong hemodynamic performance while Medtronic competes through self expanding technology suited for complex anatomies. Abbott differentiates with its edge to edge repair focus in heart failure populations. New entrants face significant challenges in conducting costly randomized trials and establishing heart team relationships. Competition is increasingly shifting toward mitral and tricuspid segments where anatomical complexity creates opportunities for novel mechanisms. Innovation cycles are accelerating with annual device iterations improving deliverability and sealing. Reimbursement pressures and value based care models are also driving companies to demonstrate long term cost effectiveness beyond procedural success. The market remains highly specialized with success dependent on deep clinical collaboration and continuous technological refinement.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global transcatheter heart valve market.

- Edwards Lifesciences Corporation

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corporation

- LivaNova PLC

- JenaValve Technology, Inc.

- Venus Medtech (Hangzhou) Inc.

- Meril Life Sciences Pvt. Ltd.

- CryoLife, Inc

- MicroPort Scientific Corporation

Top Players in the Market

Edwards Lifesciences Corporation

Edwards Lifesciences Corporation is a pioneer and global leader in transcatheter heart valve technology having introduced the first commercially approved TAVR system. The company offers a comprehensive portfolio including the SAPIEN family of aortic valves and the PASCAL system for mitral and tricuspid repair. Edwards emphasizes innovation in valve design hemodynamics and delivery precision to improve clinical outcomes. Edwards also expanded its EVOQUE tricuspid valve trial to include patients across multiple countries. These initiatives reinforce its commitment to advancing structural heart therapy across all four heart valves through rigorous clinical validation and engineering excellence.

Medtronic plc

Medtronic plc is a major participant in the transcatheter heart valve market with its CoreValve and Evolut platforms for aortic valve replacement and the Intrepid system for mitral valve replacement. The company leverages its global distribution network and integrated cardiac rhythm management portfolio to offer comprehensive heart failure solutions. Medtronic focuses on self expanding valve technology that accommodates annular calcification and enables valve in valve procedures. The company also initiated the MIRACLE II trial to evaluate transcatheter mitral replacement in heart failure patients with functional regurgitation. These efforts demonstrate Medtronic’s strategy of expanding indications and improving device performance through iterative innovation.

Abbott Laboratories

Abbott Laboratories plays a significant role in the transcatheter valve space primarily through its MitraClip and TriClip platforms for edge to edge repair of mitral and tricuspid valves. The company entered the market through strategic acquisition and has since focused on heart failure populations with functional valve regurgitation. Abbott’s technology enables precise leaflet grasping under real time imaging guidance offering a less invasive alternative to surgery. The company also expanded the TRILUMINATE Pivotal trial to include 1000 patients across North America and Europe. Abbott’s emphasis on right sided heart failure and physician training programs strengthens its position in the rapidly growing tricuspid intervention segment.

Top Strategies Used by the Key Market Participants

Key players in the transcatheter heart valve market prioritize clinical evidence generation through large scale randomized trials to support guideline inclusion and reimbursement. They invest heavily in next generation valve design focusing on lower delivery profiles enhanced repositionability and reduced paravalvular leak. Geographic expansion into emerging markets such as Asia and Latin America addresses unmet need and diversifies revenue streams. Companies also broaden their portfolios beyond aortic valves into mitral and tricuspid territories to capture new patient populations. Strategic acquisitions of innovative startups accelerate technology access and talent acquisition. Additionally they develop integrated imaging and delivery systems to improve procedural accuracy and shorten operator learning curves. Physician training and proctoring programs ensure consistent high quality implantation across global centers reinforcing brand loyalty and clinical outcomes.

RECENT MARKET HAPPENINGS

- In February 2024, Edwards Lifesciences Corporation earned U.S. Food and Drug Administration (FDA) approval for its EVOQUE transcatheter tricuspid valve replacement system, the first transcatheter therapy of its kind to be approved for the tricuspid valve. This regulatory milestone is anticipated to address the growing burden of tricuspid regurgitation and strengthen the transcatheter heart valve market presence.

- In March 2024, Medtronic plc received U.S. FDA approval for its Evolut FX+ transcatheter aortic valve system, featuring a novel frame with larger windows designed to improve coronary access. This launch is anticipated to expand the treatable patient population and strengthen the company's transcatheter heart valve market presence.

- In April 2024, Abbott Laboratories obtained U.S. FDA approval for its TriClip G4 transcatheter tricuspid valve repair system. This U.S. regulatory milestone is anticipated to address the growing burden of tricuspid regurgitation in the U.S. and strengthen the company's transcatheter heart valve market presence.

MARKET SEGMENTATION

This research report on the global transcatheter heart valve market has been segmented and sub-segmented based on the following categories.

By Product and Services

- TAVR

- TMVR

By Delivery Systems

- Transfemoral Approach

- Transapical Approach

- Transaortic Approach

By End User

- Hospitals

- Ambulatory Surgical Centers

- Cardiac Catheterization Laboratory

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa