UK Airlines Market Size, Share, Trends & Growth Forecast Report - Segmented By Transport, Application, and By Country - Industry Analysis and Forecast, 2026 to 2034

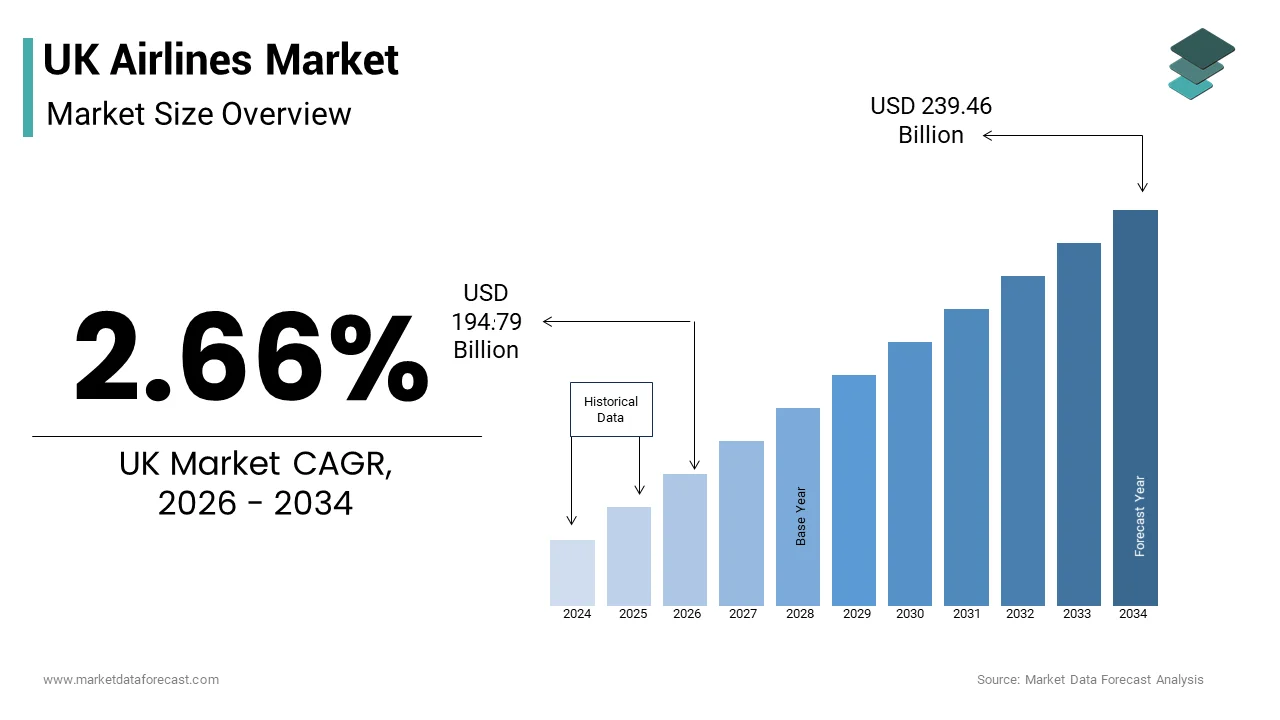

Market Size, 2025

$189.72 BnMarket Estimate, 2026

$194.79 BnMarket Forecast, 2034

$239.46 BnCAGR, 2026–2034

2.66%UK Airlines Market Report Summary

The UK airlines market was valued at USD 189.72 billion in 2025, is estimated to reach USD 194.79 billion in 2026, and is projected to reach USD 239.46 billion by 2034, growing at a CAGR of 2.66% during the forecast period from 2026 to 2034. The growth of the UK airlines market is driven by increasing international passenger traffic, expanding business and leisure travel, and the country's strategic position as a global aviation hub. Rising investments in airport infrastructure, fleet modernization, and digital passenger services are supporting operational efficiency and customer experience. The growing adoption of sustainable aviation practices, fuel-efficient aircraft, and advanced air traffic management technologies is further contributing to market expansion. Additionally, the recovery of international tourism, increasing demand for premium air travel, and the expansion of long-haul and regional connectivity continue to create significant growth opportunities for airlines operating in the United Kingdom.

Key Market Trends

- Rising demand for international air travel driven by recovering tourism, business mobility, and global trade activities.

- Increasing investments in fuel-efficient aircraft and sustainable aviation fuel (SAF) to reduce carbon emissions and improve operational efficiency.

- Growing adoption of digital technologies, including biometric boarding, AI-powered customer service, and contactless airport experiences.

- Expansion of premium travel services and loyalty programs to enhance passenger retention and improve customer satisfaction.

- Increasing focus on route optimization, fleet modernization, and strategic airline partnerships to strengthen operational performance.

Segmental Insights

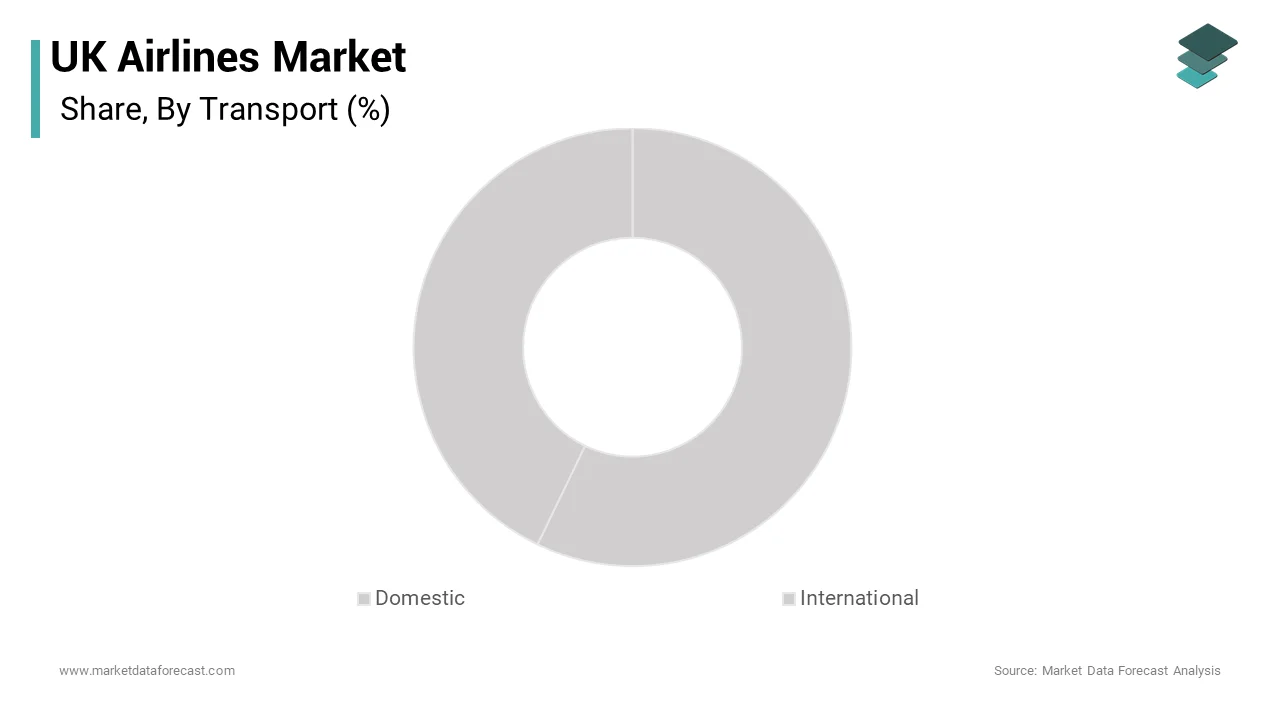

Based on transport, the international transport segment dominated the UK airlines market in 2025. The segment's leadership is attributed to the United Kingdom's extensive global air connectivity, strong demand for international business and leisure travel, and the presence of major international airports serving long-haul and short-haul destinations.

Based on application, the passenger segment held the leading share of the UK airlines market in 2025. The segment continues to dominate due to rising domestic and international passenger volumes, increasing tourism activities, growing corporate travel, and continuous expansion of airline route networks across Europe and other global destinations.

Regional Insights

The United Kingdom held the largest share of the European airlines market in 2025 and is expected to further strengthen its position as one of Europe's leading aviation hubs throughout the forecast period. The country's well-developed airport infrastructure, strong international connectivity, and high passenger traffic continue to support market growth. Major airports, including London Heathrow and other regional gateways, play a critical role in facilitating global travel and trade. Furthermore, increasing investments in airport expansion, digital aviation technologies, sustainability initiatives, and airline fleet modernization are reinforcing the UK's leadership in the European aviation industry.

Competitive Landscape

The UK airlines market is highly competitive, with leading global and regional carriers competing through network expansion, fleet modernization, service innovation, and sustainability initiatives. Airlines are investing in fuel-efficient aircraft, sustainable aviation fuel adoption, digital passenger engagement platforms, and advanced operational technologies to improve efficiency and reduce environmental impact. Strategic alliances, codeshare agreements, route expansion, and investments in premium travel experiences remain key competitive strategies across the industry. Companies are also enhancing loyalty programs, introducing personalized travel services, and leveraging artificial intelligence to optimize pricing, scheduling, and customer support. As demand for international travel continues to recover, airlines are focusing on operational resilience, enhanced passenger experience, and sustainable growth to strengthen their competitive position in the UK market.

Prominent players in the UK airlines market include Air France-KLM, American Airlines Group, ANA Holdings, British Airways, Delta Air Lines, Deutsche Lufthansa, Hainan Airlines, Virgin Atlantic Airways Limited, Japan Airlines, LATAM Airlines Group, Qantas Airways, Ryanair Holdings, Singapore Airlines, Southwest Airlines, Thai Airways International PCL, United Continental Holdings, and WestJet Airlines.

UK Airlines Market Size

The UK airlines market size was valued at USD 189.72 billion in 2025 and is anticipated to reach USD 194.79 billion in 2026 to reach USD 239.46 billion by 2034, growing at a CAGR of 2.66% during the forecast period from 2026 to 2034.

The UK airlines market is characterized by intense competition, price sensitivity, and a high degree of regulatory oversight regarding safety and environmental standards. Consumer behavior is heavily influenced by economic conditions, with leisure travel dominating demand patterns alongside significant business traffic centred on London and other major hubs. According to the UK Civil Aviation Authority, there were approximately 302 million terminal passengers in the UK in the most recent annual data, reflecting the scale of air travel activity. The geographic position of the UK as an island nation makes air transport essential for trade, tourism, and personal connections. Infrastructure constraints at key airports, such as Heathrow and Gatwick, shape operational capabilities and growth potential. The industry is currently navigating a complex transition toward sustainability, driven by government mandates and consumer awareness. Digital transformation has reshaped the customer experience, with mobile booking and biometric processing becoming standard expectations. The labor market within aviation faces unique challenges regarding skilled personnel retention and training requirements. This ecosystem requires stakeholders to balance commercial viability with social responsibility, while adapting to evolving geopolitical and economic landscapes. The resilience of the sector is tested by external shocks, but remains vital for the broader economic health of the nation.

MARKET DRIVERS

Resurgence of International Tourism and Leisure Travel Demand

The robust recovery and subsequent growth of international tourism is propelling the expansion of the UK airlines market, as consumers prioritize experiential spending and global exploration. Following periods of restricted movement, there is a pronounced pent up demand for holidays and visits to friends and relatives abroad. According to the Office for National Statistics, outbound visits by UK residents reached 94.6 million visits in 2024, which is indicating a strong desire for international connectivity. Leisure travellers are increasingly seeking diverse destinations beyond traditional European hotspots, driving expansion into long haul markets. The flexibility offered by low cost carriers has democratized air travel, making it accessible to broader demographic, including younger generations and budget conscious families. Social media influence plays a significant role in inspiring travel choices, with viral destinations creating sudden spikes in demand for specific routes. Airlines respond by adjusting capacity and launching new seasonal services to capitalize on these trends. The integration of holiday packages with flight bookings further stimulates demand, by offering convenience and value. This driver is sustained by the cultural importance of annual leave and the perception of travel as an essential component of quality life. As disposable income stabilizes, the propensity to spend on airfare remains high and is ensuring consistent load factors and revenue generation for carriers operating in the UK market.

Expansion of Business Connectivity and Corporate Travel Recovery

The gradual but steady recovery of corporate travel and the need for enhanced business connectivity is further boosting the expansion of the UK airlines market. Despite the rise of remote work, face to face interactions remain crucial for high value negotiations, team building, and client relationship management. The need for corporate physical meetings has shown steady growth, as companies resume international operations and conferences. London serves as a global financial hub, attracting executives from around the world who rely on efficient air links for short notice trips. Full service carriers benefit disproportionately from this segment, due to their premium cabin offerings and flexible ticket policies that cater to corporate needs. The emergence of bleisure travel, where professionals extend business trips for leisure purposes, adds volume to both segments. Airlines are tailoring their products to meet these hybrid needs, with improved lounge facilities and seamless digital experiences. The concentration of multinational headquarters in the UK ensures a baseline demand for premium air services. This driver is reinforced by the economic necessity of maintaining global supply chains and partnerships, which require physical presence. As confidence in business environments grows, the frequency of corporate flights increases and is supporting higher yield routes and sustaining the profitability of legacy carriers in the UK market.

MARKET RESTRAINTS

Environmental Regulations and Carbon Reduction Mandates

Stringent environmental regulations and mandatory carbon reduction targets are significantly impeding the expansion of the UK airlines market, by imposing operational costs and limiting growth potential. As per the UK Government, commitments have been made to reach net zero emissions by 2050, requiring the aviation sector to adopt sustainable practices rapidly. According to the Committee on Climate Change, the aviation industry must significantly reduce its carbon footprint through technological innovation and operational efficiency. Compliance with these mandates necessitates substantial investment in sustainable aviation fuels, which are currently more expensive than conventional jet fuel. Airlines face pressure to purchase carbon offsets or participate in emissions trading schemes, which increase operational expenses. These costs are often passed on to consumers in the form of higher fares, potentially dampening demand. Regulatory restrictions on night flights and noise pollution at major airports further constrain operational flexibility and capacity utilization. The uncertainty surrounding future tax policies, such as frequent flyer levies, creates a challenging planning environment for carriers. Smaller airlines struggle to absorb these compliance costs, compared to larger competitors with greater financial resources. This regulatory burden slows the pace of network expansion and fleet renewal, as companies balance environmental goals with financial viability. The tension between growth ambitions and ecological responsibilities remains a persistent constraint on the industry.

Infrastructure Capacity Constraints at Major Airports

Physical infrastructure limitations at key UK airports present a significant restraint on the airlines market in the UK, by capping the number of available slots and restricting network expansion. Heathrow Airport operates at near full capacity, leaving little room for new routes or increased frequency without displacing existing services. According to airport authorities, slot availability is highly competitive and expensive, limiting opportunities for new entrants and smaller carriers. Congestion leads to delays and cancellations, which damage airline reputations and increase operational costs due to compensation claims and crew scheduling disruptions. Other major hubs, such as Gatwick and Manchester, also face capacity pressures during peak seasons, constraining growth potential. The slow progress on expanding runway capacity or building new terminals exacerbates these bottlenecks. Airlines are forced to optimize existing schedules rather than grow organically, leading to higher load factors but limited market reach. Ground handling shortages and air traffic control staffing issues further compound these infrastructure challenges. The lack of scalable infrastructure prevents the UK from fully capitalizing on growing demand for air travel. This structural constraint limits competition and keeps fares artificially high on popular routes. Until significant infrastructure investments are realized, the growth of the UK airlines market will remain capped by physical limitations.

MARKET OPPORTUNITIES

Adoption of Sustainable Aviation Fuels and Green Technology

The transition toward sustainable aviation fuels and the adoption of green technology present substantial opportunities for the UK airlines market to enhance brand value and secure long term viability. Consumers and investors are increasingly prioritizing environmental responsibility, creating demand for airlines that demonstrate genuine commitment to sustainability. According to industry analysis, the development of synthetic fuels and hydrogen powered aircraft offers a pathway to decarbonization that aligns with global climate goals. Airlines that invest early in these technologies can differentiate themselves and attract eco conscious travelers willing to pay a premium for greener options. Government grants and subsidies for research and development in green aviation provide financial incentives for innovation. Partnerships with energy companies and aerospace manufacturers can accelerate the commercialization of sustainable solutions. The opportunity extends to operational efficiencies, such as optimized flight paths and weight reduction measures that lower fuel consumption. Marketing campaigns highlighting sustainability efforts can improve customer loyalty and brand perception. As regulatory pressures intensify, early adopters will gain a competitive advantage in compliance and cost management. This shift positions the UK as a leader in green aviation, fostering innovation and attracting talent. Embracing sustainability transforms a regulatory challenge into a strategic asset, driving growth and resilience.

Digital Transformation and Personalized Customer Experiences

The advancement of digital transformation and the delivery of personalized customer experiences offer significant opportunities for the UK airlines market to improve efficiency and revenue. Artificial intelligence and big data analytics enable airlines to understand passenger preferences and tailor offerings accordingly. According to tech industry reports, personalized recommendations for ancillary services, such as seat upgrades, baggage, and lounge access, can significantly increase per passenger revenue. Mobile apps with biometric check in and real time updates enhance convenience and reduce friction at airports. The integration of chatbots and virtual assistants improves customer service responsiveness, while lowering operational costs. Digital platforms allow for dynamic pricing strategies that optimize load factors and maximize yield. Loyalty programs enhanced by digital engagement foster deeper relationships with frequent flyers. The opportunity lies in creating seamless, end to end journeys that integrate rail and road transport options. Data driven insights help airlines predict demand fluctuations and adjust capacity proactively. Enhancing the digital experience appeals to younger demographics that expect instant and intuitive interactions. This technological evolution reduces dependency on traditional distribution channels and strengthens direct customer relationships. By leveraging digital tools, airlines can unlock new revenue streams and improve operational agility in a competitive market.

MARKET CHALLENGES

Volatility in Fuel Prices and Operational Costs

Fluctuations in global fuel prices and rising operational costs pose a major challenge to the UK airlines market, by impacting profitability and pricing stability. Jet fuel constitutes a significant portion of airline expenses, making carriers vulnerable to geopolitical tensions and supply chain disruptions. According to energy market data, sudden spikes in oil prices can erase profit margins and force airlines to implement surcharges that deter price sensitive customers. Hedging strategies provide some protection, but cannot fully eliminate risk, especially in volatile markets. Inflationary pressures on labor, maintenance, and airport fees further strain financial performance. Airlines must balance cost recovery with competitive pricing to maintain market share. Unpredictable costs make long term financial planning difficult, and can delay fleet renewal or route expansion plans. Smaller carriers with less financial buffer are particularly exposed to these shocks. The pass through of costs to consumers may reduce demand if fares become prohibitively high. Managing this volatility requires agile financial management and operational efficiency improvements. The challenge is compounded by the need to invest in sustainable technologies while managing current cost pressures. Without stable input costs, the financial health of the UK airlines market remains precarious.

Labor Shortages and Workforce Retention Issues

Persistent labor shortages and difficulties in workforce retention is further challenging the UK airlines market expansion, which is affecting service reliability and operational continuity. The aviation sector faces a deficit of skilled pilots, cabin crew, engineers, and ground staff following industry downturns and early retirements. For instance, recruitment and training timelines for pilots can take several years, creating a bottleneck in capacity restoration. High turnover rates among ground staff lead to inconsistent service quality and increased training costs. Competition for talent from other sectors exacerbates the shortage, driving up wage bills. Staffing gaps result in flight cancellations and delays, damaging customer trust and brand reputation. The stress of working in a high pressure environment contributes to burnout and absenteeism. Airlines must invest heavily in employee well-being and career development to improve retention. Union negotiations and industrial action related to pay and conditions add further complexity to labor management. The challenge of rebuilding a skilled workforce requires coordinated efforts between airlines, training institutions, and government bodies. Until labor stability is achieved, the UK airlines market will struggle to deliver consistent and reliable services. This human capital crisis threatens the sector’s ability to meet growing demand effectively.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.66% |

| Segments Covered | By Transport, Application, Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Market Leaders Profiled | Air France KLM, American Airlines Group, ANA Holdings, British Airways, Delta Air Lines, Deutsche Lufthansa, Hainan Airlines, Virgin Atlantic Airways Limited, Japan Airlines, LATAM Airlines Group, Qantas Airways, Ryanair Holdings, Singapore Airlines, Southwest Airlines, Thai Airways International PCL, United Continental Holdings, WestJet Airlines |

SEGMENTAL ANALYSIS

By Transport Insights

The international transport segment dominated the market by capturing the largest share of the UK market in 2025 due to the nation’s geographic status as an island and its deep economic integration with global markets. Air travel is the primary mode of long distance connectivity for both trade and tourism, given the physical separation from continental Europe and other continents. According to the Office for National Statistics, international air passenger movements reached 258.5 million in 2024, reflecting the reliance on aviation for cross border mobility. The UK serves as a major global hub, particularly through London Heathrow, which connects passengers to destinations worldwide. Business travelers depend on efficient international links to maintain corporate relationships and supply chains, while leisure travelers seek diverse holiday experiences abroad. The density of international routes far exceeds domestic options, providing consumers with extensive choice and frequency. Legacy carriers have built their networks around these long haul and short haul international corridors, leveraging alliance partnerships to expand reach. The economic value generated by inbound tourism and outbound spending further reinforces the dominance of this segment. Infrastructure investments at major airports are primarily directed toward enhancing international capacity and handling capabilities. This structural necessity ensures that international transport remains the cornerstone of the UK aviation industry, driving revenue and operational focus for all major airlines operating within the region.

On the other end, the domestic transport segment is the fastest growing segment in the UK airlines market and is estimated to record a CAGR of 4.8% during the forecast period owing to the increasing environmental awareness and improved rail air integration. Consumers are becoming more conscious of the carbon footprint associated with short haul flights, leading to a shift toward more sustainable travel options where available. However, for routes where rail alternatives are time prohibitive, such as connections to Scotland and Northern Ireland, air travel remains essential. According to the Department for Transport, efforts to streamline connections between regional airports and national rail networks are making domestic air travel more attractive and efficient. The government’s support for regional connectivity aims to balance economic development across the UK, reducing the dominance of London. Airlines are responding by optimizing schedules and using smaller, more fuel efficient aircraft for domestic routes. The perception of domestic travel as a quicker alternative to long train journeys for business purposes drives demand among time sensitive professionals. Marketing campaigns highlighting the convenience and speed of domestic flights appeal to busy travelers. As remote work trends encourage dispersion of workforce outside major cities, the need for frequent domestic trips increases. This segment benefits from targeted infrastructure improvements and policy support aimed at enhancing internal mobility. The combination of environmental scrutiny and practical necessity creates a niche for efficient domestic air services that are growing faster than the mature international sector.

By Application Insights

The passenger segment held the leading position in the UK airlines market and accounted for the major share of the UK airlines market in 2025. The growth of the passenger segment in the UK market is primarily driven by the massive scale of leisure tourism and personal mobility requirements. The desire for travel, holidays, and visiting friends and relatives constitutes the bulk of air traffic volume. According to the Civil Aviation Authority, passenger numbers significantly outweigh freight tonnage in terms of economic impact and operational frequency. The cultural norm of annual overseas holidays ensures consistent demand throughout the year, with peak seasons driving substantial capacity utilization. Low cost carriers have expanded the market by making air travel affordable for millions of households who previously relied on other modes of transport. The ease of booking and flexibility of modern ticketing systems encourage spontaneous travel decisions. Personal mobility is also driven by migration patterns and family connections across borders, requiring regular air links. The social aspect of travel and the experience economy prioritize passenger movement over cargo in terms of public visibility and infrastructure focus. Airports are designed primarily to handle passenger flows, with terminals, retail, and hospitality services generating significant non aeronautical revenue. This consumer centric model dominates the strategic planning of airlines and airport authorities. The sheer volume of individual travelers ensures that passenger application remains the primary focus of the UK aviation sector.

However, the freight segment is the fastest growing segment in the UK airlines market and is expected to exhibit a CAGR of 6.3% during the forecast period owing to the explosive expansion of e-commerce and demand for express delivery. The shift toward online shopping has created an urgent need for rapid cross border logistics that only air freight can satisfy for high value and time sensitive goods. According to logistics industry data, the volume of air cargo handled at UK airports has increased steadily, as consumers expect faster delivery times. Pharmaceutical products, electronics, and perishable foods rely heavily on air transport to maintain supply chain integrity and freshness. The growth of global online marketplaces has intensified competition among retailers to offer next day or two day delivery options internationally. Airlines are converting passenger aircraft into freighters or utilizing belly hold capacity more efficiently to meet this demand. Dedicated cargo carriers are expanding their networks to connect UK hubs with major manufacturing centers in Asia and America. The reliability and speed of air freight make it indispensable for just in time manufacturing and emergency supplies. This structural shift in consumer behavior ensures that freight volumes continue to rise. The integration of advanced tracking technologies enhances visibility and trust in air cargo services. As e commerce penetrates deeper into global markets, the demand for air freight will sustain its rapid growth trajectory.

COUNTRY ANALYSIS

The UK held the major share of the European airlines market in 2025 and is expected to further solidify its status as a leading European aviation powerhouse over the next few years due to its strategic geographic location and extensive global connectivity. As a mature market, the UK serves as a critical gateway for international travel and trade, linking Europe with North America, Asia, and beyond. According to the Civil Aviation Authority, the UK airport network handles over 300 million passengers annually, underscoring its significance in the global aviation network. The market status is robust, with a mix of legacy carriers, low cost operators, and cargo specialists contributing to a dynamic competitive landscape. London Heathrow remains one of the busiest international airports in the world, acting as a primary connector for global business and tourism. The regulatory environment is stringent, ensuring high standards of safety, security, and environmental compliance. Post Brexit adjustments have introduced new operational complexities, but the market has demonstrated resilience and adaptability. The presence of major aerospace manufacturers and maintenance providers adds depth to the aviation ecosystem. Consumer demand is driven by a strong culture of international travel and a highly integrated global economy. Infrastructure challenges, such as capacity constraints at major airports, persist, but ongoing investments aim to address these bottlenecks. The UK’s influence extends to setting industry standards and pioneering sustainable aviation initiatives. This combination of scale, connectivity, and innovation ensures that the UK remains a dominant force in the European and global airlines market.

COMPETITIVE LANDSCAPE

The competition in the UK airlines market is intense and characterized by a mix of legacy carriers low cost operators and niche regional airlines. Major players compete on price service quality and network connectivity to attract diverse passenger segments. Legacy carriers leverage their global alliances and premium offerings to dominate long haul business travel. Low cost carriers compete aggressively on price and frequency for short haul leisure and visiting friends and relatives traffic. The rise of hybrid models blurs traditional distinctions forcing all airlines to innovate. Capacity constraints at major airports like Heathrow limit entry and favor established incumbents with valuable slots. Customer loyalty programs and digital engagement are key differentiators in retaining high value travelers. Environmental performance is becoming a critical competitive factor as consumers and regulators prioritize sustainability. Airlines must balance cost efficiency with service excellence to survive in this mature and highly regulated market. Strategic partnerships and code share agreements allow carriers to extend reach without heavy capital investment. This dynamic environment requires continuous adaptation and strategic foresight to maintain profitability and market relevance.

KEY MARKET PLAYERS

A few of the market players that are dominating the UK airlines market are

- Air France KLM

- American Airlines Group

- International Consolidated Airlines Group

- ANA Holdings

- EasyJet plc

- British Airways

- Delta Air Lines

- Deutsche Lufthansa

- Hainan Airlines

- Japan Airlines

- LATAM Airlines Group

- Qantas Airways

- Ryanair Holdings

- Singapore Airlines

- Southwest Airlines

- Thai Airways International PCL

- United Continental Holdings

- WestJet Airlines

Top Players In The Market

- International Consolidated Airlines Group serves as a dominant force in the UK aviation sector through its subsidiary British Airways and other key brands. The company contributes significantly by connecting the UK to global destinations and supporting international trade and tourism. Recent actions include accelerating fleet renewal with fuel efficient aircraft to meet sustainability targets and enhance operational efficiency. IAG strengthens its market position by expanding premium service offerings and investing in digital customer experience platforms. The group focuses on optimizing route networks to maximize yield and connectivity from London hubs. By prioritizing cost discipline and strategic growth IAG maintains its leadership role while adapting to evolving consumer preferences and environmental regulations in the competitive UK aviation landscape.

- EasyJet plc is a leading low cost carrier that plays a vital role in making air travel accessible across the UK and Europe. The company operates an extensive network of short haul routes connecting regional airports with major leisure and business destinations. Recent actions involve enhancing digital capabilities through improved mobile apps and personalized booking experiences to drive direct sales. EasyJet strengthens its market position by committing to net zero carbon emissions and investing in sustainable aviation fuel initiatives. The airline focuses on operational resilience and customer service excellence to build brand loyalty. By maintaining a lean cost structure and expanding into new markets EasyJet continues to capture significant passenger volume and reinforce its status as a preferred choice for budget conscious travelers in the UK.

- Virgin Atlantic Airways Limited is a prominent long haul carrier known for its distinctive brand and premium service quality in the UK market. The company connects major UK cities with key international destinations in North America Asia and the Caribbean. Recent actions include modernizing its fleet with advanced Airbus aircraft to reduce environmental impact and improve passenger comfort. Virgin Atlantic strengthens its market position through strategic partnerships and joint ventures that expand global reach and connectivity. The airline emphasizes innovation in customer experience including enhanced inflight entertainment and dining options. By focusing on sustainability and brand differentiation Virgin Atlantic appeals to discerning travelers and maintains a strong competitive presence in the premium segment of the UK airlines market.

Top Strategies Used By Key Market Participants

Key players in the UK airlines market employ several strategic approaches to maintain competitiveness and drive growth. Fleet modernization is central with companies investing in fuel efficient aircraft to reduce costs and emissions. Digital transformation enhances customer experience through personalized services and seamless booking processes. Sustainability initiatives including sustainable aviation fuel adoption are prioritized to meet regulatory and consumer demands. Network optimization focuses on high yield routes and strategic partnerships to expand global reach. Cost management remains critical with airlines streamlining operations and improving labor productivity. These combined strategies enable key participants to navigate economic volatility and environmental challenges effectively.

MARKET SEGMENTATION

This research report on the UK airlines market is segmented and sub-segmented into the following categories.

By Transport

- Domestic

- International

By Application

- Passenger

- Freight

Frequently Asked Questions

What factors are shaping the growth trajectory of the UK airlines market?

Rising air passenger traffic, increasing international travel demand, and expansion of tourism and business travel are shaping market growth.

How is the UK airlines market segmented by service type?

The market is segmented into full-service carriers, low-cost carriers, charter airlines, and cargo airline services.

Which airline category commands the largest share of the UK airlines market?

Low-cost carriers command the largest share due to their competitive pricing and extensive domestic and international route networks.

What makes the UK one of the most significant aviation markets in Europe?

Its strong international connectivity, major airport infrastructure, and high volume of business and leisure travelers make it a significant aviation market.

Who are the primary customers within the UK airlines market?

Business travelers, leisure tourists, government travelers, cargo operators, and international passengers are the primary customers.

How are changing traveler preferences influencing airline operations in the UK?

Demand for affordable fares, seamless digital experiences, flexible booking options, and sustainable travel is influencing airline strategies.

What emerging trends are redefining the UK airlines industry?

Sustainable aviation initiatives, fleet modernization, digital passenger services, and growth in long-haul travel are redefining the industry.

What obstacles could limit expansion in the UK airlines market?

Fuel price volatility, regulatory requirements, airport capacity constraints, and economic uncertainties could limit market expansion.

How are airlines leveraging technology to improve competitiveness?

Airlines are adopting AI-driven customer service, predictive maintenance, biometric boarding systems, and advanced revenue management tools.

What long-term opportunities exist in the UK airlines market?

Growth in international tourism, sustainable aviation technologies, airport expansion projects, and increasing air travel demand are expected to create significant opportunities.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com