UK Apparel Market Size, Share, Trends & Growth Forecast Report By Type, Material, End User, Category, Distribution Channel, and Country – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$5.24 BnMarket Estimate, 2026

$5.40 BnMarket Forecast, 2034

$6.87 BnCAGR, 2026–2034

3.05%UK Apparel Market Report Summary

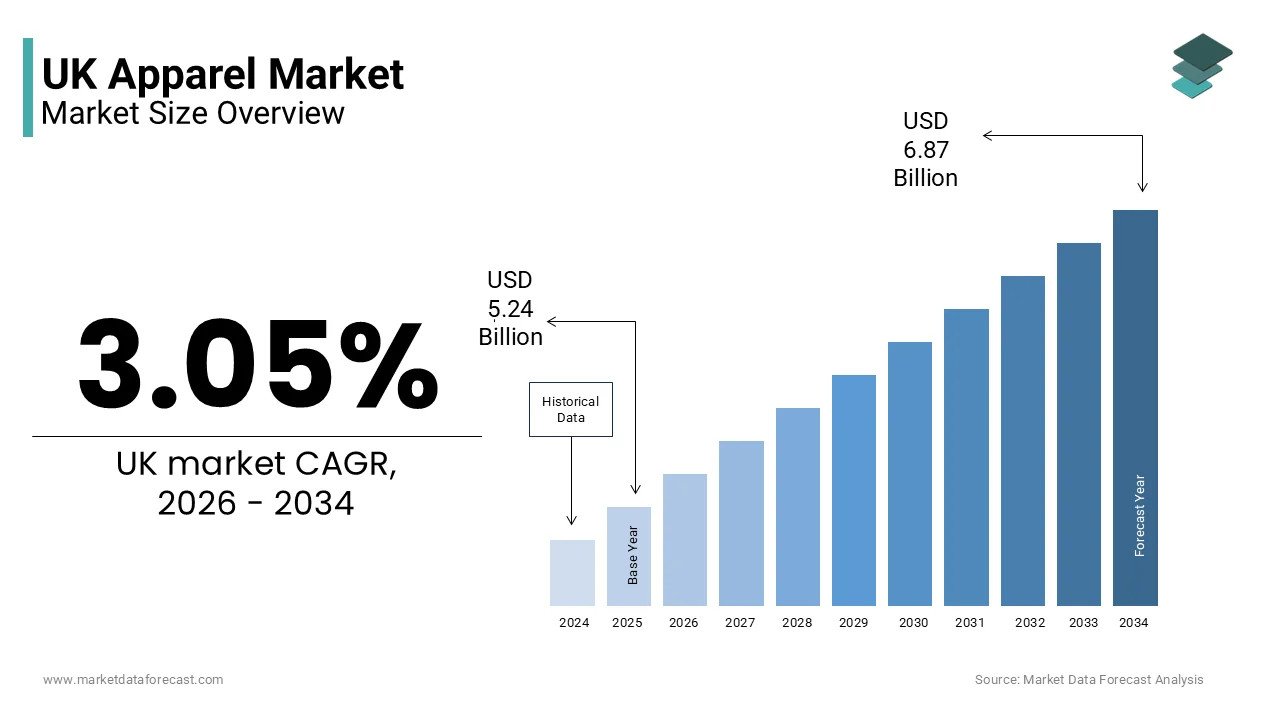

The UK apparel market was valued at USD 5.24 billion in 2025, is estimated to reach USD 5.40 billion in 2026, and is projected to reach USD 6.87 billion by 2034, growing at a CAGR of 3.05% during the forecast period. Market growth is driven by evolving fashion trends, increasing adoption of online shopping platforms, rising demand for sustainable clothing, and continuous innovation in apparel design and manufacturing. The market benefits from a strong retail ecosystem, growing consumer preference for convenience, and increasing awareness of environmentally responsible fashion choices.

Key Market Trends

- Growing demand for sustainable and ethically sourced fashion products is driving market growth.

- Increasing adoption of online shopping and digital retail channels is boosting market expansion.

- Rising consumer preference for comfortable and versatile clothing is supporting industry development.

- Expansion of fast fashion and direct to consumer business models is enhancing market opportunities.

- Innovation in sustainable materials, circular fashion, and personalized shopping experiences is influencing market advancement.

Segmental Insights

- Based on type, the casual wear and fashion wear segment accounted for the largest share of the UK apparel market in 2025. This dominance is attributed to changing lifestyle preferences, growing fashion consciousness, and strong demand for everyday clothing.

- Based on material, the cotton segment held the highest share of the UK apparel market in 2025, supported by its comfort, breathability, affordability, and widespread use across apparel categories.

- Based on distribution channel, the online e commerce segment accounted for the leading share of the UK apparel market in 2025, driven by convenience, extensive product selection, competitive pricing, and increasing digital adoption among consumers.

Regional Insights

- The United Kingdom maintained a significant position within the European apparel market in 2025 and is expected to experience continued transformation through sustainable fashion initiatives, changing consumer spending patterns, and increasing digital retail penetration.

Competitive Landscape

The UK apparel market is highly competitive, with companies focusing on fashion innovation, sustainability initiatives, omnichannel retail strategies, and customer experience enhancement to strengthen their market position. Market participants continue to invest in digital platforms, eco friendly materials, and supply chain optimization. Key companies operating in the UK apparel market include Primark, Marks & Spencer, Shein, Nike, Next plc, Adidas, George, Zara, F&F, TU, Matalan, H&M, Skechers, New Look, JD Sports Fashion plc, Louis Vuitton, and Burberry.

UK Apparel Market Size

The UK apparel market size was valued at USD 5.24 billion in 2025, and is projected to reach USD 6.87 billion by 2034 from USD 5.40 billion in 2026, growing at a CAGR of 3.05%.

According to the Office for National Statistics, the retail sales index indicates that clothing shop sales fell by 0.1% over the year, reflecting shifting spending priorities among households. The demographic profile of the UK shows a population of approximately 69.3 million people, with a significant proportion being digitally native consumers who prioritize convenience and personalization. The regulatory environment focuses on labor standards environmental sustainability and consumer protection influencing operational strategies for brands. Supply chain complexities have prompted many companies to reconsider sourcing strategies and inventory management practices. The rise of second hand and rental markets further diversifies the ecosystem offering alternatives to traditional ownership. This intricate network requires stakeholders to balance commercial objectives with social responsibility while adapting to technological advancements and changing cultural norms. The market serves as a barometer for broader economic health reflecting consumer confidence and disposable income levels through purchasing patterns and brand loyalty dynamics.

MARKET DRIVERS

Digital Commerce Integration and Omnichannel Retail Evolution

The seamless integration of digital commerce and the evolution of omnichannel retail strategies is propelling the growth of the UK apparel market. Consumers increasingly expect a unified shopping experience that blends online convenience with physical store interactions. According to the Office for National Statistics, online sales account for 28.3% of total retail expenditure, with clothing being one of the most purchased categories digitally. This shift is driven by the widespread adoption of smartphones and improved logistics networks that enable fast and reliable delivery. Retailers invest heavily in user friendly websites mobile apps and virtual try on technologies to enhance customer engagement and reduce return rates. Click and collect Services Bridge the gap between digital and physical channels allowing customers to order online and pick up in store which drives foot traffic and additional sales. Social commerce platforms facilitate direct purchasing through social media influencers and targeted advertisements creating impulse buying opportunities. The ability to access extensive product ranges and personalized recommendations online appeals to modern shoppers who value choice and efficiency. Data analytics enable retailers to understand consumer preferences and optimize inventory allocation reducing waste and improving satisfaction. This digital transformation expands market reach beyond geographic limitations allowing brands to connect with niche audiences and global customers. The convenience and accessibility of online shopping ensure sustained growth in this channel making it a critical component of overall market performance.

Growing Consumer Awareness of Sustainability and Ethical Practices

The rising consumer awareness of sustainability and ethical practices significantly drives demand for responsible apparel in the UK market, which is further boosting the UK market growth. Shoppers are becoming more conscious of the environmental and social impact of their purchases leading to a preference for brands that demonstrate transparency and accountability. According to surveys conducted by major consumer groups, a growing percentage of UK residents consider sustainability when choosing clothing brands preferring those that use organic materials fair labor practices and circular business models. This shift is reinforced by media coverage of climate change and labor rights issues which educate the public on the consequences of fast fashion. Brands respond by launching eco-friendly collections implementing recycling programs and obtaining certifications such as Global Organic Textile Standard or Fair Trade. The rise of second hand and vintage markets reflects this trend as consumers seek to extend the lifecycle of garments and reduce waste. Retailers highlight their sustainability efforts in marketing campaigns to build trust and loyalty among ethically minded buyers. Government initiatives promoting circular economy principles further encourage industry adoption of sustainable practices. This driver creates a competitive advantage for brands that authentically commit to environmental stewardship. As awareness deepens the demand for transparent supply chains and durable high quality products continues to grow reshaping the market landscape toward greater responsibility and long term value.

MARKET RESTRAINTS

Economic Volatility and Cost Of Living Pressures Restrain Spending

Economic volatility and persistent cost of living pressures are significant restraints on the UK apparel market by reducing disposable income and altering consumer spending habits. Households face increased expenses for energy housing and food leading to tighter budgets and prioritization of essential goods over discretionary items like clothing. According to the Office for National Statistics, inflation rates remained elevated above 4% for a prolonged period, impacting consumer confidence and reducing willingness to spend on non-essential purchases. Many consumers delay buying new clothes opting to repair existing items or purchase from cheaper alternatives. This trading down effect impacts mid-tier and premium brands disproportionately as buyers seek value without completely abstaining from consumption. Promotional discounts and clearance sales become necessary to drive volume but erode profit margins for retailers. The uncertainty surrounding economic conditions discourages large upfront expenditures on seasonal wardrobes or luxury items. Small independent retailers struggle to compete with larger chains that can leverage economies of scale to offer lower prices. This financial constraint creates a challenging environment for growth particularly for brands that rely on aspirational purchasing. As households adjust their spending habits the apparel market faces headwinds that require strategic adaptation to maintain relevance and affordability for cash strapped consumers.

Supply Chain Disruptions and Raw Material Instability

Persistent supply chain disruptions and instability in raw material availability present major restraints on the UK apparel market by causing delays and increasing costs. The global nature of textile manufacturing means that dependencies on international suppliers for fabrics trims and finished goods expose businesses to geopolitical tensions trade barriers and logistical bottlenecks. According to industry reports, lead times for apparel production have extended significantly due to port congestion and labor shortages in key manufacturing regions. Fluctuations in the price of cotton polyester and other raw materials create unpredictability in production expenses affecting pricing strategies and profitability. Retailers face difficulties in maintaining optimal inventory levels leading to stockouts of popular items or excess stock of slower moving products. The complexity of managing multi-tier supply chains makes it challenging to ensure compliance with ethical and environmental standards. Post Brexit regulatory changes add administrative burdens and customs delays for imports from Europe further complicating logistics. These operational challenges hinder agility and responsiveness to fast changing fashion trends. Manufacturers must invest in diversified sourcing strategies and risk management tools to mitigate these impacts. Until supply chain stability improves the market will continue to face constraints that limit growth potential and increase operational risks for all participants.

MARKET OPPORTUNITIES

Expansion of Circular Economy and Resale Platforms

The expansion of the circular economy and the rise of resale platforms present significant opportunities for UK apparel market growth. Consumers are increasingly embracing second hand clothing as a sustainable and cost effective alternative to new purchases. According to market analysis, the pre-owned fashion sector is growing rapidly with dedicated online platforms and in store take back schemes gaining popularity. Brands have the opportunity to integrate resale into their business models by launching official re-commerce channels that allow customers to sell back used items for store credit. This approach extends product lifecycles reduces waste and fosters customer loyalty through ongoing engagement. Partnerships with technology providers enable efficient sorting grading and listing of second hand items enhancing the user experience. The trend aligns with government initiatives promoting circularity and resource efficiency providing potential incentives for participating companies. Marketing campaigns highlighting the environmental benefits of buying pre owned appeal to eco conscious demographics. This opportunity allows brands to tap into a new revenue stream while addressing sustainability concerns. As stigma around second hand clothing diminishes the market for refurbished and vintage items expands. Companies that pioneer circular solutions can differentiate themselves and build strong brand equity in a competitive landscape.

Adoption of Advanced Technologies in Design and Production

The adoption of advanced technologies in design and production offers substantial opportunities for the UK apparel market expansion. Innovations such as 3D printing artificial intelligence and automated manufacturing enable faster prototyping reduced waste and personalized product offerings. For instance, digital design tools allow brands to visualize garments virtually before physical production minimizing sample costs and time to market. Artificial intelligence analyses consumer data to predict trends and optimize inventory planning reducing overproduction and markdowns. On demand manufacturing capabilities enable small batch production tailored to specific customer preferences enhancing exclusivity and satisfaction. Virtual fitting rooms and augmented reality applications improve the online shopping experience by helping customers make informed size and style choices thereby reducing return rates. These technologies support sustainability goals by minimizing material usage and energy consumption. Brands that leverage technical innovation can respond more agilely to market changes and consumer demands. The integration of smart textiles with connectivity features opens new possibilities for functional and interactive clothing. This technological evolution positions the UK market at the forefront of fashion innovation attracting investment and talent. Embracing digital transformation enhances competitiveness and operational resilience in a rapidly changing industry.

MARKET CHALLENGES

Intense Competition from Fast Fashion and Ultra Low Cost Retailers

Intense competition from fast fashion and ultra-low cost retailers is a major challenge to the UK apparel market by driving price wars and compressing margins. Established brands face pressure from agile competitors that rapidly replicate trends and offer extremely low prices appealing to budget conscious consumers. For instance, the market share of discount retailers has grown significantly forcing traditional players to reconsider their pricing and promotional strategies. This environment makes it difficult for mid-tier brands to justify higher price points without clear differentiation in quality or ethics. The rapid turnover of inventory required to keep up with fast fashion cycles increases operational complexity and waste. Smaller independent designers struggle to gain visibility against massive marketing budgets and extensive distribution networks of large chains. Consumer loyalty becomes fragmented as shoppers frequently switch brands based on price and novelty. The pressure to reduce costs can compromise labor standards and environmental practices creating reputational risks. Differentiation through unique design storytelling or superior customer service becomes essential but costly to maintain. This competitive landscape requires continuous innovation and strategic positioning to survive. Brands must balance affordability with integrity to retain relevance in a market dominated by speed and low cost.

Regulatory Compliance and Environmental Legislation Burdens

Strict regulatory compliance and evolving environmental legislation pose significant challenges to the UK apparel market by increasing operational costs and administrative burdens. Governments are introducing stricter rules on waste management chemical usage and carbon emissions requiring brands to adapt their processes and reporting methods. The introduction of extended producer responsibility schemes mandates that retailers take financial responsibility for the end of life disposal of their products. Compliance with these regulations requires investment in tracking systems recycling infrastructure and sustainable material sourcing. The complexity of navigating different regulatory frameworks across international supply chains adds further difficulty for global brands. Failure to comply can result in hefty fines legal action and damage to brand reputation. Small and medium sized enterprises often lack the resources to manage these compliance requirements effectively putting them at a disadvantage. The pace of regulatory change creates uncertainty making long term planning difficult. Companies must continuously monitor legislative developments and adjust strategies accordingly. This challenge demands robust governance structures and collaboration with industry bodies to ensure adherence. Balancing commercial viability with regulatory obligations remains a persistent hurdle for all market participants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.05% |

| Segments Covered | By Type, Material, End User, Category, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Market Leaders Profiled | Primark, Marks & Spencer, Shein, Nike, Next plc, Adidas, George, Zara, F&F, TU, Matalan, H&M, Skechers, New Look, JD Sports Fashion plc, Louis Vuitton, and Burberry |

SEGMENTAL ANALYSIS

By Type Insights

The casual wear and fashion wear segment accounted for the largest share of the UK apparel market in 2025. The dominance of casual wear and fashion wear segment in majorly driven by a fundamental shift in workplace norms and lifestyle preferences toward comfort and versatility. The widespread adoption of hybrid and remote working models has reduced the necessity for formal business attire prompting consumers to prioritize relaxed yet stylish clothing suitable for both home and informal social settings. According to the Office for National Statistics, employment data indicates that approximately 44% of the workforce continues to operate remotely or in hybrid arrangements, sustaining demand for comfortable every day wear. This trend is reinforced by the blurring of boundaries between leisure and professional life where smart casual outfits are increasingly accepted in various social and semi-professional contexts. Consumers seek garments that offer ease of movement without compromising on aesthetic appeal leading to higher sales of jeans t shirts knitwear and casual dresses. Retailers have responded by expanding their casual ranges and incorporating trendy elements that appeal to fashion conscious buyers. The influence of social media platforms showcases casual styling ideas encouraging frequent purchases to keep up with evolving trends. This segment benefits from its broad demographic appeal catering to all age groups and income levels. The versatility of casual wear allows for layering and mixing making it a practical choice for the unpredictable UK weather. As work culture continues to evolve the dominance of casual wear is expected to persist reflecting long term changes in consumer behavior and societal values.

On the other side, the sportswear and active wear segment is anticipated to record a CAGR of 7.2% during the forecast period in the UK market owing to the rising health consciousness and the pervasive athleisure trend. Consumers are increasingly prioritizing physical fitness and well-being leading to higher participation in sports gym activities and outdoor exercises. According to Sport England, survey data indicates that approximately 63% of adults in the UK engage in regular physical activity, creating sustained demand for performance oriented clothing. The athleisure trend has expanded the utility of sportswear beyond the gym allowing individuals to wear leggings joggers and technical tops for daily activities such as commuting shopping and socializing. This versatility appeals to busy lifestyles where comfort and functionality are paramount. Brands invest heavily in innovative fabrics that offer moisture wicking breathability and stretch enhancing the wearing experience. The integration of stylish designs with technical features makes active wear fashionable enough for casual wear. Marketing campaigns featuring fitness influencers and athletes reinforce the aspirational aspect of an active lifestyle. The normalization of wearing sportswear in non-athletic settings has broadened the customer base significantly. As health and wellness remain top priorities for consumers the demand for high quality versatile active wear continues to accelerate outpacing other apparel categories.

By Material Insights

The cotton segment dominated the market with the highest share of the UK market in 2025. The leading position of cotton segment in the UK market can be credited to its unparalleled comfort breathability and versatility across various clothing types. It is the preferred material for everyday garments such as t-shirts, shirts, underwear and casual dresses because it is soft against the skin and hypoallergenic. According to textile industry data, cotton accounts for approximately 30% of total fiber consumption in the UK, reflecting its enduring popularity among consumers. The natural properties of cotton make it suitable for all seasons providing warmth in winter and coolness in summer when woven appropriately. Its ease of care and durability ensure long lasting wear which appeals to budget conscious shoppers. Cotton is also highly adaptable allowing for various finishes and blends that enhance performance or aesthetic appeal. The widespread availability of cotton products at all price points from budget to luxury ensures broad market penetration. Consumer trust in cotton as a safe and natural material reinforces its dominance despite the rise of synthetic alternatives. The material’s biodegradability aligns with growing environmental concerns although water usage in production remains a challenge. Retailers prioritize cotton collections due to consistent demand and low return rates associated with fit and comfort issues. This foundational role in wardrobes ensures that cotton remains the most widely used and trusted material in the UK apparel sector.

On the other end, the synthetic materials segment is estimated to showcase a CAGR of 6.2% during the forecast period in the UK market owing to their superior performance features and durability. Fibers such as polyester nylon and elastane are essential for sportswear outerwear and swimwear due to their moisture wicking quick drying and stretch properties. According to textile reports, the demand for synthetic fabrics has surged as consumers seek functional clothing that withstands rigorous activity and harsh weather conditions. Synthetics offer greater resistance to wear and tear shrinking and fading compared to natural fibers making them ideal for long term use. The ability to engineer specific characteristics such as windproofing or thermal insulation allows manufacturers to create specialized garments for diverse environments. Advances in manufacturing have improved the texture and feel of synthetics making them more comfortable and less prone to static. The lightweight nature of synthetic fabrics appeals to travelers and outdoor enthusiasts who prioritize packability and ease of movement. Cost effectiveness also plays a role as synthetics are generally cheaper to produce than natural fibers allowing for competitive pricing. As active lifestyles become more common the reliance on high performance synthetic materials continues to expand driving rapid growth in this segment.

By Distribution Channel Insights

The online e-commerce segment led the market by accounting for the largest share of the UK apparel market in 2025. The growth of this segment in the UK market is attributed to the unmatched convenience and access to an extensive range of products. Consumers appreciate the ability to shop from anywhere at any time avoiding the constraints of store hours and location. According to the Office for National Statistics, online retail sales continue to grow with clothing being one of the most popular categories purchased digitally. The vast selection available online allows shoppers to compare styles prices and reviews across multiple brands instantly facilitating informed decision making. Advanced search filters and personalized recommendations enhance the browsing experience helping users find exactly what they need quickly. Home delivery services eliminate the hassle of carrying bags and navigating crowded stores. Flexible return policies mitigate the risk of buying clothes without trying them on building consumer confidence. Mobile apps enable seamless shopping on the go with secure payment options and saved preferences for faster checkout. The integration of social media shopping features allows direct purchasing from posts and ads capturing impulse buys. This digital ecosystem supports a broader reach for retailers including niche brands that may not have physical presence. The habit of online shopping has become entrenched particularly among younger demographics ensuring its continued dominance in the apparel market.

On the other side, the specialty stores and branded stores segment is the fastest growing segment in the UK apparel distribution channel and is likely to register a CAGR of 5.3% during the forecast period owing to the rising demand for experiential retail and strong brand loyalty. Consumers seek immersive shopping experiences where they can interact with products receive expert advice and engage with brand stories in person. For instance, flagship stores and concept shops are becoming destinations rather than just points of sale offering unique atmospheres and services. Branded stores allow companies to control the entire customer journey ensuring consistent messaging and high service standards. Knowledgeable staff provides personalized styling assistance and fitting support which enhances satisfaction and reduces returns. Exclusive in store launches and events create buzz and drive foot traffic from dedicated fans. The tactile experience of touching fabrics and trying on clothes remains crucial for many shoppers particularly for premium and luxury items. These stores often feature interactive displays and digital integrations that blend physical and online elements. The emotional connection formed through positive in store interactions fosters long term loyalty and advocacy. As consumers crave authentic connections and memorable experiences, specialty stores offer value that pure play online retailers cannot replicate driving their rapid growth.

COUNTRY LEVEL ANALYSIS

The UK held a promising share of the European apparel market in 2025 and is expected to witness highly responsive adjustments in consumer purchasing power and accelerated shifts toward sustainable fashion ecosystems over the next few years. As a mature market the UK is home to iconic global brands and influential fashion weeks that set trends worldwide. According to the British Fashion Council, the industry contributes £37 billion significantly to the national economy supporting hundreds of thousands of jobs and generating substantial export revenue. The market status is dynamic and resilient with a strong culture of individual expression and style diversity. Consumers in the UK are sophisticated and discerning demanding high quality sustainable and ethically produced clothing. The regulatory framework supports fair trade labor rights and environmental protection influencing industry practices. London serves as a creative capital attracting talent and investment from around the globe. The presence of major department stores independent boutiques and online retailers creates a competitive yet vibrant landscape. Digital adoption is high with UK shoppers among the most active online buyers in Europe. The market is also a leader in sustainable fashion initiatives with many brands pioneering circular models and eco-friendly materials. This combination of creativity commercial strength and ethical leadership ensures that the UK remains a pivotal player in the global apparel industry.

COMPETITIVE LANDSCAPE

The competition in the UK apparel market is intense and characterized by a diverse mix of traditional high street retailers fast fashion giants and digital native brands. Established players leverage their physical store networks and brand heritage to maintain customer loyalty while facing pressure from agile online competitors. Fast fashion retailers dominate through rapid trend replication and aggressive pricing strategies forcing others to innovate or reduce costs. Luxury and premium brands differentiate themselves through quality exclusivity and superior customer service. The rise of second hand and rental platforms adds another layer of competition by appealing to environmentally conscious consumers. Price sensitivity among shoppers due to economic pressures drives frequent promotions and discounts eroding margins. Retailers must balance affordability with sustainability to retain trust. Digital engagement and personalized experiences are critical differentiators as consumers expect seamless interactions across all touchpoints. The market rewards those who can adapt quickly to technological changes and shifting cultural values while maintaining operational efficiency and brand integrity in a saturated environment.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the UK apparel market are

- Primark

- Marks & Spencer

- Shein

- Nike

- Next plc

- Adidas

- George

- Zara

- F&F

- TU

- Matalan

- H&M

- Skechers

- New Look

- JD Sports Fashion plc

- Louis Vuitton

- Burberry

Top Players in the Market

- Next plc is a dominant force in the UK apparel market renowned for its extensive high street presence and robust online platform. The company contributes significantly by offering a wide range of clothing footwear and home products for men women and children. Recent actions include expanding its Total Platform service which allows other brands to utilize its logistics and digital infrastructure. Next strengthens its market position by investing heavily in data analytics to predict trends and optimize inventory levels. The company also focuses on sustainability initiatives such as reducing carbon emissions and promoting circular fashion. By balancing physical retail with digital innovation Next maintains strong customer loyalty and operational efficiency in a competitive landscape.

- Marks and Spencer Group plc is a historic retailer that plays a vital role in the UK apparel sector through its reputation for quality and trust. The company offers premium clothing lines alongside food products appealing to a broad demographic seeking reliability and style. Recent actions involve revitalizing its clothing ranges with modern designs and improved fit to attract younger customers. Marks and Spencer strengthens its position by enhancing its online user experience and integrating click and collect services seamlessly. The brand also commits to sustainable sourcing and ethical manufacturing practices to align with consumer values. By leveraging its strong brand heritage and adapting to modern retail demands Marks and Spencer continues to resonate with loyal shoppers.

- JD Sports Fashion plc is a leading specialist in sports fashion and lifestyle apparel within the UK market. The company contributes by curating exclusive collections from major global brands and developing its own private labels. Recent actions include strategic acquisitions of international retailers to expand its global footprint and product offerings. JD Sports strengthens its market position by focusing on youth culture and digital engagement through social media partnerships. The retailer invests in flagship stores that offer immersive brand experiences and limited edition releases. By maintaining strong relationships with key suppliers and understanding trend driven consumer behavior JD Sports remains a preferred destination for athletic and casual wear enthusiasts.

Top Strategies Used By Key Market Participants

Key players in the UK apparel market employ several strategic approaches to maintain competitiveness and drive growth. Digital transformation is central with companies investing in omnichannel capabilities to blend online and offline experiences. Sustainability initiatives are prioritized to meet consumer demand for ethical and eco friendly products. Supply chain optimization ensures agility and reduces lead times for faster response to trends. Data analytics are used extensively for personalized marketing and inventory management. Strategic partnerships with influencers and technology firms enhance brand visibility and innovation. These combined strategies enable key participants to adapt to changing consumer preferences and economic conditions effectively.

MARKET SEGMENTATION

This research report on the UK apparel market is segmented and sub-segmented into the following categories.

By Type

- Casual Wear/Fashion Wear

- Formal Wear

- Swimwear

- Outerwear

- Sportswear & Activewear

- Agricultural Work Clothing/Farm Apparel

- Work Wear

- Ethnic Wear

- Sleepwear

- Others

By Material

- Synthetic

- Cotton

- Wool

- Leather

- Denim

- Satin

- Others

By End User

- Men

- Women

- Children

- Unisex

By Category

- Mass/Economy

- Premium

- Luxury

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Stores/Branded Stores

- Department Stores

- Online/E Commerce

- Others

Frequently Asked Questions

1. What is the UK apparel market?

The UK apparel market includes the manufacturing, distribution, and retail sale of clothing products for men, women, and children across various categories.

2. What factors are driving the growth of the UK apparel market?

Growth is driven by evolving fashion trends, increasing online shopping, rising demand for sustainable clothing, and growing consumer spending on apparel.

3. Which apparel segments are prominent in the UK market?

Key segments include casual wear, formal wear, sportswear, activewear, outerwear, children's wear, and intimate apparel.

4. How is e commerce influencing the UK apparel market?

E commerce platforms provide consumers with greater product variety, convenience, personalized shopping experiences, and easy access to domestic and international brands.

5. What role does sustainability play in the UK apparel market?

Sustainability has become a major focus, with consumers increasingly seeking eco friendly materials, ethical sourcing practices, and recyclable apparel products.

6. How are changing fashion trends impacting the market?

Rapidly evolving fashion preferences and social media influence encourage frequent product launches and drive consumer demand for new styles.

7. Which distribution channels are important in the UK apparel market?

Major distribution channels include online stores, specialty stores, department stores, supermarkets, hypermarkets, and brand owned retail outlets.

8. How is technology transforming the UK apparel industry?

Technologies such as artificial intelligence, virtual fitting rooms, data analytics, and automated inventory management are improving operational efficiency and customer experiences.

9. What challenges does the UK apparel market face?

The market faces challenges such as supply chain disruptions, rising production costs, changing consumer preferences, and increasing regulatory requirements related to sustainability.

10. How does the athleisure trend affect the UK apparel market?

The growing popularity of athleisure has increased demand for comfortable, versatile, and performance oriented clothing suitable for both fitness and everyday use.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com