UK Building Materials Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Application, and Region – Industry Forecast From 2026 to 2034

Market Size, 2025

$13.40 BnMarket Estimate, 2026

$14.38 BnMarket Forecast, 2034

$25.26 BnCAGR, 2026–2034

7.30%UK Building Materials Market Report Summary

The UK building materials market was valued at USD 13.40 billion in 2025, is estimated to reach USD 14.38 billion in 2026, and is projected to reach USD 25.26 billion by 2034, growing at a CAGR of 7.30% from 2026 to 2034. Market growth is driven by increasing residential and commercial construction activities, rising infrastructure development projects, and growing investments in sustainable building solutions across the United Kingdom. Building materials such as aggregates, cement, concrete, bricks, and insulation products play a crucial role in supporting urban development and modernization projects. The expansion of affordable housing initiatives, renovation activities, and government infrastructure investments is further accelerating market growth.

Key Market Trends

- Rising investments in residential and infrastructure construction projects.

- Increasing demand for sustainable and energy-efficient building materials.

- Growing adoption of recycled and low-carbon construction materials.

- Expansion of smart building and green construction initiatives.

- Increasing focus on modernization and renovation of existing infrastructure.

Segmental Insights

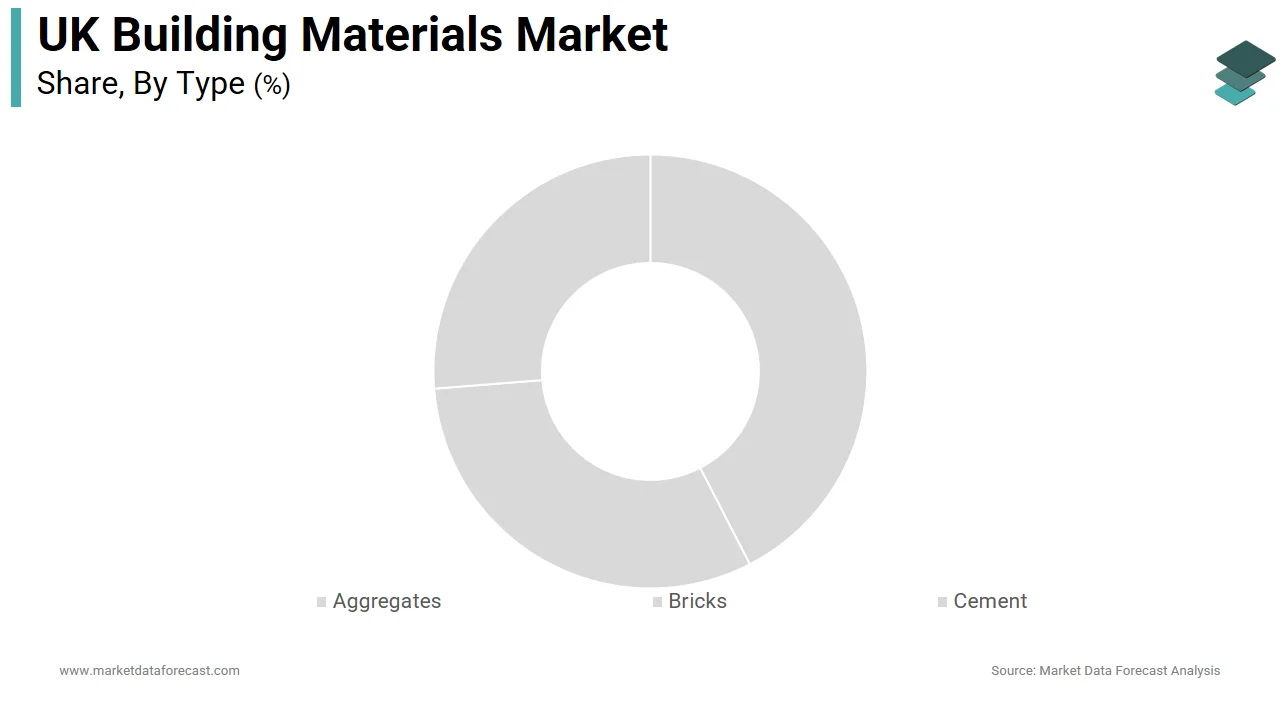

- Based on type, the aggregates segment dominated the UK building materials market in 2025 by accounting for 21.1% market share, driven by their essential role in concrete production, asphalt manufacturing, and road base construction activities.

- Based on application, the residential segment led the market by capturing 44.3% share in 2025, supported by rising housing demand, urban development projects, and increasing government focus on residential infrastructure expansion.

Regional Insights

- The United Kingdom is witnessing steady growth in the building materials market, supported by rising infrastructure investments, increasing urbanization, and expanding residential construction activities. Government initiatives promoting sustainable construction practices and energy-efficient buildings are further supporting the adoption of advanced and eco-friendly building materials across the country.

Competitive Landscape

The UK building materials market is characterized by strong competition among global construction material manufacturers and regional suppliers focusing on sustainability, production efficiency, and advanced construction solutions. Market participants are emphasizing expansion of low-carbon product portfolios, investment in recycling technologies, and strategic partnerships to strengthen market positioning. Infrastructure modernization projects and growing demand for environmentally responsible construction materials are shaping competitive dynamics across the market.

Prominent companies operating in the UK building materials market include CEMEX, LafargeHolcim, CRH plc, Saint-Gobain, Dyckerhoff AG, Buzzi Unicem, Heidelberg Materials UK, Aditya Birla Group, and Ambuja Cements.

UK Building Materials Market Size

The UK building materials market was valued at USD 13.40 billion in 2025, is estimated to reach USD 14.38 billion in 2026, and is projected to reach USD 25.26 billion by 2034, growing at a CAGR of 7.30% from 2026 to 2034.

The building materials are for residential, commercial, and infrastructure development. The Department for Levelling up Housing and Communities reported that 234,000 new homes were completed in England during the 2023 to 2024 financial year, falling short of the government target of 300,000 but indicating steady activity levels. Environmental regulations are increasingly shaping material specifications, with the Future Homes Standard mandating lower carbon emissions for new builds. These contextual statistics illustrate a market where demand is robust yet constrained by structural challenges such as labor shortages and planning complexities. The raw commodity trading includes innovative low-carbon alternatives and prefabricated components, which reflect a strategic pivot towards efficiency and environmental compliance in response to climate change imperatives and economic pressures.

MARKET DRIVERS

Government Infrastructure Investment and Public Sector Projects

The sustained government investment in large-scale infrastructure projects by creating consistent demand for heavy construction materials such as steel, concrete, and aggregates, which is attributed to boosting the growth of the United Kingdom materials market. The National Infrastructure Strategy outlines billions of pounds in funding for transport networks, energy systems, and public facilities, ensuring a steady pipeline of work for suppliers. Projects such as the High Speed 2 rail network and various highway improvements require vast quantities of structural steel and cement, directly boosting sales volumes for manufacturers. The renewal of public sector assets, including schools and hospitals, further stimulates demand for specialized materials such as fire-resistant cladding and high-performance insulation. Local authorities are also investing in social housing and community centers, supported by central government grants. This public sector spending provides a stable baseline of demand that helps mitigate volatility in the private residential sector. The long-term nature of these projects ensures multi-year contracts for material suppliers, allowing for better capacity planning and investment in production facilities.

Residential Housing Demand and Urban Regeneration Initiatives

The persistent demand for residential housing and ongoing urban regeneration initiatives are fuelling the growth of the United Kingdom building materials market. A chronic shortage of affordable housing continues to pressure developers to increase output, while urban renewal projects revitalize dormant industrial sites into mixed-use developments. As per the Ministry of Housing, Communities, and Local Government, the household population in England is projected to grow by 1.6 million between 2021 and 2031, necessitating substantial new construction to accommodate demographic changes. Urban regeneration schemes in cities, such as Manchester, Birmingham, and London, involve the demolition of obsolete structures and the construction of modern high-density residential complexes, requiring extensive amounts of bricks, glass, and steel. The conversion of office spaces to residential units, accelerated by post-pandemic working patterns, further stimulates demand for interior fit-out materials and retrofitting supplies. Developers are increasingly focused on brownfield sites to meet planning requirements, which often involves complex groundwork and foundation materials. The push for higher-density living in urban centers drives the use of advanced construction techniques and materials that maximize space efficiency and thermal performance. This sustained residential demand ensures a continuous flow of orders for material suppliers, particularly those offering products compliant with modern energy efficiency standards. The interplay between population growth and urban densification strategies creates a robust and enduring driver for the building materials sector.

MARKET RESTRAINTS

Volatility in Raw Material Costs and Energy Prices

The sharp volatility in raw material costs and energy prices, squeezing profit margins and disrupting project budgets, is also one of the restraining factors for the growth of the United Kingdom building materials market. The production of key materials such as cement, steel, and glass is energy-intensive, making manufacturers highly susceptible to fluctuations in natural gas and electricity prices. Global geopolitical tensions have exacerbated these issues by leading to unpredictable pricing for imported raw materials, such as iron ore and timber. Manufacturers struggle to pass these increased costs onto customers due to fixed price contracts and competitive pressure, resulting in reduced profitability and delayed investments in capacity expansion. Contractors face uncertainty when tendering for projects, often leading to conservative bidding or project cancellations. The instability in input costs makes long-term planning difficult for both suppliers and buyers, hindering market growth. Small and medium-sized enterprises are particularly vulnerable as they lack the financial resilience to absorb sudden price spikes. This economic pressure forces some players to reduce production volumes or seek cheaper alternatives, potentially compromising quality. Until energy markets stabilize and supply chains become more resilient, cost volatility will remain a significant constraint on the industry's ability to expand and innovate effectively.

Planning System Delays and Regulatory Bottlenecks

Inefficiencies within the planning system and regulatory hurdles, by delaying project commencement and creating uncertainty for suppliers, are additionally hampering the growth of the United Kingdom building materials market. The complexity and length of the planning approval process often result in prolonged lead times before construction can begin, causing mismatches between material production schedules and actual demand. As per the House of Commons Library, the average time for determining major planning applications in England exceeded 14 weeks in 2024, with many cases taking significantly longer due to administrative backlogs. These delays disrupt supply chains, forcing manufacturers to hold excess inventory or cancel production runs, which increases operational costs and waste. Uncertainty regarding planning outcomes discourages speculative development, reducing the overall volume of projects entering the pipeline. Changes in building regulations, such as updates to fire safety standards or energy efficiency requirements, often require manufacturers to rapidly adapt product formulations or certifications, adding compliance burdens. The lack of digitalization in local planning authorities further exacerbates processing times. Developers hesitate to commit to material orders until planning permission is secured, leading to fragmented demand patterns. This regulatory friction slows down the turnover of construction projects by limiting the frequency and volume of material purchases. Streamlining the planning process is essential to unlock latent demand and ensure a smoother flow of materials from production sites to construction zones.

MARKET OPPORTUNITIES

Adoption of Sustainable and Low-Carbon Materials

The increasing adoption of sustainable and low-carbon building materials by stringent environmental regulations and corporate sustainability goals, which is also one of the major opportunities for the growth of the United Kingdom building materials market. The construction sector is under pressure to reduce its embodied carbon footprint, prompting a shift towards materials such as cross-laminated timber, recycled steel, and low-carbon cement alternatives. As per the Green Building Council, the built environment accounts for 40% of the UK’s total carbon emissions, creating an urgent demand for greener construction solutions. Manufacturers investing in innovative products such as hempcrete, mycelium-based insulation, and carbon-capturing concrete can capture premium market segments and differentiate themselves from competitors. Government incentives such as the Future Homes Standard mandate higher energy efficiency and lower carbon intensity for new builds, encouraging developers to source certified sustainable materials. Retailers and distributors are expanding their eco-friendly product ranges to meet growing consumer and contractor demand. The circular economy model, which emphasizes recycling and reusing materials, offers opportunities for companies to develop closed-loop supply chains and reduce waste disposal costs. Collaborations between material producers and research institutions are accelerating the development of next-generation sustainable products.

Expansion of Modular and Prefabricated Construction Techniques

The expansion of modular and prefabricated construction techniques to improve efficiency and address labor shortages is also eventually to boost the growth of the United Kingdom building materials market. Off-site manufacturing allows for the precise production of building components in controlled factory environments by reducing waste and construction time. As per the Construction Leadership Council, modular construction can reduce project delivery times by up to 50% compared to traditional methods, making it an attractive option for housing and commercial developments. This shift requires specialized materials designed for modular assembly, such as lightweight steel frames, engineered wood panels, and integrated service modules. Material suppliers can collaborate with modular manufacturers to develop standardized components that optimize logistics and installation processes. The consistency of factory production ensures higher quality control and reduced material wastage, aligning with sustainability objectives. The government supports modern methods of construction through funding and policy initiatives aimed at increasing housing supply and productivity. As the industry embraces digitalization and building information modeling, the integration of materials into prefabricated systems becomes more seamless. Suppliers who adapt their product offerings to suit modular construction needs can secure long-term partnerships with leading developers. This technological evolution transforms the traditional supply chain by creating opportunities for innovation and value addition in the building materials sector.

MARKET CHALLENGES

Skilled Labor Shortages and Workforce Aging

Acute skilled labor shortages and an aging workforce are affecting both production and application sectors, which is one of the major challenges for the growth of the United Kingdom building materials market. The construction industry struggles to attract young talent, leading to a deficit in skilled workers, such as bricklayers, carpenters, and plant operators. This labor gap results in delays and increased costs, as companies compete for a limited pool of qualified workers. In the manufacturing segment, shortages of engineers and technicians hinder the maintenance and optimization of production facilities. The reliance on older workers nearing retirement exacerbates the issue, as knowledge transfer to younger generations is often insufficient. Training programs and apprenticeships are expanding, but take time to yield results. The labor shortage also affects the adoption of new technologies and materials, as skilled personnel are required to handle complex installations. Without a robust workforce strategy, the industry faces productivity constraints that limit its capacity to meet demand.

Supply Chain Disruptions and Logistics Constraints

The persistent supply chain disruptions and logistics constraints are impacting the timely delivery of essential products. The supply chain disruptions and logistics constraints are impeding the growth of the United Kingdom's building materials market. Dependence on imported materials such as timber, ceramics, and certain metals exposes the industry to global shipping delays and port congestion. As per the Chartered Institute of Procurement and Supply, lead times for key construction materials remained extended in 2024, with some items taking up to 20 weeks to arrive. Domestic logistics are also strained by driver shortages and fuel price volatility, increasing transportation costs and reducing reliability. Just-in-time delivery models, widely used in construction, are vulnerable to these disruptions, causing site stoppages and project delays. Manufacturers face challenges in securing raw materials and coordinating distribution networks amidst uncertain conditions. The lack of visibility in supply chains complicates inventory management and forecasting. Companies are forced to hold higher stock levels, tying up capital and increasing storage costs. Resilience-building measures such as diversifying suppliers and nearshoring production are costly and time-consuming. Until logistics networks stabilize and become more robust, supply chain vulnerabilities will continue to hinder operational efficiency and customer satisfaction in the building materials sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and the Humber, East Midlands. |

| Market Leaders Profiled | CEMEX, LafargeHolcim, CRH plc, Saint-Gobain, Dyckerhoff AG, Buzzi Unicem, Heidelberg Materials UK, Aditya Birla Group, Ambuja Cements, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The aggregates segment was the largest by accounting for 21.1% of the United Kingdom building materials market share in 2025, owing to its fundamental role as the primary constituent in concrete, asphalt, and road base construction. They are indispensable in road construction and maintenance, which constitutes a significant portion of public sector infrastructure spending. Roads require substantial quantities of crushed rock, sand, and gravel for subbase, base, and surfacing layers, ensuring durability and load-bearing capacity. As per the Department for Transport, the UK road network spans over 262,000 miles, requiring continuous maintenance and periodic resurfacing that consumes millions of tons of aggregates annually. The government’s commitment to improving transport connectivity through projects like the Road Investment Strategy ensures steady demand for high-quality aggregate materials. Local highways authorities rely on locally sourced aggregates to minimize transportation costs and carbon emissions, supporting regional quarries. The physical properties of aggregates, such as hardness and resistance to weathering, make them irreplaceable in creating stable and long-lasting road surfaces. Without a consistent supply of aggregates, critical infrastructure projects would face severe delays and cost overruns.

The cement segment is projected to expand at a CAGR of 4.5% throughout the forecast period, owing to the stringent environmental regulations mandating the reduction of embodied carbon in construction materials, prompting the development and adoption of low-carbon cement variants. Traditional Portland cement production is highly carbon-intensive, accounting for a significant portion of industrial emissions. As per the Committee on Climate Change, the construction sector must reduce its carbon footprint by 50% by 2030 to meet net zero targets, accelerating the shift towards green cement solutions. Manufacturers are investing in alternative binders such as ground granulated blast furnace slag and fly ash blended cements, which offer lower carbon footprints while maintaining structural integrity. Government procurement policies increasingly favor low-carbon materials, creating a premium market for sustainable cement products. The introduction of carbon taxes and emissions trading schemes further incentivizes producers to innovate and reduce clinker content in their mixes. This regulatory environment drives research and development into novel cement chemistries, such as geopolymer cements, which utilize industrial byproducts.

By Application Insights

The residential application segment was the largest by holding 44.3% of the United Kingdom building materials market share in 2025, with the chronic shortage of affordable housing in the UK, which prompts sustained government intervention and private sector development to meet population needs. The disparity between household formation rates and housing completion levels creates a structural deficit that requires continuous construction activity. The gap ensures a steady pipeline of residential projects, ranging from large-scale estate developments to individual self-build schemes. Government programs, such as Help to Buy and shared ownership schemes, stimulate demand by making homeownership more accessible, encouraging developers to launch new projects. The planning system prioritizes residential land use, allocating significant resources for housing zones. Material suppliers benefit from the consistent volume of orders generated by these projects, which require extensive inputs such as bricks, timber, insulation, and fixtures.

The commercial application segment is anticipated to witness the fastest CAGR of 5.2% throughout the forecast period, with the extensive urban regeneration projects and the modernization of office spaces to align with post-pandemic working patterns. Cities across the UK are transforming obsolete industrial and commercial zones into vibrant mixed-use districts, requiring significant material inputs. Companies are upgrading offices with advanced HVAC systems, smart lighting, and ergonomic layouts, driving demand for specialized construction materials. The shift towards hybrid work models has prompted businesses to create collaborative spaces that attract employees back to offices, stimulating fit-out activities. Green building certifications such as BREEAM and LEED encourage the use of sustainable materials in commercial projects, fostering innovation in product offerings. Local authorities support these transformations through planning incentives and infrastructure improvements, facilitating faster project delivery.

COMPETITIVE LANDSCAPE

The competition in the United Kingdom building materials market is intense and characterized by the presence of large multinational corporations alongside regional suppliers and specialized manufacturers. Major players compete on product quality, sustainability credentials, and supply chain reliability to secure contracts with large construction firms and government projects. Price competition is significant in commodity segments such as aggregates and standard cement, while differentiation is key in specialized products like high-performance insulation and smart glass. The market sees continuous innovation as companies strive to meet stringent environmental regulations and net-zero targets. Strategic partnerships and vertical integration are common strategies to control costs and ensure material availability. Local suppliers leverage proximity and customer service to compete with larger entities in specific regions. The rise of sustainable construction practices drives demand for eco-friendly materials, creating opportunities for niche players. Regulatory compliance and certification serve as barriers to entry, ensuring that only established and compliant firms thrive.

KEY MARKET PLAYERS

The major players in the UK building materials market include

- CEMEX

- LafargeHolcim

- CRH plc

- Saint Gobain

- Dyckerhoff AG

- Buzzi Unicem

- Heidelberg Materials UK

- Aditya Birla Group

- Ambuja Cements

TOP PLAYERS IN THE MARKET

- CRH plc is a leading global building materials company with a significant presence in the United Kingdom market through its extensive network of quarries and distribution centers. The company supplies aggregates, cement, and ready-mix concrete to infrastructure and residential projects across the nation. CRH recently strengthened its market position by investing in low-carbon production technologies and expanding its sustainable product portfolio. The organization has committed to reducing carbon emissions in its operations by aligning with the UK's net zero targets. CRH also focuses on digital transformation to enhance supply chain efficiency and customer service. Their strategic acquisitions and organic growth initiatives ensure they remain at the forefront of innovation in the UK building materials sector.

- Heidelberg Materials UK plays a crucial role in the United Kingdom building materials market as a major producer of cement, aggregates, and ready-mix concrete. The company operates numerous plants and quarries providing essential materials for infrastructure and housing developments. Heidelberg Materials recently strengthened its market position by launching new low-carbon cement products designed to meet stringent environmental regulations. The organization is investing heavily in carbon capture and storage technologies to reduce its industrial footprint. They have also enhanced their logistics network to improve delivery reliability and reduce transportation emissions.

- Saint-Gobain UK and Ireland is a prominent player in the United Kingdom building materials market, offering a wide range of solutions, including insulation glass and interior systems. The company serves residential, commercial, and industrial sectors with high-performance products that enhance energy efficiency and comfort. Saint-Gobain recently strengthened its market position by expanding its sustainable insulation offerings and promoting circular economy practices. The organization has invested in research and development to create innovative materials that reduce embodied carbon in buildings. They also provide technical support and training to contractors and architects, ensuring proper installation and performance.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United Kingdom building materials market primarily focus on sustainability and decarbonization to align with regulatory requirements and consumer demand. Companies invest heavily in developing low-carbon products such as green cement and recycled aggregates to reduce environmental impact. Digital transformation is another major strategy with firms adopting advanced logistics and supply chain management systems to improve efficiency and reliability. Strategic acquisitions and partnerships enable companies to expand their product portfolios and geographic reach. Innovation in manufacturing processes helps reduce energy consumption and waste generation. Customer-centric approaches, including technical support and tailored solutions, enhance brand loyalty. Diversification into renewable energy sources for production facilities reduces operational costs and carbon footprints. These strategies collectively drive competitiveness and resilience in a market characterized by strict environmental standards and evolving construction needs.

MARKET SEGMENTATION

This research report on the UK building materials market has been segmented and sub-segmented based on the following categories.

By Type

- Aggregates

- Bricks

- Cement

- Others

By Application

- Residential

- Commercial

- Industrial

Frequently Asked Questions

What is the UK building materials market?

The UK building materials market includes concrete, cement, steel, timber, bricks, insulation, and roofing materials used in construction, renovation, and home improvement projects across the United Kingdom.

Why is the UK building materials market growing?

The UK building materials market is growing due to infrastructure investments, housing demand, renovation activities, sustainability initiatives, and government support for construction and green building projects.

Who buys materials from the UK building materials market?

Construction companies, contractors, homeowners, builders, developers, and renovation specialists purchase from the UK building materials market for residential, commercial, and industrial building projects.

What products are included in the UK building materials market?

The UK building materials market includes concrete, cement, steel, timber, bricks, blocks, insulation, roofing, pipes, fittings, adhesives, and finishing materials for construction and renovation projects.

How does sustainability impact the UK building materials market?

Sustainability drives the UK building materials market through demand for low-carbon cement, recycled aggregates, energy-efficient insulation, eco-friendly products, and alignment with net-zero emissions targets.

What challenges face the UK building materials market?

Challenges in the UK building materials market include supply chain disruptions, material shortages, inflation pressures, high transportation costs, Brexit impacts, and labor shortages in the construction sector.

Which sectors drive the UK building materials market most?

Residential construction, commercial building, infrastructure projects, renovation and remodeling, and public sector construction drive demand in the UK building materials market across the country.

How does the housing market affect the UK building materials market?

The housing market significantly influences the UK building materials market through new home construction, first-time buyer demand, mortgage rates, and homeowner renovation and extension activities.

What role does green building play in the UK building materials market?

Green building is central to the UK building materials market, promoting sustainable materials, energy efficiency, carbon reduction, environmentally responsible construction, and compliance with building regulations.

Is the UK building materials market competitive?

Yes, the UK building materials market is highly competitive with major manufacturers, regional suppliers, importers, private label products, and price competition across construction material categories.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com