U.K. Carpet Market Size, Share, Trends & Growth Forecast Report By Product Type, By Material, By Price Range, and By Region (London, South East England, North West England, West Midlands, Scotland, Wales, Northern Ireland & Rest of the United Kingdom) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

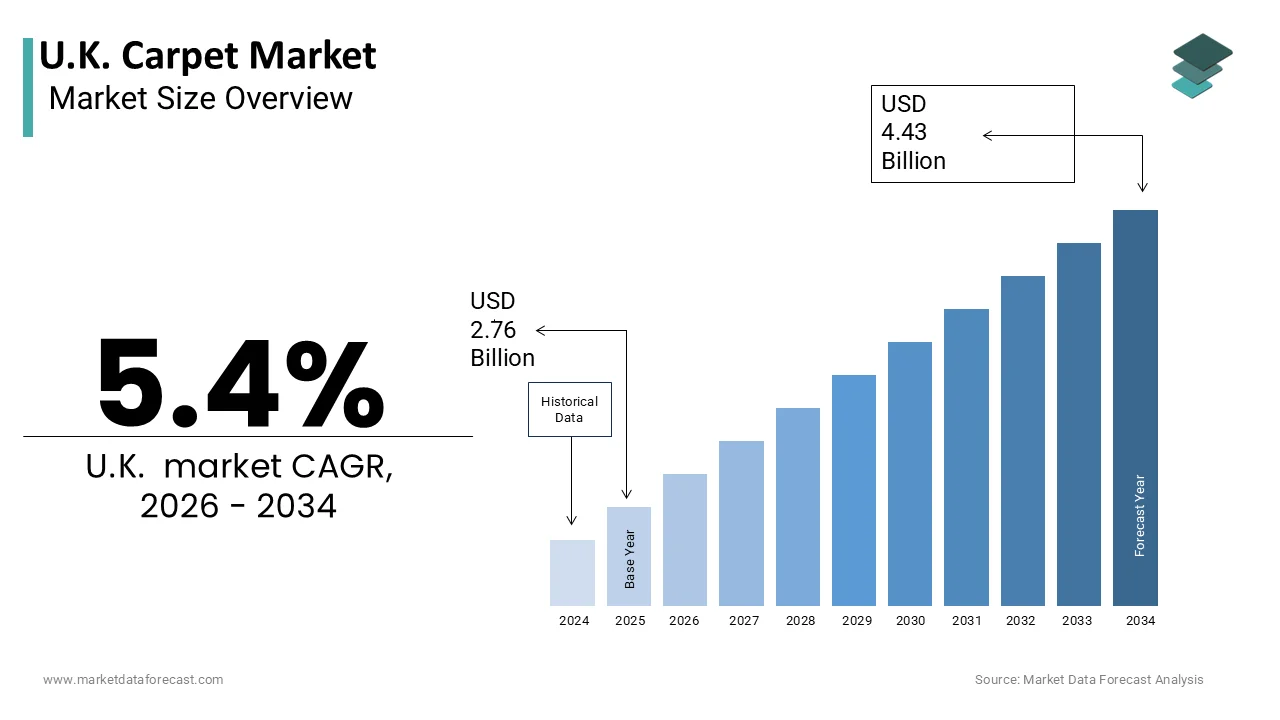

$2.76 BnMarket Estimate, 2026

$2.91 BnMarket Forecast, 2034

$4.43 BnCAGR, 2026–2034

5.4%U.K. Carpet Market Size

The U.K. Carpet Market is projected to grow from USD 2.76 billion in 2025 to USD 2.91 billion in 2026 and reach USD 4.43 billion by 2034, registering a CAGR of 5.4% during the forecast period from 2026 to 2034.

Carpets are textile floor coverings typically consisting of an upper layer of pile attached to a backing, manufactured from natural or synthetic fibers. This market is deeply embedded in the national housing infrastructure, with carpets remaining the dominant choice for bedrooms and living areas due to their thermal insulation and acoustic properties. According to the Office for National Statistics (ONS), there are approximately 30.4 million dwellings in the United Kingdom (with ~28.4 million in Great Britain), providing a massive installed base for flooring replacement and renovation activities. The UK housing stock is the oldest in Europe, with data from the English Housing Survey indicating that approximately 38% of homes were built before 1946, creating a consistent need for thermal retrofitting and renovation. This aging infrastructure necessitates regular maintenance and refurbishment, driving consistent demand for floor coverings. Recent data indicate a recovery in the sector; while spending on household goods dipped in 2024, furniture retail sales rebounded in 2025 with 4.3% growth, reflecting a renewed consumer prioritization of home comfort despite earlier economic pressures. Environmental considerations are increasingly influencing purchasing decisions, with consumers seeking sustainable materials. Research confirms that synthetic fibers like polypropylene and polyamide now dominate the mass market, accounting for the vast majority of sales volume, while wool remains the preferred choice for premium and luxury flooring sectors. Regulatory standards regarding fire safety and environmental impact, enforced by the British Standards Institution, shape product development and manufacturing processes. The market is supported by a robust distribution network comprising specialized retailers, DIY stores, and online platforms.

MARKET DRIVERS

Residential Renovation and Housing Transaction Volumes

The volume of residential property transactions and subsequent renovation activities is fuelling the growth of the United Kingdom carpet market. When homes change ownership, new occupants frequently replace existing floor coverings to suit their aesthetic preferences and hygiene standards. HM Revenue and Customs (HMRC) shows that approximately 1.1 million residential property transactions were completed in the UK in 2024, marking a return to baseline activity and serving as a key cyclical window for carpet and interior updates. Each transaction represents a potential opportunity for carpet replacement, particularly in rental properties and starter homes where wear and tear is more pronounced. Renovation trends also play a crucial role, as homeowners invest in improving their living spaces during periods of extended occupancy. Leading UK property and renovation surveys reveal that home improvements remain a massive household priority, with active renovators committing significant annual budgets toward property upgrades, among which floor coverings represent a foundational capital investment. The rise of remote work has further accelerated this trend, as individuals seek to create comfortable and professional home environments. A study notes that structural shifts toward hybrid working have structurally altered residential space utilization, with homeowners allocating higher budgets to interior finishes, including premium flooring and sound-dampening carpets, to establish dedicated home office environments. Additionally, the private rented sector accounts for approximately 20% of all UK households according to the English Housing Survey. Because rental properties experience more frequent tenant turnovers, landlords face shorter property maintenance intervals, causing more compressed carpet replacement cycles. Landlords often opt for durable and cost-effective carpet solutions to minimize void periods and attract tenants. This continuous cycle of property movement and improvement sustains a steady demand for carpet products across various segments.

Thermal Insulation and Energy Efficiency Requirements

The demand for thermal insulation and energy efficiency in homes significantly contributes to the expansion of the United Kingdom carpet market. This is particularly relevant in the context of rising energy costs. Carpets provide natural insulation, reducing heat loss through floors and contributing to lower energy consumption. Research confirms that carpets can provide up to 10 times higher thermal insulation than bare, uncarpeted hard floor coverings. By effectively preventing heat transfer, they serve as a practical element in passive residential energy efficiency. The Energy Saving Trust notes that uninsulated ground floors account for roughly 10% of standard household heat loss. Implementing optimized floor insulation solutions, including thermal underlays and heavy carpets, effectively reduces draughts and creates verifiable annual savings on domestic heating bills. With energy prices remaining volatile, consumers are increasingly prioritizing measures that enhance home warmth and reduce utility expenses. Official statistics from the Department for Energy Security and Net Zero (DESNZ) emphasize that domestic housing accounts for over a quarter of national energy consumption. This has accelerated state-supported efficiency initiatives to upgrade thermal boundaries across the aging UK housing stock. The Older Homes Act and other regulatory frameworks encourage retrofitting and insulation upgrades, indirectly boosting demand for insulating floor coverings. Wool carpets, in particular, are valued for their superior thermal properties and sustainability credentials. Furthermore, building regulations such as Part L of the Building Regulations emphasize the importance of thermal performance in new constructions and renovations. Architects and builders often specify carpets in residential projects to meet these standards. The combination of economic incentives and regulatory requirements ensures that carpets remain a preferred choice for energy-conscious consumers, driving market growth in both replacement and new build sectors.

MARKET RESTRAINTS

Competition from Hard Surface Floor Coverings

The increasing popularity of hard surface floor coverings, such as vinyl, laminate, and engineered wood, is limiting the growth of the United Kingdom carpet market. These alternatives are perceived as more durable, easier to clean, and modern in appearance, appealing to contemporary design trends. The UK Resilient Floorcovering Association (UKRFA) confirms that Luxury Vinyl Tiles (LVT) have experienced substantial, compounding market growth over the past several years, progressively capturing structural market share from traditional broadloom carpets due to design versatility. The ease of maintenance associated with hard floors is a key factor, particularly for households with pets and young children. The aesthetic versatility of hard surfaces, which can mimic natural stone or wood, also attracts design-conscious buyers. The rise of open-plan living spaces has further accelerated this shift, as homeowners seek seamless flooring solutions that extend across multiple rooms. Research suggests that the initial cost of installation for some hard surfaces has become competitive with high-quality carpets, reducing the price barrier. The perception of carpets as allergen traps, despite advancements in anti-allergenic technologies, also deters health-conscious consumers. Public health advisories from Allergy UK note that indoor air quality and dust-mite management significantly influence household flooring choices, encouraging the use of easily sanitizable, allergen-conscious surfaces alongside high-efficiency particulate air (HEPA) vacuuming routines. This structural shift in consumer preference towards hard flooring limits the growth potential of the carpet market, forcing manufacturers to innovate and highlight unique benefits such as comfort and acoustic insulation to retain relevance.

Economic Volatility and Disposable Income Constraints

Economic volatility and constraints on disposable income further hinder the expansion of the United Kingdom carpet market. This influences consumer spending behavior. During periods of economic uncertainty, households tend to defer non-essential purchases, including home improvements and decorative upgrades. Official indicators from the Office for National Statistics (ONS) show that UK real household disposable income experienced a recovery in 2024, rising by over 1% as easing inflation and wage growth began stabilizing baseline consumer confidence and discretionary spending capacity. Inflationary pressures on essential goods such as food and energy further reduce the budget available for discretionary items like carpets. The Bank of England confirms that tighter monetary policies and elevated base interest rates have directly increased debt-servicing costs for mortgage holders, reducing general disposable income and limiting overall financial flexibility for home renovations. This economic environment leads to a postponement of renovation projects, with consumers opting to repair existing carpets rather than replace them. The British Retail Consortium (BRC) shows that retail sales volumes for home furnishings contracted in real terms during periods of peak inflation, as budget-conscious consumers delayed non-essential big-ticket interior upgrades. The cost of raw materials, such as nylon and wool, has also increased due to global supply chain disruptions, leading to higher retail prices for carpets. According to Producer Price Index (PPI) datasets, elevated input costs for raw materials and industrial energy heavily pressured textile and flooring manufacturers, narrowing profit margins and driving subsequent wholesale price adjustments across consumer retail networks. The affordability crisis disproportionately affects lower-income households, who may switch to cheaper alternatives or delay purchases indefinitely. The uncertainty surrounding future economic conditions makes consumers cautious about committing to large expenditures. This financial pressure constrains demand for premium and mid-range carpet products, forcing manufacturers to compete on price and value, which can erode profit margins and limit investment in innovation.

MARKET OPPORTUNITIES

Development of Sustainable and Recycled Carpet Products

The development of sustainable and recycled carpet products offers a significant opportunity for the United Kingdom carpet market. This is in line with growing environmental consciousness among consumers. There is increasing demand for eco-friendly materials that reduce waste and carbon footprints. In compliance with the UK’s statutory target to reach net-zero emissions by 2050, members of the Carpet Foundation are actively investing in sustainable manufacturing innovations, emphasizing bio-based materials, localized supply chains, and low-carbon industrial processing. Recycled polyamide and polypropylene fibers are gaining traction as viable alternatives to virgin materials. Companies are investing in closed-loop recycling systems that allow old carpets to be processed into new fibers, reducing landfill waste. The European Union’s Circular Economy Action Plan influences UK standards, encouraging the adoption of circular business models. Consumers are willing to pay a premium for sustainable products, with a study showing that 73 percent of global consumers would change their consumption habits to reduce environmental impact. Wool carpets, being biodegradable and renewable, also offer a sustainable option that appeals to eco-conscious buyers. The British Wool Marketing Board promotes the environmental benefits of wool, highlighting its natural origin and durability. Government incentives for green building practices further support the adoption of sustainable floor coverings. Architects and specifiers are increasingly prioritizing environmentally certified products in commercial and residential projects. By leveraging these trends, manufacturers can differentiate their offerings and capture a growing segment of the market that values sustainability. This shift towards circular economy principles not only addresses environmental concerns but also creates new revenue streams and enhances brand reputation.

Expansion into Smart and Functional Carpet Technologies

The expansion into smart and functional carpet technologies is a key growth area for the United Kingdom carpet market. This integrates digital innovation with traditional floor coverings. Smart carpets equipped with sensors can monitor health metrics, detect falls, and track movement, particularly benefiting the elderly and healthcare sectors. Demographics compiled by Age UK show that there are more than 12 million people aged 65 and over in the UK, highlighting a massive, rapidly expanding market segment for assistive home technologies, mobility-adapted interior design, and supportive infrastructure. Smart flooring solutions can provide non-intrusive monitoring, enhancing safety and independence for older adults. Research tracked by The Health Foundation indicates that integrated, technology-enabled care frameworks and remote monitoring can materially alleviate pressure on acute services, driving institutional demand for smart innovations that intercept medical issues before they necessitate hospital admission. In commercial settings, smart carpets can analyze foot traffic patterns, optimizing space utilization and cleaning schedules. The Internet of Things enables these carpets to connect with building management systems, providing real-time data on usage and maintenance needs. Manufacturers are collaborating with technology firms to develop integrated solutions that combine aesthetics with functionality. Antimicrobial and air-purifying carpets are also gaining popularity, addressing health and hygiene concerns post-pandemic. These functional enhancements add value to carpet products, appealing to health-conscious consumers and commercial clients. The carpet market can embrace technological advancements. By doing so, it can expand beyond traditional applications and tap into new markets driven by health, safety, and efficiency requirements.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Volatility

Supply chain disruptions and raw material volatility are serious barriers for the United Kingdom carpet market. This affects production costs and availability. The industry relies heavily on imported raw materials such as nylon, polypropylene, and wool, making it vulnerable to global market fluctuations. Geopolitical tensions and trade restrictions further exacerbate these issues, leading to delays and increased logistics costs. The reliance on overseas suppliers for machinery and equipment also poses risks, as seen during the semiconductor shortage that affected automated production lines. Energy costs, a significant component of manufacturing expenses, have also surged, adding pressure to operational budgets. The unpredictability of supply chains makes it difficult for companies to plan long-term strategies and maintain stable pricing. Small and medium-sized enterprises are particularly affected, lacking the resources to absorb shocks or diversify suppliers. This instability threatens the competitiveness of UK manufacturers against international rivals with more resilient supply networks. Addressing these challenges requires strategic sourcing, investment in local capabilities, and greater collaboration across the supply chain to ensure continuity and cost control.

Labor Shortages and Skills Gap in Manufacturing

Labor shortages and a skills gap in the manufacturing sector are also a persistent challenge to the United Kingdom carpet market. The market faces difficulties in recruiting skilled workers for roles in machine operation, technical design, and quality control. National manufacturing labor surveys show that a critical majority of engineering and production firms report severe operational difficulties in recruiting staff with the necessary technical and digital competencies. An aging workforce exacerbates this issue, as experienced employees retire without adequate replacements. Data from the Office for National Statistics (ONS) confirms that the UK manufacturing sector has faced structurally elevated vacancy rates over the past several years, reflecting an intensely competitive domestic labor landscape. The perception of manufacturing as a declining industry discourages young people from pursuing careers in the sector, leading to a talent pipeline deficit. The Carpet Foundation emphasizes the strategic importance of specialized vocational pathways and technical apprenticeship programs to upskill the domestic workforce in advanced, automated flooring manufacturing technologies. Automation and digitalization require new competencies that are not widely available in the current labor pool. Research by the Federation of Small Businesses (FSB) indicates that small and medium-sized enterprises (SMEs) face compounding overheads when expanding internal workforce capabilities, driven by rising external training fees and the cost of pulling staff away from active production. The shortage of installers and fitters also impacts the downstream market, with delays in service delivery affecting customer satisfaction. This skills gap limits the industry’s ability to innovate and scale production efficiently. Addressing this challenge requires collaboration between industry bodies, educational institutions, and government agencies to promote vocational training and enhance the attractiveness of manufacturing careers. The UK carpet market lacks the skilled workforce it needs to thrive. Without this talent, it risks losing its competitive edge and its ability to meet evolving consumer demands.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Material, Price Range, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | London, South East England, North West England, West Midlands, Scotland, Wales, Northern Ireland |

| Market Leaders Profiled | Victoria PLC, Associated Weavers Europe NV, Balta Group, Forbo Holding AG, Tarkett S.A., Mohawk Industries, Inc., Cormar Carpets Ltd., Ulster Carpets Ltd., Brintons Carpets Limited, Axminster Carpets Ltd., Brockway Carpets Ltd., Westex Carpets Ltd. |

SEGMENTAL ANALYSIS

By Product Type Insights

The tufted carpets segment held the majority share of the United Kingdom market in 2025. Its cost efficiency and high manufacturing scalability allow for mass production at competitive price points, which drives the supremacy of this segment. The tufting process involves inserting yarn into a pre-woven backing using a needle, a method that is significantly faster and less labor-intensive than weaving or knotting. According to the Carpet Foundation, tufted carpets account for over 90 percent of all carpet production in the United Kingdom, reflecting their overwhelming prevalence in both residential and commercial sectors. This dominance is mainly driven by the ability of manufacturers to produce large volumes quickly, meeting the demands of large-scale housing developments and commercial projects. The lower production costs translate to affordable retail prices, making tufted carpets accessible to a broad consumer base. A study indicates that value for money is the leading determinant for the majority of residential flooring purchases, positioning affordable synthetic tufted carpets as a major volume driver. The versatility of tufting machines allows for a wide variety of pile heights, textures, and patterns, catering to diverse aesthetic preferences without compromising on speed. Research shows that the average lead time for tufted carpet orders is substantially shorter than for woven alternatives, enabling retailers to maintain leaner inventories and respond rapidly to market trends. This operational efficiency ensures that tufted carpets remain the default choice for builders, landlords, and budget-conscious homeowners, solidifying their position as the leading product type in the UK market.

The versatility of tufted carpets in terms of design and application also keeps this segment in the lead. Modern tufting technology enables the creation of complex patterns, multi-color designs, and varied textures that mimic more expensive woven or hand-knotted carpets. Market trends highlight that the high design versatility of modern tufted manufacturing, which allows for cost-effective color and loop configurations, has made personalized flooring aesthetics highly accessible to mid-market consumers. Manufacturers can easily adjust pile density and fiber types, such as polyamide or polypropylene, to suit different traffic levels and functional requirements. This adaptability makes tufted carpets suitable for a wide range of applications, from bedrooms and living rooms to hallways and commercial offices. The development of solution-dyed fibers has enhanced the color fastness and stain resistance of tufted carpets, addressing previous concerns about durability. As per sources, the introduction of textured tufted styles has blurred the lines between traditional carpet and modern rug aesthetics, attracting younger demographics. The ease of installation and replacement also contributes to their popularity, particularly in the rental sector, where frequent updates are common. This combination of aesthetic diversity and functional adaptability ensures that tufted carpets continue to dominate the UK market, satisfying both practical and decorative needs.

The woven carpets segment is estimated to register the fastest CAGR of 4.2% between 2026 and 2034. This rapid expansion of the segment is propelled by a resurgence of interest in heritage craftsmanship and premium quality. Unlike tufted carpets, woven carpets are constructed by interlacing warp and weft yarns, resulting in a durable and luxurious product that often retains its value over time. British Wool highlights that British-sourced fleece continues to secure a resilient foothold in premium woven carpets, driven by a growing luxury consumer segment that prioritizes sustainable sourcing and authentic, traceable raw materials. This growth is fueled by a consumer shift towards quality over quantity, with buyers willing to invest in long-lasting floor coverings that offer superior tactile experiences. Hospitality and luxury property landscape data indicate that premium woven carpets consistently outperform mass-market variants in high-end sectors, driven by sustained refurbishment budgets within boutique hotels, heritage assets, and luxury residential estates. The durability of woven structures means they can withstand heavy use while maintaining their appearance, reducing the need for frequent replacement. Advocacy from Heritage Crafts highlights that the preservation of traditional British textile production techniques has gained significant cultural importance, directly encouraging ethical consumers to support domestic manufacturers and local mills. This emotional and aesthetic connection to heritage drives the growth of the woven segment, distinguishing it from mass-produced alternatives and attracting a discerning customer base.

The preference for sustainability and natural fibers is boosting the growth of this segment. Woven carpets are frequently made from natural materials such as wool, sisal, and jute, which are biodegradable and have a lower environmental impact compared to synthetic alternatives. Consumers are increasingly aware of the carbon footprint associated with synthetic carpet production and disposal, leading them to choose woven options that align with their environmental values. Woven carpets do not require the latex backings often used in tufted carpets, which can emit volatile organic compounds. The longevity of woven carpets also supports sustainability goals, as they do not need to be replaced as often. This alignment with circular economy principles and environmental consciousness ensures that the woven segment continues to grow at a rapid pace, capturing a share of the market that prioritizes ethical and sustainable consumption.

By Material Insights

The synthetic fibers segment led the country’s market and captured a 63.5% share in 2025. This leading position of the segment was attributed to its affordability and exceptional durability, particularly in high-traffic areas. The Carpet Foundation confirms that synthetic fibers comprise the vast majority of UK residential carpet sales, heavily favored by consumers due to their superior stain resistance, durability, and cost-effectiveness compared to pure wool. Polyamide, in particular, is valued for its resilience and ability to recover from compression, making it ideal for stairs and hallways. The British Retail Consortium (BRC) highlights that price sensitivity remains a critical driver in household spending, positioning entry-level synthetic carpets as a highly practical, budget-friendly option for cost-conscious consumers. The advanced engineering of synthetic fibers has improved their stain resistance and ease of cleaning, addressing common maintenance concerns. This practical benefit appeals to families with children and pets, who constitute a significant portion of the market. The consistency of synthetic material quality ensures predictable performance, giving consumers confidence in their purchase. Manufacturers continuously innovate to enhance the softness and appearance of synthetic fibers, mimicking the look of natural wool at a fraction of the cost. This combination of economic accessibility and functional robustness ensures that synthetic fibers remain the dominant material choice in the UK carpet market.

Technological advancements in fiber performance have helped this segment hold onto its top spot. Innovations such as solution dyeing, where color is added to the polymer before extrusion, have significantly improved the color fastness and fade resistance of synthetic carpets. The longevity enhances the value proposition for consumers, reducing the frequency of replacement. The development of recycled synthetic fibers, such as Econyl, has also expanded the appeal of synthetic carpets to environmentally conscious buyers. These advancements allow synthetic carpets to meet higher environmental standards while maintaining their performance benefits. The ability to engineer fibers with specific properties, such as anti-static or anti-microbial treatments, adds functional value that natural fibers may lack. Also, the continuous improvement in texture and feel has reduced the perception gap between synthetic and natural fibers. These technological enhancements ensure that synthetic fibers remain competitive and relevant, driving their continued leadership in the market.

The plant-made yarns segment is anticipated to witness the fastest CAGR of 5.8% during the forecast period due to the rising demand for biodegradable and eco-friendly flooring solutions that minimize environmental impact. Research from WRAP acknowledges a growing consumer interest in alternatives to fossil-fuel-based synthetics, while emphasizing that developing true, closed-loop circular life cycles for plant-based textiles requires eliminating hazardous chemical binders and topically applied treatments. The natural aesthetic of plant yarns aligns with popular interior design trends such as biophilic design, which emphasizes connections to nature. Trade insights from the Interior Design Society (IDS) highlight that residential designers are increasingly incorporating natural fiber rugs and carpets into their portfolios, capitalizing on consumer demand for biophilic designs that offer warm, organic textures. Plant-made yarns are also hypoallergenic and do not emit volatile organic compounds, appealing to health-conscious households. The renewable nature of crops like jute and sisal supports sustainable agriculture practices, further enhancing their appeal. Government initiatives promoting green building materials also contribute to this growth. The British Green Building Council encourages the use of renewable resources in construction and renovation, boosting demand for plant-based floor coverings. This convergence of environmental, health, and aesthetic factors ensures that plant-made yarns continue to expand rapidly in the UK market.

The expansion of plant-made yarns in the commercial and hospitality sectors is also a significant driver of their rapid growth. Hotels, restaurants, and offices are increasingly incorporating natural fiber carpets to enhance their brand image and demonstrate a commitment to sustainability. The durability and unique texture of sisal and jute make them suitable for low to medium-traffic commercial areas, adding visual interest and warmth. Plant-made yarns offer a distinct aesthetic that differentiates spaces from those using standard synthetic carpets. The ability to blend plant fibers with wool or synthetic blends enhances their functionality while retaining their natural appeal. Also, the positive reception from guests and employees regarding natural materials reinforces this trend. This broader adoption beyond residential use expands the market potential for plant-made yarns, driving their status as the fastest-growing material segment in the UK carpet industry.

By Price Range Insights

The medium price range segment dominated the United Kingdom carpet market and accounted for a 60.4% share in 2025. This dominance of the segment was driven by its ability to offer a balance of quality and affordability for middle-income households. This segment typically includes carpets priced between 15 and 30 GBP per square meter, providing decent durability and aesthetic appeal without the high cost of premium options. Medium-range carpets often utilize blended fibers or higher-quality synthetics that mimic the look of natural materials, satisfying aesthetic desires within budget constraints. The availability of this segment in major DIY stores and online platforms ensures widespread accessibility. Manufacturers focus on optimizing production costs to maintain margins while offering attractive features such as stain resistance and warranty coverage. This strategic positioning ensures that the medium price range remains the most popular choice for mainstream renovations and new builds, sustaining its leading position in the market.

The wide availability and strength of the distribution network for medium-priced range carpets further reinforce its market dominance. Major retailers such as B&Q, Homebase, and Carpetright extensively stock medium-range products, ensuring that consumers can easily access and purchase these items. The extensive supply chain infrastructure supports efficient logistics and inventory management, reducing lead times and ensuring consistent stock levels. Online platforms have expanded the reach of medium-range carpets, enabling consumers to compare options and read reviews before purchasing. The presence of established brands in this segment builds consumer trust and loyalty, encouraging repeat purchases. Retailers often promote medium-range carpets through seasonal sales and bundle offers, further stimulating demand. This robust distribution ecosystem ensures that medium price range carpets remain readily available and visible to consumers, maintaining their status as the leading segment in the UK market.

The premium price range segment is likely to experience the fastest CAGR of 6.5% from 2026 to 2034, owing to luxury home improvement trends and high-end real estate developments. Affluent consumers are increasingly investing in high-quality floor coverings such as hand-knotted wool, silk blends, and custom-designed carpets to enhance the value and aesthetics of their properties. Premium carpets are viewed as integral elements of luxury design, offering unique textures, colors, and craftsmanship that mass-produced options cannot match. The rise of remote work has also led to increased spending on home offices and living spaces, with professionals seeking comfortable and sophisticated environments. Interior designers play a key role in specifying these products, influencing consumer choices towards higher-end options. This focus on exclusivity and quality ensures that the premium segment continues to grow rapidly, capturing a larger share of the market value.

Customization and bespoke design services are key factors accelerating the growth of the premium carpet segment. High-end consumers seek personalized solutions that align with their specific interior design visions, driving demand for made-to-order carpets. Manufacturers and retailers are responding by offering comprehensive design consultations and digital visualization tools that allow customers to preview their custom carpets. The ability to select specific fibers, colors, and pile heights enables consumers to create one-of-a-kind pieces that serve as focal points in their homes. Premium brands also offer white-glove delivery and installation services, adding value to the purchase. The integration of traditional craftsmanship with modern design techniques appeals to discerning buyers who appreciate artistry. This emphasis on personalization and service excellence distinguishes the premium segment from lower-priced alternatives, driving its rapid growth and establishing it as a dynamic and lucrative part of the UK carpet market.

COUNTRY LEVEL ANALYSIS

United Kingdom Carpet Market Analysis

The United Kingdom held a significant position in the European carpet market and occupied a 22.5% share in 2025. This position of the country’s market was propelled by a combination of housing transaction volumes, energy efficiency requirements, and evolving consumer preferences. It has a mature and established infrastructure, with a strong cultural affinity for soft flooring in residential settings. According to official housing stock statistics from the Office for National Statistics (ONS), Great Britain comprises approximately 28.4 million dwellings, scaling up to nearly 30 million across the entirety of the United Kingdom, providing a massive installed base for flooring replacement and residential renovation activities. HM Revenue and Customs (HMRC) shows that approximately 1 million residential property transactions occurred across the UK in 2024, with each transaction representing a prime chronological window for complete carpet replacement and interior refurbishment. The UK possesses notably old housing stock; data from the English Housing Survey highlights that over one-third (approximately 36%) of English homes were constructed before 1946. This legacy infrastructure requires consistent maintenance, thermal retrofitting, and floor renewals, sustaining high market demand. The Carpet Foundation confirms that wall-to-wall carpets remain the preferred and most practical flooring choice for UK bedrooms due to their critical thermal retention and sound-dampening benefits, though they increasingly compete with engineered hard flooring in primary living spaces. Regulatory frameworks such as Building Regulations Part L encourage insulation improvements, indirectly supporting carpet sales. The market is also influenced by economic conditions, with disposable income levels affecting spending on home improvements. Despite competition from hard surfaces, the comfort and warmth associated with carpets ensure their continued relevance. The industry is adapting to sustainability trends, with increasing adoption of recycled and natural fibers. This dynamic environment, shaped by regulatory, economic, and social factors, ensures that the UK remains a robust and evolving market for carpet products.

COMPETITIVE LANDSCAPE

The competition in the UK carpet market is intense and characterized by a mix of global manufacturers and local specialists. Price competition remains fierce in the economy segment, while differentiation through quality and sustainability drives the premium sector. Established brands leverage their reputation and distribution networks to maintain customer loyalty. New entrants focus on niche markets such as eco-friendly or smart carpets to gain traction. The rise of hard surface alternatives pressures carpet manufacturers to innovate and highlight unique benefits like comfort and insulation. Online retail platforms have increased transparency, allowing consumers to compare prices and features easily. This dynamic environment forces companies to continuously improve product offerings and service levels. Collaboration with interior designers and architects is crucial for securing high-value projects. Regulatory compliance regarding environmental standards adds complexity but also creates opportunities for responsible brands. The market is shifting towards value-added services such as installation and maintenance packages. Companies that adapt to changing consumer preferences and technological advancements are best positioned to succeed.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.K. Carpet Market include

- Victoria PLC

- Associated Weavers Europe NV

- Balta Group

- Forbo Holding AG

- Tarkett S.A.

- Mohawk Industries, Inc.

- Cormar Carpets Ltd.

- Ulster Carpets Ltd.

- Brintons Carpets Limited

- Axminster Carpets Ltd.

- Brockway Carpets Ltd.

- Westex Carpets Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Interface Inc is a global commercial flooring leader with a significant presence in the United Kingdom. The company is renowned for its modular carpet tile solutions and strong commitment to sustainability. Interface has strengthened its market position by advancing its Climate Take Back mission, which aims to reverse global warming. Recently,y the company launched carbon-negative carpet tiles using recycled and biobased materials. This innovation appeals to environmentally conscious commercial clients seeking to meet green building standards. Interface collaborates with UK architects and designers to create custom flooring solutions that enhance workplace aesthetics. The company also invests in circular economy initiatives,s uch as take-back schemes for old carpets. These efforts reinforce its reputation as a sustainable and innovative partner in the UK commercial sector.

- Tarkett Group is a major international player in the UK flooring market, offering a diverse range of carpet and soft flooring products. The company focuses on creating safe and healthy indoor environments through its Cradle to Cradle certified products. Tarkett has recently expanded its recycling capabilities in Europe to support closed-loop manufacturing processes. This strategy reduces waste and lowers the environmental impact of its carpet collections. The group actively partners with UK housing developers and commercial contractors to supply durable and stylish flooring solutions. Tarkett emphasizes digital tools for visualizing flooring options, which enhances customer experience and decision-making. Its commitment to health and sustainability drives its growth in both residential and commercial segments across the United Kingdom.

- Shaw Industries Group Inc is a prominent supplier of carpet products in the United Kingdom,m serving both residential and commercial sectors. As a subsidiary of Berkshire Hatha, ay the company leverages extensive resources to drive innovation and quality. Shaw has strengthened its position by introducing advanced stain-resistant technologies and eco-friendly fiber options. The company recently expanded its distribution network in the UK to improve availability and service speed. Shaw collaborates with local retailers and contractors to offer tailored flooring solutions that meet specific client needs. Its focus on durability and aesthetic versatility attracts a broad customer base. Shaw also invests in sustainable manufacturing practices, reducing water and energy consumption in production. These initiatives enhance its competitive edge and brand loyalty in the UK market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the UK carpet market employ several major strategies to maintain competitiveness. Sustainability is a primary focus,s with companies investing in recycled materials and circular economy models. Product innovation through advanced fiber technologies enhances durability and stain resistance. Digital transformation enables better customer engagement via online visualization tools and e-commerce platforms. Strategic partnerships with architects and developers secure large-scale commercial contracts. Companies also focus on customization to meet the unique design requirements of high-end clients. Cost optimization through efficient supply chain management ensures competitive pricing. Brand differentiation through heritage and craftsmanship appeals to premium segments. These strategies collectively drive growth and resilience in the evolving market landscape.

UNITED KINGDOM CARPET MARKET NEWS

- In March 2025, Interface Inc launched a new range of carbon-negative carpet tiles in the UK to enhance its sustainability leadership and strengthen its UK carpet market presence.

- In June 2025, Tarkett Group expanded its recycling facility in Europe to support closed-loop manufacturing and strengthen its UK carpet market presence.

- In September 2025, Shaw Industries introduced advanced stain-resistant technology in its UK product line to improve durability and strengthen its UK carpet market presence.

- In January 2026, Brintons Carpets partnered with a leading UK hotel chain to supply bespoke woven carpets and strengthen the UK carpet market presence.

- In February 2026, Victoria PLC acquired a regional distributor to expand its logistics network and strengthen its UK carpet market presence.

MARKET SEGMENTATION

This research report on the U.K. carpet market is segmented and sub-segmented into the following categories.

By Product Type

- Tufted Carpets

- Woven Carpets

- Needle-Punched Carpets

- Knotted Carpets

- Others

By Material

- Synthetic Fibers

- Wool

- Plant-Made Yarns

- Blended Fibers

- Others

By Price Range

- Economy/Low Price Range

- Medium Price Range

- Premium Price Range

By Country

- United Kingdom

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com