UK Chocolate Market Size, Share, Trends & Growth Forecast Report By Product Type, Form Price Range, Ingredient Type, Category, Distribution Channel, and Country – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

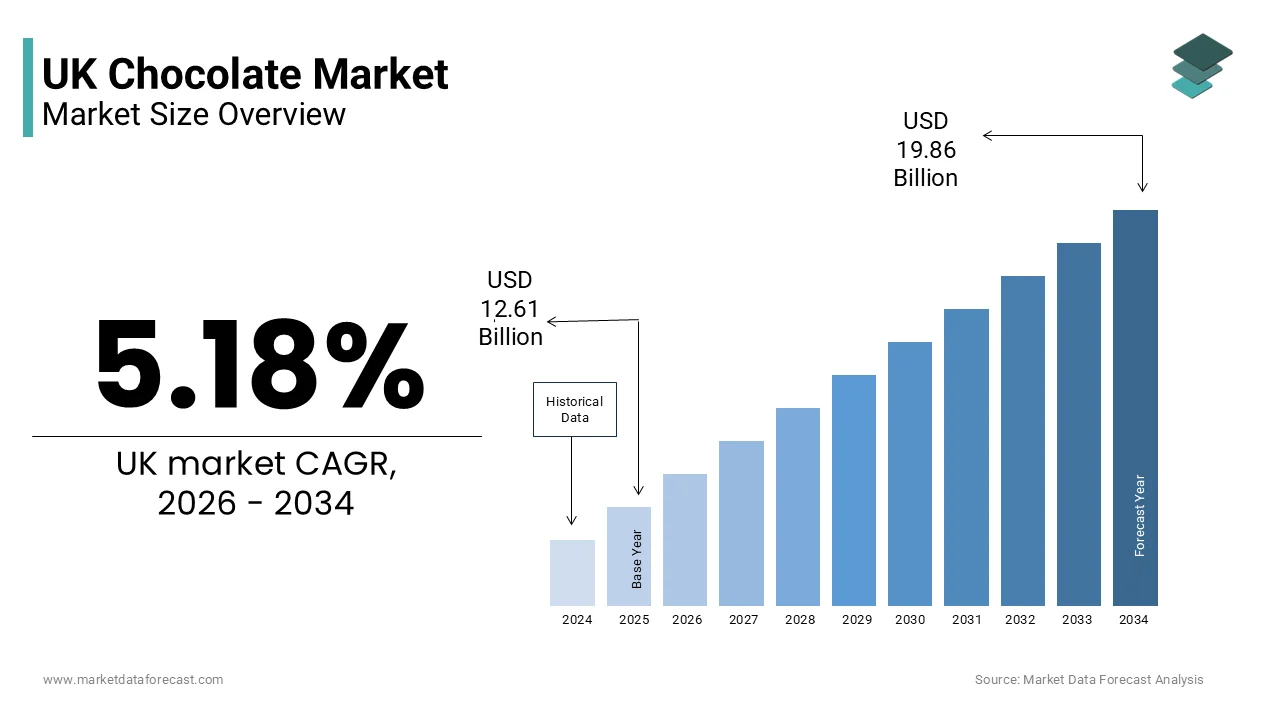

$12.61 BnMarket Estimate, 2026

$13.26 BnMarket Forecast, 2034

$19.86 BnCAGR, 2026–2034

5.18%UK Chocolate Market Report Summary

The UK chocolate market was valued at USD 12.61 billion in 2025, is estimated to reach USD 13.26 billion in 2026, and is projected to reach USD 19.86 billion by 2034, growing at a CAGR of 5.18% during the forecast period. Market growth is driven by strong consumer demand for confectionery products, increasing interest in premium and artisanal chocolates, and continuous product innovation. The market benefits from the United Kingdom's long standing chocolate consumption culture, expanding gifting trends, and rising demand for ethically sourced and sustainable chocolate products. Growing investments in premiumization and healthier chocolate alternatives are further supporting market expansion.

Key Market Trends

- Growing consumer demand for premium and artisanal chocolate products is driving market growth.

- Increasing interest in sustainable, ethically sourced, and organic chocolate is boosting market expansion.

- Rising popularity of gifting and seasonal chocolate purchases is supporting industry development.

- Expansion of innovative flavors, textures, and premium product offerings is enhancing market opportunities.

- Growing demand for reduced sugar and functional chocolate products is influencing market advancement.

Segmental Insights

- Based on product type, the milk chocolate segment accounted for 48.7% of the UK chocolate market share in 2025. This dominance is attributed to strong consumer preference, broad product availability, and widespread appeal across all age groups.

- Based on form, the tablets and bars segment held 65.4% of the UK chocolate market share in 2025, supported by convenience, affordability, and high consumption frequency.

- Based on ingredient type, the dairy based chocolate segment accounted for a substantial share of the UK market in 2025, driven by established consumer preferences and traditional chocolate formulations.

- Based on distribution channel, the supermarkets and hypermarkets segment held a significant share of the UK chocolate market in 2025, benefiting from extensive product assortments, promotional activities, and strong retail penetration.

Regional Insights

- The United Kingdom accounted for 25.3% of the European chocolate market share in 2025 and remains one of the most important chocolate consuming markets in the region. Strong retail infrastructure, high per capita chocolate consumption, and continued product innovation support market growth.

Competitive Landscape

The UK chocolate market is highly competitive, with manufacturers focusing on premiumization, sustainable sourcing, product innovation, and brand differentiation to strengthen their market position. Companies continue to invest in new product launches, ethical cocoa sourcing programs, and premium chocolate offerings.

Key companies operating in the UK chocolate market include Mars, Incorporated, Ferrero International SpA, Nestlé S.A., Chocoladefabriken Lindt & Sprüngli AG, Mondelēz International Inc., The Hershey Company, Barry Callebaut AG, The London Chocolate Company, Yıldız Holding A.Ş., Lotte Corporation, Arcor S.A.I.C., Whitakers Chocolates Ltd, Artisan du Chocolat Ltd, Morinaga & Co., Ltd., Tony's Chocolonely UK Ltd, Divine Chocolate Ltd, Pecan Deluxe Candy Company, Land Chocolate Ltd, Fazer Group, and Green & Black's Organic.

UK Chocolate Market Size

The UK chocolate market size was valued at USD 12.61 billion in 2025, and is projected to reach USD 19.86 billion by 2034 from USD 13.26 billion in 2026, growing at a CAGR of 5.18%.

Chocolate is defined as a food product made from roasted and ground cacao seeds, available in various forms including bars, boxes, and baking ingredients. The UK is renowned for its love of milk chocolate, which dominates consumer preferences due to its creamy texture and sweet profile. Moreover, the Office for National Statistics shows that while food accounts for roughly 11-12% of total household spending, chocolate is the dominant sub-category within confectionery, representing the majority of the "sugar, jam, syrups, chocolate, and confectionery" expenditure group. Research confirms that chocolate accounts for approximately 70% of UK confectionery sales by value, a figure consistent with broader retail trends monitored by the industry. Consumer behavior is increasingly influenced by ethical considerations, with a growing demand for sustainably sourced cocoa. Data from the Fairtrade Foundation indicates that the UK is one of the largest markets for Fairtrade certified cocoa products globally. The rise of health consciousness has also spurred innovation in dark chocolate and sugar free variants. Regulatory frameworks regarding labeling and nutritional information are strict, ensuring transparency for consumers. The market is supported by a robust distribution network comprising supermarkets, convenience stores, and online platforms. Seasonal peaks such as Easter and Christmas drive significant volume spikes. This dynamic landscape requires manufacturers to balance traditional appeal with modern demands for sustainability and health.

MARKET DRIVERS

Cultural Tradition and Seasonal Gifting Habits

The enduring cultural tradition of chocolate consumption and its central role in seasonal gifting habits are the main reasons behind the growth of the United Kingdom chocolate market. Chocolate is deeply embedded in British social rituals, particularly during festivals such as Easter, Christmas, and Valentine’s Day. The National Confectioners Association (US) indicates that Easter is the second-largest candy-consuming holiday, generating over $5 billion in sales, though recent growth has been driven primarily by higher prices and a 41% multi-year surge in non-chocolate candy sales. This seasonal demand creates predictable revenue spikes that manufacturers rely on for annual profitability. The tradition of giving chocolate as a gesture of affection or celebration ensures consistent baseline demand throughout the year. Research indicates that approximately 50-60% of consumers purchase chocolate for gifting during peak seasonal periods, while seasonal products collectively account for roughly 14% of the UK's annual chocolate market by value. The emotional connection associated with chocolate brands fosters loyalty and repeat purchases. As per sources, premium boxed chocolates see a significant surge in December, accounting for 30 percent of annual luxury confectionery sales. The widespread availability of seasonal assortments in retail outlets enhances accessibility and impulse buying. This cultural ingrainedness makes chocolate a resilient category less susceptible to economic downturns compared to other discretionary spends. The anticipation of festive seasons drives marketing campaigns and product launches, sustaining consumer interest and engagement. Thus, the strong association between chocolate and celebration continues to propel market growth, ensuring its dominance in the confectionery sector.

Innovation in Premium and Artisanal Segments

Innovation in premium and artisanal chocolate segments significantly drives the United Kingdom chocolate market expansion. This appeals to discerning consumers seeking quality and unique experiences. British shoppers are increasingly trading up from mass market brands to high end options that offer superior taste and ethical credentials. According to data from the Speciality & Fine Food Fair and market analysts, the premium and artisanal chocolate segment is growing at a steady rate of approximately 6-7% annually, driven by consumer demand for ethical sourcing and higher cocoa content. Consumers are willing to pay more for single origin beans, high cocoa content, and innovative flavor combinations such as sea salt or chili. Data from Kantar Worldpanel shows that while the average price of chocolate has increased by over 12%, volume sales have actually declined by approximately 6%, indicating that inflation is beginning to impact consumer demand. The rise of craft chocolate makers has introduced diverse profiles that challenge traditional norms, attracting foodies and enthusiasts. As per retail reports, independent chocolatiers have expanded their presence in urban centers, offering bespoke products that emphasize craftsmanship. The emphasis on bean to bar transparency appeals to consumers who value provenance and production methods. Social media platforms amplify this trend by showcasing visually appealing and exotic varieties, driving trial and awareness. This focus on quality and differentiation allows premium brands to capture higher margins and build dedicated customer bases. The continuous introduction of novel textures and ingredients keeps the market dynamic and engaging. Thus, innovation in the premium sector acts as a powerful catalyst for growth and diversification.

MARKET RESTRAINTS

Health Consciousness and Sugar Reduction Trends

Health consciousness and the global trend towards sugar reduction are major restraints to the United Kingdom chocolate market. This influences consumer purchasing decisions. Public health initiatives aimed at combating obesity and diabetes have led to increased scrutiny of high sugar foods, including chocolate. According to Public Health England, guidelines recommend limiting free sugar intake to no more than 30 grams per day for adults, prompting many consumers to reduce their chocolate consumption. Research indicates that approximately 45-50% of adults are actively trying to cut down on sugary snacks, whereas the National Diet and Nutrition Survey tracks actual intake, revealing that most adults still exceed the daily sugar limit. The implementation of the Soft Drinks Industry Levy has raised awareness about sugar taxes, creating a negative perception around sweet treats. The rise of alternative snacks such as fruit bars and protein balls offers healthier substitutes, diverting spending away from traditional confectionery. Manufacturers face pressure to reformulate products with lower sugar content, which can compromise taste and texture, potentially alienating loyal customers. The stigma associated with indulgent foods makes chocolate vulnerable to shifts in dietary preferences. This health driven avoidance restricts volume growth and forces companies to invest heavily in developing healthier alternatives. The tension between indulgence and wellness creates a challenging environment for traditional chocolate products, limiting their appeal among health conscious demographics.

Volatility in Cocoa Prices and Supply Chain Instability

Volatility in cocoa prices and supply chain instability are significant hindrances to the United Kingdom chocolate market. This affects production costs and pricing strategies. Cocoa is a commodity subject to fluctuating global prices due to weather conditions, political instability in producing countries, and disease outbreaks. According to the International Cocoa Organization (ICCO), cocoa prices have experienced historic surges of over 150% (tripling in some instances) in recent years due to severe harvest deficits in West Africa. This inflation directly impacts the profit margins of manufacturers who struggle to pass costs onto price sensitive consumers. The Food and Drink Federation (FDF) and AHDB shows that input costs have risen significantly, driven by record cocoa prices (ICCO) and high domestic dairy and sugar costs (AHDB), squeezing operational budgets. Supply chain disruptions caused by logistical bottlenecks and labor shortages further exacerbate the issue, leading to delays and inventory management challenges. As per studies, smaller manufacturers are particularly vulnerable to these fluctuations, lacking the financial reserves to absorb shocks. The uncertainty surrounding future cocoa availability forces companies to hedge risks and seek alternative sourcing, which can be complex and costly. Higher retail prices may dampen consumer demand, particularly for impulse purchases. The reliance on a few key growing regions creates systemic risk, making the market susceptible to external shocks. These economic and logistical pressures constrain market growth and necessitate strategic adaptations to maintain competitiveness and affordability.

MARKET OPPORTUNITIES

Expansion of Plant Based and Vegan Chocolate Products

The expansion of plant based and vegan chocolate products offers a significant opportunity for the United Kingdom chocolate market. This caters to the growing demographic of flexitarians and vegans. Consumers are seeking dairy free alternatives that do not compromise on taste or texture, driving demand for innovative formulations. According to the Vegan Society, the number of vegans in the UK has quadrupled in the last decade, creating a substantial niche market. A study indicates that 40 percent of consumers are interested in trying plant based chocolate options, expanding the potential customer base beyond strict vegans. Manufacturers are utilizing ingredients such as oat milk, almond milk, and coconut cream to create creamy alternatives to traditional milk chocolate. The opportunity lies in bridging the gap between ethical consumption and indulgence, offering products that appeal to mainstream buyers. Branding these alternatives as sustainable and cruelty free resonates with environmentally conscious shoppers. By diversifying into this segment, traditional chocolate producers can mitigate the risks associated with declining dairy consumption and tap into a rapidly expanding market. This strategic pivot allows companies to remain relevant and capture value from evolving dietary trends. The continuous improvement in flavor and mouthfeel ensures that plant based chocolate becomes a viable and attractive option for a broad audience.

Direct to Consumer and Personalized Gift Services

Direct-to-consumer and personalized gift services pave the way for the expansion of the UK chocolate market. These services leverage digital platforms to enhance customer engagement and loyalty. Online sales allow brands to bypass traditional retail intermediaries, offering higher margins and direct data insights. According to data from the Office for National Statistics, while the baseline shift to online shopping remains permanent, modern e-commerce food and drink sales have stabilized to steady single-digit year-on-year growth following the pandemic-era online boom. Data from industry analysis shows that personalized chocolate gifts, such as engraved bars or custom boxes, command premium prices and drive higher average order values. Consumers appreciate the convenience of home delivery and the ability to tailor gifts for special occasions. Consumer gift-buying surveys show that while over 60% of shoppers prefer buying personalized gifts online, custom chocolates represent a fast-growing sub-segment within this digital birthday and anniversary market. Brands are investing in user friendly websites and social media marketing to reach wider audiences. The integration of subscription services ensures recurring revenue and customer retention. The ability to offer exclusive online limited editions creates a sense of urgency and exclusivity. This digital transformation enables smaller artisanal brands to compete with larger players by reaching niche markets globally. By focusing on customization and direct engagement, chocolate companies can build stronger relationships with consumers and differentiate themselves in a crowded market. This channel expansion ensures sustained growth and resilience against retail fluctuations.

MARKET CHALLENGES

Regulatory Pressure on Packaging and Sustainability

Regulatory pressure on packaging and sustainability is a serious challenge to the United Kingdom chocolate market. This forces manufacturers to rethink their material usage and waste management. The UK government has implemented stringent rules to reduce plastic waste, including bans on single use plastics and requirements for recyclable packaging. According to DEFRA's Extended Producer Responsibility framework, companies must report their packaging data and face modulated fees based on the recyclability of their materials, creating financial penalties for non-recyclable packaging rather than an outright ban. Data from the Waste and Resources Action Programme indicates that the confectionery sector faces high scrutiny due to the complex multi layer materials often used for chocolate bars. Compliance with these regulations requires substantial investment in research and development to find suitable alternatives that maintain product freshness and quality. As per sources, transitioning to paper based or biodegradable packaging can increase production costs by up to 15 percent. Consumers are increasingly aware of environmental issues and penalize brands that fail to demonstrate genuine commitment to sustainability. The challenge lies in balancing aesthetic appeal and protection with eco friendly materials. Failure to adapt may result in reputational damage and loss of market share to competitors with stronger green credentials. Navigating this regulatory landscape requires continuous innovation and collaboration with supply chain partners. The cost and complexity of compliance pose a persistent hurdle for manufacturers aiming to maintain profitability while meeting environmental standards.

Labor Shortages and Production Cost Increases

Labor shortages and rising production costs slow down the growth of the United Kingdom chocolate market. This impacts operational efficiency and profitability. The manufacturing sector faces difficulties in recruiting skilled workers for roles in production, logistics, and quality control. According to the Food and Drink Federation (FDF), approximately 40% of food and drink manufacturers report operational difficulties rooted in a structural shortage of applicants with the necessary technical and engineering skills. An aging workforce exacerbates this issue, as experienced employees retire without adequate replacements. Data from the Office for National Statistics indicates that while wage growth has moderated to a steady 3.4% to 3.8%, it remains a core operational expense that companies must balance alongside volatile raw material costs. Energy costs, a significant component of chocolate production, have also surged, adding pressure to budgets. As per the Federation of Small Businesses, small and medium sized enterprises are particularly affected, lacking the resources to absorb these shocks. The shortage of drivers and warehouse staff leads to delays in distribution, affecting product availability and freshness. The cumulative effect of labor and energy costs forces companies to raise prices, which may dampen consumer demand. Addressing this challenge requires investment in automation and training programs, which involve significant upfront capital. The inability to secure a stable workforce threatens the consistency and quality of production. This operational instability creates a challenging environment for growth and competitiveness in the UK chocolate market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.18% |

| Segments Covered | By Product Type, Form Price Range, Ingredient Type, Category, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, and East Midlands |

| Market Leaders Profiled | Mars, Incorporated, Ferrero International SpA, Nestlé S.A., Chocoladefabriken Lindt & Sprüngli AG, Mondelēz International Inc., The Hershey Company, Barry Callebaut AG, The London Chocolate Company, Yıldız Holding A.Ş. (Godiva / Ulker), Lotte Corporation, Arcor S.A.I.C., Whitakers Chocolates Ltd, Artisan du Chocolat Ltd, Morinaga & Co., Ltd., Tony's Chocolonely UK Ltd, Divine Chocolate Ltd, Pecan Deluxe Candy Company, Land Chocolate Ltd, Fazer Group, and Green & Black's Organic |

SEGMENTAL ANALYSIS

By Product Type Insights

The milk chocolate segment held a majority share of 48.7% of the UK chocolate market in 2025, because of its deep-rooted cultural preference and widespread appeal across all age demographics. The creamy texture and balanced sweetness of milk chocolate align perfectly with the British palate, which has historically favored sweeter confectionery over bitter dark varieties. Research confirms that milk chocolate dominates the UK market, accounting for approximately 53-57% of sales volume (often grouped with white chocolate), reflecting its status as the default consumer choice. This dominance is driven by the familiarity of iconic brands that have shaped childhood memories and social traditions for generations. A study indicates that over 90% of UK consumers eat chocolate, with milk chocolate being the most popular variety, enjoyed by approximately 80% of chocolate eaters. The versatility of milk chocolate allows it to be used in various formats, from standalone bars to ingredients in biscuits and cakes, further embedding it in daily consumption habits. Sources show that milk chocolate's affordability is largely driven by its higher sugar content and economies of scale in manufacturing, though rising cocoa and milk costs are currently challenging this low-price positioning. The extensive distribution network ensures that milk chocolate is available in every retail outlet, from large supermarkets to small convenience stores. This ubiquity and emotional connection secure its leading position, making it the backbone of the UK chocolate industry.

The affordability and mass market accessibility of milk chocolate further reinforce its supremacy. Compared to dark or premium artisanal chocolates, milk chocolate is generally priced lower, making it an attractive option for impulse purchases and everyday treats. The economies of scale achieved by major manufacturers allow them to keep production costs low, passing savings onto consumers. In addition, the wide variety of formats, including sharing bags and single serve bars, caters to different consumption occasions and budgets. This economic advantage ensures that milk chocolate remains the most purchased type, sustaining high turnover rates for retailers. The ability to innovate with fillings and coatings while maintaining a low price point keeps the segment dynamic and appealing. Consequently, the combination of low cost and high availability ensures that milk chocolate continues to lead the market, resisting competition from niche segments.

The dark chocolate segment is predicted to witness the highest CAGR of 6.5% over the forecast period owing to increasing health consciousness and awareness of its antioxidant benefits. Consumers are increasingly seeking indulgent treats that offer nutritional value, and dark chocolate fits this criterion due to its high cocoa content and lower sugar levels. According to the British Nutrition Foundation, dark chocolate is rich in flavonoids, which are associated with improved heart health and cognitive function. A study indicates that 40 percent of consumers perceive dark chocolate as a healthier alternative to milk chocolate, influencing their purchasing decisions. The trend towards clean labeling and minimal processing favors dark chocolate, which often contains fewer additives. Medical professionals and dieticians often recommend moderate consumption of dark chocolate as part of a balanced diet, enhancing its credibility. This health driven demand attracts not only health enthusiasts but also older demographics looking for functional foods. The positioning of dark chocolate as a guilt free indulgence allows it to capture a growing share of the market, outpacing traditional segments.

The premiumization of dark chocolate and the introduction of gourmet flavor profiles significantly accelerate its growth. Consumers are trading up to high quality single origin bars that offer complex taste experiences, moving away from mass produced options. Data from retail analysis shows that premium dark chocolate commands higher margins, encouraging retailers to expand their assortments. The rise of craft chocolate makers has educated consumers about bean to bar processes, fostering appreciation for terroir and craftsmanship. As per consumer surveys, 35 percent of shoppers are willing to pay more for ethically sourced and sustainably produced dark chocolate. The aesthetic appeal of premium packaging and the story behind the brand enhance the perceived value, making it a popular gift item. Social media platforms amplify this trend by showcasing visually striking and exotic varieties, driving trial among younger demographics. This focus on quality and exclusivity ensures that dark chocolate continues to expand rapidly, establishing itself as a dynamic and lucrative segment in the UK market.

By Form Insights

The tablets and bars segment led the United Kingdom chocolate market and captured a 65.4% share in 2025. This leading position of the segment was attributed to its unmatched convenience and portability, catering to the fast paced lifestyles of modern consumers. Also, this form factor is easy to carry, store, and consume, making it ideal for snacking during commutes, work breaks, or leisure activities. Research confirms that tablets and bars remain the dominant format in the retail landscape, accounting for over 55% of total chocolate sales volume. The standardized sizing and packaging facilitate efficient shelf display and inventory management for retailers. The individual wrapping ensures hygiene and portion control, appealing to health conscious consumers who want to manage their intake. As per a study, the versatility of bars allows for a wide range of prices and sizes, from budget friendly singles to premium large format bars. The familiarity of the bar format reduces decision fatigue, making it the go to choice for quick satisfaction. This structural advantage ensures that tablets and bars remain the cornerstone of the chocolate market, driving consistent volume and revenue.

The effectiveness of branding and marketing strategies for tablets and bars further cements their leading position in the country’s market. Major chocolate brands invest heavily in distinctive packaging designs and advertising campaigns that highlight their bar products, creating strong brand recognition and loyalty. Data from retail scans shows that branded bars dominate eye level shelf space, maximizing exposure to shoppers. The ability to launch limited edition flavors and seasonal variations in bar format allows companies to keep the product range fresh and engaging. As per consumer feedback, the tactile experience of unwrapping a bar enhances the sensory enjoyment, reinforcing positive associations with the brand. Promotional activities such as multi buy offers and bundle deals are predominantly focused on bars, driving volume sales. The consistency in shape and size facilitates automated manufacturing and packaging, reducing costs and ensuring supply reliability. This combination of marketing prowess and operational efficiency ensures that tablets and bars continue to lead the market, maintaining their relevance and popularity among diverse consumer groups.

The boxed assortments segment is estimated to register the fastest CAGR of 7.2% between 2026 and 2034 due to the strong gifting culture and demand for special occasion treats. Consumers increasingly view boxed chocolates as premium gifts for birthdays, anniversaries, and holidays, valuing the presentation and variety they offer. Research confirms that boxed chocolates are consistently among the top three most purchased gift categories in the UK, particularly during peak seasons like Valentine's Day and Christmas. The ability to include a diverse selection of flavors and textures in one package appeals to recipients with varied preferences. As per retail reports, luxury chocolatiers have expanded their boxed ranges, introducing intricate designs and personalized options that enhance the unboxing experience. The emotional value associated with giving a beautifully packaged box drives higher spending per transaction. This trend is amplified by social media, where users share images of elaborate chocolate gifts, inspiring others to purchase similar items. The focus on experiential gifting ensures that boxed assortments continue to grow rapidly, capturing a significant share of the premium market.

The premiumization of boxed assortments and the appeal of artisanal craftsmanship significantly contribute to their rapid growth. Consumers are seeking high quality, handcrafted chocolates that offer unique taste experiences, moving away from standard mass produced options. A study shows that consumers are willing to pay a premium for boxes featuring rare cocoa beans and innovative flavor combinations. The storytelling aspect of artisanal brands, emphasizing heritage and skill, resonates with discerning buyers who value authenticity. As per consumer surveys, 40 percent of shoppers associate boxed chocolates with luxury and indulgence, making them a preferred choice for self reward and celebration. Retailers support this trend by dedicating prominent shelf space to premium boxes and offering tasting events. The exclusivity and limited availability of certain artisanal collections create a sense of urgency and desire. This focus on quality and uniqueness ensures that boxed assortments remain the fastest growing segment, attracting affluent consumers and culinary enthusiasts alike.

By Ingredient Type Insights

The dairy-based chocolate segment dominated the United Kingdom market and accounted for a substantial share in 2025. This dominance of the segment was driven by the traditional consumer preference for the creamy texture and rich flavor that milk solids provide. The combination of cocoa and dairy creates a smooth mouthfeel that is widely appreciated and deeply ingrained in British eating habits. Data from the National Confectioners Association shows that milk chocolate is the preferred type for about 40-48% of consumers, while in markets like India, dairy-based chocolates can account for over 80% of the sector due to cultural preference for sweeter, milk-rich profiles. The familiarity of milk chocolate brands ensures consistent demand across all demographic groups. Also, the established supply chain for dairy ingredients ensures stable production and competitive pricing. As per sources, the versatility of dairy based chocolate allows it to be used in a wide variety of products, from bars to baking ingredients. The emotional connection with traditional recipes and family traditions reinforces loyalty to dairy based options. This structural advantage ensures that dairy based chocolate remains the default choice, driving volume and sustaining market leadership. The inability of many plant based alternatives to fully replicate the creamy texture of dairy further solidifies this dominance.

The established supply chain and cost efficiency of dairy based chocolate further supports its leading position. The UK has a robust dairy industry that provides a reliable source of high quality milk powder and butterfat for chocolate production. Research shows that the economies of scale in dairy processing allow manufacturers to produce chocolate at lower costs compared to plant based alternatives. The widespread availability of dairy ingredients ensures consistent quality and supply stability. As per retail scans, dairy based chocolates are priced competitively, making them accessible to a broad consumer base. The familiarity of dairy formulations simplifies manufacturing processes, reducing operational complexities. This economic efficiency enables companies to invest in marketing and innovation, maintaining brand relevance. The strong infrastructure supporting dairy based production ensures that it remains the dominant ingredient type, resisting competition from emerging alternatives. The combination of cost effectiveness and supply reliability secures its position as the backbone of the UK chocolate industry.

The plant based chocolate segment is anticipated to witness the fastest CAGR of 12.5% during the forecast period. This swift expansion of the segment is propelled by rising veganism and ethical consumption trends. Consumers are increasingly avoiding animal products due to environmental concerns and animal welfare issues, seeking dairy free alternatives. According to the Vegan Society, the number of vegans in the UK has quadrupled in the last decade, creating a substantial market for plant based confectionery. Manufacturers are using ingredients such as oat, almond, and coconut milk to create creamy textures that mimic dairy. The labeling of products as cruelty free and sustainable appeals to environmentally conscious shoppers. This ethical drive ensures that plant based chocolate continues to grow rapidly, capturing a significant share of the market. The continuous improvement in flavor and texture makes these products more appealing to mainstream consumers.

Innovation in alternative milk technologies significantly accelerates the growth of the plant based chocolate segment. Advances in food science have enabled the creation of plant based milks that emulsify well with cocoa, producing smooth and rich chocolates. According to food science and manufacturing industry reports, advanced micro-milling and refining techniques for oat, rice, and nut-based milks have dramatically improved the sensory profile of vegan chocolates, resolving previous graininess issues. Brands are experimenting with novel ingredients such as rice and hemp milk to offer diverse flavor profiles. As per consumer feedback, the removal of aftertastes common in early vegan products has enhanced satisfaction and repeat purchases. The introduction of certified organic and fair trade plant based options further boosts appeal. Retailers are promoting these innovations through tastings and educational campaigns. This focus on technological advancement and quality ensures that plant based chocolate remains the fastest growing segment, attracting health conscious and ethical consumers alike.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest in the UK chocolate market and occupied a significant share in 2025. This prominence of segment was supported by its ubiquity and the convenience of one stop shopping for consumers. These retail formats offer a wide assortment of chocolate products under one roof, making them the primary destination for household grocery needs. The high footfall in these stores ensures maximum visibility and impulse purchase opportunities. In addition, the ability to compare prices and brands easily enhances the shopping experience. The extensive shelf space allows for the display of both mass market and premium brands, catering to diverse preferences. This structural advantage ensures that supermarkets remain the primary channel for chocolate distribution, sustaining high turnover rates. The integration of online grocery services further extends their reach, allowing consumers to order chocolate for home delivery.

The competitive pricing and aggressive promotional strategies of supermarkets is also a major reason for growth. Large retail chains leverage their bargaining power to negotiate lower prices from manufacturers, passing savings onto consumers. Data from retail scans shows that supermarkets frequently run seasonal promotions and loyalty card discounts on chocolate, stimulating demand. The ability to offer private label alternatives at lower price points attracts budget conscious buyers. As per industry reports, the volume driven model of supermarkets allows them to maintain profitability despite lower margins. The strategic placement of chocolate near checkouts and in end aisle displays maximizes impulse buys. This focus on price and promotion ensures that supermarkets continue to dominate the market, capturing the majority of consumer spend. The consistency in supply and availability builds trust and loyalty among shoppers. Consequently, the combination of affordability and accessibility secures the leading position of supermarkets in the UK chocolate distribution channel.

The online retail segment is likely to experience the fastest CAGR of 9.5% over the forecast period. This quick surge is fuelled by digital transformation and the expansion of home delivery services. Consumers increasingly prefer the convenience of browsing and purchasing chocolate from home, avoiding crowded stores. A study indicates that 40 percent of millennials prefer buying specialty chocolates online due to the wider selection available. The rise of quick commerce platforms allows for rapid delivery of impulse items, enhancing accessibility. As per sources, subscription services for monthly chocolate boxes have gained popularity, ensuring recurring revenue for retailers. The ability to access niche and international brands not available in local stores drives online adoption. This shift towards digital convenience ensures that online retail continues to grow rapidly, capturing a larger share of the market. The integration of personalized recommendations and user reviews enhances the shopping experience.

Personalization and direct to consumer models significantly accelerate the growth of the online retail channel. Brands are leveraging data analytics to offer customized chocolate gifts and tailored recommendations, enhancing customer engagement. According to e commerce trends, personalized products command higher average order values and foster loyalty. A study shows that 50 percent of online shoppers appreciate the ability to engrave messages or select specific flavors for gifts. Direct to consumer websites allow brands to bypass intermediaries, offering exclusive products and better margins. As per consumer surveys, the unboxing experience of online orders adds value, encouraging social sharing and word of mouth marketing. The flexibility of online platforms enables rapid launch of new products and limited editions. This focus on customization and direct engagement ensures that online retail remains the fastest growing channel, attracting tech savvy consumers and gift buyers alike. The continuous improvement in logistics and packaging supports this expansion.

COUNTRY LEVEL ANALYSIS

The United Kingdom plays a key role in the European chocolate market and accounted for a 25.3% share in 2025. This growth of the UK market was propelled by a strong tradition of indulgence and gifting, with seasonal peaks playing a crucial role in annual sales. It is a mature and highly developed landscape, with one of the highest per capita consumption rates globally. Research indicates that the average UK consumer eats approximately 8.1 kilograms of chocolate per year, ranking them among the world's top consumers. A study shows that chocolate accounts for roughly 70% of the UK's confectionery revenue, a segment supported by a highly developed retail network. Data from the British Retail Consortium shows that chocolate accounts for a significant portion of confectionery revenue, supported by a robust retail infrastructure. Consumer preferences are shifting towards premium and ethically sourced products, influencing manufacturer strategies. The rise of health consciousness has spurred innovation in dark and plant based variants, diversifying the market. Regulatory frameworks regarding sustainability and labeling are strict, ensuring transparency and accountability. The presence of major global and local brands creates a competitive environment that drives continuous innovation. Economic factors such as inflation and disposable income levels impact purchasing behavior, yet demand remains resilient due to the emotional value of chocolate. The integration of digital channels enhances accessibility and engagement. This dynamic interplay of tradition, innovation, and regulatory compliance ensures that the UK remains a vibrant and strategically important market for chocolate producers worldwide.

COMPETITIVE LANDSCAPE

The competition in the UK chocolate market is intense and characterized by the presence of global giants and niche artisanal producers. Major companies compete on brand recognition distribution networks and product innovation while smaller players differentiate through unique flavors and ethical sourcing. Price sensitivity varies across segments with private label offerings gaining traction due to economic pressures on household budgets. Premium and artisanal chocolates command higher margins by appealing to consumers seeking quality and exclusivity. The rise of plant based and healthy alternatives adds another layer of competition forcing traditional manufacturers to diversify their portfolios. Retailers play a pivotal role in shaping competitive dynamics through exclusive contracts and promotional strategies. Innovation in packaging and sustainability credentials is increasingly important for brand differentiation. Regulatory changes regarding labeling and environmental standards also impact competitive strategies. Companies must balance cost efficiency with value addition to retain market share. The market continues to evolve with shifting consumer preferences towards health convenience and responsibility driving strategic decisions and competitive positioning among key participants in the region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the UK chocolate market are

- Mars, Incorporated

- Ferrero International SpA

- Nestlé S.A.

- Chocoladefabriken Lindt & Sprüngli AG

- Mondelēz International Inc.

- The Hershey Company

- Barry Callebaut AG

- The London Chocolate Company

- Yıldız Holding A.Ş. (Godiva / Ulker)

- Lotte Corporation

- Arcor S.A.I.C.

- Whitakers Chocolates Ltd

- Artisan du Chocolat Ltd

- Morinaga & Co., Ltd.

- Tony's Chocolonely UK Ltd

- Divine Chocolate Ltd

- Pecan Deluxe Candy Company

- Land Chocolate Ltd

- Fazer Group

- Green & Black's Organic

Top Players in the Market

- Mondelez International is a dominant force in the United Kingdom chocolate sector, owning iconic brands such as Cadbury Dairy Milk and Toblerone. The company leverages its extensive distribution network to ensure widespread availability across retail and convenience channels. Recently Mondelez has invested heavily in sustainable cocoa sourcing programs to enhance brand reputation and meet consumer ethical expectations. The firm actively promotes digital engagement through interactive marketing campaigns that resonate with younger demographics. It has also expanded its premium product lines to cater to the growing demand for high quality indulgent treats. These strategic initiatives reinforce its leadership position by combining heritage appeal with modern sustainability values. The company continues to innovate in packaging solutions to reduce environmental impact while maintaining product freshness and quality for UK consumers.

- Nestle UK Ltd holds a significant presence in the market with popular brands like KitKat and Aero. The company focuses on continuous product innovation and portfolio diversification to meet evolving consumer preferences. Recently Nestle has introduced plant based alternatives and reduced sugar options to address health conscious trends. The firm strengthens its market position by collaborating with retailers on exclusive promotions and seasonal launches. Nestle invests in advanced manufacturing technologies to improve efficiency and reduce carbon emissions. Its commitment to responsible sourcing and community engagement enhances brand loyalty among British shoppers. The company also leverages data analytics to understand consumer behavior and tailor marketing strategies effectively. These efforts ensure that Nestle remains competitive and relevant in the dynamic UK chocolate landscape by balancing tradition with innovation.

- Ferrero UK Ltd contributes significantly to the market through premium brands such as Ferrero Rocher and Kinder. The company emphasizes quality craftsmanship and distinctive branding to appeal to discerning consumers. Recently Ferrero has expanded its direct to consumer capabilities by enhancing its e commerce platform and personalized gifting services. The firm actively engages in sustainability initiatives including recyclable packaging and ethical cocoa procurement. Ferrero strengthens its position by launching limited edition products that drive excitement and urgency among buyers. The company also invests in digital marketing to reach wider audiences and build emotional connections. Its focus on premium positioning and innovative customer experiences ensures sustained growth. Ferrero continues to adapt to market trends by offering healthier options and transparent sourcing information to maintain trust and loyalty in the UK.

Top Strategies Used by Key Market Participants

Key players in the UK chocolate market employ diverse strategies to maintain competitiveness and drive growth. Product innovation focuses on health conscious options such as reduced sugar and plant based variants. Sustainability initiatives prioritize ethical sourcing and eco friendly packaging to meet consumer expectations. Digital transformation enhances direct to consumer sales through e commerce platforms and personalized marketing. Strategic partnerships with retailers ensure prominent shelf placement and promotional visibility. Brand differentiation through heritage storytelling and premium positioning appeals to affluent segments. Cost optimization through supply chain efficiency helps maintain profitability amidst rising input costs. These approaches collectively strengthen market presence and adapt to evolving consumer preferences in the dynamic landscape of the United Kingdom chocolate industry.

MARKET SEGMENTATION

This research report on the UK chocolate market is segmented and sub-segmented into the following categories.

By Product Type

- Dark Chocolate

- Milk and White Chocolate

By Form

- Tablets and Bars

- Molded Blocks

- Pralines and Truffles

- Other Forms

By Price Range

- Mass

- Premium

By Ingredient Type

- Dairy-based

- Plant-based

By Category

- Single Origin Chocolate

- Conventional Chocolate

By Distribution Channel

- Supermarkets/Hypermarkets

- Online Retail Stores

- Convenience Store

- Other Distribution Channels

Frequently Asked Questions

1. How large is the UK chocolate market?

The UK chocolate market is one of the largest confectionery markets in Europe, driven by strong consumer demand, premium product innovation, and seasonal sales.

2. What factors are driving the growth of the UK chocolate market?

Growth is supported by rising demand for premium chocolates, increasing interest in sustainable and ethical sourcing, product innovation, and expanding online retail channels.

3. Which type of chocolate is most popular in the UK?

Milk chocolate remains the most widely consumed chocolate type in the UK, although dark chocolate is gaining popularity due to its perceived health benefits.

4. What is driving demand for premium chocolate products in the UK?

Consumers are increasingly seeking high quality ingredients, unique flavors, artisanal products, and ethically sourced cocoa, which is boosting the premium chocolate segment.

5. How is sustainability influencing the UK chocolate market?

Many consumers prefer chocolate products made with sustainably sourced cocoa and environmentally friendly packaging, encouraging manufacturers to adopt responsible practices.

6. What role does e commerce play in the UK chocolate market?

Online retail platforms have expanded product accessibility, enabling consumers to purchase a wide range of chocolate products conveniently from home.

7. What are the future trends in the UK chocolate market?

Future trends include premiumization, clean label products, reduced sugar formulations, sustainable sourcing initiatives, personalized chocolates, and increased demand for plant based alternatives.

8. Which distribution channel dominates the UK chocolate market?

Supermarkets and hypermarkets account for a significant share of chocolate sales due to their extensive product selection and strong retail presence.

9. How do seasonal events affect chocolate sales in the UK?

Occasions such as Christmas, Easter, Valentine's Day, and Halloween significantly boost chocolate consumption and sales throughout the year.

10. What challenges does the UK chocolate market face?

The market faces challenges including fluctuating cocoa prices, supply chain disruptions, regulatory requirements, and growing concerns about sugar consumption.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com