UK Coffee Market Size, Share, Trends & Growth Forecast Report - Segmented By Type, Application, End-User and By Country (London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$9024 MnMarket Estimate, 2026

$9,236 MnMarket Forecast, 2034

$11,122 MnCAGR, 2026–2034

2.35%UK Coffee Market Report Summary

The UK coffee market was valued at USD 9,024 million in 2025, is estimated to reach USD 9,236.05 million in 2026, and is projected to attain USD 11,122.17 million by 2034, expanding at a CAGR of 2.35% during the forecast period from 2026 to 2034. The growth of the UK coffee market is driven by the country's strong coffee-drinking culture, rising demand for premium and specialty coffee, and the expansion of café chains and independent coffee shops. Increasing consumer preference for sustainably sourced and ethically certified coffee, along with the growing popularity of ready-to-drink and convenience-based coffee products, is supporting market expansion. Moreover, innovations in coffee brewing technologies, premium home coffee machines, and the rapid growth of e-commerce and subscription-based coffee services are creating new growth opportunities across the UK.

Key Market Trends

- Rising demand for specialty and single-origin coffee driven by consumers seeking premium quality and unique flavor profiles.

- Growing preference for sustainably sourced, organic, and ethically certified coffee products across retail and foodservice channels.

- Increasing adoption of premium home brewing equipment and coffee subscription services among UK households.

- Expansion of ready-to-drink coffee and convenient on-the-go beverage options to meet changing consumer lifestyles.

- Continuous product innovation, including functional, flavored, and plant-based coffee offerings, is attracting younger consumer segments.

SEGMENTAL INSIGHTS

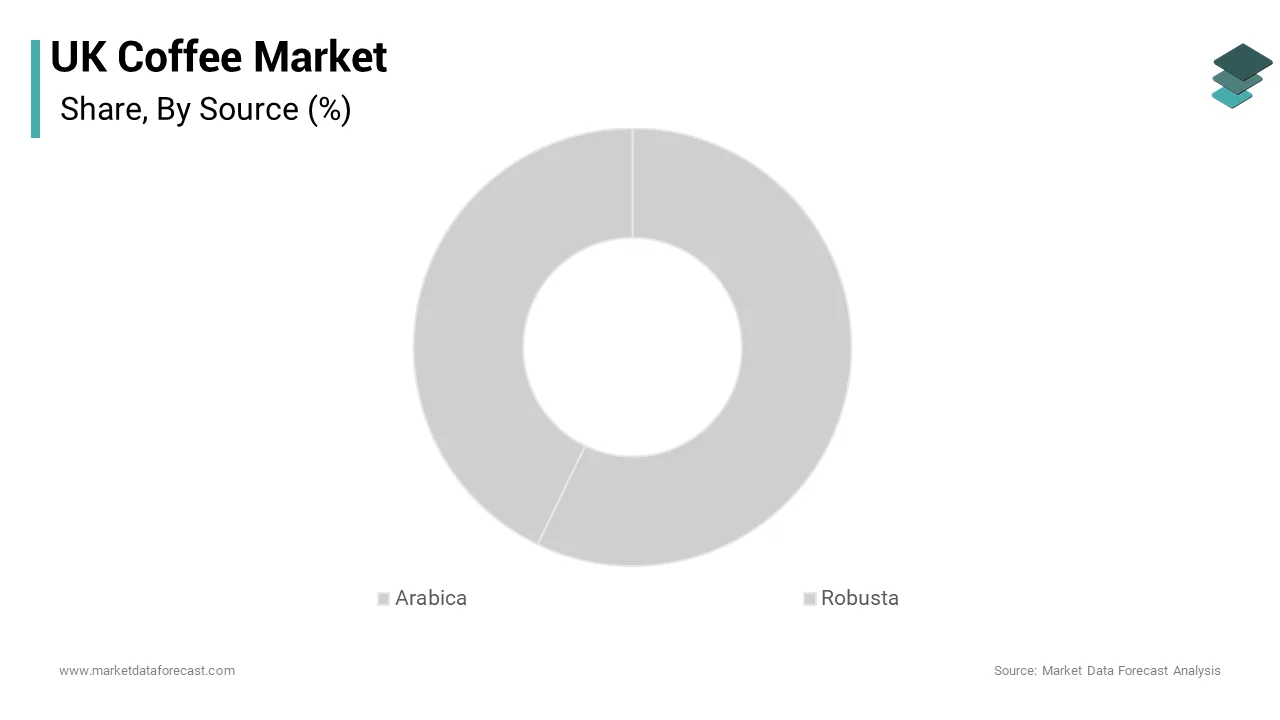

Based on source, the arabica coffee segment dominated the UK coffee market and accounted for 56.7% of the market share in 2025. The segment's leadership is attributed to its superior taste, smoother flavor profile, lower bitterness, and strong consumer preference for premium-quality coffee in both retail and café environments.

Based on type, the instant coffee segment held the largest share of 32.5% of the UK coffee market in 2025. Its dominance is primarily driven by unmatched convenience, affordability, long shelf life, and its long-standing presence in British households, making it a preferred choice for daily coffee consumption.

Based on ingredient process, the caffeinated segment accounted for the largest share of the UK coffee market in 2025. The segment continues to lead due to sustained consumer demand for energy-boosting beverages, widespread daily consumption habits, and the popularity of traditional caffeinated coffee across residential, workplace, and foodservice settings.

REGIONAL INSIGHTS

The United Kingdom remained one of the leading contributors to the European coffee market in 2025, supported by high per capita coffee consumption, a well-established café culture, and strong demand for premium coffee products. The market continues to benefit from expanding specialty coffee chains, increasing consumer awareness of sustainable sourcing, and rapid growth in online coffee retail. Rising investments in premium product offerings, innovative brewing solutions, and convenient coffee formats are further strengthening market development across the country. Urban centers continue to drive demand, while growing interest in artisanal and ethically sourced coffee is supporting long-term market expansion throughout the UK.

Competitive Landscape

The UK coffee market is highly competitive, with global coffee manufacturers, established café chains, and specialty coffee brands competing through product innovation, premiumization, and sustainability initiatives. Companies are expanding their portfolios with specialty blends, single-origin varieties, ready-to-drink beverages, and functional coffee products to address evolving consumer preferences. Leading market participants are also strengthening their omnichannel presence through supermarkets, cafés, e-commerce platforms, and subscription services while investing in ethical sourcing, recyclable packaging, and digital customer engagement. Strategic partnerships, acquisitions, and continuous investments in brand positioning and premium coffee experiences remain key competitive strategies shaping the market.

Prominent players in the UK coffee market include Nestlé UK Ltd, Starbucks Coffee Company, Costa Coffee, Starbucks (US), JDE Peet's (NL), Kraft Heinz (US), Lavazza (IT), Dunkin' (US), Peet's Coffee (US), Tchibo (DE), and Illy (IT).

UK Coffee Market Size

The UK coffee market size was valued at USD 9024 million in 2025 and is anticipated to reach USD 9236.05 million in 2026 to reach USD 11,122.17 million by 2034, at a CAGR of 2.35% during the forecast period from 2026 to 2034.

Coffee is defined as a brewed drink prepared from roasted coffee beans, available in various forms including espresso based beverages, filter coffee, and instant varieties. The UK has transitioned from a traditionally tea drinking nation to one of the most vibrant coffee cultures in Europe, with a high density of coffee shops in urban centers. According to the British Coffee Association, approximately 95 million cups of coffee are consumed in the UK every day, illustrating the sheer scale of demand. The Office for National Statistics notes that the hospitality sector, particularly independent cafes and chains, contributes significantly to local economies and employment. Consumer behavior is increasingly influenced by a desire for quality and provenance, with a growing preference for specialty and single origin beans. Data from the Allegra World Coffee Portal estimates that the UK branded coffee shop landscape has grown steadily, with outlet numbers increasing by approximately 3.5% in recent reporting periods, and independent specialty shops making up a growing segment of the market. Sustainability is also a key concern, with consumers prioritizing ethically sourced and environmentally friendly practices. The market is supported by a robust supply chain involving importers, roasters, and retailers. Regulatory frameworks regarding food safety and labeling ensure transparency for consumers. This evolving landscape requires stakeholders to balance mass market appeal with niche premium offerings to maintain relevance and growth.

MARKET DRIVERS

Proliferation of Specialty Coffee Culture and Third Wave Movement

The proliferation of specialty coffee culture and the third wave movement drives the growth of the United Kingdom coffee market. This elevates coffee from a commodity to an artisanal experience. Consumers are increasingly educated about coffee origins, processing methods, and brewing techniques, driving demand for high quality single origin beans and expertly crafted beverages. According to data from the World Coffee Portal by Allegra Strategies, the UK branded coffee shop market has shown consistent physical footprint expansion, driven by a strong consumer shift toward premiumization and specialty beverage experiences. This trend is fueled by a desire for authenticity and unique flavor profiles that mass market blends cannot offer. The rise of independent roasters and micro cafes in urban areas has created a competitive environment that fosters innovation and quality improvement. As per sources, social media platforms play a crucial role in disseminating knowledge about coffee culture, influencing consumer preferences and driving trial of new brands. The emphasis on barista skills and manual brewing methods such as pour over and AeroPress enhances the perceived value of the product. This cultural shift towards appreciation and connoisseurship ensures that the specialty segment continues to expand, attracting discerning consumers who view coffee as a craft rather than just a caffeine fix.

Expansion of Remote Work and Cafe as Third Space

The expansion of remote work and the concept of cafes as third spaces significantly fuel demand in the UK coffee market. This is because individuals increasingly seek environments outside the home and office for both work and socialization. The post pandemic shift towards hybrid working models has increased the frequency of daytime cafe visits, with professionals using these spaces for meetings and focused work. According to the Office for National Statistics, a significant portion of the UK’s hybrid workforce regularly conducts business from locations outside their home or primary office, sustaining steady footfall for hospitality businesses. Hospitality sector analyses demonstrate that cafes optimizing their spaces for "co-working", by offering high-speed Wi-Fi and ample seating, capture higher weekday daytime traffic from hybrid professionals seeking alternative workspaces. The cafe environment provides a sense of community and routine that remote workers crave, making it an essential part of their daily structure. Consumer surveys tracking remote workers show that a majority utilize local coffee shops multiple times a week as alternative working environments to vary their scenery and boost daily productivity. This behavioral change has led cafes to adapt their offerings, providing power outlets, quiet zones, and extended opening hours. The reliance on cafes for social interaction and professional networking further sustains demand. This structural shift in work habits ensures that coffee shops remain vital hubs of activity, driving consistent sales and reinforcing their role in modern urban life.

MARKET RESTRAINTS

Economic Pressure and Cost of Living Crisis

Economic pressure and the ongoing cost of living crisis are major restraints to the UK coffee market. This limits disposable income available for non essential purchases. Inflationary pressures on essential goods such as energy, food, and housing have forced many households to prioritize spending, leading to reduced expenditure on premium coffee drinks. According to indicators from the Office for National Statistics, while food and non-alcoholic beverage inflation slowed considerably throughout 2024 compared to previous record peaks, cumulative cost-of-living pressures have prompted many consumers to scale back on non-essential spending like out-of-home coffee. The Bank of England reports that real wages have stagnated, reducing purchasing power and encouraging consumers to seek cheaper alternatives. Also, the hospitality sector also faces challenges, with rising operational costs leading to higher menu prices that may deter casual drinkers. Hospitality industry studies show that severe cost pressures, including rising labor rates and utility expenses, have forced many independent coffee shops to optimize their operating hours and streamline menu choices to remain profitable. The uncertainty surrounding future economic conditions makes consumers cautious about splurging on daily luxuries. This financial constraint impacts both independent cafes and large chains, forcing them to reconsider pricing strategies and promotional activities. The inability of some consumers to justify the premium price of specialty coffee in a tight budget environment restricts market growth and limits expansion into broader demographic segments.

Supply Chain Volatility and Climate Impact on Coffee Beans

Supply chain volatility and the impact of climate change on coffee bean production further hinders the expansion of the United Kingdom coffee market. This affects availability and pricing. Coffee is primarily grown in tropical regions that are increasingly vulnerable to extreme weather events, pests, and diseases, leading to fluctuating yields and quality. According to market reports from the International Coffee Organization, the global coffee landscape has faced multi-million bag deficits as severe weather disruptions in key exporting countries like Brazil and Vietnam restricted supplies to international markets. This scarcity drives up raw material costs, which are often passed on to consumers through higher retail prices. Global trade indexes utilized by organizations like the British Coffee Association reveal that raw green coffee bean costs surged dramatically, heavily compressing gross profit margins for independent roasters and downstream cafes. Logistics disruptions, including shipping delays and port congestion, further exacerbate supply chain instability, leading to inventory shortages. As per research, smaller independent roasters are particularly vulnerable to these fluctuations, lacking the resources to hedge against price risks. The unpredictability of supply makes it difficult for businesses to plan long term strategies and maintain consistent product offerings. Consumers may become frustrated with frequent price hikes or limited availability, potentially reducing loyalty. This environmental and logistical instability creates a challenging operating environment, forcing companies to seek diverse sourcing options and invest in sustainable farming practices to mitigate risks.

MARKET OPPORTUNITIES

Growth of Ready to Drink and Convenience Formats

The growth of ready to drink (RTD) and convenience formats offers a significant opportunity for the United Kingdom coffee market. This caters to busy consumers seeking quick and high quality caffeine solutions. RTD coffee products, including cold brews, nitro coffees, and canned lattes, offer portability and consistency, appealing to on the go lifestyles. Research indicates that the Ready-to-Drink (RTD) coffee market continues to experience significant single to double-digit annual growth, fueled by strong consumer demand for canned iced lattes and cold brew options. This segment benefits from the expansion of distribution channels beyond traditional cafes, including supermarkets, convenience stores, and vending machines. Manufacturers are investing in advanced preservation technologies to maintain freshness and flavor without artificial additives. As per retail scans, premium RTD brands are gaining shelf space, competing with established soft drink giants. The ability to offer functional benefits such as added protein or vitamins further enhances appeal. The rise of e commerce also facilitates direct to consumer sales of subscription based RTD coffee services. This convenience driven trend allows coffee brands to reach new occasions and demographics, expanding market reach beyond the cafe environment. The RTD segment offers substantial growth potential for industry players. They can achieve this by leveraging portability and innovation.

Integration of Technology and Personalized Customer Experience

The integration of technology and personalized customer experience provides a strong prospect for the expansion of the United Kingdom coffee market. This enhances engagement and loyalty through digital innovation. Mobile apps, loyalty programs, and artificial intelligence enable cafes to collect data on consumer preferences and offer tailored recommendations and rewards. Digital implementation tracking shows that the vast majority of major UK coffee chains have deployed dedicated mobile application platforms to streamline consumer checkout and reduce peak-hour congestion. A study shows that customers using loyalty apps spend 20 percent more than non members, driven by personalized offers and incentives. The use of AI driven chatbots and virtual assistants enhances customer support and order accuracy. Consumer polling consistently demonstrates that a massive share of mobile application users highly value pre-ordering functionality specifically for its ability to bypass queues during peak retail windows. The integration of smart kiosks and self service stations also reduces labor costs and streamlines operations. Brands are leveraging data analytics to optimize menu offerings and inventory management, ensuring responsiveness to trends. The creation of digital communities through social media and app based interactions fosters brand advocacy. This technological transformation enables coffee businesses to deliver seamless and personalized experiences, differentiating themselves in a competitive market. By embracing digital tools, companies can build deeper connections with consumers and drive repeat business.

MARKET CHALLENGES

Environmental Sustainability and Waste Management

Environmental sustainability and waste management are slowing down the growth of the United Kingdom coffee market. Consumers and regulators are demanding greater accountability for ecological impact. The widespread use of single use cups, plastic lids, and packaging contributes to significant landfill waste, drawing criticism from environmental groups. According to the House of Commons Environmental Audit Committee, approximately 2.5 billion disposable coffee cups are thrown away in the UK each year, with less than 1 percent being recycled. This statistic has prompted stricter regulations and calls for extended producer responsibility. The Waste and Resources Action Programme (WRAP) highlight that meeting UK Plastics Pact targets requires a systemic shift toward reusable packaging, creating significant regulatory and voluntary pressure for cafes to adopt returnable cup schemes. Compliance with these initiatives requires substantial investment in infrastructure and consumer education. As per sources, the cost of sustainable packaging materials is significantly higher than conventional options, impacting profit margins. Consumers are increasingly aware of greenwashing and expect genuine commitment to sustainability, penalizing brands that fail to meet expectations. The challenge lies in balancing convenience with environmental responsibility without compromising product quality or customer experience. Failure to address these concerns may result in reputational damage and loss of market share to eco friendly competitors. Navigating this complex landscape requires collaborative efforts across the supply chain and innovative solutions to reduce waste and promote circular economy practices.

Labor Shortages and Rising Operational Costs

Labor shortages and rising operational costs are major barriers to the United Kingdom coffee market. This affects service quality and profitability. The hospitality sector faces difficulties in recruiting and retaining skilled staff, including baristas and managers, due to competitive wage demands and changing workforce expectations. UKHospitality and recruitment analyses indicates that over 60% of hospitality businesses report staffing shortages, a deficit that has forced many independent outlets to reduce trading hours and simplify menus. The Office for National Statistics and government policy announcements confirms that operational costs spiked following the 9.8% increase in the National Living Wage in April 2024, placing heavy financial strain on hospitality margins. Energy costs, a significant component of cafe operations, have also surged, adding pressure to budgets. As per the Federation of Small Businesses, small independent cafes are particularly vulnerable to these cost increases, lacking the economies of scale of larger chains. The shortage of skilled baristas affects the consistency and quality of coffee served, potentially damaging brand reputation. Training new staff requires time and resources, further straining operational capacity. The cumulative effect of labor and energy costs forces companies to raise prices, which may dampen consumer demand. Addressing this challenge requires investment in automation, employee benefits, and training programs. The inability to secure a stable and skilled workforce threatens the sustainability of many coffee businesses in the UK.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.35% |

| Segments Covered | By Source, Type, Ingredient Process, By Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Market Leaders Profiled | Nestle UK Ltd, Starbucks Coffee Company, Costa Coffee, Starbucks (US), JDE Peet's (NL), Kraft Heinz (US), Lavazza (IT), Dunkin' (US), Peet's Coffee (US), Tchibo (DE), Illy (IT) |

SEGMENTAL ANALYSIS

By Source Insights

The arabica coffee segment dominated the United Kingdom market and accounted for a 56.7% share in 2025. This dominance of the segment was driven by its superior flavor profile, which is characterized by smoother, sweeter, and more complex notes compared to the harsher taste of Robusta. British consumers have increasingly developed a palate for specialty and premium coffee experiences, driving demand for high quality Arabica beans. According to global trade data from the International Coffee Organization (ICO), Arabica beans account for approximately 60% of world coffee production. In the UK specialty sector, however, market estimates suggest this figure exceeds 80%, as the market heavily prioritizes the complex flavor profiles associated with Arabica. The Specialty Coffee Association (SCA) heavily favor Arabica for its superior cupping scores, leading the vast majority of independent UK specialty cafes to feature it as their primary offering to meet consumer quality expectations. The versatility of Arabica allows for a wide range of brewing methods, from espresso to filter, catering to diverse preferences. As per sources, the perception of Arabica as a premium product justifies higher price points, aligning with the trend towards trading up. The availability of single origin Arabica varieties from regions such as Ethiopia, Colombia, and Kenya enhances the appeal for enthusiasts seeking unique terroir driven flavors. This focus on quality and sensory experience ensures that Arabica remains the dominant source, driving value growth in the market. The cultural shift towards appreciating coffee as a craft beverage further solidifies the preference for Arabica, making it the standard for both home brewers and professional baristas.

The alignment of Arabica coffee with the growing specialty coffee trends significantly reinforces its dominance. The third wave coffee movement emphasizes transparency, sustainability, and direct trade, principles that are predominantly associated with Arabica production. The emphasis on fair trade and organic certifications is more prevalent in the Arabica sector, appealing to socially conscious consumers. As per retail reports, major supermarket chains have expanded their premium Arabica ranges to capture this growing segment. The narrative of supporting smallholder farmers and preserving biodiversity resonates with UK shoppers, enhancing brand loyalty. The educational aspect of specialty coffee, including tasting notes and origin stories, is primarily focused on Arabica varieties, fostering a deeper connection between consumers and the product. This strategic positioning within the specialty landscape ensures that Arabica continues to lead the market, driving innovation and quality standards. The integration of Arabica into lifestyle branding and experiential retail further cements its status as the preferred choice for modern coffee consumers.

The robusta coffee segment is likely to experience the fastest CAGR of 5.2% from 2026 to 2034 due to its extensive use in ready to drink and instant coffee formats. Robusta beans are favored for these applications due to their higher caffeine content, stronger flavor, and lower cost compared to Arabica. Studies indicate that the ready-to-drink (RTD) coffee market is experiencing significant double-digit growth, with many commercial formulations utilizing Robusta beans for their flavor stability and bold taste profile in canned formats. The convenience and affordability of Robusta based products appeal to budget conscious consumers and those seeking a quick caffeine fix. As per sources, the development of high quality freeze dried instant coffees using Robusta has improved perceived value, attracting younger demographics. The resilience of Robusta plants to climate change and pests also ensures a stable supply chain, supporting consistent production. This functional advantage makes Robusta ideal for mass market products, driving volume growth. The expansion of private label instant coffee ranges in supermarkets further boosts demand. Consequently, the practical benefits and economic efficiency of Robusta ensure its rapid growth, particularly in the convenience and value segments of the UK market.

Cost efficiency and widespread blending applications are key drivers accelerating the growth of this segment. Coffee manufacturers often blend Robusta with Arabica to reduce costs while maintaining a strong flavor profile and crema in espresso based drinks. Wholesale commodity indexes report that while Robusta historically trades at a deep discount compared to Arabica, severe weather disruptions in major growing regions have caused massive price surges, squeezing the traditional cost advantages enjoyed by large-scale producers. In the UK, many mainstream coffee chains and supermarket brands utilize Robusta blends to offer competitive pricing without compromising on strength. The ability of Robusta to provide a consistent and robust taste makes it ideal for automated vending machines and office coffee services. The rise of value oriented retail channels during economic uncertainty further supports the adoption of Robusta based products. Manufacturers are investing in improved processing techniques to enhance the quality of Robusta, reducing bitterness and improving acceptability. This focus on affordability and functional performance ensures that Robusta continues to expand rapidly, capturing a significant share of the mass market.

By Type Insights

In 2025, the instant coffee segment held the majority share of 32.5% of the regional market because of its unparalleled convenience and deeply established household habit. The fast paced lifestyle of British consumers favors quick preparation methods, making instant coffee the default choice for morning routines and office breaks. According to the British Coffee Association, instant coffee remains uniquely dominant in the region, accounting for approximately 70% to 80% of all coffee prepared and consumed in UK homes. The widespread availability of instant coffee in all retail formats, from supermarkets to convenience stores, ensures accessibility. As per research, the longevity of instant coffee brands has built strong consumer trust and loyalty over decades. The ability to prepare a cup without specialized equipment appeals to a broad demographic, including students and elderly individuals. The portability of instant coffee sachets also supports on the go consumption. This structural advantage ensures that instant coffee remains the dominant type, driving consistent volume sales. The resilience of this segment during economic downturns, as consumers trade down from cafe purchases, further solidifies its leadership. The continuous innovation in freeze dried technologies has also improved quality, retaining existing users while attracting new ones.

The affordability and strong value proposition of instant coffee further reinforce its leading position in the UK market. Compared to fresh ground or whole bean coffee, instant coffee offers a lower cost per cup, appealing to budget conscious consumers. According to the Office for National Statistics, food and beverage inflation has driven shoppers to seek cost effective alternatives, boosting instant coffee sales. Data from retail scans shows that private label instant coffee ranges have gained significant market share, offering competitive prices without sacrificing basic quality. The long shelf life of instant coffee reduces waste and allows for bulk purchasing, enhancing economic efficiency for households. Major brands frequently offer promotions and multi pack deals, driving volume and encouraging stockpiling. The perception of instant coffee as a practical and economical choice ensures its dominance in the mass market. The ability to control portion sizes also helps consumers manage spending. This economic advantage makes instant coffee a resilient category, maintaining its lead despite the growth of premium segments. The combination of low entry cost and high convenience ensures that instant coffee remains the backbone of the UK home coffee market.

The whole bean coffee segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 7.8% during the forecast period owing to the rise of home brewing and increased ownership of specialty equipment. Consumers are investing in high quality grinders, espresso machines, and pour over setups, seeking to replicate cafe experiences at home. The ability to grind beans immediately before brewing preserves aromatic compounds, enhancing the sensory experience. As per sources, online subscriptions for freshly roasted whole beans have gained popularity, offering convenience and variety. The educational aspect of home brewing, supported by online tutorials and communities, encourages experimentation with different origins and roast profiles. This trend towards craftsmanship and personalization drives the rapid growth of the whole bean segment. The perception of whole bean coffee as a premium and authentic product appeals to discerning consumers. Consequently, the combination of equipment adoption and desire for quality ensures that whole bean coffee continues to expand rapidly.

The perception of freshness and quality superiority significantly propels the expansion of this segment. Consumers increasingly associate whole beans with higher quality and artisanal value, distinguishing them from pre ground alternatives. According to studies, the oxidation process in ground coffee leads to flavor degradation, prompting knowledgeable buyers to choose whole beans for optimal taste. The transparency of sourcing and roasting dates on whole bean packaging enhances trust and appeal. As per consumer feedback, the ritual of grinding beans adds to the overall enjoyment and mindfulness of the coffee experience. Major roasters are highlighting the provenance and processing methods of their whole bean offerings, attracting connoisseurs. The availability of diverse single origin whole beans in specialty stores and online platforms expands choices. This focus on quality and authenticity ensures that whole bean coffee remains the fastest growing segment, capturing the attention of enthusiasts and casual drinkers alike. The continuous education on flavor profiles and brewing techniques further supports this growth trajectory.

By Ingredient Process Insights

The caffeinated segment led the United Kingdom coffee market and captured a substantial share in 2025. This leading position of the segment was attributed to the cultural dependence on caffeine for energy, focus, and social stimulation. Coffee is primarily consumed as a functional beverage to combat fatigue and enhance productivity, particularly among working professionals and students. According to the British Coffee Association, 95 million cups of coffee are consumed daily in the UK, with the vast majority containing caffeine. The widespread acceptance of caffeine as a safe and effective stimulant supports consistent demand. As per studies, the morning coffee routine is a deeply ingrained habit for millions of Britons, driving daily sales. The availability of caffeinated options across all formats, from instant to espresso, ensures accessibility. The social aspect of coffee consumption, often centered around caffeinated beverages in cafes, further reinforces its dominance. This functional and social utility ensures that caffeinated coffee remains the default choice, sustaining high volume consumption. The lack of viable alternatives that offer the same immediate energy effect maintains its leadership. Consequently, the reliance on caffeine for daily functioning secures the leading position of this segment in the UK market.

The broad availability and standard menu offerings of caffeinated coffee further cement its dominance. Virtually every cafe, restaurant, and retail outlet prioritizes caffeinated options, making them the most accessible choice for consumers. Data from retail scans shows that caffeinated coffee products occupy the majority of shelf space in supermarkets, reflecting higher turnover rates. The marketing and branding of coffee largely focus on the energizing effects of caffeine, reinforcing its appeal. The consistency in taste and availability across brands builds consumer confidence. The integration of caffeinated coffee into workplace culture and social gatherings ensures continuous demand. This ubiquity and standardization make caffeinated coffee the norm, driving sustained market leadership. The economic incentive for retailers to stock primarily caffeinated products due to higher sales volume further supports this dominance. Thus, the pervasive presence and cultural normalization of caffeinated coffee ensure its continued supremacy in the UK market.

The decaffeinated coffee segment is expected to exhibit a noteworthy CAGR of 6.5% between 2026 and 2034. This quick surge of the segment is fuelled by health consciousness and trends towards reduced caffeine intake. Consumers are increasingly aware of the potential negative effects of excessive caffeine, such as anxiety and sleep disruption, leading them to seek alternatives. The improvement in decaffeination processes, such as the Swiss Water Method, has enhanced the taste and quality of decaf options, making them more appealing. The perception of decaf as a healthier choice without compromising on the coffee experience drives adoption. The rise of evening coffee consumption, where caffeine is avoided, also boosts demand. This health driven shift ensures that decaffeinated coffee continues to grow rapidly, capturing a larger share of the market. The continuous innovation in flavor preservation supports this expansion.

The expansion of premium decaffeinated options in the hospitality sector significantly accelerates the growth of this segment. Cafes and restaurants are increasingly offering high quality decaffeinated espresso and filter coffee to cater to diverse customer needs. The marketing of decaf as a sophisticated and viable choice rather than a compromise enhances its appeal. Major coffee chains have invested in better decaf beans and training for baristas to ensure quality. This focus on quality and inclusivity ensures that decaffeinated coffee remains the fastest growing segment, attracting health conscious and sensitive consumers. The normalization of decaf in social settings further supports its growth. The continuous improvement in quality and availability drives this positive trend.

COUNTRY ANALYSIS

United Kingdom Coffee Market Analysis

The United Kingdom was the top performer in the European coffee market and accounted for a noteworthy share in 2025. It is a significant but distinct player in the European landscape. The country’s market is a mature and highly developed landscape, with one of the highest per capita consumption rates in Europe. According to the British Coffee Association, approximately 98 million cups of coffee are consumed daily in the UK, a figure that has risen from 95 million in 2018. The market is driven by a strong tradition of cafe culture and increasing home brewing trends. Data from the Office for National Statistics (ONS) confirms the hospitality sector's substantial economic contribution, while industry bodies like the British Coffee Association highlight coffee shops as a vital growth driver within this sector. Consumer preferences are shifting towards specialty and sustainable options, influencing manufacturer strategies. The rise of remote work has boosted daytime cafe visits, supporting revenue growth. Regulatory frameworks regarding sustainability and labeling are strict, ensuring transparency. The presence of major global and local brands creates a competitive environment that drives innovation. Economic factors such as inflation impact purchasing behavior, yet demand remains resilient due to the habitual nature of coffee consumption. The integration of digital channels enhances accessibility and engagement. This dynamic interplay of tradition, innovation, and regulatory compliance ensures that the UK remains a vibrant and strategically important market for coffee producers worldwide. The continuous evolution of consumer tastes and technological advancements supports sustained market development.

COMPETITIVE LANDSCAPE

The competition in the UK coffee market is intense and characterized by a mix of global chains independent specialty cafes and retail brands. Major players compete on brand recognition location convenience and digital engagement while independent shops differentiate through unique atmospheres and artisanal quality. Price sensitivity varies across segments with value oriented chains gaining traction during economic pressure. Premium and specialty coffees command higher margins by appealing to discerning consumers seeking quality and ethical sourcing. The rise of at home brewing solutions adds another layer of competition forcing out of home providers to enhance experiential value. Retailers play a pivotal role in shaping competitive dynamics through private label offerings and promotional strategies. Innovation in sustainability and digital services is increasingly important for brand differentiation. Regulatory changes regarding environmental standards also impact competitive strategies. Companies must balance cost efficiency with value addition to retain market share. The market continues to evolve with shifting consumer preferences towards convenience health and responsibility driving strategic decisions and competitive positioning among key participants in the region.

KEY MARKET PLAYERS

A few of the market players that are dominating the UK coffee market are

- Nestle UK Ltd

- Starbucks Coffee Company

- Costa Coffee

- Starbucks (US)

- JDE Peet's (NL)

- Kraft Heinz (US)

- Lavazza (IT)

- Dunkin' (US)

- Peet's Coffee (US)

- Tchibo (DE)

- Illy (IT)

Top Players In The Market

- Starbucks Coffee Company maintains a significant presence in the United Kingdom through its extensive network of company operated and licensed stores. The brand is renowned for its consistent customer experience and strong loyalty program which drives repeat visits. Recently Starbucks has focused on enhancing its digital capabilities by expanding mobile ordering and delivery services to meet changing consumer habits. The company actively invests in sustainability initiatives such as reducing single use plastics and sourcing ethically certified coffee beans. These efforts align with growing environmental consciousness among British consumers. Starbucks also introduces seasonal beverages and localized menu items to engage customers and drive footfall. Its strategic partnerships with food delivery platforms further extend its reach. Starbucks strengthens its brand loyalty and competitive position in the dynamic UK coffee landscape. It achieves this by prioritizing convenience and ethical practices.

- Costa Coffee is a dominant force in the UK market recognized for its widespread high street presence and diverse product offerings. As a homegrown brand it holds a special place in British coffee culture. Recently Costa has accelerated its expansion into non traditional locations such as transport hubs and retail parks to increase accessibility. The company has invested heavily in automation technology including self service kiosks to improve efficiency and reduce wait times. Costa also focuses on sustainability by introducing recyclable cups and committing to carbon neutral operations. Its loyalty app enhances customer engagement through personalized rewards and offers. The brand continues to innovate its food menu to complement its coffee range. These strategic moves reinforce its market leadership by adapting to modern consumer preferences for speed convenience and environmental responsibility.

- Nestle UK Ltd plays a crucial role in the UK coffee market primarily through its Nescafe and Nespresso brands. The company dominates the at home consumption segment with a wide variety of instant and capsule products. Recently Nestle has focused on premiumization by expanding its Nespresso boutique network and offering high quality single origin coffees. The company actively promotes sustainability through its AAA Sustainable Quality Program which supports farmers and protects the environment. Nestle also invests in digital marketing and e commerce platforms to reach direct consumers. Its innovation in plant based coffee alternatives addresses growing health and dietary trends. Nestlé maintains a robust position in both the retail and hospitality sectors by leveraging its strong distribution network and brand portfolio. Consequently, this ensures continued relevance and growth in the UK market.

Top Strategies Used By Key Market Participants

Key players in the UK coffee market employ diverse strategies to maintain competitiveness and drive growth. Digital transformation is a primary focus with companies investing in mobile apps and loyalty programs to enhance customer engagement. Sustainability initiatives such as ethical sourcing and waste reduction are central to brand positioning. Product innovation includes expanding plant based options and premium single origin offerings. Expansion into non traditional locations like transport hubs increases accessibility. Strategic partnerships with delivery platforms extend reach and convenience. Automation through self service kiosks improves operational efficiency. Personalized marketing driven by data analytics enhances customer retention. These strategies collectively strengthen market presence and adapt to evolving consumer preferences for convenience quality and environmental responsibility in the United Kingdom.

MARKET SEGMENTATION

This research report on the UK coffee market is segmented and sub-segmented into the following categories.

By Source

- Arabica

- Robusta

By Type

- Instant Coffee

- Ground Coffee

- Whole Bean

- Others

By Process

- Caffeinated

- Decaffeinated

By Country

- London

- South East

- North West

- East of England

- South West

- Scotland

- West Midlands

- Yorkshire and The Humber

- East Midlands

- Others

Frequently Asked Questions

Why is the UK coffee market continuing to grow despite its maturity?

The market is expanding due to rising specialty coffee consumption, growing café culture, premiumization, and increasing demand for convenient coffee products.

What is driving coffee consumption across the UK?

Busy lifestyles, changing consumer preferences, growing at-home brewing, and strong demand for premium and ethically sourced coffee are driving consumption.

Which coffee type accounts for the largest share of the UK coffee market?

Arabica coffee holds the largest market share due to its smooth flavor, premium quality, and widespread use in specialty and retail coffee products.

How is specialty coffee influencing the UK coffee market?

Specialty coffee is driving premium product demand, encouraging artisanal roasting, and attracting consumers seeking unique flavors and high-quality coffee experiences.

What factors are driving the growth of the UK coffee market?

Increasing café visits, expanding online coffee sales, rising demand for ready-to-drink coffee, and growing consumer interest in sustainable sourcing are fueling market growth.

Which distribution channels generate the highest sales in the UK coffee market?

Supermarkets, hypermarkets, cafés, coffee shops, convenience stores, online retailers, and specialty stores account for the highest coffee sales.

What trends are shaping the future of the UK coffee market?

Premium coffee, single-origin beans, functional coffee, plant-based coffee beverages, sustainable packaging, and subscription-based coffee services are shaping the market.

How are coffee brands innovating to meet changing consumer preferences?

Manufacturers are introducing specialty blends, eco-friendly packaging, ready-to-drink products, low-sugar formulations, and ethically sourced coffee offerings.

What challenges could affect the growth of the UK coffee market?

Volatile coffee bean prices, climate-related supply risks, inflation, changing consumer spending patterns, and increasing operating costs could affect market growth.

Who are the primary consumers in the UK coffee market?

Households, office workers, students, cafés, restaurants, hotels, and foodservice operators are the primary consumers of coffee products.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com