UK Commercial Real Estate Market Size, Share, Trends & Growth Forecast Report By Product Type, Business Model, End User, and Country – Industry Analysis and Forecast, 2026 to 2034

UK Commercial Real Estate Market Report Summary

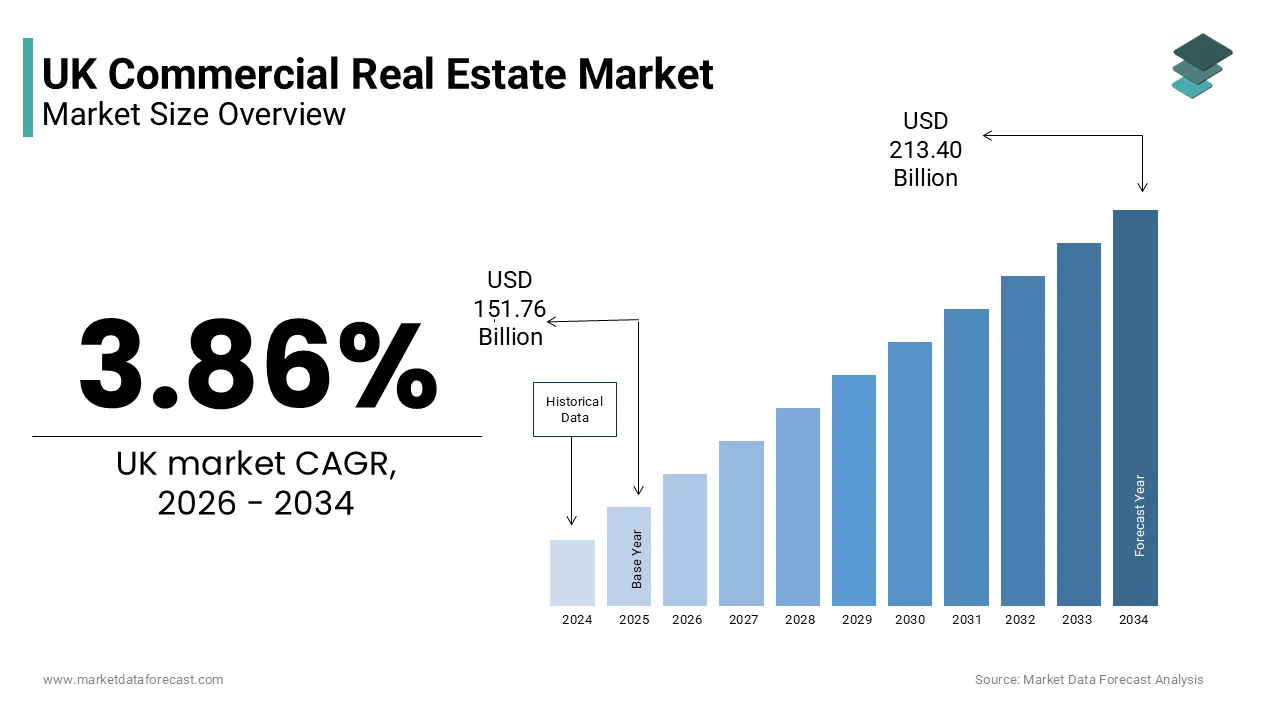

The UK commercial real estate market was valued at USD 151.76 billion in 2025, is estimated to reach USD 157.62 billion in 2026, and is projected to reach USD 213.40 billion by 2034, growing at a CAGR of 3.86% during the forecast period. Market growth is driven by increasing demand for logistics and industrial facilities, expanding e commerce activities, and rising investments in income generating real estate assets. The market continues to benefit from the United Kingdom's strong business environment, established financial sector, and ongoing urban development projects. Growing adoption of flexible leasing models, smart building technologies, and sustainable property development practices is further supporting market expansion.

Key Market Trends

- Growing demand for logistics and warehousing facilities is driving market growth.

- Increasing e commerce penetration is boosting demand for industrial and distribution properties.

- Rising adoption of sustainable and energy efficient commercial buildings is supporting industry development.

- Expansion of flexible workspace and hybrid business models is enhancing market opportunities.

- Innovation in proptech solutions, digital property management, and smart building technologies is influencing market advancement.

Segmental Insights

- Based on property type, the logistics and industrial real estate segment accounted for 28.5% of the UK commercial real estate market share in 2025. This dominance is attributed to growing warehousing requirements, supply chain optimization efforts, and expanding online retail activities.

- Based on business model, the rental model segment held 35.6% of the UK commercial real estate market share in 2025, driven by strong tenant demand, stable recurring income streams, and increasing preference for flexible occupancy arrangements.

- Based on end user, the corporates and small and medium sized enterprises (SMEs) segment accounted for the largest share of the UK commercial real estate market in 2025, supported by continuous demand for office, industrial, and mixed use commercial spaces.

Regional Insights

- The United Kingdom accounted for 23.7% of the European commercial real estate market share in 2025 and maintained a leading position within the region. Strong institutional investment activity, a mature property market, and ongoing infrastructure development continue to support market growth.

Competitive Landscape

The UK commercial real estate market is highly competitive, with property developers, real estate investment trusts, and proptech companies focusing on portfolio expansion, sustainability initiatives, and digital transformation to strengthen their market position. Market participants continue to invest in logistics assets, mixed use developments, and technology enabled property management solutions. Key companies operating in the UK commercial real estate market include Land Securities Group PLC, Segro PLC, British Land, Derwent London, Hammerson, Capital & Counties Properties PLC, Shaftesbury PLC, Tritax Big Box REIT PLC, Unite Group PLC, Wayhome, AskPorter, Landbay, Thirdfort, and RentProfile.

UK Commercial Real Estate Market Size

The UK commercial real estate market size was valued at USD 151.76 billion in 2025, and is projected to reach USD 213.40 billion by 2034 from USD 157.62 billion in 2026, growing at a CAGR of 3.86%.

Commercial Real Estate (CRE) refers to properties used exclusively for business activities or income generation. This market is characterized by its strategic importance to the national economy facilitating trade employment and urban development. The sector is deeply influenced by macroeconomic indicators demographic shifts and technological advancements. According to the Office for National Statistics the service sector accounts for approximately 80 percent of the UK economy driving demand for modern office spaces in major hubs like London Manchester and Birmingham. As per the British Property Federation (BPF) and CoStar, global capital drives a significant portion of UK commercial real estate investment, with international buyers, led by the United States, accounting for over one-quarter of all property investment volumes in recent years. Regulatory frameworks such as the Energy Performance Certificate requirements mandate strict sustainability standards influencing building valuations and retrofitting needs. Data highlights that roughly 60% of commercial buildings are rented property, meaning owners must actively upgrade them to satisfy tightening Minimum Energy Efficiency Standards (MEES) as part of the UK’s broader target to reach net-zero carbon by 2050. The rise of e commerce has transformed logistics requirements with last mile delivery facilities becoming critical assets. Urban regeneration projects supported by local councils further stimulate development activity. The market operates within a complex legal environment governed by leasehold reforms and planning permissions. Investor sentiment is closely tied to interest rate movements and inflation trends. This dynamic landscape requires stakeholders to navigate evolving tenant expectations regulatory pressures and economic volatility to maintain asset value and occupancy levels.

MARKET DRIVERS

Expansion of E Commerce and Logistics Infrastructure

The rapid expansion of e-commerce is a primary driver for the United Kingdom commercial real estate market. This growth is particularly concentrated within the industrial and logistics sectors. Consumer shifting towards online shopping has necessitated a robust network of warehouses distribution centers and last mile delivery hubs. According to the Office for National Statistics online retail sales accounted for 27 percent of total retail spending in 2024 creating sustained demand for storage and fulfillment spaces. This trend has led to a surge in construction of large scale logistics parks near major transport arteries and urban centers. Studies indicate that while immediate industrial take-up cooled following pandemic-era spikes, underlying demand for logistics space remains heavily supported by growing e-retail and third-party logistics requirements. The need for faster delivery times has driven the development of smaller urban fulfillment centers reducing vacancy rates in suburban areas. As per sources, the average size of new logistics developments has grown to accommodate automated sorting systems and higher ceiling heights. The scarcity of prime logistics land in key regions like the Midlands and South East has pushed rental yields higher attracting institutional investors. Government infrastructure investments in road and rail networks further enhance the attractiveness of these locations. This structural shift in retail behavior ensures long term demand for industrial real estate making it a resilient and high growth segment within the broader commercial market.

Corporate Focus on Environmental Social and Governance Standards

The increasing corporate focus on Environmental Social and Governance standards fuels demand for high quality sustainable office spaces in the United Kingdom commercial real estate market. Companies are prioritizing offices that align with their sustainability goals and enhance employee well being to attract top talent. Climate tracking registries note that nearly all FTSE 100 companies have committed to reaching net-zero carbon emissions, predominantly tracking toward the [official UK target of 2050, which heavily dictates corporate real estate strategies and leasing mandates. This has created a flight to quality where tenants prefer buildings with strong Energy Performance Certificate ratings such as A or B. Data from the Royal Institution of Chartered Surveyors shows that prime offices with green certifications command rental premiums of up to 10 percent compared to non compliant properties. Landlords are responding by investing heavily in retrofitting existing stock with energy efficient systems smart building technologies and biophilic design elements. Backed by advocacy from organizations like the UK Green Building Council, new developments must adhere to tightening statutory UK building regulations to enforce future-proofing, carbon reduction, and energy efficiency. The demand for healthy workplaces featuring improved air quality natural light and wellness amenities has become a key differentiator. This trend is particularly pronounced in London and other major cities where competition for skilled workers is intense. The alignment of real estate strategies with corporate sustainability targets ensures that green buildings remain in high demand driving redevelopment activity and enhancing asset values across the sector.

MARKET RESTRAINTS

High Interest Rates and Financing Costs

High interest rates and elevated financing costs are a major restraint to the United Kingdom commercial real estate market. This limits investment activity and development pipelines. The Bank of England raised base rates to combat inflation increasing the cost of borrowing for developers and investors. According to the Bank of England, the base rate began a gradual descent in late 2024 and early 2025 from its 5.25% peak, offering mild relief to leveraged transactions but keeping baseline borrowing costs high relative to historical norms. This has led to a widening of yield spreads between government bonds and commercial property reducing the attractiveness of real estate as an investment class. Commercial market trackers like MSCI Real Assets show that UK commercial property transaction volumes dropped significantly following macroeconomic headwinds, as buyers adopted a cautious "wait-and-see" approach amidst shifting interest rate expectations. Higher mortgage rates also affect tenant affordability leading to slower lease renewals and increased vacancy risks. As per sources, many development projects have been paused or cancelled due to unfavorable financing conditions impacting future supply. The uncertainty surrounding future rate cuts creates hesitation among institutional investors who require stable returns. Lenders have tightened credit criteria requiring higher equity contributions which restricts access to capital for smaller players. This financial constraint slows down market liquidity and price discovery forcing sellers to adjust expectations. The prolonged period of high borrowing costs suppresses growth and limits the ability of market participants to capitalize on emerging opportunities.

Regulatory Uncertainty and Planning Delays

Regulatory uncertainty and prolonged planning delays impose significant constraints on the United Kingdom commercial real estate market. This hinders project timelines and increases costs. The complexity of the planning system and frequent changes in local policies create unpredictability for developers and investors. According to the Ministry of Housing Communities and Local Government the average time to secure planning permission for major commercial projects exceeds 12 months causing substantial delays. This bureaucratic inefficiency increases holding costs and exposes projects to market volatility during the approval process. Data from the British Property Federation highlights that roughly 90% of developers cite planning system delays and unpredictability as a primary barrier to new construction and real estate development. Changes in building safety regulations following recent high profile incidents have added further compliance burdens and costs. As per a study, the introduction of new safety checks and certification requirements has extended project timelines by several months. The lack of clarity regarding future tax policies such as business rates reforms also discourages long term investment commitments. Local authorities often face resource constraints leading to inconsistent decision making and appeals. This regulatory friction reduces the efficiency of the market and deters foreign investment. The inability to predict approval outcomes or timelines makes risk management challenging for stakeholders. These systemic issues constrain supply responsiveness and limit the market's ability to adapt to changing demand dynamics effectively.

MARKET OPPORTUNITIES

Retrofitting and Asset Repurposing Initiatives

Retrofitting and asset repurposing offer key opportunities in the UK commercial real estate market. Stakeholders are using these methods to enhance sustainability and adapt to changing usage patterns. Older office and retail buildings are being transformed into mixed use spaces residential units or modern workspaces to meet current demands. According to the Royal Institution of Chartered Surveyors retrofitting existing stock can reduce carbon emissions by up to 50 percent compared to new construction offering a viable path to net zero. This approach aligns with government incentives and regulatory pressures promoting circular economy principles. Driven by tightening statutory requirements to achieve higher Energy Performance Certificate (EPC) ratings, property analysis indicates a massive increase in capital expenditure by UK landlords upgrading and refurbishing older commercial assets to avoid obsolescence. The conversion of obsolete retail spaces into leisure entertainment or community hubs revitalizes town centers and attracts footfall. As per research, adaptive reuse projects often qualify for tax relief and grants enhancing financial viability. The demand for flexible workspaces has driven the transformation of traditional offices into collaborative environments with shared amenities. This trend allows owners to extend the life of assets and capture higher rents from upgraded properties. The focus on sustainability and functionality creates value for investors while addressing environmental concerns. By leveraging existing structures the market can meet evolving tenant needs without the environmental cost of new builds. This strategic shift towards renovation offers a sustainable and profitable avenue for growth.

Growth of Life Sciences and Data Center Real Estate

The growth of life sciences and data center real estate provides substantial prospects in the United Kingdom commercial real estate market. This is driven by technological advancement and healthcare innovation. The UK has emerged as a global hub for biotechnology and pharmaceutical research creating demand for specialized laboratory and office spaces. According to the Association of the British Pharmaceutical Industry, the UK life sciences sector contributes more than £40 billion annually to the economy, driving aggressive real estate competition for highly technical, purpose-built laboratory and containment facilities. Clusters in Cambridge Oxford and London attract significant investment in high specification buildings with advanced ventilation and safety systems. Simultaneously the explosion of digital services and artificial intelligence has spurred demand for data centers. Research shows that the UK data center market is expanding rapidly, with overall IT load capacity projected to grow at an annual rate exceeding 15% through the decade, fueled primarily by intense demand for hyperscale AI infrastructure. These facilities require robust power infrastructure and connectivity making them attractive long term investments. As per sources, institutional investors are increasingly allocating capital to these alternative asset classes due to their resilience and high barriers to entry. The government support for digital infrastructure and scientific research further boosts confidence. The convergence of technology and real estate creates niche opportunities for developers who can deliver specialized solutions. This diversification beyond traditional office and retail sectors provides stability and growth potential in a changing market landscape.

MARKET CHALLENGES

Obsolescence of Secondary Office Stock

The obsolescence of secondary office stock is challenging the growth of the United Kingdom commercial real estate market. This is happening because tenant preferences are shifting towards high-quality, sustainable spaces. Older buildings with poor energy efficiency and outdated layouts struggle to attract tenants leading to higher vacancy rates and rental depreciation. Data from agencies like Savills shows that Central London office vacancy rates stood at approximately 7.5% to 8.8% in 2024, characterized by a sharp polarization where prime Grade A vacancy remained low (approx. 4-5%) while secondary assets faced significantly weaker demand. Tenants increasingly prioritize buildings with modern amenities smart technology and green credentials leaving older properties behind. Industry analysis highlights that retrofitting secondary stock requires massive capital expenditure, with fit-out costs rising by approximately 14% annually in recent years, often creating a viable financial case only when balanced against the significant "brown discount" (value reduction) applied to non-compliant buildings. The lack of demand for substandard offices creates stranded assets that may lose significant value or become uninvestable. As per studies, the cost of compliance with new environmental regulations further exacerbates the challenge for landlords of older buildings. The flight to quality trend intensifies competition for prime spaces while leaving secondary markets vulnerable. This bifurcation creates instability in portfolio valuations and complicates refinancing efforts. Owners face difficult decisions regarding divestment redevelopment or acceptance of lower returns. The inability to upgrade efficiently threatens the long term viability of a significant portion of the office stock. Addressing this challenge requires innovative financing and strategic planning to prevent widespread asset devaluation.

Supply Chain Disruptions and Construction Cost Inflation

Supply chain disruptions and construction cost inflation are also significant hurdles to the United Kingdom commercial real estate market. This impacts development feasibility and project delivery. Global logistical bottlenecks and material shortages have led to volatile prices for key construction inputs such as steel cement and glass. These cost escalations delay project completion and force revisions to financial models affecting viability. Data from the Royal Institution of Chartered Surveyors (RICS) shows that while skills shortages and financial constraints were reported by roughly 50% of firms in 2024, issues with material availability had eased notably compared to the supply chain crises of previous years. Labor shortages in the skilled trades sector further compound the problem driving up wages and extending timelines. As per sources, the uncertainty surrounding supply chains makes it difficult to fix contract prices increasing risk for both developers and contractors. The inflationary environment erodes the value of fixed price contracts and leads to disputes over variations. This instability discourages new starts and slows down the delivery of much needed commercial space. The cumulative effect of higher costs and delays reduces the overall efficiency of the development pipeline. Stakeholders must navigate these complexities through careful risk management and flexible contracting strategies. The persistent nature of these supply side issues remains a critical hurdle for market growth and stability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.86% |

| Segments Covered | By Product Type, Business Model, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, and East Midlands |

| Market Leaders Profiled | Land Securities Group PLC, Segro PLC, British Land, Derwent London, Hammerson, Capital & Counties Properties PLC, Shaftesbury PLC, Tritax Big Box REIT PLC, Unite Group PLC, Wayhome, AskPorter, Landbay, Thirdfort, and RentProfile |

SEGMENTAL ANALYSIS

By Property Type Insights

The logistics and industrial real estate segment dominated the United Kingdom commercial real estate market and accounted for a 28.5% share in 2025. This dominance of the segment was driven by the sustained expansion of e commerce and the strategic need for supply chain resilience. The shift in consumer behavior towards online shopping has created an insatiable demand for warehousing and distribution facilities to handle increased parcel volumes. According to the Office for National Statistics online retail sales consistently account for over 25 percent of total retail spending necessitating extensive storage infrastructure. This structural change has led to a surge in demand for modern logistics hubs particularly in key regions like the Midlands and the South East. Commercial property trackers show that UK logistics take-up stabilized in 2024 following previous historic highs, keeping national supply steady with average prime vacancy rates hovering around 5% to 6.5%. The need for faster delivery times has prompted retailers to invest in last mile distribution centers closer to urban populations. As per sources, the average size of new logistics developments has increased to accommodate automated sorting technologies and higher inventory levels. The scarcity of developable land near major transport networks has further intensified competition among tenants driving rental growth. Government investments in infrastructure such as road and rail improvements support the efficiency of these logistics networks. This robust demand profile ensures that the logistics sector remains the most resilient and dominant component of the commercial real estate market providing stable yields for investors amidst economic uncertainty.

The requirement for operational efficiency and advanced automation capabilities significantly drives the dominance of this segment. Modern supply chains rely heavily on technology to optimize inventory management and reduce labor costs leading to a preference for high specification buildings. Driven by the push for operational efficiency, global warehousing analyses show that approximately 60% of logistics operations are escalating investments in advanced automation and robotics, directly requiring modern buildings with higher internal clear heights and enhanced floor load capacities. Property research from Savills reveals that best-in-class, energy-efficient logistics assets can command average rental premiums reaching up to 55% over older, non-compliant secondary stock. The transition towards just in time manufacturing and distribution models necessitates reliable and efficient storage solutions that minimize downtime. As per research, the integration of smart building systems allows for real time monitoring of energy usage and security enhancing operational performance. Tenants are increasingly prioritizing sustainability with many seeking buildings that meet high environmental standards to align with corporate net zero goals. Industry bodies like the UK Warehousing Association note that energy-efficient warehouses dramatically reduce baseline utility outlays, making sustainable properties highly sought after by cost-conscious, carbon-reduction-focused businesses. This focus on technological advancement and sustainability ensures that modern industrial real estate remains in high demand. The inability of older facilities to support these advanced operations creates a clear divide in the market reinforcing the dominance of new high quality logistics properties.

The life sciences real estate is the fastest growing segment is predicted to witness the highest CAGR of 8.5% from 2026 to 2034 due to substantial government investment and the emergence of innovation clusters. The UK government has identified life sciences as a key sector for economic growth leading to targeted funding for research and development infrastructure. According to the Department for Business and Trade, the thriving UK life sciences sector generates over £94 billion in annual turnover, heavily stimulating commercial investment in highly specialized laboratory, incubator, and office infrastructure. Established clusters in Cambridge Oxford and London attract significant capital from pharmaceutical companies and biotech startups seeking collaborative environments. Data from JLL indicates that following a post-pandemic peak, occupier demand for life sciences real estate stabilized in 2024 as companies focused on capital preservation, though long-term requirements for core innovation clusters remain robust. The concentration of world class universities and research institutions in these regions fosters innovation and talent acquisition making them ideal locations for industry players. As per a study, the development of dedicated science parks with shared facilities and regulatory support further accelerates growth. The availability of venture capital for biotech firms enables rapid expansion and leasing activity. This ecosystem of support and collaboration ensures that life sciences real estate continues to expand rapidly. The strategic importance of health and pharmaceutical research post pandemic has further heightened interest in this sector attracting both domestic and international investors seeking long term growth opportunities.

The need for specialized infrastructure and the high barriers to entry in life sciences real estate contribute to its rapid growth and premium valuation. Laboratories require complex mechanical electrical and plumbing systems including advanced ventilation waste disposal and safety protocols that are not found in standard office buildings. Property cost analyses indicate that constructing life sciences facilities can require capital expenditures higher than traditional premium offices due to strict requirements for advanced MEP infrastructure, vibration controls, and specialized ventilation. This complexity limits the supply of suitable properties creating a scarcity value that drives rental growth. Data from CBRE shows that vacancy rates for life sciences assets remain below 2 percent in key hubs reflecting the intense demand for compliant spaces. Tenants often enter into long term leases to secure these specialized facilities providing stability for landlords. As per sources, the rigorous regulatory environment means that once a facility is approved it retains its value and utility for extended periods. The difficulty in converting existing stock into laboratories further restricts supply enhancing the attractiveness of purpose built developments. Investors are drawn to this segment due to its resilience and potential for high yields. The combination of technical specificity and limited availability ensures that life sciences real estate remains the fastest growing and most dynamic sector in the UK commercial property market.

By Business Model Insights

In 2025, the rental model segment captured a 35.6% share to lead the United Kingdom commercial real estate market. This leading position of the segment is attributed to its ability to offer flexibility and capital preservation for businesses facing economic uncertainty. Leasing allows companies to occupy prime locations without the substantial upfront capital required for purchase freeing resources for core business activities. Surveys confirm that the vast majority of small and medium-sized enterprises (SMEs) lease rather than own commercial premises, primarily to preserve working capital liquidity and maintain operational flexibility. This preference is particularly strong in the retail and office sectors where location flexibility is crucial for customer access and talent recruitment. Data from the Royal Institution of Chartered Surveyors indicates that the majority of commercial transactions involve lease agreements rather than freehold sales. The ability to negotiate lease terms such as break clauses and rent reviews provides tenants with risk management tools against economic volatility. As per research, short term leases have become more common allowing businesses to adjust their footprint in response to performance trends. Landlords benefit from steady income streams and the ability to retain asset ownership for long term appreciation. The regulatory framework governing commercial leases provides clarity and protection for both parties encouraging widespread adoption. This mutual benefit ensures that the rental model remains the dominant method of occupying commercial property in the UK. The trend towards flexible workspaces and serviced offices further reinforces the preference for leasing over ownership.

Investor preference for stable income yield greatly fuels the top position of the rental model. Institutional investors such as pension funds and insurance companies prioritize assets that generate consistent cash flows to meet liability obligations. The predictability of rental income allows for accurate financial modeling and portfolio management. In addition, the transparency of the UK leasing market enhances confidence among international investors who seek reliable income streams. The ability to refinance properties based on rental income further leverages investment potential. This focus on yield stability ensures that the rental model remains the primary structure for commercial real estate investment. The demand for income generating assets sustains high occupancy rates and supports rental growth in prime locations. Thus, the alignment of investor objectives with tenant needs cements the rental model as the cornerstone of the UK commercial property sector.

The sales model segment is estimated to register the fastest CAGR of 6.2% during the forecast period owing to asset optimization and portfolio restructuring strategies. Companies are increasingly selling owned properties to unlock capital and focus on core competencies a trend known as sale and leaseback. According to the Financial Times sale and leaseback transactions in the UK increased by 25 percent in 2024 as businesses sought to improve balance sheets and reduce debt. This strategy allows firms to release trapped equity while retaining operational use of the premises. A study indicates that institutional investors are actively acquiring these assets to expand their portfolios providing liquidity to the sales market. The desire to divest non core assets has led to increased transaction volumes in the retail and office sectors. Also, the current market environment with stabilizing interest rates has encouraged buyers to re enter the market driving sales activity. This strategic shift towards asset light models ensures that the sales segment continues to grow rapidly. The availability of capital from sovereign wealth funds and private equity further supports transaction momentum. Consequently the focus on financial flexibility and capital efficiency propels the sales model as a dynamic and expanding component of the market.

Foreign direct investment and renewed market confidence significantly accelerate the growth of the sales model. International investors view UK property as a safe haven asset class offering stability and long term capital appreciation. Buyers from North America Asia and the Middle East are actively acquiring prime assets in London and regional cities. Data from Savills shows that cross border transactions accounted for 40 percent of total sales volume in the first half of 2025. The transparency and legal robustness of the UK market enhance trust among overseas buyers. Moreover, the perception of the UK as a gateway to European markets despite Brexit continues to attract international capital. This influx of foreign money drives sales volumes and supports price stability. The competitive bidding environment created by global investors ensures that the sales segment remains vibrant and fast growing. The continuous flow of international capital underscores the enduring appeal of UK commercial real estate as a premier investment destination.

By End User Insights

The corporates and small and medium sized enterprises (SMEs) segment held the majority share of the UK commercial real estate market in 2025. It serves as the backbone of the national economy. These entities drive demand for office retail and industrial spaces essential for business operations and employment generation. According to the Office for National Statistics SMEs account for 99 percent of the UK business population and contribute significantly to GDP necessitating diverse property requirements. Data from the Federation of Small Businesses indicates that over 5 million SMEs operate in the UK creating sustained demand for flexible and affordable commercial units. Large corporations anchor prime office markets in major cities providing stability and long term lease commitments. As per a study, the clustering of businesses in urban centers fosters collaboration and innovation enhancing productivity. The need for physical presence for customer interaction and team cohesion maintains demand for office and retail spaces despite digital trends. Government initiatives supporting entrepreneurship and business growth further stimulate property uptake. The resilience of the corporate sector ensures consistent occupancy levels across various property types. This broad base of users provides a stable foundation for the commercial real estate market. The diverse needs of corporates and SMEs drive innovation in property design and leasing structures. Consequently their central role in the economy secures their position as the dominant end user segment.

The operational necessity and the need for brand presence drive the dominance of this segment. Physical locations serve as critical touchpoints for customer engagement service delivery and brand visibility. Corporates utilize flagship offices to project image and attract talent reinforcing the importance of prime locations. SMEs rely on local high street units to build community connections and serve niche markets. The inability to fully replicate these physical interactions online ensures continued demand for commercial space. Businesses invest in fit outs and branding to differentiate themselves driving value addition in the property sector. This strategic use of real estate for operational and marketing purposes sustains the leading position of corporates and SMEs. The ongoing evolution of workplace and retail concepts further reinforces their reliance on physical assets. Thus the functional and symbolic value of commercial property ensures their continued dominance.

The technology and digital services firms segment is anticipated to witness the fastest CAGR of 7.8% between 2026 and 2034. This quick surge of the segment is propelled by digital transformation and adaptation to remote work models. These companies require flexible and technologically advanced spaces to support hybrid working arrangements and collaborative innovation. The need for high speed connectivity meeting rooms and breakout areas shapes their property preferences. Moreover, the concentration of tech hubs in cities like London Manchester and Edinburgh attracts talent and investment fueling leasing activity. The agility of these firms allows them to respond quickly to market changes influencing leasing trends. This dynamic growth ensures that technology and digital services firms become increasingly influential in the commercial property sector. Their preference for sustainable and flexible spaces drives innovation in property development. Consequently their rapid expansion propels them as the fastest growing end user segment.

The emergence of innovation hubs and collaborative ecosystems greatly accelerates the growth of technology and digital services firms as end users. These firms thrive in environments that facilitate networking knowledge sharing and partnership formation. The proximity to academic institutions and research centers enhances access to talent and intellectual property. Tech firms often prioritize locations with vibrant social amenities and transport links to attract skilled workers. The development of specialized tech parks with integrated facilities supports this trend. Investors are responding by creating tailored environments that foster community and innovation. This focus on ecosystem benefits ensures that technology firms continue to expand their real estate footprint rapidly. The synergy between property and productivity enhances their competitive advantage. Thus the strategic value of collaborative spaces propels the growth of this segment in the UK market.

COUNTRY LEVEL ANALYSIS

The United Kingdom was top position was the European market and occupied a 23.7% share in 2025. This growth was supported by its maturity depth and global significance serving as a key hub for international investment. According to the British Property Federation, the total value of UK commercial property assets stands at approximately £883 billion, representing about 13% of the UK's total built environment and reflecting its massive economic footprint. The market is driven by a diverse economy with strong service finance and technology sectors that generate consistent demand for office and industrial spaces. Data from the Office for National Statistics indicates that the service sector accounts for 80 percent of GDP underpinning the need for commercial infrastructure. London remains a global financial center attracting multinational corporations and high value transactions. Regional cities such as Manchester Birmingham and Leeds are experiencing growth due to regeneration projects and improved connectivity. The government’s levelling up agenda aims to redistribute economic activity boosting demand in northern regions. Regulatory frameworks such as the Energy Performance Certificate mandates drive sustainability improvements and retrofitting activity. Foreign investment remains robust with the UK viewed as a stable and transparent market. The resilience of the logistics sector amid e commerce growth provides a counterbalance to office market challenges. This combination of global appeal regional development and regulatory evolution ensures that the UK remains a dynamic and strategically important commercial real estate market. The continuous adaptation to economic and environmental trends sustains its competitive position globally.

COMPETITIVE LANDSCAPE

The competition in the UK commercial real estate market is intense and characterized by a mix of large real estate investment trusts private equity firms and regional developers. Major players compete on asset quality location sustainability credentials and tenant services. The market is segmented by property type with logistics and life sciences experiencing high demand while traditional retail faces structural challenges. Price sensitivity varies across sectors with investors seeking resilient income streams and capital appreciation. The rise of environmental regulations forces competitors to innovate in green building technologies and energy efficiency. Digital platforms enhance transparency and accessibility influencing leasing and investment decisions. Regional disparities create opportunities in emerging hubs outside London driving decentralization trends. Private equity influx increases transaction volumes and valuation pressures. Companies must differentiate through superior asset management and strategic partnerships to retain market share. The shift towards flexible workspaces and experiential retail reshapes competitive dynamics. Adaptability to economic fluctuations and regulatory changes is crucial for sustained success. This dynamic environment fosters continuous innovation and strategic realignment among key participants in the region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the UK commercial real estate market are

- Land Securities Group PLC

- Segro PLC

- British Land

- Derwent London

- Hammerson

- Capital & Counties Properties PLC

- Shaftesbury PLC

- Tritax Big Box Reit PLC

- Unite Group PLC

- Wayhome

- AskPorter

- Landbay

- Thirdfort

- RentProfile

Top Players in the Market

- British Land plc is a leading real estate investment trust in the United Kingdom with a significant portfolio of office and retail assets. The company focuses on creating vibrant places that foster community and economic growth. Recently British Land has accelerated its sustainability agenda by committing to net zero carbon emissions across its operations. It actively invests in retrofitting existing buildings to improve energy efficiency and meet stringent environmental standards. The firm strengthens its market position by developing mixed use schemes in key locations such as London and regional cities. British Land also prioritizes tenant well being through enhanced amenities and flexible workspace solutions. These strategic initiatives enhance asset value and attract high quality occupiers. The company integrates technology and sustainability into its core strategy. Consequently, it maintains a competitive edge and long-term resilience in the dynamic UK commercial property landscape.

- Segro plc is a prominent owner and developer of modern logistics and industrial real estate in the UK. The company plays a crucial role in supporting the e commerce supply chain and last mile delivery networks. Segro strengthens its market position by acquiring strategic land parcels near major urban centers and transport hubs. It focuses on building high specification warehouses equipped with advanced technology and sustainable features. Recently the company has expanded its portfolio through targeted acquisitions and development projects in high demand regions. Segro actively collaborates with customers to design tailored solutions that enhance operational efficiency. Its commitment to environmental responsibility includes investing in renewable energy and biodiversity improvements. These actions ensure that Segro remains a preferred partner for logistics providers and retailers. The company drives growth and maintains its leadership in the UK logistics real estate landscape. It achieves this by delivering innovative and sustainable industrial spaces.

- Landsec is one of the largest commercial property companies in the UK specializing in retail and office destinations. The company manages iconic assets such as Bluewater and Trinity Leeds which serve as community hubs. Landsec strengthens its market position by transforming its portfolio to focus on experiential retail and leisure offerings. It actively invests in placemaking initiatives that enhance visitor experience and drive footfall. Recently the company has prioritized sustainability by achieving high environmental certifications for its properties. Landsec also explores mixed use developments that integrate residential and commercial elements to create vibrant neighborhoods. The firm leverages data analytics to understand consumer behavior and optimize tenant mix. These strategies ensure that its assets remain relevant and attractive in a changing retail landscape. Landsec maintains strong performance in the UK commercial real estate market. This success is achieved by focusing on high-quality assets and active community engagement.

Top Strategies Used by Key Market Participants

Key players in the UK commercial real estate market employ diverse strategies to maintain competitiveness and drive growth. Sustainability is a primary focus with companies investing in net zero carbon initiatives and green building certifications. Asset optimization through retrofitting and repurposing obsolete stock enhances value and meets regulatory demands. Digital transformation enables smart building management and improved tenant experiences. Strategic acquisitions in high growth sectors such as logistics and life sciences expand portfolio diversity. Flexible leasing models cater to evolving business needs and support tenant retention. Placemaking and community engagement initiatives drive footfall and enhance asset appeal. Cost efficiency through operational excellence ensures profitability amidst economic uncertainty. These approaches collectively strengthen market presence and adapt to shifting consumer and regulatory landscapes in the United Kingdom.

MARKET SEGMENTATION

This research report on the UK commercial real estate market is segmented and sub-segmented into the following categories.

By Property Type

- Offices

- Retail

- Logistics

- Others (Industrial Real Estate, Hospitality Real Estate, etc.)

By Business Model

- Sales

- Rental

By End User

- Individuals / Households

- Corporates & SMEs

- Others

Frequently Asked Questions

1. What is the UK commercial real estate market?

The UK commercial real estate market consists of properties used for business purposes, including offices, retail spaces, logistics facilities, industrial buildings, hospitality properties, and mixed use developments.

2. What factors are driving growth in the UK commercial real estate market?

Market growth is driven by urban development, increasing demand for logistics facilities, business expansion, infrastructure investments, and the growth of e commerce.

3. Which property type holds the largest share of the UK commercial real estate market?

Office and logistics properties account for a significant share of the market due to strong demand from businesses, corporate tenants, and distribution operators.

4. Why is the logistics segment growing rapidly in the UK?

The expansion of e commerce, supply chain modernization, and the need for efficient warehousing and distribution centers are driving demand for logistics real estate.

5. How has remote and hybrid work affected the office real estate sector?

Remote and hybrid work models have increased demand for flexible office spaces, high quality work environments, and strategically located office properties.

6. What role does sustainability play in the UK commercial real estate market?

Sustainability is becoming a key factor, with investors and tenants increasingly seeking energy efficient buildings that meet environmental, social, and governance goals.

7. How important is London to the UK commercial real estate market?

London remains a major commercial real estate hub, attracting domestic and international investment due to its strong business ecosystem and financial services sector.

8. Who are the primary end users of commercial real estate in the UK?

Key end users include corporations, small and medium sized enterprises, retailers, logistics companies, hospitality businesses, and individual investors.

9. What challenges does the UK commercial real estate market face?

Challenges include economic uncertainty, rising interest rates, changing workplace preferences, construction costs, and regulatory compliance requirements.

10. How is technology influencing the UK commercial real estate market?

Technology is improving property management, tenant experiences, smart building operations, energy efficiency, and investment decision making through data analytics.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com