Europe Commercial Real Estate Market Size, Share, Trends & Growth Forecast Report By Property Type, By Business Model, By End User, and By Country (Germany, United Kingdom, France, Netherlands, Sweden, Italy, Spain & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Commercial Real Estate Market Size

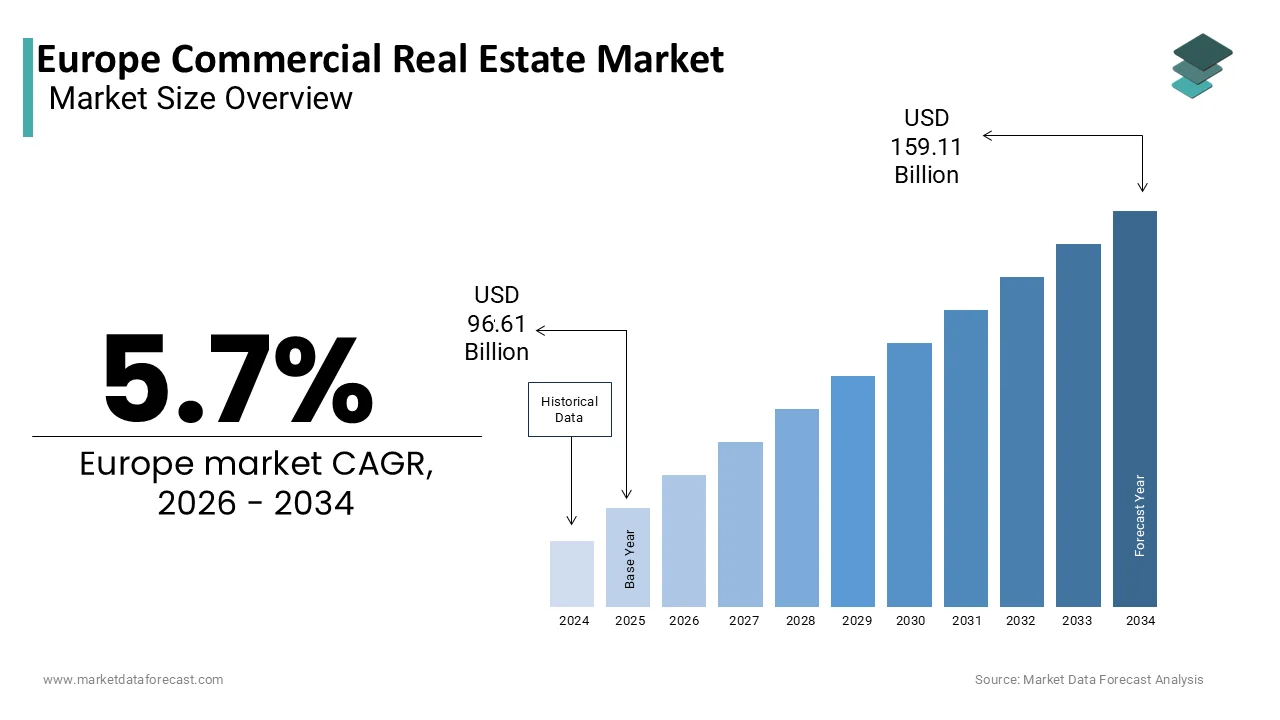

The europe commercial real estate market was valued at USD 96.61 billion in 2025, is estimated to reach USD 102.12 billion in 2026, and is projected to reach USD 159.11 billion by 2034, growing at a CAGR of 5.7% from 2026 to 2034.

Commercial real estate encompasses income-generating properties used for business purposes, including office buildings, retail spaces, industrial warehouses, logistics centers, and specialized assets such as data centers and life science facilities. This market functions as a critical barometer of economic activity, reflecting trends in employment, consumer behavior, supply chain dynamics, and technological adoption across the European Union and associated nations. Its structure is shaped by a complex interplay of local zoning laws, national tax regimes, and EU-wide sustainability mandates. As per Eurostat, the European Union recorded a significant number of enterprises in 2025, with the majority classified as small or medium-sized entities that collectively drive demand for flexible, accessible commercial space. As per the European Environment Agency, buildings account for a substantial share of the EU’s total energy consumption, placing commercial real estate at the heart of the bloc’s Green Deal decarbonization agenda. This dual role as both an economic enabler and a climate action focal point defines the market’s strategic significance in Europe’s post-pandemic recovery and long-term structural transformation.

MARKET DRIVERS

Accelerated E-commerce Growth Is Fuelling Demand for Modern Logistics and Last-Mile Warehousing

The sustained expansion of online retail has fundamentally reshaped spatial requirements across Europe’s commercial property landscape, which is one of the major factors driving the growth of the European commercial real estate market. As per Eurostat, e-commerce has grown significantly in recent years, driving strong demand for high-specification logistics facilities. Developers are prioritizing locations within close proximity to major urban centers to enable same-day delivery, creating intense competition for land in key corridors like the Rhine-Ruhr region and the Paris Basin. According to the European Logistics Association, logistics leases have expanded in size, with tenants increasingly demanding advanced features such as greater clear heights, cross-docking capabilities, and EV charging infrastructure. This shift has elevated industrial real estate to the highest-performing asset class. The structural nature of this trend ensures continued investment in modern distribution networks across the continent.

EU Green Building Regulations Are Compelling Asset Upgrades and Redevelopment

The European Union’s Energy Performance of Buildings Directive mandates that all commercial buildings achieve a minimum energy efficiency rating of B by 2030, which is effectively rendering older and inefficient structures obsolete are further contributing to the regional market expansion. As per the European Commission, a large portion of Europe’s existing office stock was constructed before 1990 and does not meet current thermal performance standards. This regulatory pressure is triggering a wave of capital expenditure, with landlords investing in deep retrofits involving façade insulation, LED lighting, smart HVAC systems, and on-site renewable generation to avoid obsolescence and tenant attrition. In cities like Amsterdam and Copenhagen, municipal ordinances prohibit renting out buildings rated below C. Conversely, newly certified green buildings command rental premiums, as documented by the European Real Estate Society. This policy-driven revaluation is accelerating the physical and financial renewal of Europe’s commercial property portfolio.

MARKET RESTRAINTS

Persistent Office Vacancy Pressures Are Eroding Asset Values in Secondary Cities

The hybrid work model has permanently reduced corporate demand for traditional office space, particularly in non-core urban locations, which is impeding the growth of the European commercial real estate market. According to the European Central Bank’s 2025 Financial Stability Review, office occupancy rates in major European cities remain well below pre-pandemic levels, with secondary markets like Milan, Brussels, and Warsaw experiencing elevated vacancy rates. This oversupply is depressing rental incomes and triggering downward revaluations. Banks have reclassified a significant volume of commercial real estate loans as non-performing, primarily tied to office portfolios. The challenge is exacerbated by rigid lease structures that prevent rapid repurposing. Unlike industrial assets, offices require significant capital to convert into residential or mixed-use schemes, and zoning restrictions often block such transitions. This structural mismatch between supply and demand is creating a two-tier market where only prime, sustainable assets retain value, while older buildings face steep depreciation and financing difficulties.

Rising Interest Rates Are Squeezing Refinancing Capacity and Transaction Volumes

The European Central Bank’s monetary tightening cycle has significantly increased borrowing costs, which is directly impacting commercial real estate liquidity and further hindering the growth of the regional market. As per the European Banking Authority, the average cost of commercial mortgage debt has risen considerably, compressing net operating income coverage ratios and forcing many owners to sell assets at discounted prices. This environment has chilled transaction activity, with cross-border investment volumes declining, according to the European Real Estate Investors Association. The pressure is most acute for highly leveraged funds that acquired assets during the low-rate era and now face maturity walls without sufficient cash flow to refinance. In response, developers are delaying new projects, and institutional buyers are demanding higher yields, creating a valuation gap that stalls market clearing. Until interest rate volatility subsides, the market will remain constrained by limited capital availability and pricing uncertainty.

MARKET CHALLENGES

Repurposing Obsolete Office Stock into Residential Units Addresses Housing Shortages

Europe’s chronic housing deficit creates a compelling opportunity to convert underutilized office buildings into much-needed homes. Cities like Berlin, Paris, and Barcelona have introduced fast-track permitting and density bonuses for such conversions, recognizing their dual benefit of revitalizing urban cores and expanding affordable housing supply. As per the Urban Land Institute, office-to-residential conversions in central London have shown stronger returns compared to ground-up development due to lower land acquisition costs and existing infrastructure. Moreover, these projects align with EU sustainability goals by avoiding demolition waste and reducing urban sprawl. With a large volume of vacant office space identified across major European capitals, this adaptive reuse strategy offers a scalable, socially beneficial path to asset revitalization that transforms liability into community value.

Expansion of Data Centers and AI Infrastructure Is Creating Premium Demand for Specialized Real Estate

The exponential growth of cloud computing, artificial intelligence, and digital services is driving robust demand for high-power data center facilities across Europe, which is another prominent opportunity in the European commercial real estate market. As per the European Data Centre Association, the region has added significant new capacity, with hyperscalers like Microsoft and Amazon securing long-term leases in markets with stable power grids and cool climates, such as Sweden and Ireland. These facilities require unique specifications, including strong floor loads, redundant fiber connectivity, and access to renewable energy. Developers who can deliver shovel-ready sites with pre-approved grid connections are commanding premium rents and achieving near-instant occupancy. This niche but high-growth segment offers inflation-linked, long-duration income streams that are largely immune to economic cycles, positioning data centers as a cornerstone of resilient European real estate portfolios in the digital age.

MARKET CHALLENGES

Fragmented National Regulatory Frameworks Impede Cross-Border Investment and Standardization

Despite EU-level directives, commercial real estate remains governed by divergent national laws on taxation, zoning, tenancy rights, and environmental compliance, which is challenging the growth of the European commercial real estate market. For instance, property transfer taxes vary widely across countries, while eviction procedures for non-paying tenants differ significantly. According to the European Real Estate Federation, this fragmentation increases due diligence costs for pan-European investors and discourages portfolio diversification. The absence of harmonized energy performance certification further complicates asset benchmarking, making it difficult to compare sustainability metrics across borders. Until member states align core regulatory elements, the market will struggle to achieve the scale and liquidity of more integrated regions like the United States, limiting institutional capital deployment and innovation in cross-border real estate finance.

Labor Shortages in Construction Are Delaying Deliveries and Inflating Development Costs

Europe’s commercial construction sector faces a severe shortage of skilled workers, directly impacting project timelines and economics. As per the European Construction Industry Federation, there is a notable deficit in qualified tradespeople across the EU, with the gap most acute in Germany, Poland, and the Nordic countries. This scarcity has driven wage inflation and contributed to project delays, according to the European Real Estate Development Council. For time-sensitive assets like logistics warehouses, these delays mean missing critical leasing windows and losing tenants to competitors. The problem is compounded by restrictive immigration policies and aging demographics, which limit workforce replenishment. Without targeted vocational training programs and streamlined labor mobility mechanisms, the supply pipeline will remain constrained, exacerbating space shortages in high-demand sectors and undermining Europe’s competitiveness in attracting global corporate tenants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Property Type, Business Model, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Unibail-Rodamco-Westfield, Vonovia SE, Segro plc, Landsec, Klépierre, British Land Company PLC, Covivio SA, Gecina, Hines Europe, AXA Investment Managers – Real Assets, CBRE Group, Inc., JLL, Savills plc, Knight Frank LLP, Colliers International Group Inc., PGIM Real Estate, LaSalle Investment Management, Name Holders Real Estate Europe, Deka Immobilien GmbH, Ivanhoé Cambridge |

SEGMENTAL ANALYSIS

By Property Type Insights

The logistics properties segment accounted for 33.9% of the European commercial real estate market share in 2025. The dominance ofthe logistics properties segment in the European market is driven by two structural economic shifts. The first is the irreversible growth of e-commerce. As per Eurostat, online retail has expanded significantly, necessitating vast networks of distribution centers. Developers are prioritizing locations within close proximity to major urban hubs to enable same-day delivery, creating intense demand for high-specification warehouses with advanced features. The second driver is supply chain resilience. As per the European Logistics Association, corporations have increased warehouse space requirements to strengthen inventory strategies. This dual pressure of consumer-driven speed and corporate-driven redundancy has elevated logistics to the highest-performing asset class.

By Business Model Insights

The rental model segment led the market by capturing 71.9% of the European market share in 2025. The growth of the rental model segment in the regional market is attributed to capital efficiency and risk mitigation. The first key driver is corporate preference for operational flexibility. As per the European Central Bank, a majority of European firms lease rather than own their premises to preserve capital for core business activities and adapt quickly to market changes. The second factor is institutional investor strategy. Pension funds and REITs favor long-term leases that provide stable, inflation-linked income with minimal management overhead. This symbiotic relationship between tenant agility and investor stability ensures rental remains the cornerstone of European commercial real estate transactions.

The sales segment is expected to exhibit a CAGR of 7.5% over the forecast period in the European market. The strategic asset consolidation and owner-occupier demand are propelling the expansion of the sales segment in the European market. As per Preqin, private equity funds hold significant uninvested capital, driving competitive bidding for core assets. Additionally, family offices and sovereign wealth funds are acquiring trophy properties in prime locations as inflation-resistant stores of value. This shift toward ownership reflects a recalibration of risk-return expectations in a higher-rate environment, where control and long-term appreciation outweigh short-term flexibility.

By End-User Insights

The corporates and SMEs segment occupied the highest share of the European commercial real estate market in 2025. The leading position of corporates and SMEs segment is attributed to their role as the primary economic engine of the continent. The first driving factor is employment scale. As per Eurostat, enterprises with fewer than 250 employees represent the overwhelming majority of EU businesses and employ millions of people, generating consistent demand for office, retail, and light industrial space. The second factor is regulatory compliance. EU workplace directives mandate minimum space per employee, natural lighting, and accessibility standards, compelling even small firms to secure compliant premises. This structural necessity ensures corporates and SMEs remain the bedrock of commercial real estate demand across all property types.

The individuals and households segment is a promising segment and is expected to register a CAGR of 9.15% over the forecast period. The blurring line between residential and commercial use is driving the expansion of individuals and the household segment in the European market. As per Eurostat, millions of Europeans operated registered micro-businesses from home in 2025, requiring dedicated commercial-grade spaces for studios, clinics, or workshops. A second major factor is co-living and flexible workspace integration. In cities like Berlin and Barcelona, developers are designing mixed-use buildings with ground-floor units zoned for commercial activity, leased directly to freelancers and solopreneurs. Additionally, the EU’s Digital Europe Programme has funded numerous local innovation hubs, many of which operate in repurposed retail spaces rented by individual creators. This shift reflects a broader societal move toward decentralized, personalized work models that transform individuals from passive residents into active commercial real estate participants.

COUNTRY-LEVEL ANALYSIS

Germany Commercial Real Estate Market Analysis

Germany dominated the commercial real estate market in Europe in 2025 with 22.9% of the regional market share. The dominating position of Germany in the European market is driven by the continent’s manufacturing and logistics hub and robust demand for high-specification industrial and logistics assets, particularly in the Rhine-Ruhr and Munich corridors. As per the German Federal Statistical Office, a significant portion of the national GDP is linked to trade, necessitating vast warehousing and distribution networks. Additionally, Germany’s Energiewende policy has spurred demand for green-certified offices and data centers powered by renewable energy. The country’s strict tenant protection laws also ensure long-term lease stability, attracting institutional capital. This combination of industrial depth, energy transition alignment, and legal predictability makes Germany the most liquid and resilient commercial real estate market in Europe.

United Kingdom Commercial Real Estate Market Analysis

The United Kingdom was the second-largest regional segment in the European commercial real estate market in 2025. The growth of the UK in the European market is attributed to London’s role as a global financial and tech hub. Its market status is characterized by deep liquidity and premium pricing for prime assets, despite Brexit-related uncertainties. As per the UK’s Office for National Statistics, a majority of central London office purchases in 2025 were made by overseas investors, drawn by the rule of law and currency stability. Simultaneously, the expansion of Tech City has revitalized East London, with life science and AI firms leasing large volumes of lab and office space. The government’s Levelling Up agenda is also redirecting investment to regional cities like Manchester and Birmingham, creating a multi-polar market. This blend of global appeal and domestic rebalancing sustains the UK’s position as a premier destination for high-value commercial real estate.

France Commercial Real Estate Market Analysis

France is predicted to witness a promising CAGR in the European commercial real estate market during the forecast period. Paris’s transformation into a sustainable and innovation-driven metropolis, aggressive urban renewal policies, and corporate decarbonization mandates are propelling the growth of the French market. As per the Société du Grand Paris, the Grand Paris Express project has catalyzed extensive mixed-use development along its routes. Additionally, France’s Climate Law requires all commercial buildings to achieve an energy rating of B by 2030, accelerating retrofits and conversions. A large volume of obsolete offices was approved for residential conversion in Paris in 2025. This fusion of infrastructure-led growth and regulatory-driven renewal positions France as a laboratory for next-generation urban real estate that balances density, sustainability, and livability.

Netherlands Commercial Real Estate Market Analysis

The Netherlands is expected to exhibit a healthy CAGR in the European commercial real estate market during the forecast period. The Netherlands is renowned for its world-class logistics infrastructure and digital connectivity. Its market status is defined by strategic geographic advantages, with Schiphol Airport and the Port of Rotterdam forming Europe’s largest cargo gateway. As per the Dutch Central Bureau of Statistics, logistics absorption reached record levels in 2025, with vacancy rates remaining very low. Simultaneously, the Netherlands has emerged as Europe’s top data center destination due to its stable grid, abundant renewable energy, and favorable tax regime. Hyperscalers leased substantial capacity in 2025, primarily in the Amsterdam and Eemshaven corridors. This dual dominance in physical and digital infrastructure cements the Netherlands as a critical node in Europe’s supply chain and cloud economy.

Sweden Commercial Real Estate Market Analysis

Sweden is predicted to account for a notable share of the European commercial real estate market over the forecast period. Sweden is notable for its leadership in green building and tech-driven workplaces. Its market status reflects a society-wide commitment to climate neutrality, with Stockholm aiming to be fossil-free by 2040. As per Statistics Sweden, a large majority of new commercial developments in 2025 achieved top-tier environmental certifications, commanding rental premiums. Additionally, Sweden’s cool climate and abundant hydropower have attracted major data center investments from global technology firms. The government’s Innovation Leap program also subsidizes life science real estate, fueling growth in clusters like Medicon Valley. This integration of sustainability, digital infrastructure, and scientific advancement makes Sweden a model for future-proof commercial real estate in Europe.

COMPETITIVE LANDSCAPE

The competition in the European commercial real estate market is increasingly defined by sustainability credentials, technological integration, and adaptive reuse capabilities rather than mere asset ownership. Large institutional investors and REITs compete on ESG performance, with green-certified buildings commanding significant rental premiums and attracting long-term tenants. Simultaneously, specialized developers focus on high-growth niches like data centers, last-mile logistics, and life science labs, where technical expertise and location access create high barriers to entry. The market is also witnessing consolidation, as financially strained owners sell discounted assets to well-capitalized funds with dry powder. Regulatory complexity favours players with deep local knowledge and agile compliance frameworks. This environment rewards innovation in asset repositioning and penalizes passive ownership, creating a dynamic landscape where value is derived from active stewardship and future-proofing.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Commercial Real Estate Market include

- Unibail-Rodamco-Westfield

- Vonovia SE

- Segro plc

- Landsec (Land Securities Group plc)

- Klépierre

- British Land Company PLC

- Covivio SA

- Gecina

- Hines Europe

- AXA Investment Managers – Real Assets

- CBRE Group, Inc.

- JLL (Jones Lang LaSalle Incorporated)

- Savills plc

- Knight Frank LLP

- Colliers International Group Inc.

- PGIM Real Estate

- LaSalle Investment Management

- Name Holders Real Estate Europe

- Deka Immobilien GmbH

- Ivanhoé Cambridge

TOP LEADING PLAYERS IN THE MARKET

- Vonovia SE is Europe’s largest residential real estate company, but its strategic expansion into commercial assets has made it a pivotal player in the broader commercial real estate market. Headquartered in Germany, Vonovia contributes globally by pioneering ESG-integrated asset management, with over 90% of its portfolio now aligned with EU Taxonomy criteria. The company has recently accelerated its conversion of underutilized office spaces into affordable housing and micro-logistics hubs in urban centers like Berlin and Dortmund. It also launched a digital twin platform for predictive maintenance and energy optimization across its commercial holdings. These actions reinforce its role as a sustainability leader while addressing Europe’s dual challenges of housing shortages and supply chain resilience.

- Unibail-Rodamco-Westfield is a Franco-Dutch leader in retail and mixed-use commercial real estate, operating iconic shopping destinations across Europe. URW contributes globally by redefining urban retail through its “Better Places” strategy, which integrates commerce, culture, and community services. In recent years, the company has transformed flagship properties like Westfield London and Les Ateliers Gaîté in Paris into multi-functional ecosystems featuring offices, residences, hotels, and public plazas. URW has also committed to achieving net-zero operational emissions by 2035 and is retrofitting all assets to meet EU energy performance class B standards. This holistic approach positions URW at the forefront of adaptive reuse and sustainable urban regeneration in the European commercial landscape.

- CBRE’s European operations serve as a dominant force in commercial real estate services, advising on transactions, property management, and investment strategies across all major asset classes. While headquartered in the United States, CBRE’s European arm plays a critical role in shaping market dynamics through data-driven insights and cross-border capital placement. The firm has recently expanded its ESG advisory practice to help clients navigate the EU’s Sustainable Finance Disclosure Regulation and Energy Performance of Buildings Directive. It also launched a proprietary AI-powered platform that forecasts rental trends and vacancy risks using real-time mobility and economic data. These innovations strengthen CBRE’s position as an indispensable partner for institutional investors navigating Europe’s complex and evolving regulatory environment.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European commercial real estate market are prioritizing environmental, social, and governance compliance by retrofitting existing assets to meet EU energy performance standards and achieve green building certifications. They are actively repurposing obsolete office stock into residential units, logistics hubs, or life science facilities to address structural demand shifts. Companies are leveraging artificial intelligence and digital twin technology for predictive maintenance, energy optimization, and tenant experience enhancement. Strategic partnerships with renewable energy providers are being formed to secure power purchase agreements for data centers and industrial parks. Additionally, firms are expanding their mixed-use development pipelines to create integrated urban ecosystems that combine retail, work, living, and leisure in response to evolving consumer and corporate preferences.

MARKET SEGMENTATION

This research report on the europe commercial real estate market is segmented and sub-segmented into the following categories.

By Property Type

- Office Properties

- Retail Properties

- Industrial & Logistics Properties

- Hospitality Properties

- Data Centers

- Mixed-Use Developments

- Others

By Business Model

- Rental / Leasing

- Sales / Ownership

By End User

- Corporates

- Small & Medium Enterprises (SMEs)

- Individuals & Households

- Government & Public Sector

- Institutional Occupiers

- Others

By Country

- Germany

- United Kingdom

- France

- Netherlands

- Sweden

- Italy

- Spain

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com