UK Consumer Credit Market Size, Share, Trends & Growth Forecast Report By Credit Type (Revolving Credits, Non-revolving Credits), Issuer, Payment Method, and Country – Industry Analysis and Forecast, 2026 to 2034

UK Consumer Credit Market Report Summary

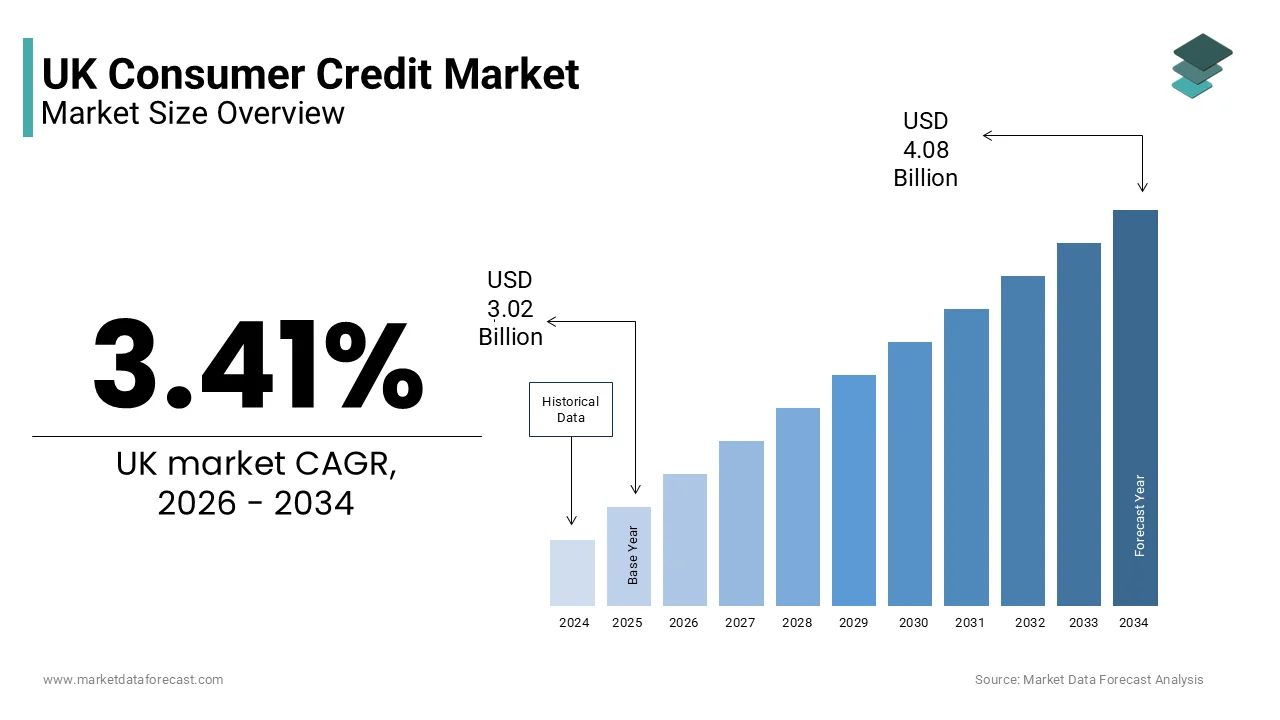

The UK consumer credit market was valued at USD 3.02 billion in 2025, is estimated to reach USD 3.12 billion in 2026, and is projected to reach USD 4.08 billion by 2034, growing at a CAGR of 3.41% during the forecast period. Market growth is driven by increasing consumer spending, rising adoption of digital lending platforms, expanding access to credit products, and the growing use of flexible financing solutions. The market continues to evolve through technological advancements in lending, enhanced credit assessment tools, and changing consumer borrowing preferences. Regulatory developments and the increasing adoption of digital payment ecosystems are also shaping market dynamics.

Key Market Trends

- Growing demand for flexible consumer financing options is driving market growth.

- Increasing adoption of digital lending and fintech platforms is boosting market expansion.

- Rising use of data analytics and automated credit assessment tools is supporting industry development.

- Expansion of buy now pay later and alternative credit solutions is enhancing market opportunities.

- Increasing focus on responsible lending practices and regulatory compliance is influencing market advancement.

Segmental Insights

- Based on credit type, the revolving credit segment accounted for the largest share of the UK consumer credit market in 2025. This dominance is attributed to the widespread use of credit cards and flexible borrowing facilities that allow consumers to access funds as needed.

- Based on issuer, the banks and traditional finance companies segment held the dominant share of the UK consumer credit market in 2025, supported by established customer relationships, extensive branch networks, and diversified lending portfolios.

- Based on payment method, the direct deposit segment accounted for the major share of the UK consumer credit market in 2025 due to its reliability, automation capabilities, and alignment with regular salary payment cycles.

Regional Insights

- The United Kingdom is expected to experience continued evolution in consumer borrowing patterns over the forecast period. Ongoing digital transformation, changing regulatory frameworks, and shifts in consumer financial behavior are expected to influence future market development.

Competitive Landscape

The UK consumer credit market is highly competitive, with traditional financial institutions and fintech companies focusing on digital innovation, customer experience enhancement, and risk management capabilities to strengthen their market position. Market participants continue to invest in advanced lending technologies, personalized credit solutions, and digital banking platforms. Key companies operating in the UK consumer credit market include Barclays, Lloyds Banking Group, NatWest Group, HSBC, Santander, Nationwide Building Society, Virgin Money, Lendable, Zilch, and NewDay Ltd..

UK Consumer Credit Market Size

The UK consumer credit market size was valued at USD 3.02 billion in 2025, and is projected to reach USD 4.08 billion by 2034 from USD 3.12 billion in 2026, growing at a CAGR of 3.41%.

As per the Bank of England, total outstanding consumer credit in the UK reached £230.5 billion in early 2024, reflecting sustained demand despite macroeconomic headwinds. The Financial Conduct Authority regulates this landscape to ensure fair treatment and transparency for borrowers, mandating strict affordability checks and responsible lending practices. According to the Office for National Statistics, household debt to income ratios reached 118% in late 2024, indicating that while borrowing levels are high, they are currently supported by wage growth. The digital transformation of financial services has democratized access, with fintech firms offering streamlined application processes and instant decisioning. This evolution has shifted consumer expectations towards speed and convenience, compelling traditional banks to modernize their legacy systems. The market is characterized by a diverse mix of incumbent institutions and agile challengers, each competing on interest rates, user experience, and product flexibility. Regulatory scrutiny remains intense, particularly regarding high cost short term credit, ensuring that the market evolves in a manner that protects vulnerable consumers while fostering financial inclusion and economic stability.

MARKET DRIVERS

Resilient Household Consumption Patterns Driving Credit Demand

The persistent strength of household consumption is majorly driving the expansion of the UK consumer credit market, as individuals utilize borrowed funds to maintain living standards and finance discretionary purchases. Despite inflationary pressures, consumer spending has demonstrated remarkable resilience, supported by a tight labor market and steady wage increases. According to the Office for National Statistics, retail sales volumes fell by 0.8% compared with their pre coronavirus level, with many households turning to credit facilities to bridge the gap between rising prices and income. As per the Bank of England, net lending to individuals increased by £1.7 billion in recent months, signaling continued confidence in borrowing for big ticket items such as home improvements and vehicles. This behavior is particularly pronounced among younger demographics that prioritize experiences and immediate gratification over long term savings. The availability of flexible repayment options encourages consumers to spread costs over time, making expensive purchases more accessible. Furthermore, the cultural normalization of debt for non-essential goods has reduced the stigma associated with borrowing, leading to higher uptake of unsecured credit products. As per data from UK Finance, credit card spending rose by 8.2% year on year, driven largely by travel and hospitality sectors recovering to pre pandemic levels. This sustained demand for consumption financing ensures a steady flow of new business for lenders, which is underpinning the market’s growth trajectory even in uncertain economic times.

Digital Innovation Enhancing Access and User Experience

Rapid technological advancement and the proliferation of digital platforms significantly drive the UK consumer credit market by lowering barriers to entry and improving customer engagement. Fintech companies have revolutionized the lending process through the use of artificial intelligence and machine learning algorithms that assess creditworthiness more accurately and efficiently than traditional methods. According to Innovate Finance, the UK fintech sector attracted £1.3 billion in investment in 2023, with a substantial portion directed towards lending and payments solutions. These digital lenders offer seamless mobile applications that allow users to apply for credit in minutes, receive instant approvals, and manage repayments with ease. This convenience appeals strongly to tech savvy consumers who value speed and transparency over branch based interactions. Traditional banks have responded by investing heavily in their own digital infrastructure, resulting in a competitive landscape that benefits borrowers through better terms and enhanced services. The integration of open banking APIs enables lenders to access real time financial data, facilitating more personalized product offerings and dynamic risk assessment. As per the Financial Conduct Authority, the number of active digital only bank accounts surpassed 10 million in the UK, creating a large addressable market for embedded credit products. This digital shift not only expands the reach of credit providers but also fosters financial inclusion by serving underserved segments who may lack extensive credit histories but possess strong cash flow profiles.

MARKET RESTRAINTS

Elevated Interest Rates Increasing Borrowing Costs

The sustained elevation of interest rates by the Bank of England is a significant restraint on the UK consumer credit market, increasing the cost of borrowing and dampening demand for new credit facilities. As the central bank raises the base rate to combat inflation, lenders pass these higher costs onto consumers through increased annual percentage rates on loans and credit cards. According to the Bank of England, the average interest rate on new personal loans rose to 7.5% in 2024, compared to 4.5% in the previous year, making debt substantially more expensive for households. This price sensitivity leads to a decline in application volumes as consumers reconsider the affordability of financed purchases. Higher repayment obligations also strain existing borrowers, reducing their capacity to take on additional debt and increasing the risk of default. The Money and Pensions Service reported that inquiries for debt advice increased by 15% during periods of rate hikes, indicating growing financial stress among consumers. Lenders respond by tightening credit criteria and reducing approval rates to mitigate risk, further restricting access to credit for marginal borrowers. This contraction in supply and demand dynamics slows market growth and forces lenders to compete more aggressively on non-price factors. The prolonged period of high rates creates an environment of caution, where both lenders and borrowers adopt a more conservative approach to credit utilization, limiting the expansion potential of the market.

Stringent Regulatory Compliance Burdens

Strict regulatory requirements imposed by the Financial Conduct Authority are further hindering the UK consumer credit market growth. The regulatory framework mandates rigorous affordability assessments, transparent pricing disclosures, and robust treatment of vulnerable customers, which require significant investment in compliance infrastructure and personnel. According to the Financial Conduct Authority, fines and enforcement actions related to consumer credit misconduct totaled £50 million in 2023, highlighting the severe consequences of non-compliance. These regulatory burdens slow down the launch of new products as firms must undergo extensive testing and approval processes to ensure adherence to rules. The complexity of regulations also creates uncertainty, causing some lenders to exit certain high risk segments such as subprime lending or high cost short term credit. This reduction in market participants limits competition and choice for consumers, particularly those with poor credit histories who rely on specialized lenders. The requirement to maintain detailed records and report regularly to regulators adds administrative overhead, reducing profit margins and diverting resources from customer acquisition and service improvement. As per industry surveys, compliance costs account for up to 12% of operating expenses for smaller lenders, posing a barrier to entry for new firms. This restrictive environment, while protective of consumers, constrains the agility and scalability of credit providers, hindering the overall dynamism of the market.

MARKET OPPORTUNITIES

Expansion of Buy Now Pay Later Solutions

The rapid growth of Buy Now Pay Later services presents a significant opportunity for the UK consumer credit market, which is offering a flexible and interest free alternative to traditional credit cards and loans. This payment method allows consumers to split purchases into smaller instalments, appealing to budget conscious shoppers who wish to avoid interest charges. According to UK Finance, the value of Buy Now Pay Later transactions reached £10 billion in 2023, representing a 20% increase from the previous year. This surge indicates strong consumer preference for transparent and manageable repayment structures. Retailers are increasingly integrating these solutions at checkout to boost conversion rates and average order values, creating a symbiotic relationship between merchants and lenders. The regulatory oversight of this sector is evolving, with the Financial Conduct Authority planning to bring Buy Now Pay Later providers under its remit, which will enhance consumer protection and legitimize the product. This formalization opens doors for established financial institutions to enter the space, leveraging their capital and expertise to offer competitive rates. The demographic appeal of Buy Now Pay Later extends to younger consumers who are often excluded from traditional credit markets due to limited credit history. By capturing this segment, lenders can build long term relationships and cross sell other financial products. The integration of these services into e commerce platforms and physical stores ensures widespread accessibility, driving further adoption and market expansion.

Integration of Artificial Intelligence for Risk Assessment

The adoption of artificial intelligence and advanced data analytics offers a promising opportunity for the UK consumer credit market by enabling more accurate risk assessment and personalized lending decisions. Traditional credit scoring models rely heavily on historical data, which may exclude individuals with thin files or unconventional income streams. AI algorithms can analyze alternative data sources such as utility payments, rental history, and transaction patterns to create a holistic view of creditworthiness. According to a study by the University of Cambridge, AI driven lending models can reduce default rates by up to 25% compared to traditional methods, allowing lenders to extend credit to previously underserved populations safely. This technological capability enables financial institutions to offer tailored products with dynamic interest rates based on real time risk profiles. The automation of underwriting processes reduces operational costs and speeds up decision making, enhancing customer satisfaction. Furthermore, AI tools can monitor borrower behavior continuously, allowing for proactive intervention in cases of financial distress and reducing loss provisions. The Financial Conduct Authority has expressed support for responsible innovation in this area, encouraging firms to use technology to improve fairness and inclusion. As data privacy regulations evolve, lenders who can effectively leverage data while maintaining trust will gain a competitive edge. This shift towards intelligent lending not only expands the addressable market but also improves the overall efficiency and sustainability of the credit ecosystem.

MARKET CHALLENGES

Rising Cost of Living Impacting Repayment Capacity

The escalating cost of living is a major challenge to the UK consumer credit market, which is eroding household disposable income and increasing the likelihood of loan defaults and arrears. Inflation in essential categories such as energy, food, and housing has forced many families to rely on credit to cover basic needs, leading to unsustainable debt levels. According to the Office for National Statistics, the consumer price index remained elevated above 4% for much of 2024, placing continuous pressure on household budgets. This financial strain reduces the ability of borrowers to meet repayment obligations, resulting in higher delinquency rates for lenders. The StepChange debt charity reported that it advised over 600,000 people in 2023, with a significant portion citing unaffordable credit repayments as a primary concern. Lenders face increased provisioning requirements and write offs, which impact profitability and necessitate tighter lending criteria. This defensive posture restricts credit availability, creating a vicious cycle where those most in need of financial support are denied access. The psychological stress associated with debt also affects consumer confidence and spending behavior, further slowing economic activity. Regulators are closely monitoring these trends, potentially imposing stricter affordability checks that could limit market growth. The challenge lies in balancing the need to support consumers during difficult times with the imperative to maintain financial stability and prevent systemic risk within the lending sector.

Cybersecurity Threats and Data Privacy Concerns

The increasing frequency and sophistication of cyberattacks is further challenging the expansion of the UK consumer credit market, which is threatening the integrity of sensitive financial data and undermining consumer trust. As lenders digitize their operations and store vast amounts of personal information, they become attractive targets for hackers seeking to commit identity theft and fraud. According to the National Cyber Security Centre, the financial services sector experienced a 30% increase in reported cyber incidents in 2023, highlighting the escalating threat landscape. A successful breach can result in significant financial losses, regulatory penalties, and reputational damage that is difficult to repair. Consumers are becoming more aware of data privacy issues and are hesitant to share personal information with providers that do not demonstrate robust security measures. The General Data Protection Regulation imposes strict requirements on data handling, and any failure to comply can lead to substantial fines. Lenders must invest heavily in advanced encryption, multi factor authentication, and continuous monitoring systems to protect their infrastructure. However, the rapid evolution of cyber threats means that defenses must be constantly updated, requiring ongoing expenditure and specialized expertise. The fear of fraud also leads to false positives in automated screening processes, causing inconvenience for legitimate applicants and potentially losing business. Maintaining a secure environment while ensuring a seamless user experience remains a complex balancing act that tests the operational resilience of credit providers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.41% |

| Segments Covered | By Credit Type, Issuer, Payment Method, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Market Leaders Profiled | Barclays, Lloyds Banking Group, NatWest Group, HSBC, Santander, Nationwide Building Society, Virgin Money, Lendable, Zilch, and NewDay Ltd. |

SEGMENTAL ANALYSIS

By Credit Type Insights

The revolving credits segment dominated the market by holding the major share of the UK market in 2025. The dominance of revolving credits segment in the UK market can be credited to the ubiquity of credit cards and authorized overdrafts that offer continuous access to funds. This dominance is also driven by the flexibility these products provide, allowing consumers to borrow up to a pre approved limit and repay varying amounts each month. According to UK Finance, outstanding balances on credit cards and overdrafts accounted for approximately 65% of total unsecured consumer lending in 2023. The convenience of revolving credit makes it the preferred choice for managing daily expenses and unexpected costs, as users do not need to reapply for new loans for each transaction. The integration of contactless payment technology has further entrenched this habit, with millions of transactions processed daily via credit facilities. As per the Bank of England, the average interest rate on outstanding credit card debt remained stable, encouraging sustained usage despite broader economic pressures. Retailers also promote revolving credit through loyalty programs and cashback offers, incentivizing consumers to maintain active accounts. The ability to carry a balance while maintaining purchasing power appeals to households seeking liquidity without the commitment of fixed installment plans. This structural advantage ensures that revolving credit remains the backbone of household borrowing, supported by established infrastructure and high consumer familiarity.

However, the non-revolving credits segment is experiencing the fastest growth in the UK market and is predicted to record a CAGR of 10.5% during the forecast period owing to the rising popularity of personal loans and point of sale financing for specific large purchases such as vehicles, home improvements, and electronics. Consumers increasingly prefer the certainty of fixed monthly repayments and defined end dates, which helps with budgeting and financial planning. According to the Finance and Leasing Association, lending for motor finance and personal loans increased by 12% in 2023, reflecting strong demand for structured debt solutions. The transparency of non-revolving products, with no hidden fees or variable interest rates, builds trust among borrowers who are wary of accumulating open ended debt. Digital lenders have streamlined the application process for these products, offering instant decisions and rapid fund disbursement, which enhances their appeal. As per data from MoneySuperMarket, searches for personal loans rose by 18% year on year, indicating heightened consumer interest in consolidated borrowing options. The shift towards responsible lending practices also favors non revolving credits, as affordability checks are more straightforward for fixed term loans. This segment’s growth is further supported by the expansion of buy now pay later services that operate on a non-revolving basis, which is capturing younger demographics who seek disciplined repayment structures.

By Issuer Insights

The banks and traditional finance companies segment captured the dominating share of the UK market in 2025. The dominance of banks and traditional finance companies segment in the UK market is attributed to their extensive branch networks, established brand trust, and comprehensive product portfolios. These institutions benefit from long standing relationships with customers, allowing them to cross sell credit products alongside current accounts and savings vehicles. According to the Bank of England, major high street banks accounted for over 70% of new personal lending approvals in 2023, demonstrating their continued influence. Their ability to offer competitive interest rates due to lower cost of funds gives them a significant advantage over non bank lenders. The regulatory framework favors established entities with robust compliance infrastructures, enabling them to navigate complex legal requirements more effectively than smaller competitors. As per UK Finance, customer retention rates for bank issued credit products exceed 85%, highlighting the stickiness of these relationships. Banks also invest heavily in digital platforms, ensuring that their online and mobile services meet modern expectations for speed and convenience. The perception of security and stability associated with traditional banks attracts risk averse borrowers, particularly for larger loan amounts. Furthermore, their access to detailed transaction history allows for more accurate risk assessment and personalized offers. This combination of trust, scale, and technological investment ensures that banks and finance companies remain the primary source of consumer credit for the majority of the population.

On the other hand, the fintech firms and non-bank lenders segment is estimated to showcase CAGR of 16.2% during the forecast period owing to their agility, innovative use of technology, and ability to serve underserved segments that traditional banks often overlook. These lenders utilize alternative data sources and advanced algorithms to assess creditworthiness, enabling them to approve applicants with thin credit files or irregular income streams. According to Innovate Finance, the number of active fintech lending platforms in the UK doubled between 2020 and 2023, reflecting intense innovation and market entry. Their user centric design focuses on seamless digital experiences, with applications completed entirely on mobile devices in minutes. This convenience appeals strongly to younger consumers who prioritize speed and transparency over traditional banking relationships. As per a survey by Deloitte, 40% of millennials prefer using fintech apps for borrowing due to their intuitive interfaces and clear fee structures. Non bank lenders also specialize in niche products such as green loans for energy efficient home upgrades, catering to specific consumer needs. The lack of legacy systems allows them to adapt quickly to regulatory changes and market trends. Their collaborative approach, often partnering with retailers and service providers for embedded finance solutions, further accelerates growth. This dynamic segment challenges incumbents by offering greater inclusivity and efficiency, capturing an increasing share of new originations.

By Payment Method Insights

The direct deposit segment held the major share of the UK market in 2025 as it is favored for its reliability, automation, and alignment with salary cycles. Most borrowers set up standing orders or direct debits from their current accounts to ensure timely repayment of credit obligations, avoiding late fees and negative impacts on credit scores. According to the Payments Systems Regulator, over 80% of regular consumer loan repayments are processed via direct debit mechanisms, highlighting its dominance. This method reduces administrative burden for both lenders and borrowers, as it eliminates the need for manual transactions each month. The integration of open banking has enhanced this process, allowing lenders to verify account details and initiate payments securely with customer consent. As per UK Finance, the failure rate for direct debit repayments is significantly lower than other methods, contributing to better portfolio performance for lenders. Consumers appreciate the predictability of automatic deductions, which helps in managing household budgets effectively. The widespread adoption of digital banking apps makes it easy for users to monitor and adjust these payments as needed. Furthermore, regulatory mandates requiring affordable repayment plans often rely on direct deposit data to assess disposable income accurately. This structural integration into the banking system ensures that direct deposit remains the cornerstone of credit repayment, supported by high trust levels and operational efficiency.

The digital wallets and alternative payment methods segment is another promising segment and is predicted to witness a CAGR of 21.2% during the forecast period. This surge is driven by the increasing penetration of smartphone usage and the convenience of managing finances through integrated apps. Platforms such as PayPal, Apple Pay, and Google Pay allow users to link multiple funding sources and schedule payments seamlessly. According to Juniper Research, the number of UK consumers using digital wallets for financial management reached 35 million in 2023, creating a large base for credit related interactions. These methods offer greater flexibility, enabling borrowers to make partial or early repayments instantly without logging into separate banking portals. The gamification features and spending insights provided by digital wallet apps encourage responsible financial behavior and timely repayments. As per a study by the University of Oxford, users of digital finance tools are 20% more likely to stay current on their debt obligations due to real time notifications and reminders. Lenders are increasingly integrating with these platforms to offer frictionless repayment experiences, reducing churn and improving customer satisfaction. The ability to switch funding sources easily within the app provides a safety net for users facing temporary cash flow issues. This technological shift reflects broader changes in consumer preferences towards mobile first financial solutions, driving rapid adoption in the credit sector.

COUNTRY LEVEL ANALYSIS

The UK is expected to experience highly specialized adjustments in its consumer debt structures and tightened credit accessibility over the next few years. According to the Bank of England, total consumer credit outstanding in the UK reached £230.5 billion in 2024, which is representing a significant portion of European household debt. This volume is driven by a culture of consumption and the widespread availability of diverse credit products ranging from mortgages to buy now pay later schemes. The country’s advanced digital banking ecosystem facilitates rapid credit decisioning and distribution, setting it apart from many continental peers. As per the Office for National Statistics, household debt to income ratios reached 118% in late 2024, indicating manageable but elevated leverage levels. The post pandemic recovery saw a surge in borrowing for travel and leisure, reinforcing the resilience of consumer demand. Regulatory initiatives such as price caps on high cost short term credit has reshaped the landscape, which is protecting vulnerable borrowers while encouraging responsible lending. The presence of major global banks and innovative fintech firms creates a competitive environment that drives product innovation and customer service improvements. This dynamic interplay between tradition and innovation ensures that the UK remains a central pillar of the European consumer credit market.

COMPETITIVE LANDSCAPE

The competition in the UK consumer credit market is intense and characterized by the presence of established high street banks alongside agile fintech challengers and specialized non bank lenders. Traditional institutions leverage their brand trust and extensive customer bases to retain dominance while innovating digitally to match the speed of newer entrants. Fintech firms disrupt the status quo by offering superior user experiences and utilizing alternative data for credit scoring which allows them to serve underserved segments effectively. Price competition remains fierce particularly for personal loans and balance transfers prompting providers to offer attractive introductory rates and fee waivers. Regulatory compliance acts as a significant barrier to entry ensuring that only well capitalized and robust entities can operate sustainably. The rise of buy now pay later services has added another layer of complexity forcing traditional lenders to adapt their product offerings. Differentiation increasingly relies on customer service quality financial wellness tools and seamless digital integration rather than interest rates alone. This dynamic landscape drives continuous innovation and benefits consumers through greater choice and improved transparency in lending practices.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the UK consumer credit market are

- Barclays

- Lloyds Banking Group

- NatWest Group

- HSBC

- Santander

- Nationwide Building Society

- Virgin Money

- Lendable

- Zilch

- NewDay Ltd.

Top Players in the Market

- Barclays maintains a prominent position in the UK consumer credit market through its extensive portfolio of credit cards and personal loans. The bank leverages its large retail customer base to offer tailored financial products that meet diverse borrowing needs. Recent initiatives include the enhancement of its digital lending platform to provide faster approval times and personalized interest rates based on individual credit profiles. Barclays has also invested in artificial intelligence tools to improve fraud detection and risk assessment capabilities. The institution actively promotes responsible lending practices by offering financial education resources to help customers manage debt effectively. Its integration of open banking features allows for seamless account management and real time spending insights. These efforts strengthen customer loyalty and ensure compliance with regulatory standards while driving sustainable growth in the unsecured lending segment.

- Lloyds Banking Group plays a critical role in the UK consumer credit landscape by providing accessible financing solutions to millions of households across the nation. The group focuses on simplifying the borrowing experience through user friendly mobile applications and online portals. Recent actions involve the expansion of its buy now pay later partnerships with major retailers to capture younger demographics seeking flexible payment options. Lloyds has also upgraded its underwriting algorithms to assess affordability more accurately using real time transaction data. The bank emphasizes community support by offering hardship assistance programs for borrowers facing financial difficulties. Its commitment to digital transformation ensures that customers can apply for and manage credit facilities with minimal friction. These strategic moves enhance operational efficiency and reinforce its reputation as a trusted provider of consumer finance.

- NatWest Group contributes significantly to the UK consumer credit market by offering a wide range of unsecured lending products including overdrafts and installment loans. The group prioritizes innovation by integrating advanced analytics into its credit decisioning processes to serve customers with varying credit histories. Recent developments include the launch of green loan products that incentivize environmentally friendly purchases such as electric vehicles and energy efficient home improvements. NatWest has strengthened its cybersecurity measures to protect customer data and prevent identity theft in an increasingly digital environment. The bank collaborates with fintech firms to embed credit options within everyday banking apps for greater convenience. Its focus on financial wellbeing includes tools that help users track spending and plan repayments. These initiatives demonstrate a commitment to sustainable growth and customer centric service delivery in the competitive lending sector.

Top Strategies Used by Key Market Participants

Key players in the UK consumer credit market primarily employ strategies focused on digital transformation and data driven personalization to enhance customer engagement and operational efficiency. Institutions invest heavily in artificial intelligence and machine learning technologies to streamline underwriting processes and improve risk assessment accuracy. Developing seamless mobile experiences allows lenders to offer instant approvals and easy account management which appeals to tech savvy consumers. Partnerships with retailers and fintech firms enable embedded finance solutions that integrate credit options directly into purchasing journeys. Companies also prioritize responsible lending by implementing robust affordability checks and providing financial education resources to support borrower wellbeing. Enhancing cybersecurity measures protects sensitive data and builds trust among users. These multifaceted approaches help firms differentiate their offerings and maintain competitiveness in a regulated environment.

MARKET SEGMENTATION

This research report on the UK consumer credit market is segmented and sub-segmented into the following categories.

By Credit Type

- Revolving Credits

- Non-revolving Credits

By Issuer

- Banks and Finance Companies

- Credit Unions

- Others

By Payment Method

- Direct Deposit

- Debit Card

- Others

Frequently Asked Questions

1. What is the UK consumer credit market?

The UK consumer credit market comprises financial products that allow individuals to borrow money for personal use, including credit cards, personal loans, overdrafts, and retail financing.

2. What factors are driving the growth of the UK consumer credit market?

Market growth is driven by rising consumer spending, increasing digital lending adoption, greater access to credit products, and the expansion of fintech services.

3. What are the major types of consumer credit available in the UK?

Key products include credit cards, personal loans, overdrafts, hire purchase agreements, point of sale financing, and buy now pay later services.

4. How are digital technologies influencing the UK consumer credit market?

Digital platforms and mobile applications have simplified loan applications, credit assessments, approvals, and account management, improving customer convenience.

5. What role do fintech companies play in the UK consumer credit market?

Fintech companies are enhancing competition by offering innovative lending solutions, faster approvals, personalized products, and digital first customer experiences.

6. How do interest rates affect the consumer credit market?

Changes in interest rates influence borrowing costs, consumer demand for credit, repayment affordability, and overall lending activity.

7. What is the impact of buy now pay later services on the market?

Buy now pay later solutions have gained popularity by providing flexible payment options for consumers, particularly in the retail and e commerce sectors.

8. Which consumer group represents a significant share of credit demand in the UK?

Working professionals, households, and younger consumers seeking flexible financing options contribute significantly to market demand.

9. What challenges does the UK consumer credit market face?

Key challenges include rising default risks, economic uncertainty, regulatory compliance requirements, and concerns related to consumer debt levels.

10. What is the future outlook for the UK consumer credit market?

The market is expected to grow steadily due to digital transformation, expanding fintech participation, increasing demand for flexible financing, and ongoing innovation in lending services.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com