U.S Athletic Footwear Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Training Shoes, Running Shoes, Lifestyle Shoes, Outdoor Shoes, Others), End User, Distribution Channel, And Country (California, Washington, Oregon, New York & Rest Of The United States) – Industry Analysis And Forecast, 2026 To 2034

U.S. Athletic Footwear Market Report Summary

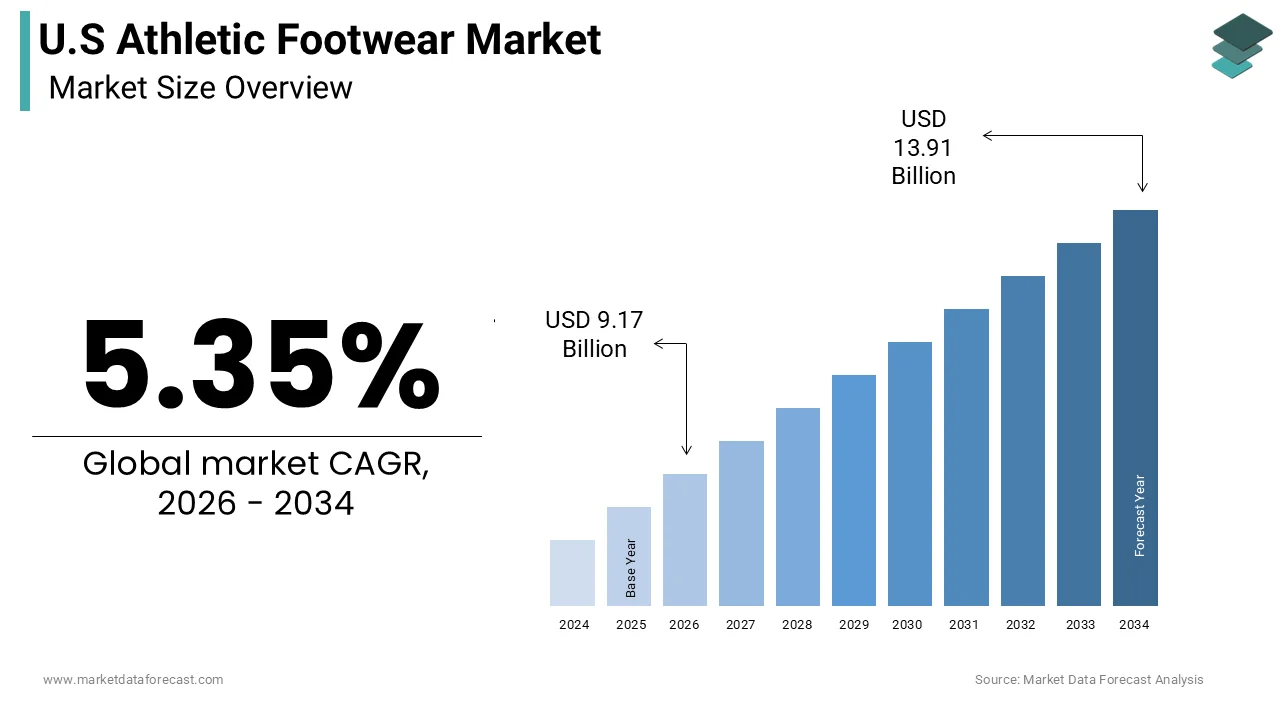

The United States athletic footwear market was valued at USD 8.70 billion in 2025 and is projected to reach USD 13.91 billion by 2034, growing from USD 9.17 billion in 2026 at a CAGR of 5.35% during the forecast period. Market growth is driven by increasing participation in sports and fitness activities, rising consumer preference for athleisure products, and growing awareness regarding health and wellness. Innovations in footwear technology, sustainable materials, and performance-enhancing designs are further accelerating the growth of the U.S. athletic footwear market.

Key Market Trends

- Rising popularity of athleisure and fitness culture

- Increasing demand for lightweight and performance-enhancing footwear

- Growth in sustainable and eco-friendly shoe materials

- Expansion of direct-to-consumer and e-commerce sales channels

- Increasing celebrity endorsements and sports brand collaborations

Segmental Insights

- Based on product type, the running shoes segment dominated the U.S. athletic footwear market in 2025 by accounting for 31.2% of the market share, driven by growing participation in running, jogging, and fitness activities

- Based on end user, the men’s segment held a prominent market share in 2025 due to high spending on sports and lifestyle footwear products

- Based on distribution channel, the specialty stores segment led the market in 2025 by capturing 56.3% of the market share, supported by personalized customer service, product variety, and brand-focused shopping experiences

Competitive Landscape

- The U.S. athletic footwear market is highly competitive, with companies focusing on innovative product designs, comfort technologies, and sustainable manufacturing. Market players are investing in smart footwear, advanced cushioning systems, and digital marketing strategies to strengthen their market presence.

- Prominent players in the U.S. athletic footwear market include Nike, Adidas, PUMA, Under Armour, New Balance, Skechers, ASICS, Brooks Sports, Reebok, and Converse.

U.S Athletic Footwear Market Size

The U.S. athletic footwear market was valued at USD 8.70 billion in 2025, is estimated to reach USD 9.17 billion in 2026, and is projected to reach USD 13.91 billion by 2034, growing at a CAGR of 5.35% from 2026 to 2034.

The athletic footwear is specialized shoes designed for sports and physical exercise, including running, basketball, training, and walking categories. This sector intersects with broader lifestyle trends where performance gear transitions into everyday casual wear, reflecting a cultural shift toward health-conscious living. The definition extends beyond mere utility to encompass fashion identity and technological innovation in material science. Consumer participation in physical activities serves as the foundational pillar for demand. Furthermore, data from the Bureau of Labor Statistics shows that average annual expenditures on footwear per consumer unit reached 423 dollars, demonstrating significant household allocation toward foot care and style. The integration of advanced cushioning technologies and sustainable materials has redefined product expectations. As per the Centers for Disease Control and Prevention, over 70% of adults are overweight or obese, which drives demand for supportive footwear that aids in weight management and joint protection. The rise of remote work has also blurred the lines between professional and leisure attire, making athletic shoes acceptable in more social contexts. This versatility ensures consistent relevance across diverse demographic segments. The market is characterized by rapid innovation cycles where brands compete on comfort, durability, and aesthetic appeal. Environmental consciousness further influences purchasing decisions as shoppers seek eco-friendly options.

MARKET DRIVERS

Rising Health Consciousness and Participation in Fitness Activities Fuel Demand

The increasing emphasis on personal health and wellness is fuelling the growth of the United States athletic footwear market. Americans are increasingly engaging in regular exercise routines to combat sedentary lifestyles and manage chronic conditions. The health club membership in the United States reached approximately 64 million individuals, reflecting a strong commitment to structured fitness, as per the study. This participation necessitates specialized footwear that provides adequate support, cushioning, and stability to prevent injuries during high-impact activities. Running remains one of the most popular forms of exercise, with millions of participants requiring durable shoes that can withstand repetitive stress. The running shoes account for the largest share of athletic footwear sales due to their universal appeal and frequent replacement cycle. The trend toward preventive healthcare encourages individuals to invest in high-quality gear that enhances performance and safety. Moreover, the proliferation of fitness apps and wearable technology has gamified exercise, creating a community-driven motivation to stay active. Social media platforms showcase fitness journeys, influencing peers to adopt similar habits and purchase corresponding apparel. The psychological benefit of exercise also drives repeat purchases as consumers associate new shoes with renewed motivation. Government initiatives promoting physical activity in schools and communities further embed these habits from a young age.

Integration of Athletic Footwear into Casual Fashion Trends Expands Usage Occasions

The emergence of performance technology with streetwear aesthetics has transformed athletic shoes into versatile fashion staples, which is fuelling the growth of the United States athletic footwear market. This phenomenon, known as athleisure, allows consumers to wear sneakers in non-athletic settings such as offices, social gatherings, and travel. The comfort offered by modern foam midsoles and breathable uppers appeals to individuals who prioritize ease of movement throughout the day. Celebrity endorsements and collaborations with high-fashion designers have elevated the status of sneakers, making them coveted luxury items. The global sneaker culture has created a secondary market for limited edition releases, driving hype and exclusivity. Younger generation, Millennials and Gen Z, particularly, view sneakers as a form of self-expression and status symbol. This cultural shift reduces the stigma associated with wearing sports shoes in formal environments, expanding the total addressable market. Brands respond by releasing colorways and designs that align with current fashion trends rather than just performance metrics. The versatility of these products means consumers own multiple pairs for different occasions, increasing overall volume. Additionally, the rise of remote work has relaxed dress codes, further normalizing athletic footwear in daily life.

MARKET RESTRAINTS

Environmental Concerns Regarding Synthetic Material Usage and Waste Generation

The growing scrutiny over its environmental footprint due to heavy reliance on synthetic materials, such as polyester, nylon, and rubber, is restraining the growth of the United States athletic footwear market. These petroleum-based components are difficult to recycle and contribute significantly to landfill waste. According to the Environmental Protection Agency, approximately 13 million tons of textile waste were generated in the United States, with footwear representing a substantial portion due to its complex construction. Consumers are increasingly aware of the ecological impact of their purchases, leading to hesitation in buying products from brands with poor sustainability records. The production process involves high energy consumption and chemical usage, which exacerbates carbon emissions. Regulatory pressures are mounting as states introduce stricter waste management laws and extended producer responsibility schemes. Brands face challenges in transitioning to bio-based or recycled materials without compromising performance, durability, or cost. The complexity of shoe assembly with glued layers makes disassembly for recycling technically difficult and expensive. Greenwashing accusations further erode trust when claims do not match actual practices. This environmental backlash forces companies to invest heavily in research for circular design principles. Balancing ecological responsibility with commercial viability remains a significant hurdle for market expansion.

Supply Chain Vulnerabilities and Raw Material Price Volatility Impact Profitability

The global supply chains, primarily located in Asia for manufacturing and raw material sourcing, are additionally hindering the growth of the United States athletic footwear market. This dependence exposes brands to geopolitical tensions, trade disputes, and logistical disruptions that can delay production and increase costs. Manufacturing indices have shown fluctuations due to shortages in key inputs like rubber and foam compounds. Fluctuating oil prices directly affect the cost of synthetic materials, which constitute a major part of shoe composition. The producer prices for footwear materials have experienced volatility, impacting profit margins for manufacturers and retailers. Tariffs imposed on imports from certain countries add another layer of financial burden, forcing companies to rethink sourcing strategies. The lack of domestic manufacturing capacity limits flexibility in responding to sudden demand spikes or supply shocks. Natural disasters in producing regions can halt operations, causing ripple effects across the global network. Inventory management becomes challenging as businesses struggle to predict lead times accurately. These uncertainties often result in stockouts or excess inventory, both of which negatively affect financial performance. Smaller brands with limited resources are particularly vulnerable to these disruptions. While some companies are exploring nearshoring options, the transition is slow and capital-intensive.

MARKET OPPORTUNITIES

Adoption of Circular Economy Models and Sustainable Innovation Initiatives

The shift toward circular economy principles for brands to differentiate themselves and capture eco-conscious consumers is creating new opportunities for the growth of the United States athletic footwear market. Innovations in recyclable materials and take-back programs allow companies to reduce waste and create closed-loop systems. The members are increasingly adopting tools like the Higgs Index to measure and improve environmental performance. Brands that successfully implement recycling technologies can transform old shoes into new products or raw materials, reducing reliance on virgin resources. Such initiatives resonate with younger demographics, who prioritize sustainability in purchasing decisions. Collaborations with material science startups enable the development of bio-based foams and plant-based leathers that offer comparable performance. The resale market for athletic footwear is also expanding, providing opportunities for brands to engage in certified pre-owned segments. Regulatory incentives for sustainable practices further encourage investment in green technologies. This transition not only mitigates environmental risks but also opens new revenue streams. Brands that lead in sustainability can command premium pricing and enhance brand equity.

Expansion into Digital Commerce and Virtual Try-On Technologies

The acceleration of digital transformation offers immense potential for enhancing customer experience and driving sales through online channels, and to leverage the growth of the United States athletic footwear market. Advanced technologies, such as augmented reality and artificial intelligence, enable virtual try-ons and personalized fit recommendations, reducing return rates. Merchants using augmented reality features report a significant increase in conversion rates as customers gain confidence in their purchases. The convenience of online shopping combined with detailed product information appeals to busy consumers seeking efficiency. Direct-to-consumer models allow brands to gather valuable data on consumer preferences, enabling targeted marketing and product development. Social commerce integrates shopping seamlessly into social media platforms, where influencers showcase products to engaged audiences. The use of big data analytics helps optimize inventory management and predict trends accurately. Subscription services for regular replacements or exclusive access create recurring revenue streams. Mobile apps provide personalized experiences with loyalty rewards and early access to launches. The integration of omnichannel strategies allows customers to buy online and pick up in store, bridging the gap between digital and physical retail. This digital ecosystem enhances engagement and fosters brand loyalty.

MARKET CHALLENGES

Counterfeiting and Intellectual Property Theft Undermine Brand Integrity

The prevalence of counterfeit athletic footwear affects brand reputation and revenue integrity, which is one of the major challenges for the growth of the United States footwear market. High demand for popular sneaker models creates a lucrative market for fake products that mimic established designs. These inferior copies often fail to meet safety and performance standards, potentially causing injuries to consumers. The seizures of counterfeit footwear remain high, indicating the scale of the issue. Counterfeits dilute brand exclusivity and erode consumer trust in authentic products. The rise of online marketplaces makes it easier for counterfeiters to reach unsuspecting buyers, who may not distinguish between real and fake items. Legal enforcement is challenging due to the cross-border nature of these operations and varying intellectual property laws. Brands must invest heavily in anti-counterfeiting technologies, such as holograms and blockchain verification. However, these measures add to production costs and complexity. The presence of fakes also disrupts pricing strategies and devalues limited edition releases. Consumers who inadvertently purchase counterfeits may develop negative perceptions of the brand. Protecting intellectual property requires constant vigilance and collaboration with law enforcement agencies.

Intense Competition and Market Saturation Limit Growth Potential

The high saturatedsaturationerous established players and emerging brands competing for consumer attention, which is also hampering the growth of the United States athletic footwear market. This intense rivalry leads to aggressive marketing campaigns and price wars that compress profit margins. The number of footwear brands available in the US has increased significantly, making differentiation difficult. Consumers are spoiled for choice, leading to fragmented loyalty and frequent brand switching. The promotional discounts have become common practice, as brands strive to clear inventory and attract bargain hunters. This environment makes it challenging for new entrants to gain traction without substantial investment. Established brands must continuously innovate to maintain relevance, which increases research and development costs. The pressure to release new collections frequently can lead to product fatigue among consumers. Retail shelf space is limited, forcing brands to compete fiercely for visibility. Online advertising costs have risen as competition for digital attention intensifies. Smaller brands struggle to match the marketing budgets of giants, limiting their reach. The saturation also leads to shorter product life cycles, requiring faster turnover and efficient supply chains. Failure to adapt quickly to trends can result in obsolete inventory. This competitive landscape demands strategic agility and strong brand storytelling.

REPORT COVERAGE

|

| DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.35% |

| Segments Covered | By Product Type, End User, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Nike, Adidas, PUMA, Under Armour, New Balance, Skechers, ASICS, Brooks Sports, Reebok, Converse |

SEGMENTAL ANALYSIS

By Product Type Insights

The running shoes segment was the largest by accounting for 31.2% of the United States athletic footwear market share in 2025, with the widespread participation in running as a primary form of cardiovascular exercise. This category encompasses performance-oriented footwear designed for road and track running, which appeals to both competitive athletes and casual joggers. The accessibility of running as a low-cost activity that requires minimal equipment beyond a reliable pair of shoes. The health benefits associated with regular running, including weight management and improved mental health, further sustain demand. The adults who engage in regular aerobic activity, like running, have a lower risk of chronic diseases, which motivates consistent participation. Technological advancements in cushioning and energy return have also enhanced the appeal of modern running shoes, encouraging frequent upgrades. Major brands invest heavily in research to develop proprietary foam technologies that reduce impact stress on joints. The proliferation of running clubs and marathons across the country creates a community-driven environment that reinforces product loyalty. Furthermore, the integration of running into daily commuting and fitness routines ensures steady replacement cycles. The versatility of running shoes for walking and gym use also broadens their utility.

The outdoor shoes segment is expected to grow at the fastest CAGR of 7.2% from 2026 to 2034, with the increasing popularity of outdoor recreational activities and the desire for nature-based experiences post-pandemic. Consumers are increasingly seeking adventure tourism and weekend getaways that involve trekking, climbing, and trail running. According to the Outdoor Foundation, participation in outdoor activities reached record levels, with over 160 million Americans engaging in at least one outdoor activity annually. This shift toward nature-centric leisure drives demand for specialized footwear that offers superior traction, durability, and protection on uneven terrains. As per data from the National Park Service, visitation numbers have surged, indicating a robust interest in exploring natural landscapes. The design evolution of outdoor shoes has made them more versatile, allowing for a transition from trails to urban settings. Modern trail shoes feature lightweight materials and waterproof membranes that appeal to consumers seeking all-weather functionality. The rise of social media platforms showcasing outdoor adventures inspires followers to adopt similar lifestyles and purchase appropriate gear. Brands are responding by launching eco-friendly outdoor lines that align with the environmental values of nature enthusiasts. The durability of these products also justifies higher price points, contributing to revenue growth. This convergence of lifestyle trends and product innovation positions the outdoor shoes segment for sustained rapid expansion.

By End User Insights

The men's segment held a prominent share of the United States athletic footwear market in 2025, with the higher participation rates in high-impact sports and greater frequency of product replacement. Male consumers typically engage in activities, such as basketball, football, and running, which require specialized footwear with robust support and durability. The cultural emphasis on sports performance among men encourages investment in premium technical shoes that enhance athletic capabilities. The sneaker culture also plays a significant role, with men often collecting limited edition releases and collaborating with brands for exclusive designs. This hobbyist approach leads to multiple purchases beyond functional needs. The availability of a wide range of sizes and widths for men further facilitates market penetration. Corporate wellness programs often target male employees, encouraging physical activity and subsequent footwear purchases. Additionally, the trend of wearing athletic shoes in casual and professional settings has normalized their use among men of all ages. The durability requirements for male-dominated sports mean that shoes wear out faster, necessitating regular replacements.

The women's segment is expected to register the fastest CAGR of 6.8% from 2026 to 2034, with the increasing female participation in fitness and the expansion of style-focused product lines. Historically underserved by the industry, women now have access to footwear specifically designed for female biomechanics and aesthetic preferences. The participation in sports among girls and women has increased significantly, with millions engaging in running, yoga, and team sports. This rise in activity levels directly translates to higher demand for specialized athletic shoes. The women are increasingly purchasing athletic footwear for lifestyle use, blending performance with fashion trends. The rise of female influencers and athletes endorsing brands has empowered women to view athletic shoes as symbols of strength and style. Brands are responding by launching dedicated women’s collections with diverse colorways and fits that cater to narrower heels and wider forefeet. The focus on inclusivity and body positivity in marketing campaigns resonates strongly with female consumers. Additionally, the growth of women-specific fitness communities and events fosters a sense of belonging and encourages gear acquisition. The expansion of plus-size offerings ensures that women of all body types can find suitable footwear.

By Distribution Channel Insights

The specialty stores segment was the largest by holding 56.3% of the United States athletic footwear market share in 2025 due to the expertise and extensive product assortments they offer. These stores provide a curated shopping experience, where knowledgeable staff assist customers in selecting the right footwear based on foot type and activity level. The specialty retailers account for a significant portion of athletic footwear sales as consumers value personalized service and fitting technologies. The ability to try on multiple brands and models in one location allows shoppers to compare features and comfort levels effectively. Many specialty stores offer gait analysis and professional fitting services, which build trust and loyalty among serious athletes. The presence of flagship stores in major urban centers serves as a brand showcase, enhancing visibility and prestige. Exclusive releases and limited edition drops are often available only through these channels, driving foot traffic and urgency. The immersive store environments with interactive displays and testing areas enhance the overall shopping experience. Consumers perceive specialty stores as authoritative sources for high-performance gear, reducing the perceived risk of purchasing expensive footwear. The strong relationships between retailers and manufacturers ensure timely access to new launches.

The online stores segment is likely to grow at a CAGR of 9.5% from 2026 to 2034, with the convenience, extensive selection, and advanced digital tools. E-commerce platforms allow consumers to browse thousands of styles and sizes from the comfort of their homes, eliminating geographical constraints. The online sales of footwear have grown consistently as logistics and return policies have improved, making digital shopping more reliable. The integration of augmented reality and virtual try-on technologies helps mitigate the inability to physically test shoes, increasing consumer confidence. The brands that offer detailed size guides and customer reviews see higher conversion rates and lower return rates. Direct-to-consumer websites enable brands to control the customer journey and offer exclusive products not available in retail stores. Subscription models and loyalty programs further enhance retention by providing perks such as early access and free shipping. The ability to compare prices across multiple retailers instantly empowers consumers to find the best deals. Social media integration allows for seamless discovery and purchase through shoppable posts. The pandemic accelerated the shift to online shopping habits, which have persisted as consumers appreciate the time savings.

COMPETITION OVERVIEW

The competitive landscape of the United States athletic footwear market is characterized by intense rivalry among global giants and emerging niche brands. Established players leverage strong brand equity and extensive distribution networks to maintain dominance while innovating continuously to stay relevant. New entrants challenge incumbents by offering unique designs and targeted marketing to specific consumer segments. Price competition is fierce in the mass market segment, whereas prestige brands compete on exclusivity and technology. The rise of digital commerce has lowered barriers to entry, allowing direct-to-consumer brands to gain traction quickly. Consumer loyalty is increasingly fragmented as shoppers prioritize comfort, style, and sustainability over brand heritage alone. Retailers play a crucial role by curating assortments that balance popular staples with trending items. Private label offerings from major retailers add further pressure on branded manufacturers. Intellectual property protection is vital as counterfeiting remains a persistent issue. Companies must adapt rapidly to changing consumer preferences and technological advancements. Success depends on balancing innovation with operational efficiency and strong brand storytelling. This dynamic environment requires constant vigilance and strategic agility to sustain long-term growth and profitability.

KEY MARKET PLAYERS

A few major players of the U.S athletic footwear market include

- Nike

- Adidas

- PUMA

- Under Armour

- New Balance

- Skechers

- ASICS

- Brooks Sports

- Reebok

- Converse

Top Strategies Used by Key Market Participants

Key players in the United States athletic footwear market employ diverse strategies to maintain a competitive advantage and drive growth. Product innovation remains central, with companies investing heavily in research and development to create advanced cushioning and sustainable materials. Brands focus on direct-to-consumer channels by enhancing digital platforms and mobile apps to offer personalized shopping experiences. Strategic collaborations with athletes, celebrities, and fashion designers help generate hype and cultural relevance. Sustainability initiatives are increasingly important as consumers demand eco-friendly products and transparent supply chains. Companies also leverage data analytics to optimize inventory and predict trends accurately. Omnichannel integration ensures seamless experiences between online and physical stores. Limited edition releases create scarcity and drive urgency among sneaker enthusiasts.

Leading Players in the United States Athletic Footwear Market

- Nike Inc maintains its leadership position through continuous innovation in performance technology and strong brand storytelling. The company focuses on developing proprietary materials such as ZoomX foam and Air cushioning systems that enhance athlete performance. Recent actions include expanding its direct-to-consumer digital platforms, which allow for personalized shopping experiences and exclusive product releases. Nike has also invested heavily in sustainability initiatives, aiming to reduce its carbon footprint through recycled materials in shoe production. Collaborations with high-profile athletes and celebrities keep the brand culturally relevant and desirable among younger demographics. The company leverages data analytics to optimize inventory management and predict consumer trends accurately.

- Adidas North America strengthens its market presence by blending sports performance with streetwear culture through strategic partnerships and innovative designs. The company focuses on boosting its Boost and Primeknit technologies to offer superior comfort and style to consumers. Recent efforts include collaborations with major fashion brands and influencers to create limited edition sneakers that generate significant hype and demand. Adidas has also prioritized sustainability by launching footwear made from ocean plastic waste, appealing to environmentally conscious shoppers. The brand enhances its digital ecosystem by improving mobile app features and online retail capabilities to engage directly with customers. Investments in local community sports programs help build brand loyalty and grassroots support.

- Under Armour Inc contributes to the market by focusing on high-performance footwear designed for serious athletes and fitness enthusiasts. The company emphasizes technical innovation in areas such as energy return and stability, catering to running and training segments. Recent actions include revamping its product lines with updated technologies like HOVR and Flow foam to improve comfort and durability. Under Armour has strengthened its digital presence by enhancing its e-commerce platform and leveraging data for personalized marketing campaigns. The brand collaborates with professional athletes to validate product performance and build credibility among core consumers. Efforts to streamline operations and reduce costs have improved efficiency and profitability. Under Armour also focuses on expanding its women’s category with specialized designs that address specific biomechanical needs.

MARKET SEGMENTATION

This research report on the US athletic footwear market has been segmented and sub-segmented based on product type, end user, distribution channel & region.

By Product Type

- Training Shoes

- CrossFit/Cross Training

- Running Shoes

- Performance

- Lifestyle Shoes

- Skateboarding

- Outdoor Shoes

- Trail

- Others

By End User

- Men

- Women

- Children

By Distribution Channel

- Supermarket/ Hypermarket

- Specialty Stores/Sporting Goods Stores

- Department Stores

- Online Stores/E-commerce

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What factors are driving the growth of the U.S. athletic footwear market?

Growing health awareness, increasing participation in sports and fitness activities, rising athleisure trends, and technological advancements in footwear are driving market growth.

2. Which product segment is leading the market?

Running shoes and lifestyle sneakers hold a major share due to strong consumer demand and fashion trends.

3. Who are the major players in the U.S. athletic footwear market?

Major players include Nike, Adidas, PUMA, Under Armour, and New Balance.

4. Which consumer group contributes most to market demand?

Young adults, fitness enthusiasts, athletes, and fashion-conscious consumers are major contributors to market demand.

5. What technologies are commonly used in athletic footwear?

Common technologies include cushioned midsoles, breathable materials, lightweight foam, energy-return soles, and smart shoe technologies.

6. Why are sustainable athletic shoes becoming popular?

Consumers are increasingly demanding eco-friendly footwear made from recycled and sustainable materials.

7. Which distribution channels dominate the market?

Sporting goods stores, branded retail outlets, supermarkets, and e-commerce platforms are major distribution channels.

8. What challenges does the U.S. athletic footwear market face?

High competition, counterfeit products, fluctuating raw material prices, and supply chain disruptions are major challenges.

9. How does innovation influence consumer purchasing decisions?

Consumers prefer shoes with advanced comfort, durability, performance enhancement, and stylish designs.

10. What is the future outlook for the U.S. athletic footwear market?

The market is expected to grow steadily due to increasing fitness participation, rising sneaker culture, digital retail expansion, and innovation in sustainable footwear.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com