U.S Concierge Medicine Market Size, Share, Trends & Growth Forecast Report Segmented By Application (Primary Care, Cardiology, Pediatrics, Psychiatry, Internal Care, Others), And Country (California, Washington, Oregon, New York & Rest Of The United States) – Industry Analysis And Forecast, 2026 To 2034

Market Size, 2025

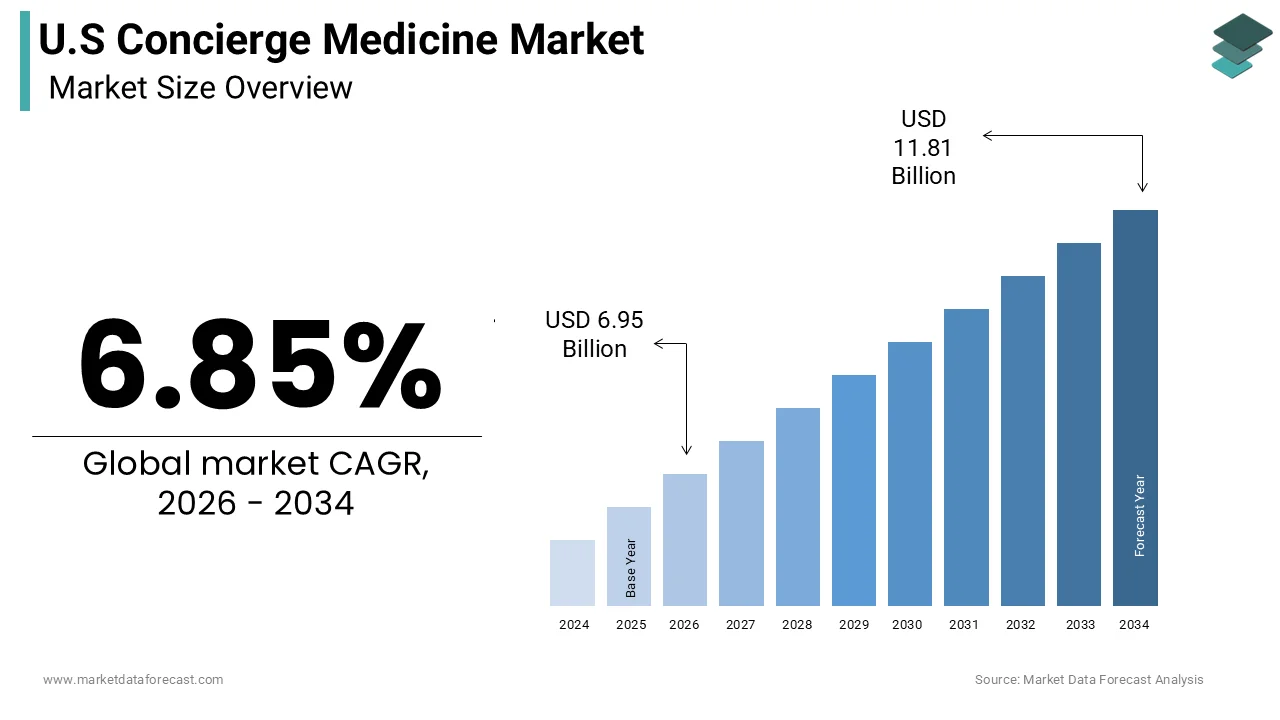

$6.50 BnMarket Estimate, 2026

$6.95 BnMarket Forecast, 2034

$11.81 BnCAGR, 2026–2034

6.85%U.S Concierge Medicine Market Size

The U.S concierge medicine market size was calculated to be USD 6.50 billion in 2025 and is anticipated to be worth USD 11.81 billion by 2034, from USD 6.95 billion in 2026, growing at a CAGR of 6.85% during the forecast period.

Concierge medicine is a transformative shift in primary care delivery characterized by a direct financial relationship between patients and physicians. This model bypasses traditional insurance reimbursement structures, allowing providers to offer enhanced accessibility, personalized attention, and comprehensive health management services. Patients typically pay an annual membership fee, which grants them unlimited or extended access to their physician, including same-day appointments, prolonged consultation time,s and 24/7 communication via digital platforms. The fundamental appeal lies in the restoration of the doctor-patient relationship, which has often been strained by the high-volume requirements of fee-for-service models. As per the American Medical Association, approximately 10500 physicians in the United States practiced concierge or direct primary care in 2025, reflecting a steady adoption of this alternative care structure. The increasing dissatisfaction with conventional healthcare systems, where average wait times for appointments can exceed several weeks.

MARKET DRIVERS

Escalating Dissatisfaction With Traditional Primary Care Accessibility

The profound dissatisfaction with the accessibility and quality of traditional primary care is majorly fuelling the growth of the United States concierge medicine market. Patients in conventional settings often face significant barriers, including prolonged wait times for appointments, brief consultations, and limited availability of their preferred physicians. This delay can exacerbate health issues and lead to increased utilization of emergency services for non-urgent conditions. In contrast, concierge practices guarantee same-day or next-day appointments, ensuring that patients receive immediate attention when needed. The average duration of a visit in a traditional practice is approximately 15 to 20 minutes, whereas concierge physicians often spend 45 to 60 minutes with each patient, allowing for thorough evaluations and detailed discussions. This extended interaction fosters a deeper understanding of the patient’s health history and lifestyle factors, leading to more accurate diagnoses and effective treatment plans. Furthermore, the administrative burden on traditional physicians often results in burnout, affecting the quality of care provided.

Rising Prevalence Of Chronic Diseases And Demand For Preventive Care

The escalating prevalence of chronic diseases and the subsequent demand for proactive preventive care are additionally escalating the growth of the United States concierge medicine market. Chronic conditions, such as hypertension, diabetes, and obesity, require continuous monitoring and lifestyle modifications, which are often difficult to achieve in fragmented traditional care settings. As per the Centers for Disease Control and Prevention, 6 in 10 adults in the United States have a chronic disease, and four in ten have two or more, highlighting the urgent need for comprehensive management strategies. Concierge medicine emphasizes preventive measures, including advanced screening, nutritional counseling, and fitness planning to mitigate the risk of disease progression. This proactive approach aligns with the growing consumer preference for wellness-oriented healthcare rather than reactive sick care. Patients enrolled in concierge practices are more likely to adhere to preventive guidelines due to the consistent support and accountability provided by their physicians. Concierge physicians utilize sophisticated health tracking technologies to monitor vital signs and biomarkers in real time, enabling early intervention when abnormalities are detected. This level of engagement empowers patients to take ownership of their health, leading to improved outcomes and quality of life. The aging population further amplifies this demand as older adults require more frequent and specialized medical attention.

MARKET RESTRAINTS

High Out-of-Pocket Costs Limiting Market Accessibility

The substantial out-of-pocket costs associated with the advanced technologies are slowly hindering the growth of the United States concierge medicine market. Unlike traditional primary care, which is often covered partially or fully by insurance plans, concierge services require patients to pay an annual membership fee that ranges from 1500 to 5000 dollars or more, depending on the level of service provided. This fee is typically not reimbursable by insurance companies, creating a financial barrier for middle and lower-income households. Consequently, concierge medicine remains largely accessible to affluent individuals who can afford these extra costs without financial strain. This economic disparity limits the market potential to a niche segment of the population, excluding a vast majority of Americans who might benefit from enhanced primary care services. Furthermore, the lack of transparency in pricing and service offerings can deter potential clients who are uncertain about the value proposition. Some practices charge additional fees for specialized tests or procedures not included in the base membership,ip adding to the overall cost burden. The perception of concierge medicine as a luxury service rather than a necessary healthcare option further restricts its appeal.

Regulatory Ambiguity And Insurance Reimbursement Complexities

The regulatory ambiguity and complexities surrounding insurance reimbursement are impeding the growth of the United States concierge medicine market. The legal framework governing concierge practices varies by state, creating uncertainty for physicians regarding compliance with federal and state healthcare laws. One major concern is the potential violation of anti-kickback statutes and the False Claims Act if concierge fees are perceived as influencing referral patterns or billing practices. The physicians must navigate intricate regulations to ensure that their membership models do not conflict with Medicare or Medicaid guidelines. For instance, Medicare beneficiaries may face restrictions on participating in concierge practices if the membership fee is considered a duplicate payment for services already covered by the program. This regulatory landscape discourages some physicians from adopting the concierge model due to the risk of legal repercussions and administrative burdens. Additionally, the lack of standardized coding and billing procedures for concierge services complicates interactions with insurance providers. While some practices operate on a direct primary care basis without billing insurance, others have hybrid models that attempt to integrate both systems, leading to confusion and inefficiencies. The absence of clear guidance from regulatory bodies creates a precarious environment for practitioners who must constantly adapt to changing rules. This uncertainty hinders the standardization of concierge care and limits its integration into the mainstream healthcare ecosystem. Physicians must invest significant resources in legal counsel and compliance measures, further increasing operational costs.

MARKET OPPORTUNITIES

Integration Of Advanced Digital Health Technologies

The integration of advanced digital health technologies is expected to bolster the growth of the United States concierge medicine market. Concierge practices are uniquely positioned to leverage telemedicine, remote monitoring devices, and artificial intelligence-driven analytics to deliver superior patient care. The adoption of wearable health trackers allows physicians to monitor patients’ vital signs continuously, providing real-time data that facilitates early detection of health issues. According to a report by the Consumer Technology Association, sales of wearable health devices in the United States exceeded 50 million units in 2025, indicating a robust infrastructure for remote health monitoring. Concierge physicians can utilize this data to personalize treatment plans and adjust interventions promptly, improving health outcomes. Telemedicine platforms enable seamless communication between patients and providers, allowing for virtual consultations that save time and enhance accessibility. This digital integration supports the concierge model’s promise of 24/7 availability and immediate response to patient concerns. Furthermore, artificial intelligence tools can analyze large datasets to identify health trends and predict potential risks, enabling proactive preventive care. The use of electronic health records integrated with mobile applications empowers patients to access their health information securely and engage actively in their care management. These technological advancements not only enhance the efficiency of concierge practices but also elevate the patient experience by providing convenient and personalized services.

Expansion Into Corporate Wellness And Employer-Sponsored Programs

The expansion of concierge medicine into corporate wellness and employer-sponsored programs is another factor that is also boosting the growth of the United States concierge medicine market. Employers are increasingly recognizing the value of preventive care in reducing healthcare costs and improving employee productivity. By partnering with concierge practices, companies can provide their employees with access to high-quality primary care services that emphasize wellness and early intervention. According to the International Foundation of Employee Benefit Plans, 68% of employers expressed interest in incorporating direct primary care or concierge models into their benefit packages in 2025 to manage rising healthcare expenditures. These partnerships allow employers to negotiate fixed annual fees for their workforce, providing predictable healthcare costs and eliminating surprise bills for employees. Concierge practices can tailor their services to meet the specific health needs of corporate populations, including stress management, ergonomic assessments, and chronic disease prevention programs. This B2B model expands the customer base beyond individual affluent clients to include large groups of employees, thereby enhancing economies of scale. Furthermore, improved employee health leads to reduced absenteeism and higher job satisfaction, which are key metrics for corporate success. The ability to offer exclusive health benefits also serves as a recruitment and retention tool for companies competing for top talent.

MARKET CHALLENGES

Physician Burnout And Workforce Sustainability Issues

The physician burnout and workforce sustainability for long-term viability are one of the major challenges for the growth of the United States concierge medicine market. While the concierge model is often touted as a solution to burnout due to smaller patient panels, the transition from traditional practice can be stressful and financially risky for physicians. Establishing a concierge practice requires significant upfront investment in marketing infrastructure and legal compliance, which can be daunting for independent practitioners. The pressure to maintain a full panel of paying members to sustain revenue can create financial instability, particularly in the initial years of operation. Additionally, the limited number of concierge practices means that there are fewer opportunities for physicians to collaborate and share best practices, leading to professional isolation. The aging physician workforce further exacerbates this challenge as older doctors may be reluctant to adopt new business models or invest in the necessary technological upgrades. The shortage of primary care physicians in the United States means that those who do transition to concierge models leave behind patients in traditional settings, potentially worsening access issues for the general population. This ethical dilemma creates tension within the medical community and may lead to regulatory scrutiny. Ensuring a sustainable pipeline of physicians willing and able to enter the concierge space is critical for market growth.

Equity And Access Disparities In Healthcare Delivery

The issue of equity and access disparities in healthcare delivery also inhibits the growth of the United States concierge medicine market. By catering primarily to affluent individuals, who can afford membership fees, concierge practices risk exacerbating existing health inequalities in the United States. This two-tiered system, where wealthy patients receive superior care while others struggle with limited access, raises ethical concerns among healthcare advocates and policymakers. The United States ranks last among high-income countries in terms of healthcare equity and access, amplifying the systemic issues that concierge medicine may inadvertently reinforce. Critics argue that the migration of primary care physicians to concierge models reduces the availability of providers for underserved populations, particularly in rural and low-income urban areas. This brain drain from traditional practices can lead to longer wait times and reduced quality of care for Medicaid and uninsured patients. The perception of concierge medicine as an elitist service can generate public backlash and political pressure for stricter regulations or taxes on membership fees. Furthermore, the lack of diversity in the patient population of concierge practices limits the ability of physicians to address health disparities and social determinants of health effectively. Addressing these equity concerns is essential for the social license of concierge medicine to operate.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.85% |

| Segments Covered | By Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | MDVIP, SignatureMD, PartnerMD, Specialdocs Consultants, Crossover Health, One Medical, Castle Connolly Private Health Partners, Priority Physicians, Destination Health MD, Hint Health, Concierge Choice Physicians, Peninsula Doctor, U.S. Preventive Medicine, HealthLynked, Privia Health |

SEGMENTAL ANALYSIS

By Application Insights

The primary care segment accounted in holding 34.2% of the United States concierge medicine market share in 2025, owing to the fundamental role of primary care physicians in managing overall health, preventive screenings, and chronic disease management, which aligns perfectly with the value proposition of concierge medicine. Patients seek primary care concierge services to establish a long-term relationship with a physician who can coordinate their healthcare needs across various specialties. The American Academy of Family Physicians states that there are approximately 135000 family physicians in the United States, many of whom are transitioning to or incorporating concierge models to reduce administrative burdens and improve patient care quality. Concierge primary care offers this continuity, ensuring that patients receive personalized attention and timely interventions. The Centers for Disease Control and Prevention reports that chronic diseases account for 90% of the nation's healthcare expenditures, highlighting the critical need for effective primary care management. By focusing on preventive measures and early detection, concierge primary care practices help reduce the incidence of severe complications, thereby lowering overall healthcare costs for patients.

The psychiatry segment is swiftly emerging at an anticipated CAGR of 12.5% during the forecast period, with the increasing recognition of mental health as a component of overall well-being. The stigma surrounding mental health issues is gradually diminishing, encouraging more individuals to seek professional help. The National Alliance on Mental Illness reports that 1 in 5 adults in the United States experiences mental illness each year, highlighting the vast need for accessible psychiatric services. Concierge psychiatry offers a unique advantage by providing longer consultation times, private settings, and immediate access to care, which are often lacking in traditional mental health services. The shortage of psychiatrists in the conventional system, where wait times can extend to several months, has created a significant gap that concierge practices are filling. Patients are willing to pay premium fees for the confidentiality and personalized attention that concierge psychiatrists provide. The integration of telepsychiatry has further accelerated this growth, allowing patients to receive care from the comfort of their homes.

COMPETITION OVERVIEW

The competition in the United States concierge medicine market is characterized by a mix of established national networks, independent practitioners, and emerging digital health startups. Major players compete by differentiating their service offerings through specialized care models such as functional medicine or tech-enabled primary care. Customer retention is a key focus area with providers leveraging superior patient experiences and continuous engagement to maintain membership levels. Technology plays a pivotal role in competition as companies invest in user-friendly apps and virtual care platforms to enhance accessibility. Pricing strategies vary, with some firms positioning themselves as premium luxury services while others aim for broader affordability through scaled operations. Strategic partnerships with corporations and insurance providers are increasingly used to gain a competitive advantage and secure stable revenue streams. The entry of large tech companies into the healthcare space further intensifies competition by introducing innovative solutions and disrupting traditional models. Regulatory compliance and quality assurance remain critical differentiators as patients seek trustworthy and reliable care providers.

KEY MARKET PLAYERS

A few major players of the U.S concierge medicine market include

- MDVIP

- SignatureMD

- PartnerMD

- Specialdocs Consultants

- Crossover Health

- One Medical

- Castle Connolly Private Health Partners

- Priority Physicians

- Destination Health MD

- Hint Health

- Concierge Choice Physicians

- Peninsula Doctor

- U.S. Preventive Medicine

- HealthLynked

- Privia Health

Top Strategies Used by Key Market Participants

Key players in the United States concierge medicine market primarily employ strategies such as strategic acquisitions, technological integration, and geographic expansion to strengthen their positions. Companies increasingly acquire smaller practices or technology firms to broaden their service offerings and enhance operational efficiency. The integration of advanced digital health platforms, including telemedicine and remote monitoring tools, is a critical strategy for improving patient accessibility and engagement. Providers focus on developing proprietary software solutions that streamline administrative tasks and facilitate seamless communication between patients and physicians. Geographic expansion into underserved urban and suburban areas allows firms to tap into new customer bases and increase market penetration. Partnerships with employers and insurance companies are also common tactics to offer concierge services as part of corporate wellness programs. These collaborations help stabilize revenue streams and expand reach beyond individual consumers. Additionally, companies invest heavily in branding and marketing to differentiate their services and highlight the value of preventive care. Educational initiatives targeting both physicians and patients promote the benefits of concierge models. These combined strategies ensure sustained growth and competitiveness in the dynamic healthcare landscape.

Leading Players in the United States Concierge Medicine Market

- MDVIP stands as a prominent player in the United States concierge medicine market by operating a large network of affiliated primary care practices across multiple states. The company focuses on providing comprehensive annual wellness exams and preventive care services to its members through a standardized model. MDVIP supports its affiliated physicians with marketing, administrative services, and clinical protocols, ensuring consistent quality of care. Recent actions include the expansion of its network into new geographic regions and the integration of advanced diagnostic technologies such as genetic testing and cardiac screening. The company emphasizes a data-driven approach to health management, utilizing electronic health records to track patient outcomes and improve service delivery. This hybrid model allows for scalability while maintaining the personalized touch of concierge care. MDVIP also invests in physician education and support, helping practitioners transition smoothly from traditional fee-for-service models. Its focus on preventive care and chronic disease management aligns with the growing demand for proactive health solutions. The company’s strategic partnerships with laboratories and imaging centers further enhance the value proposition for members.

- One Medical has established itself as a key innovator in the United States concierge medicine market by combining human-centered care with advanced technology. The company operates a membership-based primary care model that integrates digital tools with in-person visits to provide seamless healthcare experiences. One Medical utilizes a proprietary platform that allows patients to book appointments, access medical records, and communicate with providers online. The company focuses on creating a welcoming and efficient environment for patients, reducing wait times, and improving satisfaction. One Medical also emphasizes preventive care and wellness, offering personalized health plans and coaching services. Its approach appeals to tech-savvy individuals and corporations seeking modern healthcare solutions. The company’s acquisition by Amazon has further amplified its reach and resources, enabling greater investment in technology and service expansion. This strategic move positions One Medical to leverage Amazon’s logistics and cloud computing capabilities to enhance healthcare delivery. The integration of retail health concepts with primary care creates new opportunities for member engagement.

- Parsley Health represents a distinct segment of the United States concierge medicine market by focusing on functional medicine and holistic wellness. The company combines primary care with nutrition, fitness, and mental health support to address the root causes of chronic diseases. Parsley Health utilizes a membership model that provides patients with access to a multidisciplinary team of healthcare providers, including doctors, nutritionists, and health coaches. Recent actions include the development of digital health programs and the expansion of its virtual care offerings to reach a broader audience. The company emphasizes personalized care plans based on comprehensive health assessments and laboratory testing. Parsley Health’s approach appeals to individuals seeking alternative and integrative medicine solutions for conditions such as autoimmune disorders and hormonal imbalances. The company invests heavily in content creation and education, empowering patients to make informed health decisions. Its digital platform facilitates continuous engagement and support, fostering a community-oriented approach to wellness. Parsley Health’s focus on lifestyle medicine differentiates it from traditional concierge practices, attracting a niche but growing segment of health-conscious consumers.

MARKET SEGMENTATION

This research report on the U.S concierge medicine market has been segmented and sub-segmented based on application & region.

By Application

- Primary Care

- Cardiology

- Pediatrics

- Psychiatry

- Internal Care

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What is the expected growth rate of the U.S. concierge medicine market?

The market is expected to grow at a healthy pace during the forecast period, driven by rising healthcare expenditures, an aging population, and growing interest in preventive care.

2. What factors are driving the growth of the concierge medicine market in the United States?

Key growth drivers include increasing demand for personalized healthcare, shorter waiting times, better physician-patient relationships, and the expansion of telehealth services.

3. How does concierge medicine differ from traditional healthcare models?

Unlike traditional healthcare, concierge medicine limits the number of patients per physician, allowing doctors to spend more time with each patient and provide more individualized care.

4. Who are the primary users of concierge medicine services?

Primary users include high-income individuals, executives, retirees, patients with chronic conditions, and people seeking personalized and convenient healthcare experiences.

5. What are the benefits of concierge medicine for patients?

Benefits include improved physician accessibility, longer consultations, personalized treatment plans, reduced waiting times, proactive healthcare management, and enhanced patient satisfaction.

6. What challenges are affecting the growth of the U.S. concierge medicine market?

Major challenges include high membership costs, limited affordability for some patients, physician shortages, and concerns regarding healthcare accessibility and equity.

7. How is telemedicine influencing concierge healthcare services?

Telemedicine enhances concierge care by enabling virtual consultations, remote monitoring, digital health management, and convenient communication between physicians and patients.

8. How are technological advancements shaping the concierge medicine industry?

Technologies such as electronic health records, AI-driven health analytics, wearable health devices, remote patient monitoring, and telehealth platforms are improving care delivery and patient engagement.

9. What are the future opportunities in the U.S. concierge medicine market?

Future opportunities include expanding telehealth integration, growing demand for preventive healthcare, increasing adoption among aging populations, personalized wellness programs, and partnerships with employers seeking premium healthcare benefits.

10. Who are the leading companies operating in the U.S. concierge medicine market?

Leading companies include MDVIP, SignatureMD, PartnerMD, Specialdocs Consultants, One Medical, Concierge Choice Physicians, Crossover Health, and Privia Health.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com