U.S. Dermal Fillers Market Size, Share, Trends & Growth Forecast Report By Material, Product, Application, End User, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Dermal Fillers Market Report Summary

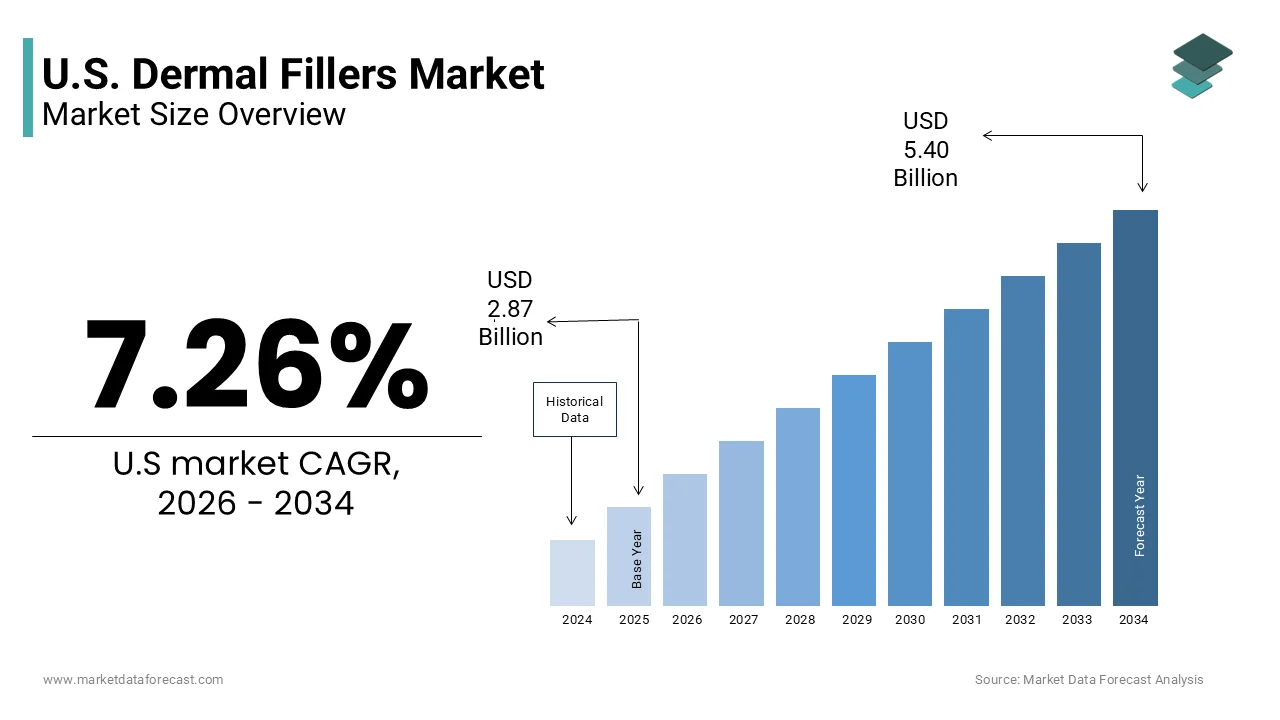

The U.S. dermal fillers market was valued at USD 2.87 billion in 2025, is estimated to reach USD 3.08 billion in 2026, and is projected to reach USD 5.40 billion by 2034, growing at a CAGR of 7.26% during the forecast period. Market growth is driven by increasing demand for minimally invasive cosmetic procedures, rising awareness regarding aesthetic enhancement treatments, and growing aging population concerns related to facial appearance and skin rejuvenation. Dermal fillers are widely used for wrinkle correction, facial contouring, lip enhancement, and skin volumization due to shorter recovery times and non surgical treatment benefits. The growing popularity of personalized aesthetic procedures and advancements in injectable technologies are further supporting strong market expansion across the United States.

Key Market Trends

- Rising demand for minimally invasive aesthetic procedures is driving market growth.

- Increasing consumer focus on anti aging and facial rejuvenation treatments is boosting dermal filler adoption.

- Growing popularity of personalized cosmetic enhancement procedures is supporting market expansion.

- Expansion of medical aesthetic clinics and dermatology centers is enhancing treatment accessibility.

- Innovation in biodegradable fillers, long lasting formulations, and advanced injection techniques is influencing market development.

Segmental Insights

- Based on material, the hyaluronic acid segment accounted for a substantial share of the U.S. dermal fillers market in 2025. This dominance is attributed to its biocompatibility, natural appearance, and widespread use in facial volumizing procedures.

- Based on product, the biodegradable fillers segment held a significant share of the U.S. dermal fillers market in 2025, driven by increasing preference for safe, temporary, and naturally absorbable filler materials.

- Based on application, the wrinkle correction treatment segment accounted for 33.5% of the U.S. dermal fillers market share in 2025, supported by rising demand for anti aging and skin rejuvenation procedures.

Regional Insights

- The U.S. dermal fillers market is experiencing strong growth across aesthetic clinics, dermatology centers, and cosmetic surgery practices, supported by rising beauty consciousness and increasing acceptance of non surgical cosmetic procedures. The growing influence of social media and celebrity driven beauty trends is further strengthening market development.

Competitive Landscape

The U.S. dermal fillers market is highly competitive, with key players focusing on advanced injectable technologies, long lasting filler formulations, and expansion of aesthetic treatment portfolios to strengthen their market position. Companies are investing in research and development, physician training programs, and minimally invasive cosmetic innovations. Prominent players in the U.S. dermal fillers market include Allergan Aesthetics, Revance Therapeutics, Inc., Merz Pharma, GALDERMA, Suneva Medical, Prollenium Medical Technologies, Bioxis pharmaceuticals, and Sinclair.

U.S. Dermal Fillers Market Size

The U.S. dermal fillers market size was valued at USD 2.87 billion in 2025, is estimated to reach USD 3.08 billion in 2026, and is projected to reach USD 5.40 billion by 2034, growing at a CAGR of 7.26% from 2026 to 2034.

Dermal fillers are a dynamic segment of the medical aesthetics industry focused on minimally invasive procedures designed to restore volume, smooth wrinkles, and enhance facial contours. These injectable treatments primarily utilize hyaluronic acid calcium hydroxylapatite poly L lactic acid and polymethylmethacrylate to achieve natural looking rejuvenation without the need for surgical intervention. The sector is characterized by rapid technological advancements and an expanding consumer base that increasingly views aesthetic enhancements as part of routine self care. According to the American Society of Plastic Surgeons 2022 Statistics Report, there were over 23.7 million cosmetic minimally invasive procedures performed in the United States in 2022. Soft tissue fillers (hyaluronic acid) accounted for over 4.8 million of these, representing a significant portion of the total. The American Board of Cosmetic Surgery notes that demand has surged among individuals aged 35 to 50 who seek preventive aging solutions. Regulatory oversight by the Food and Drug Administration ensures that only approved substances enter the market maintaining high safety standards. The Centers for Disease Control and Prevention emphasizes the importance of sterile injection practices to prevent complications such as infections or vascular occlusions. Consumer confidence is further bolstered by the availability of board certified practitioners who adhere to strict clinical guidelines. As social media continues to influence beauty standards the acceptance of aesthetic treatments has grown across diverse demographics. This market landscape reflects a shift toward non surgical options that offer immediate results with minimal downtime appealing to busy professionals and younger consumers alike.

MARKET DRIVERS

Growing Social Acceptance and Destigmatization of Aesthetic Procedures

The increasing social acceptance and destigmatization of aesthetic procedures is a primary driver for the United States dermal fillers market. This trend is fueled by shifting cultural perceptions that view these treatments as mainstream wellness practices. Historically cosmetic interventions were often kept private but today they are openly discussed on social media platforms and celebrated in popular culture. This openness is largely driven by influencers and celebrities who transparently share their experiences with dermal fillers normalizing the practice for a broader audience. Furthermore the concept of self care has expanded to include aesthetic enhancements as a means of boosting confidence and mental well being. The American Psychological Association notes that improving physical appearance can positively impact self esteem and social interaction. As a result individuals are more willing to invest in non surgical options that offer subtle yet effective improvements. Medical spas and dermatology clinics have responded by creating welcoming environments that emphasize education and consultation rather than just sales. This cultural shift reduces the psychological barrier to entry allowing the market to expand beyond traditional affluent demographics to include middle income consumers who prioritize personal grooming and anti aging maintenance as part of their lifestyle.

Technological Advancements in Product Formulation and Longevity

Technological advancements in product formulation and longevity are also propelling the growth of the United States dermal fillers market. This offers safer more effective and longer lasting solutions for patients. Modern hyaluronic acid based fillers have evolved to include cross linking technologies that enhance stability and resistance to enzymatic degradation thereby extending the duration of results. These innovations enable practitioners to treat a wider range of concerns from fine lines to deep volume loss with greater predictability. The American Academy of Dermatology states that advanced fillers can last between 12 to 24 months depending on the treatment area and product type reducing the frequency of touch up appointments for patients. Additionally the development of reversible fillers using hyaluronidase enzymes provides a safety net for patients concerned about adverse outcomes or unsatisfactory results. This reversibility increases consumer confidence and willingness to try treatments for the first time. Manufacturers are also investing in research to create bio stimulatory fillers that encourage collagen production offering gradual and long term improvements in skin quality. The National Institutes of Health supports ongoing studies into biomaterials that integrate seamlessly with human tissue minimizing inflammation and allergic reactions. These scientific breakthroughs not only improve clinical outcomes but also expand the addressable market by attracting patients who previously hesitated due to concerns about safety or temporary effects.

MARKET RESTRAINTS

Stringent Regulatory Oversight and Approval Processes

Stringent regulatory oversight and complex approval processes are significantly restraining the expansion of the United States dermal fillers market. This limits the speed at which new products can reach consumers. The Food and Drug Administration requires rigorous clinical trials to demonstrate the safety and efficacy of dermal fillers before granting approval which can take several years and involve substantial financial investment. Under the FDA's Premarket Approval (PMA) process for Class III devices, manufacturers must present scientific evidence mitigating severe risks like granuloma formation, vascular occlusion, and filler migration. This lengthy timeline delays the introduction of innovative products to the market potentially stifling competition and keeping prices high. Additionally post market surveillance requirements mandate that manufacturers monitor and report adverse events which adds to operational costs. Any safety concerns raised during this period can lead to recalls or restricted usage guidelines impacting brand reputation and sales. While these measures protect public health they also create barriers to entry for novel technologies. Consequently the pace of innovation may slow as companies prioritize compliance over rapid development. This regulatory environment necessitates that firms maintain robust quality assurance systems which can be resource intensive particularly for emerging biotechnology startups seeking to disrupt the established market landscape.

High Cost and Lack of Insurance Coverage for Cosmetic Procedures

The high cost of dermal filler treatments combined with the lack of insurance coverage further limits the growth of the United States dermal fillers market. This limits accessibility to affluent consumers. Dermal fillers are classified as elective cosmetic procedures meaning they are not covered by health insurance plans regardless of medical necessity or psychological benefit. According to the American Society of Plastic Surgeons the average cost of soft tissue fillers ranges from 600 to 800 dollars per syringe with many patients requiring multiple syringes to achieve desired results. This financial burden excludes a large segment of the population who may desire aesthetic improvements but cannot afford out of pocket expenses. Furthermore the temporary nature of most fillers necessitates repeat treatments every 6 to 18 months creating a recurring financial commitment that can be unsustainable for middle income earners. Medical spas often offer financing options but interest rates and eligibility criteria can still pose barriers. As a result the market remains skewed toward higher income demographics limiting overall volume growth. Economic downturns or periods of financial uncertainty further exacerbate this issue as consumers cut back on non essential services. This economic constraint forces providers to compete heavily on price and promotions which can erode profit margins and impact the perceived value of premium brands.

MARKET OPPORTUNITIES

Expansion into Male Aesthetics and Gender Neutral Marketing

The proliferation into male aesthetics and gender-neutral marketing offers a substantial opportunity for the US dermal fillers market. This is because of the fact that societal norms around masculinity evolve. Traditionally cosmetic procedures were marketed predominantly to women but there is a growing trend of men seeking aesthetic enhancements to maintain a youthful and professional appearance. Historically tracked data published by the American Society of Plastic Surgeons (ASPS) and affiliated cosmetic organizations shows that the number of men seeking aesthetic intervention has experienced a massive shift, with male cosmetic procedures rising by over 28% since the turn of the millennium as minimally invasive treatments dominate the market. This demographic shift is driven by competitive job markets where younger appearances are often associated with vitality and relevance. Men typically seek treatments for specific areas such as the jawline chin and under eye regions to achieve a more defined and rested look. Marketing campaigns are increasingly adopting inclusive language and imagery that appeal to male consumers without compromising masculine ideals. The Pew Research Center indicates that attitudes toward gender roles are becoming more flexible allowing men to engage in self care practices without stigma. Clinics are responding by offering specialized consultations that address male anatomical differences and aesthetic goals. Additionally corporate wellness programs are beginning to include aesthetic treatments as part of holistic health benefits attracting professional men who value efficiency and discretion. This untapped segment offers significant growth potential as awareness increases and tailored products are developed. By addressing the unique needs of male patients manufacturers and providers can diversify their customer base and reduce reliance on traditional female dominated markets. This strategic pivot aligns with broader cultural trends toward inclusivity and individual expression.

Integration of Artificial Intelligence in Treatment Planning and Personalization

The integration of artificial intelligence in treatment planning and personalization provides a clear path for the growth of the United States dermal fillers market. This enhances precision and patient satisfaction. AI powered imaging tools allow practitioners to simulate potential outcomes and customize treatment plans based on individual facial anatomy and aging patterns. According to the American Academy of Facial Plastic and Reconstructive Surgery digital simulation technologies improve communication between doctors and patients by providing visual expectations before procedures begin. This transparency builds trust and reduces anxiety leading to higher conversion rates and patient loyalty. AI algorithms can analyze skin texture volume loss and symmetry to recommend optimal filler types and injection sites ensuring natural looking results. The National Institutes of Health supports research into machine learning applications that predict long term outcomes and potential complications enabling proactive risk management. Furthermore AI driven inventory management systems help clinics optimize stock levels and reduce waste by predicting demand trends. Telemedicine platforms equipped with AI assessment tools allow for remote consultations expanding access to patients in rural or underserved areas. The Federal Communications Commission promotes broadband expansion which facilitates the adoption of these digital health solutions. By leveraging technology providers can offer a premium personalized experience that differentiates them from competitors. This innovation not only improves clinical efficacy but also streamlines operations reducing administrative burdens. Consumers are becoming more tech-savvy, driving a higher expectation for personalized, data-driven care. In this evolving aesthetic landscape, AI integration has become a key competitive advantage.

MARKET CHALLENGES

Risk of Vascular Complications and Adverse Events

The risk of vascular complications and adverse events poses a major challenge to the United States dermal fillers market. Safety concerns can deter potential patients and lead to legal liabilities. Although rare incidents such as vascular occlusion blindness or skin necrosis can occur if filler is inadvertently injected into blood vessels. According to the American Society of Plastic Surgeons proper anatomical knowledge and injection techniques are critical to preventing these serious complications. However variations in practitioner skill levels and the proliferation of non medical injectors increase the likelihood of errors. High profile cases of complications reported in media can create public fear and skepticism regarding the safety of fillers. Malpractice insurance premiums for aesthetic practitioners have risen reflecting the increased legal risks associated with these procedures. The Food and Drug Administration issues safety communications to educate both providers and consumers about risks emphasizing the importance of seeking qualified medical professionals. Despite these efforts misinformation spreads quickly on social media amplifying fears. Patients may hesitate to undergo treatments due to anxiety about permanent damage or disfigurement. This challenge necessitates continuous education and rigorous adherence to safety protocols. Manufacturers must also provide comprehensive training programs for clinicians to ensure competent administration. Failure to address these safety concerns can result in stricter regulations and reduced consumer confidence impacting market growth and reputation.

Proliferation of Counterfeit and Unapproved Products

The proliferation of counterfeit and unapproved dermal filler products is a critical barrier to the United States dermal fillers market. This undermines consumer safety and brand integrity. Illicit imports and black market sales of fake fillers containing unsafe substances such as silicone or industrial grade materials pose severe health risks. According to the Food and Drug Administration numerous seizures of counterfeit aesthetic products have been recorded at US borders indicating a persistent supply chain vulnerability. These unregulated products often lack sterility and proper labeling leading to infections allergic reactions and permanent tissue damage. The American Medical Association warns that patients seeking cheaper alternatives online or at unlicensed facilities are particularly at risk. Social media platforms sometimes facilitate the sale of these dangerous products bypassing regulatory oversight. The Federal Trade Commission monitors deceptive marketing practices but the anonymity of online transactions makes enforcement difficult. Counterfeit goods erode trust in legitimate brands as consumers may associate negative outcomes with the entire category rather than just the fake product. Legal battles to protect intellectual property rights are costly and time consuming for manufacturers. Additionally the presence of cheap counterfeits creates unfair price competition forcing authorized distributors to lower margins. The Centers for Disease Control and Prevention collaborates with law enforcement to track outbreaks linked to illegal injections highlighting the public health threat. Combating this issue requires coordinated efforts among regulators manufacturers and healthcare providers to educate consumers and secure distribution channels. The market faces ongoing reputational and safety challenges. This will continue until these illicit markets are curtailed.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.26% |

| Segments Covered | By Material, Product, Application, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Allergan Aesthetics (AbbVie Inc.), Revance Therapeutics, Inc., Merz Pharma, GALDERMA, Suneva Medical, Prollenium Medical Technologies, Bioxis Pharmaceuticals, and Sinclair |

SEGMENTAL ANALYSIS

By Material Insights

The hyaluronic acid dominated the United States dermal fillers market and accounted for a substantial share in 2025. This dominance of the segment was driven by its exceptional biocompatibility versatility and reversibility. Also, this naturally occurring substance is found in human skin and connective tissues making it highly compatible with the body and reducing the risk of allergic reactions. According to the American Society of Plastic Surgeons hyaluronic acid based fillers account for the vast majority of soft tissue augmentation procedures performed annually in the country. The main driver of this dominance is the ability to reverse the effects of the treatment using hyaluronidase an enzyme that breaks down hyaluronic acid. This safety feature provides patients with peace of mind knowing that unsatisfactory results or complications can be corrected. The Food and Drug Administration has approved numerous hyaluronic acid products for various indications including lip augmentation and correction of moderate to severe facial wrinkles. The American Academy of Dermatology notes that the predictable outcomes and minimal downtime associated with these fillers make them the preferred choice for first time patients. Additionally manufacturers have developed varied formulations with different particle sizes and cross linking densities allowing practitioners to customize treatments for specific anatomical areas. From fine lines around the eyes to deep nasolabial folds hyaluronic acid offers a comprehensive solution. The widespread availability of these products in medical spas and dermatology clinics further cements their market leadership. Consumer awareness campaigns by major aesthetic brands have also educated the public on the benefits of hyaluronic acid reinforcing its status as the gold standard in non surgical facial rejuvenation.

On the other hand, the calcium hydroxylapatite segment is predicted to witness the highest CAGR of 6.2% from 2026 and 2034 due to its dual action of immediate volume restoration and long term collagen stimulation. This biodegradable material consists of microspheres suspended in a water based gel that provides instant results while stimulating the body to produce new collagen over time. According to clinical data published in dermatological journals calcium hydroxylapatite fillers can last up to 12 months or longer offering a durable solution for patients seeking sustained improvement. The American Board of Cosmetic Surgery highlights that calcium hydroxylapatite is particularly effective for treating deeper wrinkles and restoring volume in areas such as the cheeks and jawline. Its thicker consistency allows for structural support which is increasingly demanded by patients seeking facial contouring rather than just wrinkle smoothing. Furthermore the biostimulatory effect improves skin quality and elasticity providing added value beyond simple filling. As patients become more knowledgeable about anti aging mechanisms they are gravitating toward products that offer regenerative benefits. The safety profile of calcium hydroxylapatite is well established with a low incidence of adverse events when administered by trained professionals. Manufacturers are investing in educational programs to train providers on advanced injection techniques for this material expanding its application scope. This combination of longevity structural support and collagen induction drives the rapid expansion of the calcium hydroxylapatite segment in the competitive US market.

By Product Insights

The biodegradable fillers segment led the US dermal fillers market and captured a significant share in 2025. This leading position of the segment was attributed to consumer preference for temporary and reversible aesthetic enhancements. These products including hyaluronic acid calcium hydroxylapatite and poly L lactic acid are gradually absorbed by the body over time allowing patients to adjust their appearance as their preferences or facial structure changes. According to the American Society of Plastic Surgeons the majority of minimally invasive cosmetic procedures utilize biodegradable materials reflecting a shift away from permanent implants. One of the major drivers of this top position is the flexibility it offers patients who may wish to modify their look in the future without undergoing surgical removal. The Food and Drug Administration emphasizes the safety advantages of biodegradable fillers as they reduce the risk of long term complications such as migration or granuloma formation associated with permanent substances. Additionally the transient nature of these fillers aligns with current beauty trends that favor natural and subtle enhancements over dramatic alterations. Patients appreciate the ability to test different aesthetics before committing to more permanent solutions. The American Academy of Facial Plastic and Reconstructive Surgery notes that biodegradable fillers allow for periodic touch ups that maintain a refreshed appearance without looking overdone. This adaptability is particularly appealing to younger demographics who view aesthetic treatments as part of ongoing self care rather than one time fixes. The robust recycling of capital through repeat purchases also benefits providers creating a sustainable business model. Therefore, the demand for safe reversible and adaptable options ensures that biodegradable fillers remain the cornerstone of the US dermal aesthetics industry.

But the non biodegradable fillers segment is estimated to register the fastest CAGR of 11.2% during the forecast period owing to specific patient demands for permanent solutions in targeted applications. Polymethylmethacrylate or PMMA is the primary non biodegradable filler used in the United States offering long lasting correction for deep wrinkles and acne scars. The growth of this segment is fueled by patients who seek a one time treatment solution to avoid the recurring costs and maintenance associated with biodegradable fillers. The American Society for Dermatologic Surgery indicates that while overall preference leans toward temporary fillers there is a niche market of individuals who prioritize longevity and cost effectiveness over reversibility. PMMA microspheres provide a scaffold for collagen production resulting in permanent structural support. This appeals to older patients or those with significant volume loss who do not wish to undergo frequent injections. Additionally advancements in injection techniques have improved the safety profile of PMMA reducing the risk of nodules and irregularities. Practitioners are becoming more skilled in placing these fillers in deep subdermal layers where they are less likely to cause visible issues. The psychological benefit of a permanent fix also drives adoption among patients with body dysmorphic concerns or those who have had consistent satisfaction with previous temporary treatments. Regulatory scrutiny remains high. Nevertheless, the unique value proposition of permanence ensures continued interest and gradual expansion in this specialized segment.

By Application Insights

The wrinkle correction treatment segment was the largest by occupying a 33.5% share of the US dermal fillers market in 2025. This segment addresses the primary aging concern among consumers. Nasolabial folds marionette lines and forehead wrinkles are primary targets for filler injections due to their visibility and impact on facial expression. According to the American Society of Plastic Surgeons wrinkle correction accounts for the largest share of dermal filler procedures performed annually in the United States. The driving factor behind this dominance is the universal desire to maintain a youthful and rested appearance in both personal and professional contexts. The American Psychological Association notes that perceived age can influence social and occupational opportunities motivating individuals to seek effective anti aging solutions. Dermal fillers provide immediate and noticeable improvement in wrinkle depth restoring smoothness to the skin surface. The predictability of outcomes with hyaluronic acid based products makes them the go to choice for this application. Furthermore the minimally invasive nature of the procedure allows patients to return to daily activities quickly which is crucial for busy professionals. Media representation of aging often emphasizes smooth skin reinforcing the cultural imperative to reduce wrinkles. Clinics widely promote wrinkle correction packages attracting first time patients who are typically motivated by these visible signs of aging. The broad demographic appeal ranging from individuals in their 30s seeking prevention to those in their 60s seeking correction ensures a steady and high volume demand. This widespread applicability and strong cultural drive cement wrinkle correction as the primary application segment in the market.

But the lip enhancement segment is anticipated to witness the fastest CAGR of 7.5% between 2026 and 2034. This rapid expansion of the segment is propelled by shifting beauty standards and social media influence. Full and defined lips have become a prominent aesthetic ideal popularized by celebrities and influencers on platforms like Instagram and TikTok. According to the American Board of Cosmetic Surgery the number of lip augmentation procedures has increased significantly among younger demographics particularly those aged 20 to 35. The main driver is the desire for enhanced facial symmetry and proportion as lips play a central role in facial harmony. Younger consumers view lip fillers as a form of self expression and beauty enhancement rather than just anti aging. The accessibility of the procedure and relatively lower cost compared to full facial rejuvenation make it an entry point for many first time patients. Social media filters that exaggerate lip size have created a digital dysmorphia effect where individuals seek to replicate these enhanced features in real life. Practitioners have developed specialized techniques for lip shaping and volumizing that offer natural looking results avoiding the overfilled appearance associated with earlier trends. The American Academy of Dermatology highlights the importance of artistic skill in lip augmentation to achieve balanced outcomes. As stigma decreases and acceptance grows lip enhancement continues to attract a diverse patient base seeking to align their physical appearance with contemporary beauty ideals.

COUNTRY LEVEL ANALYSIS

The United States was the top performer in the North American dermal fillers market and captured a 90.8% share in 2025. This dominance of the US market was driven by its advanced healthcare infrastructure and high consumer spending power. The market status within the country is characterized by a mature yet rapidly evolving landscape driven by technological innovation and changing societal attitudes toward aesthetic enhancements. According to the American Society of Plastic Surgeons (ASPS), the United States consistently leads globally in the volume of cosmetic procedures, driven by millions of minimally invasive treatments like neuromodulator injections and fillers, which indicates a sustained high demand for aesthetic services. The presence of leading global manufacturers and a robust network of board certified practitioners ensures high standards of care and product availability. The Food and Drug Administration plays a critical role in regulating the market ensuring that only safe and effective products reach consumers which builds trust and confidence. Economic factors such as high disposable income and the availability of financing options facilitate access to aesthetic treatments for a broad segment of the population. The Centers for Disease Control and Prevention (CDC) provides essential infection control guidelines and investigates specific outbreaks. However, the continuous monitoring of safety trends and clinical practice improvements in plastic surgery is primarily led by professional organizations such as the ASPS and facility accreditation boards. Demographic shifts including an aging population seeking rejuvenation and a younger generation embracing preventive aesthetics drive sustained demand. The integration of digital marketing and telemedicine has further expanded reach allowing providers to engage with patients more effectively. Additionally the strong emphasis on research and development within the US fosters innovation in filler materials and injection techniques. This combination of regulatory rigor economic strength and cultural acceptance positions the United States as the premier market for dermal fillers setting trends that influence global practices and consumption patterns.

COMPETITIVE LANDSCAPE

The competition in the United States dermal fillers market is intense and characterized by the presence of several global pharmaceutical and aesthetic companies vying for dominance. Major players compete primarily on product efficacy safety profiles and brand reputation rather than price alone. The market is consolidated with a few key entities holding significant influence due to their established distribution channels and strong relationships with healthcare providers. Innovation plays a crucial role as companies strive to launch next generation fillers that offer longer lasting results and more natural appearances. Regulatory approval from the Food and Drug Administration serves as a significant barrier to entry ensuring that only high quality products reach the market. However this also limits the number of competitors allowing established brands to maintain their positions. Marketing efforts are heavily focused on educating both practitioners and consumers about the benefits and safety of specific products. Social media influence and celebrity endorsements also shape competitive dynamics by driving consumer demand for certain brands. Additionally companies invest in comprehensive training programs for injectors to ensure proper usage and minimize adverse events. This focus on education and safety helps build loyalty among medical professionals. The rise of medical spas and non physician injectors adds another layer of competition as accessibility increases. Overall the market requires continuous innovation and strategic marketing to maintain relevance and capture share in a highly discerning consumer landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. dermal fillers market are

- Allergan Aesthetics (AbbVie Inc.) (U.S.)

- Revance Therapeutics, Inc. (U.S.)

- Merz Pharma (Germany)

- GALDERMA (Switzerland)

- Suneva Medical (U.S.)

- Prollenium Medical Technologies (Canada)

- Bioxis pharmaceuticals (France)

- Sinclair (U.K.)

Top Players in the Market

- Allergan Aesthetics an AbbVie Company remains a pivotal force in the United States dermal fillers market with its extensive portfolio including the Juvederm collection. The company leverages its robust distribution network and strong brand recognition to maintain a dominant presence across medical spas and dermatology clinics. Recently Allergan has focused on expanding its educational initiatives for healthcare providers ensuring safe and effective injection techniques. The corporation continues to invest in research and development to introduce new formulations tailored to specific facial areas such as lips and cheeks. By launching innovative products with improved longevity and natural looking results Allergan strengthens its appeal to both practitioners and patients. The company also emphasizes digital marketing campaigns that highlight patient testimonials and before and after visuals. These strategic efforts reinforce its leadership by fostering trust and demonstrating clinical excellence while adapting to evolving consumer preferences for minimally invasive aesthetic enhancements.

- Galderma S.A. is a key participant in the US dermal fillers market known for its Restylane family of hyaluronic acid based products. The company distinguishes itself through a science driven approach focusing on personalized aesthetic solutions that cater to individual patient needs. Galderma actively collaborates with healthcare professionals to provide comprehensive training on facial anatomy and advanced injection methods. Recent actions include the introduction of new product variants designed for specific tissue depths and structural support enhancing treatment precision. The firm also invests in digital tools that assist practitioners in treatment planning and patient consultation. By prioritizing safety and efficacy Galderma builds strong relationships with clinicians who value evidence based outcomes. The company’s commitment to sustainability and ethical sourcing further enhances its brand reputation. These initiatives enable Galderma to capture a loyal customer base and maintain a competitive edge in the dynamic landscape of non surgical facial rejuvenation.

- Merz Aesthetics contributes significantly to the US dermal fillers market with its diverse range of products including Belotero and Radiesse. The company focuses on innovation and quality delivering solutions that address various aesthetic concerns from fine lines to volume loss. Merz actively supports healthcare providers through extensive educational programs and clinical workshops promoting best practices in aesthetic medicine. Recently the company has expanded its product line to include combination therapies that integrate fillers with neuromodulators for holistic facial rejuvenation. This approach appeals to patients seeking comprehensive anti aging treatments. Merz also leverages digital platforms to engage with consumers and raise awareness about the benefits of professional aesthetic care. By emphasizing patient safety and satisfaction Merz strengthens its market position. The company’s strategic partnerships with leading dermatologists and plastic surgeons ensure widespread adoption of its products. These efforts collectively drive growth and reinforce its status as a trusted provider in the competitive US aesthetics industry.

Top Strategies Used by Key Market Participants

Key players in the United States dermal fillers market primarily employ product innovation strategies to differentiate their offerings and meet evolving consumer demands. Companies invest heavily in research and development to create fillers with enhanced longevity natural feel and safety profiles. Educational initiatives are another critical strategy as firms provide extensive training to healthcare providers on injection techniques and facial anatomy. This ensures optimal patient outcomes and builds trust in their brands. Strategic partnerships with medical spas and dermatology clinics help expand distribution networks and increase market reach. Digital marketing and social media engagement are utilized to educate consumers and reduce stigma around aesthetic procedures. Companies also focus on regulatory compliance to maintain high safety standards and protect brand reputation. Additionally some firms pursue acquisitions of smaller biotechnology companies to access novel technologies and broaden their product portfolios. These combined strategies enable participants to sustain competitiveness and drive growth in a mature yet dynamic market environment.

MARKET SEGMENTATION

This research report on the U.S. dermal fillers market is segmented and sub-segmented into the following categories.

By Material

- Hyaluronic Acid

- Calcium Hydroxylapatite

- Poly-L-lactic Acid

- PMMA (Poly (methyl methacrylate))

- Fat Fillers

- Others

By Product

- Biodegradable

- Non-biodegradable

By Application

- Scar Treatment

- Wrinkle Correction Treatment

- Lip Enhancement

- Restoration of Volume/Fullness

- Others

By End User

- Specialty & Dermatology Clinics

- Hospitals & Clinics

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1.What is driving the growth of the U.S. dermal fillers market?

The growth of the U.S. dermal fillers market is driven by increasing demand for minimally invasive cosmetic procedures, rising awareness regarding aesthetic treatments, and advancements in filler technologies.

2.What are dermal fillers used for?

Dermal fillers are used for wrinkle reduction, facial contouring, lip enhancement, scar treatment, and restoration of facial volume and fullness.

3.Which materials are commonly used in dermal fillers?

Common materials used in dermal fillers include hyaluronic acid, calcium hydroxylapatite, poly L lactic acid, PMMA, and fat fillers.

4.Why is hyaluronic acid widely used in dermal fillers?

Hyaluronic acid is widely used because it provides natural looking results, improves skin hydration, and offers temporary yet effective facial enhancement.

5.What are biodegradable dermal fillers?

Biodegradable dermal fillers are products that naturally break down and are absorbed by the body over time, making them safer and more commonly preferred for cosmetic procedures.

6.What applications are driving demand for dermal fillers in the United States?

Major applications driving demand include wrinkle correction, lip enhancement, scar treatment, facial contouring, and restoration of facial volume.

7.How are specialty and dermatology clinics contributing to market growth?

Specialty and dermatology clinics are contributing to market growth by offering advanced aesthetic procedures, personalized treatments, and increasing accessibility to cosmetic services.

8.What are the benefits of minimally invasive cosmetic procedures?

Minimally invasive cosmetic procedures provide shorter recovery times, reduced surgical risks, lower treatment costs, and quick visible results compared to traditional surgeries.

9.What challenges are faced by the U.S. dermal fillers market?

The market faces challenges such as high treatment costs, potential side effects, strict regulatory requirements, and concerns regarding counterfeit products.

10.Which companies are among the leading players in the U.S. dermal fillers market?

Leading companies in the U.S. dermal fillers market include Allergan Aesthetics, GALDERMA, Merz Pharma, Revance Therapeutics, and Prollenium Medical Technologies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com