U.S. Earth Observation Market Size, Share, Trends & Growth Forecast Report By Orbit, Solution, Imaging Resolution, Application, Technology, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

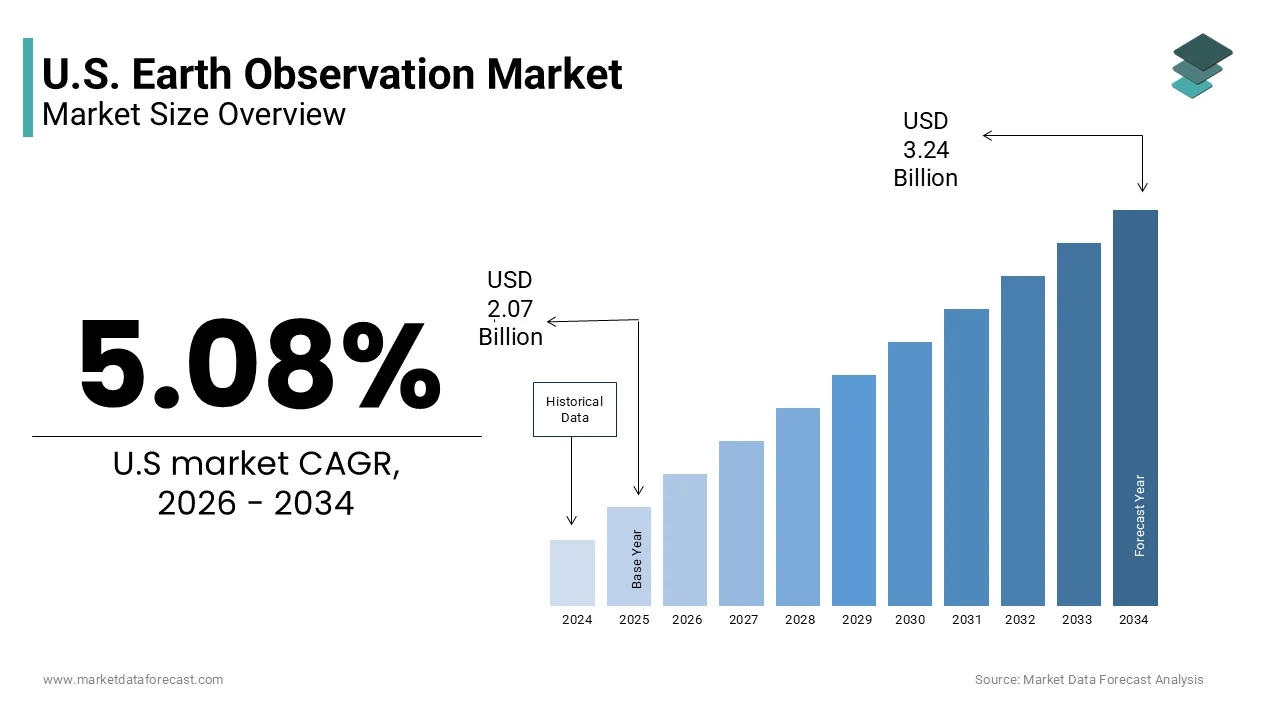

Market Size, 2025

$2.07 BnMarket Estimate, 2026

$2.18 BnMarket Forecast, 2034

$3.24 BnCAGR, 2026–2034

5.08%U.S. Earth Observation Market Report Summary

The U.S. earth observation market was valued at USD 2.07 billion in 2025, is estimated to reach USD 2.18 billion in 2026, and is projected to reach USD 3.24 billion by 2034, growing at a CAGR of 5.08% during the forecast period. Market growth is driven by increasing demand for satellite based monitoring, expanding geospatial intelligence applications, and rising adoption of earth observation technologies across defense, agriculture, environmental monitoring, and disaster management sectors. Advancements in satellite imaging capabilities, analytics platforms, and remote sensing technologies continue to strengthen market development across the United States.

Key Market Trends

- Growing demand for satellite based monitoring and geospatial intelligence is driving market growth.

- Increasing adoption of earth observation technologies across defense and environmental applications is boosting market expansion.

- Rising demand for very high resolution imaging and analytics solutions is supporting industry development.

- Expansion of commercial satellite constellations is enhancing data availability and operational capabilities.

- Innovation in remote sensing technologies and AI powered image analysis is influencing market advancement.

Segmental Insights

- Based on orbit type, the low earth orbit segment accounted for 53.1% of the U.S. earth observation market share in 2025. This dominance is attributed to lower latency, high resolution imaging capabilities, and increasing deployment of observation satellites in low earth orbit systems.

- Based on solution, the imagery data segment held a significant share of the U.S. earth observation market in 2025, supported by growing demand for geospatial intelligence and satellite imagery analytics.

- Based on imaging resolution, the very high resolution segment accounted for 45.6% of the U.S. earth observation market share in 2026, driven by increasing requirements for detailed observation capabilities across commercial and government applications.

- Based on application, the security and intelligence segment held 35.4% of the U.S. earth observation market share in 2025, supported by rising defense surveillance requirements and national security initiatives.

Regional Insights

- The United States remains a major contributor to the global earth observation industry due to strong defense investments, expanding commercial satellite ecosystems, and increasing adoption of remote sensing technologies across multiple sectors.

Competitive Landscape

The U.S. earth observation market is highly competitive, with companies focusing on satellite imaging innovation, geospatial analytics platforms, and next generation observation technologies to strengthen their market position. Market participants continue investing in advanced imaging capabilities and data intelligence solutions. Prominent players in the U.S. earth observation market include ImageSat International, SARsatX, ICEYE, Planet Labs PBC, Maxar Technologies, Northrop Grumman Corp, Lockheed Martin Corp, Airbus SE, Thales, and L3Harris Technologies Inc.

U.S. Earth Observation Market Size

The U.S. earth observation market size was valued at USD 2.07 billion in 2025, is estimated to reach USD 2.18 billion in 2026, and is projected to reach USD 3.24 billion by 2034, growing at a CAGR of 5.08%.

The earth observation is the satellites sensor and data analytic platforms designed to monitor physical chemical and biological systems of the planet. The strategic value of this infrastructure lies in its ability to provide real time insights into climate change, national security agriculture, and urban development. As per the National Oceanic and Atmospheric Administration, the United States operates a fleet of over 30 environmental satellites that collect critical data on weather patterns and atmospheric conditions daily. The integration of artificial intelligence with geospatial data has transformed raw imagery into predictive models enhancing decision making capabilities across industries. This extensive data repository supports diverse applications ranging from disaster response to resource management. The proliferation of small satellite constellations has further democratized access to high resolution imagery reducing latency and increasing revisit rates. Federal agencies, such as the Department of Defense and NASA continue to drive innovation through substantial investments in next generation sensor technologies. The emergence of commercial space capabilities with government mandates creates a dynamic environment, where data accuracy and accessibility are paramount.

MARKET DRIVERS

Increasing Government Investment in National Security and Defense

The increasing government investment in national security and defense is majorly lavishing the growth of the United States earth observation market. The Department of Defense relies heavily on satellite imagery for situational awareness target identification and mission planning in contested environments. According to the Department of Defense, annual budget request for fiscal year 2025 approximately 10 billion USD is allocated specifically for space based intelligence surveillance and reconnaissance programs. This substantial funding enables the development of advanced sensors capable of detecting subtle changes in terrain and infrastructure. The National Defense Strategy emphasizes the need for resilient and redundant space architectures to counter anti-satellite threats from near peer adversaries. The Pentagon is accelerating the deployment of low earth orbit constellations to provide global coverage with minimal latency. These systems integrate optical infrared and radar technologies to ensure all weather monitoring capabilities. The urgency to maintain technological superiority drives continuous innovation in image resolution and data processing speeds. Military operations increasingly depend on real time geospatial intelligence to support joint all domain command and control initiatives. The integration of commercial earth observation data into military networks further enhances operational flexibility and reduces costs. This strategic imperative ensures sustained demand for high performance earth observation solutions.

Rising Demand for Climate Monitoring and Environmental Data

The rising demand for climate monitoring and environmental data is greatly influencing the growth of the United States earth observation market. Federal and state agencies utilize satellite imagery to track greenhouse gas emissions, deforestation, and water resource depletion. According to the Environmental Protection Agency, the United States has committed to reducing net greenhouse gas emissions by 50% below 2005 levels by 2030. Earth observation satellites provide the granular data required to verify compliance with environmental regulations and assess the impact of conservation efforts. The National Aeronautics and Space Administration operates multiple missions dedicated to studying earth system science including sea level rise and ice sheet dynamics. The satellite data is essential for predicting extreme weather events such as hurricanes and wildfires, which are becoming more frequent due to climate change. Agricultural sectors also rely on this data to optimize irrigation and monitor crop health in response to changing climate conditions. The integration of earth observation data into climate models improves the accuracy of long term forecasts aiding policy makers in resource allocation. Private companies are increasingly leveraging this data to assess environmental risks for insurance and investment purposes. The growing awareness of climate change impacts drives both public and private sector investment in monitoring infrastructure. This trend ensures a steady demand for specialized sensors and analytics platforms.

MARKET RESTRAINTS

High Costs Associated with Satellite Development and Launch

The high costs associated with satellite development and launch, particularly for smaller enterprises and new entrants is limiting the growth of the United States earth observation market. Building a satellite involves complex engineering rigorous testing and expensive materials to withstand the harsh space environment. According to the Aerospace Corporation, the average cost to design build and test a medium sized earth observation satellite ranges from 100 million to 300 million USD excluding launch expenses. These financial barriers limit the ability of startups to compete with established defense contractors and government agencies. Launch services add another layer of expense although reusable rockets have reduced prices significantly. The long development cycles further delay return on investment requiring companies to secure long term funding commitments. Insurance premiums for space missions also contribute to the overall cost burden protecting against launch failures and orbital debris collisions. The complexity of obtaining regulatory approvals from the Federal Communications Commission and other agencies adds administrative costs and delays. These financial constraints force many innovators to rely on government contracts or venture capital which may not always be available. The high entry threshold consolidates market power among a few major players limiting competition and innovation.

Regulatory Complexities and Spectrum Allocation Issues

The regulatory complexities and spectrum allocation issues to the operational efficiency is impeding the growth of the United States earth observation market. Satellites require specific radio frequencies to transmit data to ground stations and these spectra are limited and highly contested. According to the Federal Communications Commission the process of obtaining spectrum licenses can take several years involving extensive coordination with international bodies such as the International Telecommunication Union. Delays in spectrum allocation hinder the deployment of new constellations and limit the bandwidth available for high resolution data transmission. The increasing number of satellites in low earth orbit exacerbates congestion leading to interference risks that degrade signal quality. The demand for spectrum resources is outpacing supply creating bottlenecks for emerging technologies. Compliance with export control regulations such as the International Traffic in Arms Restrictions that further complicates the global distribution of earth observation data and technology. Companies must navigate an intricate web of legal requirements to ensure their products do not violate national security protocols. The lack of harmonized international standards for data sharing and privacy also creates uncertainty for commercial operators.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Real Time Analytics

The integration of artificial intelligence for real time analytics is substantially inhibiting the growth of the United States earth observation market. Traditional methods of analyzing satellite imagery are time consuming and labor intensive whereas AI algorithms can process vast amounts of data instantly. The implementation of machine learning models has reduced the time required to identify objects in imagery from days to seconds. This capability enables immediate response to dynamic events such as natural disasters, military movements, or agricultural changes. The use of deep learning techniques enhances the accuracy of feature extraction allowing for the detection of subtle patterns that human analysts might miss. The AI driven platforms can predict crop yields with 90% accuracy by analyzing multispectral data over time, as per the study. This precision supports decision making in agriculture logistics and urban planning. Commercial providers are developing software as a service models that deliver actionable insights rather than raw data creating new revenue streams. The ability to automate routine monitoring tasks frees up resources for more complex analytical challenges. Government agencies are increasingly adopting AI tools to enhance their intelligence capabilities and improve operational efficiency. The synergy between earth observation and artificial intelligence opens up applications in autonomous vehicle navigation and infrastructure monitoring. This technological convergence drives innovation and expands the utility of geospatial data.

Expansion of Small Satellite Constellations for High Revisit Rates

The expansion of small satellite constellations for high revisit rates for enhancing the temporal resolution of earth observation data is additionally to elevate new opportunities for the growth of the United States earth observation market. Traditional large satellites often have long revisit times limiting their ability to monitor rapidly changing phenomena. Small satellites or CubeSats can be deployed in large numbers to provide daily or even hourly coverage of specific areas. This proliferation enables continuous monitoring of critical infrastructure agricultural fields and disaster zones. The modularity of small satellites allows for rapid technology upgrades and replacement of failed units ensuring consistent service availability. A leading provider of small satellite imagery their constellation captures images of the entire landmass of the earth every day. This high frequency data supports applications such as change detection supply chain monitoring and environmental compliance. Commercial users benefit from the ability to track assets and activities in near real time improving operational efficiency. The scalability of small satellite networks allows providers to tailor coverage to specific customer needs offering flexible pricing models. This shift towards distributed architectures reduces the risk of single point failures and enhances system resilience.

MARKET CHALLENGES

Threat of Space Debris and Orbital Congestion

The threat of space debris and orbital congestion to the sustainability and safety is to pose as a challenge for the growth of the United States earth observation market. The increasing number of satellites in low earth orbit raises the risk of collisions, which can generate cascading fragments known as the Kessler syndrome. A single collision can disable expensive earth observation assets and disrupt critical data services. The cost of maneuvering satellites to avoid debris increases fuel consumption and shortens mission lifespans. As per the United States Space Command, the frequency of close approach alerts has increased by 50% annually requiring constant monitoring and adjustment of satellite trajectories. The lack of effective debris removal technologies exacerbates the problem leaving defunct satellites and rocket stages in orbit for decades. Insurance premiums for space missions are rising due to the heightened risk of damage affecting the economic viability of new projects. Regulatory efforts to mitigate debris are still in early stages and lack enforceable international standards. The uncertainty surrounding long term orbital stability discourages investment in large constellations. Companies must invest in advanced collision avoidance systems adding to operational costs. The potential loss of key satellites due to debris impacts could disrupt national security and commercial operations.

Data Privacy and Security Concerns

The data privacy and security concerns is anticipated to decline the growth of the United States earth observation market. High resolution imagery can inadvertently capture sensitive information such as private property military installations and personal activities raising ethical and legal issues. The ability to monitor individuals from space without consent violates expectations of privacy and requires robust regulatory frameworks. The potential for misuse of geospatial data by malicious actors for surveillance or targeting adds to security risks. The protection of infrastructure data from cyber-attacks is a top priority necessitating advanced encryption and access control measures. The integration of earth observation data with other datasets, such as social media and location services amplifies privacy risks through re-identification possibilities. Companies must navigate complex legal landscapes including the General Data Protection Regulation for international operations and varying state laws within the United States. The lack of clear guidelines on data ownership and usage rights creates uncertainty for commercial providers and users. Breaches of data security can lead to reputational damage and legal liabilities undermining trust in earth observation services. The need to balance transparency with privacy protection requires careful policy development and technical safeguards.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.08% |

| Segments Covered | By Orbit, Solution, Imaging Resolution, Application, Technology, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | ImageSat International, SARsatX, ICEYE, Planet Labs PBC, Maxar Technologies, Northrop Grumman Corp, Lockheed Martin Corp, Airbus SE, Thales, and L3Harris Technologies Inc |

SEGMENTAL ANALYSIS

By Orbit Insights

The low earth orbit segment was accounted in holding 53.1% of the United States earth observation market share in 2025. Proximity advantages for high resolution and low latency data transmission drives the growth of the segment. Satellites in LEO orbit at altitudes between 160 and 2000 kilometers above the earth significantly closer than Geostationary Orbit satellites, which operate at 35786 kilometers. This closeness reduces signal travel time enabling near real time data delivery which is critical for time sensitive applications, such as disaster response and military surveillance. LEO satellites can achieve revisit times of less than one hour, when deployed in constellations providing continuous monitoring capabilities. The reduced distance also lowers the power requirements for transmission by allowing for smaller and more cost effective satellite designs. This efficiency enables the launch of large numbers of satellites creating robust networks that ensure data redundancy and reliability. The ability to capture detailed images of small objects such as vehicles and infrastructure supports a wide range of commercial applications including supply chain monitoring and urban planning. These technical benefits make LEO the most versatile and widely used orbit for earth observation missions.

The very low earth orbit segment is expected to witness a fastest CAGR of 14.5% from 2026 to 2034 owing to the enhanced image resolution and signal strength. Operating at altitudes below 450 kilometers that allows satellites to capture imagery with centimeter level detail, which is superior to standard LEO capabilities. According to the European Space Agency, satellites in VLEO can achieve resolution improvements of up to 50% compared to those at 600 kilometers due to the reduced distance to the target. This ultra-high resolution is critical for applications requiring precise identification such as infrastructure inspection and military intelligence. The assets provide stronger signal returns for radar systems by enhancing the quality of synthetic aperture radar data. The improved signal strength also reduces the size and power requirements for ground receivers making data access more accessible. The ability to monitor small changes in terrain or structures supports predictive maintenance and security applications. The strategic advantage of superior data quality justifies the higher operational complexities associated with this orbit.

By Solution Insights

The imagery data segment held a significant share of the United States earth observation market in 2025. Government agencies, such as the National Geospatial Intelligence Agency rely heavily on raw satellite imagery for national security and defense planning. This consistent demand ensures a steady revenue stream for imagery providers. The integration of commercial imagery into classified networks has expanded significantly enhancing situational awareness for military operations. The ability to access high resolution images of remote or hostile areas without physical presence is invaluable for strategic decision making. The sheer volume of data required for comprehensive monitoring drives large scale procurement contracts. Imagery data serves as the primary source for creating maps identifying targets and assessing damage after conflicts. The reliability and accuracy of optical and radar imagery make it indispensable for intelligence analysts. The ongoing modernization of defense systems further increases the need for timely and precise visual data.

The imagery data analytical service segment is anticipated to grow at a fastest CAGR of 16.2% from 2026 to 2034. Integration of artificial intelligence for automated insights is fuelling the growth of the United States earth observation market. Traditional manual analysis of satellite imagery is time consuming and prone to error, whereas AI algorithms can process vast datasets instantly. The efficiency is for applications, such as disaster response and military operations, where speed is essential. The use of machine learning models improves the accuracy of feature detection, such as identifying buildings vehicles and vegetation. Automated analytics allow for continuous monitoring of changes over time providing predictive insights for urban planning and environmental management. The ability to detect anomalies automatically enhances security and compliance monitoring for commercial clients. Software as a service models make these advanced analytics accessible to a broader range of users without requiring specialized expertise. The scalability of AI platforms allows providers to handle increasing data volumes efficiently. This technological transformation adds significant value to raw imagery creating new revenue opportunities.

By Imaging Resolution Insights

The very high resolution segment was accounted in holding 45.6% of the United States earth observation market share in 2026. Military operations require precise imagery to identify targets verify intelligence and assess battle damage. The ability to distinguish between different types of vehicles and structures provides a tactical advantage. As per the National Geospatial Intelligence Agency, over 80% of classified intelligence products utilize very high resolution data for accurate analysis. The detailed visual information supports counter terrorism efforts and border security monitoring. The strategic value of this data justifies the higher costs associated with its acquisition. Government contracts for very high-resolution imagery remain robust ensuring steady demand for providers. The continuous improvement in sensor technology enhances the clarity and usability of this data. The need for real time updates in dynamic security situations further drives the preference for very high resolution.

The medium resolution segment is lucratively growing at a fastest CAGR of 12.8% from 2026 to 2034. Suitability for large scale agricultural and environmental monitoring is elevating the growth of the segment. This resolution provides sufficient detail to assess crop health soil moisture and forest cover over vast areas. The medium resolution data from satellites like Landsat is used to monitor crop conditions across millions of acres. The broad coverage allows for regional analysis that is not feasible with very high-resolution imagery. The medium resolution sensors are essential for tracking climate change indicators, such as sea surface temperature and ice melt. Environmental agencies use this data to monitor water quality and detect pollution sources. The cost effectiveness of medium resolution imagery makes it accessible for routine monitoring programs. The ability to cover large geographic areas frequently supports timely decision making in agriculture and environmental management.

By Application Insights

The security and intelligence segment was the largest by holding 35.4% of the United States earth observation market share in 2025. Strategic imperative for national defense and border security sustains the dominance of Security and Intelligence in the United States earth observation market. The Department of Defense relies on satellite imagery for situational awareness and threat assessment in global hotspots. This funding ensures access to high quality and timely imagery for military operations. The earth observation data is for monitoring border activities and detecting illegal crossings. The ability to observe remote areas continuously enhances national security capabilities. The integration of commercial imagery into government networks expands coverage and reduces costs. The ongoing geopolitical tensions increase the demand for reliable intelligence sources. The strategic value of earth observation in maintaining national security ensures consistent investment.

The agriculture segment is projected to witness a fastest CAGR of 15.5% from 2026 to 2034. Adoption of precision farming techniques is likely to fuel the growth of the segment. Farmers use satellite data to monitor crop health soil conditions and weather patterns for optimized decision making. Earth observation provides the spatial data necessary for variable rate application of fertilizers and pesticides. As per the American Farm Bureau Federation, over 40% of large farms now use geospatial data for management purposes. The ability to detect issues early prevents losses and improves profitability. The integration of earth observation with farm machinery enables automated operations. The growing population and food demand necessitate efficient farming practices. This technological adoption drives consistent demand for agricultural earth observation services. The value of data driven farming ensures sustained growth in this segment.

COMPETITIVE LANDSCAPE

The competition in the United States earth observation market is characterized by intense rivalry among established defense contractors and innovative commercial space companies striving to deliver superior data and analytics. Major players compete based on image resolution revisit frequency and the sophistication of analytical tools provided to end users. The market features a mix of large integrated corporations and agile startups leveraging small satellite technology to disrupt traditional models. Companies differentiate themselves by offering specialized solutions for specific industries such as agriculture defense and environmental monitoring. Strategic alliances with technology firms enhance capabilities in artificial intelligence and cloud computing creating value added services. The barrier to entry remains high due to significant capital requirements for satellite development and launch operations. However, the decreasing cost of launch services has enabled new entrants to challenge incumbents. Intellectual property protection and proprietary algorithms serve as key competitive advantages.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. earth observation market include

- ImageSat International

- SARsatX

- ICEYE

- Planet Labs PBC

- Maxar Technologies

- Northrop Grumman Corp

- Lockheed Martin Corp

- Airbus SE

- Thales

- L3Harris Technologies Inc

Top Players in the Market

- Maxar Technologies stands as a premier provider of high resolution earth imagery and geospatial solutions in the United States. The company operates a sophisticated constellation of optical satellites that deliver critical data for national security and commercial applications. Recent actions include the expansion of its WorldView Legion satellite series which significantly enhances revisit rates and coverage capabilities. Maxar actively collaborates with government agencies to integrate artificial intelligence into image analysis workflows improving speed and accuracy. The firm focuses on delivering timely and precise intelligence to support defense operations and disaster response efforts. Their strategic emphasis on cloud based data platforms allows customers to access and process information efficiently. These initiatives reinforce its position as a key enabler of modern geospatial intelligence and maintain its competitive edge in the dynamic market landscape.

- Planet Labs PBC contributes significantly to the market through its extensive fleet of small satellites that provide daily global monitoring capabilities. The company specializes in high frequency data collection enabling users to track changes on the earth surface in near real time. The developments involve the launch of next generation Pelican satellites, which offer improved resolution and spectral bands for diverse applications. Planet Labs partners with agricultural and environmental organizations to deliver actionable insights for sustainability and resource management. The firm leverages machine learning algorithms to automate data processing and enhance user experience. Its focus on accessibility allows a broad range of clients from governments to enterprises to utilize earth observation data effectively. These efforts strengthen its role as a leader in continuous earth monitoring and support the growing demand for timely geospatial intelligence across various industries.

- Lockheed Martin Corporation plays a crucial role by developing advanced space systems and sensors for government earth observation missions. The company designs and builds sophisticated satellites that support weather forecasting climate research and national security objectives. Recent actions include the successful deployment of Next Generation Overhead Persistent Infrared satellites which enhance missile warning capabilities. Lockheed Martin integrates cutting edge technologies such as artificial intelligence and cyber security into its space architectures. The firm collaborates with the Space Development Agency to create resilient low earth orbit constellations for global surveillance. Its expertise in system integration ensures reliable performance in harsh space environments. By focusing on innovation and operational excellence Lockheed Martin supports critical national infrastructure and defense needs.

Top Strategies Used by Key Market Participants

Key players in the United States earth observation market primarily employ strategies focused on technological innovation and strategic partnerships to maintain competitive advantage. Companies invest heavily in research and development to enhance satellite sensor capabilities and data processing speeds. Mergers and acquisitions are common tactics used to expand service portfolios and acquire specialized analytical tools. Firms prioritize the integration of artificial intelligence to automate image analysis and deliver actionable insights rapidly. Collaborations with government agencies ensure alignment with national security priorities and secure long term contracts. Providers also focus on launching small satellite constellations to improve revisit rates and reduce latency. Emphasis on cloud-based platforms facilitates easier data access and scalability for commercial clients. Additionally, companies adopt sustainable practices in satellite manufacturing and disposal to address environmental concerns.

MARKET SEGMENTATION

This research report on the U.S. earth observation market is segmented and sub-segmented into the following categories.

By Orbit

- LEO (Low Earth Orbit)

- MEO (Medium Earth Orbit)

- GEO (Geostationary Earth Orbit)

- Others

By Solution

- Imagery Data

- Imagery Data Analytical Service

- Others

By Imaging Resolution

- Very High Resolution

- High Resolution

- Medium Resolution

- Low Resolution

By Application

- Urban Development

- Mapping & Surveying

- Agriculture

- Environmental Monitoring

- Natural Resource Exploration

- Security & Intelligence

- Disaster & Emergency Management

- Others

By Technology

- Optical Imaging

- Radar Imaging

- Spectral Imaging

- Thermal Imaging

- LiDAR

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1.What challenges affect the U.S. Earth Observation Market?

High deployment costs, data processing complexity, cybersecurity concerns, and regulatory requirements remain key market challenges.

2.What factors are driving the growth of the U.S. Earth Observation Market?

Growth is driven by rising demand for environmental monitoring, disaster management, precision agriculture, defense surveillance, and urban planning applications.

3.What is Earth Observation technology?

Earth Observation technology involves collecting information about the Earth using satellites, aircraft, and remote sensing systems to monitor environmental and human activities.

4.Which industries commonly use Earth Observation data?

Industries such as agriculture, defense, energy, mining, environmental management, transportation, and infrastructure planning extensively use Earth Observation data.

5.What role do satellites play in the Earth Observation Market?

Satellites capture imagery and geospatial information that supports weather forecasting, land mapping, climate monitoring, and disaster response activities.

6.Which imaging technologies are widely used in Earth Observation?

Optical imaging, radar imaging, thermal imaging, spectral imaging, and LiDAR technologies are commonly used across Earth Observation applications.

7.How does Earth Observation support agriculture in the United States?

Earth Observation helps farmers monitor crop health, soil conditions, irrigation patterns, and agricultural productivity.

8.Why is Earth Observation important for disaster management?

Earth Observation improves emergency preparedness by providing real time information for floods, wildfires, hurricanes, and other natural disasters.

9.How is artificial intelligence influencing the U.S. Earth Observation Market?

Artificial intelligence enhances image analytics, automated object detection, predictive modeling, and faster processing of large geospatial datasets.

10.What is the future outlook for the U.S. Earth Observation Market?

The market is expected to expand steadily due to technological advancements, increasing commercial satellite launches, and growing demand for location based intelligence solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com