U.S. Fast Food Market Size, Share, Trends & Growth Forecast Report By Type, By Distribution Platform, By End User, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Fast Food Market Size

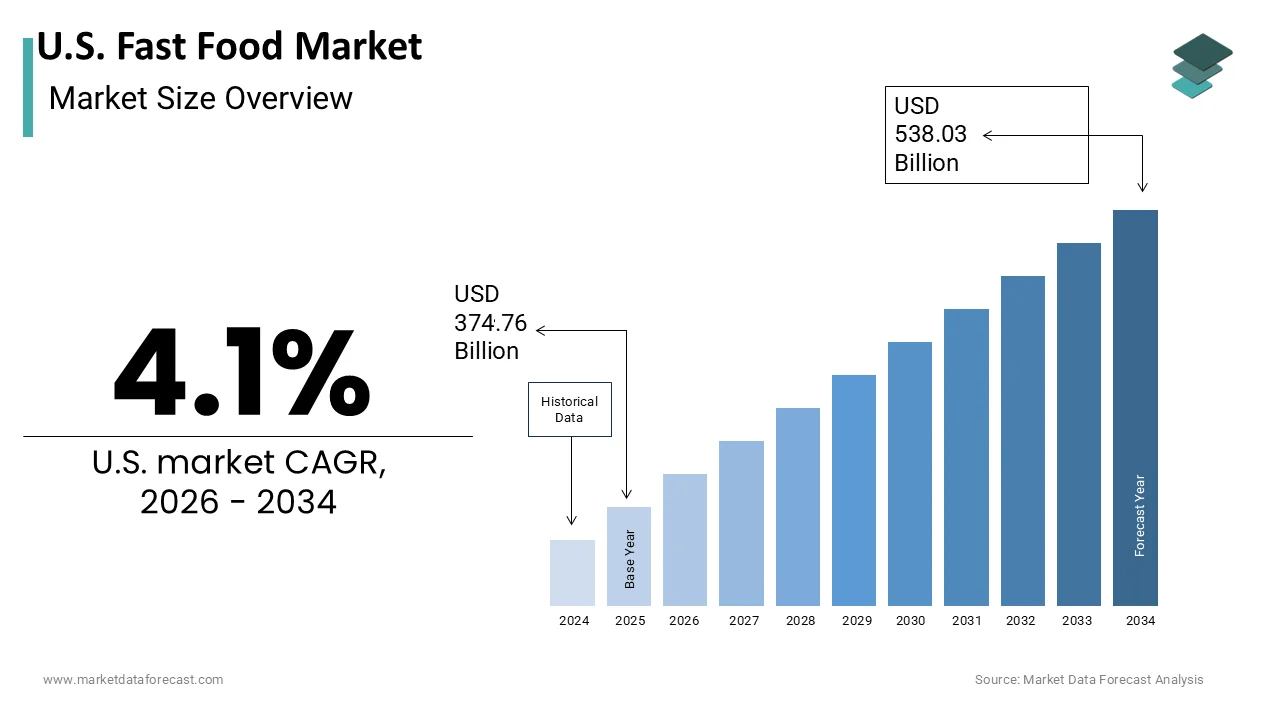

The U.S. Fast Food Market was valued at USD 374.76 billion in 2025, is estimated to reach USD 390.13 billion in 2026, and is projected to reach USD 538.03 billion by 2034, growing at a CAGR of 4.1% from 2026 to 2034.

Fast food refers to mass-produced, highly processed food designed for rapid preparation, commercial resale, and immediate consumption, often sold through restaurants or drive-throughs. This market serves as a critical component of the broader food service industry, catering to consumers seeking immediate meal solutions amidst busy lifestyles. The operational model relies heavily on efficient supply chains, an automated cooking process, es and extensive franchise networks that ensure consistent product delivery across diverse geographic regions. As per the National Restaurant Association, ion the limited service restaurant segment accounts for a significant portion of total commercial foodservice sales, reflecting its entrenched position in American dining habits. Consumer behavior indicates a strong preference for value-driven meals, with approximately 45 to 50 percent of U.S. adults visiting quick-service establishments at least once a week, according to consumer survey data. The proliferation of digital ordering platforms has further integrated these services into daily routines, allowing for seamless transactions and reduced wait times. Demographic trends show that younger generations, particularly millennials and Generation Z, constitute a large share of the customer base,se driving demand for innovative menu items and sustainable practices. The market structure is highly competitive, with major chains dominating through brand recognition and economies of scale, while independent operators' niche segments contribute to overall diversity. Regulatory frameworks regarding labor minimum wage and food safety standards significantly influence operational costs and strategic planning within this dynamic ecosystem.

MARKET DRIVERS

Rising Consumer Preference for Convenience and Speed Drives Market Expansion

The accelerating pace of modern life has cemented convenience as a primary determinant in food selection decisions among American consumers, which is among the main reasons behind the growth of the United States fast food market. Individuals increasingly prioritize time-saving solutions due to demanding work schedules and urban commuting patterns, which limit opportunities for home cooking. According to the Bureau of Labor Statistics,, cs the average American spends approximately 8.5 hours per day working or on work-related activities, leaving minimal time for meal preparation. This temporal constraint fuels consistent demand for ready-to-eat options that require little to no waiting period. Quick service restaurants have capitalized on this trend by optimizing drive-thru services and mobile order-ahead capabilities, which reduce transaction times to under three minutes in many leading chains. Data from QSR Magazine indicates that drive-thru sales account for nearly 70 percent of total revenue for major burger chains, demonstrating the critical role of accessibility. Furthermore,e the integration of third-party delivery apps has expanded the reach of these establishments, allowing customers to receive meals without leaving their homes or offices. The convenience factor extends beyond speed to include ease of payment and personalized ordering experiences enabled by artificial intelligence. As urbanization continues to rise,e with over 83 percent of the US population living in urban areas, as per the United States Census Bureau, the density of fast food outlets increases to meet localized demand. This structural shift ensures that convenience remains a robust driver sustaining high frequency visits and customer loyalty in a competitive environment.

Increasing Adoption of Digital Technology and Automation Enhances Operational Efficiency

The rapid integration of digital technologies and automation systems has revolutionized the operational framework of the United States fast food market. This enables greater efficiency and enhanced customer engagement. Restaurants are increasingly deploying self-service kiosks, mobile applications, and artificial intelligence-driven chatbots to streamline ordering processes and reduce labor dependency. According to a study, the adoption of automation and digital tools can streamline up to 25 percent of transactional sales functions and up to 35 percent of back-office consumer workflows, significantly driving operational efficiency. Major chains have reported that digital orders now constitute over 40 percent of total transactions, highlighting the shift toward tech-enabled interactions. These platforms facilitate personalized marketing through data analytics, allowing brands to offer targeted promotions based on individual purchasing histories, which increases average check sizes. Additionally, automation in kitchen operations, such as robotic fryers and burger flippers, helps maintain consistency and quality while addressing labor shortages. The National Restaurant Association states that approximately 60 percent of operators are actively investing in technology to enhance customer experiences, with a clear majority viewing digital integration as an essential asset to handle rising labor and food costs. Investment in cloud-based point of sale systems further enables real-time inventory management and predictive analytics for demand forecasting. This technological evolution not only reduces operational costs but also improves the overall customer experience by providing faster and more accurate service. Consumers are becoming increasingly digitally native, creating a high demand for seamless, integrated shopping experiences. Consequently, businesses are investing heavily in innovation to meet these expectations.

MARKET RESTRAINTS

Growing Health Consciousness and Demand for Nutritious Alternatives Restrain Growth

American consumers are increasingly aware of health and wellness, which creates a significant restraint for the traditional fast food segment within the United States fast food market. That segment is, in turn, challenged by its long-term association with processed, high-calorie foods. Public health initiatives and educational campaigns have highlighted the risks of obesity, diabetes, and cardiovascular diseases linked to excessive consumption of fast food. According to the Centers for Disease Control and Prevention, the prevalence of obesity in the United States was 41.9 percent in recent years, prompting many individuals to seek healthier dietary options. This shift in consumer sentiment has led to a decline in frequent visits to conventional quick service restaurants among health-conscious demographics, particularly millennials and Generation Z, who prioritize transparency in ingredient sourcing and nutritional content. Many consumers are actively reducing their intake of sodium, saturated fats, and added sugars, which are staples in standard fast food menus. Data from the International Food Information Council reveals that 52 percent of Americans are trying to limit or avoid sugars in their diet, influencing their restaurant choices. Consequently, traditional chains face pressure to reformulate recipes and introduce lighter alternatives, which often involve higher production costs and complex supply chain adjustments. The rise of fast casual dining concepts that emphasize fresh and organic ingredients further erodes the market share of traditional fast food providers. This evolving consumer preference necessitates substantial investment in research and development to align with health trends while maintaining affordability and taste profiles that define the sector.

Stringent Regulatory Pressures and Labor Cost Inflation Impact Profitability

Stringent regulatory environments and rising labor costs are major limitations for the United States fast food market. This directly impacts operational margins and pricing strategies. Federal and state governments have implemented stricter labor laws, including increased minimum wage requirements and mandates for employee benefits, which elevate overhead expenses for restaurant operators. According to the Economic Policy Institute, the federal minimum wage has remained stagnant while numerous states have enacted laws raising the minimum wage to 15 dollars per hour or higher s, significantly increasing payroll liabilities. Additionally, the implementation of predictable scheduling laws in various jurisdictions restricts managerial flexibility in staffing, ng leading to inefficiencies and increased labor costs. Regulatory scrutiny regarding food safety labeling and environmental sustainability also imposes compliance burdens that require capital investment and administrative resources. The Occupational Safety and Health Administration enforces rigorous standards for workplace safety, which necessitate ongoing training and equipment upgrades. Furthermore, potential legislation targeting single-use plastics and packaging waste adds another layer of complexity and cost to operations. As per the National Restaurant Association, labor costs typically account for 30 to 35 percent of total expenses, making wage inflation a critical financial challenge. These regulatory and economic pressures force operators to raise menu prices, which may deter price-sensitive customers and reduce transaction volumes. The cumulative effect of these factors constrains profitability and limits the ability of chains to expand aggressively or invest in innovation without compromising financial stability.

MARKET OPPORTUNITIES

Expansion into Plant-Based and Alternative Protein Menus Offers Growth Potential

The burgeoning demand for plant-based and alternative protein products offers a lucrative opportunity for the U.S. fast food market. It is an ideal way to attract health-conscious and environmentally aware consumers. Societal attitudes toward sustainability and animal welfare are evolving. In response, major quick-service restaurants are integrating vegan and vegetarian options into their core menus to capture this growing demographic. According to historical retail data from the Plant Based Foods Association, sales of plant-based foods surged by 27 percent in 2020, outpacing total food market growth during pandemic lockdowns, establishing a baseline consumer footprint that has since entered a market stabilization phase. Leading chains have launched proprietary plant-based burgers, chicken nuggets, and breakfast items, leveraging partnerships with specialized food technology companies to ensure taste and texture parity with traditional meat products. This strategic diversification allows brands to appeal to flexitarians who seek to reduce meat consumption without eliminating it from their diets. The introduction of these items also enhances brand image by demonstrating commitment to environmental stewardship and ethical sourcing, which resonates with younger consumers. By offering inclusive menu options, fast food operators can increase foot traffic and average order values while differentiating themselves in a saturated market. Furthermore, the scalability of plant-based ingredients often provides supply chain stability compared to volatile animal protein markets. This transition not only opens new revenue streams but also future-proofs businesses against shifting dietary norms and regulatory trends favoring sustainable food systems.

Integration of Artificial Intelligence for Personalized Customer Engagement

The strategic integration of artificial intelligence and machine learning technologies unlocks potential for the United States fast food market. This allows for enhanced customer engagement and optimizes marketing effectiveness. By leveraging vast amounts of consumer data generated through mobile apps and loyalty programs, restaurants can deliver highly personalized recommendations and promotions that drive repeat visits and increased spending. According to a report by Accenture,91 percent of consumers are more likely to shop with brands that provide relevant offers and recommendations, highlighting the value of personalization. AI algorithms analyze purchasing patterns, dietary preferences, and location data to create dynamic menus and targeted advertising campaigns that resonate with individual users. This level of customization improves the customer experience by reducing decision fatigue and ensuring that offers are timely and relevant. Additionally, AI-powered chatbots and virtual assistants facilitate seamless customer service interactions, resolving queries and processing orders efficiently without human intervention. The use of predictive analytics enables operators to anticipate demand fluctuations and optimize inventory levels, reducing waste and improving operational efficiency. As per Deloitte, companies that utilize advanced analytics for customer insights achieve significantly higher retention rates and customer lifetime value. By adopting these technologies, fast food chains can build deeper emotional connections with customers, fostering loyalty in an increasingly competitive landscape. This digital transformation also provides actionable insights for product development,t allowing brands to innovate based on real-time feedback and emerging trends.

MARKET CHALLENGES

Persistent Labor Shortages and Workforce Retention Issues Challenge Operations

Persistent labor shortages and high employee turnover rates are negatively impacting the growth of the United States fast food market. These factors severely disrupt operational continuity and service quality. The sector historically relies on entry-level workers, yet changing demographic trends and competing employment opportunities have made recruitment increasingly difficult. According to the Bureau of Labor Statistics, cs the leisure and hospitality sector experienced one of the highest quit rates among all industries,s reflecting widespread dissatisfaction with wages, es working conditions,s and career advancement prospects. This instability forces restaurants to operate with reduced staff, leading to longer wait times, decreased accuracy,y and diminished customer satisfaction. High turnover also incurs significant costs related to recruiting,g hiring, and training new employees, which strains financial resources and managerial bandwidth. The lack of experienced staff impacts the consistency of food preparation and adherence to safety protocol,s posing risks to brand reputation. Furthermore, re the reliance on transient labor limits the ability of chains to implement long-term training programs and foster a cohesive corporate culture. As per the National Restaurant Association, the average annual turnover rate in the limited service restaurant sector exceeds 70 percent, creating a perpetual cycle of staffing challenges. Addressing this issue requires substantial investments in employee benefits, career development pathways,s and workplace improvements, which may not yield immediate returns. The inability to secure a stable workforce hinders expansion plans and operational efficiency, making labor retention a critical challenge for sustained growth and competitiveness in the market.

Volatility in Raw Material Prices and Supply Chain Disruptions

Fluctuating costs of raw materials and ongoing supply chain vulnerabilities are a formidable challenge to the United States fast food market. This affects profit margins and pricing stability. The industry depends on a complex global network of suppliers for ingredients such as be, ef poul, potatoesota, to,, es and cooking oi, ls which are subject to price volatility due to weather conditions, geopolitical tensions, and logistical bottlenecks. According to the Producer Price Index published by the Bureau of Labor Statistics, food commodity prices have experienced significant swings in recent years, driven by inflationary pressures and supply constraints. These fluctuations make it difficult for operators to predict costs and maintain consistent menu pricing without alienating price-sensitive customers. Supply chain disruptions caused by transportation delays, labor strikes,s or natural disasters can lead to temporary shortages of key items,s forcing restaurants to alter menus or face stockouts. Such inconsistencies damage customer trust and brand reliability, which are essential for maintaining market share. Additionally, the concentration of suppliers in certain regions increases susceptibility to localized shock, requiring diversification strategies that are costly and time-consuming to implement. As per the Food Marketing Institute, supply chain resilience has become a top priority for retailers and restaurants, yet achieving it requires substantial capital investment in technology and infrastructure. The inability to fully mitigate these risks exposes operators to margin compression and financial instability. Consequently, ly managing supply chain complexity and cost volatility remains a persistent challenge that demands agile strategic responses and robust risk management frameworks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Distribution Platform, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | McDonald’s Corporation, Yum! Brands, Inc., Restaurant Brands International Inc., Wendy’s Company, Domino’s Pizza, Inc., Chipotle Mexican Grill, Inc., Subway IP LLC, Papa John’s International, Inc., The Coca-Cola Company, Starbucks Corporation, Dunkin’ Brands Group, Inc., Jack in the Box Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The burger and sandwich segment dominated the United States fast food market and accounted for a 42.5% share in 2025. This dominance of the segment was driven by its deep cultural entrenchment and widespread consumer acceptance. Also, this category benefits from decades of brand building by major chains that have standardized the quick service experience around these core items. The ubiquity of beef and poultry production in the United States ensures a stable, cost-effective supply chain, which allows operators to maintain competitive pricing while preserving margins. The versatility of the sandwich format enables continuous innovation through limited-time offers and premium ingredients, which keeps the menu fresh and engaging for repeat customers. Major players like McDonald's and Burger King invest heavily in marketing campaigns that reinforce the emotional connection between consumers and their flagship burger products. The ease of customization further enhances appeal, allowing individuals to tailor meals to specific dietary preferences or taste profiles without compromising speed. Data aligned with the National Restaurant Association and industry menu tracking confirms that sandwiches remain the most frequently ordered overall item category in American food service, driven heavily by breakfast and lunch dayparts, while categories like burgers and pizza capture a larger share of dinner transactions. This consistent demand across diverse demographic groups solidifies the segment's leadership position. Additionally,y the portability of burgers and sandwiches aligns with the on-the-go lifestyle of the modern workforce perfectly,e ensuring steady traffic during peak commuting hours. The segment's ability to adapt to trending flavors while maintaining its core identity ensures its continued dominance in the competitive landscape. Furthermore, the enduring popularity of burgers and sandwiches is deeply rooted in American culinary culture, where these items are viewed as staple comfort foods. Generations of consumers have grown up associating major fast food brands with family outings, social gatherings, and convenient meal solutions, creating a powerful emotional bond that transcends mere nutrition. According to a study, approximately 70 percent of Americans report eating fast food at least once a month, with burgers remaining the most heavily considered item category during those visits. This cultural resonance is amplified by extensive advertising efforts that link burger consumption with happiness, convenience,e and national identity. The standardization of taste profiles across thousands of locations ensures that customers receive a predictable and satisfactory experience regardless of location, which reinforces trust and loyalty. Major chains leverage this loyalty by introducing nostalgic menu items or retro packaging that appeals to consumer sentimentality. The simplicity of the burger format also facilitates rapid service, which is critical for meeting the expectations of time-constrained customers. Furthermore, the widespread availability of beef and bread ingredients ensures that prices remain accessible to a broad socioeconomic spectrum. This combination of cultural significance, brand trust, and operational efficiency creates a formidable barrier to entry for competitors and sustains the segment's leading position in the market. The dominance of the burger and sandwich segment is significantly bolstered by the robust and efficient supply chain infrastructure for key ingredients such as beef, poultry,y and wheat. The United States is one of the world's largest producers of beef and grain,s providing domestic quick service restaurants with a reliable and cost-effective source of raw materials. According to the United States Department of Agriculture, the domestic beef production reached approximately 27 billion pounds in recent years, rs ensuring ample supply for the food service industry. This local sourcing reduces dependency on imports and mitigates risks associated with global logistical disruptions or currency fluctuations. The economies of scale achieved by major chains allow them to negotiate favorable contracts with suppliers, further lowering input costs and enhancing profitability. Data from the Bureau of Labor Statistics indicates that both food at home and food away from home prices have experienced steady upward inflation, while separate corporate financial reports reveal that major burger chains have utilized menu engineering and automated store efficiencies to buffer these margins. The standardized nature of burger preparation also minimizes waste and simplifies inventory management, contributing to overall cost efficiency. Additionally, the vertical integration strategies employed by some leading chains provide greater control over quality and pricing stability. This supply chain resilience enables operators to maintain consistent menu pricing, which is crucial for retaining price-sensitive customers in an inflationary environment. The ability to deliver high-volume products at competitive prices without compromising quality ensures that the burger segment remains the most accessible and frequently consumed option in the fast food market.

The Asian and Latin American food segment is anticipated to witness the fastest CAGR of 6.8% between 2026 and 2034 due to increasing demographic diversity and evolving consumer palates. In addition, the rising population of Hispanic and Asian Americans has created a substantial base of consumers seeking authentic flavors from their heritage cultures. According to the United States Census Bureau, the Hispanic population grew by 23 percent in the last decade,e becoming a significant demographic force influencing non-Hispanic consumers. Simultaneously, non-Hispanic consumers are increasingly exploring international cuisines, driven by travel exposure, social media influence, and a desire for culinary adventure. Quick service restaurants are responding by introducing tacos, burritos, ramen, and stir-fry dishes that offer bold flavors and perceived freshness. The versatility of these cuisines allows for healthy, interpretative, vegetable-rich bowls and,, vegetable rich shealth-consciousappeal to health-conscious diners. Also, the innovation potential in this segment is vast as operators experiment with fusion concepts and regional specialties that differentiate them from standardized burger offerings. Furthermore, the use of fresh herbs, spices, nd vegetables in Asian and Latin American dishes aligns with the growing demand for transparent and wholesome ingredients. This combination of demographic shifts, consumer curiosity, and menu innovation positions this segment as the primary engine of future growth in the US fast food landscape. The rapid expansion of the Asian and Latin American food segment is primarily fueled by significant demographic changes in the United States that have diversified the national palate. The increasing proportion of Hispanic and Asian populations has introduced a strong demand for authentic culinary experiences that reflect their cultural heritage. According to research, Hispanics are projected to comprise nearly 25 percent of the US population by 2060, creating a sustained and growing market for Latin American cuisine. This demographic trend is complemented by the rising influence of Asian cultures through media, technology,gy and immigration, which has popularized dishes such as sushi ph, pho, and Korean barbecue. Younger generations, particularly millennials and Generation Z, are more likely to experiment with diverse flavors and view food as a means of cultural exploration. Data from the National Restaurant Association reveals that 60 percent of consumers are more likely to visit restaurants that offer ethnic or international foods, indicating a broad appeal beyond specific demographic groups. The presence of vibrant immigrant communities in major urban centers has also fostered the development of authentic eateries that attract a wider audience. These communities serve as incubators for culinary trends that eventually permeate the mainstream fast food sector. As these demographics gain economic power,r their purchasing preferences significantly shape market dynamics. The integration of traditional ingredients and cooking methods into quick service formats allows operators to cater to this diverse customer demographic. hi.. This demographic-driven demand ensures that the Asian and Latin American segment continues to expand at a robust pace,e capturing market share from traditional categories. The Asian and Latin American food segment is benefiting from a wave of culinary innovation that emphasizes fusion concepts and healthier ingredient profiles, which resonate with modern consumer preferences. Operators are increasingly blending traditional flavors with contemporary dining trends to create unique and appealing menu items that stand out in a crowded market. For instance,ce the integration of Asian inspired sauces into grain bowls or the use of plant-based, rich spices and plant-based proteins offers novel taste experiences that attract adventurous diners. According to sources, menus featuring Asian and Latin American flavors have seen a double-digit increase in penetration across quick service restaurants in recent years. Consumers perceive these cuisines as healthier alternatives to traditional fast food due to their frequent use of fresh vegetables, lean proteins, ns and complex carbohydrates. The emphasis on fresh ingredients aligns with the growing demand for transparency and clean labeling in food products. Data from the International Food Information Council shows that 70 percent of consumers are trying to eat more plant-based foods, which Asian and Latin American menus often accommodate with vegetable-based rice and vegetable-based dishes. Additionally, the visual appeal of these dishes makes them highly shareable on social media platforms, driving organic marketing and brand awareness. The flexibility of these cuisines allows for easy adaptation to dietary restrictions such as gluten-free or vegan options, further expanding their customer base. This continuous innovation and positive health perception drive frequent visits and higher spending, ng making this segment the fastest growing component of the US fast food market.

By Distribution Platform Insights

The Quick Service Restaurants (QSR) segment led the United States fast food market and captured a 58.2% share in 2025. This leading position of the segment was attributed to the extensive physical footprint of established chains and the inherent convenience of immediate service. QSRs offer a standardized and reliable dining experience that consumers trust for quick meals during busy schedules. According to data from the National Restaurant Association, the limited-service restaurant segment generates over $450 billion in annual sales, cementing its massive footprint within a broader $1.5 trillion domestic food service economy. The strategic location of QSR outlets in high-traffic areas such as highways, shopping centers, and urban districts ensures maximum drive-thru and accessibility. Drive-thru facilities, which are a hallmark of the QSR mode, provide an additional layer of convenience that appeals to car-dependent consumers. Data from QSdrive-thru indicates that drive-thru lanes contribute to nearly 70 percent of sales for top burger chains, highlighting the importance of this service channel. The ability to serve large volumes of customers efficiently through automated systems and streamlined workflows allows QSRs to maintain low prices and high throughput. Furthermore,e the integration of digital kiosks and mobile ordering within physical stores has enhanced the customer experience by reducing wait times and improving order accuracy. The strong brand recognition of major QSR chains fosters customer loyalty and repeat business. Despite the rise of delivery services, es the physical QSR location remains the primary hub for order fulfillment and brand interaction. This entrenched infrastructure and operational efficiency ensure that QSRs continue to lead the market in terms of revenue and market share. The leadership of the Quick Service Restaurant segment is underpinned by its vast and strategically located physical infrastructure, which ensures unparalleled accessibility for consumers. Major chains have invested decades in real estate acquisition and development, resulting in thousands of outlets across the country,y ranging from rural towns to dense urban centers. According to IBISWorld, there are over 200000 fast food restaurants in the United States, es with QSRs comprising the largest portion of this total. This widespread presence allows consumers to find familiar brands conveniently wherever they are,e reducing the friction associated with meal decisions. The proximity of QSRs to workplaces, schools, malls, and residential areas makes them the default choice for quick lunches and dinners. The design of these establishments prioritizes speed and efficiency with dedicated drive-thru lanes, pickup counters, and seating areas optimized for rapid turnover. Data from the Bureau of Transportation Statistics shows that the majority o,,f Americans commute by car, making drive-thru services particularly valuable for capturing this traffic. The consistency of the physical environment across locations builds trust and reduces perceived risk for customers who know exactly what to expect in terms of service and quality. Additionally, the physical store serves as a critical touchpoint for brand marketing and customer engagement through signage, promotions, and in-store experiences. The sheer scale of this network creates significant barriers to entry for competitors who lack the capital to replicate such extensive coverage. This physical dominance ensures that QSRs remain the primary channel for fast food consumption in the United States. The competitive advantage of the Quick Service Restaurant segment is largely derived from its highly refined operational efficiency and standardized service models, which enable consistent quality and speed. QSRs have perfected the art of mass production in a fooservice context,t utilizing assembly line techniques and specialized equipment to minimize preparation time. Operational case studies highlighted across the Harvard Business Review show that menu and workflow standardization can reduce service fulfillment time by up to 30 percent compared to non-standardized food service models. This efficiency enables QSRs to handle peak-hour rushes effectively without compromising order accuracy or customer satisfaction. The use of proprietary technology, such as automated fryers, digital timers, and inventory management systems, further streamlines operations and reduces labor requirements. Training programs for employees are designed to ensure uniform execution of tasks, which maintains brand consistency across all locations. The ability to serve customers quickly is a key determinant of success in the fast food industry, where time is a critical value proposition. Standardized menus and supply chains also facilitate economies of scale, which lower costs and allow for competitive pricing. This operational excellence enables QSRs to maintain high profit margins while offering affordable meals. The reliability of the service model builds customer confidence and encourages repeat visits. As consumer expectations for speed and consistency continue to rise,e the operational strengths of QSRs ensure their continued dominance in the distribution landscape.

On the other hand, the online food delivery services segment is likely to experience the fastest CAGR of 12.5% during the forecast period, owing to the increasing adoption of digital platforms and the changing preferences of consumers who prioritize convenience and variety. Moreover, the proliferation of smartphones and high-speed internet has made online ordering seamless and accessible to a broad demographic. Third-party delivery apps such as DoorDash, Uber Eats, ts and Grubhub have expanded the reach of fast food restaurants beyond their physical locations, allowing them to serve customers who prefer dining at home or work. The convenience of browsing multiple menus, comparing prices, and tracking orders in real time enhances the user experience and encourages frequent usage. Also, the COVID-19 pandemic accelerated this trend by normalizing contactless delivery and expanding the customer base to include older demographics. Restaurants are increasingly investing in their own digital ordering platform, reducing reliance on third-party commissions and capturing valuable customer data. The ability to offer exclusive deals and personalized recommendations through apps drives customer retention and increases average order values. This digital transformation of food distribution is reshaping the competitive landscape and positioning online delivery as the primary growth engine for the industry. The exponential growth of the Online Food Delivery Services segment is fundamentally supported by the widespread penetration of digital technologies and high smartphone adoption rates among American consumers. The ubiquity of mobile devices has transformed how individuals interact with food services, es making it possible to order meals with just a few taps. According to the Pew Research Center, 5 percent of Americans own a smartphone, riding a vast installed base for delivery applications. This high level of connectivity ensures that online ordering is accessible to a diverse range of users across different age groups and income levels. The user-friendly interfaces of delivery apps simplify the ordering process by storing payment information,, saing favorite orderordersd providing real-time updates on delivery status. The integration of GPS technology allows for precise tracking of delivery drivers, which enhances transparency and reduces anxiety about wait times. Furthermore, the availability of high-speed internet connections in both urban and suburban areas ensures that apps function smoothly without latency issues. The seamless integration of digital wallets and contactless payment options further reduces friction in the transaction process. As digital literacy continues to improve across the population, the barrier to entry for using online delivery services diminishes. This technological foundation enables the sector to scale rapidly and reach new customer segments. The convenience offered by digital platforms aligns perfectly with the on-demand economy, driving sustained growth in this distribution channel. Besides these, the rapid expansion of the Online Food Delivery Services segment is significantly driven by the aggressive growth of third-party logistics networks and strategic partnerships with restaurant chains. Delivery platforms have invested heavily in building extensive fleets of independent contractors and optimizing algorithms for efficient route planning, ing which reduces delivery times and costs. According to DoorDash's annual reports, the company operates in over 7000 cities and towns in the United States, demonstrating the vast reach of its logistics network. These platforms have formed exclusive annon-exclusiveve partnerships with major fast food chains, ensuring that popular brands are available to a wide audience of app users. Such colco-brandeds often inclco-brandednded marketing campaigns and exclusive menu items that drive user engagement and order volume. The ability of these platforms to aggregate demand from multiple restaurants allows for economies of scale in delivery operations, which improves profitability. Additionally,y the data collected from these transactions provides valuable insights into consumer preferences, es which helps restaurants optimize their menus and pricing strategies. The continuous improvement in delivery infrastructure,ure including the introduction of electric vehicles and autonomous delivery pilots, further enhances efficiency. This robust logistical framework enables online delivery services to offer reliable and fast service, which is critical for customer satisfaction. The synergy between technology platforms and restaurant operators creates a virtuous cycle of growth that sustains the momentum of this segment.

COUNTRY LEVEL ANALYSIS

United States Fast Food Market Analysis

The United States remained the largest by occupying a 82.4% share of the North American regional market. This prominence of the country’s market was supported by a unique combination of cultural factors, economic conditions, and infrastructural advantages that have cemented quick-service dining as a central pillar of American life. The country's vast geographic size and car-centric urban planning have facilitated the proliferation of drive-thru establishments, which are integral to the fast food model. According to data aligned with the National Restaurant Association and the U.S. Census Bureau, the United States is home to over 300,000 limited-service restaurants (including over 200,000 fast-food locations), generating hundreds of billions of dollars in annual revenue. The high disposable income levels of American consumers allow for frequent dining out despite economic fluctuations. Data from the Bureau of Economic Analysis indicates that personal consumption expenditures on food services remain robust, reflecting the resilience of the sector. The presence of headquarters for major global fast food chains such as McDonald's, Yum Brands, and Restaurant Brands International provides a competitive advantage in terms of innovation, marketing,, ng and supply chain management. These companies continuously invest in research and development to introduce new products and technologies that keep the market dynamic. The diverse population of the United States also drives demand for a wide variety of cuisines, encouraging operators to expand their menus beyond traditional offerings. Furthermore, the strong franchise model prevalent in the US enables rapid expansion and local adaptation, which sustains growth in both urban and rural areas. The regulatory environment, while challenging, also provides a structured framework for operations, ensuring consistency and safety standards. This combination of scale, wealth innovation, and cultural acceptance ensures that the United States remains the undisputed leader in the global fast food industry. The entrenched position of the United States in the global fast food market is largely attributable to the deep integration of quick service dining into the national lifestyle and cultural fabric. Fast food is not merely a convenience option but a habitual part of daily routines for millions of Americans who value speed and affordability. The Centers for Disease Control and Prevention (CDC) shows that nearly 37 percent of American adults consume fast food on any given day, illustrating the high frequency of engagement. The busy nature of American work life,e characterized by long hours and limited vacation time,ime encourages reliance on ready-to-eat meals. Data from the Organisation for Economic Co-operation and Development (OECD) shows that the average American worker logs significantly more hours annually than peers in most other developed nations, leaving less time for home cooking. This temporal pressure makes fast food an attractive solution for families and individuals alike. The cultural normalization of eating on the go is further reinforced by the prevalence of car culture, which supports the drive-thru model. The social aspect of fast food also plays a role, with many chains serving as community hubs for casual gatherings. Marketing efforts by major brands have successfully linked their products with American values such as freedom, om convenience, and enjoyment. The widespread acceptance of fast food across all socioeconomic groups ensures a broad and stable customer base. Additionally,y the influence of American media and entertainment globally reinforces the domestic demand for these brands. This cultural synergy between lifestyle patterns and food consumption habits creates a resilient demand structure that sustains the market's leadership position. The economic scale of the United States, combined with relentless corporate innovation, serves as a primary driver for its dominance in the fast food sector. The large consumer base and high spending power provide a fertile ground for testing new concepts and scaling successful models rapidly. According to the Bureau of Economic Analysis (and frequently cited by the Federal Reserve), consumer spending accounts for nearly 70 percent of U.S. economic activity, with food services representing a notable portion of this expenditure. Major fast food corporations headquartered in the US invest billions annually in technology, marketing, and supply chain optimization to maintain their competitive edge. These companies leverage advanced data analytics to understand consumer behavior and personalize marketing efforts, which increases customer retention and lifetime value. The adoption of automation and artificial intelligence in kitchen operations and customer service enhances efficiency and reduces costs. Furthermore, the strong venture capital ecosystem in the US supports the emergence of innovative food tech startups that introduce new dining concepts and delivery solutions. The ability of US companies to attract top talent in technology and management further strengthens their operational capabilities. The robust legal and financial infrastructure supports franchise expansion and international growth, which reinforces the domestic market's centrality. This combination of economic strength and corporate agility ensures that the United States remains at the forefront of global fast food trends and developments.

COMPETITIVE LANDSCAPE

The competition in the United States fast food market is intensely fierce, characterized by the presence of numerous global chains and emerging local operators vying for consumer attention. Major players compete aggressively on price, convenience,e and product innovation to capture market share in a saturated landscape. Brand loyalty plays a crucial role as established companies leverage decades of marketing investment to retain customers. The rise of fast casual dining concepts has further intensified rivalry by offering higher-quality ingredients at competitive prices. Digital capabilities have become a key differentiator, with companies investing billions in technology to streamline ordering and delivery processes. Labor shortages and rising wage pressures add another layer of complexity, ty forcing operators to balance cost management with service quality. Supply chain volatility impacts pricing strategies and menu availability,ity creating additional competitive challenges. Consumers increasingly demand transparency and sustainability, prompting brands to adapt their practices to meet ethical standards. This dynamic environment requires continuous innovation and strategic agility as companies strive to differentiate themselves and maintain profitability amidst shifting consumer preferences and economic uncertainties.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. fast food market include

- McDonald’s Corporation

- Yum! Brands, Inc.

- Restaurant Brands International Inc.

- Wendy’s Company

- Domino’s Pizza, Inc.

- Chipotle Mexican Grill, Inc.

- Subway IP LLC

- Papa John’s International, Inc.

- The Coca-Cola Company

- Starbucks Corporation

- Dunkin’ Brands Group, Inc.

- Jack in the Box Inc.

TOP LEADING PLAYERS IN THE MARKET

- McDonald's Corporation maintains its position as a dominant force in the United States fast food landscape through extensive brand recognition and operational excellence. The company leverages its vast network of franchised locations to ensure consistent service quality and widespread accessibility for consumers across diverse regions. Recent strategic initiatives focus heavily on digital transformation,n including the expansion of mobile ordering capabilities and personalized marketing through its loyalty program. McDonald's has also invested significantly in modernizing its restaurant interiors and enhancing drive-thru efficiency to meet evolving consumer expectations for speed and convenience. The introduction of limited-time offers featuring popular collaborations helps sustain customer interest and drive frequent visits. McDonald's reinforces its leadership by prioritizing technology integration and menu innovation. This strategy allows the company to adapt to changing dietary preferences and competitive pressures within the dynamic quick-service sector.

- Yum Brands Inc exerts significant influence in the US market through its portfolio of iconic brands, including KFC, Pizza Hut, and Taco Bell. The company drives growth by empowering franchisees with robust support systems and innovative marketing campaigns that resonate with diverse demographic groups. Taco Bell has been particularly successful in capturing younger consumers through creative menu items and strong social media engagement. Yum Brands focuses on enhancing digital experiences by integrating advanced ordering platforms and delivery partnerships to increase convenience. Recent efforts include remodeling stores to create modern dining environments and expanding late-night service options to capture additional revenue streams. The company emphasizes operational efficiency and supply chain resilience to maintain profitability amidst economic fluctuations. Yum Brands leverages the distinct strengths of its individual brands to address varied consumer preferences. Consequently, they sustain a strong competitive edge within the fast-food industry.

- Restaurant Brands International strengthens its presence in the United States through its flagship brands Burger King, Popeyes, es and Tim Hortons. The company focuses on revitalizing core menus and introducing bold flavors that differentiate its offerings from competitors. Burger King has undertaken significant restaurant remodeling projects to improve customer experience and operational efficiency. Popeyes continues to expand its footprint by capitalizing on the growing demand for chicken-based meals and leveraging viral marketing successes. Restaurant Brands International prioritizes digital innovation by enhancing mobile apps and implementing artificial intelligence-driven tools for personalized customer interactions. The company also emphasizes sustainability initiatives and responsible sourcing to align with consumer values. Restaurant Brands International (RBI) effectively navigates market challenges and captures expansion opportunities in the competitive US fast-food sector. This is achieved by fostering strong franchisee relationships and investing in brand-specific growth strategies.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States fast food market primarily employ digital transformation strategies to enhance customer engagement and operational efficiency. Companies invest heavily in mobile applications and loyalty programs to collect data and personalize marketing efforts. Automation technologies such as self-service kiosks and AI-driven kitchen equipment are widely adopted to reduce labor costs and improve service speed. Menu innovation remains a critical strategy with frequent introduction of limited-time offers and plant-based options to attract health-conscious consumers. Expansion of delivery channels through third-party partnerships and proprietary platforms ensures broader market reach. Franchise model optimization allows for rapid scaling while minimizing capital expenditure. Strategic real estate selection focuses on high traffic areas and drive-thru accessibility. Sustainability initiatives, including eco-friendly packaging and responsible sourcing, are increasingly used to build brand reputation. These combined approaches enable companies to maintain competitiveness and adapt to evolving consumer preferences in a dynamic market environment.

MARKET SEGMENTATION

This research report on the U.S. fast food market is segmented and sub-segmented into the following categories.

By Type

- Burger and Sandwich

- Pizza and Pasta

- Chicken

- Seafood

- Asian and Latin American Food

- Others

By Distribution Platform

- Quick Service Restaurants (QSR)

- Online Food Delivery Services

- Cafeterias

- Food Trucks

- Others

By End User

- Adults

- Teenagers

- Children

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com