U.S. Feminine Hygiene Products Market Size, Share, Trends & Growth Forecast Report By Product Type, By Distribution Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Feminine Hygiene Products Market Size

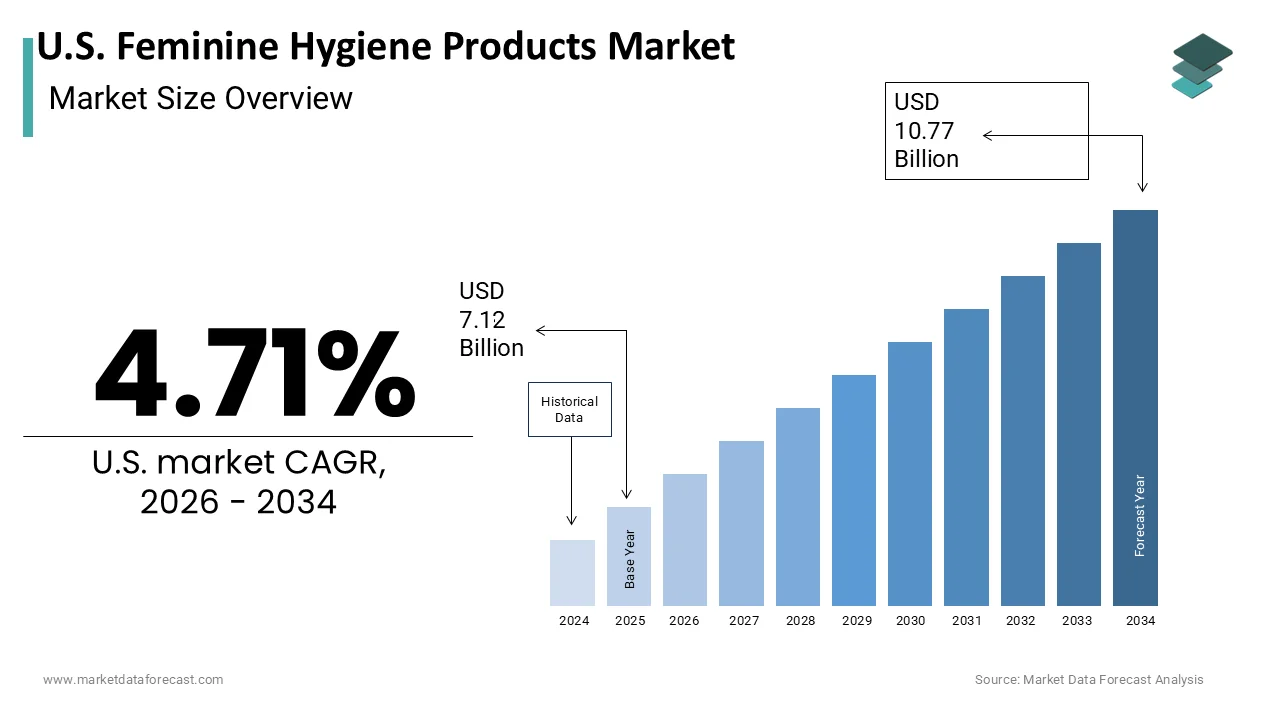

The U.S. Feminine Hygiene Products Market was valued at USD 7.12 billion in 2025, is estimated to reach USD 7.46 billion in 2026, and is projected to reach USD 10.77 billion by 2034, growing at a CAGR of 4.71% from 2026 to 2034.

Feminine hygiene products are a diverse array of personal care items designed for menstrual management and intimate health, including sanitary pads, tampons, menstrual cups, and intimate washes. This market is fundamentally driven by biological necessity, yet increasingly influenced by evolving social attitudes, sustainability concerns, and technological innovation. The market serves a vast demographic base comprising millions of menstruating individuals across various age groups. According to the United States Census Bureau, there are approximately 75 million women and girls of menstruating age in the country, ensuring a consistent and substantial consumer pool. Public health initiatives have brought urgent attention to period poverty, with data from the Alliance for Period Supplies revealing that one in four menstruators struggles to purchase necessary products due to financial constraints. This has spurred legislative actions in multiple states to provide free products in schools and public facilities. Furthermore, according to the American College of Obstetricians and Gynecologists (ACOG), the average woman menstruates over a reproductive lifespan of roughly 38 to 40 years, underscoring the decades-long consistency of product consumption. The shift towards organic and chemical-free options is gaining momentum as consumers become more aware of potential health risks associated with synthetic materials. These factors collectively define a market that is transitioning from basic utility to a realm of health consciousness and ethical consumption.

MARKET DRIVERS

Rising Health Awareness and Preference for Organic Materials

The increasing awareness regarding reproductive health and the potential risks associated with conventional feminine hygiene products is a major factor behind the growth of the United States feminine hygiene products market. Consumers are becoming more educated about the ingredients used in traditional pads and tampons, such as chlorine bleach, fragrances, and synthetic fibers. Dermatological and reproductive health studies tracked by the National Institute of Environmental Health Sciences (NIEHS) reveal that chronic exposure to specific chemical compounds in personal care items, such as phthalates anparabense ,,ns can act as endocrine disruptors and trigger active contact allergens. This knowledge has prompted a significant shift towards organic cotton-based products, which are perceived as safer and more breathable. The Organic Trade Association (OTA) highlights strong momentum across organic non-food categories, matching independent market analysis that shows organic and natural period care solutions expanding steadily to meet clean-ingredient consumer demands. Major brands are responding by obtaining certifications from organizations like the Global Organic Textile Standard to validate their claims.

Additionally, medical professionals are increasingly recommending organic options for patients with sensitive skin or conditions such as endometriosis. The American Academy of Dermatology emphasizes that using unbleached, fragrance-free, and hypoallergenic materials on sensitive areas dramatically reduces the clinical risk of contact dermatitis and localized vulvar irritations. This medical endorsement further reinforces consumer confidence in organic products. As a result, manufacturers are investing heavily in research and development to create high-performance organic alternatives that match the absorbency and convenience of traditional products. This trend is not limited to niche markets but is becoming mainstream as major retailers expand their organic offerings.

Destigmatization of Menstruation and Open Dialogue

The progressive destigmatization of menstruation in American society is fostering an environment where open dialogue and education drive the United States feminine hygiene products market expansion. Historically taboo topics surrounding periods are now being discussed openly in media, schools, and workplaces, which encourages women to seek better quality products and solutions. Advocacy research published by Plan International USA confirms that structural period stigma harms young women's educational access, fueling grassroots policy pushes and shifting consumer demand toward inclusive, body-positive intimate care brands. Social media platforms play a crucial role in this transformation, with influencers and health advocates sharing information about different menstrual health options. This cultural shift has also led to the introduction of innovative products such as menstrual discs and period underwear,r which cater to varied lifestyle needs. Educational programs in schools are increasingly including comprehensive menstrual health curriculum, which helps young users make informed choices early on. The Department of Education supports these initiatives by providing grants for health education resources. As conversations around menstruation become normalized, consumers feel more empowered to experiment with new products and prioritize their comfort and health. This societal change creates a dynamic market where innovation thrives, and consumer loyalty is built on shared values and openness.

MARKET RESTRAINTS

High Cost of Premium and Sustainable Products

The elevated price point of premium and sustainable feminine hygiene products acts as a significant restraint on accessibility for lower-income demographics of the United States feminine hygiene products market. Organic cotton tampons and reusable menstrual cups often cost more than conventional synthetic alternatives. According to the Bureau of Labor Statistics, the Consumer Price Index for personal care products has faced severe upward pressure, outpacing real wage growth for many low-income households and inflating the baseline cost of essential hygiene items. This financial barrier prevents a substantial segment of the population from adopting healthier and more environmentally friendly options. Advocacy benchmarks from the Alliance for Period Supplies demonstrate that period poverty creates a disproportionate financial burden for individuals living below the poverty line, who frequently must choose between buying menstrual products or basic nutritional essentials. While some states have implemented tax exemptions for menstrual products known as the pink tax repeal,l these measures do not address the underlying high retail prices. Many consumers continue to rely on cheaper conventional products despite being aware of the potential health benefits of organic alternatives. The lack of universal insurance coverage for menstrual products further exacerbates this issue,ue as most health plans do not reimburse for these essential items. Consequently, price sensitivity remains a critical factor limiting the widespread adoption of premium segments. Manufacturers face the challenge of balancing cost efficiency with sustainable practices to make these products more affordable without compromising quality.

Regulatory Ambiguity and Ingredient Transparency Issues

Regulatory ambiguity regarding the classification and ingredient disclosure requirements for these hygiene products creates uncertainty and hinders consumer trust, which hampers the growth of the United States feminine hygiene products market. In the United States, menstrual products are regulated as medical devices by the Food and Drug Administration, but the specific standards for ingredient labeling have historically been inconsistent. Regulatory frameworks show that under traditional FDA medical device classifications, manufacturers were historically not mandated to disclose all raw materials, processing aids, or proprietary fragrances on packaging, prompting individual states to pass independent transparency laws. This lack of transparency makes it difficult for consumers to make fully informed decisions about potential allergens or toxins. Although recent legislation has mandated clearer labeling,g implementation varies across brands and product lines. This regulatory gap leads to skepticism among health-conscious consumers who may opt for alternative methods or reduce usage rather than risk exposure to unknown substances. The absence of standardized testing protocols for new materials such as those used in period underwear also complicates the assessment of safety and efficacy. The market faces resistance from educated consumers who demand higher levels of accountability and clarity from manufacturers. This is happening until comprehensive and uniform regulations are established.

MARKET OPPORTUNITIES

Expansion of Subscription-Based Direct-to-Consumer Models

The proliferation of subscription-based direct-to-consumer models is a key area for growth for the United States feminine hygiene products market. These services offer convenience, customization,n and consistent delivery which aligns with the busy lifestyles of modern consumers. Research shows that the subscription e-commerce model historically experienced explosive triple-digit annual growth during its emergence, paving the way for a highly mature multi-billion-dollar recurring retail ecosystem. Companies like Lola and Cora have capitalized on this trend by providing personalized boxes of organic tampons and pads delivered directly to customers' doors. This model reduces the friction of recurring purchases and ensures that users never run out of essential products. The ability to customize box contents allows consumers to mix and match products based on their flow and preferences, enhancing satisfaction. Furthermore, direct-to-consumer brands can gather valuable data on usage patterns, which informs product development and marketing strategies. The elimination of intermediaries also allows for competitive pricing despite the premium nature of organic products. As logistics networks improve and delivery speeds increase, the appeal of subscription services continues to grow. This shift not only drives revenue stability for brands but also fosters long-term customer relationships through consistent engagement and personalized experiences.

Innovation in Reusable and Zero Waste Solutions

The growing environmental consciousness among consumers has created a robust opportunity for reusable and zero-waste feminine hygiene products. This development is expected to propel the expansion of the United States feminine hygiene products market. Items such as menstrual cups, clothpads, and period underwear are gaining popularity as sustainable alternatives to single-use disposables. Life-cycle assessments highlight that the average consumer uses approximately 11,000 disposable menstrual products in their lifetime, generating significant volumes of single-use plastic and fiber waste destined for local landfills. This statistic has motivated many individuals to seek eco-friendly options that reduce their carbon footprint. The global reusable feminine care market is projected to expand rapidly as awareness of plastic pollution increases. Brands like Thinx and DivaCup have pioneered innovative designs that offer comfort and reliability comparable to traditional products. Retailers are responding by dedicating shelf space to reusable options and offering educational resources on their use.

Additionally, government initiatives promoting waste reduction support the adoption of reusable items through incentives and public awareness campaigns. As technology advances, the performance and ease of use of reusable products continue to improve,e making them accessible to a broader audience. This trend represents a fundamental shift in consumer behavior towards sustainability, ty offering substantial growth potential for companies that prioritize ecological responsibility.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Sourcing

Supply chain volatility and the scarcity of key raw materials are major hurdles to the stability of the United States feminine hygiene products market. The production of organic cotton and biodegradable materials relies on agricultural outputs that are susceptible to climate change and geopolitical disruptions. Data from the United States Department of Agriculture (USDA) confirms that domestic cotton production has faced severe volatility due to extreme weather, with intense regional droughts and floods causing double-digit crop volume drops that directly restrict raw textile supply chains. These variations lead to unpredictable pricing and availability of raw materials, affecting manufacturing costs and timelines. The pandemic further exposed vulnerabilities in global supply chains, with shipping delays and port congestion impacting the import of essential components. The Federal Reserve Bank of New York’s Global Supply Chain Pressure Index indicates a severe re-escalation in logistics volatility, with the index spiking to multi-year highs as geopolitical conflicts disrupt global maritime shipping routes and prolong merchant delivery windows. Manufacturers face the dilemma of maintaining inventory levels while managing rising storage and transportation costs. Additionally, the sourcing of certified organic materials requires strict adherence to supply chain traceability, which adds complexity and expense. Any disruption in the supply of specialized absorbent polymers or natural fibers can lead to stockouts and lost sales. Companies must invest in diversified sourcing strategies and resilient logistics networks to mitigate these risks. However, these adaptations require significant capital investment,t which can strain profit margins, ns particularly for smaller players in the market.

Intense Competition and Market Saturation

Intense competition and saturation are also limiting the expansion of the United States feminine hygiene products market. This makes it challenging for new entrants and established players alike to differentiate their offerings. The market is dominated by a few major conglomerates that control significant distribution channels and brand loyalty. This concentration leads to aggressive pricing wars and heavy marketing expenditure, res which erode profit margins. New brands often struggle to gain visibility amidst the noise of established advertising campaigns. The rise of private label products from major retailers further intensifies competition by offering lower-priced alternatives that mimic premium features. The Private Label Manufacturers Association (PLMA) reveals that store-brand beauty and personal care sales expanded by 2.8%, reflecting strong and steady consumer migration toward private label value alternatives. Differentiation through innovation becomes difficult as product features converge and patents expire.

Additionally, consumer switching costs are low, allowing shoppers to easily try new brands based on promotions or recommendations. This dynamic forces companies to continuously innovate and invest in brand building to maintain relevance. The saturation of traditional retail spaces also limits physical expansion opportunities, pushing brands to compete fiercely in the digital arena where customer acquisition costs are rising.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, and the rest of the United States |

| Market Leaders Profiled | Procter & Gamble Co., Kimberly-Clark Corporation, Edgewell Personal Care Company, Essity Aktiebolag, Johnson & Johnson, Kao Corporation, Unicharm Corporation, Ontex Group NV, First Quality Enterprises, Inc., Natracare LLC, Cora, Thinx Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

The sanitary napkins segment led the United States feminine hygiene products market and captured a 45.8% share in 2025. This leading position of the segment was attributed to its unmatched convenience and ease of use compared to other menstrual care options. The non-invasive nature of pads makes them the preferred choice for a vast majority of consumers, particularly among teenagers and women who are new to menstruation or those who prefer not to insert internal products. Large-scale demographic tracking reveals that sanitary pads remain the dominant method of menstrual management, utilized regularly by nearly 89% of menstruating individuals in the United States due to comfort, familiarity, and ease of use. This high adoption rate is driven by the simplicity of application and removal,l which requires minimal training or comfort with one’s body. Furthermore, re the availability of various sizes and absorbency levels allows users to customize their protection based on flow intensity, thereby ensuring reliability throughout the day. This reliability is crucial for maintaining daily productivity and confidence.

Additionally, the widespread availability of pads in virtually all retail outlets, from gas stations to grocery stores, ensures that consumers can easily access them in emergencies. The cultural normalization of pad usage in media and education further reinforces this preference. As a result,t the segment benefits from consistent repeat purchases and a broad demographic appeal that spans across age groups and lifestyles, es sustaining its dominance in the market.

Furthermore, the domination of the sanitary napkins segment is further reinforced by continuous technological advancements that enhance absorption, breathability, lightness, and overall comfort. Manufacturers have invested heavily in research and development to crultra-thin thin pads that offer superior protection without the bulkiness associated with traditional products. These improvements address common consumer complaints about discomfort and irritation, making pads a more viable option for active lifestyles. The integration of organic cotton covers and hypoallergenic materials has also attracted health-conscious consumers who are concerned about skin sensitivity. Additionally, the development of overnight and extra-long pads has expanded the usage scenarios, allowing women to rely on pads for extended periods, including sleep. These technological enhancements not only improve user experience but also justify premium pricing strategies. Consequently, the sanitary napkins segment maintains its leadership by evolving to meet the sophisticated demands of modern consumers who seek both functionality and comfort in their menstrual care solutions.

But the menstrual cups segment is predicted to witness the highest CAGR of 5.8% between 2026 and 203,4 owing to increasing environmental consciousness among consumers who are seeking sustainable alternatives to single-use disposable products. Menstrual cups, which are reusable for up to 10 years,s offer a zero-waste solution that aligns with the values of eco-conscious individuals. Younger demographics, particularly millennials and Generation Z, are leading this shift as they prioritize sustainability in their purchasing decisions. Menstrual cups eliminate the need for packaging waste associated with monthly purchases of pads and tampons. Furthermore, thecost-effectivenesss of cups over time appeals to budget-conscious consumers despite the higher upfront cost. The American Sustainable Business Council supports initiatives that promote reusable hygiene products as part of broader corporate responsibility goals. This convergence of environmental ethics and economic practicality fuels the rapid expansion of the menstrual cups segment.

The segment’s fast growth is boosted even more by the compelling value proposition of long-term cost savings and potential health benefits. While the initial purchase price of a menstrual cup ranges from $20 to $40, it eliminates the recurring expense of buying disposable products every month. Over a decade, this amounts to substantial savings,s making cups an economically attractive option. Additionally, menstrual cups are made of medical-grade silicone, which is inert and less likely to cause allergic reactions or irritations compared to the bleached cotton and synthetic fibers found in some disposables. The Food and Drug Administration recognizes medical-grade silicone as safe for internal use, reducing the risk of toxic shock syndrome,e which is associated with prolonged tampon use. The ability to wear a cup for up to 12 hours provides greater freedom and flexibility for work and travel. As more healthcare providers educate patients about these benefits, the stigma surrounding internal reusable devices diminishes. This combination of financial prudence and health safety accelerates the adoption rate of menstrual cups,s positioning it as the fastest growing segment in the market.

By Distribution Channel Insights

The supermarkets segment captured the majority share of 38.4% of the United States feminine hygiene products market in 2025. This supremacy of the segment was credited to its ubiquitous presence and the convenience of one-stop shopping. Consumers prefer purchasing essential personal care items alongside their regular grocery needs to save time and effort. The integration of feminine care aisles within larger retail environments allows for impulse buys and easy replenishment of stock. Major chains like Walmart, Kroger,r and Target offer extensive assortments ranging from budget-friendly private labels to premium organic brands, catering to diverse consumer preferences. Supermarkets also benefit from established supply chain efficiencies that ensure consistent product availability and competitive pricing. Promotional activities such as weekly discounts and bundle offers further drive sales volume in this channel. The familiarity of the shopping environment reduces the perceived risk of trying new products,s as consumers can easily compare prices and read labels in person. Additionally, the physical presence of products allows shoppers to verify package integrity and expiration dates, which is crucial for personal care items. These factors collectively sustain the dominance of supermarkets as the primary conduit for feminine hygiene product distribution in the United States.

In addition, the strong presence of private label offerings in supermarkets significantly contributes to their leadership in the feminine hygiene products distribution channel. Retailers have developed high-quality store brands that compete directly with national brands on both price and performance. Supermarkets leverage their direct relationships with manufacturers to offer these products at lower price points, attracting budget-conscious shoppers. The ability to control pricing strategies allows supermarkets to maintain healthy margins while offering competitive deals. This significant share demonstrates the trust consumers place in retailer brands. Furthermore, supermarkets often place private label products adjacent to national brands, facilitating direct comparison and encouraging trial. The consistent quality improvement of store brands has reduced the stigma previously associated with generic products. Loyalty programs integrated with supermarket apps provide personalized coupons and rewards for feminine care purchases, further enhancing customer retention. The strategic placement of these products in high-traffic areas ensures maximum visibility. By balancing national brand appeal with profitable private label options, supermarkets create a compelling value proposition that drives foot traffic and sustains their dominant position in the distribution landscape.

But the online retail stores segment is estimated to register the fastest CAGR of 7.2% from 2026 to 2034. Modern consumers are driving this segment’s growth by favoring the privacy and home delivery convenience of the shopping experience. Many individuals prefer purchasing feminine hygiene products online to avoid the potential embarrassment or awkwardness associated with buying them in physical stores. The ability to browse a wide range of products from the comfort of home allows consumers to make informed decisions without pressure. Subscription services offered by online retailers further enhance convenience by ensuring automatic delivery of essential items before they run out. This model is particularly popular for menstrual products, which are recurring necessities.

Additionally, online platforms provide detailed product descriptions and customer reviews,w hich help users select the most suitable items for their needs. The expansion of logistics networks has reduced delivery times, making online shopping a viable alternative for urgent needs. As digital literacy increases and mobile shopping becomes more prevalent,t the online channel continues to capture market share rapidly.

A further key factor accelerating the growth of online retail stores is the extensive access to niche and premium organic brands that are often unavailable in traditional supermarkets. Online platforms serve as a marketplace for specialized brands that focus on organic cotton, on biodegradable materials, as well as unique designs such as period underwear and menstrual cups. These niche brands often rely on digital marketing and direct-to-consumer sales channels to reach their target audience effectively. Social media influencers and health advocates play a significant role in promoting these products online, creating awareness and driving traffic to e-commerce sites. Online retailers also provide educational content and resources that help consumers understand the benefits of alternative products. This informational support builds trust and encourages trial among skeptical buyers. Furthermore, the ability to compare prices and features across multiple brands instantly empowers consumers to find the best value. The global reach of online marketplaces allows smaller brands to scale quickly without the burden of physical retail overhead. This dynamic ecosystem fosters innovation and competition,n driving the rapid growth of the online distribution channel.

COUNTRY MARKET ANALYSIS

U.S. Feminine Hygiene Products Analysis

The United States dominated the North American feminine hygiene products market and accounted for a 81.5% share in 2025. This expansion of the US market was driven by the country's large population, high healthcare expenditure, and advanced retail infrastructure. The market status is characterized by a mature yet dynamic environment where innovation and consumer preferences drive continuous evolution. According to recent U.S. Census Bureau estimates, the female population of reproductive age (15–49) is approximately 75 million, providing a massive, consistent consumer base for the menstrual care market. The high prevalence of health awareness campaigns has educated consumers about intimate hygiene,e leading to increased demand for specialized cleaning and deodorizing products. The Centers for Disease Control and Prevention (CDC) advocates for comprehensive health education to reduce risk behaviors. However, their recent surveillance reports indicate that access to sexual and reproductive health education in U.S. schools has actually declined, leaving significant gaps in student knowledge and preparedness.

Additionally, the United States has a robust regulatory framework enforced by the Food and Drug Administration, which ensures product safety and quality, building consumer trust. The presence of major global players and innovative startups fosters intense competition, resulting in a wide array of product options. High disposable income levels allow consumers to purchase premium and organic products, contributing to market value growth. The trend towards sustainability is particularly strong in the United States, with many states implementing bans on plastic microbeads and promoting eco-friendly alternatives. Furthermore, the rise of telehealth and digital health platforms has facilitated access to professional advice regarding feminine health issues. These structural, demographic, and economic factors solidify the United States as the leading market for feminine hygiene products in the region, with sustained growth potential driven by health consciousness and technological advancements.

COMPETITIVE LANDSCAPE

The competition in the United States feminine hygiene products market is intense and characterized by a mix of established global conglomerates and agile niche brands. Major players leverage their extensive distribution networks and brand recognition to maintain dominance, while newer entrants disrupt the market with innovative, sustainable solutions. The rivalry is further amplified by the increasing convergence of health consciousness and environmental responsibility, where product safety and eco-friendliness are key differentiators. Companies are constantly innovating to offer organic cotton, biodegradable materials,s and reusable options to meet diverse consumer needs. Price competition is fierce, particularly in the mass market segment where private labels offer affordable alternatives. Traditional brands face pressure to adapt to digital-first strategies and subscription models that enhance customer retention. The threat of substitution from menstrual cups and period underwear also influences competitive dynamics. Brand loyalty is cultivated through transparent communication and social advocacy initiatives. Regulatory compliance and ingredient transparency serve as critical factors in building consumer trust. Overall, the market demands continuous adaptation to technological trends and societal values to sustain competitive advantage and profitability in this evolving industry landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Feminine Hygiene Products Market include

- Procter & Gamble Co.

- Kimberly-Clark Corporation

- Edgewell Personal Care Company

- Essity Aktiebolag

- Johnson & Johnson

- Kao Corporation

- Unicharm Corporation

- Ontex Group NV

- First Quality Enterprises, Inc.

- Natracare LLC

- Cora

- Thinx Inc.

TOP LEADING PLAYERS IN THE MARKET

- Procter and Gamble is a pivotal force in the United States feminine hygiene sector through its iconic Tampax and Always brands. The company consistently drives innovation by introducing advanced absorbency technologies and sustainable material options to meet evolving consumer needs. Recently, Procter and Gamble has focused on expanding its organic product lines to cater to health-conscious shoppers seeking chemical-free alternatives. The corporation actively engages in social responsibility initiatives such as the Always Period Poverty program, which provides products and education to underserved communities. These efforts enhance brand loyalty and reinforce its commitment to accessibility. By leveraging its extensive distribution network and robust research capabilities, the company maintains a strong presence in both retail and digital channels. Their continuous investment in marketing campaigns that destigmatize menstruation further solidifies their cultural relevance and consumer connection in the competitive landscape.

- Kimberly Clark is a major contributor to the United States feminine hygiene market with its well-known Kotex brand, which offers a diverse range of pads, tampons,s and disposable underwear. The company focuses on delivering comfort and reliability through continuous product refinement and design innovation. Recently, Kimberly-Clark has emphasized sustainability by launching biodegradable options and reducing plastic usage in packaging to align with environmental goals. They have also expanded their digital engagement strategies using social media platforms to connect with younger demographics and promote open conversations about menstrual health. The company collaborates with influencers and health experts to educate consumers on proper hygiene practices. By prioritizing user feedback and adapting to changing preferences, Kimberly-Clark strengthens its brand equity. Their commitment to affordability ensures broad accessibility while premium innovations attract value-driven consumers seeking enhanced performance and eco-friendly solutions in their personal care routines.

- Edgewell Personal Care plays a significant role in the United States feminine hygiene market through its Playtex and Stayfree brands, which are recognized for their innovative designs and reliability. The company focuses on providing high-quality products that address specific consumer needs, such as active lifestyles and sensitive skin. Recently,y Edgewell has invested in expanding its organic and natural product portfolios to capture the growing segment of health-conscious buyers. They have also enhanced their supply chain efficiency to ensure consistent product availability across various retail channels. The company actively participates in community outreach programs aimed at ending period poverty and improving menstrual health education. By leveraging strategic partnerships with retailers and healthcare providers, Edgewell increases its market reach. Their focus on product differentiation through unique features like flexible fit technology helps them stand out in a crowded marketplace. These initiatives collectively strengthen their competitive position and foster long-term customer loyalty in the dynamic feminine care sector.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States feminine hygiene products market employ several strategic initiatives to maintain competitiveness and drive growth. Product innovation remains a primary strategy with companies investing heavily in organic materials and biodegradable options to appeal to environmentally conscious consumers. Brands are increasingly adopting direct-to-consumer models and subscription services to enhance customer convenience and loyalty. Digital marketing and social media engagement are crucial for destigmatizing menstruation and connecting with younger demographics. Strategic partnerships with non-profits and educational organizations help build brand trust and address period poverty. Companies are also focusing on sustainability by reducing plastic packaging and implementing recycling programs. Price competitiveness is maintained through efficient supply chain management and private label offerings. Regulatory compliance and transparency in ingredient labeling are prioritized to meet consumer demands for safety. These strategies collectively enable companies to adapt to evolving preferences and strengthen their market presence effectively.

U.S. Feminine Hygiene Products Market NEWS

- In March 2023, Procter and Gamble, a consumer goods giant, launched a new organic cotton line for its Always brand. This launch is anticipated to attract health-conscious consumers and strengthen the US feminine hygiene products market presence.

- In June 2023, Kimberly-Clark, a personal care corporation, introduced biodegradable packaging for its Kotex product range. This initiative is anticipated to reduce environmental impact and strengthen the US feminine hygiene products market presence.

- In September 2023, Edgewell Personal Care, a hygiene company, expanded its subscription service for Playtex tampons and pads. This expansion is anticipated to enhance customer convenience and strengthen the US feminine hygiene products market presence.

- In January 2024, Procter and Gamble, a global leader, partnered with a national nonprofit to distribute free period products in schools. This partnership is anticipated to address period poverty and strengthen the US feminine hygiene product market presence.

- In May 2024, Kimberly-Clark, a major manufacturer, invested in new manufacturing facilities dedicated to sustainable feminine care products. This investment is anticipated to increase production capacity and strengthen the US feminine hygiene products market presence.

MARKET SEGMENTATION

This research report on the U.S. feminine hygiene products market is segmented and sub-segmented into the following categories.

By Product Type

- Sanitary Napkins

- Tampons

- Panty Liners

- Menstrual Cups

- Others

By Distribution Channel

- Supermarkets

- Pharmacies & Drug Stores

- Convenience Stores

- Online Retail Stores

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com