U.S. Flexible Packaging Market Size, Share, Trends & Growth Forecast Report By Material Type, Product Type, End User Industry, Distribution Channel, and Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$71.19 BnMarket Estimate, 2026

$74.23 BnMarket Forecast, 2034

$103.72 BnCAGR, 2026–2034

4.27%U.S. Flexible Packaging Market Report Summary

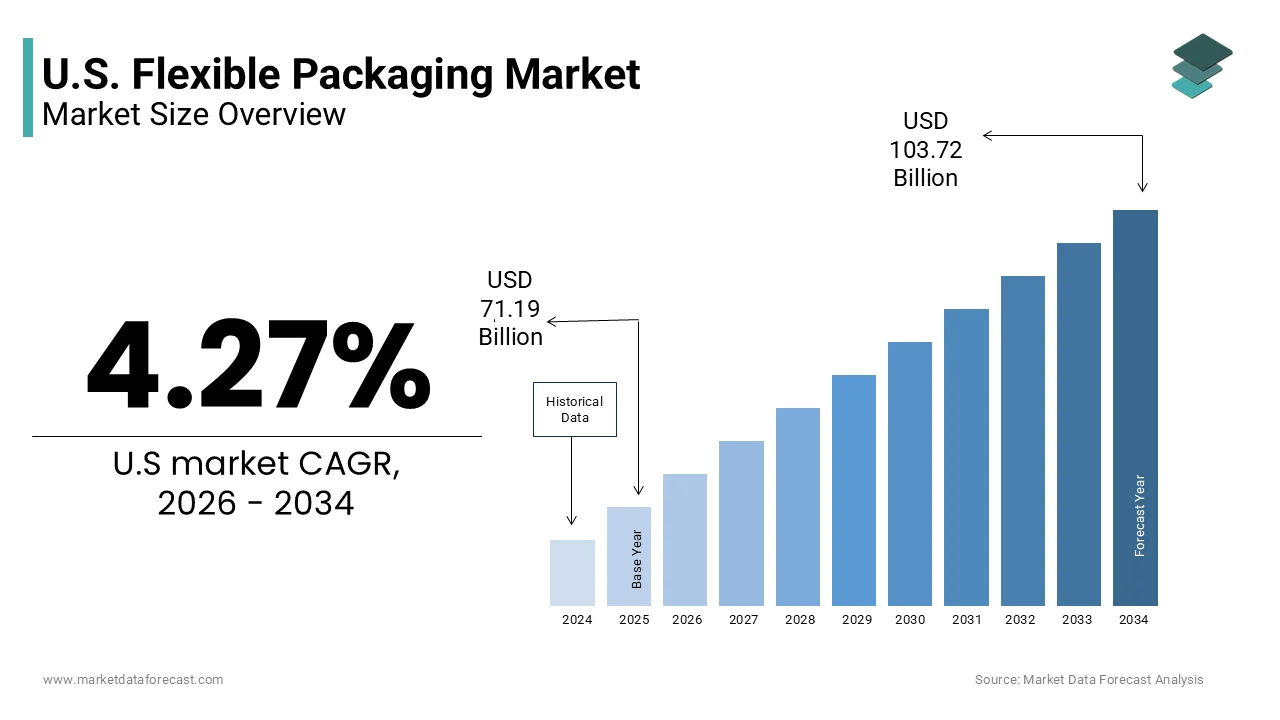

The U.S. flexible packaging market was valued at USD 71.19 billion in 2025, is estimated to reach USD 74.23 billion in 2026, and is projected to reach USD 103.72 billion by 2034, growing at a CAGR of 4.27% during the forecast period. Market growth is driven by increasing demand for lightweight packaging solutions, rising food and beverage consumption, and expanding e commerce activities. Flexible packaging is gaining widespread adoption due to its cost efficiency, product protection capabilities, and sustainability advantages. Growing investments in recyclable materials and advanced packaging technologies are further supporting market expansion across the United States.

Key Market Trends

- Growing demand for lightweight and sustainable packaging solutions is driving market growth.

- Increasing food and beverage consumption is boosting flexible packaging adoption.

- Rising e commerce activities and product distribution requirements are supporting market expansion.

- Expansion of recyclable and environmentally efficient packaging technologies is enhancing industry development.

- Innovation in barrier protection technologies and smart packaging solutions is influencing market advancement.

Segmental Insights

- Based on material type, the plastics segment accounted for 44.3% of the U.S. flexible packaging market share in 2025. This dominance is attributed to durability, lightweight characteristics, and versatility across packaging applications.

- Based on product type, the bags and sachets segment held 54.2% of the U.S. flexible packaging market share in 2025, supported by broad usage across food, personal care, and industrial packaging applications.

- Based on end user industry, the food industry segment accounted for 34.3% of the U.S. flexible packaging market share in 2025, driven by growing packaged food demand and product shelf life requirements.

- Based on distribution channel, the direct business to business channel segment held a significant share of the U.S. flexible packaging market in 2025, supported by large scale industrial procurement and manufacturing partnerships.

Regional Insights

- The U.S. flexible packaging market continues to experience stable growth due to increasing packaging innovation, rising demand for convenience oriented products, and growing sustainability initiatives across consumer industries.

Competitive Landscape

The U.S. flexible packaging market is highly competitive, with companies focusing on recyclable materials, advanced barrier technologies, and sustainable packaging innovation to strengthen their market position. Manufacturers continue investing in production efficiency and environmentally responsible packaging solutions. Prominent players in the U.S. flexible packaging market include Amcor plc, Berry Global Inc., Mondi, Sonoco Products Company, Constantia Flexibles, Sealed Air, TC Transcontinental, WINPAK LTD, Bemis Company, Inc., and Coveris Holdings S.A..

U.S. Flexible Packaging Market Size

The U.S. flexible packaging market size was valued at USD 71.19 billion in 2025, is estimated to reach USD 74.23 billion in 2026, and is projected to reach USD 103.72 billion by 2034, growing at a CAGR of 4.27%.

The flexible packaging is the production of non-rigid packaging solutions constructed from materials, such as plastic films, paper foil, and their combinations. These packages are engineered to conform to the shape of the contained product offering advantages in material efficiency storage and transportation compared to rigid alternatives. The flexible packaging generates significantly less waste by weight compared to rigid containers contributing to reduced landfill volume. The manufacturing sector for plastics and rubber products employs hundreds of thousands of workers reflecting the labor intensive nature of film extrusion and converting processes. Consumer behavior shifts towards on-the-go consumption have further accelerated demand for lightweight and portable packaging formats. The perishable food items in retail environments utilize some form of flexible packaging to extend shelf life and maintain freshness.

MARKET DRIVERS

Expansion of E Commerce and Direct to Consumer Logistics

The rapid expansion of e-commerce and direct to consumer sales channels due to the unique logistical requirements of online is propelling the growth of the United States flexible packaging market. Unlike traditional brick and mortar retail, where packaging primarily serves marketing and shelf presence functions e-commerce packaging must withstand rigorous shipping conditions, while minimizing dimensional weight to reduce freight costs. Flexible packaging, such as poly mailers and padded envelopes offers superior protection against moisture and abrasion, while occupying minimal space during storage and transit compared to rigid boxes. The retailers are increasingly adopting right sized packaging strategies to optimize shipping efficiency, which favors flexible formats that can conform to product shapes. Additionally, the rise of subscription based services for groceries and personal care items has intensified the need for resealable and tamper evident flexible pouches that enhance user experience. These mailers often utilize multi-layer films that provide barrier properties essential for preserving product integrity during extended transit times. The cost advantage of flexible packaging in terms of material usage and shipping fees makes it an indispensable component of modern logistics infrastructure.

Demand for Convenience and Portability in Food Consumption

The shifting consumer lifestyles characterized by busy schedules and increased mobility have driven substantial demand for convenient and portable solutions is additionally fuelling the growth of the United States flexible packaging market. Modern consumers prioritize ease of use leading to the widespread adoption of stand-up pouches resealable bags and single serve sachets that facilitate on the go consumption. A significant majority of shoppers indicate that convenience is a key factor influencing their purchasing decisions, particularly for snack foods and ready to eat meals. Flexible packaging enables manufacturers to create lightweight and compact formats that fit easily into bags pockets and lunchboxes appealing to students professionals and travelers. The consumption of processed and packaged foods has risen as households seek time saving meal solutions. Stand up pouches in particular have gained popularity due to their stability on shelves and ability to be resealed maintaining product freshness after opening. This format also allows for high quality printing and vibrant graphics which enhance brand visibility and consumer engagement at the point of sale. Furthermore, the versatility of flexible films allows for the integration of features such as spouts zippers and tear notches, which improve usability for diverse demographics including children and elderly individuals.

MARKET RESTRAINTS

Complexities in Recycling Infrastructure for Multi Layer Films

The intricate composition of multi-layer flexible packaging due to challenges in recycling and waste management is hindering the growth of the United States flexible packaging market. Most flexible packages consist of multiple layers of different materials, such as polyethylene, polyester, and aluminum, laminated together to provide barrier properties against oxygen moisture and light. These multi-material structures are difficult to separate and recycle using conventional mechanical recycling processes, which are designed for single stream mono materials. This low recycling rate has drawn criticism from environmental groups and regulators leading to increased pressure on brands to adopt more sustainable packaging alternatives. Many municipal recycling programs explicitly exclude flexible films from curbside collection due to the risk of machinery jamming and contamination of other recyclables. Although, store drop off programs exist for certain plastic films consumer participation remains low due to lack of awareness and convenience. The inability to effectively close the loop on flexible packaging waste undermines corporate sustainability goals and exposes companies to reputational risks.

Volatility in Resin and Raw Material Prices

The volatility in prices of key raw materials, such as polyethylene, polypropylene, and polyester resins on the profitability and stability is also hampering the growth of the United States flexible packaging market. These polymers are derived from crude oil and natural gas making their costs highly susceptible to fluctuations in global energy sector and geopolitical tensions. The Producer Price Index for plastics materials and resins has experienced significant variability in recent years with swings affecting manufacturing costs. When resin prices spike packaging converters face margin compression as they struggle to pass these increased costs onto price sensitive customers in competitive sectors like food and beverage. The American Chemistry Council notes that supply chain disruptions and feedstock shortages can exacerbate price instability leading to unpredictable procurement expenses for manufacturers. Additionally, the transition towards bio based and recycled resins often involves higher premiums compared to virgin fossil-based materials further straining budgets. Companies must constantly adjust their pricing strategies and hedging mechanisms to manage this volatility which can disrupt long term planning and investment decisions. Small and medium sized converters are particularly vulnerable to these fluctuations as they lack the purchasing power and financial reserves of larger integrated firms. This economic uncertainty discourages innovation and capacity expansion as firms prioritize cost containment over growth initiatives.

MARKET OPPORTUNITIES

Adoption of Mono Material and Recyclable Structures

The development and adoption of mono material flexible packaging structures to address sustainability concerns, while maintaining performance standards is likely to fuel the growth of the United States flexible packaging market. Mono material designs utilize a single type of polymer, such as all polyethylene or all polypropylene throughout the package structure enabling easier recycling through existing streams. Technological advancements in coating and adhesive technologies, now allow mono material films to achieve barrier properties comparable to traditional multi-layer laminates. The shifting to mono materials is a step towards achieving a circular economy for plastics. Companies investing in research and development of these structures can differentiate themselves in the market and secure contracts with environmentally conscious clients. Government incentives and tax credits for sustainable packaging innovations that further encourage adoption and commercialization. Additionally, the establishment of standardized design guidelines for recyclability by organizations such as the How2Recycle label helps consumers properly dispose of these packages increasing recovery rates. As regulatory pressure intensifies and consumer awareness grows, the market for mono material flexible packaging is poised for robust expansion.

Integration of Smart and Active Packaging Technologies

The integration of smart and active packaging technologies to enhance product safety and consumer engagement is also to elevate the growth of the United States flexible packaging market. Smart packaging incorporates elements, such as QR codes near field communication tags and time temperature indicators that provide real time information about product quality and authenticity. The active packaging systems can extend shelf life by absorbing oxygen ethylene or moisture, thereby reducing food waste and improving sustainability. The Food and Drug Administration supports the use of these technologies as they enhance traceability and safety in the supply chain particularly for perishable goods and pharmaceuticals. Brands are leveraging smart packaging to connect directly with consumers offering interactive experiences such as recipe suggestions provenance tracking and loyalty rewards. As Internet of Things connectivity expands, the potential applications for smart flexible packaging grow across various sectors, including healthcare where patient compliance monitoring is important. Manufacturers who incorporate these advanced features can command premium pricing and strengthen brand loyalty. The convergence of packaging with digital technology transforms passive containers into interactive platforms creating new revenue streams and value propositions.

MARKET CHALLENGES

Regulatory Pressure and Extended Producer Responsibility Laws

The introduction of stringent regulations and extended producer responsibility EPR laws constitutes a major challenge for the United States flexible packaging market. Several states, including California, Maine, and Oregon, have enacted or are considering EPR legislation that requires producers to fund the collection sorting and recycling of their packaging waste. These laws shift the cost of waste management from municipalities to packaging producers, necessitating significant investments in infrastructure and compliance systems. Companies must navigate a complex and fragmented regulations, where requirements vary by jurisdiction creating administrative inefficiencies and increased legal costs. The need for standardized national policies but until then firms must adapt to disparate local rules. Compliance with EPR mandates often requires detailed reporting on material composition and volume which can be difficult for complex supply chains. Additionally, the definition of recyclability under these laws is evolving forcing companies to redesign products frequently to meet changing criteria. Failure to comply can result in hefty fines and restrictions on market access. The uncertainty surrounding future regulatory developments creates a challenging environment for long term strategic planning. Manufacturers must balance the cost of compliance with the need to remain competitive while accelerating the transition to sustainable materials.

Supply Chain Disruptions and Material Shortages

The persistent supply chain disruptions and material shortages by affecting production continuity and customer satisfaction is also to inhibit the growth of the United States flexible packaging market. The industry relies on a global network of suppliers for resins additives and machinery components making it vulnerable to geopolitical tensions trade disputes and logistical bottlenecks. The manufacturing lead times have remained elevated in recent years due to port congestion and labor shortages in the transportation sector. The chip shortages have also impacted the production of advanced converting equipment delaying capacity expansions and maintenance upgrades. These disruptions force manufacturers to hold higher inventory levels tying up capital and increasing storage costs. Additionally, unexpected shutdowns at resin production facilities due to weather events or maintenance issues can create sudden shortages of critical raw materials. Customers facing delays may switch to alternative packaging formats or suppliers eroding long term relationships. Managing these risks requires diversified sourcing strategies and robust contingency planning which can be resource intensive. The unpredictability of global supply chains complicates production scheduling and order fulfillment undermining reliability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.27% |

| Segments Covered | By Material Type, Product Type, End User Industry, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Amcor plc, Berry Global Inc., Mondi, Sonoco Products Company, Constantia Flexibles, Sealed Air, TC Transcontinental, WINPAK LTD, Bemis Company, Inc., and Coveris Holdings S.A. |

SEGMENTAL ANALYSIS

By Material Type Insights

The plastics segment was accounted in holding 44.3% of the United States flexible packaging market share in 2025 due to their unparalleled ability to provide barrier protection against moisture oxygen and light, which is for preserving product quality. Multi-layer plastic films can be engineered to offer specific permeability rates that significantly extend the shelf life of perishable goods such as meats cheeses and fresh produce. The effective packaging barriers are essential for preventing foodborne illnesses and reducing spoilage, which accounts for a significant portion of food waste. Polyethylene and polypropylene films are widely used because they are lightweight durable and cost effective compared to alternative materials. The versatility of plastic allows for the integration of active packaging technologies such as oxygen scavengers and antimicrobial agents further enhancing preservation capabilities. This functional superiority ensures that plastics remain the material of choice for manufacturers who prioritize product safety and longevity. The ability to customize film structures for specific applications ranging from high barrier retort pouches to breathable produce bags solidifies the dominance of plastics in the market.

The paper segment is expected to register a fastest CAGR of 6.3% from 2026 to 2034 with the stringent regulatory pressures and consumer demand for sustainable compostable packaging options. Governments and municipalities are increasingly implementing bans on single use plastics and mandating higher recycled content in packaging, which favors paper based alternatives. The several states have enacted laws restricting plastic bags and promoting reusable or compostable options by creating a favorable environment for paper packaging innovation. The Environmental Protection Agency emphasizes the importance of shifting towards materials with established recycling infrastructure and paper boasts one of the highest recovery rates among packaging materials. Advances in coating technologies now allow paper films to offer improved moisture and grease resistance making them viable for a wider range of food applications. Major brands are transitioning to paper-based pouches and wrappers to meet corporate sustainability goals and enhance brand image.

By Product Type Insights

The bags and sachets segment was the largest by holding 54.2% of the United States flexible packaging market share in 2025 due to their ubiquitous presence in retail environments and unparalleled convenience for consumers. This product type includes a wide range of formats, such as stand-up pouches flat bottom bags and single serve sachets, which are used for everything from snacks and coffee to personal care samples. The majority of packaged food items sold in supermarkets utilize bag or sachet formats due to their ease of handling and storage. The versatility of bags allows for various closure mechanisms including zippers spouts and tear notches which enhance user experience and product freshness. The convenience factor is particularly important for on the go consumption trends where portability and resealability are key purchasing drivers. Stand up pouches have gained significant traction because they offer stable shelf presence and efficient use of retail space compared to rigid containers. The stand-up pouches are one of the fastest growing package formats in the food industry due to their consumer appeal and manufacturing efficiency. The ability to customize sizes from single serve portions to family packs enables brands to target diverse consumer segments effectively.

The pouches segment is esteemed to grow at an anticipated CAGR of 5.1% from 2026 to 2034 with their expansion into premium and value-added product categories. Brands are increasingly adopting stand up pouches for products, such as organic foods pet food and health supplements to convey a sense of quality and modernity. The structural integrity of stand up pouches allows them to sit upright on shelves providing excellent visibility and branding space which is critical for attracting consumer attention in crowded retail aisles. The ability to incorporate features such as clear windows resealable zippers and spouts enhances functionality and perceived value. Premium brands leverage these features to justify higher price points and differentiate themselves from competitors using traditional packaging. The aesthetic appeal of pouches combined with their practical benefits makes them ideal for launching new products and revitalizing existing brands.

By End User Industry Insights

The food industry segment was the dominant by holding 34.3% of the United States flexible packaging market share in 2025 due to the role packaging plays in preserving food quality and ensuring safety. Flexible packaging provides essential barriers against contaminants moisture and oxygen, which are necessary to prevent spoilage and extend shelf life. The proper packaging is a primary control point for preventing foodborne illnesses and maintaining compliance with safety standards. The majority of fresh and processed food products are packaged in flexible formats, such as films bags and pouches. The versatility of flexible packaging allows it to accommodate a wide range of food types from fresh produce and meats to dry goods and frozen items. Modified atmosphere packaging techniques, which utilize flexible films to alter the gas composition inside the package further enhance preservation and reduce waste. The ability to maintain freshness during long distribution chains is vital for the national food supply network. As consumer demand for fresh and minimally processed foods increases, the reliance on high performance flexible packaging solutions grows.

The pharmaceutical and medical segment is likely to grow at a fastest CAGR of 4.3% from 2026 to 2034 owing to the stringent regulatory requirements for sterility and tamper evidence. Flexible packaging materials, such as blister packs, foil pouches, and sterile barrier systems, which are essential for protecting sensitive medical devices and medications from contamination. The medical packaging must meet rigorous standards for barrier performance and integrity to ensure patient safety. The aging population and increasing prevalence of chronic diseases have led to higher consumption of prescription drugs and over the counter medications, which require secure packaging. The demand for unit dose packaging, which often utilizes flexible films is rising due to its ability to improve medication adherence and reduce errors. Flexible packaging offers lightweight and compact solutions for distributing medical supplies, which is for hospitals and home healthcare settings. The need for child resistant and senior friendly features further drives innovation in flexible pharmaceutical packaging.

By Distribution Channel Insights

The direct business to business B2B channels segment held a significant share of the United States flexible packaging market in 2025 due to the industrial scale of procurement and deep integration into manufacturing supply chains. Large food beverage and consumer goods manufacturers purchase flexible packaging in bulk directly from converters to ensure consistent supply and cost efficiency. Direct B2B transactions allow for customized packaging solutions tailored to specific production lines and automation requirements. Long term contracts between manufacturers and packaging suppliers provide stability and predictability for both parties. The ability to coordinate just in time delivery reduces inventory holding costs and optimizes warehouse space for large corporations. The National Association of Manufacturers emphasizes the importance of reliable supply chain partnerships for maintaining operational efficiency. Direct relationships also facilitate collaboration on innovation and sustainability initiatives allowing brands to develop proprietary packaging formats.

The e-commerce and fulfilment segment is lucratively growing at a fastest CAGR of 8.1% during the forecast period with the explosive growth of online retail and direct to consumer DTC models. As more consumers shop online, the demand for durable lightweight and protective shipping packaging has surged. DTC brands prefer flexible packaging for its cost effectiveness and branding potential allowing them to create unboxing experiences that enhance customer loyalty. The retailers are investing heavily in fulfilment infrastructure to meet the demands of online shoppers. Flexible packaging such as poly mailers is ideal for e commerce because it reduces dimensional weight and shipping costs compared to boxes.

COMPETITIVE LANDSCAPE

The competition in the United States flexible packaging market is intense and characterized by the presence of large multinational corporations alongside numerous regional and niche players. Leading companies compete on the basis of innovation sustainability and cost efficiency, while smaller firms often focus on specialized applications or local service excellence. Established players leverage their extensive distribution networks and technical expertise to maintain dominance. However, agile competitors disrupt the market by introducing novel materials and designs that address emerging consumer needs. Price competition remains significant particularly in commodity segments where differentiation is limited. Strategic partnerships and collaborations are common as firms seek to share risks and accelerate innovation. Sustainability has become a key differentiator with companies racing to develop circular packaging solutions. Regulatory pressures and changing consumer preferences drive continuous adaptation.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. flexible packaging market are

- Amcor plc

- Berry Global Inc.

- Mondi

- Sonoco Products Company

- Constantia Flexibles

- Sealed Air

- TC Transcontinental

- WINPAK LTD

- Bemis Company, Inc.

- Coveris Holdings S.A.

Top Players in the Market

- Amcor plc is a global leader in packaging solutions with a significant presence in the United States flexible packaging sector. The company provides a wide range of innovative and sustainable packaging products for food beverage healthcare and other consumer goods. Amcor has recently focused on expanding its portfolio of recyclable and compostable flexible packaging solutions to meet growing environmental demands. The company invested in advanced manufacturing technologies to enhance production efficiency and product quality. Amcor also strengthened its position through strategic acquisitions and partnerships that broaden its geographic reach and technical capabilities. Their commitment to circular economy principles drives the development of new materials and designs that reduce waste and carbon footprint.

- Sonoco Products Company is a major provider of consumer packaging industrial products and protective solutions in the United States. The company plays a vital role in the flexible packaging market by offering diverse film and pouch solutions for various industries. Sonoco has recently emphasized sustainability by launching new recyclable flexible packaging structures and increasing the use of recycled content. The company expanded its converting capabilities to support faster turnaround times and customized solutions for clients. Sonoco also invested in digital printing technologies to enhance branding opportunities for customers. Their focus on operational excellence and customer centric innovation strengthens their competitive position.

- Berry Global Inc is a leading manufacturer of packaging and protection products with a strong footprint in the US flexible packaging market. The company produces a vast array of flexible films bags and pouches for food healthcare and industrial applications. Berry Global has recently accelerated its sustainability initiatives by developing advanced recycling technologies and introducing mono material flexible packaging solutions. The company expanded its production capacity through strategic investments in new facilities and equipment upgrades. Berry Global also focuses on collaborating with customers to create lightweight and efficient packaging designs that reduce material usage. Their commitment to innovation and sustainability drives value for stakeholders and supports environmental goals.

Top Strategies Used by Key Market Participants

Key players in the United States flexible packaging market primarily employ sustainability driven innovation and strategic consolidation to maintain competitive advantage. Companies invest heavily in research and development to create recyclable compostable and bio-based materials that align with environmental regulations and consumer preferences. Mergers and acquisitions are frequently utilized to expand product portfolios enhance technological capabilities and access new customer segments. Operational efficiency is improved through automation and digitalization of manufacturing processes, which reduces costs and improves quality consistency. Partnerships with brand owners facilitate co development of customized packaging solutions that meet specific functional and aesthetic requirements. Expansion into high growth sectors such as e commerce and healthcare diversifies revenue streams. Additionally, firms focus on supply chain resilience by sourcing raw materials locally and optimizing logistics networks. These multifaceted strategies enable companies to adapt to market dynamics while delivering value through innovation and sustainability.

MARKET SEGMENTATION

This research report on the U.S. flexible packaging market is segmented and sub-segmented into the following categories.

By Material Type

- Plastics

- Polyethylene (PE)

- Biaxially Oriented Polypropylene (BOPP)

- Cast Polypropylene (CPP)

- Polyvinyl Chloride (PVC)

- Ethylene Vinyl Alcohol (EVOH)

- Paper

- Aluminum Foil

By Product Type

- Pouches

- Bags and Sachets

- Films and Wraps

- Shrink Sleeves and Labels

- Other Product Types

By End User Industry

- Food

- Frozen Food

- Dairy Products

- Fruits and Vegetables

- Meat, Poultry and Seafood

- Baked Goods and Snacks

- Confectionery

- Other Food

- Beverage

- Pharmaceutical and Medical

- Household and Personal Care

- Industrial and Chemical

- Other End User Industries

By Distribution Channel

- Direct B2B

- E commerce & Fulfilment

- Retail

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1.What is flexible packaging?

Flexible packaging refers to packaging made from materials such as plastic, paper, and aluminum foil that can easily change shape and are used to protect, preserve, and transport products.

2.What factors are driving the growth of the U.S. flexible packaging market?

Increasing demand for lightweight packaging, rising food and beverage consumption, and growing preference for sustainable packaging solutions are driving market growth.

3.What materials are commonly used in flexible packaging?

Common materials include polyethylene, biaxially oriented polypropylene, cast polypropylene, polyvinyl chloride, paper, and aluminum foil.

4.Which industries are major users of flexible packaging?

Food, beverage, pharmaceutical, medical, household care, personal care, and industrial sectors are major end users of flexible packaging.

5.Why is flexible packaging gaining popularity in the food industry?

Flexible packaging helps improve product shelf life, reduces packaging waste, and provides convenience for storage and transportation.

6.What types of products are included in flexible packaging solutions?

Flexible packaging products include pouches, bags, sachets, films, wraps, shrink sleeves, and labels.

7.How does flexible packaging support sustainability goals?

Flexible packaging often uses fewer raw materials and reduces transportation costs, helping companies lower environmental impact.

8.What role does e commerce play in the U.S. flexible packaging market?

The growth of e commerce is increasing demand for durable, lightweight, and protective packaging solutions.

9.What technological advancements are influencing flexible packaging?

Innovations in recyclable materials, barrier technologies, and smart packaging solutions are shaping market development.

10.What challenges affect the U.S. flexible packaging market?

Raw material price fluctuations, recycling challenges, and environmental regulations can impact market growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com