U.S. Food Retail Market Size, Share, Trends & Growth Forecast Report By Product Type (Fresh Food, Packaged / Processed Food, Organic & Health Foods), Sales Channel, and Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$180.52 BnMarket Estimate, 2026

$190.83 BnMarket Forecast, 2034

$297.56 BnCAGR, 2026–2034

5.71%U.S. Food Retail Market Report Summary

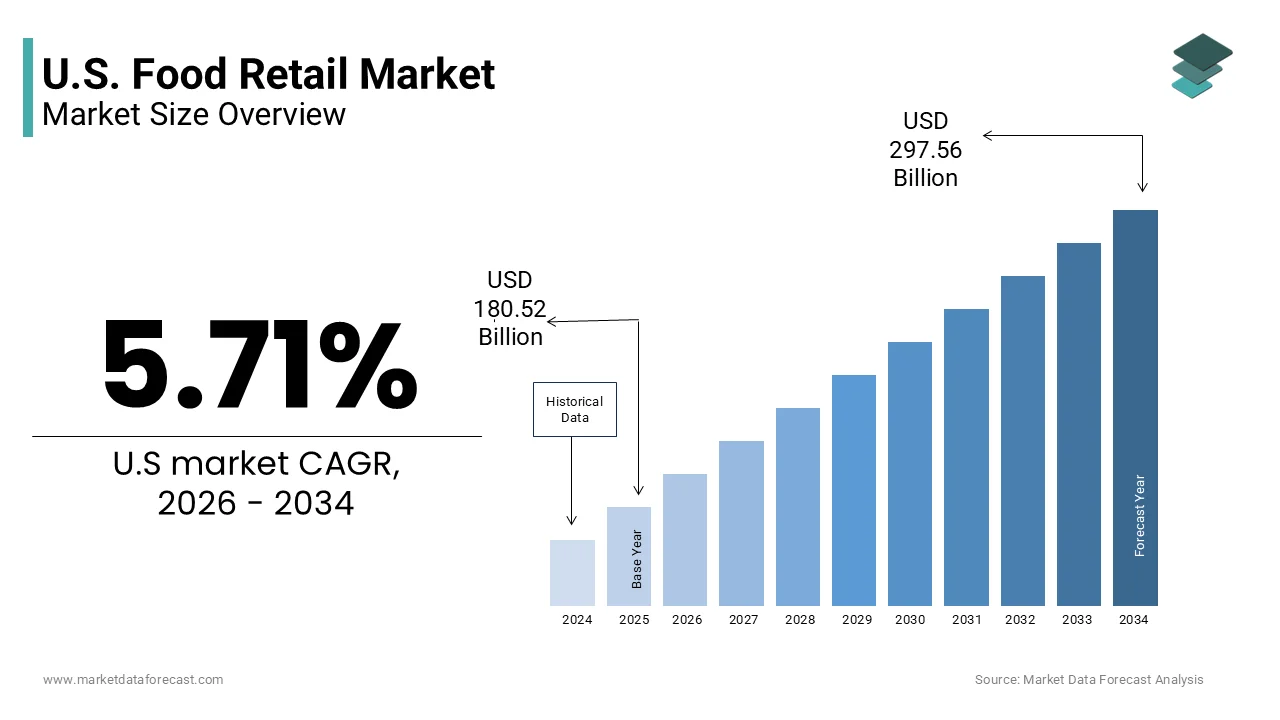

The U.S. food retail market was valued at USD 180.52 billion in 2025, is estimated to reach USD 190.83 billion in 2026, and is projected to reach USD 297.56 billion by 2034, growing at a CAGR of 5.71% during the forecast period. Market growth is driven by increasing consumer spending on food products, expanding organized retail networks, and rising demand for convenience, packaged, and ready to consume food items. The food retail sector continues to evolve through digital transformation, omnichannel shopping experiences, and growing adoption of online grocery platforms. Changing consumer preferences, health conscious purchasing behavior, and technological advancements are further supporting market expansion across the United States.

Key Market Trends

- Growing consumer demand for convenience foods and ready to eat products is driving market growth.

- Increasing adoption of online grocery shopping and omnichannel retail strategies is boosting market expansion.

- Rising demand for packaged, processed, and value added food products is supporting industry development.

- Expansion of private label offerings and loyalty programs is enhancing customer engagement.

- Innovation in digital retail technologies, automated fulfillment, and personalized shopping experiences is influencing market advancement.

Segmental Insights

- Based on product type, the packaged and processed food segment accounted for 44.8% of the U.S. food retail market share in 2025. This dominance is attributed to convenience, longer shelf life, and strong consumer demand across households.

- Based on sales channel, the supermarkets and hypermarkets segment held 51.5% of the U.S. food retail market share in 2025, supported by extensive product assortments, competitive pricing, and broad geographic presence.

Regional Insights

- The United States accounted for 81.3% of the North American food retail market share in 2025 and maintained its dominant regional position. Strong consumer purchasing power, advanced retail infrastructure, and widespread adoption of modern retail formats continue to support market growth.

Competitive Landscape

The U.S. food retail market is highly competitive, with retailers focusing on digital transformation, supply chain optimization, private label expansion, and customer experience enhancement to strengthen their market position. Companies continue to invest in e commerce capabilities, automated logistics, and omnichannel retail strategies. Prominent players in the U.S. food retail market include Walmart, Amazon, Costco Wholesale, Carrefour S.A., The Schwarz Group, Kroger, Aldi, Tesco, Seven & I Holdings, Target, Ahold Delhaize, and Reliance Retail.

U.S. Food Retail Market Size

The U.S. food retail market size was valued at USD 180.52 billion in 2025, and is projected to reach USD 297.56 billion by 2034 from USD 190.83 billion in 2026, growing at a CAGR of 5.71%.

Food retail is the business sector responsible for selling food and grocery products directly to consumers for personal or household consumption. This market serves as a critical component of the national economy reflecting shifting consumer preferences technological advancements and supply chain dynamics. The landscape is characterized by intense competition among traditional supermarkets convenience stores warehouse clubs and rapidly expanding e commerce giants. According to the USDA Economic Research Service, household spending on food accounted for 11.2% of total disposable personal income in 2023, remaining near historical highs and reflecting the significant financial commitment Americans continue to make toward nutrition. As per the Bureau of Labor Statistics, the Consumer Price Index for food at home saw an annual average increase of 5.0% in 2023, with inflation cooling significantly from a peak of 11.3% in 2022 to just 1.3% by December 2023. The proliferation of digital channels has transformed shopping habits with omnichannel strategies becoming essential for retailer survival. Consumers increasingly prioritize convenience health and sustainability influencing product assortments and store formats. The integration of artificial intelligence and data analytics enables retailers to personalize offerings and optimize inventory management. Furthermore the rise of private label brands offers cost effective alternatives amid economic uncertainty. Regulatory frameworks regarding food safety labeling and nutritional standards also shape market operations. The convergence of technology and traditional retail creates a dynamic environment where adaptability and customer centricity determine success. This evolving sector continues to respond to demographic changes and lifestyle trends ensuring its relevance in the daily lives of American households.

MARKET DRIVERS

Rising Consumer Preference for Health and Wellness Products

The growing emphasis on health and wellness significantly drives the US food retail market. As a result, consumers are increasingly seeking out nutritious, organic, and functional food options. This shift is fueled by heightened awareness of the link between diet and chronic disease prevention leading to higher demand for fresh produce whole grains and plant based proteins. According to the International Food Information Council (IFIC), 52% of Americans followed a specific eating pattern or diet in 2023, with high-protein regimens and mindful eating ranking as the most popular choices. As per the Centers for Disease Control and Prevention (CDC), adult obesity rates in the United States reached historical highs of nearly 42% over the last decade, reinforcing ongoing public health initiatives aimed at improving dietary habits and nutrition access. Retailers respond by expanding their organic sections and introducing private label health focused lines that cater to diverse dietary needs such as gluten free keto and vegan preferences. The millennial and Gen Z demographics particularly influence this trend as they are more likely to research ingredient sourcing and nutritional benefits before purchasing. Supermarkets are redesigning store layouts to highlight fresh and perimeter departments which typically house healthier options compared to center aisles. Additionally the incorporation of wellness centers and nutritionist consultations within stores enhances the shopping experience and builds customer loyalty. The demand for transparency in supply chains further encourages retailers to partner with local farmers and sustainable producers. This holistic approach to health not only attracts conscious consumers but also differentiates retailers in a crowded marketplace. Therefore, the alignment of product offerings with wellness trends remains a powerful driver of growth and innovation in the food retail market.

Expansion of E Commerce and Omnichannel Shopping Convenience

The rapid expansion of e commerce and the adoption of omnichannel shopping models accelerates the growth of the US food retail market. This offers unparalleled convenience and accessibility. Consumers increasingly prefer the flexibility of ordering groceries online for home delivery or curbside pickup saving time and reducing physical store visits. According to data from the U.S. Census Bureau and market tracking indicators, e-commerce sales within the food and beverage retail sector have maintained a elevated plateau well above pre-pandemic baselines, reflecting permanent digital adoption by modern consumers. Retailers invest heavily in robust digital platforms mobile applications and last mile logistics to meet these expectations. The use of advanced algorithms for personalized recommendations and dynamic pricing enhances user engagement and increases basket size. Furthermore the integration of smart technologies such as automated replenishment and voice assisted shopping simplifies the purchasing process for busy households. The ability to access a wider variety of products including niche and international items online expands consumer choice beyond local store limitations. Retailers also leverage data from online interactions to optimize inventory and reduce waste. The convenience factor is particularly appealing to working professionals and families who value efficiency. Digital infrastructure improvements and growing consumer comfort with online transactions are driving market expansion. Consequently, the e-commerce segment is reshaping competitive dynamics in the food retail market.

MARKET RESTRAINTS

Persistent Inflation and Economic Pressure on Household Budgets

Persistent inflation and economic pressure on household budgets are major restraints to the US food retail market. This alters consumer spending patterns and reduces discretionary income. Rising prices for essential goods force shoppers to prioritize affordability over brand loyalty or premium features leading to increased price sensitivity. According to the Bureau of Labor Statistics (BLS), the annual average Consumer Price Index for food at home rose by 5.0% in 2023, reflecting cooling yet persistent inflationary pressures on household grocery budgets throughout the year. As per the Federal Reserve Bank of New York, total household debt and nominal credit card balances climbed to historic highs in 2023, with credit card balances surpassing the $1 trillion threshold by the second half of the year. This financial strain prompts consumers to trade down from national brands to private labels or discount retailers seeking better value. Promotional activities and discounts become critical tools for retailers to attract budget conscious shoppers but often compress profit margins. The uncertainty surrounding economic stability leads to cautious spending behavior with households reducing frequency of purchases or opting for smaller pack sizes. Additionally the rising cost of labor and utilities further squeezes retailer profitability limiting their ability to invest in expansions or innovations. Small and independent grocers face particular challenges in competing with large chains that can leverage economies of scale to offer lower prices. The cumulative effect of these economic pressures restricts market growth and forces retailers to adopt defensive strategies focused on cost containment and value proposition. Thus, the financial burden on consumers remains a formidable restraint on the overall vitality and expansion of the food retail sector.

Supply Chain Disruptions and Logistics Complexities

Supply chain disruptions and logistics complexities are major constraints to the US food retail market. This causes inventory shortages, price volatility, and operational inefficiencies. The intricate global nature of food sourcing makes the sector vulnerable to external shocks such as geopolitical tensions natural disasters and transportation bottlenecks. According to data and industry tracking from the American Trucking Associations (ATA), the structural long-haul truck driver shortage remains a persistent long-term bottleneck for domestic supply chains and retail distribution networks. According to the United States Department of Agriculture (USDA), severe weather events, including localized flooding and prolonged regional droughts, disrupted domestic crop yields, introducing heightened price volatility into primary agricultural commodity markets. These disruptions force retailers to deal with inconsistent stock levels which can erode consumer trust and lead to lost sales. The need for cold chain integrity adds another layer of complexity and cost particularly for fresh and frozen products. Retailers must invest in advanced tracking systems and diversified supplier networks to mitigate risks but these measures require significant capital expenditure. Labor shortages in warehouses and distribution centers further exacerbate logistical challenges delaying order fulfillment and increasing operational costs. The unpredictability of supply conditions makes it difficult for retailers to plan inventory accurately leading to either excess waste or stockouts. Additionally regulatory changes regarding imports and safety standards can introduce delays and compliance burdens. These logistical hurdles constrain the ability of retailers to maintain consistent product availability and competitive pricing thereby restraining market stability and growth potential in the face of ongoing global uncertainties.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Personalized Shopping Experiences

The integration of artificial intelligence and personalized shopping experiences offers a significant opportunity for the US food retail market. This trend helps to enhance customer engagement and operational efficiency. AI technologies enable retailers to analyze vast amounts of consumer data to predict preferences optimize inventory and tailor marketing messages. According to McKinsey & Company, implementing comprehensive omnichannel personalization strategies can drive a 10% to 15% revenue lift for retail brands by fostering deeper customer loyalty and relevant interactions. As per research highlighted by the National Retail Federation (NRF), artificial intelligence and automation have emerged as top strategic priorities for retail executives seeking to optimize operational efficiency and enhance the customer experience. Retailers utilize machine learning algorithms to forecast demand accurately reducing waste and ensuring popular items are always in stock. Dynamic pricing models powered by AI allow for real time adjustments based on demand expiration dates and competitor activity maximizing revenue. Virtual assistants and chatbots provide instant customer support enhancing satisfaction and resolving issues quickly. The use of computer vision in stores enables cashier less checkout experiences reducing wait times and improving convenience. Personalized loyalty programs driven by data insights foster deeper connections with customers by offering rewards aligned with their purchasing habits. Additionally AI helps in optimizing supply chain routes and warehouse operations leading to cost savings and faster delivery times. The ability to create hyper personalized shopping journeys differentiates retailers in a competitive landscape. By leveraging AI companies can transform raw data into actionable insights driving growth and innovation. This technological advancement offers a pathway to smarter more responsive retail environments that meet the evolving expectations of modern consumers.

Growth of Private Label Brands and Value Oriented Offerings

The growth of private label brands and value-oriented offerings provides a lucrative prospect for the US food retail market. This shift occurs as consumers actively seek high-quality yet affordable alternatives to national brands. Retailers are investing heavily in developing premium private label lines that compete directly with established brands in terms of taste packaging and nutritional value. According to data from the Private Label Manufacturers Association (PLMA), historical perceptions have shifted dramatically, with a vast majority of US shoppers now viewing store brands as equal or superior in quality to name brands. This shift allows retailers to improve profit margins since private labels eliminate intermediary costs and branding expenses. Stores are expanding their private label portfolios to include organic gluten free and specialty items catering to diverse dietary preferences. The exclusivity of these products drives customer loyalty as shoppers return to specific retailers for unique offerings. Marketing campaigns emphasizing transparency and sourcing stories help build trust and appeal to conscious consumers. Additionally private labels provide retailers with greater control over pricing and supply chain resilience during periods of inflation. The ability to quickly adapt private label formulations to emerging trends offers a competitive advantage over slower moving national brands. By positioning private labels as premium yet affordable options retailers can attract a broader demographic including budget conscious and quality focused shoppers. This strategic focus on own brand development strengthens market position and drives sustainable revenue growth.

MARKET CHALLENGES

Intensifying Competition from Discount Retailers and Non Traditional Players

Intensifying competition from discount retailers and non traditional players is an impediment to the US food retail market. Traditional supermarkets face increasing threats from hard discounters warehouse clubs and online giants that offer lower prices and greater convenience. Warehouse clubs like Costco and Sam s Club appeal to bulk buyers offering significant savings on staple items which draws traffic away from conventional grocers. The entry of dollar stores into the fresh food segment further fragments the market providing accessible options for low income households. Traditional retailers struggle to match the pricing power of these competitors without sacrificing profitability. The need to invest in digital infrastructure and delivery capabilities adds to operational costs making it difficult to compete on price alone. Brand differentiation becomes challenging as product assortments overlap significantly across formats. Customer loyalty is increasingly transient with shoppers willing to switch retailers based on immediate deals and convenience. This fragmented competitive landscape requires traditional grocers to constantly innovate and optimize operations to retain relevance. The pressure to lower prices while maintaining service quality creates a delicate balancing act. So, the rise of alternative retail formats challenges the dominance of traditional supermarkets and necessitates strategic adaptation to survive in a hyper competitive environment.

Labor Shortages and Rising Workforce Costs

Labor shortages and rising workforce costs are a serious challenge to the US food retail market. This impacts operational efficiency and service quality. The industry relies heavily on human labor for stocking customer service and checkout operations but faces difficulties in attracting and retaining employees. According to the Bureau of Labor Statistics (BLS), the leisure and hospitality sector, which includes food services, maintained an elevated monthly quit rate averaging over 4% in 2023, reflecting highly competitive labor market conditions and frequent job switching. As per the National Grocers Association (NGA), recruiting and retaining qualified personnel remains a critical operational challenge for independent grocers, requiring businesses to adapt their store operations to navigate labor constraints. To attract workers retailers are forced to increase wages and offer enhanced benefits which raises operational expenses and compresses margins. The tight labor market also limits the ability of stores to expand hours or introduce new services that require additional personnel. Training new employees is time consuming and costly further straining resources. High turnover rates disrupt team cohesion and consistency in customer service affecting shopper satisfaction. Automation offers a potential solution but requires significant upfront investment and may face resistance from workers and unions. The reliance on temporary or part time staff can lead to inconsistencies in store presentation and inventory management. Additionally regulatory changes regarding minimum wage and labor rights add complexity to workforce management. These labor related challenges hinder the ability of retailers to operate efficiently and deliver a seamless shopping experience. Consequently addressing workforce issues remains a critical hurdle for sustaining growth and profitability in the US food retail sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.71% |

| Segments Covered | By Product Type, Sales Channel and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Walmart, Amazon, Costco Wholesale, Carrefour S.A., The Schwarz Group, Kroger, Aldi, Carrefour, Tesco, Seven & I Holdings, Target, Ahold Delhaize, and Reliance Retail. |

SEGMENTAL ANALYSIS

By Product Type Insights

The packaged and processed food segment dominated the US food retail market and accounted for a 44.8% share in 2025. This dominance of the segment was driven by consumer demand for convenience shelf stability and affordability. Moreover, this segment includes ready to eat meals canned goods snacks and frozen foods which align with the fast paced lifestyles of American households. According to the USDA Economic Research Service, expenditures on processed and packaged foods account for the clear majority of total food-at-home spending, representing a foundational component of modern household grocery budgets. As per FMI – The Food Industry Association, center-store packaged items and convenient meal solutions remain major revenue drivers for grocery retailers, highly valued by consumers for their convenience and shelf stability. The prevalence of dual income families has reduced the time available for cooking from scratch leading to increased reliance on pre prepared and semi prepared options. Manufacturers continuously innovate with new flavors and health conscious formulations such as low sodium or high protein variants to retain consumer interest. The extensive distribution networks of major brands ensure widespread availability across all retail channels from supermarkets to convenience stores. Additionally the cost effectiveness of mass produced packaged goods makes them attractive during periods of economic uncertainty when consumers seek value. The ability of these products to withstand supply chain disruptions better than fresh produce further solidifies their market leadership. Retailers prioritize shelf space for high turnover packaged items which generate consistent revenue streams. The cultural acceptance of convenience foods across diverse demographic groups ensures sustained demand. Consequently the packaged and processed food segment remains the cornerstone of the US food retail landscape due to its alignment with modern lifestyle constraints and economic realities.

However, the organic and health foods segment is anticipated to witness the fastest CAGR of 8.3% between 2026 and 2034 due to increasing health consciousness and environmental awareness among consumers. This segment includes organic produce gluten free products plant based alternatives and functional foods fortified with vitamins and minerals. According to the Organic Trade Association (OTA), sales of organic food in the United States reached a record $63.8 billion in 2023, representing a growth rate of 3.4% over the previous year despite persistent inflationary headwinds. The millennial and Gen Z demographics are particularly influential in this trend as they prioritize sustainability and ethical sourcing in their purchasing decisions. Retailers are expanding their organic offerings to include private label options which provide lower price points and increase accessibility. The rise of chronic health conditions such as diabetes and heart disease has also prompted consumers to adopt healthier eating habits supported by medical recommendations. Government initiatives promoting organic farming and clear labeling standards further boost consumer confidence in these products. Innovation in plant based proteins and dairy alternatives attracts flexitarians and vegans expanding the customer base beyond traditional organic shoppers. The integration of online platforms allows niche health brands to reach wider audiences effectively. As transparency in supply chains becomes a competitive advantage the organic and health food segment continues to outpace conventional categories in growth potential.

By Sales Channel Insights

The supermarkets and hypermarkets segment maintained the lead in the US food retail market and captured a 51.5% share in 2025. This leading position of the segment was attributed to its comprehensive product assortments one stop shopping convenience and established consumer trust. These large format stores offer a wide variety of fresh produce packaged goods household items and often pharmacy services under one roof. The ability of these retailers to leverage economies of scale allows them to offer competitive pricing and frequent promotions that attract budget conscious shoppers. Investments in store remodels and enhanced fresh departments have improved the shopping experience making supermarkets destinations for quality and variety. The integration of digital tools such as mobile apps for loyalty programs and digital coupons enhances customer engagement and retention. Supermarkets also serve as key pickup and delivery hubs for online grocery orders bridging the gap between physical and digital retail. Their strong relationships with suppliers ensure consistent stock levels and exclusive product launches. The familiarity and reliability of supermarket brands foster long term loyalty among diverse demographic groups. Despite competition from discounters and e commerce giants supermarkets remain the primary channel for weekly grocery shopping due to their unmatched combination of selection service and convenience.

On the other hand, the discount and wholesale stores segment is estimated to register the fastest CAGR of 5.2% over the forecast period. This quick surge of the segment is propelled by inflationary pressures and the consumer shift toward value oriented shopping. Formats such as warehouse clubs and hard discounters offer significant savings through bulk purchasing limited assortments and efficient operational models. The rising cost of living has prompted middle and upper income households to adopt trade down behaviors seeking lower prices without compromising significantly on quality. Discount retailers like Aldi and Lidl have expanded their footprint aggressively introducing fresh produce and private label goods that challenge traditional supermarkets on price. The psychological appeal of finding deals and the tangible savings from bulk buying resonate strongly with financially constrained consumers. These stores also benefit from lower overhead costs due to simplified store layouts and minimal staffing requirements. The expansion of private label brands within these channels offers higher margins for retailers and lower prices for shoppers. The value proposition of discount and wholesale stores continues to attract a broader customer base as economic uncertainty persists. Consequently, these stores are driving rapid expansion and market share gains in the competitive food retail market.

COUNTRY LEVEL ANALYSIS

The United States was the top performer in the North American food retail market and accounted for a 81.3% share in 2025. This expansion of the US market was driven by its massive population high disposable income and advanced retail infrastructure. The market status is characterized by intense competition among diverse formats including traditional supermarkets e commerce platforms and discount chains. Moreover, the widespread adoption of digital technologies has transformed shopping behaviors with online grocery sales continuing to grow as consumers prioritize convenience. The presence of major global retailers such as Walmart Kroger and Amazon ensures a dynamic and innovative market environment. Supply chain resilience and logistical efficiency are critical factors enabling retailers to maintain product availability across vast geographic areas. Consumer preferences for health sustainability and convenience drive product innovation and store format evolution. Regulatory frameworks regarding food safety and labeling influence operational standards and consumer trust. The diversity of the US population creates varied demand patterns requiring retailers to customize offerings for different demographic segments. Economic fluctuations and inflation rates directly impact purchasing power and shopping habits necessitating agile strategic responses from market participants. The United States remains the primary engine of growth and innovation in the continental food retail industry setting trends that influence global markets.

COMPETITIVE LANDSCAPE

The competition in the US food retail market is intense and characterized by a mix of traditional supermarkets discount chains warehouse clubs and e commerce giants. Major players compete on price convenience product quality and technological innovation to capture consumer spending. Traditional grocers face pressure from discount retailers like Aldi and Lidl which offer lower prices through efficient operational models. Warehouse clubs such as Costco attract bulk buyers with membership based value propositions. E commerce leaders like Amazon leverage technology and logistics to dominate online grocery sales. The rise of private labels allows retailers to differentiate offerings and improve margins while competing with national brands. Consumer loyalty is increasingly fragmented as shoppers prioritize value and convenience over brand allegiance. Retailers invest heavily in digital platforms and delivery infrastructure to meet expectations for speed and ease. Supply chain efficiency and sustainability practices also serve as key differentiators. The market sees frequent mergers and acquisitions as companies seek scale and diversification. Price wars and promotional activities are common tactics to drive foot traffic. Ultimately success depends on the ability to adapt to shifting demographics economic pressures and technological advancements while delivering consistent value and superior customer experiences in a highly dynamic environment.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. food retail market are

- Walmart

- Amazon

- Costco Wholesale

- Carrefour S.A.

- The Schwarz Group

- Kroger

- Aldi

- Carrefour

- Tesco

- Seven & I Holdings

- Target

- Ahold Delhaize

- Reliance Retail

Top Players in the Market

- Walmart Inc remains a dominant force in the US food retail sector by leveraging its extensive network of supercenters and robust supply chain infrastructure. The company focuses on offering everyday low prices which attracts budget conscious consumers across diverse income levels. Recent actions include significant investments in automated fulfillment centers to enhance online grocery pickup and delivery capabilities. Walmart has also expanded its private label offerings such as Great Value to provide high quality affordable alternatives to national brands. The integration of digital tools like the Walmart app allows for seamless shopping experiences and personalized promotions. By prioritizing sustainability initiatives and local sourcing programs the company strengthens community ties and brand loyalty. These strategic moves ensure Walmart maintains its competitive edge through operational efficiency and customer centric innovation in the evolving retail landscape.

- The Kroger Co operates as a leading traditional supermarket chain in the United States known for its strong presence in multiple states and diverse store formats. The company emphasizes fresh produce quality and customer service to differentiate itself from discount competitors. Recent efforts involve advancing its digital ecosystem through the Kroger Boost membership program which offers exclusive benefits and fuel points. Kroger has invested heavily in data analytics via its subsidiary to personalize marketing and optimize inventory management. The retailer is also expanding its prepared meal sections and ready to eat options to cater to busy lifestyles. Partnerships with third party delivery services enhance accessibility for online shoppers. Kroger focuses on health, wellness trends, and sustainable sourcing practices. As a result, the company reinforces its position as a trusted provider of quality groceries and household essentials for American families.

- Amazon.com Inc has transformed the US food retail market through its acquisition of Whole Foods Market and the launch of Amazon Fresh stores. The company leverages its advanced logistics network and technology platform to offer convenient grocery delivery and pickup services. Recent actions include the expansion of cashier less Just Walk Out technology in select locations to streamline the shopping experience. Amazon integrates its Prime membership benefits with grocery purchases providing discounts and free delivery to subscribers. The retailer uses artificial intelligence to predict demand and optimize supply chain efficiency reducing waste and improving product availability. By combining online convenience with physical store presence Amazon creates an omnichannel ecosystem that appeals to tech savvy consumers. Continuous innovation in automation and data driven personalization strengthens its competitive position and drives growth in the digital grocery segment.

Top Strategies Used by Key Market Participants

Key players in the US food retail market employ diverse strategies to maintain competitiveness and drive growth. Expansion of private label brands is a primary tactic allowing retailers to offer lower prices while improving profit margins. Investment in digital transformation including mobile apps and online ordering platforms enhances customer convenience and engagement. Omnichannel integration enables seamless transitions between online and offline shopping experiences through curbside pickup and home delivery services. Data analytics are utilized to personalize marketing efforts and optimize inventory management reducing waste and improving efficiency. Strategic partnerships with third party delivery providers expand reach and accessibility for customers. Sustainability initiatives such as reducing plastic packaging and sourcing locally resonate with environmentally conscious consumers. Loyalty programs incentivize repeat purchases and provide valuable consumer insights. Automation technologies like self checkout kiosks and robotic warehouse systems reduce labor costs and improve operational speed. These multifaceted approaches help retailers adapt to changing consumer preferences and economic conditions while sustaining long term profitability and market relevance.

MARKET SEGMENTATION

This research report on the U.S. food retail market is segmented and sub-segmented into the following categories.

By Product Type

- Fresh Food

- Packaged / Processed Food

- Organic & Health Foods

By Sales Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Discount / Wholesale Stores

- Specialty Stores

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1. What is the U.S. food retail market?

The U.S. food retail market comprises businesses that sell food and beverage products directly to consumers through supermarkets, hypermarkets, convenience stores, specialty stores, discount retailers, and online grocery platforms.

2. What factors are driving the growth of the U.S. food retail market?

Growth is driven by population expansion, changing consumer preferences, increasing demand for convenience, rising online grocery shopping, and growing interest in healthy and organic food products.

3. Which product segment holds a significant share of the U.S. food retail market?

Fresh food products, including fruits, vegetables, dairy, meat, and seafood, account for a substantial share of the market due to consistent consumer demand.

4. Why are organic and health foods gaining popularity in the United States?

Consumers are becoming more health conscious and are increasingly seeking natural, organic, and minimally processed food products that support healthier lifestyles.

5. What role do supermarkets and hypermarkets play in the market?

Supermarkets and hypermarkets remain the dominant sales channel by offering a wide variety of food products, competitive pricing, and convenient one stop shopping experiences.

6. How is e commerce transforming the U.S. food retail market?

Online grocery platforms, home delivery services, and click and collect options are improving convenience and expanding consumer access to food products.

7. What impact does technology have on food retail operations?

Technologies such as artificial intelligence, self checkout systems, digital payment solutions, inventory management software, and data analytics help retailers improve efficiency and customer experience.

8. What challenges does the U.S. food retail market face?

Key challenges include inflationary pressures, supply chain disruptions, labor shortages, changing consumer preferences, and intense competition among retailers.

9. Why are convenience stores important in the food retail market?

Convenience stores provide quick access to essential food and beverage products, making them a popular option for consumers seeking fast and accessible purchases.

10. What is the future outlook for the U.S. food retail market?

The market is expected to grow steadily due to increasing consumer spending on food, expansion of digital retail channels, rising demand for healthy food options, and ongoing innovations in retail technology.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com