U.S. Gin Market Size, Share, Trends, and Growth Analysis Report, Segmented by Product Type, End User, Category, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

U.S. Gin Market Report Summary

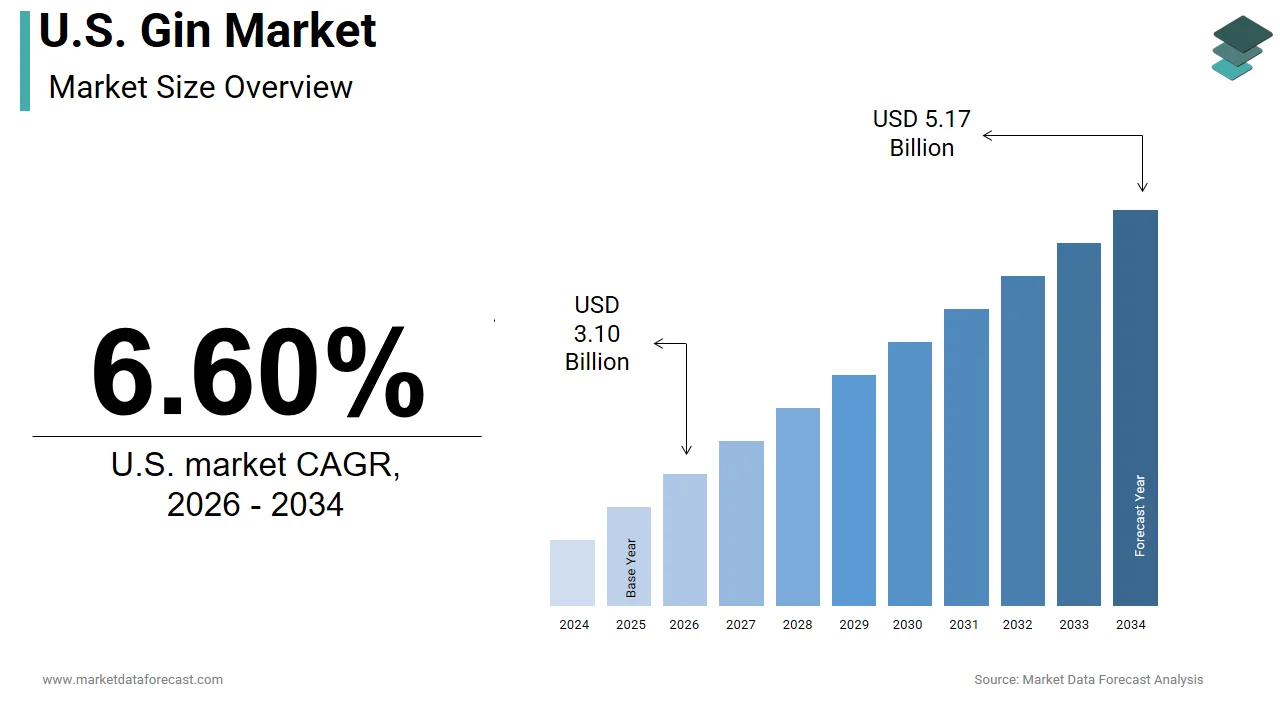

The U.S. gin market was valued at USD 2.91 billion in 2025, is estimated to reach USD 3.10 billion in 2026, and is projected to reach USD 5.17 billion by 2034, growing at a CAGR of 6.60% from 2026 to 2034. Market growth is driven by rising consumer interest in premium spirits, expanding cocktail culture, and increasing demand for craft alcoholic beverages. Consumers are increasingly exploring flavored and artisanal gin varieties, supported by the popularity of mixology and premium on-premise experiences. Additionally, the growth of e-commerce alcohol sales and innovative product launches are further contributing to the expansion of the U.S. gin market.

Key Market Trends

- Rising demand for premium and craft gin products.

- Increasing popularity of cocktail culture and mixology.

- Growth in flavored and botanical-infused gin variants.

- Expansion of off-trade and e-commerce alcohol sales channels.

- Increasing consumer preference for artisanal and small-batch spirits.

Segmental Insights

- Based on product type, the London dry gin segment dominated the United States gin market by capturing 39.8% share in 2025, driven by its classic flavor profile and widespread consumer preference.

- Based on end user, the men segment held the majority share in 2025, supported by higher consumption trends among male consumers.

- Based on distribution channel, the off-trade channel segment led the market with 57.4% share in 2025, driven by strong retail and online sales of alcoholic beverages.

Country-Level Insights

- The United States dominated the North American gin market by holding 78.5% share in 2025, supported by strong consumer spending, expanding premium spirits consumption, and a well-established alcoholic beverage industry.

Competitive Landscape

The U.S. gin market is highly competitive, with companies focusing on premiumization, flavor innovation, and expansion of distribution networks. Strategic marketing campaigns, craft spirit launches, and partnerships with bars and restaurants are shaping the competitive landscape.

Prominent companies operating in the U.S. gin market include Diageo plc, Bacardi Limited, Pernod Ricard SA, William Grant & Sons Ltd, and Davide Campari-Milano N.V.

U.S. Gin Market Size

The U.S. gin market was valued at USD 2.91 billion in 2025, is estimated to reach USD 3.10 billion in 2026, and is projected to reach USD 5.17 billion by 2034, growing at a CAGR of 6.60% from 2026 to 2034.

Gin is defined as a distilled alcoholic beverage that derives its predominant flavour from juniper berries and often includes a complex array of botanicals such as coriander citrus peel and angelica root. This category has transcended its traditional associations to become a canvas for culinary innovation appealing to consumers who value artisanal production methods and unique flavor profiles. The cultural resurgence of cocktail culture in the US has played a pivotal role in this transformation with bars and restaurants increasingly featuring gin based mixtures on their menus. According to the 2025 Craft Spirits Data Project (by ACSA and Park Street), the number of active craft distilleries in the U.S. has declined (reporting a drop to approximately 2,282 active producers) due to economic pressures, though many remaining producers continue to innovate in categories like small-batch gin and whiskey. This proliferation reflects a consumer preference for locally sourced ingredients and transparent supply chains. Furthermore, data from the Bureau of Labor Statistics confirms that household spending on alcoholic beverages has fluctuated, while market observers and research attribute resilient at-home consumption to consumers seeking to replicate bar-quality experiences in domestic settings. The demographic profile of gin drinkers is also shifting with younger adults showing a marked interest in low alcohol and non alcoholic alternatives that retain the botanical complexity of traditional gin. As per various sources, while overall alcohol consumption patterns fluctuate, the demand for premium spirits remains robust, driven by a desire for sophistication and variety. Meanwhile, the National Institute on Alcohol Abuse and Alcoholism (NIAAA) continues to track these consumption patterns strictly for their public health and epidemiological impact.

MARKET DRIVERS

Resurgence of Craft Cocktail Culture and Mixology Trends

The revitalization of craft cocktail culture is contributing to the growth of the United States gin market. This growth is spurred by consumers increasingly viewing gin as a versatile base for sophisticated mixology. The rise of speakeasy style bars and dedicated cocktail lounges has educated patrons on the nuances of botanical profiles encouraging experimentation beyond standard brands. According to the National Restaurant Association's "What's Hot" forecasts, classic cocktails and simpler, nostalgic beverages (like the Espresso Martini) remain top trends. Broader industry data supports the resurgence of the Martini and Negroni, often driven by a move toward "minimalism," but the NRA specifically highlights the "Espresso Martini" and "Spritz" in recent top rankings. This cultural shift is supported by the proliferation of bartending competitions and educational programs that highlight the artistry involved in gin preparation. Data from the Specialty Food Association indicates that consumers are willing to pay a premium for artisanal spirits that offer unique taste experiences and storytelling elements. The visual appeal of gin cocktails often enhanced by garnishes and specialized glassware further drives social media engagement creating a viral marketing effect that boosts demand. Additionally the flexibility of gin allows it to pair well with a wide range of mixers from tonic water to fresh fruit juices appealing to diverse palates. As per the United States Bartenders' Guild (USBG) [or International Bartenders Association], the number of skilled mixologists has grown, ensuring a steady supply of professionals to innovate and promote spirit-based creations. This professional endorsement validates the quality of craft gins and encourages consumers to explore higher priced options thereby driving market growth through elevated perceived value and cultural relevance.

Growing Consumer Preference for Premium and Artisanal Products

The increasing consumer preference for premium and artisanal products is a significant driver propelling the United States gin market forward. Shoppers are increasingly prioritizing quality over quantity in their alcoholic beverage choices. This trend is part of a broader movement toward mindful consumption where individuals seek out spirits with distinct characteristics and ethical production standards. According to the Distilled Spirits Council of the United States premium and super premium spirits categories have consistently outpaced value segments in terms of volume and revenue growth. Consumers are drawn to small batch gins that feature locally sourced botanicals and innovative distillation techniques such as vacuum distillation or barrel aging. The transparency of ingredient sourcing and the narrative behind each brand resonate with millennials and Gen Z buyers who value authenticity and sustainability. Furthermore the willingness to experiment with new flavors such as floral herbal or spicy notes encourages brands to continuously innovate their portfolios. As per the Specialty Food Association artisanal food and beverage products are perceived as higher quality and more trustworthy by consumers who are skeptical of mass produced items. This perception drives loyalty and repeat purchases as customers develop preferences for specific botanical profiles. The emphasis on craftsmanship and exclusivity allows premium gin brands to command higher price points thereby enhancing profitability and sustaining market expansion despite broader economic uncertainties.

MARKET RESTRAINTS

Regulatory Constraints and Complex Compliance Requirements

Stringent regulatory constraints and complex compliance requirements are hampering the growth of the United States gin market. These hurdles are particularly challenging for small and medium-sized distillers. The alcohol industry is heavily regulated at both federal and state levels with agencies such as the Alcohol and Tobacco Tax and Trade Bureau enforcing strict rules on production labeling and distribution. The U.S. Small Business Administration (SBA) notes that small firms bear a disproportionate regulatory compliance burden, often requiring significant administrative resources that can challenge the entry and growth of emerging brands. The three tier distribution system mandated in many states requires producers to sell to distributors who then sell to retailers creating barriers to direct market access. This structure limits the ability of small distillers to build direct relationships with consumers and capture full retail margins. Data from the American Craft Spirits Association indicates that regulatory compliance costs can account for a significant portion of operating expenses for small businesses reducing their competitiveness against larger established corporations. Additionally varying state laws regarding direct to consumer shipping and tasting room operations create a fragmented market landscape that complicates national expansion efforts. As per the Alcohol and Tobacco Tax and Trade Bureau (TTB), changes in tax codes or labeling guidelines require constant monitoring, adding to the operational burden for spirits producers. These regulatory hurdles slow down product launches and increase time to market discouraging innovation and limiting the diversity of offerings available to consumers. The complexity of the legal framework thus acts as a brake on market dynamism particularly for new entrants seeking to establish a foothold.

Health Consciousness and Moderation Trends

Growing health consciousness and trends toward moderation are hindering the expansion of the United States gin market. This is because consumers are increasingly scrutinizing the health impacts of alcohol consumption. Public health campaigns and dietary guidelines have emphasized the risks associated with excessive alcohol intake leading many individuals to reduce their overall consumption. According to the Centers for Disease Control and Prevention excessive alcohol use is linked to numerous health issues including liver disease and cardiovascular problems prompting a shift toward healthier lifestyles. The rise of the sober curious movement has encouraged people to participate in dry January or limit their drinking days reducing the frequency of gin purchases. Data from the National Institute on Alcohol Abuse and Alcoholism reveals that while adult alcohol use remains prevalent, there has been a steady decline in underage drinking and an increase in abstention among younger demographics. This shift challenges traditional gin brands that rely on regular consumption patterns for revenue growth. Furthermore the calorie content of gin and its common mixers such as tonic water which often contains high amounts of sugar detracts from its appeal to health focused consumers. As per the International Food Information Council a majority of Americans are actively trying to limit their sugar and alcohol intake favoring functional beverages or non alcoholic alternatives. Although the market has responded with low alcohol options the perception of gin as an indulgent rather than a health promoting product limits its appeal in this growing segment. This cultural shift toward wellness thus constrains market expansion by reducing the total addressable audience for traditional alcoholic gin products.

MARKET OPPORTUNITIES

Expansion into Non Alcoholic and Low Alcohol Segments

The expansion into non-alcoholic and low-alcohol segments offers a major opportunity for the United States gin market. This shift allows manufacturers to adapt to changing consumer preferences for healthier alternatives. The development of alcohol free gin alternatives that retain the complex botanical flavors of traditional gin allows brands to capture the growing population of moderate drinkers and abstainers. According to the Distilled Spirits Council of the United States the non alcoholic spirits category has experienced significant growth driven by innovation in distillation and extraction technologies that preserve aromatic profiles without the ethanol content. Brands are launching sophisticated non alcoholic gins that can be enjoyed in classic cocktails offering a guilt free experience for health conscious consumers. The diversification allows gin producers to broaden their customer base and maintain relevance in a wellness oriented market. Furthermore the inclusion of functional ingredients such as adaptogens or vitamins in non alcoholic gins adds value and appeals to consumers seeking holistic benefits. As per the Specialty Food Association products that combine indulgence with health benefits are gaining traction among millennials and Gen Z shoppers. By embracing this trend gin manufacturers can mitigate the risks associated with declining alcohol consumption and unlock new revenue streams. The ability to offer inclusive options ensures that brands remain accessible to all consumers regardless of their drinking preferences thereby fostering long term loyalty and market resilience.

Innovation in Sustainable and Eco Friendly Production Practices

Innovation in sustainable and eco-friendly production practices provides a clear path for the expansion of the United States gin market. This approach allows brands to differentiate themselves and appeal to environmentally conscious consumers. Distilleries are increasingly adopting green manufacturing processes such as using renewable energy sources reducing water usage and implementing waste reduction strategies. Research indicates that businesses prioritizing sustainability enjoy enhanced brand reputation and loyalty, as 85% of global consumers have shifted purchasing habits toward more sustainable options. Gin producers are sourcing organic and locally grown botanicals supporting local agriculture and reducing carbon footprints associated with transportation. Data from the Specialty Food Association shows that consumers are willing to pay a premium for products that are certified organic or sustainably produced. Additionally the use of recyclable or biodegradable packaging materials addresses concerns about plastic waste and aligns with circular economy principles. Some distilleries are even repurposing spent botanicals into compost or other useful products further minimizing environmental impact. As per the Green Business Bureau sustainability initiatives can lead to operational efficiencies and cost savings in the long run making them financially viable as well as ethically sound. By championing eco friendly practices gin brands can attract a dedicated segment of consumers who prioritize ethical consumption. This strategic focus not only enhances brand image but also future proofs the business against increasingly stringent environmental regulations. The commitment to sustainability thus serves as a powerful driver for growth and differentiation in a competitive market landscape.

MARKET CHALLENGES

Intense Market Saturation and Brand Proliferation

Intense market saturation and brand proliferation are major hurdles for the U.S. gin market. The sheer number of available options creates noise and dilutes brand visibility. The low barrier to entry for craft distilling has led to an explosion of new gin brands each vying for shelf space and consumer attention. According to the American Craft Spirits Association the number of craft distilleries in the US has more than doubled in the past decade resulting in a crowded marketplace. This oversupply makes it difficult for individual brands to stand out and justify premium pricing without significant marketing investment. The fragmentation of consumer attention across numerous niche products reduces the effectiveness of traditional advertising and requires brands to invest heavily in digital marketing and experiential activations. As per the Small Business Administration small distillers often struggle to compete with the marketing budgets of large multinational corporations which can dominate retail displays and promotional activities. The lack of differentiation among many craft gins further exacerbates the challenge as consumers may perceive little difference between various botanical profiles. This saturation leads to price wars and margin compression threatening the viability of smaller players. Many new entrants lack clear unique selling propositions or strong brand narratives. Without these, they risk failure in this highly competitive environment.

Supply Chain Volatility and Ingredient Sourcing Issues

Supply chain volatility and ingredient sourcing issues are slowing down the expansion of the United States gin market. This affects production consistency and cost stability. Gin production relies on a variety of botanicals such as juniper berries coriander and citrus peels which are subject to agricultural fluctuations and climate change impacts. According to the US Department of Agriculture extreme weather events can disrupt crop yields leading to shortages and price spikes for key ingredients. For instance poor harvests of juniper berries in Europe have historically affected global supply chains forcing US distillers to seek alternative sources or pay higher prices. Data from the Bureau of Labor Statistics shows that input costs for food and beverage manufacturing have risen due to inflation and logistical bottlenecks squeezing profit margins for producers. The reliance on imported botanicals also exposes distillers to currency fluctuations and trade policy changes which can further destabilize costs. As per the National Association of Manufacturers supply chain disruptions have become more frequent and severe requiring companies to hold larger inventories or diversify suppliers. However finding high quality alternative sources for specific botanicals can be difficult as flavor profiles are critical to brand identity. This vulnerability to external shocks makes long term planning challenging and can lead to inconsistent product availability. The need to balance cost efficiency with quality assurance in a volatile supply environment remains a critical operational hurdle for gin manufacturers striving to maintain competitiveness and consumer trust.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Diageo plc, Bacardi Limited, Pernod Ricard SA, William Grant & Sons Ltd., Davide Campari-Milano NV, and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

In 2025, the London dry gin segment remained the largest by occupying a 39.8% share of the United States gin market. This prominence of the segment was supported by its status as the foundational spirit for iconic cocktails such as the Martini, Gin and Tonic, and Negroni. Also, this style is characterized by its juniper forward profile and lack of added sugar after distillation, making it versatile for mixology. According to the Distilled Spirits Council of the United States (DISCUS), while the resurgence of cocktail culture has driven premiumization and revenue growth for gin, overall category volumes have moderated, with a shift toward Super Premium brands which grew 187% since 2019. The familiarity of London Dry Gin among consumers reduces the barrier to entry for new gin drinkers who may be intimidated by more experimental botanical profiles. The consistency of flavor across major global brands ensures that consumers receive a predictable product regardless of where they purchase it. Furthermore, the widespread availability of London Dry Gin in various price points from value to super premium allows it to capture a broad demographic spectrum. According to analysis featured at the National Restaurant Association Show, gin remains a staple in bar inventories. However, craft and botanical-forward varieties are increasingly challenging London Dry for menu prominence as bartenders seek unique flavor profiles. This ubiquity ensures that London Dry Gin remains the default choice for both casual drinkers and connoisseurs, sustaining its market leadership through sheer volume and cultural entrenchment. The dominance of London Dry Gin is further reinforced by the strong brand heritage and consumer trust associated with established legacy brands. Many leading London Dry Gin producers have histories spanning centuries, creating a narrative of authenticity and quality that resonates with American consumers. According to various sources and reports from the Distilled Spirits Council, shoppers often prioritize legacy brands with established heritage when purchasing premium spirits for special occasions, as they associate these brands with consistent quality and social status. Major brands invest heavily in marketing campaigns that highlight their traditional distillation methods and historical significance, fostering deep emotional connections with customers. Data from IRI shows that top tier London Dry Gin brands maintain high loyalty rates, with repeat purchase frequencies exceeding those of newer craft entrants. The perception of London Dry Gin as the standard bearer for the category means that it serves as the benchmark against which other gin styles are measured. This positioning allows legacy brands to command premium pricing while maintaining substantial market share. As per the Beverage Information Group, the stability of London Dry Gin sales provides a reliable revenue stream for distributors and retailers, ensuring prominent shelf placement and promotional support. The combination of historical prestige and consistent quality assurance creates a formidable moat around the segment, making it difficult for alternative styles to displace its leading position in the overall market hierarchy.

On the other hand, the Other Product Types segment is likely to experience the fastest CAGR of 11.2% between 2026 and 2034 due to intense innovation in botanical profiles and flavor experimentation. Consumers, particularly millennials and Gen Z, are seeking unique and personalized drinking experiences that deviate from traditional juniper heavy profiles. According to the American Craft Spirits Association, the number of craft distilleries producing innovative gin variations has increased significantly, with many focusing on local ingredients such as citrus, herbs, and spices native to specific US regions. This localization strategy appeals to consumers interested in terroir and sustainability. The introduction of unconventional flavors such as lavender, cucumber, and grapefruit attracts younger demographics who prefer lighter and more aromatic spirits. The flexibility of craft production allows distillers to release limited edition batches, creating a sense of urgency and exclusivity that fuels demand. This continuous cycle of innovation ensures that the Other Product Types segment remains dynamic and responsive to evolving consumer tastes, driving its rapid expansion. The rapid growth of the Other Product Types segment is also fueled by its alignment with the broader trend of premiumization and experiential consumption in the spirits industry. Consumers are increasingly willing to pay higher prices for spirits that offer a story, unique packaging, or distinct production methods. Craft distillers often emphasize hand crafted processes, small batch distillation, and sustainable sourcing, which resonate with ethically conscious buyers. A study shows that premium and super premium priced gins within this segment have achieved higher profit margins and faster turnover rates compared to value oriented traditional brands. The experiential aspect extends to tasting rooms and distillery tours, which have become popular leisure activities. As per the US Travel Association, culinary tourism including visits to local distilleries has grown, providing craft gin producers with direct to consumer sales channels and brand advocacy. The ability of these brands to create immersive experiences around their products fosters strong community loyalty and word of mouth marketing. This strategic focus on quality, storytelling, and engagement allows the Other Product Types segment to capture value driven consumers who prioritize uniqueness over tradition, propelling its status as the fastest growing segment in the market.

By End User Insights

The men segment maintained the majority share of the United States gin market in 2025. This supremacy of the segment was attributed to traditional consumption patterns and strong brand loyalty established over decades. Historically, gin has been marketed toward male demographics through associations with classic masculinity and sophisticated cocktail culture. According to the National Institute on Alcohol Abuse and Alcoholism, men generally report higher frequencies of alcohol consumption than women, particularly in the spirits category. This behavioral trend translates into higher volume purchases of gin by male consumers who often view it as a staple for social gatherings and home entertaining. The preference for strong, juniper forward profiles typical of London Dry Gin aligns with traditional male taste preferences, reinforcing their dominance in this segment. The establishment of gin clubs and enthusiast groups predominantly attended by men further solidifies their role as key influencers in the market. This entrenched consumption behavior ensures that men remain the primary drivers of volume sales, maintaining the segment's leadership position through consistent and habitual purchasing habits. The leadership of the male segment is further supported by higher disposable income and greater willingness to purchase premium gin products. Men often occupy higher earning brackets in certain industries, allowing them to allocate more budget toward luxury spirits. According to the US Census Bureau, median earnings for men remain higher than for women in many sectors, influencing spending power on non essential goods such as premium alcohol. The tendency to collect rare or limited edition bottles also drives high value transactions within this demographic. Retailers and distributors tailor their inventory and promotions to appeal to this affluent buyer group, ensuring wide availability of high end products. The combination of financial capacity and interest in luxury goods enables men to sustain the market's revenue growth, particularly in the high value tiers. This economic influence ensures that the male segment remains central to the strategic focus of gin manufacturers aiming to maximize profitability and brand prestige.

However, the women segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 5.6% over the forecast period owing to a shifting preference toward lighter, floral, and fruit forward flavor profiles that differ from traditional juniper heavy gins. Modern gin formulations often incorporate botanicals such as rose, elderflower, and citrus, which appeal to female palates seeking refreshing and aromatic beverages. These products offer convenience and approachability, lowering the barrier to entry for those who may find straight spirits too intense. The aesthetic appeal of packaging and branding also plays a crucial role, with many new brands designing visually striking bottles that resonate with female consumers. This shift in taste preferences and product availability is expanding the female consumer base, making it the most dynamic growth engine in the market. The quick surge of the female segment is significantly accelerated by social media influence and lifestyle marketing strategies that position gin as a fashionable and social beverage. Platforms such as Instagram and TikTok feature extensively curated content showcasing gin cocktails in aesthetically pleasing settings, inspiring female users to try new brands and recipes. Brands leverage this by partnering with female influencers who promote gin as part of a sophisticated and enjoyable lifestyle. Data from IRI shows that products with strong social media presence experience higher sales spikes among female demographics compared to those relying on traditional advertising. The emphasis on mindfulness and moderate drinking also appeals to women who are leading the sober curious movement, opting for high quality non alcoholic or low alcohol gin alternatives. As per the International Wine and Spirit Record, the engagement levels of female consumers with digital content correlate strongly with purchase intent in the spirits category. This digital connectivity allows brands to build communities and foster loyalty among female drinkers, driving sustained growth and transforming women into a pivotal force in the evolving gin landscape.

By Distribution Channel Insights

The off-trade channel segment led the United States gin market by capturing a 57.4% share in 2025. This leading position of the segment was attributed to the convenience it offers and the rising trend of home consumption. Consumers increasingly prefer purchasing spirits for home use to save money and enjoy greater control over their drinking environment. The availability of a wide variety of gin brands in retail stores allows shoppers to compare prices and read labels at their own pace, enhancing the shopping experience. The expansion of craft sections in mainstream grocery stores has also made niche gin brands more accessible to the average consumer. As per the Distilled Spirits Council of the United States, the ease of purchasing gin alongside other grocery items encourages impulse buys and regular restocking. The ability to store gin for extended periods without spoilage further supports its popularity in the off trade channel. This convenience factor ensures that off trade remains the primary conduit for gin distribution, capturing the bulk of consumer demand through extensive retail networks and competitive pricing strategies. Competitive pricing and aggressive promotional activities in the Off-Trade channel significantly contribute to its market dominance. Retailers frequently offer discounts, bundle deals, and loyalty rewards that attract price sensitive consumers and drive volume sales. According to IRI, promotional events such as holiday sales and summer barbecues lead to substantial spikes in gin purchases through off trade outlets. The ability of large retail chains to negotiate lower wholesale prices allows them to pass savings on to customers, making gin more affordable than in on trade establishments. Data from the National Association of Convenience Stores shows that targeted promotions in liquor sections effectively increase basket size and frequency of visits. Online retailers further enhance this advantage by offering direct to consumer shipping and subscription services that provide additional savings and convenience. The combination of lower prices and attractive promotions creates a compelling value proposition that draws consumers away from bars and restaurants. This economic advantage ensures that the off trade channel maintains its leadership by maximizing accessibility and affordability for a broad consumer base.

The on-trade channel segment is expected to exhibit a noteworthy CAGR of 3.2% from 2026 to 2034. This swift expansion of the segment is fuelled by the revival of bar culture and the demand for authentic mixology experiences. Consumers are returning to social venues to enjoy professionally crafted cocktails that showcase the complexity of premium gin brands. According to the National Restaurant Association, on premise dining and drinking have rebounded strongly, with gin based cocktails featuring prominently on menus. The expertise of bartenders in creating unique and visually appealing drinks enhances the perceived value of gin, encouraging consumers to try new varieties. Data from the Distilled Spirits Council of the United States indicates that on trade sales of premium and super premium gins are growing at a faster rate than off trade, reflecting the willingness of patrons to pay for quality and service. The social aspect of drinking in bars fosters brand discovery and loyalty, as recommendations from staff and peers influence choices. This experiential demand drives rapid growth in the on trade channel, as consumers seek memorable social interactions centered around high quality spirits. The rapid growth of the On-Trade channel is further fueled by premiumization and the availability of exclusive gin offerings that are not accessible through retail stores. Bars and restaurants often secure limited edition releases and small batch craft gins that appeal to discerning drinkers seeking uniqueness. Establishments curate their gin lists to highlight rare botanicals and innovative production methods, attracting enthusiasts willing to pay a premium for these experiences. Research shows that average check sizes for gin cocktails in upscale venues have increased, reflecting the trend toward higher spending on quality beverages. The integration of gin tastings and pairing events also enhances customer engagement and education, fostering deeper appreciation for the spirit. This focus on exclusivity and elevated service positions the on trade channel as a key driver of growth, capturing the high value segment of the market through differentiated and immersive offerings.

COUNTRY ANALYSIS

U.S. Gin Market Analysis

The United States outperformed other countries in the North American gin market and accounted for a 78.5% share in 2025. This dominance of the U.S. market was driven by its large population and robust spirits culture. The market status is characterized by a mature yet evolving landscape where traditional brands coexist with a vibrant craft sector. The position of the US is underpinned by a strong regulatory framework and a well established distribution network that facilitates widespread availability. According to the Distilled Spirits Council of the United States (DISCUS), the gin category has seen significant revenue growth reaching $1 billion in 2024, though volumes have stabilized at approximately 8.3 million cases as the market transitions into a more mature, premium-focused phase. The cultural significance of cocktails in American society ensures a steady baseline demand for gin as a primary mixer. The presence of numerous craft distilleries across various states contributes to a diverse product ecosystem that caters to varied consumer preferences. As per the Alcohol and Tobacco Tax and Trade Bureau (TTB), the number of registered distilled spirits plants has quadrupled since 2010, reflecting the rapid expansion of the craft distilling movement and increased competition. The US market serves as a trendsetter for global gin consumption, influencing flavor profiles and marketing strategies worldwide. The resilience of the sector during economic fluctuations highlights its entrenched position in consumer lifestyles. With a strong emphasis on premiumization and experiential drinking, the United States continues to lead the region in both volume and value, setting the standard for market dynamics and consumer engagement in the gin category. The primary driving factor for the United States gin market is the convergence of premiumization trends and the resurgence of cocktail culture. Consumers are increasingly willing to invest in high quality spirits that offer unique flavor experiences and social prestige. According to the National Restaurant Association, the demand for craft cocktails has revitalized interest in gin, with bars reporting increased sales of premium and super premium brands. This shift is supported by data from NielsenIQ, which shows that value segments are stagnating while premium categories grow. The influence of social media also plays a crucial role, with platforms like Instagram driving visual appeal and brand discovery among younger demographics. As per research, consumers are highly active on visual platforms like Instagram and TikTok, which industry participants like Diageo utilize to drive discovery and trial among younger demographics. Additionally, the rise of health consciousness has led to the development of low alcohol and non alcoholic gin alternatives, expanding the total addressable market. The Distilled Spirits Council of the United States notes that these innovations are attracting new consumers who previously avoided traditional alcohol. The combination of cultural revival, digital influence, and product innovation creates a robust growth environment. The economic stability of the US consumer base further supports discretionary spending on premium spirits. These factors collectively ensure that the United States remains the central hub for gin consumption and innovation, driving sustained market expansion and setting global trends in the spirits industry.

COMPETITIVE LANDSCAPE

The competition in the United States gin market is intense and characterized by a mix of established multinational corporations and agile craft distilleries. Major players compete fiercely on brand heritage product quality and innovation to capture the attention of discerning consumers. The market sees continuous launches of flavored and contemporary gins as brands strive to differentiate themselves in a crowded landscape. Craft distillers have gained significant traction by offering unique local ingredients and transparent production stories forcing national brands to respond with their own artisanal lines. Innovation in packaging and sustainability has become a key battleground for differentiation as consumers increasingly prioritize ethical consumption. Supply chain efficiency and distribution reach are critical competitive advantages ensuring consistent availability and cost management. Marketing efforts focus heavily on digital engagement and experiential events to build emotional connections with shoppers. This dynamic environment drives constant evolution requiring companies to adapt quickly to changing consumer preferences and regulatory conditions to maintain their competitive edge and market relevance in the evolving spirits sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. gin market include

- Diageo plc

- Bacardi Limited

- Pernod Ricard SA

- William Grant & Sons Ltd

- Davide Campari-Milano NV

TOP PLAYERS IN THE MARKET

- Diageo North America maintains a dominant presence in the United States gin market through its iconic Tanqueray and Gordon s brands which are staples in bars and households alike. The company leverages its extensive distribution network to ensure widespread availability across all retail channels. Recent initiatives include launching limited edition flavors and sustainable packaging solutions to appeal to environmentally conscious consumers. Diageo invests heavily in digital marketing campaigns that highlight mixology trends and brand heritage. By partnering with top bartenders and hosting virtual tasting events the company strengthens consumer engagement and brand loyalty. These strategic actions reinforce its position as a leader in the premium spirits segment while adapting to evolving consumer preferences for quality and sustainability in their alcoholic beverage choices.

- Pernod Ricard USA contributes significantly to the market with its premium Beefeater and Monkey 47 brands which cater to discerning drinkers seeking unique botanical profiles. The company focuses on innovation by introducing craft inspired variations and collaborating with local distillers to create exclusive releases. Recent actions include expanding its portfolio with organic and low alcohol options to meet health conscious demand. Pernod Ricard emphasizes experiential marketing through sponsorships of culinary festivals and cocktail competitions. This approach enhances brand visibility and connects with younger demographics who value authenticity and craftsmanship. The company is solidifying its reputation as a key player in the competitive United States gin landscape. It achieves this by prioritizing product diversity and cultural relevance to drive growth and sophistication.

- Bacardi Limited strengthens its position in the United States gin market through its Bombay Sapphire brand which is renowned for its distinctive blue bottle and vapor infused distillation process. The company targets premium consumers by emphasizing artistry and global botanical sourcing in its marketing efforts. Recent strategies include launching ready to drink cocktails and flavored variants to capture the convenience driven segment. Bacardi invests in sustainability initiatives such as water conservation and responsible sourcing to align with corporate social responsibility goals. By leveraging its strong brand equity and innovative product development the company appeals to modern drinkers who seek both quality and ethical production practices. These efforts ensure continued relevance and growth in the dynamic and competitive American spirits industry.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States gin market primarily employ premiumization strategies to differentiate their offerings and capture higher value segments. Companies frequently introduce artisanal and small batch gins with unique botanical profiles to appeal to sophisticated palates. Another major strategy involves expanding into the non alcoholic and low alcohol categories to cater to health conscious consumers and the sober curious movement. Strategic partnerships with bars and restaurants help manufacturers secure prominent menu placement and drive on trade sales. Digital marketing and social media engagement are utilized extensively to build brand communities and reach younger demographics through influencer collaborations. Additionally firms invest in sustainable packaging and eco friendly production methods to enhance brand image and meet environmental standards. Price optimization through limited edition releases and exclusive bundles remains crucial for maintaining competitiveness and driving revenue growth across diverse consumer groups.

MARKET SEGMENTATION

This research report on the U.S. gin market has been segmented and sub-segmented into the following categories.

By Product Type

- London Dry Gin

- Plymouth Gin

- Old Tom Gin

- Other Product Types

By End User

- Men

- Women

By Category

- Mass

- Premium

By Distribution Channel

- On-Trade

- Off-Trade

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. gin market?

The U.S. gin market covers sales and trends for juniper‑based spirits, from mass brands to craft distillers shaping retail and bar menus nationwide.

How does the U.S. gin market operate?

The U.S. gin market moves product through distillers, distributors, retailers, and on‑premise venues, driven by branding, cocktails, and tasting events.

What drives growth in the U.S. gin market?

Innovation in botanicals, craft distilleries, and cocktail culture drive interest in the U.S. gin market among modern spirit drinkers.

Which gin styles lead the U.S. gin market?

London dry, contemporary botanical, and flavored variants dominate offerings that define the U.S. gin market across bars and stores.

How important are craft distillers to the U.S. gin market?

Craft distillers inject variety and local identity into the U.S. gin market with small batch releases and experimental botanicals.

What role do cocktails play in the U.S. gin market?

Cocktail menus and classic serves like the G and T shape consumer demand and visibility for the U.S. gin market in bars and restaurants.

How does premiumization affect the U.S. gin market?

Premium and super‑premium positioning elevates the U.S. gin market by appealing to consumers seeking quality and unique tasting profiles.

What trends shape the U.S. gin market?

Botanical experimentation, low ABV serves, and gin tourism influence trends and product launches across the U.S. gin market.

How do retailers impact the U.S. gin market?

Shelf placement, tastings, and curated displays help retailers drive discovery and sales within the U.S. gin market.

What challenges face the U.S. gin market?

Competition from other spirits, shifting consumer tastes, and market saturation challenge growth across the U.S. gin market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com