U.S. Headphone Market Size, Share, Trends, and Growth Analysis Report, Segmented by Product, Technology, Type, and Country – Industry Forecast From 2026 to 2034

U.S. Headphone Market Report Summary

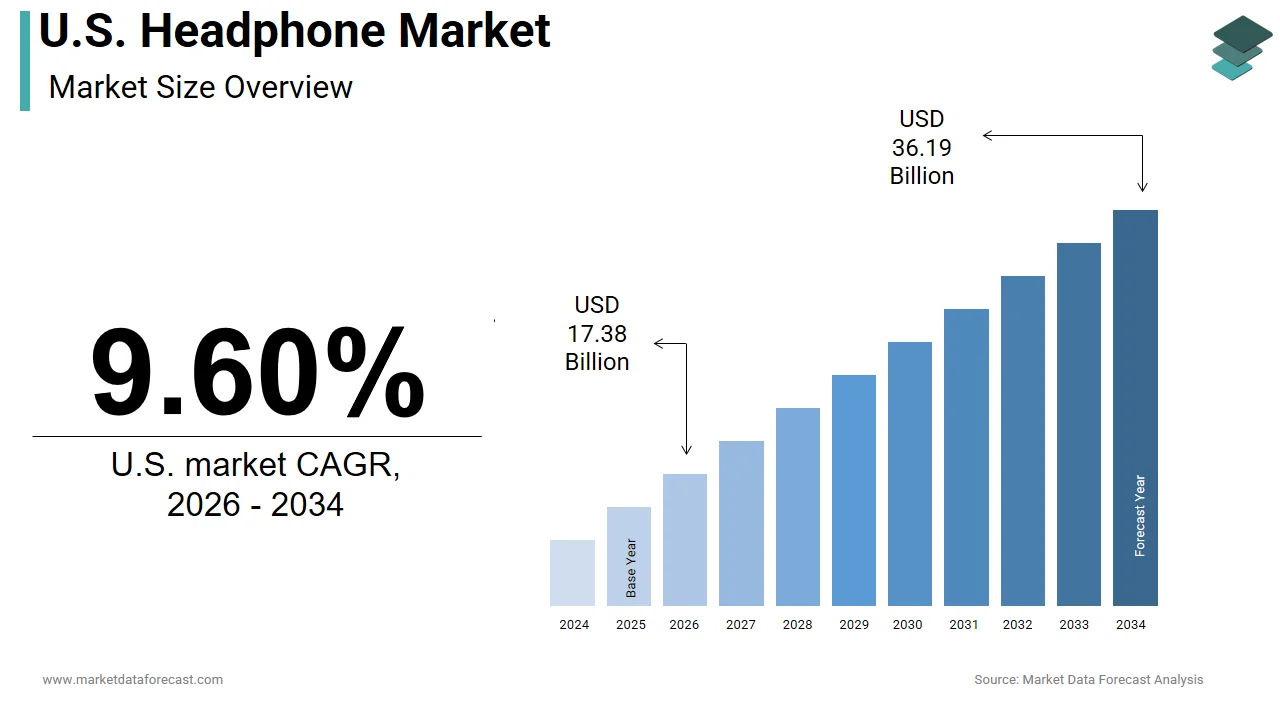

The U.S. headphone market was valued at USD 15.86 billion in 2025, is estimated to reach USD 17.38 billion in 2026, and is projected to reach USD 36.19 billion by 2034, growing at a CAGR of 9.60% from 2026 to 2034. Market growth is driven by increasing adoption of wireless audio devices, rising smartphone penetration, and growing consumer demand for immersive entertainment and gaming experiences. Advancements in Bluetooth connectivity, active noise cancellation, spatial audio, and AI-enabled sound technologies are significantly transforming the headphone industry. Additionally, the expansion of music streaming platforms, remote working culture, and fitness-oriented audio products is accelerating market growth across the United States.

Key Market Trends

- Rising demand for wireless and Bluetooth-enabled headphones.

- Increasing popularity of noise cancellation and spatial audio technologies.

- Growth in gaming, fitness, and entertainment-oriented audio devices.

- Expansion of smart audio ecosystems and AI-powered sound features.

- Increasing consumer preference for portable and in-ear audio products.

Segmental Insights

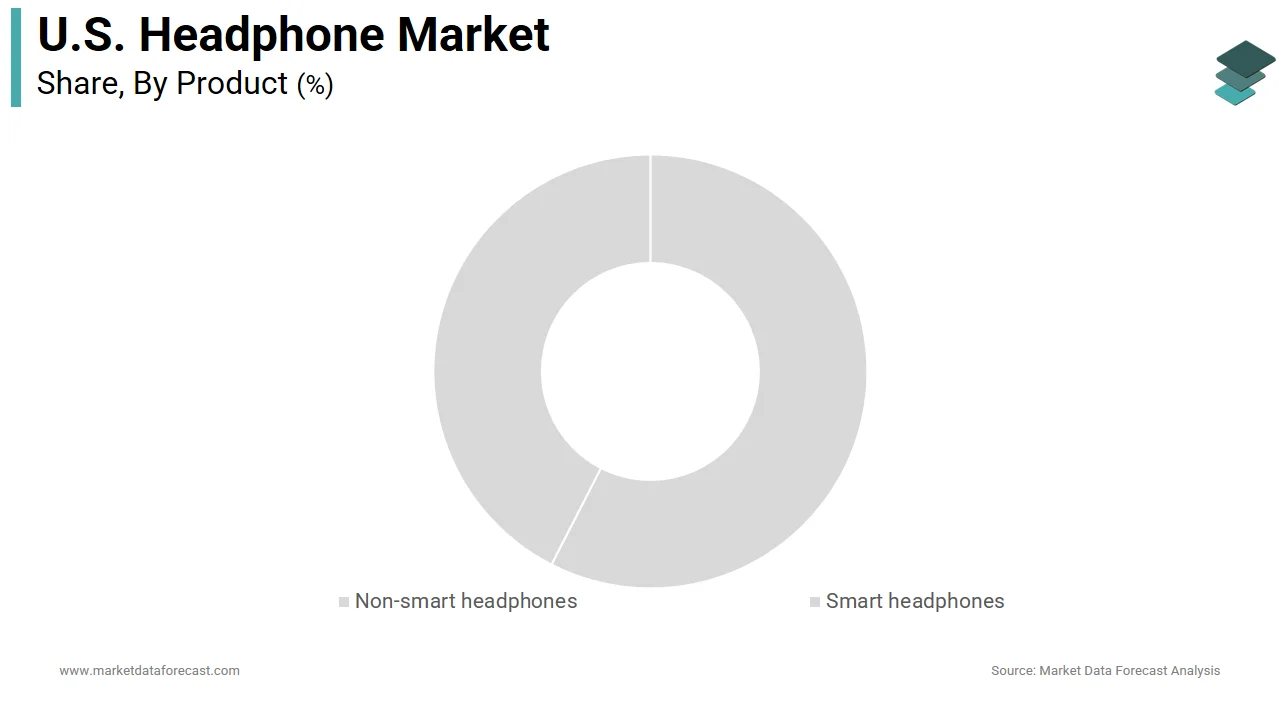

- Based on product, the non-smart headphones segment dominated the United States headphone market in 2025, driven by affordability and widespread consumer usage across entertainment and communication applications.

- Based on technology, the wireless headphones segment held the leading share in 2025, supported by increasing consumer preference for convenience, portability, and seamless connectivity.

- Based on type, the in-ear headphones segment led the market by accounting for 54.8% share in 2025, driven by compact design, comfort, and rising adoption among smartphone users and fitness enthusiasts.

Country-Level Insights

- The United States dominated the North American headphone market by capturing 82.5% share in 2025, supported by high consumer electronics spending, rapid adoption of advanced audio technologies, and strong presence of premium audio brands.

Competitive Landscape

The U.S. headphone market is highly competitive, with companies focusing on wireless innovation, premium audio quality, and smart connectivity features. Investments in AI-driven sound personalization, gaming audio solutions, and sustainable product designs are shaping the competitive landscape.

Prominent companies operating in the U.S. headphone market include Apple Inc., Audio-Technica, beyerdynamic, Bluei Store Pvt. Ltd., Bose Corporation, Bragi, Creative Technology, GN Store Nord, Grado Labs, JVCKENWOOD Corporation, LG Electronics, Logitech, Monster Inc., Northbaze Group, Panasonic Holdings Corporation, Samsung Electronics, Sennheiser, Shure Inc., Skullcandy, and Sony Group Corporation.

U.S. Headphone Market Size

The U.S. headphone market was valued at USD 15.86 billion in 2025, is estimated to reach USD 17.38 billion in 2026, and is projected to reach USD 36.19 billion by 2034, growing at a CAGR of 9.60% from 2026 to 2034.

Headphones are a pair of small, electroacoustic transducers worn over or inside the ears to convert electrical signals into sound. This market is fundamentally driven by the ubiquity of smartphones and the increasing consumption of digital media rather than functioning merely as an accessory domain. The fundamental necessity for private audio engagement in public and professional spaces ensures consistent demand across all age groups. Research confirms near-universal connectivity, with 97% of U.S. adults owning a cellphone and 90% specifically owning a smartphone, establishing a massive, tech-fluent baseline consumer market for Bluetooth and compatible audio devices. This technological penetration ensures market resilience regardless of economic fluctuations. The shift towards remote work has further amplified this requirement as individuals seek high-quality audio solutions for virtual meetings and focused work environments. According to the Bureau of Labor Statistics, more than 22% of U.S. employees continue to work remotely or follow hybrid structures at least part of the time, cementing a permanent structural shift in demand for ergonomic, noise-canceling, and communication-heavy headsets. Additionally, the widespread adoption of streaming services has led to an increase in daily audio consumption, with the average American spending over 4 hours per day listening to music or podcasts, according to sources. This phenomenon has spurred demand for specialized headphones with enhanced battery life and superior sound quality. The market is thus defined by a convergence of connectivity necessity and lifestyle adaptation, where consumer choices are increasingly influenced by convenience and audio fidelity rather than aesthetic preferences alone.

MARKET DRIVERS

Proliferation of Wireless Technology and Bluetooth Connectivity

The rapid adoption of wireless technology and advanced Bluetooth connectivity contributes to the growth and expansion of the United States headphone market. Consumers are increasingly prioritizing convenience and mobility, leading to a decisive shift away from wired audio solutions. The Consumer Technology Association (CTA) establishes that wireless units have solidified an overwhelming dominance in personal audio, capturing over 75% of total sales revenue in the United States. This significant rise translates into a larger pool of individuals upgrading their existing wired devices to wireless alternatives. Furthermore, the improvement in Bluetooth standards such as Bluetooth 5.0 and later versions has enhanced connection stability and range, making wireless options more reliable for daily use. This regulatory support encourages manufacturers to innovate and release products with lower latency and higher data throughput. Additionally, the removal of headphone jacks from many flagship smartphones has forced consumers to adopt wireless solutions or use dongles, which further accelerates the market transition. Consequently, manufacturers are seeing increased frequency in product launches featuring advanced pairing capabilities and multi-device connectivity. This accelerated replacement cycle directly boosts volume sales for manufacturers and retailers alike.

Rising Consumption of Streaming Media and Podcasts

The escalating consumption of streaming media and podcasts is a significant accelerator for the United States headphone market. Users are increasingly seeking immersive and private listening experiences. Digital audio content has become a staple of daily entertainment and information acquisition for millions of Americans. Research confirms the staggering growth of digital talk media, reporting that monthly podcast listenership in the United States surged past 120 million, engaging a highly dedicated demographic of the population aged 12 and older. This extensive audience requires reliable and comfortable headphones for extended listening sessions. Furthermore, the growth of music streaming platforms such as Spotify and Apple Music has led to an increase in high-resolution audio offerings, which necessitate headphones capable of reproducing detailed soundscapes. The Recording Industry Association of America (RIAA) highlights the absolute dominance of digital distribution formats, with streaming revenues consistently capturing over 82% of the total recorded music market. This shift drives demand for headphones with features such as active noise cancellation, which allows users to isolate themselves from ambient noise and focus on content. Additionally, the popularity of audiobooks has grown, with Audible reporting millions of active users who rely on headphones for long-duration listening. These factors collectively ensure that the headphone segment remains a dominant force in the consumer electronics market.

MARKET RESTRAINTS

Health Concerns Related to Prolonged Audio Exposure

The growing awareness of health risks associated with prolonged exposure to high-volume audio is a major restraint on the United States headphone market. This is particularly true among younger demographics. Medical professionals have raised alarms about the potential for noise-induced hearing loss, which is irreversible and can significantly impact quality of life. The Centers for Disease Control and Prevention (CDC) reveals that approximately 12.5% of children aged 6 to 19 and 15% of adults aged 20 to 69 exhibit audiometric signs of permanent noise-induced hearing loss, highlighting a critical public health need for safe listening features. This statistic has prompted parents and health advocates to limit the use of headphones among children and teenagers. The World Health Organization (WHO) estimates that over 1 billion young people worldwide are at risk of hearing loss due to unsafe listening practices, an alarming benchmark that continues to drive the adoption of sound-exposure alerts and volume-limiting features in consumer audio hardware. In response, some consumers are reducing their usage duration or opting for speakers instead of headphones to mitigate risk. The American Speech-Language-Hearing Association (ASHA) champions the 60/60 rule, recommending that users keep headphone volumes under 60% and limit listening sessions to 60 minutes, directly challenging the daily habits of heavy media consumers. This health consciousness leads to a more cautious approach to purchasing new devices, with some consumers delaying upgrades or choosing models with built-in volume limiters. Consequently, a segment of the population is becoming more resistant to frequent purchases driven by fashion or minor feature updates. This shift towards health preservation hampers market growth for premium, high-volume, capable products and encourages a more conservative consumption pattern.

High Cost of Premium Audio Features and Economic Sensitivity

The substantial financial burden associated with purchasing premium headphones featuring advanced technologies is also a hurdle to the United States headphone market penetration. This is particularly true among budget-conscious consumers. While basic audio functionality is accessible, the cost of headphones with active noise cancellation, high-fidelity drivers, and premium build materials often exceeds the discretionary spending limits of many households. The Bureau of Labor Statistics demonstrates that audio equipment and consumer electronics frequently undergo deflationary pricing trends, keeping entry-level personal audio highly accessible despite broader inflationary pressures on household staples. This financial barrier prevents a substantial portion of the population from adopting high-end audio solutions. Research indicates that personal audio devices have shifted from discretionary luxuries to essential remote-work and lifestyle utilities, sustaining market demand across diverse income brackets. Many consumers continue to rely on inexpensive bundled earbuds or older devices despite being aware of the benefits of premium audio. The lack of perceived necessity for high-end features among casual listeners further exacerbates this issue, as basic models suffice for phone calls and background music. Consequently, price sensitivity remains a critical factor limiting the widespread adoption of the premium segment. Manufacturers face the challenge of balancing cost efficiency with technological innovation to make these products more affordable without compromising quality. However, the inherent costs of components such as batteries and chips make significant price reductions difficult. This economic reality constrains market expansion in the high-value segment.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Smart Features

The integration of artificial intelligence and smart features offers a strong opening for manufacturers to enhance user experience and differentiate their products, which is likely to drive the United States headphone market forward. Modern consumers are seeking devices that offer more than just audio playback, such as voice assistant integration, real-time translation, and adaptive sound control. Headphones equipped with AI can analyze ambient noise and automatically adjust noise cancellation levels, providing optimal listening conditions in varying environments. This technology not only improves comfort but also extends battery life by optimizing power usage. Major tech companies are investing heavily in developing proprietary algorithms that learn user preferences and adjust equalizer settings accordingly. This feature appeals to gamers and home theater enthusiasts who seek cinema-quality experiences. Additionally, AI-driven health monitoring features such as heart rate tracking and posture correction are being integrated into premium models. These innovations transform headphones from passive audio tools into active health and productivity assistants. As consumers become more accustomed to smart home ecosystems, the demand for interconnected audio devices will rise. This technological evolution offers a pathway for brands to capture higher margins and foster brand loyalty through unique functional benefits.

Expansion into Gaming and Esports Audio Solutions

The rapid growth of the gaming and esports industry provides a clear path for headphone manufacturers to develop specialized audio solutions tailored to gamers, which is expected to fuel the expansion of the United States headphone market. Competitive gaming requires precise audio cues and clear communication, which drives demand for high-performance headsets with low latency and surround sound capabilities. Gamers are willing to pay premium prices for headsets that offer competitive advantages such as directional audio and noise-isolating microphones. Furthermore, the rise of streaming platforms like Twitch has created a community of content creators who require high-quality audio for broadcasting. This demographic values aesthetics and customization, leading to opportunities for branded collaborations and limited edition releases. Manufacturers are responding by introducing wireless gaming headsets with long battery lives and RGB lighting effects that appeal to the gaming culture. The integration of haptic feedback in some models adds another layer of immersion, enhancing the overall gaming experience. As cloud gaming services expand, the need for versatile low-latency headphones will increase. This segment represents a high-growth area where technical performance and cultural relevance drive purchasing decisions.

MARKET CHALLENGES

Supply Chain Volatility and Semiconductor Shortages

Persistent supply chain disruptions and shortages of critical semiconductors are a significant challenge to the stability and profitability of the headphone manufacturing sector. This inhibits the growth of the United States headphone market. The production of wireless headphones relies heavily on chips for Bluetooth connectivity, noise cancellation, and battery management, which are subject to global supply constraints. These delays result in inventory stockouts and an inability to meet consumer demand, particularly during peak shopping seasons. These cost increases are often difficult to pass on to consumers in a highly competitive market, leading to compressed margins. Additionally, geopolitical tensions and trade policies affect the availability of raw materials such as rare earth metals used in speakers and magnets. Manufacturers relying on just-in-time inventory systems have faced significant operational challenges, forcing them to hold larger safety stocks, which ties up capital. Furthermore, the concentration of manufacturing in specific regions creates vulnerability to local disruptions such as natural disasters or labor strikes. These factors create uncertainty in production planning and pricing strategies, making it difficult for companies to maintain consistent product availability.

Environmental Regulations and E-Waste Management

Navigating the complex landscape of environmental regulations and e-waste management is an obstacle for headphone manufacturers in the country, which slows down the expansion of the United States headphone market. The widespread adoption of wireless headphones has contributed to a surge in electronic waste due to the presence of non-replaceable lithium-ion batteries and complex internal components. New state-level regulations, such as those in California and New York, are imposing stricter requirements on battery disposal and product recyclability. Noncompliance can result in legal penalties and reputational damage. Additionally, the European Union's right to repair legislation is influencing global standards, pushing manufacturers to design products that are easier to disassemble and repair. This shift requires significant investment in research and development to create modular designs without compromising water resistance or aesthetic appeal. The cost of implementing take-back programs and recycling infrastructure further strains budgets, particularly for smaller brands. Consumers are increasingly holding brands accountable for their environmental impact, which adds pressure to adopt circular economy principles. Balancing regulatory compliance with cost efficiency and product performance remains a difficult task for industry participants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Technology, Type, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Apple Inc., Audio-Technica US Inc., beyerdynamic GmbH & Co. KG, Bluei Store Pvt. Ltd., Bose Corp., BRAGI GmbH, Creative Technology Ltd., GN Store Nord AS, Grado Labs Inc., JVCKENWOOD Corp., LG Electronics Inc., Logitech International SA, Monster Inc., Northbaze Distribution AB, Panasonic Holdings Corp., Samsung Electronics Co. Ltd., Sennheiser Electronic GmbH & Co. KG, Shure Inc., Skullcandy Inc., Sony Group Corp., and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The non-smart headphones segment held the majority share of the United States market in 2025. This supremacy of the segment was credited to its affordability and broad accessibility across diverse consumer segments. Unlike smart headphones, which incorporate advanced sensors and artificial intelligence, non-smart models focus on core audio performance at a lower price point. The Bureau of Labor Statistics (BLS) consumer expenditure surveys highlight that households allocate a distinct portion of their entertainment budgets to audio-visual equipment, driving an aggressive retail demand for cost-efficient, entry-level electronic alternatives. Standard, non-smart headphones typically range from under $15 to $150, remaining highly accessible to students, casual listeners, and budget-conscious households looking for pure audio utility without premium software markups. The Consumer Technology Association (CTA) highlights that while price sensitivity shapes the entry-level audio market, feature complexity, such as battery optimization and active noise cancellation, remains a major catalyst for mid-to-high tier headphone sales. This demographic preference ensures high-volume sales for manufacturers offering reliable audio quality without premium add-ons. Additionally, the simplicity of non-smart devices reduces the learning curve for older adults and technologically hesitant users who prefer plug-and-play functionality. The absence of complex software updates and connectivity issues further enhances user satisfaction and reduces return rates. Retailers favor these products due to their faster inventory turnover and lower support costs. Consequently, the non-smart segment maintains its dominance by catering to the mass market where value and reliability outweigh the desire for cutting-edge technology. This widespread adoption sustains revenue stability even as niche smart segments emerge.

Furthermore, the domination of the non-smart headphones segment is further reinforced by their superior durability and lower maintenance requirements compared to smart alternatives. Non-smart headphones lack complex internal components such as microprocessors and multiple sensors, which are prone to failure and battery degradation. Consumers appreciate the longevity of traditional headphones, which can last for several years with minimal care. Furthermore, non-smart headphones do not require frequent firmware updates or compatibility checks with specific operating systems, ensuring consistent performance over time. This reliability is particularly valued in professional settings such as studios and offices, where equipment failure can disrupt workflows. Additionally, the absence of battery anxiety allows users to rely on wired connections or simple rechargeable units without worrying about power management. These practical advantages ensure that non-smart headphones remain a preferred choice for users prioritizing function and longevity over digital integration.

However, the smart headphones segment is expected to exhibit a noteworthy CAGR of 12.5% from 2026 to 2034 due to the integration of health monitoring and biometric sensors that transform headphones into wearable health devices. Modern smart headphones can track heart rate, body temperature, and even detect falls, providing valuable health insights to users. Sources confirm that the global wearables market is scaling rapidly, propelled by a convergence where traditional audio headphones are increasingly outfitted with advanced health and fitness tracking sensors. The Centers for Disease Control and Prevention (CDC) indicates that the vast majority of U.S. healthcare costs are driven by chronic conditions, fueling a massive consumer health migration toward continuous digital tracking and biometric monitoring tools. Smart headphones offer a discreet and convenient way to collect health data without the need for additional devices. Companies like Bose and Sony have introduced models with sensors that adjust noise cancellation based on user stress levels or the environment. This functionality appeals to health-conscious individuals and fitness enthusiasts who seek comprehensive wellness solutions. As insurance companies begin to incentivize healthy behaviors through data tracking, the adoption of smart headphones is expected to accelerate. This convergence of audio entertainment and health monitoring creates a unique value proposition that drives rapid market growth.

A further significant factor driving the rapid growth of the smart headphones segment is the seamless integration of advanced voice assistants and artificial intelligence connectivity features. Consumers increasingly rely on voice commands for hands-free operation during commuting, working, and exercising. Smart headphones allow users to access Siri, Google Assistant, and Alexa instantly, enabling tasks such as sending messages, navigating, and controlling smart home devices without touching a phone. This convenience enhances productivity and safety, particularly for drivers and multitaskers. Furthermore, AI-driven features such as real-time language translation and adaptive sound profiles personalize the listening experience. These capabilities appeal to global travelers and professionals who require efficient communication tools. The proliferation of 5G networks also supports faster data transmission, enabling more sophisticated cloud-based AI processing. As users become accustomed to the efficiency of voice-controlled interfaces, the demand for smart headphones with enhanced connectivity continues to surge. This technological synergy ensures that the smart segment outpaces traditional audio devices in growth rate.

By Technology Insights

The wireless headphones segment led the United States market and captured a significant share in 2025. This leading position of the segment was attributed to the unmatched convenience and mobility they offer to consumers with active lifestyles. The elimination of tangled wires allows users to move freely during exercise, commuting, and daily activities, enhancing the overall user experience. The Consumer Technology Association (CTA) establishes that wireless headphone revenue surpassed wired units for the first time in 2016, with Bluetooth configurations continuing to dominate the market by capturing over 75% of total sales revenue. This shift is driven by the widespread adoption of smartphones without headphone jacks, which forces users to adopt Bluetooth solutions. Furthermore, advancements in battery technology have extended playback times to over 20 hours per charge, addressing previous concerns about power longevity. According to data from the Sports and Fitness Industry Association (SFIA), over 75% of the U.S. population participates in fitness or sports activities annually, fueling a massive, continuous retail demand for secure-fit, sweatproof wireless headphones. Additionally, the rise of true wireless stereo earbuds has made compact and portable audio solutions highly popular among commuters and travelers. The ease of pairing with multiple devices, such as laptops, tablets, and phones, further enhances utility. These factors collectively ensure that wireless technology remains the preferred choice for the majority of consumers seeking flexibility and ease of use in their audio devices.

Moreover, the domination of the wireless headphones segment is further reinforced by significant improvements in audio quality and connectivity standards that rival wired performance. Recent advancements in Bluetooth codecs, such as aptX HD and LDAC, enable high-resolution audio streaming over wireless connections, minimizing the quality gap with traditional wired headphones. This widespread adoption has driven economies of scale, allowing manufacturers to produce high-quality wireless chips at lower costs. Additionally, the implementation of Bluetooth 5.0 and later versions has doubled the transmission range and quadrupled the data throughput compared to previous generations. These technical improvements have alleviated consumer skepticism regarding wireless audio fidelity. Major brands now offer wireless models with active noise cancellation and spatial audio features that provide immersive listening experiences. As consumers recognize that wireless no longer means compromised quality, the preference for cable-free solutions solidifies. This technological parity ensures that wireless headphones maintain their leadership in the market.

But the wired headphones segment is predicted to witness the highest CAGR of 7.2% over the forecast period, owing to demand from audiophiles and professional studio engineers who prioritize uncompressed audio fidelity. Wired connections provide a stable and lossless signal path that is essential for critical listening and mixing tasks. The Recording Industry Association of America (RIAA) highlights a massive, multi-year resurgence in vinyl sales driven heavily by younger demographics who value tangible media and high-fidelity audio aesthetics. Professional studios and broadcast stations continue to rely on wired headphones for their zero latency and reliability during recording sessions. The Audio Engineering Society (AES) emphasizes that uncompressed, zero-latency monitoring is best achieved through wired analog or digital connections, making legacy inputs essential for audio engineering professionals. Additionally, the gaming community includes a segment of competitive players who prefer wired headsets for their instantaneous response times and lack of battery dependency. The ESL FACEIT Group mandates that professional esports competitors use wired headsets and peripherals during live stages to prevent radio-frequency interference and eliminate audio latency in high-density stadium environments. Furthermore, the durability of wired headphones makes them a cost-effective long-term investment for users who do not need wireless convenience. The availability of high-end cables and connectors allows for customization and upgrades appealing to enthusiasts. This dedicated niche ensures that the wired segment retains relevance and experiences steady growth in specialized applications despite the broader wireless trend.

The fast growth here is helped by their reliability in critical communication and industrial settings where wireless interference can be hazardous. In environments such as aviation, manufacturing, and emergency services, wired headsets provide secure and uninterrupted audio channels. Industrial facilities often have high levels of electromagnetic noise, which can disrupt wireless signals, making wired connections safer and more effective. Additionally, wired headphones do not require charging, eliminating the risk of power failure during critical operations. This dependability is valued in medical settings where doctors and nurses use wired headsets for telemedicine consultations without worrying about battery life. These specialized applications create a consistent demand for high-quality wired headphones that cannot be easily replaced by wireless alternatives. The wired segment maintains a stable foothold in professional markets. This is because these industries prioritize safety and reliability.

By Type Insights

The in-ear headphones segment was the largest by occupying a 54.8% share of the United States market in 2025. This prominence of the segment was supported by its exceptional portability and convenience for on-the-go usage. Their compact size allows them to fit easily into pockets and small bags, making them ideal for commuters, travelers, and athletes. The lightweight design reduces fatigue during extended wear, which is particularly appealing for users who listen to audio for several hours a day. Additionally, the discrete nature of in-ear headphones allows for private listening in public spaces without drawing attention. The rise of remote work has also increased the use of in-ear models for video calls as they are less cumbersome than over-ear headsets. Major smartphone manufacturers bundle in-ear headphones with their devices, further boosting adoption rates. The affordability of entry-level in-ear options makes them accessible to a wide demographic, including students and young professionals. These factors collectively ensure that in-ear headphones remain the most popular choice for everyday consumers seeking convenience and versatility.

In addition, the spearheading of the in-ear headphones segment is further reinforced by advancements in fit and noise isolation technology that enhance comfort and audio immersion. Modern in-ear models come with multiple ear tip sizes and materials such as silicone and memory foam to ensure a secure and comfortable seal. This feature is highly valued by commuters and office workers who need to focus in noisy environments. Additionally, the development of ergonomic designs based on 3D ear scans has improved long-term wearability, reducing discomfort and slippage. Furthermore, the integration of active noise cancellation in premium in-ear models has closed the performance gap with larger over-ear headphones. Brands like Apple and Sony have introduced adaptive transparency modes that allow users to hear their surroundings when needed, enhancing safety and situational awareness. These technological improvements have made in-ear headphones a viable option for a wider range of use cases, from travel to professional work. As consumers prioritize both comfort and performance, the in-ear segment continues to lead the market.

On the contrary, the over-ear headphones segment is estimated to register the fastest CAGR of 8.5% over the forecast period. This swift growth of the segment is mainly propelled by the superior comfort and immersive audio experience they provide for extended listening sessions. Over-ear models distribute weight evenly around the ears, reducing pressure points and fatigue compared to on-ear or in-ear options. The large drivers in over-ear headphones deliver richer bass and wider soundstages, which appeal to music enthusiasts and gamers. Additionally, the rise of high-resolution streaming services has increased demand for headphones capable of reproducing detailed audio nuances. Over-ear models are also preferred for noise cancellation as their larger cups provide better passive isolation. These factors collectively drive the rapid adoption of over-ear headphones among users prioritizing comfort and audio quality.

A further key factor driving the growth of the over-ear headphones segment is the growing popularity of home office and gaming setups that require high-quality audio and microphone performance. Remote workers and gamers spend long hours in front of screens, necessitating comfortable and reliable headsets. Over-ear headphones often feature boom microphones and mute buttons, which are essential for clear communication during meetings and multiplayer games. Additionally, the aesthetic appeal of sleek and modern over-ear designs has made them a staple of home office decor. Social media platforms showcase setup tours where over-ear headphones are featured prominently, influencing consumer preferences. The durability and replaceable parts of many over-ear models also appeal to users seeking long-term value. The boundary between work and leisure is blurring. Consequently, the versatility of over-ear headphones for both professional and recreational use ensures their continued rapid growth in the market.

COUNTRY ANALYSIS

U.S. Headphone Market Analysis

The United States was the top performer in the North American headphone market and occupied a 82.5% share in 2025. This dominance of the US market was driven by the country's high disposable income, advanced technological infrastructure, and strong culture of personal audio consumption. The market status is characterized by a mature yet innovative environment where consumers readily adopt new technologies such as true wireless and smart features. According to U.S. Census Bureau estimates, the national population has surpassed 342 million, establishing a massive, tech-forward consumer base highly receptive to new consumer electronics and digital accessories. The high prevalence of smartphone ownership ensures a large addressable base for compatible audio devices. Research confirms that 90% of American adults now own a smartphone, an expansive mobile ecosystem that acts as an unyielding catalyst for wireless and Bluetooth-enabled headphone sales. Additionally, the United States is home to major global headphone brands and tech giants that launch flagship products domestically first. This local availability fosters strong brand loyalty and awareness. The robust e-commerce landscape, facilitated by companies like Amazon and Best Buy, ensures wide distribution and competitive pricing. Furthermore, the cultural emphasis on fitness and personal wellness drives sales of sports-oriented audio gear. The Federal Communications Commission supports innovation in wireless technologies, which benefits the headphone industry. These structural, economic, and cultural factors solidify the United States as the leading market for headphones in the region, with sustained growth potential driven by technological advancement and lifestyle trends.

COMPETITIVE LANDSCAPE

The competition in the United States headphone market is intense and characterized by a mix of established technology giants and specialized audio manufacturers. Major players leverage their brand equity and extensive distribution networks to maintain dominance while newer entrants disrupt the market with innovative features and competitive pricing. The rivalry is further amplified by the rapid pace of technological advancement, where noise cancellation, battery life, and connectivity standards serve as key differentiators. Companies are constantly innovating to offer superior sound quality and user experience through artificial intelligence and machine learning integration. Price competition is fierce, particularly in the mid-range segment, where consumers seek value for money. Traditional audio brands face pressure from tech companies that bundle headphones with broader ecosystems, creating lock-in effects. The threat of substitution from smart speakers and earbuds also influences competitive dynamics. Brand loyalty is cultivated through consistent quality and customer service excellence. Regulatory compliance regarding wireless standards and environmental sustainability serves as a barrier to entry. Overall, the market demands continuous adaptation to consumer preferences and technological trends to sustain competitive advantage and profitability in this dynamic industry landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. headphone market include

- Apple Inc.

- Audio Technica US Inc.

- beyerdynamic GmbH and Co. KG

- Bluei Store Pvt. Ltd.

- Bose Corp.

- BRAGI GmbH

- Creative Technology Ltd.

- GN Store Nord AS

- Grado Labs Inc.

- JVCKENWOOD Corp.

- LG Electronics Inc.

- Logitech International SA

- Monster Inc.

- Northbaze Distribution AB

- Panasonic Holdings Corp.

- Samsung Electronics Co. Ltd.

- Sennheiser Electronic GmbH and Co. KG

- Shure Inc.

- Skullcandy Inc.

- Sony Group Corp.

TOP PLAYERS IN THE MARKET

- Apple Inc maintains a formidable presence in the United States headphone market through its AirPods lineup, which has become synonymous with wireless audio. The company leverages its integrated ecosystem to provide seamless connectivity across iPhones, iPads, and Macs, enhancing user convenience. Recently, Apple has focused on advancing spatial audio technology and adaptive noise cancellation to differentiate its products from competitors. The introduction of health monitoring features such as hearing health tracking further strengthens its value proposition. By controlling both hardware and software, Apple ensures a superior user experience that fosters brand loyalty. Their continuous investment in custom silicon chips allows for improved battery life and processing power. These strategic innovations reinforce Apple's position as a leader in premium personal audio devices while driving widespread adoption of true wireless stereo technology among consumers seeking high-quality and integrated solutions.

- Sony Group Corporation is a key contributor to the United States headphone market, known for its industry-leading noise cancellation technology and high-resolution audio capabilities. The company appeals to audiophiles and professionals who prioritize sound quality and comfort in their listening devices. Recently, Sony has enhanced its product line with advanced artificial intelligence-driven noise-cancelling processors that adapt to user environments in real time. The brand actively promotes sustainability by using recycled materials in its packaging and product components. Sony also strengthens its market position through strategic partnerships with streaming services to offer exclusive high-fidelity content. Their commitment to innovation is evident in the development of multipoint connectivity, allowing users to switch between devices effortlessly. These efforts ensure that Sony remains a top choice for consumers seeking premium audio performance and cutting-edge technological features in a competitive landscape.

- Bose Corporation holds a significant role in the United States headphone market by pioneering active noise cancellation technology and delivering exceptional acoustic performance. The brand is renowned for its comfortable designs and reliable build quality, which appeal to travelers and professionals. Recently, Bose has expanded its product portfolio to include smart audio glasses and specialized gaming headsets, diversifying its offerings beyond traditional headphones. The company focuses on enhancing user experience through intuitive controls and robust mobile applications that allow customization of sound profiles. Bose also invests heavily in research and development to improve battery efficiency and connectivity stability. Their emphasis on customer service and warranty support builds trust and long-term loyalty. By consistently delivering innovative solutions that address specific consumer needs, Bose maintains its reputation as a premium audio brand. These actions solidify its competitive stance and drive growth in the high-end segment of the headphone market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States headphone market employ several strategic initiatives to maintain competitiveness and drive growth. Product innovation remains a primary strategy with companies investing heavily in active noise cancellation and spatial audio technologies to enhance user immersion. Brands are increasingly focusing on ecosystem integration, ensuring seamless connectivity with smartphones and other smart devices. Sustainability is becoming a critical focus as manufacturers adopt recycled materials and eco-friendly packaging to appeal to environmentally conscious consumers. Direct-to-consumer sales channels are being expanded to improve margins and gather valuable customer data. Strategic partnerships with content providers and tech firms help create unique value propositions. Marketing efforts emphasize lifestyle branding and influencer collaborations to reach younger demographics. Companies also prioritize software updates to extend product lifespan and add new features post-purchase. These strategies collectively enable brands to differentiate themselves and sustain relevance in a rapidly evolving technological landscape.

U.S. HEADPHONE MARKET NEWS

- In March 2023, Apple Inc, a technology giant, launched the second generation of its AirPods Pro with enhanced noise cancellation. This launch is anticipated to attract premium users and strengthen the U.S. headphone market presence

- In June 2023, Sony Group Corporation, an electronics leader, introduced new WH-1000XM5 headphones with improved AI-driven noise canceling. This introduction is anticipated to boost sales and strengthen the U.S. headphone market presence

- In September 2023, Bose Corporation, an audio specialist, released updated QuietComfort earbuds with customizable sound profiles. This release is anticipated to enhance user satisfaction and strengthen the U.S. headphone market presence

- In January 2024, Apple Inc, a major innovator, integrated advanced hearing health features into its latest headphone models. This integration is anticipated to expand utility and strengthen the U.S. headphone market presence

- In May 2024, Sony Group Corporation, a global brand, partnered with a leading streaming service for exclusive high-resolution audio content. This partnership is anticipated to drive subscriptions and strengthen the U.S. headphone market presence

MARKET SEGMENTATION

This research report on the U.S. headphone market has been segmented and sub-segmented into the following categories.

By Product

- Non-smart headphones

- Smart headphones

By Technology

- Wired headphones

- Wireless headphones

By Type

- In-ear headphones

- Over-ear headphones

- On-ear headphones

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. headphone market?

The U.S. headphone market includes audio devices such as wired, wireless, and true wireless models used for entertainment, work, and fitness.

How does the U.S. headphone market function?

The U.S. headphone market works through manufacturers, distributors, and retailers that sell products online and in physical stores.

What drives growth in the U.S. headphone market?

The U.S. headphone market grows from wireless adoption, remote work, gaming, fitness use, and rising demand for premium audio quality.

Which product types lead the U.S. headphone market?

Wireless and true wireless models lead the U.S. headphone market, while over-ear and gaming headsets remain important categories.

How important are wireless models in the U.S. headphone market?

Wireless models are central to the U.S. headphone market because they offer convenience, mobility, and Bluetooth compatibility.

What role does noise cancellation play in the U.S. headphone market?

Noise cancellation strengthens the U.S. headphone market by improving focus, travel comfort, and premium product appeal

How does e-commerce affect the U.S. headphone market?

E-commerce expands the U.S. headphone market by improving price comparison, reviews, and access to a wide product range.

What trends shape the U.S. headphone market?

The U.S. headphone market is shaped by true wireless adoption, smart features, battery improvements, and style-driven purchases

How does gaming influence the U.S. headphone market?

Gaming supports the U.S. headphone market through demand for headsets with clear microphones, surround sound, and comfort.

What is the role of battery life in the U.S. headphone market?

Battery life is a key purchase factor in the U.S. headphone market for commuters, travelers, and daily wireless users.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com