U.S. Hard Seltzer Market Size, Share, Trends & Growth Forecast Report By Packaging, ABV Content, Distribution Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Hard Seltzer Market Report Summary

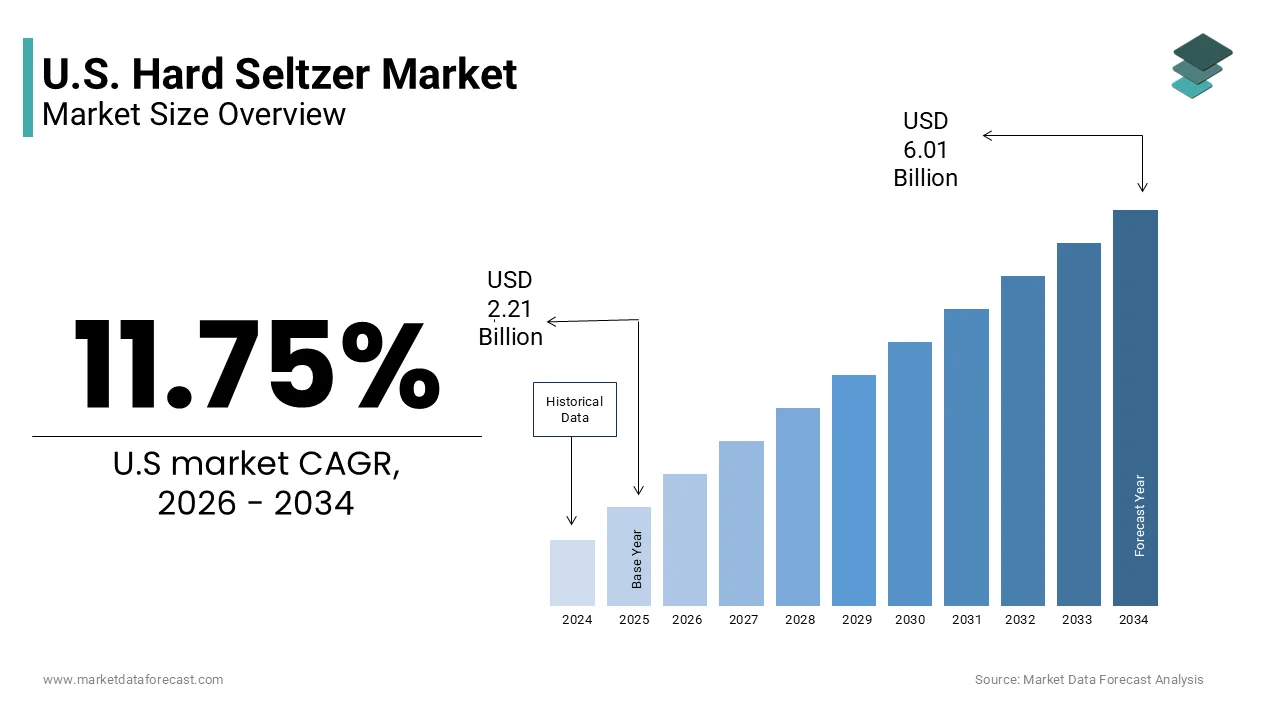

The U.S. hard seltzer market was valued at USD 2.21 billion in 2025, is estimated to reach USD 2.47 billion in 2026, and is projected to reach USD 6.01 billion by 2034, growing at a CAGR of 11.75% during the forecast period. Market growth is driven by increasing consumer preference for low calorie alcoholic beverages, rising demand for flavored alcoholic drinks, and growing health conscious drinking habits. Hard seltzers are gaining popularity due to their light flavor profiles, lower sugar content, and convenient ready to drink format. The expansion of premium alcoholic beverage categories and continuous flavor innovation are further supporting strong market growth across the United States.

Key Market Trends

- Rising consumer preference for low calorie and low sugar alcoholic beverages is driving market growth.

- Increasing demand for flavored ready to drink alcoholic products is boosting hard seltzer consumption.

- Growing health conscious drinking habits among younger consumers are supporting market expansion.

- Expansion of off trade retail channels and e commerce alcohol sales is enhancing product accessibility.

- Innovation in premium flavors, organic ingredients, and functional alcoholic beverages is influencing market development.

Segmental Insights

- Based on packaging, the metal cans segment held a substantial share of the U.S. hard seltzer market in 2025. This dominance is attributed to portability, convenience, sustainability, and strong consumer preference for canned beverages.

- Based on ABV content, the less than 5% ABV segment accounted for a significant share of the U.S. hard seltzer market in 2025, driven by increasing demand for lighter alcoholic beverages suitable for casual consumption.

- Based on distribution channel, the off trade channel segment held the majority share of the U.S. hard seltzer market in 2025, supported by strong sales through supermarkets, liquor stores, and retail chains.

Regional Insights

- The U.S. hard seltzer market is experiencing strong growth across the country, supported by changing alcohol consumption preferences, premiumization trends, and rising demand for convenient alcoholic beverage formats. Expanding product portfolios and aggressive marketing strategies are further strengthening market development.

Competitive Landscape

The U.S. hard seltzer market is highly competitive, with key players focusing on flavor innovation, premium branding, and expansion of distribution networks to strengthen their market position. Companies are investing in low calorie formulations, celebrity endorsements, and seasonal flavor launches. Prominent players in the U.S. hard seltzer market include Anheuser Busch InBev, Boston Beer Company, Mark Anthony Brands, Molson Coors Beverage Company, Heineken N.V., The Coca Cola Company, Constellation Brands, Diageo, Pabst Brewing Co., Bon & Viv, Crook & Marker, Press Premium Alcohol Seltzer, Bud Light Seltzer, REZ Hard Seltzer, and New Belgium Brewing Company.

U.S. Hard Seltzer Market Size

The U.S. hard seltzer market size was valued at USD 2.21 billion in 2025, is estimated to reach USD 2.47 billion in 2026, and is projected to reach USD 6.01 billion by 2034, growing at a CAGR of 11.75 % from 2026 to 2034.

Hard seltzer is defined as a carbonated water based alcoholic drink typically flavored with fruit extracts and containing alcohol derived from fermented cane sugar or malted barley. This category has transcended its initial novelty status to become a staple in social gatherings and casual consumption occasions. The cultural shift toward wellness and moderation has significantly influenced consumer preferences driving demand for beverages that align with active lifestyles. According to the CDC, nearly half (49.1%) of American adults attempted to lose weight during the most recent survey period, a trend that aligns with the increased market demand for low-calorie and reduced-sugar dietary options. Furthermore data from the US Department of Agriculture indicates that per capita consumption of added sugars has declined in recent years reflecting a broader societal move away from high sugar diets. The demographic profile of hard seltzer drinkers skews younger with millennials and Gen Z consumers leading adoption rates due to their preference for transparent labeling and natural ingredients. As per the National Institute on Alcohol Abuse and Alcoholism while overall alcohol consumption remains stable the composition of preferred beverages is shifting toward lighter options. This transition underscores the importance of hard seltzer as a bridge between traditional alcoholic beverages and the growing non alcoholic movement positioning it as a key player in the future of social drinking in the United States.

MARKET DRIVERS

Shift Toward Health Conscious Consumption and Low Calorie Preferences

The profound shift toward health conscious consumption and the increasing preference for low calorie alcoholic beverages is driving the growth of the United States hard seltzer market. Modern consumers are scrutinizing nutritional labels more closely than ever before seeking products that fit within their dietary goals without sacrificing social enjoyment. Hard seltzers typically contain between 90 and 100 calories per can and zero grams of sugar making them an attractive alternative to beer and wine which often have higher caloric and carbohydrate contents. According to the International Food Information Council more than 70 percent of Americans are trying to limit or avoid sugars in their diet a trend that directly benefits the hard seltzer category. The rise of fitness culture and the popularity of diets such as keto and paleo have further amplified this demand as these regimes strictly regulate carbohydrate intake. Gen Z and Millennial consumers are more likely than older generations to prioritize health-conscious attributes when selecting food and beverages. This demographic dominance ensures a sustained base of consumers who view hard seltzer not just as a drink but as a lifestyle choice. Additionally the transparency of ingredients in hard seltzers appeals to consumers who are wary of artificial additives and preservatives commonly found in other alcoholic beverages. As per the USDA Economic Research Service the demand for clean label products continues to grow across all food and beverage categories. This alignment with broader health trends positions hard seltzer as a preferred option for those seeking balance between indulgence and wellness.

Expansion of Flavor Innovation and Product Diversification

Flavor innovation and product diversification is propelling the expansion of the United States hard seltzer market. These strategies work by continuously refreshing consumer interest and expanding the addressable audience. Initially dominated by basic fruit flavors such as lime and black cherry the category has evolved to include exotic and complex profiles such as yuzu mango hibiscus and even dessert inspired tastes. This evolution keeps the product line exciting and encourages repeat purchases from consumers eager to try new experiences. According to the Specialty Food Association innovative flavor combinations are a key factor in driving trial and loyalty in the beverage sector. Brands are also experimenting with functional ingredients such as adaptogens caffeine and probiotics creating hybrid products that offer additional benefits beyond hydration and intoxication. Data from NielsenIQ indicates that new product launches with unique flavor profiles often see higher initial sales velocities compared to standard offerings. The introduction of variety packs allows consumers to sample multiple flavors reducing the risk of commitment and enhancing the discovery process. Furthermore seasonal limited edition releases create a sense of urgency and exclusivity driving spikes in demand during specific periods. As per the Beverage Marketing Corporation the ability to rapidly iterate on flavor trends allows hard seltzer brands to stay relevant in a fast moving market. This continuous cycle of innovation ensures that the category remains vibrant and appealing to a broad spectrum of tastes preventing stagnation and fostering long term growth.

MARKET RESTRAINTS

Market Saturation and Intense Competitive Pressure

Market saturation and intense competitive pressure are hampering the growth of the United States hard seltzer market. This is happening because the barrier to entry for new brands remains relatively low. The initial success of the category led to an influx of competitors ranging from established beer giants to startup breweries resulting in a crowded shelf space that makes differentiation difficult. According to the Beer Institute the number of hard seltzer brands available in the US has multiplied several fold in recent years leading to fragmentation of consumer attention. This oversupply often results in price wars and heavy promotional spending which can erode profit margins for both large and small players. Research shows that while volume sales remain strong the rate of growth has slowed as the market matures and early adopters stabilize their consumption habits. Retailers are becoming more selective about which brands to carry due to limited shelf space leading to challenges for smaller brands trying to gain visibility. As per the Federal Trade Commission increased competition has also led to stricter scrutiny of marketing claims and labeling practices adding compliance costs for manufacturers. The sheer volume of options can also lead to consumer fatigue where shoppers feel overwhelmed by choices and revert to familiar legacy brands. This dynamic creates a challenging environment for new entrants and forces existing players to invest heavily in marketing and innovation to maintain relevance. The resulting consolidation trend may limit diversity in the long run as larger companies acquire successful niche brands to secure their position.

Regulatory Scrutiny and Labeling Compliance Issues

Regulatory scrutiny and labeling compliance issues are restricting the U.S. hard seltzer market. This stems from authorities tightening rules on alcohol content and ingredient disclosure. The Alcohol and Tobacco Tax and Trade Bureau TTB has implemented stricter guidelines for labeling particularly regarding the source of alcohol and the use of terms such as natural or craft. According to the TTB mislabeling or misleading claims can result in significant fines and product recalls which damage brand reputation and consumer trust. Many hard seltzers are made from fermented cane sugar rather than malted barley which affects how they are classified and taxed under federal law. This distinction requires careful navigation to ensure compliance with both federal and state regulations which can vary significantly. Data from the Small Business Administration indicates that regulatory compliance costs can be disproportionately high for smaller producers who lack the legal resources of larger corporations. Additionally there is growing pressure from health advocacy groups to require clearer warning labels about the health risks associated with alcohol consumption. As per the Centers for Disease Control and Prevention increased awareness of alcohol related health issues may lead to stricter advertising restrictions and higher taxes. These regulatory hurdles increase operational complexity and cost potentially slowing down product launches and innovation. The uncertainty surrounding future regulations creates a cautious business environment where companies must balance agility with strict adherence to evolving legal standards.

MARKET OPPORTUNITIES

Development of Premium and Craft Hard Seltzer Segments

The development of premium and craft hard seltzer segments offers a significant opportunity for the United States market. This shift can elevate its value proposition and attract discerning consumers. The mainstream market is becoming saturated, leading to a growing demand for higher-quality products. Consumers are specifically looking for items with organic ingredients, real fruit juice, and unique botanicals. According to the Specialty Food Association premium beverages are experiencing robust growth as consumers seek authenticity and superior taste experiences. Craft hard seltzers often differentiate themselves through small batch production methods and artisanal branding which appeals to shoppers willing to pay a premium for perceived quality. A study confirms that while total volume in alcohol has seen slight declines, "Dollar Growth" remains positive due to consumers "trading up" to premium-priced spirits and seltzers. This trend, often called "drinking less but better," sees premium segments outperforming value tiers by 2–4 percentage points in revenue growth. This shift allows brands to escape the race to the bottom on price and build stronger emotional connections with their audience. Furthermore the integration of sustainable packaging such as aluminum cans and recyclable materials aligns with the values of environmentally conscious buyers. Research indicates that sustainability-marketed products are outperforming their conventional counterparts in growth and consumer retention. By focusing on quality craftsmanship and ethical practices premium hard seltzer brands can carve out a distinct niche that commands higher margins and fosters dedicated followings. This strategic pivot toward premiumization provides a pathway for sustained profitability and differentiation in a crowded marketplace.

Integration of Functional Ingredients and Wellness Benefits

The integration of functional ingredients and wellness benefits provides a clear path for the expansion of the United States hard seltzer market. This allows the sector to expand beyond traditional alcoholic consumption. Consumers are increasingly seeking beverages that offer additional health advantages such as hydration stress relief or energy boosting properties. According to the Global Wellness Institute the wellness economy is growing rapidly with functional beverages representing a key segment of this expansion. Hard seltzer brands are incorporating ingredients like electrolytes CBD ashwagandha and green tea extract to create products that support mental and physical well being. Data from the International Food Information Council indicates that a majority of consumers are interested in functional foods and drinks that provide specific health benefits. This trend allows hard seltzers to compete with non alcoholic functional beverages and energy drinks broadening their usage occasions beyond social drinking. For instance caffeinated hard seltzers appeal to consumers looking for a lighter alternative to high calorie energy drinks while maintaining alertness. As per the National Institutes of Health interest in natural remedies and adaptogens is rising particularly among younger demographics who prioritize holistic health. By positioning hard seltzers as functional wellness products brands can attract health focused consumers who might otherwise avoid alcohol. This innovation opens new revenue streams and enhances the perceived value of the product transforming it from a simple recreational drink into a lifestyle enhancer.

MARKET CHALLENGES

Supply Chain Volatility and Ingredient Sourcing Challenges

Supply chain volatility and ingredient sourcing challenges are impeding the growth of the United States hard seltzer market. This affects production consistency and cost stability. The production of hard seltzer relies on a steady supply of high quality carbonated water fruit concentrates and alcohol bases which are subject to agricultural and logistical fluctuations. According to the US Department of Agriculture extreme weather events and climate change can disrupt crop yields leading to shortages and price spikes for key fruit ingredients. For example poor harvests of berries or citrus can significantly impact the availability and cost of popular flavors. Data from the Bureau of Labor Statistics shows that input costs for food and beverage manufacturing have risen due to inflation and transportation bottlenecks squeezing profit margins for producers. The reliance on imported ingredients for certain exotic flavors further exposes manufacturers to currency fluctuations and trade policy changes. As per the National Association of Manufacturers supply chain disruptions have become more frequent requiring companies to hold larger inventories or diversify suppliers which increases storage costs. Additionally the shortage of aluminum cans and other packaging materials has previously caused delays and forced brands to limit production. These vulnerabilities make long term planning difficult and can lead to inconsistent product availability on shelves. The need to balance cost efficiency with quality assurance in a volatile supply environment remains a critical operational hurdle for hard seltzer manufacturers striving to maintain competitiveness and consumer trust.

Consumer Fatigue and Shifting Taste Preferences

Consumer fatigue and shifting taste preferences are serious barriers to the United States hard seltzer market. This is happening as the novelty of the category wears off. After years of rapid growth some consumers are becoming bored with the standard flavor profiles and are seeking new beverage experiences. According to the Beverage Marketing Corporation the rate of new trial for hard seltzers has declined as the market matures and early adopters move on to other trends. This shift requires brands to continuously innovate to keep consumers engaged which can be costly and risky. The rise of alternative beverages such as ready to drink cocktails non alcoholic beers and kombucha further fragments the market and draws attention away from hard seltzers. As per the National Restaurant Association bars and restaurants are diversifying their menus to include a wider variety of low alcohol and non alcoholic options reducing the dominance of hard seltzers in social settings. Additionally some consumers are criticizing the artificial aftertaste of certain hard seltzers preferring more natural tasting alternatives. This evolving landscape demands that hard seltzer brands remain agile and responsive to changing consumer sentiments. Failure to adapt to these shifting preferences can result in declining sales and loss of market share to more innovative or authentic competitors.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.75% |

| Segments Covered | By Packaging, ABV Content, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Anheuser Busch InBev, Boston Beer Company (Truly), Mark Anthony Brands (White Claw), Molson Coors Beverage Company (Vizzy), Heineken N.V., The Coca Cola Company (Topo Chico Hard Seltzer), Constellation Brands, Diageo (Smirnoff Seltzers), Pabst Brewing Co., Bon & Viv, Crook & Marker, Press Premium Alcohol Seltzer, Bud Light Seltzer, REZ Hard Seltzer, and New Belgium Brewing Company |

SEGMENTAL ANALYSIS

By Packaging Insights

The metal cans segment dominated the United States hard seltzer market and accounted for a substantial share in 2025. This dominance of the segment is mainly driven by its unmatched portability and strong environmental sustainability credentials which align with the values of modern consumers. Aluminum cans are lightweight durable and infinitely recyclable making them the preferred choice for outdoor activities such as beach trips hiking and festivals where glass is often prohibited. According to the Aluminum Association, the consumer recycling rate for aluminum cans is approximately 45-49%, which remains significantly higher than the rates for plastic (PET) and glass. This high recyclability appeals to environmentally conscious millennials and Gen Z consumers who prioritize brands with sustainable practices. Data from the Environmental Protection Agency indicates that recycling aluminum saves 95 percent of the energy required to make new material from virgin ore further enhancing its eco friendly appeal. The compact shape of cans also allows for efficient storage and transportation reducing logistics costs for manufacturers and retailers. As per the Beverage Marketing Corporation the convenience of single serve cans fits perfectly with the on the go lifestyle of target demographics who value ease of consumption. Furthermore cans provide superior protection against light and oxygen ensuring product freshness and flavor integrity over time. This combination of functional benefits and environmental responsibility solidifies the dominance of metal cans in the hard seltzer packaging landscape. The dominance of metal cans is further reinforced by their superior branding capabilities and rapid cooling efficiency which enhance consumer appeal and purchase intent. Aluminum cans offer a 360 degree canvas for vibrant graphics and innovative designs allowing brands to stand out in crowded retail environments. According to the Can Manufacturers Institute the print quality on aluminum allows for high resolution imagery and tactile finishes that attract attention on shelves. This visual appeal is crucial in a market driven by novelty and aesthetic presentation. Additionally aluminum has high thermal conductivity meaning cans chill faster than glass or plastic bottles providing immediate refreshment which is a key selling point for cold beverages. The ability to stack cans efficiently also maximizes shelf space utilization for retailers encouraging prominent placement and promotional displays. As per the Specialty Food Association the tactile experience of holding a cold can enhances the sensory enjoyment of the beverage contributing to overall satisfaction. These factors combine to make metal cans not just a container but a strategic marketing tool that drives sales and brand loyalty in the competitive hard seltzer sector.

The glass bottles segment is estimated to register the fastest CAGR of 17.5% from 2026 to 2034 due to the premiumization trend and the desire for a craft aesthetic among discerning consumers. Glass is increasingly used by boutique and craft brands to signal higher quality and sophistication. According to the Glass Packaging Institute glass is perceived as a premium material that preserves the purity of flavor without any risk of metallic aftertaste which can be a concern with aluminum. This perception appeals to consumers willing to pay a premium for a more refined drinking experience. The transparency of glass allows consumers to see the clarity and color of the liquid which can be a marketing advantage for brands using natural fruit juices or unique botanicals. As per the Specialty Food Association the weight and feel of a glass bottle convey substance and quality enhancing the perceived value of the product. This segment is particularly strong in urban markets and upscale restaurants where presentation matters. The growth of glass bottles reflects a bifurcation in the market where mass convenience coexists with a rising demand for artisanal and luxury experiences. Furthermore, the rapid growth of the glass bottle segment is also fueled by reusability trends and the shift toward home consumption where durability and aesthetics are valued. Consumers are increasingly purchasing multi pack glass bottles for home gatherings and dinner parties where the beverage is served in glasses rather than consumed directly from the container. According to the National Restaurant Association the rise of home entertaining has led to increased sales of premium packaged beverages that look attractive on dining tables. Glass bottles are often designed with resealable caps allowing for partial consumption and storage which is not possible with standard cans. Data from the Bureau of Labor Statistics shows that spending on alcoholic beverages for home consumption has risen as consumers seek restaurant quality experiences at home. The ability to recycle glass indefinitely without loss of quality also appeals to eco conscious buyers who view it as a sustainable option despite its heavier weight. The combination of aesthetic appeal functional resealability and sustainability credentials drives the accelerated adoption of glass bottles in the hard seltzer market particularly among older and more affluent demographics.

By ABV Content Insights

The less than 5% ABV segment led the United States hard seltzer market and captured a significant share in 2025 because it aligns perfectly with the growing consumer preference for moderation and health conscious lifestyles. Most mainstream hard seltzers feature an ABV between 4 and 5 percent which provides a mild intoxicating effect without the heavy calories or impairment associated with stronger drinks. According to the National Institute on Alcohol Abuse and Alcoholism there is a rising trend toward mindful drinking where consumers seek to limit their alcohol intake while still participating in social rituals. This demographic prefers beverages that allow them to maintain control and avoid hangovers making lower ABV options highly attractive. Data from the Centers for Disease Control and Prevention indicates that a significant portion of adults are actively monitoring their alcohol consumption for health reasons. The lower alcohol content also means fewer calories per serving which complements the low calorie positioning of hard seltzers. As per the International Food Information Council consumers are increasingly looking for products that support their wellness goals including weight management and mental clarity. The 5 percent threshold is widely accepted as the standard for sessionable drinks that can be enjoyed over longer periods without excessive intoxication. This balance of enjoyment and responsibility ensures that the less than 5 percent ABV segment remains the dominant choice for the majority of hard seltzer drinkers. The top position of the less than 5 percent ABV segment is further supported by regulatory ease and broad retail accessibility which facilitate widespread distribution and consumption. In many US states beverages with an ABV below 5 percent are classified similarly to beer allowing them to be sold in grocery stores convenience stores and gas stations without the restrictions applied to higher proof spirits. According to the Alcohol and Tobacco Tax and Trade Bureau this classification simplifies licensing requirements for retailers making it easier for hard seltzers to achieve ubiquitous presence. Data from the National Association of Convenience Stores shows that lower ABV beverages have higher turnover rates and broader appeal across diverse age groups within the legal drinking age. This accessibility ensures that hard seltzers are available wherever consumers shop for everyday items increasing impulse purchases. As per the Beverage Information Group the ease of purchase contributes significantly to volume sales as consumers do need to visit specialized liquor stores. The lower tax burden on beverages under 5 percent ABV also allows for competitive pricing making them affordable for regular consumption. These structural advantages create a favorable environment for the less than 5 percent segment to maintain its leadership by maximizing availability and minimizing barriers to entry for consumers.

The more than 5% ABV segment is anticipated to witness the fastest CAGR of 24.6% during the forecast period owing to consumer demand for higher potency and better value perception. Some consumers are seeking stronger alternatives as the market matures. They want a more pronounced effect similar to beer or wine, while maintaining a low-calorie profile. According to DISCUS, while premium RTD cocktails are growing rapidly, the primary consumer interest is in high-quality, spirit-based versions of classic cocktails that offer convenience and consistent flavor profiles rather than just "high-strength" efficiency. Brands are launching hard seltzers with ABV levels ranging from 6 to 8 percent or even higher appealing to drinkers who want fewer cans to achieve the desired level of intoxication. The higher ABV also allows brands to differentiate themselves in a saturated market by targeting a niche audience of experienced drinkers. This shift reflects a segmentation of the market where convenience meets strength driving rapid growth in the higher ABV category. Innovation in malt based and spirit based formulations is accelerating the growth of the more than 5 percent ABV segment as producers experiment with different alcohol sources to achieve higher strengths without compromising taste. Traditional hard seltzers made from fermented sugar often struggle to reach higher ABV levels without affecting flavor so manufacturers are turning to malted barley or neutral spirits. According to the Brewers Association malt based hard seltzers can achieve higher alcohol content while maintaining a clean taste profile similar to light beers. Data from the Beer Institute shows that malt based innovations are expanding the definition of hard seltzer and attracting beer drinkers looking for lighter alternatives. Spirit based seltzers which use vodka or other distilled alcohols also offer a smoother mouthfeel at higher ABVs appealing to cocktail enthusiasts. As per the Beverage Marketing Corporation these formulation advancements allow for greater flexibility in product development enabling brands to create robust flavors that stand up to higher alcohol levels. The introduction of these varied bases broadens the appeal of high ABV seltzers and drives experimentation among consumers. This technical innovation supports the rapid expansion of the segment by offering diverse and satisfying options for those seeking stronger beverages.

By Distribution Channel Insights

The Off-Trade channel segment held the majority share of the United States hard seltzer market in 2025. This supremacy of the segment is credited to the convenience it offers and the prevalence of volume purchasing habits. Consumers prefer buying hard seltzers in multi packs for home consumption parties and casual gatherings which is facilitated by the wide availability of these products in retail outlets. According to the Food Marketing Institute off trade sales account for the majority of alcoholic beverage revenue as shoppers appreciate the ability to compare prices and choose from a wide variety of brands in one location. The ease of accessing hard seltzers during routine grocery shopping trips integrates the product into weekly household budgets. The ability to purchase cold single serves or large cases provides flexibility for different usage occasions. This accessibility and economic advantage ensure that off trade remains the primary conduit for hard seltzer distribution capturing the bulk of consumer demand. The dominance of the Off-Trade channel is further reinforced by the extensive shelf space and visibility dedicated to hard seltzers in major retail chains. Retailers recognize the high turnover rate of hard seltzers and allocate prime real estate such as end caps and eye level shelves to maximize sales. According to the National Association of Convenience Stores strategic placement significantly influences purchase decisions with visible products experiencing higher sales volumes. Data from IRI indicates that hard seltzers often feature in seasonal displays and promotional flyers attracting attention from casual shoppers. The variety of flavors and brands available in off trade stores allows consumers to explore new options without commitment fostering trial and discovery. As per the Specialty Food Association the competitive retail environment encourages brands to invest in packaging and point of sale materials that enhance visibility. The presence of knowledgeable staff in liquor stores also aids in guiding consumers toward new or premium brands. This robust retail infrastructure ensures that hard seltzers remain top of mind for consumers sustaining the leadership of the off trade channel through constant exposure and accessibility.

The On-Trade channel segment is likely to experience the fastest CAGR of 15.5% over the forecast period. This rapid expansion of the segment is fuelled by the desire for social experiences and immediate consumption. Pandemic restrictions eased, prompting consumers to return to venues for socializing. Consequently, on-premise drinking surged. According to the National Restaurant Association on trade sales of ready to drink beverages including hard seltzers have rebounded strongly as patrons seek convenient and refreshing options while out. Data from Technomic indicates that hard seltzers are increasingly featured on cocktail menus and as standalone offerings appealing to guests who prefer light and easy to drink beverages. The social atmosphere of bars and clubs encourages trial of new brands and flavors often influenced by peer recommendations and bartender suggestions. The immediacy of consumption in these venues drives higher frequency of purchase compared to home use. This revival of social drinking culture propels the on trade segment as a key growth engine for the industry. Rapid growth in the On-Trade segment is also fueled by premium pricing strategies and higher margin opportunities for establishments. Bars and restaurants can charge a premium for hard seltzers served in branded glassware or as part of curated flight experiences enhancing perceived value. According to the National Restaurant Association beverage margins in on trade settings are typically higher than food margins making hard seltzers an attractive addition to menus. Data from Technomic shows that consumers are willing to pay more for convenience and ambiance leading to increased average check sizes. Establishments are leveraging this by offering exclusive or limited edition hard seltzers that are not available in retail stores creating a sense of exclusivity. As per the Specialty Food Association the ability to upsell hard seltzers with food pairings further boosts revenue. The professional presentation and service quality in on trade venues justify higher prices driving revenue growth for both vendors and venues. This economic incentive encourages widespread adoption of hard seltzers in hospitality settings accelerating the expansion of the on trade channel.

COUNTRY LEVEL ANALYSIS

The United States was the top performer in the North American hard seltzer market in 2025 because of its pioneering role in popularizing the category. This market has reached a state of maturity and consolidation, resulting in dominant, established brands and highly innovative, niche competitors. The position of the US is underpinned by a strong cultural emphasis on health and wellness which drove the initial explosion of hard seltzer popularity. According to the Beverage Marketing Corporation the US hard seltzer market has evolved from a niche trend to a mainstream staple with widespread acceptance across demographics. The regulatory framework supports the production and sale of these beverages with clear guidelines for labeling and taxation. Data from the Alcohol and Tobacco Tax and Trade Bureau shows that the US has a robust infrastructure for alcoholic beverage distribution ensuring nationwide availability. The presence of major beverage conglomerates has stabilized the market while fostering continuous innovation in flavors and formats. As per the Distilled Spirits Council of the United States the country remains the primary driver of global hard seltzer trends influencing product development and marketing strategies worldwide. The mature nature of the US market provides a benchmark for other regions aspiring to develop their own hard seltzer sectors. Furthermore, the main driving factor for the United States hard seltzer market is the enduring consumer preference for low calorie and low sugar alcoholic beverages amidst a broader health consciousness movement. Data from the International Food Information Council reveals that over 70 percent of consumers are trying to limit sugar consumption making hard seltzers an ideal alternative to sugary cocktails and beers. The demographic shift toward younger drinkers who prioritize transparency and natural ingredients further supports this trend. As per the Pew Research Center millennials and Gen Z constitute a significant portion of alcohol consumers and are more likely to choose beverages that align with their wellness values. The widespread availability of hard seltzers in retail and on trade channels ensures easy access for these consumers. Additionally the innovation in flavors and functional ingredients keeps the category fresh and engaging. The combination of health benefits convenience and variety ensures that the United States remains the central hub for hard seltzer consumption and innovation driving continued market stability and growth.

COMPETITIVE LANDSCAPE

The competition in the United States hard seltzer market is intense and characterized by a mix of established beverage giants and agile craft breweries vying for consumer attention. Major players compete fiercely on brand identity flavor innovation and pricing strategies to differentiate their offerings in a crowded marketplace. The initial surge in popularity has led to market saturation prompting companies to focus on niche segments such as premium organic or high alcohol content variants. Private label brands from major retailers also pose a significant threat by offering lower priced alternatives that appeal to budget conscious shoppers. Innovation in packaging and sustainability has become a key battleground as consumers increasingly prioritize eco friendly practices. Marketing efforts emphasize lifestyle alignment and social responsibility to build emotional connections with target audiences. The ease of entry for new brands ensures continuous disruption requiring incumbents to remain agile and responsive to changing trends. This dynamic environment drives constant evolution in product offerings and promotional tactics ensuring that only the most adaptable and innovative firms thrive in the competitive landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. hard seltzer market are

- Anheuser Busch InBev

- Boston Beer Company (Truly)

- Mark Anthony Brands (White Claw)

- Molson Coors Beverage Company (Vizzy)

- Heineken N.V.

- The Coca Cola Company (Topo Chico Hard Seltzer)

- Constellation Brands

- Diageo (Smirnoff Seltzers)

- Pabst Brewing Co.

- Bon & Viv

- Crook & Marker

- Press Premium Alcohol Seltzer

- Bud Light Seltzer

- REZ Hard Seltzer

- New Belgium Brewing Company

Top Players in the Market

- Mark Anthony Brands International revolutionized the United States hard seltzer market with its flagship White Claw brand which defined the category and spurred widespread adoption. The company focuses on maintaining product consistency and broad distribution to ensure availability across all retail channels. Recent actions include expanding flavor portfolios with seasonal limited editions and investing in sustainable packaging initiatives. Mark Anthony leverages strong brand recognition to dominate shelf space and maintain consumer loyalty through targeted digital marketing campaigns. The company continues to innovate with new formats such as larger cans and variety packs to meet diverse consumer preferences. By prioritizing quality and authenticity Mark Anthony solidifies its position as a pioneer in the industry while adapting to evolving market trends and competitive pressures to sustain long term growth and relevance.

- Boston Beer Company contributes significantly to the market through its Truly Hard Seltzer brand which emphasizes organic ingredients and unique flavor combinations. The company targets health conscious consumers by offering gluten free and low calorie options that align with modern wellness trends. Recent strategies include launching craft inspired flavors and collaborating with local artists for distinctive packaging designs. Boston Beer Company invests heavily in direct to consumer sales channels and e commerce platforms to enhance customer engagement. The firm also focuses on sustainability by using recycled materials in production and reducing carbon footprints. These efforts strengthen its reputation as an innovative and responsible player in the hard seltzer sector appealing to discerning drinkers who value transparency and environmental stewardship in their beverage choices.

- Anheuser Busch InBev leverages its extensive brewing expertise and distribution network to compete effectively in the United States hard seltzer market with brands like Bon & Viv and SpikedSeltzer. The company utilizes its massive scale to ensure widespread availability and competitive pricing across various retail outlets. Recent actions include reformulating products to improve taste profiles and introducing higher alcohol content options to cater to diverse preferences. Anheuser Busch InBev invests in aggressive marketing campaigns featuring high profile endorsements and social media engagement to boost brand visibility. The company also explores partnerships with entertainment venues and festivals to increase on premise consumption. By combining operational efficiency with strategic marketing Anheuser Busch InBev maintains a strong presence in the competitive landscape while driving innovation and consumer interest in its hard seltzer offerings.

Top Strategies Used by Key Market Participants

Key players in the United States hard seltzer market primarily focus on flavor innovation and product diversification to capture consumer interest and drive repeat purchases. Companies frequently introduce limited edition and seasonal flavors to create urgency and excitement among shoppers. Strategic expansion into premium and craft segments allows brands to appeal to discerning consumers seeking higher quality ingredients and unique experiences. Sustainability initiatives such as using recyclable packaging and reducing water usage are increasingly adopted to enhance brand image and meet environmental standards. Digital marketing and social media engagement are utilized extensively to build brand communities and reach younger demographics through influencer collaborations. Additionally firms invest in supply chain optimization to ensure consistent product availability and cost efficiency. Price competitiveness and promotional bundles remain crucial for maintaining market presence and attracting budget conscious buyers in a saturated retail environment.

MARKET SEGMENTATION

This research report on the U.S. hard seltzer market is segmented and sub-segmented into the following categories.

By Packaging

- Glass Bottles

- Metal Cans

- Plastic Bottles

By ABV Content

- Less Than 5%

- More Than 5%

By Distribution Channel

- Off-trade

- On-trade

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1. What is the U.S. hard seltzer market?

The U.S. hard seltzer market includes alcoholic sparkling water beverages that are typically made with carbonated water, alcohol, and fruit flavorings.

2. What factors are driving the growth of the U.S. hard seltzer market?

Growing consumer preference for low calorie alcoholic beverages, rising demand for flavored drinks, and increasing health consciousness are major growth drivers.

3. What are the common flavors available in hard seltzer products?

Popular flavors include lemon, lime, mango, berry, watermelon, pineapple, grapefruit, black cherry, and mixed fruit combinations.

4. Why is hard seltzer popular among consumers?

Hard seltzer is popular because it generally contains lower calories, lower sugar content, and lighter alcohol content compared to many traditional alcoholic beverages.

5. Which packaging formats are commonly used in the hard seltzer market?

Metal cans are the most widely used packaging format due to their convenience, portability, and sustainability benefits.

6. Which distribution channels are important in the U.S. hard seltzer market?

Major distribution channels include supermarkets, liquor stores, convenience stores, bars, restaurants, and online retail platforms.

7. How are health and wellness trends influencing the hard seltzer market?

Consumers are increasingly seeking gluten free, low carbohydrate, low calorie, and natural ingredient alcoholic beverages, supporting market expansion.

8. What challenges affect the U.S. hard seltzer market?

Challenges include intense market competition, changing consumer preferences, product saturation, and regulatory restrictions related to alcoholic beverages.

9. How is product innovation shaping the hard seltzer market?

Manufacturers are introducing new flavors, premium ingredients, seasonal editions, and higher alcohol variants to attract consumers and strengthen brand loyalty.

10. Who are the leading companies in the U.S. hard seltzer market?

Major companies include Anheuser Busch InBev, Boston Beer Company, Mark Anthony Brands, and Molson Coors Beverage Company.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com