U.S. Honey Market Size, Share, Trends & Growth Forecast Report By Type, By Application, By Packaging, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Honey Market Size

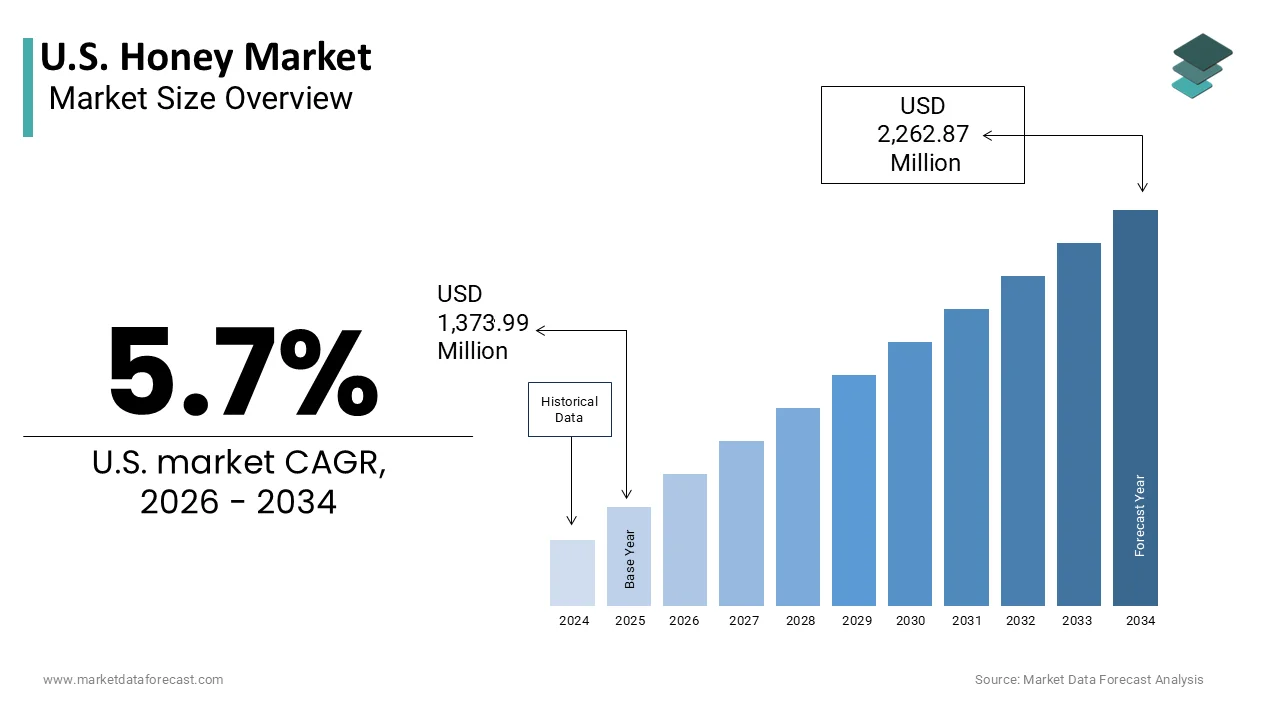

The United States Honey Market was valued at USD 1,373.99 million in 2025, is estimated to reach USD 1,452.31 million in 2026, and is projected to reach USD 2,262.87 million by 2034, growing at a CAGR of 5.7% from 2026 to 2034.

Honey is a thick, viscous, sweet liquid produced by bees from flower nectar, serving as a primary natural sweetener and ingredient in food and medicine. This market is integral to both the culinary landscape and the agricultural ecosystem, serving as a primary natural sweetener and a critical component in pollination services. Honey is valued for its unique flavor profiles, which vary based on floral sources such as clover, wildflower, and orange blossom, as well as its perceived health benefits over refined sugars. According to the United States Department of Agriculture (USDA), domestic honey production has declined significantly in recent years, dropping to a record low of 116 million pounds in 2025, largely driven by environmental stressors and reduced colony yields. As per the USDA Economic Research Service, per capita consumption of honey in the United States reached a record high of 2.0 pounds annually in 2024, reflecting a rapidly growing consumer preference for natural ingredients. The market structure is characterized by a mix of small-scale local apiaries and large commercial operations that supply bulk honey to food manufacturers. Regulatory frameworks enforced by the Food and Drug Administration ensure labeling accuracy and quality standards, addressing concerns regarding adulteration. The industry also plays a vital role in supporting biodiversity, as healthy bee populations are essential for the reproduction of many crops. Consumer trends indicate a shift toward premium, raw, and locally sourced honey varieties, driven by awareness of sustainability and nutritional value. This dynamic environment requires stakeholders to navigate complex supply chain challenges while meeting evolving dietary preferences.

MARKET DRIVERS

Rising Consumer Preference for Natural Sweeteners

The increasing consumer preference for natural sweeteners serves as a primary driver for the United States honey market. This trend is fueled by individuals seeking healthier alternatives to refined sugar and artificial additives. Health consciousness has surged among Americans, leading to a reevaluation of dietary choices and a reduction in processed sugar intake. According to the International Food Information Council, a significant majority of consumers are actively trying to limit their consumption of added sugars, prompting a shift toward natural options like honey. As per NielsenIQ data, sales growth rates of natural sweeteners have outpaced those of traditional white sugar in various retail categories, indicating a robust demand trajectory. Honey is perceived not only as a sweetener but also as a functional food with antioxidant and antimicrobial properties, enhancing its appeal to health-focused demographics. The clean label movement further supports this trend, with shoppers scrutinizing ingredient lists for recognizable and minimally processed components. Food and beverage manufacturers are responding by reformulating products to include honey, thereby attracting health-conscious buyers. The versatility of honey in applications ranging from breakfast cereals to salad dressings ensures its widespread adoption. Additionally, the rise of plant-based diets has elevated the status of honey as a preferred natural energy source. This cultural shift toward wellness and transparency in food sourcing sustains strong demand for honey across multiple consumer segments.

Expansion of Organic and Premium Honey Segments

The expansion of organic and premium honey segments is also boosting the growth of the United States honey market. This expansion caters to discerning consumers willing to pay for quality and authenticity. There is a growing segment of shoppers who prioritize organic certification, believing it ensures higher safety standards and environmental sustainability. According to the Organic Trade Association, sales of organic food products continue to grow, with organic honey representing a notable niche within this category. As per Specialty Food Association statistics, premium and artisanal honey varieties are experiencing double-digit growth rates, driven by consumers seeking unique flavor experiences and traceable origins. Local and regional honey brands benefit from the farm-to-table movement, which emphasizes community support and reduced carbon footprints. Retailers are expanding their offerings of single-origin and raw honey to meet this demand, often highlighting specific floral sources such as manuka or acacia. The willingness of consumers to pay a premium for these specialized products encourages producers to invest in high-quality processing and packaging. Certification programs and third-party validations enhance consumer trust, differentiating authentic products from commoditized blends. This trend toward premiumization allows smaller apiaries to compete effectively against large-scale producers by emphasizing craftsmanship and purity. The desire for transparency in sourcing further fuels the growth of this segment, as buyers seek to connect with the stories behind their food.

MARKET RESTRAINTS

Prevalence of Honey Adulteration and Fraud

The prevalence of honey adulteration and fraud acts as a serious hurdle for the United States honey market. This hinders consumer trust and distorts pricing mechanisms. Adulteration involves the addition of cheap syrups such as high fructose corn syrup or rice syrup to pure honey, which dilutes the quality and misleads buyers. According to the Food and Drug Administration (FDA), approximately 10 percent of imported honey samples tested positive for undeclared sweeteners in a 2021–2022 sampling assignment, raising concerns about product integrity. As per the Food and Drug Administration, detecting these adulterants requires sophisticated testing methods that are not always routinely applied, allowing fraudulent products to enter the supply chain. This issue disproportionately affects domestic producers who adhere to strict quality standards but struggle to compete with lower-priced imports. Consumers become skeptical of honey labels, potentially reducing overall consumption or shifting to alternative sweeteners. The lack of uniform global standards for honey purity complicates enforcement and verification efforts. Industry groups advocate for stricter testing protocols and mandatory origin labeling to combat this problem. However, the cost of compliance and testing can be prohibitive for smaller operators. The presence of adulterated honey in the market creates an uneven playing field, discouraging investment in high-quality production. The threat of fraud remains a persistent barrier to market confidence and growth. This will continue until robust verification systems are universally adopted.

Declining Bee Populations and Environmental Stressors

Declining bee populations and environmental stressors pose a major barrier to the United States honey market. This threatens the stability of domestic production. Colony Collapse Disorder, pesticide exposure, habitat loss, and climate change have contributed to substantial losses in honey bee colonies across the country. According to the United States Department of Agriculture, annual winter mortality rates for honey bee colonies have averaged around 30 percent in recent years, impacting the availability of bees for both honey production and pollination. As per the Xerces Society for Invertebrate Conservation, the reduction in diverse floral resources due to monoculture farming limits the nutritional intake of bees, weakening their immune systems. These environmental challenges increase operational costs for beekeepers who must invest in supplemental feeding and medical treatments to maintain hive health. The unpredictability of honey yields makes it difficult for producers to fulfill contracts and maintain consistent supply levels. Import reliance increases as domestic production falls short of demand, exposing the market to international price fluctuations and supply chain disruptions. The ecological crisis also raises public awareness about the fragility of the food system, prompting some consumers to reduce consumption out of ethical concern. Addressing these environmental issues requires coordinated efforts among policymakers, farmers, and researchers, but progress is slow. The vulnerability of bee populations thus remains a critical constraint on the long-term viability of the domestic honey industry.

MARKET OPPORTUNITIES

Integration of Honey in Functional Foods and Beverages

The integration of honey in functional foods and beverages offers a significant opportunity for the United States honey market. This leverages its health-promoting properties. Consumers are increasingly seeking products that offer benefits beyond basic nutrition, such as immune support and energy enhancement. According to a study, the functional food sector is evolving with a focus on 'Age Reframed' (longevity) and 'Eating, Optimised,' where natural ingredients are valued for their 'health halo.' While honey remains a popular natural sweetener, recent reports highlight rapid expansion in brain health and hydration formulations rather than honey-specific snacks. As per the Global Wellness Institute's 2022 trends, the demand for immunity-boosting products surged. However, their 2024-2025 reports now emphasize 'Food for Brain Health' and 'Hydration for an Extended Lifespan' as the leading drivers in the wellness economy. Manufacturers are developing honey-infused teas, energy bars, and probiotic drinks that appeal to health-conscious individuals. The natural antimicrobial and anti-inflammatory properties of honey make it an attractive ingredient for wellness-oriented products. Collaborations between honey producers and functional food brands can lead to innovative offerings that differentiate themselves in crowded markets. The versatility of honey allows it to be used in various formats, from liquid syrups to powdered extracts, enhancing its applicability in product development. Marketing campaigns that highlight the scientific benefits of honey can further drive consumer interest and adoption. This trend aligns with the broader movement toward preventive healthcare and natural remedies. The market can tap into new revenue streams by positioning honey as a functional ingredient. This strategy helps expand its presence beyond traditional culinary uses.

Growth of E-Commerce and Direct-to-Consumer Sales

The growth of e-commerce and direct-to-consumer sales provides a potential for the United States honey market. This enables producers to bypass traditional retail channels and connect directly with buyers. Online platforms allow small and medium-sized apiaries to reach a national audience, showcasing their unique stories and product qualities. According to the United States Census Bureau, retail e-commerce sales continued to grow, reaching approximately $1.23 trillion in 2025, with the 'Food and Beverage' category contributing to this expansion. Industry groups like the Specialty Food Association interpret this as a robust channel for specialty products. Sources indicate that platforms like Etsy and Amazon Handmade remain key channels for niche sellers, with Etsy hosting approximately 90 million active buyers. Direct-to-consumer models enable producers to retain higher margins by eliminating intermediaries and offering personalized customer experiences. Subscription services for monthly honey deliveries are gaining popularity, ensuring recurring revenue and customer loyalty. Social media marketing plays a crucial role in driving traffic to these online stores, allowing brands to engage with consumers through educational content and behind-the-scenes insights. The ability to provide detailed information about sourcing and production processes builds trust and transparency. Furthermore, e-commerce facilitates the sale of bundled gift sets and seasonal varieties, enhancing average order values. This digital transformation empowers local producers to compete with larger brands and expand their market reach efficiently.

MARKET CHALLENGES

Regulatory Complexity and Labeling Standards

Regulatory complexity and inconsistent labeling standards are key factors hampering the growth of the United States honey market. This creates confusion for consumers and compliance burdens for producers. The definition of honey and the requirements for labeling origin and contents vary across jurisdictions, complicating interstate and international trade. Groups like the American Beekeeping Federation argue that the FDA's non-binding guidelines on honey labeling are subject to interpretation, leading to discrepancies in how products are marketed. As per the American Beekeeping Federation and other industry watchdogs, the lack of a unified federal standard for defining pure honey allows for loopholes that can be exploited by bad actors. Producers must navigate a patchwork of state regulations in addition to federal requirements, increasing administrative costs and legal risks. The debate over whether certain processing methods disqualify honey from being labeled as raw or natural adds to the ambiguity. Consumers may become confused by conflicting claims on packaging, eroding trust in the category. Industry associations are advocating for clearer and more stringent regulations to protect the integrity of honey products. However, achieving consensus among stakeholders with diverse interests is challenging. The uncertainty surrounding regulatory enforcement can deter innovation and investment in new product lines. Ensuring compliance while maintaining competitive pricing requires careful strategic planning and legal expertise. This regulatory landscape remains a persistent hurdle for the industry as it seeks to establish clear and trustworthy standards.

Climate Change Impact on Floral Diversity

Climate change's impact on floral diversity further impedes the expansion of the United States honey market. This alters the availability and quality of nectar sources. Shifts in temperature and precipitation patterns affect the blooming cycles of plants, leading to mismatches between bee activity and flower availability. According to the U.S. Department of Agriculture and independent researchers, changing weather patterns (confirmed by NOAA data) have resulted in more frequent droughts and extreme weather events, which stress both bees and flora. As per the United States Department of Agriculture, environmental changes like rising CO₂ levels reduce the protein content of pollen available to bees, impacting the nutritional support available to colonies and their overall health. Monoculture farming practices exacerbate this issue by limiting the variety of food sources for bees throughout the season. The resulting honey may have inconsistent flavors and lower yields, affecting producer profitability. Adaptation strategies such as planting cover crops and restoring native habitats are necessary but require significant investment and time. The unpredictability of seasonal conditions makes long-term planning difficult for beekeepers. Furthermore, the migration of pests and diseases due to warmer climates adds another layer of complexity to hive management. Addressing these climate-related challenges requires collaborative efforts to promote sustainable agricultural practices and protect biodiversity. The resilience of the honey market depends on the ability of the industry to adapt to these evolving environmental conditions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, Packaging, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Nature Nate’s Honey Co., Sioux Honey Association Co-op, Barkman Honey LLC, Dutch Gold Honey Inc., GloryBee Inc., Bee Maid Honey Limited, Savannah Bee Company, Miller Honey Company, Golden Heritage Foods, Rice Honey LLC, Adee Honey Farms, Desert Creek Honey |

SEGMENTAL ANALYSIS

By Type Insights

The clover honey dominated the United States honey market and accounted for a 32.6% share in 2025. This dominance of the segment is driven by its mild flavor profile and widespread availability, making it the preferred choice for commercial food manufacturers and bakers. Its neutral taste allows it to sweeten products without overpowering other ingredients, which is essential for large-scale production of cereals, granola bars, and baked goods. The consistency in color and viscosity of clover honey makes it ideal for industrial applications where uniformity is critical. Major food corporations rely on this variety for its predictable performance in recipes and processing conditions. The extensive cultivation of clover as a cover crop and forage plant further supports the reliability of this honey type. Retailers also favor clover honey for their private label brands because of its broad consumer appeal and lower cost compared to specialty varieties. This economic efficiency and functional versatility ensure that clover honey remains the standard against which other types are measured. The entrenched position of clover honey in both retail and industrial sectors solidifies its leadership in the market. Consumer familiarity and price competitiveness are key factors driving the domination of clover honey in the US market. For decades, clover honey has been the default variety found in grocery stores, creating a strong brand recognition and habit among shoppers. The perception of clover honey as a staple household item ensures steady demand regardless of economic fluctuations. Marketing efforts by industry groups often feature clover honey as the representative image of honey, reinforcing its status as the archetypal product. Its light color and smooth texture appeal to a wide demographic, including children and families who prefer less intense flavors. The availability of clover honey in various package sizes, from single-serve packets to bulk containers, enhances its accessibility. This combination of affordability, familiarity, and versatility makes clover honey the go-to choice for everyday use. The lack of strong seasonal or regional limitations in its production further supports its year-round availability, maintaining its dominant position in the competitive landscape.

The specialty honeys segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 9.4% from 2026 to 2034 due to its recognized medicinal and functional properties. Consumers are increasingly seeking natural remedies for health issues such as sore throats, digestive problems, and skin conditions, driving demand for high-potency honeys. The scientific validation has transformed specialty honey from a culinary ingredient into a health supplement. Retailers are responding by dedicating shelf space to these premium products in the health and wellness aisles. The rise of self-care trends has further accelerated this growth, as individuals incorporate honey into their daily health routines. Online platforms provide detailed information about the Unique Manuka Factor ratings, educating consumers and building trust. The exclusivity and perceived efficacy of these honeys justify their higher prices, attracting affluent and health-conscious buyers. This shift toward functional nutrition ensures that specialty honeys continue to experience robust growth rates. Premiumization and the expansion of the gift market are significant drivers of the rapid growth in the specialty honey segment. High-end honeys such as Manuka, Acacia, and Sourwood are marketed as luxury items, appealing to consumers seeking unique gastronomic experiences. Packaging plays a crucial role in this segment, with elegant jars and branded presentations enhancing the perceived value. Specialty honey brands often emphasize their origin, harvesting methods, and sustainability practices, creating an emotional connection with buyers. The rise of e-commerce has facilitated the distribution of these niche products to a national audience, bypassing geographic limitations. Social media influencers and food bloggers highlight the unique flavors and uses of specialty honeys, driving awareness and desire. Corporate gifting programs also contribute to this growth, as businesses seek distinctive and high-quality presents for clients and employees. The ability of specialty honeys to command high margins encourages retailers and producers to invest in this segment. This combination of luxury positioning and strategic marketing ensures sustained expansion.

BY Application Insights

The food and beverages segment captured the majority share of 61.2% of the US honey market in 2025. This leading position of the segment is attributed to the versatile culinary applications of honey as a sweetener and ingredient. Honey is extensively used in baking, cooking, and beverage formulation, replacing refined sugar in many recipes for its distinct flavor and moisture-retaining properties. The clean label trend has encouraged manufacturers to use honey as a natural alternative to high fructose corn syrup, enhancing the health profile of their products. Consumer preference for natural ingredients in packaged foods drives demand for honey as a primary sweetener. The ability of honey to enhance flavor profiles in both sweet and savory dishes makes it indispensable in professional and home kitchens. Retail sales of honey are also driven by its use in household cooking, with many households keeping honey as a pantry staple. The integration of honey into popular dietary trends such as paleo and Whole30 further boosts its usage. This broad applicability across various food categories ensures that the food and beverages segment remains the dominant application area. The staple status of honey in household consumption significantly contributes to the dominance of the food and beverages segment. Honey is a traditional breakfast item, commonly used on toast, in yogurt, and with oatmeal, ensuring daily usage in millions of American homes. The perception of honey as a healthier sweetener for children drives its inclusion in family diets, particularly as parents seek to reduce processed sugar intake. Seasonal traditions such as using honey in holiday baking and teas during cold seasons also spike demand. The availability of honey in convenient formats such as squeeze bottles and single-serve packs facilitates its use in busy lifestyles. Educational campaigns by industry groups highlight the nutritional benefits of honey, reinforcing its position as a wholesome food choice. The cultural embedding of honey in American cuisine ensures that it remains a constant presence in grocery carts. This consistent household demand provides a stable foundation for the food and beverages segment, outweighing other applications in terms of volume and frequency.

The personal care and cosmetics segment is expected to exhibit a noteworthy CAGR of 4.5% during the forecast period, owing to natural skincare trends and the humectant properties of honey. Honey is widely recognized for its ability to retain moisture, soothe irritation, and promote healing, making it a valuable ingredient in lotions, masks, and lip balms. The antimicrobial properties of honey make it suitable for acne treatments and sensitive skin care, broadening its appeal. Brands are leveraging the clean beauty movement by highlighting honey as a safe and sustainable alternative to synthetic chemicals. The visual and textural appeal of honey in packaging and formulations enhances the sensory experience for users. Social media platforms showcase DIY honey skincare recipes, driving consumer interest and trial. The alignment with wellness and self-care trends ensures that honey-based personal care products continue to gain market share. This growth is supported by innovation in formulation technologies that stabilize honey extracts for cosmetic use. The expansion of organic and clean-label beauty products accelerates the growth of the personal care and cosmetics segment for honey. Consumers are increasingly scrutinizing ingredient lists, preferring products free from parabens, sulfates, and artificial fragrances. Brands are obtaining certifications to validate their claims, building trust with discerning buyers. The transparency of sourcing and the ethical implications of bee-friendly practices resonate with environmentally conscious consumers. Retailers are expanding their natural beauty sections, providing greater visibility for honey-based products. The versatility of honey allows it to be incorporated into a wide range of items, from shampoos to body scrubs. Collaborations between beekeepers and beauty brands create authentic stories that enhance brand value. The premium pricing of organic honey cosmetics supports higher margins for manufacturers. This shift toward conscientious consumption ensures that the personal care segment remains a dynamic and rapidly expanding area for honey application.

By Packaging Insights

The Glass jars segment was the largest segment in the US honey market and occupied a share of 44.6% in 2025. This prominence of the segment is supported by its premium perception and superior product preservation capabilities. Glass is inert and does not react with honey, ensuring that the flavor and quality remain intact over time. The transparency of glass allows shoppers to inspect the color and clarity of the honey, which is a key purchasing factor. Glass jars are also reusable and recyclable, aligning with sustainability goals that are increasingly important to buyers. Retailers favor glass packaging for its aesthetic appeal on shelves, which enhances brand visibility. The weight and feel of glass convey a sense of substance and value, distinguishing premium brands from commodity products. The ability of glass to withstand heat during the filling process ensures safe and efficient packaging operations. This combination of functional and aesthetic benefits solidifies the position of glass jars as the leading packaging format. The enduring popularity of glass reflects consumer trust in its safety and environmental profile. Tradition and consumer preference for reusability drive the continued dominance of glass jars in the honey market. For generations, honey has been packaged in glass, creating a strong cultural association between the two. The practical benefit enhances the value proposition of glass-packaged honey, encouraging repeat purchases. The classic appearance of glass jars fits well with rustic and artisanal branding strategies, which are prevalent in the honey industry. Local beekeepers often use glass jars to convey authenticity and craftsmanship, appealing to supporters of small businesses. The durability of glass ensures that the product arrives in good condition, reducing returns and complaints. Retail promotions often highlight the reusable nature of glass containers, reinforcing this preference. The emotional connection to traditional packaging formats sustains the demand for glass jars. This blend of practicality and nostalgia ensures that glass remains the primary choice for honey packaging in the United States.

The squeeze bottles and tubes segment is predicted to witness the highest CAGR of 4.1% between 2026 and 2034. This quick acceleration of the segment is propelled by the demand for convenience and ease of use in modern lifestyles. These formats allow for precise dispensing and mess-free application, appealing to busy consumers and families with children. The ability to control portion size reduces waste and simplifies meal preparation, making these formats attractive for daily use. Squeeze bottles are also durable and lightweight, making them ideal for lunchboxes and outdoor activities. The no-drip design enhances the user experience, addressing common complaints about sticky spills. Manufacturers are innovating with ergonomic designs and easy-open caps to further improve usability. The compatibility of squeeze bottles with quick service restaurants and cafes supports their growth in the foodservice sector. This shift toward functional packaging reflects changing consumer expectations for efficiency and cleanliness. The practical advantages of squeeze bottles ensure their continued rapid adoption in the market. Portability and on-the-go consumption trends accelerate the growth of squeeze bottles and tubes in the honey market. Single-serve tubes and small squeeze bottles are ideal for snacking and travel, catering to mobile consumers who seek healthy energy sources. Honey tubes are popular among athletes and hikers for quick energy boosts, expanding the user base beyond traditional household settings. The compact size of these packages fits easily into bags and pockets, enhancing accessibility. Retailers are placing these items near checkout counters and in impulse buy zones, driving incremental sales. The novelty of tube packaging attracts younger demographics who value innovation and convenience. Branding opportunities on tubes allow for targeted marketing messages and engaging visuals. The reduction in packaging material compared to jars also appeals to environmentally conscious shoppers looking for lighter options. This focus on mobility and instant gratification ensures that squeeze bottles and tubes remain a high-growth segment.

COUNTRY LEVEL ANALYSIS

United States

The United States held a prominent position in the global honey market and accounted for a 15.7% share in 2025. This growth trajectory of the US market is attributed to a significant reliance on imports to meet domestic demand, as local production falls short of consumption levels. According to the United States Department of Agriculture, the country imports over 500 million pounds of honey annually (as of 2024), primarily from India, Argentina, and Brazil, to supplement domestic supplies. As per the National Honey Board and USDA data, the US has reached an all-time high in total honey consumption, yet remains a moderate per capita consumer (~1.5 pounds/year) compared to leading nations like Turkey and Germany. The market is influenced by high consumer awareness regarding health and wellness, which fuels demand for premium and organic varieties. Regulatory frameworks enforced by the Food and Drug Administration play a critical role in maintaining quality standards and combating adulteration. The presence of a robust beekeeping industry supports local production, although challenges such as colony collapse disorder persist. The United States serves as a trendsetter for honey innovation, with significant developments in packaging, branding, and functional applications. The diversity of floral sources across different regions allows for a wide variety of domestic honeys, contributing to market richness. Trade policies and tariffs impact the flow of imports, shaping pricing and availability. The mature retail infrastructure ensures widespread distribution, from supermarkets to specialty stores. This combination of high demand, import reliance, and regulatory oversight defines the unique status of the US honey market in the global landscape.

COMPETITIVE LANDSCAPE

The competition in the United States honey market is intense and characterized by a mix of large international importers, domestic producers,s and artisanal brands. Major players compete based on price, quality authenticityi, ty and brand reputation to capture consumer attention. The prevalence of imported honey creates pressure on domestic producers who often struggle to match lower prices despite higher quality standards. Artisanal and local beekeepers differentiate themselves by emphasizing purity, their regional origin, and sustainable practices, appealing to discerning buyers. Private label brands from major retailers also pose a significant challenge by offering affordable alternatives that mimic premium qualities. Counterfeit and adulterated honey remains a critical issue undermining trust and distorting market dynamics. Companies invest heavily in certification and testing to prove authenticity and justify premium pricing. Marketing efforts focus on educating consumers about the benefits of real honey and the dangers of fake products. The rise of e-commerce allows smaller brands to bypass traditional barriers and reach national audiences. This fragmented landscape requires constant innovation and strategic positioning to maintain relevance and profitability in a complex and evolving market environment.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Honey Market include

- Nature Nate’s Honey Co.

- Sioux Honey Association Co-op

- Barkman Honey LLC

- Dutch Gold Honey Inc.

- GloryBee Inc.

- Bee Maid Honey Limited

- Savannah Bee Company

- Miller Honey Company

- Golden Heritage Foods

- Rice Honey LLC (Local Hive Honey)

- Adee Honey Farms

- Desert Creek Honey

TOP LEADING PLAYERS IN THE MARKET

- Savanna Bee Company is a prominent player in the global honey market known for its commitment to quality and sustainability. The company sources raw, unfiltered honey from diverse floral origins,s ensuring superior taste and nutritional value. Savanna Bee actively supports bee conservation efforts and educates consumers about the importance of pollinators. Recent actions include expanding its retail presence through partnerships with major grocery chains and specialty stores. The company has also launched innovative product lines such as honey-infused snacks and skincare items. These initiatives strengthen its market position by diversifying revenue streams and appealing to health-conscious buyers. Savanna Bee leverages digital marketing to engage directly with customers, fostering brand loyalty. Its focus on transparency and ethical sourcing resonates with modern consumers seeking authentic products. Savanna Bee continues to grow its influence in the competitive honey industry. They achieve this by maintaining high standards and promoting environmental stewardship.

- Langnese Honig GmbH is a leading international honey brand with a strong reputation for purity and consistency. The company operates globally,y offering a wide range of honey varieties, including monofloral and blended options. Langnese emphasizes strict quality control measures and sustainable beekeeping practices to ensure product integrity. Recent actions involve upgrading production facilities to enhance efficiency and meet rising demand. The company has expanded its distribution network in North America and Asia, targeting emerging markets. Langnese also invests in research and development to create honey-based products for food and pharmaceutical applications. These strategies strengthen its market position by increasing accessibility and product diversity. The brand’s long-standing heritage and trustworthiness appeal to traditional and modern consumers alike. Langnese continues to prioritize innovation and sustainability, maintaining its status as a key global player in the honey sector.

- Capilano Honey Limited is a major global honey producer and exporter based in Australia with significant reach in the United States. The company is renowned for its advanced processing technology and extensive supply chain capabilities. Capilano supplies bulk and retail honey to various international markets,s ensuring consistent quality and availability. Recent actions include strategic acquisitions of local honey brands to expand its portfolio and market share. The company has also implemented sustainable sourcing programs to support beekeepers and protect biodiversity. Capilano focuses on innovation by developing convenient packaging formats and value-added honey products. These efforts strengthen its market position by enhancing operational efficiency and customer satisfaction. The company’s strong financial performance and global footprint enable it to compete effectively in dynamic markets. Capilano remains committed to delivering high-quality honey while promoting environmental responsibility and industry growth.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States honey market employ several major strategies to maintain competitiveness and drive growth. Product differentiation is central to these efforts, with companies offering unique varietals such as manuka or wildflower to appeal to niche segments. Sustainability initiatives are increasingly important as brands highlight ethical sourcing and bee conservation to attract environmentally conscious consumers. Strategic partnerships with retailers and food manufacturers help secure shelf space and bulk contracts. Digital marketing and e-commerce platforms are utilized to reach direct consumers and build brand loyalty through storytelling. Innovation in packaging formats such as squeeze bottles and single-serve tubes enhances convenience and usability. Companies also focus on transparency by providing detailed origin information and third-party certifications to combat adulteration concerns. These combined strategies allow participants to navigate market challenges and capitalize on evolving consumer preferences effectively.

MARKET SEGMENTATION

This research report on the U.S. honey market is segmented and sub-segmented into the following categories.

By Type

- Clover Honey

- Specialty Honeys

By Application

- Food and Beverages

- Personal Care and Cosmetics

By Packaging

- Glass Jars

- Squeeze Bottles and Tubes

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com