U.S. Lingerie Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Price Range, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

U.S. Lingerie Market Report Summary

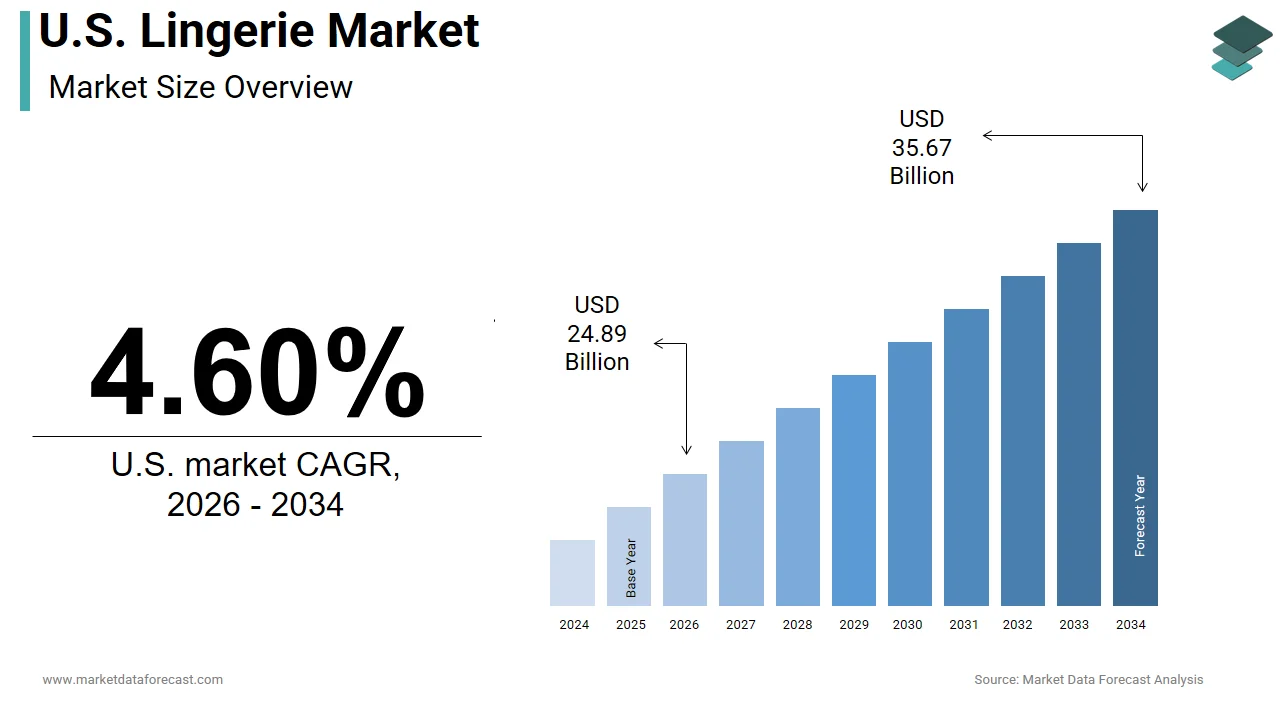

The U.S. lingerie market was valued at USD 23.80 billion in 2025, is estimated to reach USD 24.89 billion in 2026, and is projected to reach USD 35.67 billion by 2034, growing at a CAGR of 4.60% from 2026 to 2034. Market growth is driven by rising consumer focus on comfort, fashion, and body positivity, along with increasing demand for premium and inclusive lingerie collections. Brands are increasingly introducing innovative fabrics, size-inclusive products, and athleisure-inspired intimate wear to cater to evolving consumer preferences. Additionally, the expansion of e-commerce platforms, celebrity-led brands, and growing demand for sustainable lingerie products are supporting market growth across the United States.

Key Market Trends

- Rising demand for comfortable and size-inclusive lingerie products.

- Increasing popularity of premium and fashion-oriented intimate wear.

- Growth in e-commerce and direct-to-consumer lingerie sales.

- Expansion of sustainable and eco-friendly lingerie collections.

- Increasing influence of celebrity and social media-driven lingerie brands.

Segmental Insights

- Based on type, the bras segment dominated the United States lingerie market by accounting for 61.8% share in 2025, driven by its essential role in daily wear and strong consumer demand across multiple categories.

- Based on price range, the economy segment held the leading share in 2025, supported by affordability and widespread accessibility among consumers.

- Based on distribution channel, the store-based segment dominated the market in 2025, driven by strong consumer preference for in-store fitting experiences and physical retail availability.

Country-Level Insights

- The United States dominated the North American lingerie market by capturing 83.6% share in 2025, supported by strong consumer spending on apparel, extensive retail infrastructure, and growing demand for fashion and comfort-oriented intimate wear products.

Competitive Landscape

The U.S. lingerie market is highly competitive, with companies focusing on product innovation, inclusive sizing, sustainable materials, and omnichannel retail strategies. Celebrity collaborations, digital marketing, and expansion of premium product portfolios are shaping the competitive landscape.

Prominent companies operating in the U.S. lingerie market include Victoria's Secret, Hanesbrands, Calvin Klein, Aerie, ThirdLove, Savage X Fenty, Lise Charmel, Chantelle, Boux Avenue, and Intimissimi.

U.S. Lingerie Market Size

The size of the U.S. lingerie market was worth USD 23.80 billion in 2025. The market is anticipated to grow at a CAGR of 4.60% from 2026 to 2034 and be worth USD 35.67 billion by 2034 from USD 24.89 billion in 2026.

Lingerie refers to fashionable, often luxurious or sensual women's underwear and nightclothes, typically crafted from delicate materials like silk, lace, or satin. This market has evolved significantly from purely utilitarian undergarments to a vital component of personal expression and self-care. Modern consumers view lingerie as an extension of their identity, which drives demand for products that offer both comfort and style. The cultural shift towards body positivity has redefined industry standards, encouraging brands to cater to a wider range of body types and skin tones. Based on US Census Bureau projections, the female population in the United States is estimated to reach approximately 173 million in 2025, representing a substantial and growing consumer base for intimate apparel. Additionally, data from the Bureau of Labor Statistics indicates that women aged 25 to 54 achieved a historic labor force participation rate of 78.0% in late 2025, boosting purchasing power and driving demand for versatile, professional wardrobe essentials. The rise of remote work has also altered consumption patterns with a notable increase in demand for comfortable yet presentable loungewear and bralettes. According to the National Retail Federation, consumer spending on apparel and accessories remains resilient despite economic fluctuations, demonstrating the enduring nature of this category. The integration of advanced fabrics such as moisture-wicking materials and seamless construction techniques further enhances product appeal. These demographic and behavioral trends create a dynamic environment where innovation and inclusivity are paramount for brand success in the contemporary landscape.

MARKET DRIVERS

Body Positivity and Inclusivity Drive Expanded Consumer Base

The widespread adoption of body positive movements has fuelled the growth of the US lingerie market. This has compelled brands to expand their size ranges and diversify marketing campaigns. Consumers increasingly demand representation and products that fit various body shapes rather than conforming to traditional, narrow beauty standards. This cultural shift has opened new revenue streams for companies that prioritize inclusivity in their design and production processes. According to research by McKinsey & Company, two out of three American consumers state that social values now shape their shopping choices, with a significant majority expecting brands to back up their diversity and inclusion statements with authentic action. Major retailers have responded by extending size offerings up to 40G or higher and introducing adaptive lingerie for individuals with disabilities. The Federal Trade Commission has intensified its scrutiny of the fashion industry by penalizing brands for deceptive marketing practices, such as blocking negative customer reviews and making false manufacturing claims, forcing the sector toward greater transparency. Brands that fail to adapt risk alienating a significant portion of the market as social media amplifies consumer voices and holds companies accountable for a lack of representation. This driver is not merely a trend but a structural change in consumer expectations that requires long-term strategic commitment from industry participants to maintain relevance and loyalty among a diverse customer base.

Rising Health Consciousness Influences Fabric and Design Choices

Growing health awareness among US consumers is driving demand for lingerie made from natural, breathable, and hypoallergenic materials that promote skin health and overall well-being, and thereby contribute to the expansion of the US lingerie market. Shoppers are increasingly scrutinizing fabric compositions and avoiding synthetic materials that may cause irritation or discomfort during extended wear. This trend aligns with the broader wellness movement, where personal care extends to every aspect of daily life, including undergarments. According to data cited by the Centers for Disease Control and Prevention, chronic skin conditions affect tens of millions of Americans, significantly heightening consumer demand for non-irritant, skin-friendly clothing options. The Organic Trade Association reported that U.S. sales of organic textiles, led by organic cotton, grew by 5.8% in 2025 to reach $2.7 billion, reflecting a steady consumer preference for sustainable fabrics. Consumers are also seeking antimicrobial and moisture-wicking properties that enhance hygiene and reduce the risk of infections. Medical professionals often recommend specific types of supportive underwear for post-surgical recovery or maternity care, which creates specialized niche markets within the broader industry. The Food and Drug Administration regulates claims related to the medical benefits of textiles, which ensures that manufacturers adhere to strict standards when marketing health-focused products. This driver encourages innovation in textile technology as brands invest in research to develop fabrics that offer therapeutic benefits without compromising on style or comfort. The intersection of health and fashion thus serves as a powerful catalyst for product development and differentiation in the competitive lingerie landscape.

MARKET RESTRAINTS

Supply Chain Volatility Impacts Production Costs and Availability

Ongoing volatility in global supply chains affects the cost and availability of raw materials and finished goods, which restrains the growth of the US lingerie market. Many manufacturers rely on imported fabrics and components from Asia and Europe, making them vulnerable to geopolitical tensions, trade tariffs, and logistical disruptions. Data from Yale's Budget Lab and other analyses reveal that while the overall U.S. effective tariff rate hovered around 16.8% in 2025, the textile and apparel sector faced significantly higher weighted average rates (peaking between 36% and 54%), drastically increasing production costs for domestic brands. Freight delays and port congestion further exacerbate these issues, leading to inventory shortages and delayed product launches. Fluctuating prices of raw materials such as cotton and nylon also create uncertainty in pricing strategies and profit margins. The Environmental Protection Agency has introduced stricter regulations on chemical usage in textile processing, which require additional compliance costs for suppliers. These factors collectively strain operational efficiency and force companies to seek alternative sourcing strategies or absorb higher costs. The inability to predict lead times accurately complicates inventory management and increases the risk of overstock or stockouts. As a result, brands must invest in resilient supply chain infrastructure and local sourcing initiatives to mitigate these risks and maintain competitive pricing in a challenging economic environment.

Economic Inflation Reduces Discretionary Spending on Premium Products

Persistent inflation in the country is a serious hurdle for the US lingerie market. This reduces disposable income and shifts consumer preferences towards value-oriented purchases. High inflation rates erode purchasing power, which leads shoppers to prioritize essential goods over discretionary items such as premium lingerie. According to the Bureau of Labor Statistics, the consumer price index for apparel rose by approximately 3.4% to 3.5% annually by early 2026, driven by rising input costs, which have dampened consumer demand for higher-priced intimate apparel. Consumers are increasingly trading down to private label or discounted brands to manage household budgets effectively. The Federal Reserve Bank of New York reported that household debt rose to record levels in 2025, which further constrained spending on non-essential items. Retailers face pressure to offer promotions and discounts to attract price-sensitive customers, which compresses profit margins and limits investment in innovation. This economic environment makes it difficult for luxury and mid-tier brands to maintain sales volumes without sacrificing brand equity. Additionally, rising interest rates affect borrowing costs for retailers, which limits their ability to expand store networks or invest in marketing campaigns. The cumulative effect of these financial pressures creates a challenging landscape for growth and profitability in the US lingerie sector.

MARKET OPPORTUNITIES

Expansion into Adaptive Lingerie for Underserved Segments

The development of adaptive lingerie provides a significant opportunity for brands to tap into an underserved market segment comprising individuals with disabilities and mobility challenges, which is anticipated to boost the growth of the US lingerie market. This niche requires specialized designs featuring easy closure mechanisms, magnetic fasteners, and soft seams that accommodate sensory sensitivities and physical limitations. Data from the Centers for Disease Control and Prevention indicates that over 70 million adults in the United States reported having a disability in 2022, representing a massive and growing consumer base with specific functional apparel needs. Major brands have begun launching adaptive collections, which signals growing recognition of this opportunity and its commercial potential. The American Association of People with Disabilities advocates for greater inclusivity in fashion, which drives awareness and demand for functional yet stylish options. Regulatory support through the Americans with Disabilities Act encourages businesses to provide accessible products, which further validates this market segment. Companies that invest in inclusive design can differentiate themselves and build strong brand loyalty among consumers who value accessibility. The global adaptive clothing landscape is projected to grow significantly as awareness increases and design innovations make these products more appealing. Collaborations with occupational therapists and patient advocacy groups help brands create solutions that truly meet user needs. This opportunity allows companies to demonstrate social responsibility while accessing a loyal customer base that is often overlooked by mainstream retailers. Brands can unlock new revenue streams by addressing these unique requirements. Doing so enhances their reputation as leaders in inclusivity and innovation within the intimate apparel industry.

Integration of Sustainable and Circular Business Models

The shift towards sustainability opens the door for US lingerie brands to adopt circular business models that emphasize recycling, repair, and resale of products, and is expected to drive the expansion of the US lingerie market. Consumers are increasingly concerned about the environmental impact of fast fashion and seek brands that demonstrate commitment to ethical practices. Brands that implement take-back programs or use recycled materials can appeal to environmentally conscious shoppers and differentiate themselves in a crowded market. The Ellen MacArthur Foundation promotes the circular economy framework, which encourages designers to create durable and recyclable products. Companies like Patagonia have successfully demonstrated the viability of resale platforms, which can be adapted for the lingerie sector with proper hygiene protocols. Investment in biodegradable fabrics and closed-loop production processes reduces environmental footprint and aligns with regulatory trends towards extended producer responsibility. The Federal Trade Commission is updating its Green Guides to prevent greenwashing, which rewards brands with genuine sustainability credentials. By embracing circularity, companies can reduce material costs and create new revenue streams through refurbished or upcycled products. This approach not only mitigates environmental risks but also enhances brand image and customer loyalty among younger demographics who prioritize ethical consumption. The transition to sustainable practices thus represents a strategic avenue for long-term growth and resilience in the evolving lingerie landscape.

MARKET CHALLENGES

Intense Competition from Private Label and Direct-to-Consumer Brands

Intense competition from private label offerings and direct-to-consumer startups is reshaping the US lingerie market. They challenge established brands by offering better price points and greater agility. Retail giants such as Target and Amazon have expanded their private label lingerie lines, which offer comparable quality at lower price points. According to the Private Label Manufacturers Association, total U.S. store-brand sales climbed to a record $277 billion by late 2025, demonstrating massive consumer acceptance of private labels as retailers increasingly win on value and premium design over national brands. Direct-to-consumer brands leverage digital marketing and social media to reach niche audiences with personalized messaging and rapid product iterations. These agile competitors can respond quickly to trending styles and consumer feedback, which traditional brands often struggle to match. The Federal Trade Commission closely monitors deceptive retail marketing and unfair business practices, establishing consumer trust while inadvertently forcing industry incumbents to focus on corporate transparency and operational compliance. Established brands face the challenge of maintaining brand equity while competing on price and speed. The rise of social commerce allows new entrants to bypass traditional distribution channels and build direct relationships with customers. This fragmentation of the market dilutes brand loyalty and forces companies to invest heavily in digital presence and customer experience. The ability to differentiate through unique value propositions, such as superior fit technology or exclusive designs, becomes critical for survival. Without continuous innovation and strategic positioning, legacy brands risk losing market share to these nimble and cost-effective competitors.

Counterfeit Products and Intellectual Property Theft Risks

The prevalence of counterfeit lingerie products is a significant challenge to legitimate brands within the US lingerie market. These fakes undermine brand integrity and cause substantial revenue losses. Online marketplaces facilitate the sale of fake goods, which often mimic popular designs and logos, making it difficult for consumers to distinguish authentic items. Data from U.S. Customs and Border Protection and international trade agencies highlights that counterfeit goods comprise roughly 2.3% of global trade, with apparel, footwear, and accessories consistently ranking among the top categories seized at borders. Counterfeit products typically use inferior materials and manufacturing processes which can lead to customer dissatisfaction and damage brand reputation when mistaken for genuine articles. The International Trademark Association highlights that intellectual property theft costs the US economy billions of dollars annually across all sectors, including fashion. Brands must invest in anti-counterfeit technologies such as holographic tags and blockchain verification to protect their products and assure customers of authenticity. Legal enforcement against counterfeiters is complex and resource-intensive, particularly when operations span multiple jurisdictions. The rise of social media influencers promoting dubious products further complicates efforts to control brand image and distribution. Consumers who unknowingly purchase counterfeits may associate poor quality with the original brand, which erodes trust and loyalty. This challenge requires comprehensive strategies involving legal action, consumer education, and technological innovation to safeguard brand value and ensure fair competition in the marketplace.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Price Range, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Victoria's Secret (US), Hanesbrands (US), Calvin Klein (US), Aerie (US), ThirdLove (US), Savage X Fenty (US), Lise Charmel (FR), Chantelle (FR), Boux Avenue (GB), Intimissimi (IT) |

SEGMENTAL ANALYSIS

By Type Insights

The bras segment held the majority share of 61.8% of the US lingerie market in 2025. Its status as an essential daily garment for the majority of women drives the supremacy of this segment. This category drives consistent revenue because bras are considered a necessity rather than a discretionary purchase, ensuring steady demand regardless of economic fluctuations. The dominance is further reinforced by the wide variety of styles required for different occasions, such as sports, work, and leisure, which encourages multiple purchases per consumer. Research indicates that undergarments represent an essential, recurring category within the domestic wardrobe, with functional foundations like bras commanding the highest consumer expenditure share within the intimate apparel segment. The need for regular replacement due to wear and tear also contributes to high volume sales, as experts recommend replacing bras every six to twelve months. Additionally, the increasing awareness of proper fit and support has led consumers to invest in higher-quality bras that offer better durability and comfort. The proliferation of specialized bra types, including push-up minimizer and wireless options, allows brands to cater to diverse preferences and body types. Retailers often use bras as an entry point to build customer loyalty, which leads to cross-selling of matching panties and other intimate apparel. The extensive distribution network for bras across department stores, specialty shops, and online platforms ensures high accessibility for consumers. This combination of functional necessity, frequent replacement cycles, and product diversification solidifies the bras segment as the cornerstone of the US lingerie industry.

The shapewear segment is likely to experience the fastest CAGR of 8.2% from 2026 to 2034. This rapid expansion of the segment is propelled by the evolving perception of shapewear from a corrective garment to a fashion staple that enhances confidence and silhouette. The influence of celebrity endorsements and social media trends has normalized the use of shapewear among younger demographics who view it as a tool for body contouring rather than just weight concealment. Data from the National Center for Health Statistics indicates that the age-adjusted adult obesity rate in the United States stands at 40.3%, driving a massive, structurally consistent addressable market for supportive, smoothing, and shaping garments. Innovations in fabric technology have also played a crucial role by introducing breathable, lightweight materials that provide compression without discomfort. Brands like Skims have revolutionized the sector by offering inclusive size ranges and skin tone matches, which have broadened the appeal beyond traditional users. The rise of bodycon dresses and fitted clothing styles in mainstream fashion further fuels demand for seamless shapewear solutions. Additionally, the integration of shapewear into everyday wardrobes for work and casual settings has increased usage frequency. The segment benefits from strong marketing campaigns that emphasize empowerment and self-expression rather than shame. These cultural and technological shifts collectively accelerate the adoption of shapewear, making it the most dynamic segment in the contemporary lingerie landscape.

By Price Range Insights

The economy segment led the US lingerie market and accounted for a substantial share in 2025. Its accessibility and alignment with the budget-conscious behavior of a large portion of the population are reasons behind the leading position of this segment. This segment includes mass market brands sold through department stores, discount retailers, and supermarkets, which offer affordable options for everyday wear. The dominance is driven by the high volume of sales generated by price-sensitive consumers who prioritize value and functionality over luxury features. According to the U.S. Census Bureau income distribution models, roughly one-quarter of American households earn an annual income below $50,000, creating a significant, value-driven market segment that heavily prioritizes affordability in daily essentials. Economic uncertainty and inflationary pressures further reinforce the preference for economy products as consumers seek to maximize their purchasing power. Major retailers like Walmart and Target have expanded their private label lingerie lines, which offer competitive quality at lower price points, attracting a broad customer base. The frequency of purchases in the economy segment is higher as consumers tend to buy more items at lower prices rather than investing in fewer expensive pieces. Promotional activities and discounts are common strategies used by brands in this segment to drive traffic and increase basket size. The widespread availability of economy lingerie through various channels ensures that it remains the go-to choice for young professionals and large families. This broad appeal and high turnover rate establish the economy segment as the largest contributor to market revenue in terms of unit sales.

The premium segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 7.5% during the forecast period, owing to rising disposable incomes and the desire for luxury experiences. Consumers are increasingly willing to pay higher prices for lingerie that offers superior quality, intricate designs, and brand prestige. This trend is fueled by the growing affluent middle class, who view premium lingerie as a form of self-indulgence and personal care. Economic data maintained by the Federal Reserve Bank of St. Louis (FRED) shows that the real U.S. median household income has climbed past $80,610, expanding mid-tier and premium purchasing power across mass-market apparel categories. The influence of social media and influencer marketing has elevated the status of premium brands, making them desirable symbols of lifestyle and status. Premium lingerie often incorporates advanced fabrics such as silk lace and sustainable materials, which appeal to environmentally conscious and quality-focused shoppers. The rise of direct-to-consumer luxury brands has made premium products more accessible by bypassing traditional retail markups and offering personalized shopping experiences. Additionally, the trend of gifting premium lingerie during special occasions such as weddings and anniversaries contributes to segment growth. Brands in this category focus on exclusivity and craftsmanship, which creates strong emotional connections with customers. The shift towards buying less but better quality items aligns with the values of modern consumers who prioritize longevity and ethical production. These factors collectively propel the premium segment as the fastest expanding area in the US lingerie market.

By Distribution Channel Insights

The store-based segment dominated the US lingerie market and captured a significant share in 2025. This dominance of the segment was supported by the critical importance of fit and tactile experience in purchasing intimate apparel. Consumers prefer to try on bras and shapewear in physical stores to ensure proper sizing and comfort, which reduces the likelihood of returns. Department stores, specialty lingerie shops, and mall boutiques provide expert fitting services and personalized advice that enhance the shopping experience. The ability to feel the fabric and assess the quality firsthand is a significant advantage for store-based channels, especially for premium and complex items like underwire bras. Many consumers also value the immediate gratification of taking home their purchases without waiting for delivery. Retailers have invested in creating inviting store environments with private fitting rooms and knowledgeable staff to attract customers. The presence of flagship stores in major cities serves as a brand showcase and builds trust among shoppers. Additionally, promotional events and in-store exclusives drive foot traffic and encourage impulse buys. The integration of omnichannel services, such as buy online, pick up in store, further strengthens the position of physical outlets. This combination of sensory engagement, expert assistance, and convenience ensures that store-based channels remain the primary destination for lingerie shoppers in the United States.

The non-store-based segment is expected to exhibit a noteworthy CAGR of 9.1% over the forecast period due to the convenience of online shopping and advancements in digital technology. E-commerce platforms offer a vast selection of styles, sizes, and brands that may not be available in local stores, appealing to a wider audience. The ease of comparing prices, reading reviews, and accessing detailed product information online empowers consumers to make informed decisions. Improvements in return policies and virtual fitting tools have addressed previous concerns about sizing and fit, making online purchases less risky. Subscription services and personalized recommendations based on browsing history enhance customer engagement and loyalty. The rise of mobile commerce allows shoppers to browse and buy lingerie anytime and anywhere, increasing accessibility. Social media integration enables seamless purchasing through influencers and targeted ads, which drives traffic to online stores. Direct-to-consumer brands leverage digital channels to build strong communities and offer exclusive content that resonates with modern shoppers. The ability to reach rural and underserved areas where physical stores are scarce further expands the market potential. These technological and behavioral shifts position non-store-based channels as the primary driver of future growth in the US lingerie industry.

COUNTRY ANALYSIS

U.S. Lingerie Market Analysis

The United States was the top performer in the North American lingerie market and occupied a 83.6% share in 2025. This growth of the US market was fuelled by its large population, high disposable income, and advanced retail infrastructure. The market status is characterized by a mature yet evolving landscape where innovation in sustainability, inclusivity, and technology drives competition. The country serves as a trendsetter for global lingerie styles and business models, influencing markets worldwide. According to the US Census Bureau population estimates, the female population aged 15 and older now exceeds 141 million; market observers identify this demographic as the core driver for the multibillion-dollar intimate apparel market. The high level of urbanization and internet penetration facilitates the growth of both physical and online retail channels. Consumer preferences in the US are diverse, ranging from value-oriented mass market products to luxury niche brands, which support a wide array of market participants. The strong presence of major international and domestic brands fosters intense competition and continuous product innovation. Mandatory regulatory standards for textile safety and labeling ensure product safety and transparency, creating a baseline of compliance that fosters consumer confidence. The cultural emphasis on individuality and self-expression encourages brands to offer diverse sizes, styles, and marketing messages. Additionally, the robust logistics network enables efficient distribution and quick delivery times, which enhance customer satisfaction. The integration of health and wellness trends into lingerie design further distinguishes the US market from other regions. These factors collectively maintain the United States as the largest and most influential market for lingerie in North America.

COMPETITIVE LANDSCAPE

The competition in the United States lingerie market is intense and characterized by a mix of established legacy brands and agile direct-to-consumer startups. Market leaders compete on factors such as brand reputation, product quality, inclusivity, and digital engagement rather than price alone. The rise of body positivity has forced traditional brands to rethink their marketing and product offerings to remain relevant. New entrants leverage social media and influencer partnerships to build strong communities and challenge incumbent players with fresh perspectives. Sustainability and ethical production have become key differentiators as consumers increasingly prefer brands that demonstrate social responsibility. The market sees frequent launches of innovative fabrics and designs that prioritize comfort and functionality alongside aesthetics. Private label offerings from major retailers also exert pressure by providing affordable alternatives with decent quality. Technological advancements in virtual fitting and personalized recommendations enhance customer experience and drive loyalty. Mergers and acquisitions are common as companies seek to expand their portfolios and enter new segments. The dynamic nature of consumer preferences requires continuous adaptation and innovation. Brands must balance heritage with modernity to succeed. This competitive environment fosters creativity and drives the industry towards greater inclusivity and sustainability, ensuring that only those who evolve with the times thrive in this vibrant sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. lingerie market include

- Victoria's Secret (US)

- Hanesbrands (US)

- Calvin Klein (US)

- Aerie (US)

- ThirdLove (US)

- Savage X Fenty (US)

- Lise Charmel (FR)

- Chantelle (FR)

- Boux Avenue (GB)

- Intimissimi (IT)

TOP PLAYERS IN THE MARKET

- Victoria’s Secret remains a pivotal force in the United States lingerie landscape by undergoing a comprehensive brand transformation focused on inclusivity and modern femininity. The company has shifted its marketing strategy to feature diverse models and body types, which resonates with contemporary consumer values. Recent initiatives include launching the VS Collective, comprising influential women from various fields to guide product development and brand messaging. This strategic pivot aims to rebuild trust and relevance among younger demographics who previously criticized the brand for outdated standards. Victoria’s Secret also expanded its product line to include more comfortable wireless bras and adaptive lingerie catering to broader needs. The retailer continues to leverage its extensive physical store network while enhancing its digital platform to offer seamless omnichannel experiences. By prioritizing community engagement and social responsibility, the company strives to maintain its iconic status while adapting to evolving market dynamics. These efforts demonstrate a committed approach to sustaining leadership through cultural alignment and product innovation in the competitive intimate apparel sector.

- Savage X Fenty has rapidly established itself as a major disruptor in the US lingerie market by championing radical inclusivity and body positivity. Founded by Rihanna, the brand offers an extensive range of sizes and styles that celebrate diversity and empower consumers of all backgrounds. Its direct-to-consumer model leverages a strong social media presence and high-profile fashion shows to build a loyal community. Savage X Fenty recently expanded its retail footprint by opening flagship stores in key locations, which enhances brand visibility and customer engagement. The company also introduced innovative marketing campaigns that challenge traditional beauty norms and foster a sense of belonging among its audience. By prioritizing authentic representation and accessible luxury, the brand has captured significant attention from millennial and Gen Z shoppers. Its agile supply chain and data-driven approach allow for rapid response to trending styles and consumer feedback. This combination of cultural relevance and operational efficiency positions Savage X Fenty as a formidable competitor, driving change in the industry.

- HanesBrands Inc contributes significantly to the US lingerie market through its portfolio of mass market brands, including Maidenform and Bali, which prioritize comfort and affordability. The company focuses on delivering essential intimate apparel that meets the daily needs of a broad consumer base across various demographic segments. HanesBrands has strengthened its position by investing in sustainable manufacturing practices and introducing eco-friendly product lines that appeal to environmentally conscious shoppers. Recent actions include optimizing its supply chain to improve efficiency and reduce costs, which allows for competitive pricing in a value-driven market. The company also enhances its digital capabilities by expanding e-commerce offerings and personalized online shopping experiences. By leveraging its extensive distribution network in department stores and mass retailers, HanesBrands ensures wide accessibility for its products. The focus on innovation in fabric technology, such as moisture-wicking and seamless construction, further differentiates its offerings. These strategic moves reinforce its role as a reliable provider of quality intimate apparel in the United States.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the US lingerie market employ several major strategies to maintain and enhance their competitive positions. Product innovation remains a primary focus as companies develop comfortable, inclusive, and sustainable intimate apparel that aligns with modern consumer values. Brands are increasingly expanding size ranges and offering adaptive options to cater to diverse body types and needs. Digital transformation is another critical strategy with investments in e-commerce platforms, virtual fitting tools, and personalized marketing to enhance online shopping experiences. Strategic collaborations with influencers and celebrities help brands build cultural relevance and reach younger audiences effectively. Sustainability initiatives, such as using recycled materials and ethical sourcing practices, are adopted to appeal to environmentally conscious consumers. Omnichannel integration ensures seamless connectivity between physical stores and digital channels, providing convenience and flexibility for shoppers. Companies also focus on brand storytelling and community building to foster loyalty and emotional connections with customers. These combined efforts enable market participants to adapt to changing preferences and sustain growth in a dynamic and competitive industry landscape.

MARKET SEGMENTATION

This research report on the U.S. lingerie market has been segmented and sub-segmented into the following categories.

By Type

- Briefs

- Bras

- Shapewear

By Price Range

- Economy

- Premium

By Distribution Channel

- Store-Based

- Non-Store-Based

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. lingerie market?

The U.S. lingerie market includes bras, panties, shapewear, and sleepwear sold as intimate apparel for comfort, support, and style.

How does the U.S. lingerie market function?

The U.S. lingerie market operates through brands, retailers, and online stores that offer varied sizes, styles, and fabrics to shoppers.

What drives growth in the U.S. lingerie market?

The U.S. lingerie market grows from fashion trends, comfort demand, size inclusivity, and rising online shopping for intimate apparel.

Which products lead the U.S. lingerie market?

Bras and panties lead the U.S. lingerie market, while shapewear and sleepwear also contribute strongly to sales and brand loyalty.

Why is shapewear important in the U.S. lingerie market?

Shapewear is important in the U.S. lingerie market because it offers smoothing, support, and special-occasion styling benefits.

How do bras shape the U.S. lingerie market?

Bras remain core to the U.S. lingerie market through everyday support, sports styles, wireless comfort, and premium fashion designs.

What role does e-commerce play in the U.S. lingerie market?

E-commerce expands the U.S. lingerie market by improving privacy, product choice, fit guidance, and direct-to-consumer access.

What trends shape the U.S. lingerie market?

The U.S. lingerie market is shaped by body positivity, inclusive sizing, seamless fabrics, and comfort-focused design.

How does comfort influence the U.S. lingerie market?

Comfort drives the U.S. lingerie market as shoppers prefer soft materials, flexible fits, and everyday wearability.

What is the role of luxury brands in the U.S. lingerie market?

Luxury brands strengthen the U.S. lingerie market with premium fabrics, fashion appeal, and elevated shopping experiences.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com