U.S. Online Grocery Market Size, Share, Trends & Growth Forecast Report By Product Type, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Online Grocery Market Report Summary

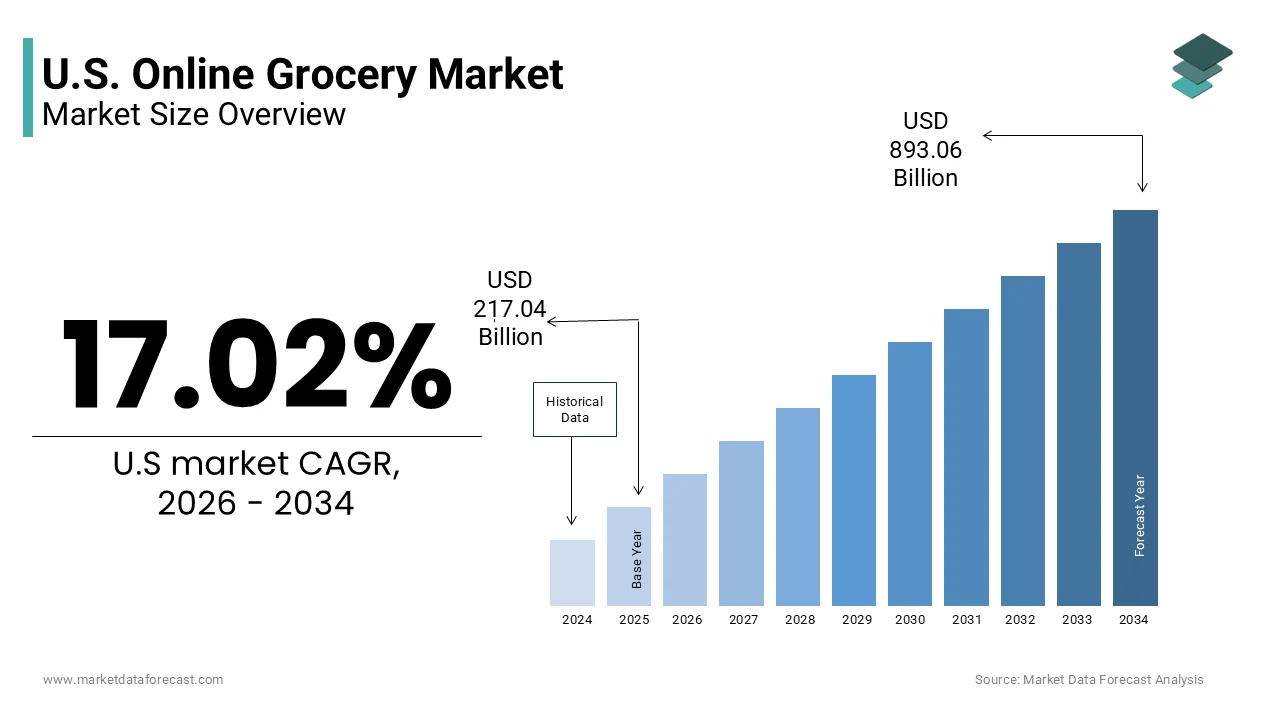

The U.S. online grocery market was valued at USD 217.04 billion in 2025, is estimated to reach USD 253.98 billion in 2026, and is projected to reach USD 893.06 billion by 2034, growing at a CAGR of 17.02% during the forecast period. Market growth is driven by increasing consumer preference for digital shopping convenience, rising adoption of mobile commerce platforms, and expanding same day delivery services. Online grocery platforms provide consumers with easy access to food products, household essentials, and fresh produce through digital ordering and doorstep delivery solutions. The growing integration of AI powered recommendations, automated fulfillment systems, and advanced logistics networks is further supporting rapid market expansion across the United States.

Key Market Trends

- Rising consumer preference for convenient online shopping is driving market growth.

- Increasing adoption of mobile apps and digital payment systems is boosting online grocery demand.

- Growing expansion of same day and quick commerce delivery services is supporting market expansion.

- Integration of AI powered personalization and smart inventory systems is enhancing customer experience.

- Innovation in automated warehouses, robotic fulfillment, and digital retail technologies is influencing market development.

Segmental Insights

- Based on product type, the staples and cooking essentials segment held the dominant share of the U.S. online grocery market in 2025. This dominance is attributed to frequent household purchasing patterns and increasing reliance on digital grocery platforms for daily necessities.

Regional Insights

- The U.S. online grocery market is expected to witness strong growth during the forecast period, supported by improving digital infrastructure, widespread internet penetration, and increasing consumer reliance on e commerce platforms. The integration of AI technologies, predictive analytics, and advanced delivery systems is further strengthening the country’s leadership in digital grocery retail.

Competitive Landscape

The U.S. online grocery market is highly competitive, with key players focusing on rapid delivery capabilities, AI driven shopping experiences, and expansion of omnichannel retail strategies to strengthen their market position. Companies are investing in automated fulfillment centers, subscription services, and advanced logistics technologies. Prominent players in the U.S. online grocery market include Walmart, Amazon, The Kroger Co., Instacart, DoorDash, Target Corporation, Albertsons Companies, Ahold Delhaize, Costco Wholesale, and CVS Health.

U.S. Online Grocery Market Size

The U.S. online grocery market size was valued at USD 217.04 billion in 2025, is estimated to reach USD 253.98 billion in 2026, and is projected to reach USD 893.06 billion by 2034, growing at a CAGR of 17.02% from 2026 to 2034.

Online grocery represents a fundamental transformation in consumer retail behavior characterized by the digital procurement of food and household essentials through web based platforms and mobile applications. This sector encompasses various fulfillment models including home delivery curbside pickup and rapid commerce services that leverage local micro fulfillment centers. The adoption of these services has shifted from a niche convenience to a mainstream necessity driven by technological integration and changing lifestyle dynamics. According to the U.S. Census Bureau, e-commerce sales reached $291.6 billion in the fourth quarter of 2024, accounting for 15.6% of total retail sales, which reflects a structural shift in how Americans shop for daily necessities. The proliferation of high speed internet and smartphone penetration facilitates seamless transactions with the Pew Research Center noting that approximately 90% of American adults own a smartphone as of early 2024, which serves as the primary interface for grocery shopping apps. Furthermore the increasing urbanization and dual income households contribute to time scarcity making efficient shopping solutions highly valued. As per the Department of Agriculture, Americans spent approximately 52.5% of their total food budget on food away from home in 2023, and digital platforms are increasingly used to access a wider range of products including organic and specialty items that may not be available in local physical stores. This market is defined not only by transaction volume but by the integration of data analytics personalization and supply chain innovation that enhance the overall consumer experience and operational efficiency.

MARKET DRIVERS

Time Scarcity and Convenience Driven Consumer Lifestyles

The pervasive time scarcity experienced by modern consumers who prioritize convenience and efficiency in their daily routines is majorly driving the expansion of the U.S. online grocery market. With an increasing number of dual income households and demanding professional schedules individuals seek to minimize the time spent on routine chores such as grocery shopping. According to the Bureau of Labor Statistics, full-time employed people in 2024 worked an average of 8.1 hours on days they worked, which significantly limits leisure and household management time. This temporal constraint drives demand for services that offer seamless ordering and reliable delivery or pickup options. As per the American Time Use Survey, 80% of the population engaged in household activities on an average day in 2024, spending about two hours on these tasks, which indicates a continued need for time-saving shopping solutions. Online grocery platforms address this need by allowing users to shop anytime and anywhere reducing the physical effort and travel time associated with traditional store visits. The ability to schedule deliveries or pickups at convenient times further enhances the appeal of these services. Additionally the integration of saved lists and repeat order features streamlines the shopping process making it faster and more efficient. Consumers are willing to pay a premium for this convenience as it allows them to reallocate saved time to more valued activities. This behavioural shift towards valuing time over cost sustains the growth of the online grocery sector.

Expansion of Digital Infrastructure and Smartphone Penetration

The extensive expansion of digital infrastructure and the high penetration of smartphones that facilitate easy access to online shopping platforms is further contributing to the online grocery market growth in the U.S. The widespread availability of high speed internet and advanced mobile devices enables consumers to browse select and purchase groceries with ease. According to the Federal Communications Commission, high-speed internet access has expanded such that 100 Mbps downstream connections increased by 18% between 2020 and 2024, ensuring that a majority of households have the connectivity required for online transactions. As per the Pew Research Center, smartphone ownership has reached 90% among all U.S. adults in 2024, with ownership among those aged 18 to 29 standing at nearly 100%. This ubiquity allows retailers to reach a broad demographic through user friendly apps that offer personalized recommendations and real time updates. The improvement in mobile payment security and ease of use further encourages transactions as consumers feel confident in sharing financial information online. Additionally the integration of voice assistants and artificial intelligence into shopping apps enhances the user experience by simplifying search and navigation. The continuous advancement in logistics technology such as real time tracking and automated warehousing supports the reliability of online grocery services. This robust digital ecosystem creates a favorable environment for the sustained growth and adoption of online grocery shopping across diverse population segments.

MARKET RESTRAINTS

Logistical Complexities and Last Mile Delivery Costs

The logistical complexity and high costs associated with last mile delivery that impact profitability and service affordability are primarily hindering the U.S. market growth. Delivering perishable goods requires specialized handling temperature controlled vehicles and precise timing to ensure product quality which increases operational expenses. According to the National Retail Federation, last mile delivery can account for up to 53% of total shipping costs, which creates a significant financial burden for retailers. As per the Bureau of Transportation Statistics, truck transportation employment decreased by 20,000 workers in February 2026 compared to the previous year, while motor fuel prices saw a 30.9% increase per gallon in early 2026, making it challenging for companies to offer competitive pricing without incurring losses. The need for rapid delivery windows adds pressure on logistics networks requiring dense infrastructure and efficient routing algorithms that are costly to develop and maintain. Additionally the low average order value of grocery items compared to other e commerce categories makes it difficult to absorb delivery fees leading to higher prices for consumers or reduced margins for retailers. Rural and suburban areas present additional challenges due to lower population density and longer distances which increase delivery times and costs. These logistical hurdles limit the scalability of online grocery services and restrict access for some consumers. Until innovative solutions such as autonomous delivery or consolidated drop off points become widespread the high cost of last mile logistics will remain a significant barrier to market expansion.

Consumer Preference for Physical Product Inspection

The growth of the U.S. online grocery market is restrained by the persistent consumer preference for physically inspecting fresh produce and perishable items before purchase. Many shoppers rely on sensory cues such as touch smell and visual appearance to assess the quality of fruits vegetables meats and dairy products which cannot be replicated in an online environment. According to the Food Marketing Institute, online grocery sales accounted for 7.1% of all grocery sales in 2024, yet 35% of supermarket transactions still utilize self-checkout as consumers continue to visit physical locations for fresh items. As per industry data, trust in the retailer's ability to select high quality items is a critical factor influencing online grocery adoption yet remains a barrier for many first time users. The inability to choose specific items leads to dissatisfaction and potential waste if replacements are not acceptable. This preference is particularly strong among older demographics and those who prioritize cooking with fresh ingredients. While some retailers offer substitution preferences and refund policies these measures do not fully alleviate the concern. The tactile experience of shopping also serves as a social and recreational activity for many individuals which online platforms cannot replace. This inherent limitation of the digital medium restricts the complete migration of grocery shopping online and necessitates hybrid models that combine digital convenience with physical assurance.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Personalized Shopping Experiences

The integration of artificial intelligence and machine learning to create highly personalized shopping experiences that enhance customer engagement and loyalty is likely to a big opportunity for the U.S. online grocery market. AI algorithms can analyze past purchase history browsing behavior and dietary preferences to offer tailored product recommendations and meal planning suggestions. According to the McKinsey Global Institute, the operations segment using AI dominated the market with a 20.4% share in 2025, showing that automation in order processing and personalization significantly improves efficiency. As per the International Data Corporation, the global artificial intelligence market is projected to reach $3,497.26 billion by 2033, expanding at a CAGR of 30.6% from 2026 to 2033, which indicates massive investment into retail AI. Online grocery platforms can use predictive analytics to anticipate replenishment needs and send timely reminders for recurring purchases thereby simplifying the shopping process. Additionally AI powered chatbots can provide instant customer support and recipe ideas based on available ingredients enhancing the overall user experience. The ability to offer dynamic pricing and personalized promotions based on individual shopping patterns further drives conversion rates. By leveraging data insights retailers can create a sticky ecosystem that encourages repeat usage and reduces churn. This technological advancement transforms online grocery shopping from a transactional activity into a curated service that adds value beyond mere convenience.

Expansion into Quick Commerce and Micro Fulfillment Centers

The expansion into quick commerce and the establishment of micro fulfillment centers that enable rapid delivery of groceries within hours or even minutes is another prominent opportunity for the U.S. online grocery market. This model addresses the growing demand for immediacy and convenience among urban consumers who require fresh ingredients for immediate consumption. According to the Urban Land Institute, the development of micro fulfillment centers allows retailers to reduce delivery times while lowering costs by placing inventory within close proximity to customers. As per Statista, the U.S. quick commerce market reached a significant valuation and is expected to grow by double digits through 2026 as speed becomes a primary differentiator for shoppers. By utilizing dark stores and automated picking systems retailers can optimize inventory management and fulfil orders more efficiently than traditional warehouses. This approach also enables the offering of a wider variety of fresh and prepared foods that appeal to busy professionals and families. Partnerships with third party delivery platforms can further extend reach and capacity without significant capital investment. The ability to provide ultra-fast delivery differentiates retailers in a crowded market and attracts tech savvy consumers who prioritize convenience. As urbanization continues to rise the demand for quick commerce solutions is expected to grow offering a lucrative avenue for market expansion and innovation.

MARKET CHALLENGES

Intense Competition and Price Sensitivity Among Consumers

The intense competition among established retailers new entrants and third party platforms that leads to price wars and margin compression is a significant challenge to the expansion of the U.S. online grocery market. Consumers are highly price sensitive when it comes to groceries often comparing prices across multiple platforms to find the best deals. According to the Federal Trade Commission, a study on surveillance pricing was initiated in 2024 to investigate how AI and personal data are used to set dynamic retail prices, reflecting the competitive pressure in the sector. As per the Bureau of Labor Statistics, the Consumer Price Index for all urban consumers showed that while overall food inflation moderated, the cost of cereals and bakery products still rose 2.1% through March 2026, keeping consumers budget-conscious. This environment forces online grocery providers to invest heavily in marketing and subsidies to attract and retain customers which strains financial resources. The presence of large traditional retailers with established supply chains and economies of scale poses a significant threat to pure play online startups that lack similar advantages. Additionally the low switching costs for consumers mean that loyalty is difficult to maintain without continuous incentives. The need to balance competitive pricing with sustainable business models creates a precarious operating environment. Companies must innovate in service quality and efficiency rather than relying solely on price to differentiate them. Navigating this competitive landscape requires strategic positioning and operational excellence to ensure long term viability.

Supply Chain Vulnerabilities and Inventory Management Issues

The U.S. online grocery market faces significant challenges due to supply chain vulnerabilities and complexities in inventory management which can lead to stockouts and service disruptions. The perishable nature of grocery items requires precise demand forecasting and efficient cold chain logistics to maintain product quality and availability. According to the Department of Agriculture, domestic food at home spending accounted for 5.0% of disposable income in 2024, and any disruption in the flow of these essential goods directly impacts household security. As per the Institute for Supply Management, volatility in lead times and supplier performance remains a primary concern for retailers managing real-time inventory across digital and physical channels. Online grocery platforms must manage real time inventory across multiple channels to prevent overselling and ensure accurate order fulfillment which is technically challenging. Stockouts of popular items can lead to customer dissatisfaction and loss of trust as substitutes may not meet expectations. Additionally the complexity of managing a wide assortment of SKUs with varying shelf lives increases the risk of waste and spoilage. These operational inefficiencies raise costs and reduce profitability. Building resilient supply chains with diversified sourcing and advanced analytics is essential but requires substantial investment. Until these systemic issues are addressed supply chain instability will remain a persistent challenge for the online grocery sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 17.02% |

| Segments Covered | By Product Type and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Walmart, Amazon, The Kroger Co., Instacart, DoorDash, Target Corporation, Albertsons Companies, Ahold Delhaize, Costco Wholesale, and CVS Health |

SEGMENTAL ANALYSIS

By Product Type Insights

The staples and cooking essentials segment had the major share of the U.S. online grocery market in 2025. The growth of the staples and cooking essentials segment in the U.S. market is driven by their fundamental role in daily meal preparation and household maintenance. This category includes items such as rice pasta flour oils spices and canned goods which are non-perishable and have a long shelf life. According to the U.S. Department of Agriculture, food at home spending represented a stable 5.0% of disposable income in 2024, with a large portion directed toward these core pantry items. As per the Bureau of Labor Statistics Consumer Expenditure Survey, the index for cereals and bakery products increased 2.1% over the year ending March 2026, while non-alcoholic beverages rose 4.7%, indicating high expenditure in these staple categories. The predictable nature of consumption for these items makes them ideal for online replenishment as consumers can easily forecast their needs and set up recurring orders. The stability of demand for staples ensures a steady stream of transactions for online grocery platforms. Furthermore the heavy weight and bulkiness of many staple items such as large bags of rice or cases of canned goods make home delivery particularly attractive as it eliminates the physical burden of transporting these goods from physical stores. This convenience factor drives high adoption rates for online purchasing of staples. The ability to stock up on these essentials during promotional periods further encourages larger basket sizes and frequent purchases. The universal need for these basic ingredients across all demographic groups solidifies the dominance of this segment in the online grocery landscape.

On the other hand, the fresh produce segment is estimated to grow at the fastest CAGR in the U.S. market during the forecast period owing to the increasing health consciousness and a strong demand for organic and locally sourced fruits and vegetables. Consumers are prioritizing nutritious diets and seeking high quality fresh items that support their wellness goals. According to the Organic Trade Association, the U.S. organic market grew to new highs in 2023 with fresh produce remaining the top-selling organic category, reaching billions in annual sales. As per the Centers for Disease Control and Prevention, only about 12.3% of adults met fruit intake recommendations and 10.0% met vegetable recommendations in recent years, prompting increased digital availability to improve these numbers. Online grocery platforms facilitate this by offering a wider variety of fresh produce including exotic and organic options that may not be available in local supermarkets. The ability to filter searches for specific dietary preferences such as organic non GMO or locally grown enhances the shopping experience for health conscious consumers. Furthermore, the convenience of having fresh produced delivered directly to the door encourages more frequent purchases and reduces the barrier of visiting multiple stores. Retailers are investing in improved packaging and cold chain logistics to ensure that fresh items arrive in pristine condition thereby building trust. The alignment of online grocery services with health and wellness trends drives the rapid expansion of the fresh produce segment.

COUNTRY LEVEL ANALYSIS

The U.S. is poised to strengthen its global leadership in digital retail over the next few years as infrastructure improvements and AI integration refine the online grocery experience for millions of households. The country serves as a testing ground for new business models technologies and delivery strategies that influence global trends. According to the U.S. Census Bureau, retail e-commerce sales for the full year of 2024 reached $1.2 trillion, an increase of 9.4% from 2023, providing a massive base for the grocery sector. The market status is characterized by intense competition among traditional supermarket chains pure play e commerce giants and emerging quick commerce startups. The presence of major technology companies and logistics providers facilitates the development of sophisticated infrastructure supporting rapid delivery and efficient fulfillment. As per the Department of Commerce, e-commerce penetration in the grocery sector has accelerated significantly as digital sales now make up over 15% of total retail trade. The mature nature of the U.S. market means that growth is driven by service differentiation customer experience and operational efficiency rather than just initial adoption. The U.S. also leads in the integration of artificial intelligence and data analytics into grocery retailing enhancing personalization and supply chain management. This leadership position ensures that the U.S. market remains the primary focus for strategic investments and product launches by international and domestic players. The robust digital ecosystem and high consumer spending power sustain the dynamic growth of the online grocery market.

COMPETITIVE LANDSCAPE

The competition in the U.S. online grocery market is intense and characterized by the presence of traditional retailers technology giants and specialized delivery platforms vying for consumer attention. Major supermarket chains leverage their established supply chains and physical footprints to offer curbside pickup and home delivery services. Technology companies utilize their logistics networks and data analytics capabilities to provide rapid delivery and personalized shopping experiences. Price competitiveness remains a critical factor as consumers compare costs across multiple platforms prompting aggressive promotional strategies. Innovation in last mile delivery solutions such as autonomous vehicles and drones serves as a key differentiator for market leaders. Customer loyalty is driven by convenience reliability and product quality rather than brand allegiance alone. The rise of quick commerce has intensified rivalry by offering ultra-fast delivery times for immediate needs. Retailers must continuously invest in technology and infrastructure to meet evolving consumer expectations. Strategic alliances with local producers and exclusive brand partnerships help differentiate offerings. This dynamic environment requires agility and customer centric strategies to sustain market position and achieve long term profitability.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. online grocery market include

- Walmart

- Amazon

- The Kroger Co.

- Instacart

- DoorDash

- Target Corporation

- Albertsons Companies

- Ahold Delhaize

- Costco Wholesale

- CVS Health

Top Players in the Market

- Amazon Fresh leverages its extensive logistics network and technological prowess to dominate the U.S. online grocery sector. The company integrates seamless delivery options with its Prime membership ecosystem offering same day and two hour delivery services in major metropolitan areas. Recent strategic actions include expanding its physical footprint with new Amazon Fresh stores that serve as both retail locations and fulfillment hubs. Amazon has enhanced its algorithmic recommendation engines to personalize shopping experiences and improve inventory management efficiency. The introduction of Dash Cart technology in stores bridges the gap between online and offline shopping. By utilizing advanced data analytics Amazon optimizes supply chain operations to reduce costs and improve speed. These initiatives strengthen its position by providing unmatched convenience and value to consumers seeking efficient grocery solutions.

- Walmart utilizes its vast network of physical stores to support a robust online grocery pickup and delivery service. The company focuses on leveraging its existing infrastructure to offer competitive pricing and wide product availability to millions of customers. Recent actions involve expanding its Walmart+ subscription program which provides free delivery and fuel discounts to enhance customer loyalty. Walmart has invested heavily in automated fulfillment centers and drone delivery trials to increase operational efficiency. The retailer also partners with third party delivery platforms to extend its reach in urban areas. By integrating digital tools with its brick and mortar presence Walmart ensures a seamless omnichannel experience. These efforts reinforce its market leadership by combining affordability with convenient access for diverse consumer segments across the nation.

- Instacart operates as a leading third party platform connecting consumers with local grocery stores for rapid delivery and pickup services. The company partners with thousands of retailers nationwide providing a flexible solution for shoppers who prefer specific store brands. Recent strategic initiatives include launching advertising platforms for consumer packaged goods brands to generate additional revenue streams. Instacart has introduced AI powered tools such as smart carts and personalized recommendations to enhance user engagement. The expansion into financial services through Instacart Pay offers integrated payment solutions for users and shoppers. By focusing on technology and partnerships Instacart improves delivery speed and accuracy. These actions strengthen its position by creating a comprehensive ecosystem that benefits retailers, brands and consumers while maintaining its role as a key intermediary in the online grocery landscape.

Top Strategies Used by Key Market Participants

Key players in the U.S. online grocery market primarily focus on expanding omnichannel capabilities to integrate physical stores with digital platforms for seamless customer experiences. Companies are investing in micro fulfillment centers and automated technologies to accelerate delivery speeds and reduce operational costs. Strategic partnerships with third party logistics providers enable broader geographic reach and flexible delivery options. Loyalty programs and subscription models are utilized to enhance customer retention and increase lifetime value. Personalization through artificial intelligence drives targeted marketing and improved product recommendations. Retailers emphasize private label development to improve margins and differentiate offerings. Sustainability initiatives including eco-friendly packaging and electric delivery vehicles appeal to environmentally conscious consumers. These strategies enable firms to maintain competitiveness and drive growth in a dynamic industry landscape.

MARKET SEGMENTATION

This research report on the U.S. online grocery market is segmented and sub-segmented into the following categories.

By Product Type

- Fresh Produce

- Breakfast & Dairy

- Snacks & Beverages

- Meat & Seafood

- Staples & Cooking Essentials

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1. What is the U.S. online grocery market?

The U.S. online grocery market refers to digital platforms and mobile applications that allow consumers to purchase groceries and household essentials through online channels.

2. What products are commonly sold through online grocery platforms?

Online grocery platforms typically offer fresh produce, dairy products, packaged foods, beverages, frozen foods, bakery items, personal care products, and household essentials.

3. What factors are driving the growth of the U.S. online grocery market?

Rising internet penetration, increasing smartphone usage, demand for convenience, faster delivery services, and changing consumer shopping habits are major growth drivers.

4. Which delivery models are used in the online grocery market?

Common delivery models include home delivery, click and collect, curbside pickup, same day delivery, and subscription based grocery delivery services.

5. How are mobile applications influencing online grocery shopping?

Mobile apps provide personalized recommendations, digital payments, order tracking, loyalty rewards, and seamless shopping experiences that improve customer engagement.

6. Which consumers are driving demand for online grocery services?

Urban households, working professionals, millennials, and digitally connected consumers are among the key customer groups driving market demand.

7. What challenges does the U.S. online grocery market face?

Major challenges include delivery logistics, inventory management, high operational costs, maintaining product freshness, and intense market competition.

8. How is artificial intelligence used in online grocery platforms?

AI is used for demand forecasting, personalized product recommendations, inventory optimization, route planning, and customer service automation.

9. What role does quick commerce play in the market?

Quick commerce services focus on ultra fast delivery, often within minutes, which is increasing customer expectations for speed and convenience.

10. What is the future outlook of the U.S. online grocery market?

The market is expected to witness strong growth due to digital transformation, expansion of same day delivery networks, rising consumer preference for convenience, and advancements in retail technology.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com