U.S. Outdoor Power Equipment Market Size, Share, Trends & Growth Forecast Report By Type, Power Source, Sales Channel, Application, and Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Outdoor Power Equipment Market Report Summary

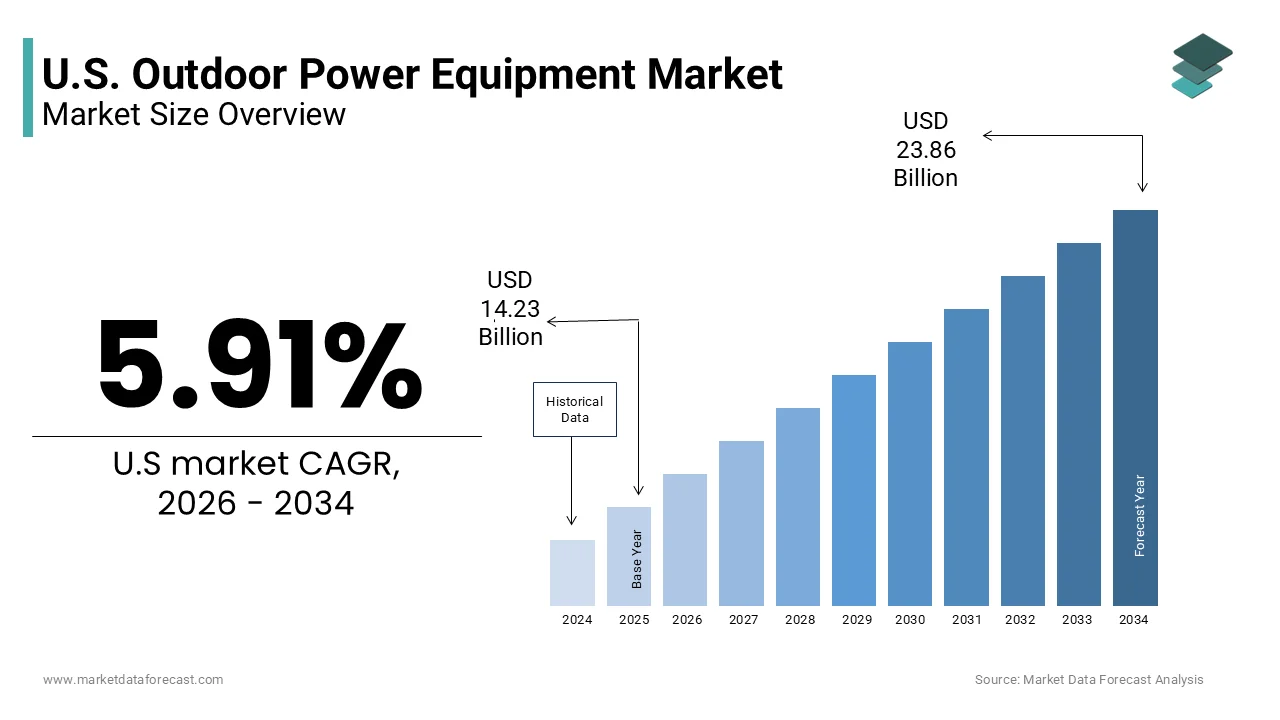

The U.S. outdoor power equipment market was valued at USD 14.23 billion in 2025, is estimated to reach USD 15.07 billion in 2026, and is projected to reach USD 23.86 billion by 2034, growing at a CAGR of 5.91% during the forecast period. Market growth is driven by increasing residential landscaping activities, rising consumer interest in lawn maintenance, and expanding demand for efficient outdoor maintenance equipment. Outdoor power equipment plays a critical role in residential, commercial, and landscaping applications by improving productivity and operational efficiency. The increasing adoption of battery powered technologies and smart outdoor equipment solutions is further supporting market expansion across the United States.

Key Market Trends

- Rising demand for landscaping and lawn maintenance equipment is driving market growth.

- Increasing residential home improvement and outdoor renovation activities are boosting equipment sales.

- Growing adoption of battery powered and environmentally efficient equipment is supporting market expansion.

- Expansion of residential gardening and do it yourself outdoor projects is enhancing product demand.

- Innovation in connected outdoor equipment and smart power technologies is influencing market development.

Segmental Insights

- Based on type, the lawn mowers segment accounted for the dominant share of the U.S. outdoor power equipment market in 2025. This dominance is attributed to widespread residential lawn care activities and growing landscaping requirements.

- Based on power source, the gasoline powered equipment segment held the leading share of the U.S. outdoor power equipment market in 2025, driven by strong power output and broad adoption across residential and commercial applications.

- Based on application, the residential do it yourself segment accounted for the largest share of the U.S. outdoor power equipment market in 2025, supported by rising homeowner participation in lawn care and outdoor maintenance activities.

Regional Insights

- The United States remains the largest national market for outdoor power equipment in North America, supported by strong consumer spending on lawn care, widespread residential landscaping trends, and continuous product innovation. Rising interest in smart outdoor technologies and energy efficient equipment continues to strengthen market development.

Competitive Landscape

The U.S. outdoor power equipment market is highly competitive, with companies focusing on battery powered technologies, automation features, and smart equipment innovation to strengthen their market position. Manufacturers are investing in product efficiency improvements and sustainable outdoor maintenance solutions. Prominent players in the U.S. outdoor power equipment market include Deere and Company, Husqvarna Group, Toro Company, Briggs and Stratton Corporation, STIHL Incorporated, Honda Power Equipment, Cub Cadet, Echo Incorporated, Ariens, and Greenworks Tools.

U.S. Outdoor Power Equipment Market Size

The U.S. outdoor power equipment market size was valued at USD 14.23 billion in 2025, is estimated to reach USD 15.07 billion in 2026, and is projected to reach USD 23.86 billion by 2034, growing at a CAGR of 5.91% from 2026 to 2034.

According to the U.S. Environmental Protection Agency, greenhouse gas emissions from non-road engines, including lawn and garden equipment, contribute significantly to the national transportation sector total, which reached approximately 1,800 million metric tons of carbon dioxide equivalents in recent years. Concurrently, the rise of suburban homeownership, now at 66% of U.S. households according to the U.S. Census Bureau, fuels consistent baseline demand for yard care. As per the U.S. Department of Agriculture, the average American single family lot measures 0.27 acres, creating routine maintenance needs that drive equipment ownership. With over 40 million households performing weekly lawn care, as confirmed by the Outdoor Power Equipment Institute, this category remains deeply embedded in domestic routines while undergoing rapid electrification and automation.

MARKET DRIVERS

Stringent Emission Regulations Accelerating Electrification

Federal and state level environmental mandates is fundamentally reshaping power source preferences in the outdoor equipment sector, which is a key factor driving the growth of the U.S. outdoor power equipment market. The California Air Resources Board’s 2022 regulation banning the sale of new gas powered small off road engines by 2024 has triggered a nationwide ripple effect, with manufacturers pre-emptively redesigning national product lines. According to the U.S. Environmental Protection Agency, a single gas powered lawn mower operating for an hour can produce a substantial amount of volatile organic compounds, which contribute directly to ground level ozone formation. This regulatory pressure is amplified by the Inflation Reduction Act, which allocates 150 million dollars for state level clean landscaping incentive programs. As a result, battery powered equipment sales surged, and as per retail sector reports, alternative battery powered yard tools have expanded significantly, pushing the segment's growth beyond traditional market benchmarks. Major retailers, like Home Depot, now dedicate over 60% of lawn mower floor space to battery and corded models, reflecting supply chain realignment. These policy driven shifts are compressing the traditional gasoline equipment lifecycle, and compelling manufacturers to invest heavily in lithium ion platform scalability and charging infrastructure.

Expansion of Professional Landscaping Services amid Labor Shortages

The commercial landscaping sector is experiencing robust growth driven by labor scarcity and rising property standards, which, in turn, elevates demand for high productivity outdoor power equipment and propels the U.S. market expansion. According to the estimations of the National Association of Landscape Professionals, over 120,000 landscaping businesses operate in the U.S., serving more than 50 million residential and commercial properties. With the industry facing a severe workforce shortfall, as per the Bureau of Labor Statistics, the job opening rate in the administrative and waste services sector, which includes landscaping, reached 7.4% in late 2023. Firms are increasingly substituting manual labor with mechanized solutions, such as zero turn mowers and multi-function attachments. A single commercial zero turn mower can cover 5 acres per hour, compared to 1 acre for a push mower, drastically improving crew efficiency. Additionally, homeowner associations and municipal contracts now mandate year round curb appeal, intensifying service frequency. The Department of Housing and Urban Development reports that 78 million Americans live in managed communities, where landscaping compliance is contractually enforced. This institutional demand ensures steady procurement of durable, commercial grade equipment, even during economic downturns, creating a resilient B2B segment that anchors manufacturer revenue streams.

MARKET RESTRAINTS

High Upfront Cost of Advanced Battery Platforms

Despite long term operational savings, the initial investment required for premium battery powered outdoor equipment remains a significant adoption barrier for average consumers. A high capacity cordless lawn mower with a 60 volt battery and dual blade system typically retails for 650 to 950 dollars, compared to 250 to 400 dollars for comparable gasoline models, according to pricing data compiled by Consumer Reports in 2023. This price differential is exacerbated by the need for ecosystem compatibility, and users often must purchase multiple tools from the same brand to share batteries, increasing total outlay. According to the Department of Energy, swapping a gas mower for an electric variant can lower energy costs to roughly 108 dollars per year, which is over 32 times less than the fuel expenditures of its gasoline counterpart. Furthermore, replacement battery packs cost 150 to 250 dollars, and degrade after 300 to 500 charge cycles, as per Argonne National Laboratory testing, limiting lifecycle value perception. These financial hurdles are particularly acute in rural and low income regions, where yard size necessitates high power equipment, yet disposable income for premium tools is constrained.

Limited Runtime and Performance in Extreme Conditions

Battery powered outdoor equipment continues to face functional limitations in large property or adverse weather applications, which is undermining reliability perceptions among core users and further hampering the U.S. market expansion. At temperatures below 40 degrees Fahrenheit, lithium ion battery capacity can drop by 20 to 30%, as confirmed by testing at the National Renewable Energy Laboratory, reducing mowing time during early spring or late fall. Similarly, high grass density or wet conditions increase motor load, causing premature battery depletion, and according to engineering testing metrics, standard cordless mowers experience a notable reduction in battery runtime under extreme moisture loads, compared to ideal dry parameters. For properties exceeding half an acre, which constitute 42% of U.S. single family lots, per the U.S. Department of Agriculture, this necessitates mid job recharging, disrupting workflow. Snow throwers face even steeper challenges, and battery models struggle with wet, heavy snow common in the Northeast and Midwest, limiting their utility during critical winter events. These performance gaps sustain gasoline equipment loyalty among serious homeowners and professionals, despite environmental drawbacks.

MARKET OPPORTUNITIES

Integration of Smart Features and Connectivity

The embedding of digital intelligence into outdoor power equipment to enhance precision, convenience, and data driven maintenance is a prominent opportunity for the U.S. outdoor power equipment market. Leading manufacturers now offer mowers with GPS navigation, geofencing, and mobile app diagnostics, enabling autonomous operation and usage tracking. According to the Consumer Technology Association, over 18% of premium lawn mowers sold in 2023 included smart connectivity features, up from 5% in 2020. These capabilities appeal to tech savvy homeowners and commercial operators alike, and landscape contractors use runtime and coverage data to optimize crew scheduling and billing accuracy. Additionally, smart blowers and trimmers with variable speed control linked to moisture sensors reduce energy waste and noise pollution, aligning with municipal ordinances. The convergence with home automation ecosystems, such as integration with Amazon Alexa or Google Home, further enhances user engagement. As 5G and edge computing mature, these tools are poised to evolve from standalone machines to coordinated outdoor robotics platforms, creating new service and subscription revenue models beyond hardware sales.

Growth in Urban Green Space Management and Municipal Adoption

Municipalities and urban planners are increasingly investing in sustainable grounds keeping solutions to meet climate action goals and reduce public noise pollution, which is another prominent opportunity for the U.S. market. According to the U.S. Conference of Mayors, 145 cities have adopted clean fleet mandates, requiring 100% zero emission outdoor equipment by 2035. New York City alone committed to electrifying its entire parks department fleet of over 1,200 units by 2026, as per its GreenThumb initiative. This institutional shift is amplified by federal funding, and the Environmental Protection Agency’s 2023 Clean Communities Program allocated 85 million dollars specifically for municipal acquisition of electric blowers, mowers, and trimmers. Urban green space expansion further drives demand, and as per the Trust for Public Land, the percentage of the population living within a 10 minute walk of a public park across major U.S. cities reached 76% by 2023. Unlike residential buyers, municipalities prioritize total cost of ownership and noise compliance, making them ideal early adopters for premium battery platforms. This public sector momentum provides manufacturers with stable volume contracts and real world validation that accelerates broader consumer acceptance.

MARKET CHALLENGES

Supply Chain Volatility for Lithium and Rare Earth Materials

The shift toward battery powered outdoor equipment has intensified dependence on critical minerals whose supply chains remain geopolitically fragile and price volatile, which is a major challenge to the U.S. market growth. Lithium, cobalt, and neodymium, essential for high performance motors and batteries, are predominantly sourced from China, Chile, and the Democratic Republic of Congo, creating import concentration risks. According to the U.S. Geological Survey, domestic lithium production met only 12% of national demand in 2023, with the remainder imported primarily from Australia and Chile. Price fluctuations have been severe, and lithium carbonate prices spiked to 80,000 dollars per metric ton in late 2022, before crashing to 12,000 dollars by mid-2023, introducing severe cost forecasting uncertainty for manufacturers. This volatility complicates long term pricing strategies and delays investment in next generation platforms. Although recycling infrastructure is emerging, the Institute for Energy Research notes that less than 5% of lithium from consumer batteries was recovered in 2023, limiting circular economy benefits. Until domestic refining capacity scales or alternative chemistries, like sodium ion, mature, the outdoor power equipment industry will remain exposed to upstream mineral market shocks.

Fragmented Regulatory Landscape across States

The absence of a uniform federal standard for small engine emissions has resulted in a patchwork of state level regulations that complicate product development and inventory management for manufacturers, which is further challenging the U.S. market growth. While California enforces a complete ban on new gas powered outdoor equipment sales by 2024, states like Texas and Florida maintain no such restrictions, creating divergent market requirements. According to the National Conference of State Legislatures, 18 states have adopted California’s Advanced Clean Equipment standards, while 22 others follow weaker federal EPA Tier 4 guidelines. This regulatory fragmentation forces companies to maintain dual production lines and segmented distribution networks, increasing operational complexity. Retailers face similar challenges, and a Home Depot store in Sacramento must stock only electric mowers, while its counterpart in Houston offers predominantly gasoline models. Such inconsistency delays nationwide electrification and inflates compliance costs, estimated at 45 million dollars annually per major OEM, as per the Outdoor Power Equipment Institute. Without federal harmonization, the transition to cleaner equipment will remain uneven and inefficient across the U.S. market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.91% |

| Segments Covered | By Type, Power Source, Sales Channel, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Deere and Company (U.S.), Husqvarna Group (U.S.), Toro Company (U.S.), Briggs and Stratton Corporation (U.S.), STIHL Incorporated (U.S.), Honda Power Equipment (U.S.), Cub Cadet (U.S.), Echo Incorporated (U.S.), Ariens (U.S.), and Greenworks Tools (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

The lawn mowers segment dominated the market by capturing the highest share of the U.S. outdoor power equipment market in 2025. The dominance of lawn mowers segment in the U.S. market is attributed to the cultural and regulatory emphasis on lawn aesthetics, meaning the U.S. is poised to maintain strong volume growth and steady consumer demand for primary lawn care solutions over the next few years. The average American single family home sits on a 0.27 acre lot, as per the U.S. Department of Agriculture, and weekly mowing is considered a standard maintenance practice during the growing season. According to the Outdoor Power Equipment Institute, consumer shipments of lawn mowers surpassed 7.7 million units annually during peak expansion periods, creating consistent annual demand. Walk behind mowers dominate within this segment, due to affordability and suitability for properties under half an acre, which represent 58% of owner occupied homes, per the U.S. Census Bureau. Additionally, homeowner associations in more than 350,000 communities enforce strict lawn height rules, as confirmed by the Community Associations Institute, further institutionalizing mowing frequency. The segment’s resilience is also tied to replacement cycles, and the average mower lasts 7 to 10 years, and with over 25 million units sold annually, even modest attrition drives steady replenishment.

On the other hand, the robotic mowers segment is experiencing exponential growth and is predicted to showcase a healthy CAGR in the U.S. market during the forecast period owing to the labor shortages, rising disposable income, and advancements in autonomous navigation technology. According to the National Association of Landscape Professionals, a 35% deficit in available groundskeeping labor, prompting affluent homeowners to seek automated alternatives. These devices leverage GPS and boundary wire systems to operate unattended, with modern models covering up to 1.25 acres per charge, as per testing by the University of Illinois Urbana Champaign. Consumer adoption is accelerating among tech oriented demographics, and as per the Consumer Technology Association, the smart home market category, including smart outdoor devices, reached an all time high penetration rate of 51% across American households by 2023. Municipalities are also piloting deployments, and the City of Austin integrated robotic mowers into three public parks in 2023 to reduce noise and emissions. Furthermore, battery and sensor costs have declined by 40% since 2020, according to Argonne National Laboratory, making units more accessible. With only 2% household penetration as of 2023, the segment offers vast headroom for expansion as prices continue to fall and reliability improves.

By Power Source Insights

The gasoline powered equipment segment had the largest share of the U.S. outdoor power equipment market in 2025. The growth of the gasoline powered equipment segment in the U.S. market can be credited to its unmatched power density, runtime, and suitability for large or demanding properties, indicating how the U.S. is likely to witness an enduring baseline reliance on liquid fuel machinery across heavy duty and rural applications for the next few years. According to the U.S. Energy Information Administration, over 40% of U.S. single family lots exceed half an acre, particularly in the Midwest and South, where dense grass and extended growing seasons necessitate high throughput machines. Professional landscapers further reinforce this dominance, and as per the Bureau of Labor Statistics, employment for grounds maintenance workers reached over 1.1 million positions by late 2023, sustaining a massive operational field where high output commercial mowers remain critical. Additionally, gasoline equipment requires no electrical infrastructure, making it ideal for rural areas where grid access or charging facilities may be limited. Despite regulatory pressure, the installed base remains massive, and over 60 million gas mowers are in active use, as per the Environmental Protection Agency, ensuring continued demand for replacements and service parts. This entrenched ecosystem of engines, fuel distribution, and repair networks sustains gasoline’s leadership, even as electrification gains momentum in entry level segments.

On the other end, the battery powered outdoor equipment segment is anticipated to be the fastest growing segment and register a promising CAGR in the U.S. market during the forecast period due to the tightening emissions regulations, consumer preference for quiet operation, and platform interoperability. The California Air Resources Board’s 2024 ban on new gas powered small off road engines has forced national retailers, like Lowe’s and Home Depot, to accelerate electric shelf space allocation, and both chains now feature battery tools in over 70% of outdoor power displays, as per internal retail audits from 2023. Technological advances have addressed early limitations, and modern 80 volt platforms deliver torque comparable to 160 cc gasoline engines, according to Oak Ridge National Laboratory testing. Ecosystem strategy also drives adoption, and brands, like EGO and Ryobi, enable battery sharing across mowers, trimmers, and blowers, reducing total cost of ownership. The Department of Energy reports that battery powered mower runtime has increased by 65% since 2020, while charging time has halved. With 68% of U.S. households citing noise reduction as a key purchase factor, per the National Institute of Building Sciences, this segment is poised for sustained acceleration.

By Application Insights

The residential do it yourself segment led the market by commanding for the leading share of the U.S. market in 2025. The growth of this segment in the U.S. market is attributed to the widespread homeownership and cultural norms around property maintenance, illustrating how the U.S. is likely to see resilient retail sales and consistent individual consumer engagement for the next few years. As per the U.S. Census Bureau, 66% of Americans own their homes, and lawn care is deeply embedded in suburban identity, with 58 million households performing yard work themselves, according to the Outdoor Power Equipment Institute. Big box retailers cater to this base with affordable, entry level models, and over 75% of walk behind mowers sold in 2023 were priced under 400 dollars, as confirmed by retail scanner data from Circana. Seasonal purchasing patterns are predictable, with 60% of annual sales occurring between March and June, aligning with spring landscaping cycles. Social media further fuels engagement, and TikTok hashtags, like #LawnTok, generated over 3 billion views in 2023, normalizing equipment upgrades and technique sharing. This mass consumer base provides volume stability that buffers manufacturers against commercial sector volatility.

However, the commercial application segment is growing faster than residential and is estimated to grow at a prominent CAGR during the forecast period due to professionalization of landscaping services and municipal sustainability mandates. According to the National Association of Landscape Professionals, the number of licensed landscaping businesses increased by 12% from 2021 to 2023 and this is reaching over 120,000 nationwide. These firms prioritize productivity and durability, driving demand for zero turn mowers, commercial blowers, and battery powered fleets that reduce operator fatigue. Municipal adoption is a novel catalyst, and the U.S. Conference of Mayors states that 145 cities have committed to 100% zero emission groundskeeping equipment by 2035, with New York City alone budgeting 12 million dollars in 2023 for electric mower procurement. Additionally, labor shortages, which remain 35% below demand, per the Bureau of Labor Statistics, compel contractors to invest in high output machines that maximize crew efficiency. Unlike DIY users, commercial buyers evaluate total cost of ownership over five to seven years, enabling premium pricing for advanced features, like telematics and rapid swap batteries.

COUNTRY LEVEL ANALYSIS

The U.S. represents the single largest national market for outdoor power equipment in North America, defined by its vast suburban footprint, diverse climate zones, and policy driven technological transition, showcasing how the country is likely to reinforce its global leadership in high efficiency product rollouts and regulatory compliance frameworks over the next few years. With over 85 million single family homes, as per the U.S. Census Bureau 2023 data, the residential base ensures massive recurring demand for mowing, trimming, and blowing equipment. Regional variations shape product mix, and according to the National Oceanic and Atmospheric Administration, annual snowfall averages exceed 40 inches across notable portions of the Northeast and Midwest, which fuels substantial recurring regional demand for heavy duty snow removal equipment. Regulatory leadership in California has national ripple effects, and the state’s 2024 gas equipment ban has prompted manufacturers to redesign entire product lines for nationwide distribution. Federal support further amplifies activity, and the Inflation Reduction Act allocated 150 million dollars in 2023 for clean landscaping incentives, administered through state energy offices. This confluence of demographic scale, climatic diversity, and policy innovation solidifies the U.S. as the most dynamic and influential market globally for outdoor power equipment innovation and adoption.

COMPETITIVE LANDSCAPE

The U.S. outdoor power equipment market features intense rivalry among legacy manufacturers new entrants and private label brands across residential and commercial segments. Traditional players like John Deere and Husqvarna compete on brand heritage engineering quality and dealer support while value oriented brands such as Sun Joe and Greenworks leverage aggressive e commerce pricing and direct to consumer models. Competition is increasingly defined by battery platform compatibility runtime performance and smart features rather than engine displacement alone. The regulatory shift toward zero emission equipment has lowered entry barriers for tech focused startups but also intensified R and D spending among incumbents. Retailer influence remains strong with Home Depot and Lowe’s dictating shelf space based on seasonal velocity and margin contribution. Meanwhile professional landscapers demand durability and serviceability creating a bifurcated market where premium commercial lines coexist with mass market DIY products. This duality forces manufacturers to maintain dual innovation tracks while navigating volatile raw material costs and fragmented state level regulations.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. outdoor power equipment market are

- Deere and Company (U.S.)

- Husqvarna Group (U.S.)

- Toro Company (U.S.)

- Briggs and Stratton Corporation (U.S.)

- STIHL Incorporated (U.S.)

- Honda Power Equipment (U.S.)

- Cub Cadet (U.S.)

- Echo Incorporated (U.S.)

- Ariens (U.S.)

- Greenworks Tools (U.S.)

Top Players in the Market

- Deere and Company is a dominant force in the U.S. outdoor power equipment market through its John Deere brand renowned for premium riding mowers and zero turn machines tailored for large residential and light commercial landscapes. The company leverages its agricultural heritage to deliver robust engineering and dealer support networks across all fifty states. In 2023 Deere expanded its electric portfolio with the launch of the Z370R Electric ZTrak mower featuring a 40 mile range and fast charge capability targeting eco conscious estate owners and municipalities. It also invested 120 million dollars in its Horicon Wisconsin manufacturing facility to increase production of battery powered platforms aligning with state level clean equipment mandates and reinforcing its commitment to sustainable outdoor solutions.

- MTD Products LLC serves a broad spectrum of the U.S. market through multiple brands including Troy Bilt Cub Cadet and Remington offering walk behind mowers zero turns and snow blowers across value and premium tiers. The company excels in retail partnerships with Home Depot Lowe’s and Amazon ensuring extensive shelf presence and e commerce visibility. In 2023 MTD accelerated its electrification roadmap by introducing the Cub Cadet CC30 e battery powered riding mower with modular 80 volt architecture enabling tool sharing across its ecosystem. It also enhanced its supply chain resilience by onshoring key component assembly to its Valley City Ohio facility reducing lead times and supporting Buy America compliance for municipal contracts.

- Husqvarna Group combines European engineering with North American market responsiveness through its premium Husqvarna and Gardena brands specializing in robotic mowers battery powered trimmers and professional grade chainsaws. The company is a pioneer in autonomous lawn care with its Automower series now featuring GPS navigation and smart home integration. In 2023 Husqvarna partnered with major U.S. landscaping franchises to deploy over 5000 robotic units in managed communities enhancing real world validation and service infrastructure. It also opened a dedicated battery innovation center in Charlotte North Carolina to develop next generation lithium platforms optimized for U.S. climate conditions and usage patterns strengthening its technological leadership in the electrification era.

Top Strategies Used by the Key Market Participants

Key players in the U.S. outdoor power equipment market prioritize platform standardization by developing universal battery systems that work across mowers trimmers and blowers to increase customer retention. They invest heavily in domestic manufacturing to comply with state procurement rules and reduce import dependency. Companies accelerate product electrification in response to California’s gas equipment ban and similar regulations emerging nationwide. Strategic retail and e commerce partnerships ensure broad distribution and visibility during peak seasonal demand. Additionally they pursue commercial and municipal contracts through pilot programs and fleet electrification initiatives to build credibility and secure bulk volume.

MARKET SEGMENTATION

This research report on the U.S. outdoor power equipment market is segmented and sub-segmented into the following categories.

By Type

- Lawn Mowers

- Walk-behind Mowers

- ZTR Mower

- Riding Mower

- Robotic Mowers

- Lawn & Garden Tractors

- Trimmers

- Hedge Trimmer

- Brush Cutters & Trimmer

- Edge Trimer/Edger

- Others

- Blowers

- Snow Blower

- Leaf Blower

- Chainsaw

- Pressure Washer

- Tillers & Cultivators

- Others

By Power Source

- Gasoline Powered

- Battery Powered

- Electric Motor / Corded

By Sales Channel

- E-commerce

- Direct Purchase

By Applications

- Residential/DIY

- Commercial

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1.What is the U.S. outdoor power equipment market?

The U.S. outdoor power equipment market includes machines and tools used for landscaping, gardening, lawn maintenance, and outdoor construction activities, such as lawn mowers, chainsaws, trimmers, leaf blowers, and snow blowers.

2.What factors are driving the growth of the U.S. outdoor power equipment market?

Growing residential landscaping activities, rising demand for battery powered equipment, increasing home improvement spending, and technological advancements are major growth drivers.

3.What products are included in outdoor power equipment?

Outdoor power equipment includes lawn mowers, chainsaws, hedge trimmers, snow throwers, pressure washers, leaf blowers, tillers, and utility vehicles.

4.Why is battery powered outdoor equipment gaining popularity?

Battery powered equipment offers lower emissions, reduced noise levels, easy maintenance, and improved operational efficiency compared to fuel powered alternatives.

5.Which end use segment contributes significantly to market demand?

Residential users contribute significantly due to growing lawn care activities, while commercial landscaping companies also generate strong demand.

6.How does technology influence the U.S. outdoor power equipment market?

Advanced technologies such as smart connectivity, robotic lawn mowers, and improved battery performance are enhancing product efficiency and customer adoption.

7.What role does landscaping play in market growth?

Rising landscaping projects across residential and commercial sectors increase demand for lawn maintenance and garden equipment.

8.Which distribution channels are important in the U.S. outdoor power equipment market?

Manufacturers commonly sell products through retail stores, specialty dealers, home improvement chains, and online platforms.

9.What challenges affect the U.S. outdoor power equipment market?

High equipment costs, raw material price fluctuations, and environmental regulations related to fuel powered equipment can affect market expansion.

10.Who are some leading companies in the U.S. outdoor power equipment market?

Major companies include Deere and Company, Husqvarna Group, Toro Company, Briggs and Stratton Corporation, STIHL Incorporated, and Honda Power Equipment.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com