U.S. Pickup Truck Market Size, Share, Trends & Growth Forecast Report By Truck Type, Propulsion Type, Component, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Pickup Truck Market Report Summary

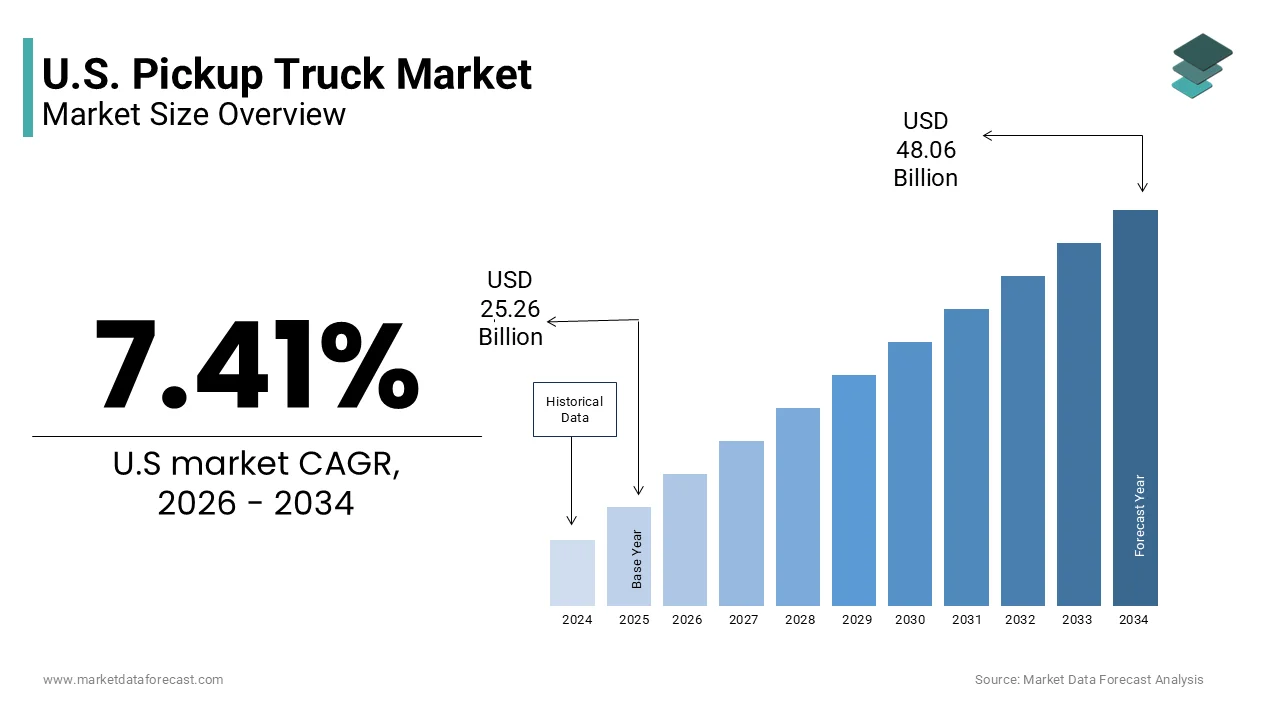

The U.S. pickup truck market was valued at USD 25.26 billion in 2025, is estimated to reach USD 27.13 billion in 2026, and is projected to reach USD 48.06 billion by 2034, growing at a CAGR of 7.41% during the forecast period. Market growth is driven by rising demand for utility vehicles, increasing adoption of advanced vehicle technologies, and growing consumer preference for versatile transportation solutions across personal and commercial applications. Pickup trucks continue to play a vital role in construction, logistics, agriculture, and recreational activities due to their durability, towing capacity, and multifunctional capabilities. Expanding electrification trends and technological advancements are further supporting market expansion across the United States.

Key Market Trends

- Growing demand for utility and multipurpose vehicles is driving market growth.

- Increasing adoption of advanced driver assistance systems and connectivity features is boosting market expansion.

- Rising consumer preference for high performance and premium pickup trucks is supporting market demand.

- Expansion of electric and hybrid vehicle technologies is influencing market transformation.

- Innovation in vehicle electronics, safety technologies, and fuel efficiency solutions is shaping industry development.

Segmental Insights

- Based on truck type, the full size pickup trucks segment accounted for the dominant share of the U.S. pickup truck market in 2025. This dominance is attributed to strong consumer preference for towing capacity, cargo capability, and versatility across personal and commercial applications.

- Based on propulsion type, the gasoline powered pickup trucks segment held the leading share of the U.S. pickup truck market in 2025, supported by widespread infrastructure availability and established consumer demand.

- Based on component, the electrical and electronics segment accounted for the majority share of the U.S. pickup truck component market in 2025, driven by increasing integration of advanced vehicle technologies and connected automotive systems.

Regional Insights

- The United States remains one of the largest pickup truck markets globally, supported by strong consumer demand, expanding commercial vehicle applications, and ongoing advancements in vehicle technologies. Increasing investment in electrification and connected mobility solutions continues to strengthen market development.

Competitive Landscape

The U.S. pickup truck market is highly competitive, with manufacturers focusing on electrification, connectivity technologies, fuel efficiency improvements, and advanced safety systems to strengthen their market position. Companies are investing in premium vehicle features and next generation mobility technologies. Prominent players in the U.S. pickup truck market include Ford Motor Company, General Motors Holdings LLC, STELLANTIS N.V., Toyota Motor Corporation, Nissan Motor Co., Ltd., Honda Motor Co., Ltd., Tesla, Inc., Rivian Europe B.V., Workhorse Group, Inc., and Mitsubishi Motors Corporation.

U.S. Pickup Truck Market Size

The U.S. pickup truck market was valued at USD 25.26 billion in 2025, is estimated to reach USD 27.13 billion in 2026, and is projected to reach USD 48.06 billion by 2034, growing at a CAGR of 7.41% from 2026 to 2034.

A pickup truck is a versatile light-duty vehicle with an enclosed passenger cabin and an open, flat cargo bed at the rear. These vehicles have evolved from purely utilitarian workhorses into sophisticated multi-purpose machines that serve both commercial enterprises and personal lifestyle needs. The cultural significance of the pickup truck in America is profound with these vehicles symbolizing independence ruggedness and practicality. According to automotive market data reviewed by the U.S. Bureau of Transportation Statistics, light trucks, including pickups, sport utility vehicles (SUVs), and crossovers, collectively dominated roughly 75% of all new light-duty vehicle sales in the United States, reflecting a decisive, long-term shift away from traditional sedans. According to the latest comprehensive fleet analyses from S&P Global Mobility, the average age of light vehicles operating on U.S. roads has climbed to a record 12.8 years, indicating that consumers are maintaining their vehicles longer and extending overall replacement cycles. Furthermore, the Federal Highway Administration states that there are over 4 million miles of public roads in the United States much of which traverses rural and semi urban areas where pickup trucks are often the most viable transportation option due to their durability and off road capabilities. The integration of advanced safety technologies and luxury amenities has further broadened the appeal of pickup trucks attracting demographics that previously favored sport utility vehicles or sedans. This transformation underscores the market's resilience and its ability to adapt to changing economic conditions and consumer lifestyles while maintaining its core identity as a versatile and robust mode of transportation essential to the American way of life.

MARKET DRIVERS

Robust Growth in Construction and Infrastructure Development

The sustained expansion of the construction industry and significant federal investments in infrastructure are a major factor accelerating the growth of the United States pickup truck market. Pickup trucks are indispensable assets for contractors builders and tradespeople who require reliable vehicles to transport tools materials and equipment to job sites. According to the U.S. Census Bureau, the total annual value of construction put in place for 2023 reached nearly $2.0 trillion ($1,978.7 billion), signaling sustained, high-volume activity across residential and non-residential sectors. This high level of construction activity necessitates a fleet of durable and capable vehicles that can handle heavy loads and navigate rough terrain. The Bipartisan Infrastructure Law authorizes $1.2 trillion in total spending, including $550 billion in new federal investment, targeting roads, bridges, and broadband, which directly amplifies long-term demand for commercial construction vehicles. The Associated General Contractors of America (AGC) notes that while federal infrastructure funding has bolstered project backlogs, actual ground-breaking has faced headwinds from regulatory compliance rules and acute labor shortages, sustaining a complex but high-demand environment for fleet expansion. Pickup trucks offer the versatility required for diverse tasks ranging from hauling lumber to towing trailers making them the preferred choice for professionals in the field. The reliability and payload capacity of modern pickup trucks ensure that they can meet the rigorous demands of daily construction operations without compromising on performance. This consistent industrial demand provides a stable foundation for market growth ensuring that manufacturers continue to prioritize features that enhance utility and durability for commercial users.

Increasing Consumer Preference for Versatility and Lifestyle Utility

Beyond commercial applications the growing consumer preference for vehicles that offer versatility and lifestyle utility greatly drives the United States pickup truck market. Modern buyers increasingly seek vehicles that can seamlessly transition from weekday work duties to weekend recreational activities such as camping boating and off roading. According to J.D. Power the average transaction price for a pickup truck has risen steadily reflecting the addition of premium features and advanced technologies that appeal to retail customers. The ability of pickup trucks to tow boats trailers and recreational vehicles makes them ideal for families and individuals who engage in outdoor hobbies. The RV Industry Association (RVIA) reports that while total shipments normalized following the pandemic boom, the towable RV segment remains the dominant category, sustaining structural demand for heavy-duty pickup trucks capable of hauling travel trailers. The spacious interiors and customizable bed configurations allow users to adapt the vehicle to various needs enhancing its overall value proposition. Furthermore the perception of pickup trucks as safer and more commanding on the road compared to smaller cars influences purchasing decisions among suburban and rural households. Manufacturers have responded by offering crew cab configurations with luxurious amenities blurring the lines between work trucks and premium SUVs. This dual purpose appeal ensures a broad customer base that values both functionality and comfort thereby sustaining high demand levels across diverse demographic segments throughout the United States.

MARKET RESTRAINTS

Volatility in Fuel Prices and Operational Costs

The volatility of fuel prices and the associated operational costs is a significant hurdle for the United States pickup truck market. Pickup trucks generally have lower fuel efficiency compared to smaller passenger vehicles due to their larger engines and heavier builds. According to data from the U.S. Energy Information Administration (EIA), retail prices for regular gasoline have exhibited intense volatility, with national averages topping $5.00 per gallon and regional markets peaking well above $6.00 per gallon during severe supply shocks. These high fuel costs increase the total cost of ownership for pickup truck owners particularly for those who use their vehicles for daily commuting or long-distance travel. Fleet evaluation reports from the U.S. Environmental Protection Agency (EPA) confirm that the average real-world fuel economy for pickup trucks stands at approximately 21.5 mpg, highlighting a persistent operational cost gap when compared to standard passenger cars. This disparity makes pickup trucks less attractive to budget conscious consumers who are sensitive to recurring fuel expenses. Additionally, the potential for future carbon taxes or emissions regulations could further increase operating costs discouraging some buyers from choosing large displacement engines. While diesel options offer better torque and efficiency they often come with higher upfront costs and maintenance requirements. The uncertainty surrounding long term energy prices creates hesitation among potential buyers who may opt for more fuel-efficient alternatives such as crossover SUVs or electric vehicles. This economic pressure constrains market growth by limiting the affordability and appeal of traditional internal combustion engine pickup trucks in an increasingly cost conscious environment.

Stringent Emissions Regulations and Environmental Compliance

Stringent emissions regulations and the push for environmental compliance are a substantial restraint on the traditional pickup truck landscape within the United States market. Government agencies are implementing tougher standards to reduce greenhouse gas emissions and air pollutants from light duty vehicles including pickup trucks. According to the Environmental Protection Agency the revised greenhouse gas emissions standards for model years 2027 through 2032 require significant reductions in carbon dioxide emissions compelling manufacturers to invest heavily in cleaner technologies. These regulations often necessitate the adoption of complex exhaust after treatment systems which can increase vehicle weight and reduce payload capacity. Vehicle manufacturers face substantial development overhead and extended launch timelines to navigate compliance testing, as the National Highway Traffic Safety Administration (NHTSA) harmonizes its CAFE standards alongside strict emission verification paths. Manufacturers must balance performance and utility with environmental responsibility which can be challenging for large vehicles designed for heavy duty tasks. The transition to compliant engines may also lead to higher retail prices as costs are passed on to consumers. Furthermore some local jurisdictions are introducing low emission zones that restrict access for older or higher emitting vehicles limiting the usability of certain pickup trucks in urban areas. These regulatory pressures force manufacturers to rethink design strategies and powertrain options potentially alienating traditional buyers who prioritize raw power and simplicity. The ongoing tension between regulatory mandates and consumer expectations creates a complex landscape that restrains the unchecked growth of conventional pickup truck segments.

MARKET OPPORTUNITIES

Expansion of Electric and Hybrid Pickup Truck Segments

The rapid expansion of electric and hybrid pickup truck segments generates new potential for growth and innovation within the United States pickup truck market. Automakers are increasingly investing in electrified powertrains to meet consumer demand for sustainable yet capable vehicles. According to the International Energy Agency (IEA), global electric car sales surpassed 10 million units in 2022, laying the groundwork for manufacturers to expand zero-emission platforms into commercial trucking and consumer utility segments. In the United States models such as the Ford F 150 Lightning and the Rivian R1T have demonstrated strong consumer interest proving that electric pickups can deliver comparable performance to traditional counterparts. Administered via the Internal Revenue Service (IRS), federal clean vehicle tax credits of up to $7,500 incentivize the adoption of qualified electric pickups that satisfy stringent North American assembly, critical mineral, and battery component criteria. Electric pickups offer unique advantages such as instant torque silent operation and the ability to serve as mobile power sources for tools and homes. These features appeal to both commercial users and tech savvy consumers looking for innovative solutions. The development of dedicated electric platforms allows for optimized interior space and storage enhancing usability. Furthermore the growing network of fast charging stations across the country alleviates range anxiety making electric pickups more practical for daily use. By capitalizing on this trend manufacturers can capture new market segments and differentiate their offerings in a crowded landscape. The shift toward electrification also aligns with corporate sustainability goals attracting environmentally conscious buyers and fleet operators seeking to reduce their carbon footprints.

Integration of Advanced Connectivity and Autonomous Features

The integration of advanced connectivity and autonomous driving features opens the door for enhancing the value and appeal of these trucks, which is likely to promote the expansion of the United States pickup trucks market. Consumers are increasingly expecting smart technologies that improve safety convenience and productivity in their vehicles. According to the Consumer Technology Association the adoption of connected car services is rising with users seeking seamless integration with smartphones and home devices. Modern pickup trucks are being equipped with sophisticated infotainment systems over the air update capabilities and advanced driver assistance systems such as adaptive cruise control and lane keeping assist. Statistical research from the Insurance Institute for Highway Safety (IIHS) demonstrates that vehicles outfitted with advanced driver assistance systems (ADAS), such as automatic emergency braking, experience significantly lower collision rates, lowering risk profiles for insurance carriers. The ability to monitor vehicle health remotely and schedule maintenance proactively enhances the ownership experience and reduces downtime for commercial users. Furthermore, the development of semi-autonomous towing aids simplifies the process of hitching and maneuvering trailers addressing a common pain point for pickup owners. These technological advancements create new revenue streams for manufacturers through software subscriptions and data services. By positioning pickup trucks as high-tech hubs rather than just utility vehicles automakers can attract a younger demographic that values digital connectivity. This evolution opens up possibilities for personalized user experiences and enhanced functionality thereby strengthening brand loyalty and driving market growth in the premium segment.

MARKET CHALLENGES

Supply Chain Disruptions and Semiconductor Shortages

Supply chain disruptions and persistent semiconductor shortages are holding back the growth of the United States pickup truck market. The production of modern pickup trucks relies heavily on complex electronic components for everything from engine management to infotainment systems. Microeconomic data shows that consecutive global semiconductor shortages have resulted in the loss of millions of vehicle productions worldwide, severely crippling dealership inventory levels and extending consumer delivery windows. These disruptions force manufacturers to prioritize high margin models such as premium pickup trucks leaving lower trim levels with limited inventory. As per the Federal Reserve Bank of St. Louis supply chain bottlenecks have contributed to elevated vehicle prices reducing affordability for many consumers. The reliance on single source suppliers for critical components increases vulnerability to geopolitical tensions and natural disasters. For instance delays in chip fabrication in Asia can halt assembly lines in North America causing significant financial losses. Manufacturers are struggling to balance production schedules with uncertain component supplies leading to inconsistent dealer inventories. This unpredictability frustrates customers who face long wait times for their desired configurations. Additionally the cost of securing alternative supply chains and stockpiling components increases operational expenses for automakers. Until the supply chain stabilizes and diversifies the market will continue to face constraints that limit growth and customer satisfaction. Addressing these logistical hurdles requires strategic partnerships and investment in domestic manufacturing capabilities to ensure resilience against future shocks.

Intense Competition and Market Saturation

Intense competition and market saturation are a serious challenge to established players in the United States pickup truck market. The segment is dominated by a few key manufacturers who continuously innovate to maintain their market positions leading to a highly competitive environment. This saturation means that manufacturers must invest heavily in marketing and incentives to attract buyers which erodes profit margins. A study indicates that the average manufacturer incentive spend per vehicle has risen steadily, as a structural rebound in dealership inventory availability compels brands to offer aggressive promotional discounts to attract buyers. New entrants including electric vehicle startups are disrupting the traditional landscape by offering novel designs and technologies that appeal to early adopters. This fragmentation of the market forces legacy automakers to accelerate their innovation cycles and diversify their product portfolios. The pressure to differentiate through niche features such as off road packages or luxury interiors adds complexity to production and supply chains. Furthermore customer loyalty is being tested as buyers explore alternative options that offer better value or unique capabilities. The constant need to outperform competitors in terms of technology price and reliability creates a stressful operational environment. Navigating this saturated market requires strategic agility and a deep understanding of evolving consumer preferences to sustain long term success.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.41% |

| Segments Covered | By Truck Type, Propulsion Type, Component, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Ford Motor Company, General Motors Holdings LLC, STELLANTIS N.V., Toyota Motor Corporation, Nissan Motor Co., Ltd., Honda Motor Co., Ltd., Tesla, Inc., Rivian Europe B.V., Workhorse Group, Inc., and Mitsubishi Motors Corporation |

SEGMENTAL ANALYSIS

By Truck Type Insights

The full size pickup trucks segment dominated the United States pickup truck market and accounted for a substantial share in 2025. This dominance of the segment was driven by the unparalleled versatility and capability that these vehicles offer to both commercial and consumer segments. One of the major factors driving this segment is the critical role full size trucks play in the American construction and agricultural industries. According to the Bureau of Labor Statistics the construction industry employed approximately 8 million workers in 2023 many of whom rely on full size pickups for transporting heavy equipment and materials. These vehicles provide the necessary payload capacity often exceeding 2000 pounds and towing capabilities ranging from 10000 to 14000 pounds which are essential for professional tradespeople. Also keeping this segment in the lead is the cultural entrenchment of full size trucks as primary family vehicles in suburban and rural areas. As per J.D. Power full size pickups consistently rank high in consumer satisfaction due to their spacious interiors and advanced technology features that rival luxury SUVs. The shift towards luxury has broadened the appeal beyond traditional work users to include affluent buyers seeking status and comfort. Manufacturers continue to innovate with crew cab configurations that offer ample passenger space making them practical for daily commuting and family travel. The combination of industrial utility and lifestyle appeal ensures that full size trucks remain the backbone of the US automotive market.

However, the midsize pickup truck segment is estimated to register the fastest CAGR of 6.5% over the forecast period. This rapid expansion of the segment is fuelled by changing consumer preferences towards more manageable vehicle sizes without sacrificing utility. The main driver for this growth is the increasing demand for versatile vehicles that can navigate urban environments while still offering off road capabilities. According to Edmunds midsize trucks such as the Toyota Tacoma and Ford Ranger have seen significant sales increases as buyers seek alternatives to larger full size models that are difficult to park and maneuver in cities. These vehicles offer a balanced footprint that appeals to younger demographics and outdoor enthusiasts who value agility. A further key driving factor is the introduction of new models and refreshed designs that have revitalized consumer interest in the segment. Additionally the availability of diesel engine options in some midsize models provides better fuel efficiency which is a key consideration for cost conscious buyers. The growing popularity of overlanding and recreational activities also boosts demand as midsize trucks are ideal for carrying camping gear and navigating rough trails. This combination of urban practicality and outdoor readiness positions the midsize segment for sustained growth as consumers prioritize flexibility and efficiency in their vehicle choices.

By Propulsion Type Insights

The gasoline powered pickup trucks segment led the United States market and captured a significant share in 2025. This leading position of the segment was attributed to the established infrastructure and consumer familiarity with internal combustion engines. The main reason this segment is on top is the extensive network of gasoline refueling stations across the country which ensures convenience and reliability for drivers. According to data from the National Association of Convenience Stores (NACS), there are over 116,000 convenience stores selling fuel across the United States, providing a ubiquitous fueling infrastructure that supports both urban and remote rural pickup truck operations. This accessibility eliminates range anxiety and supports the long distance travel needs of commercial and personal users. A key reason for continued top ranking is the lower upfront cost of gasoline trucks compared to electric or hybrid alternatives. As per Kelley Blue Book the average price of a gasoline powered half ton pickup remains significantly lower than its electric counterpart making it a more affordable option for budget conscious buyers. Additionally, gasoline engines offer proven durability and ease of repair with a wide availability of parts and skilled mechanics. The performance characteristics of modern gasoline engines including high torque and horsepower meet the demanding requirements of towing and hauling. Despite the rise of alternative fuels the maturity and reliability of gasoline technology ensure its continued leadership in the market. Consumers trust the predictable performance and maintenance costs of gasoline engines which reinforces their preference for this propulsion type in the rugged and demanding context of pickup truck usage.

On the other hand, the electric propulsion segment is anticipated to witness the fastest CAGR of 25.5% from 2026 to 2034 owing to technological advancements and supportive government policies aimed at reducing emissions. The driving force behind the rise is the introduction of compelling electric models that match or exceed the performance of traditional gasoline trucks. According to the Department of Energy the Ford F 150 Lightning and Rivian R1T have demonstrated that electric pickups can offer superior torque instant acceleration and innovative features such as vehicle to load power output. These capabilities appeal to both tech savvy consumers and commercial users who benefit from lower operating costs. A major factor keeping them ahead is the availability of federal incentives that reduce the effective purchase price of electric vehicles. Additionally state level rebates and access to carpool lanes further enhance the value proposition. The growing charging infrastructure supported by the Bipartisan Infrastructure Law also alleviates range concerns. As battery costs decline and energy density improves electric pickups are becoming increasingly practical for daily use. This convergence of performance incentives and infrastructure development positions electric propulsion as a transformative force in the pickup truck market.

By Component Insights

In 2025, the electrical and electronics segment held the majority share of the United States pickup truck component market because of the increasing integration of advanced technologies in modern vehicles. Manufacturers incorporate these parts to provide sophisticated systems for safety, connectivity, and performance. A major reason for this dominance is the widespread adoption of advanced driver assistance systems (ADAS) which rely heavily on sensors cameras and radar. Driven by a voluntary safety commitment monitored by the Insurance Institute for Highway Safety (IIHS), the vast majority of new pickup trucks now feature automatic emergency braking (AEB) as standard equipment, dramatically improving crash-mitigation rates across the light truck segment. These systems require complex electronic architectures and software integration increasing the demand for high quality electrical components. Further strengthening this lead is the consumer demand for connected infotainment and digital cockpit experiences. Features such as large touchscreens smartphone integration and over the air updates have become standard expectations for buyers. Additionally, the electrification of powertrains necessitates high voltage wiring harnesses and battery management systems which further boost the electrical component segment. The reliance on software defined vehicles means that electronics are no longer just accessories but core elements of vehicle functionality. This trend ensures that the electrical and electronics segment remains central to the value chain and innovation strategy of pickup truck manufacturers.

On the contrary, the interior component segment is likely to experience the fastest CAGR of 5.8% over the forecast period due to the transformation of pickup trucks into luxury lifestyle vehicles that prioritize comfort and convenience. The primary driver for this expansion is the increasing consumer expectation for premium materials and ergonomic designs in truck cabins. According to J.D. Power interior quality and comfort are among the top factors influencing purchase decisions for pickup truck buyers. Manufacturers are responding by incorporating leather upholstery heated and ventilated seats and ambient lighting into their models. The segment moves ahead quickly, driven by the need for enhanced storage and workspace solutions within the cabin. As per Consumer Reports modern pickup trucks are being designed with flexible seating arrangements and integrated work surfaces to accommodate mobile professionals. The rise of remote work has led to greater demand for vehicles that can serve as mobile offices requiring robust connectivity and comfortable seating for extended periods. Additionally the focus on noise reduction and climate control systems enhances the overall driving experience making the interior a key differentiator. As pickup trucks compete with luxury SUVs the investment in high quality interior components becomes essential for attracting affluent buyers. This shift towards premiumization ensures that the interior segment continues to grow in value and importance within the overall vehicle architecture.

COUNTRY LEVEL ANALYSIS

Texas was the top performer in the United States pickup truck market and accounted for a 15.5% share. This position is driven by the state's robust energy and construction industries which rely heavily on pickup trucks for daily operations. The main factor sustaining this dominance is the extensive oil and gas sector in Texas which requires durable vehicles for transporting equipment and personnel to remote sites. According to data reviewed by the Texas Comptroller of Public Accounts, the energy sector remains a foundational driver of the state's economy, with hundreds of active drilling rigs operating across major basins like the Permian, continuously generating substantial regional demand for fleet and support vehicles. Pickup trucks are essential for navigating the rugged terrain of oil fields and construction sites. A further key factor is the cultural affinity for pickup trucks in Texas where they are seen as symbols of independence and practicality. Commercial auto sales data indicates that pickup trucks consistently rank as the top-selling consumer vehicles in Texas, highlighting deep-rooted regional utility and market preferences across the state's workforce. The large geographic size of Texas also necessitates vehicles with long range and high towing capacity for personal and commercial use. Additionally the state's favorable tax policies and lack of income tax increase disposable income allowing residents to invest in higher trim levels and specialized models. The presence of major manufacturing facilities and dealerships further supports the market by ensuring easy access to vehicles and service. These economic cultural and logistical factors combine to make Texas the undisputed leader in the US pickup truck market.

California is rapidly growing in the United States pickup truck market due to strong regulatory pressure and environmental awareness that drive the adoption of zero emission vehicles. One of the major drivers for this unique market dynamic is the California Advanced Clean Fleets regulation which mandates the transition to zero emission trucks for certain commercial applications. As per the California Air Resources Board the state aims to have all new medium and heavy duty vehicle sales be zero emission by 2045 influencing pickup truck procurement strategies. This regulatory framework encourages both businesses and consumers to consider electric pickup options. A different factor is the high concentration of technology adopters and environmentally conscious consumers in urban areas such as Los Angeles and San Francisco. The state's extensive charging infrastructure supported by government investments also facilitates the use of electric pickups. Additionally the diverse geography of California ranging from coastal cities to mountainous regions creates demand for versatile vehicles that can handle various conditions. While traditional gasoline trucks remain popular the shift towards sustainable mobility positions California as a key market for future innovations in the pick

COMPETITIVE LANDSCAPE

The competition in the United States pickup truck market is intense characterized by fierce rivalry among established automakers striving for dominance. Ford General Motors and Stellantis lead the sector with strong brand heritage and extensive distribution networks. These companies continuously innovate to differentiate their offerings through advanced technology superior performance and luxury features. The entry of new electric vehicle manufacturers adds pressure prompting legacy brands to accelerate their electrification plans. Price wars and promotional incentives are common tactics used to attract budget conscious buyers during economic fluctuations. Product launches are strategically timed to maximize visibility and capture market attention. Manufacturers invest heavily in research and development to improve fuel efficiency and reduce emissions complying with stringent regulatory standards. Customer service and dealership experiences play crucial roles in influencing purchase decisions. Brand loyalty remains high but is increasingly tested by the availability of compelling alternatives. The market sees constant evolution as companies adapt to shifting consumer preferences towards sustainability and connectivity. This dynamic environment drives continuous improvement and innovation ensuring that consumers benefit from enhanced vehicle capabilities and value propositions across all segments.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. pickup truck market are

- Ford Motor Company

- General Motors Holdings LLC

- STELLANTIS N.V.

- Toyota Motor Corporation

- Nissan Motor Co., Ltd.

- Honda Motor Co., Ltd.

- Tesla, Inc.

- Rivian Europe B.V.

- Workhorse Group, Inc.

- Mitsubishi Motors Corporation

Top Players in the Market

- Ford Motor Company remains a cornerstone of the United States pickup truck market with its iconic F Series lineup serving as a benchmark for capability and innovation. The company has heavily invested in electrifying its flagship models notably launching the F 150 Lightning to cater to evolving consumer preferences for sustainable transportation. Ford continues to enhance its manufacturing capabilities by expanding production facilities in Michigan and Kentucky to meet robust demand. Recent initiatives include integrating advanced software platforms such as BlueCruise for hands free driving which enhances user experience and safety. The company also focuses on commercial solutions through Ford Pro offering tailored services for fleet managers to optimize productivity. By leveraging its extensive dealer network and strong brand loyalty Ford maintains a competitive edge. Strategic partnerships with technology firms further enable the development of connected vehicle features that appeal to modern buyers. These efforts ensure Ford remains at the forefront of innovation while addressing diverse customer needs across personal and commercial segments.

- General Motors strengthens its position in the United States pickup truck market through its Chevrolet and GMC brands which offer a diverse portfolio of full size and heavy duty trucks. The company has prioritized the development of electric variants such as the Chevrolet Silverado EV and GMC Hummer EV to capture emerging market segments. GM is investing billions in upgrading its assembly plants in Indiana and Texas to support increased production volumes and efficiency. Recent actions include the introduction of Ultium battery technology which provides enhanced range and performance for electric trucks. The company also emphasizes premium features in its GMC Sierra line targeting luxury buyers with high end interiors and advanced towing technologies. General Motors collaborates with charging network providers to ensure seamless infrastructure support for electric vehicle owners. By focusing on durability and cutting edge innovation GM appeals to both traditional truck enthusiasts and new age consumers. Their commitment to sustainability and technological advancement reinforces their leadership in the competitive landscape.

- Stellantis N.V. competes vigorously in the United States pickup truck market with its Ram brand known for combining rugged utility with refined comfort. The company has gained significant traction by introducing innovative features such as the Ram 1500 REV an all electric pickup designed to challenge established players. Recent strategies include enhancing the Uconnect digital ecosystem to provide superior connectivity and entertainment options for drivers. The company also focuses on lightweight materials and aerodynamic designs to improve fuel efficiency across its lineup. Ram’s emphasis on luxury interiors and versatile storage solutions like the RamBox distinguishes it from competitors. Stellantis leverages its global scale to optimize supply chains and reduce costs ensuring competitive pricing. By balancing traditional diesel performance with forward looking electric innovations Stellantis captures a broad spectrum of customers seeking reliability and modern amenities in their pickup trucks.

Top Strategies Used by Key Market Participants

Key players in the United States pickup truck market employ diverse strategies to maintain competitiveness and drive growth. Manufacturers prioritize product differentiation by introducing electric and hybrid models that align with environmental regulations and consumer demand for sustainability. Investment in advanced manufacturing technologies enables efficient production and cost reduction while ensuring high quality standards. Companies focus on enhancing digital connectivity through integrated software platforms that offer over the air updates and personalized user experiences. Strategic partnerships with technology firms facilitate the development of autonomous driving features and smart safety systems. Expanding charging infrastructure collaborations supports the adoption of electric pickups by alleviating range anxiety. Marketing efforts emphasize versatility and lifestyle appeal targeting both commercial users and recreational buyers. Customization options allow customers to tailor vehicles to specific needs increasing brand loyalty. After sales services including maintenance packages and warranty extensions strengthen customer relationships. These multifaceted approaches enable manufacturers to adapt to changing market dynamics and secure long term success in a highly competitive environment.

MARKET SEGMENTATION

This research report on the U.S. pickup truck market is segmented and sub-segmented into the following categories.

By Truck Type

- Small Size

- Midsize

- Full Size

By Propulsion Type

- Diesel

- Gasoline

- Hybrid

- Electric

By Component

- Drivetrain

- Interior

- Body

- Electrical & Electronics

- Chassis

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1.What is the U.S. Pickup Truck Market?

The U.S. Pickup Truck Market refers to the industry involved in the manufacturing, distribution, and sale of pickup trucks designed for personal transportation, commercial use, construction activities, and recreational purposes across the United States.

2.What factors are driving the growth of the U.S. Pickup Truck Market?

The market is growing due to increasing demand for utility vehicles, rising construction and logistics activities, technological advancements in vehicle performance, and growing consumer preference for versatile transportation options.

3.What are the major types of pickup trucks available in the U.S. market?

The market includes compact pickup trucks, midsize pickup trucks, full size pickup trucks, and heavy duty pickup trucks designed for different applications.

4.Who are the major consumers in the U.S. Pickup Truck Market?

Individual consumers, commercial fleet operators, construction companies, agricultural businesses, and logistics providers represent major end users in the market.

5.How are electric pickup trucks influencing the U.S. Pickup Truck Market?

Electric pickup trucks are expanding market opportunities by offering improved energy efficiency, reduced emissions, and advanced technology features.

6.What role does technology play in the U.S. Pickup Truck Market?

Manufacturers are integrating advanced driver assistance systems, connectivity features, enhanced safety technologies, and fuel efficient powertrain solutions.

7.What challenges affect the U.S. Pickup Truck Market?

Challenges include fluctuating raw material costs, supply chain disruptions, fuel price volatility, and increasing regulatory requirements related to emissions and safety.

8.Which trends are shaping the U.S. Pickup Truck Market?

Key trends include increasing electrification, rising demand for connected vehicle technologies, growing popularity of premium pickup models, and advancements in autonomous driving technologies.

9.How is sustainability influencing the U.S. Pickup Truck Market?

Manufacturers are investing in electric vehicle development, lightweight materials, and fuel efficient technologies to support sustainability initiatives.

10.Who are the key players operating in the U.S. Pickup Truck Market?

Major companies include Ford Motor Company, General Motors Holdings LLC, STELLANTIS N.V., Toyota Motor Corporation, Nissan Motor Co., Ltd., Honda Motor Co., Ltd., Tesla, Inc., Rivian Europe B.V., Workhorse Group, Inc., and Mitsubishi Motors Corporation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com