U.S. Printer Market Size, Share, Trends & Growth Forecast Report By Type, Technology, Output Type, Application, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Printer Market Report Summary

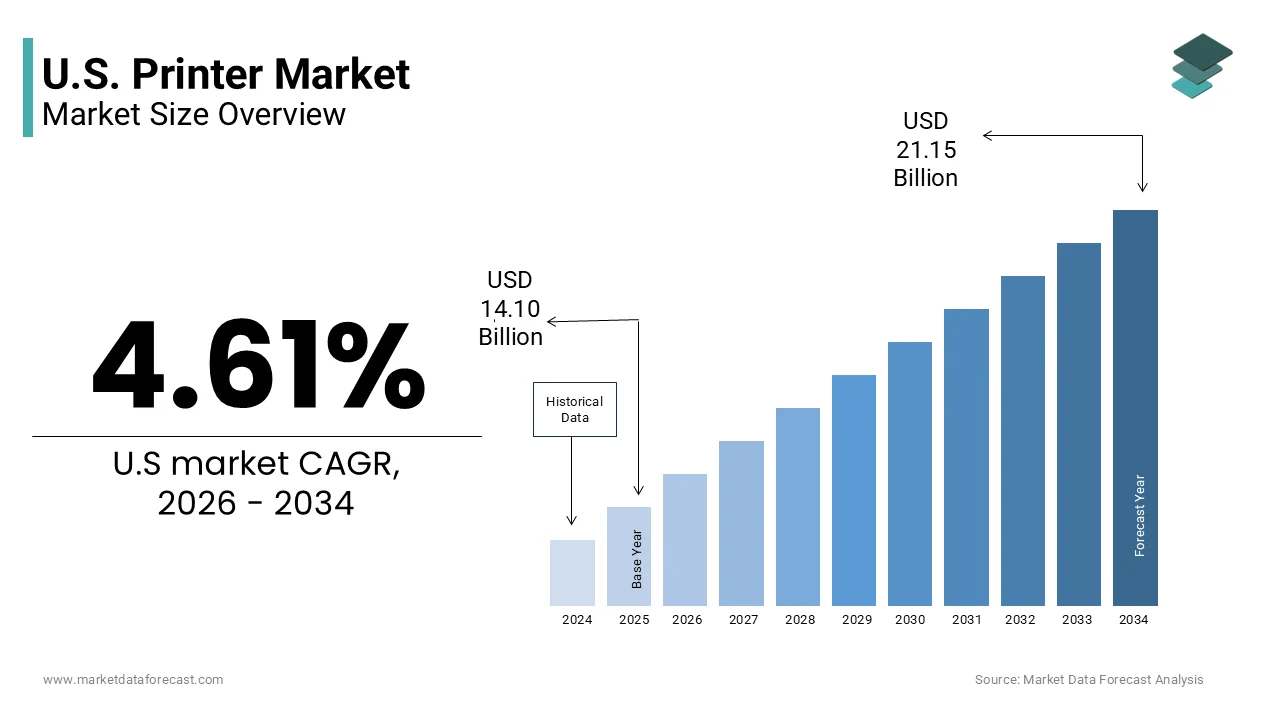

The U.S. printer market was valued at USD 14.10 billion in 2025, is estimated to reach USD 14.75 billion in 2026, and is projected to reach USD 21.15 billion by 2034, growing at a CAGR of 4.61% during the forecast period. Market growth is driven by increasing demand for commercial printing solutions, rising adoption of advanced office technologies, and expanding requirements for high efficiency printing systems across enterprises and institutions. Printers continue to play a critical role in offices, educational institutions, healthcare facilities, and industrial applications despite ongoing digital transformation trends. The growing integration of cloud printing, wireless connectivity, and managed print services is further supporting market expansion across the United States.

Key Market Trends

- Rising demand for efficient and high speed printing solutions is driving market growth.

- Increasing adoption of wireless, cloud based, and managed print technologies is boosting market expansion.

- Growing commercial and institutional printing requirements are supporting product demand.

- Expansion of multifunction printers and smart office infrastructure is enhancing operational efficiency.

- Innovation in energy efficient printers, automation, and remote print management is influencing market development.

Segmental Insights

- Based on type, the laser printer segment accounted for the dominant share of the U.S. printer market in 2025. This dominance is attributed to high speed printing capabilities, lower operating costs, and strong demand across commercial environments.

- Based on technology, the server based printing technology segment held the leading share of the U.S. printer market in 2025 and is expected to remain prominent in institutional and enterprise settings due to centralized management and security advantages.

- Based on application, the commercial segment accounted for the largest share of the U.S. printer market in 2025, driven by extensive use across offices, enterprises, educational institutions, and industrial printing operations.

Regional Insights

- The United States accounted for 33.7% of the global printer market share in 2025 and is expected to maintain its leadership position during the forecast period, supported by strong enterprise infrastructure, technological innovation, and widespread adoption of advanced printing solutions. Continued investments in smart office environments and enterprise printing systems are further strengthening market development.

Competitive Landscape

The U.S. printer market is highly competitive, with key players focusing on multifunction printing systems, cloud integration, and advanced commercial printing technologies to strengthen their market position. Companies are investing in energy efficient devices, wireless connectivity, and managed print services. Prominent players in the U.S. printer market include Brother Industries Ltd, Roland DG Corp, Ricoh Co Ltd, Xerox Holdings Corp, Toshiba Corporation, FUJIFILM Holdings Corp, Canon Inc, Panasonic Holdings Corp, and Seiko Epson Corp.

U.S. Printer Market Size

The U.S. printer market size was valued at USD 14.10 billion in 2025, is estimated to reach USD 14.75 billion in 2026, and is projected to reach USD 21.15 billion by 2034, growing at a CAGR of 4.61% from 2026 to 2034.

As remote work becomes entrenched, the demand for home office printing solutions has stabilized after an initial pandemic surge. According to the Bureau of Labor Statistics, approximately 22% of employed Americans continue to work from home at least part time, which is sustaining the need for reliable personal printing equipment. The educational sector remains a significant consumer of printing technology, with schools and universities requiring robust systems for administrative and instructional materials. According to the National Center for Education Statistics, there are approximately 128600 K 12 schools in the U.S. that rely on printed materials for standardized testing and classroom activities. Furthermore, the healthcare industry utilizes specialized printers for patient records, labels, and diagnostic images. As per the American Hospital Association, there are 6120 hospitals that employ high volume printing systems for operational efficiency. The integration of Internet of Things capabilities allows for predictive maintenance and automated supply replenishment, enhancing user experience. This technological evolution ensures that printers remain relevant despite the broader trend toward digitization, serving as critical nodes in hybrid work and operational environments.

MARKET DRIVERS

Persistent Demand for Physical Documentation in Legal and Healthcare Sectors

The enduring necessity for physical documentation in regulated industries, such as legal services and healthcare is one of the major factors driving the growth of the U.S. printer market. Despite digital transformation initiatives, many legal and medical processes require hard copies for compliance, archival, and client interaction purposes. According to the American Bar Association, approximately 62% of law firms still maintain physical case files and require high quality printing for court submissions and client contracts. This reliance ensures a steady demand for reliable laser and multifunction printers, capable of handling large volumes with precision. In the healthcare sector, patient safety and record keeping often depend on printed labels, wristbands, and prescription documents. According to the Office of the National Coordinator for Health Information Technology, while electronic health records are widespread, 30% of healthcare interactions still involve printed materials for patient education and consent forms. The strict regulatory requirements for data retention and authenticity make physical copies indispensable in these fields. Furthermore, the aging population increases the volume of medical records and prescriptions generated. As per the Centers for Medicare and Medicaid Services, the number of beneficiaries aged 65 and older is projected to reach 80 million by 2040, driving sustained printing needs. These sectors prioritize security and reliability over cost, leading to the adoption of enterprise grade printing solutions. The inability to fully digitize certain legal and medical procedures ensures that printers remain essential infrastructure in these critical industries.

Growth in E Commerce and Logistics Fuelling Label Printing Needs

The exponential growth of the e-commerce and logistics sectors in the U.S. significantly drives the demand for specialized label and barcode printers, which is further boosting the U.S. printer market expansion. As online shopping becomes the dominant retail channel, the volume of packages requiring shipping labels, tracking codes, and return instructions has surged. According to the U.S. Postal Service, parcel volume reached 7.1 billion pieces in the last fiscal year, reflecting the continuous expansion of online retail. Each package typically requires at least one printed label, creating a massive recurring demand for thermal transfer and direct thermal printers. Major retailers and third party logistics providers invest heavily in automated printing systems to streamline warehouse operations and reduce processing time. According to the Council of Supply Chain Management Professionals, 73% of logistics companies have upgraded their printing infrastructure to support higher throughput and accuracy. The rise of same day delivery services further intensifies the need for rapid and reliable label generation at distribution centers. Additionally, small businesses and home based sellers contribute to this demand by purchasing desktop label printers for order fulfillment. As per the Small Business Administration, there are 34 million small businesses in the U.S., many of which rely on e commerce platforms. The integration of printing solutions with inventory management software enhances operational efficiency. This structural shift in retail behavior ensures that label printing remains a robust and growing segment within the broader printer market.

MARKET RESTRAINTS

Accelerated Digital Transformation and Paperless Initiatives

The accelerated adoption of digital transformation and paperless initiatives across corporate and government sectors is a key restraint to the U.S. printer market growth. Organizations are increasingly migrating to cloud based document management systems, electronic signature platforms, and digital collaboration tools to reduce costs and improve sustainability. According to the International Data Corporation, 60% of enterprises have implemented paperless policies aimed at reducing printing volume by at least 30% over the next three years. This strategic shift diminishes the frequency of printer replacements and consumable purchases. Government agencies are also leading this transition, with the Office of Management and Budget mandating federal agencies to move towards electronic records management. According to the General Services Administration, federal printing expenditures decreased by 15% in the last two years due to digital alternatives. The convenience of mobile devices and tablets for reading and signing documents further reduces the need for physical copies. As per the Pew Research Center, 90% of Americans own smartphones, which serve as primary devices for information consumption. Educational institutions are similarly adopting digital textbooks and online assignments, limiting the use of printers in academic settings. The environmental consciousness among consumers and corporations drives the preference for digital over physical media. These trends collectively suppress the growth potential of the traditional printer market, as organizations optimize their workflows for digital efficiency and reduced physical footprint.

High Operational Costs and Environmental Concerns Regarding Consumables

High operational costs associated with printer consumables and growing environmental concerns regarding waste are further impeding the printer market expansion in the U.S. Consumers and businesses are increasingly sensitive to the total cost of ownership, which includes expensive ink and toner cartridges. According to Consumer Reports, the cost of ink can reach $50 per ounce, making it a substantial ongoing expense for users. This high cost prompts many individuals and small businesses to delay printer purchases or seek alternative printing services. Additionally, the disposal of plastic cartridges and electronic waste poses environmental challenges that deter eco conscious buyers. According to the Environmental Protection Agency, approximately 375 million empty toner and ink cartridges are thrown away each year, with the rest ending up in landfills. This waste generation contradicts corporate sustainability goals and consumer values. Many organizations are implementing strict procurement policies that favor vendors with comprehensive recycling programs or lower environmental impact. As per the Green Electronics Council, the demand for certified sustainable printing products has grown by 20% annually. The complexity of recycling processes and lack of awareness further hinder responsible disposal. Manufacturers face pressure to develop more sustainable materials and refillable systems, which can increase initial product costs. These financial and ecological factors create resistance to frequent printer upgrades and limit market expansion, particularly in price sensitive and environmentally aware segments.

MARKET OPPORTUNITIES

Integration of Cloud Computing and Mobile Printing Technologies

The integration of cloud computing and mobile printing technologies is a significant opportunity for the U.S. printer market by enhancing connectivity and user convenience. Modern printers equipped with Wi Fi Direct, cloud printing services, and mobile apps allow users to print from anywhere using smartphones, tablets, or laptops. According to the International Data Corporation, the adoption of cloud enabled printers in small and medium businesses has increased by 25% in the last year. This connectivity aligns with the hybrid work model, where employees need seamless access to office resources from remote locations. Manufacturers are developing intuitive interfaces and voice activated printing features to improve user experience. According to the Consumer Technology Association, 50% of new printer models now support voice assistants such as Alexa and Google Assistant. The ability to scan documents directly to cloud storage services like Dropbox and Google Drive adds value beyond simple printing. As per a study by Forrester Research, companies that adopt integrated cloud printing solutions report a 15% increase in workforce productivity. Furthermore, security features such as encrypted data transmission and user authentication address privacy concerns associated with wireless printing. The rise of Internet of Things platforms enables predictive maintenance and automatic supply ordering, reducing downtime. These technological advancements transform printers from standalone devices into intelligent nodes within smart office ecosystems. By focusing on connectivity and ease of use, manufacturers can attract tech savvy consumers and businesses seeking efficient and flexible document management solutions.

Expansion of 3D Printing in Manufacturing and Healthcare Applications

The expansion of 3D printing technology in manufacturing, healthcare, and education sectors offers a promising opportunity for the U.S. printer market. Unlike traditional 2D printing, 3D printing creates physical objects from digital models, enabling rapid prototyping, custom manufacturing, and complex medical device production. According to Wohlers Associates, the adoption of additive manufacturing in the U.S. has grown by 20% annually, with aerospace and automotive industries leading the charge. This technology allows for the creation of lightweight and durable components that are difficult to produce using conventional methods. In healthcare, 3D printers are used to create patient specific implants, prosthetics, and surgical guides, improving treatment outcomes. According to the Food and Drug Administration, over 100 medical devices produced via 3D printing have received regulatory approval in the past five years. Educational institutions are also integrating 3D printers into STEM curricula to foster innovation and hands on learning. As per the National Science Foundation, 40% of high schools in the U.S. now have access to 3D printing facilities. The decreasing cost of entry level 3D printers makes them accessible to small businesses and hobbyists. Material innovations, including biocompatible and recyclable filaments, expand the range of applications. By investing in 3D printing solutions, manufacturers can tap into high value industrial and medical markets. This diversification reduces reliance on the declining traditional 2D printing segment and positions companies at the forefront of advanced manufacturing trends.

MARKET CHALLENGES

Supply Chain Volatility and Semiconductor Shortages

Supply chain volatility and semiconductor shortages are challenging the expansion of the U.S. printer market, which is affecting production schedules and product availability. Printers increasingly rely on sophisticated chips for connectivity, processing, and control, making them vulnerable to global semiconductor disruptions. According to the Semiconductor Industry Association, global semiconductor sales reached $526.8 billion in 2023, with lead times for critical microcontrollers remaining a challenge for printer manufacturing. This scarcity forces companies to delay product launches and limit inventory levels, leading to lost sales opportunities. Additionally, logistical bottlenecks at ports and transportation networks exacerbate delays in receiving raw materials and finished goods. According to the Institute for Supply Management, 60% of manufacturing firms experienced significant supply chain disruptions in the past year. The reliance on overseas production for components, such as print heads and circuit boards, exposes manufacturers to geopolitical risks and trade policy changes. As per the U.S. International Trade Commission, tariffs on imported electronics have increased production costs by 10% for some manufacturers. These cost increases are often passed on to consumers, potentially dampening demand. Small and medium sized manufacturers are disproportionately affected, as they lack the bargaining power to secure priority supply allocations. Diversifying supply chains and nearshoring production are strategic responses, but require substantial investment and time. The unpredictability of global logistics complicates long term planning and inventory management. Ensuring consistent product availability while managing costs remains a critical operational challenge for industry leaders navigating this volatile environment.

Cybersecurity Threats and Data Privacy Risks

Cybersecurity threats and data privacy risks are further challenging the U.S. printer market growth. Modern multifunction printers store sensitive documents and connect to corporate networks, making them potential entry points for cyberattacks. According to the Cybersecurity and Infrastructure Security Agency, approximately 15% of reported network breaches involved printers in the last year. Vulnerabilities in firmware and outdated security protocols allow hackers to intercept data or use printers as bots in distributed denial of service attacks. Consumers and businesses are becoming more aware of these risks, leading to stricter procurement criteria for secure printing solutions. According to the Ponemon Institute, 45% of organizations have experienced a security incident related to internet of things devices, including printers. Compliance with data protection regulations, such as the California Consumer Privacy Act, requires manufacturers to implement robust encryption and authentication measures. As per the Federal Trade Commission, companies failing to protect user data face significant fines and reputational damage. The complexity of securing diverse printer models and legacy systems adds to the challenge. Manufacturers must invest continuously in security updates and vulnerability assessments to maintain trust. However, many users neglect to update firmware, leaving devices exposed. This gap between manufacturer efforts and user behavior creates ongoing security vulnerabilities. Addressing these risks requires a collaborative approach involving manufacturers, IT departments, and end users to ensure safe and reliable printing operations in an interconnected world.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.61% |

| Segments Covered | By Type, Technology, Output Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Brother Industries Ltd, Roland DG Corp, Ricoh Co Ltd, Xerox Holdings Corp, Toshiba Corporation, FUJIFILM Holdings Corp, Canon Inc, Panasonic Holdings Corp, and Seiko Epson Corp |

SEGMENTAL ANALYSIS

By Type Insights

The laser printer segment dominated the market by holding the highest share of the U.S. market in 2025 and is expected to maintain its status as the primary choice for professional and institutional printing through the next few years due to its superior speed, reliability, and cost efficiency for high volume printing tasks. This technology is preferred in corporate and educational environments, where consistent output quality and low cost per page are critical operational requirements. Laser printers utilize toner cartridges that have a significantly higher page yield compared to inkjet cartridges, resulting in a lower cost per page. According to the Bureau of Labor Statistics, administrative support occupations, which rely heavily on document processing, constitute 13% of the total US workforce, creating sustained demand for efficient printing solutions. According to the General Services Administration, federal agencies prioritize laser technology for internal communications due to its durability and speed. The ability to print thousands of pages without frequent cartridge replacements reduces downtime and maintenance costs. As per a study by Keypoint Intelligence, laser printers offer a 40% lower total cost of ownership over five years, compared to inkjet models for offices printing more than 1000 pages monthly. This economic advantage is crucial for budget conscious organizations. Furthermore, laser printers are less prone to clogging and drying out, ensuring reliability during intermittent use. The robustness of laser technology supports the rigorous demands of legal, financial, and healthcare sectors, where document integrity is paramount. These factors collectively cement the laser segment as the leading choice for professional and institutional printing needs in the U.S.

However, the inkjet printer segment is likely to experience steady growth over the coming years, as home based creative and small business applications continue to rise. While traditionally seen as slower, inkjet technology has evolved to meet diverse printing needs, including photo reproduction and specialized media handling. The unparalleled versatility of inkjet printers in handling various media types and delivering superior photo quality that appeals to residential users and creative professionals is further contributing to the expansion of this segment in the U.S. market. Unlike laser printers, inkjets can print on glossy paper, canvas, and fabric, making them ideal for photography, arts, and crafts. According to the Consumer Technology Association, consumer electronics spending in the U.S. reached $505 billion in 2023, with home photo printers seeing continued interest for physical memory preservation. The integration of wireless connectivity and mobile printing capabilities has further enhanced user convenience. According to the Pew Research Center, 90% of Americans own smartphones, facilitating seamless printing from mobile devices. Inkjet manufacturers have also introduced tank based systems that offer lower running costs, addressing previous concerns about expense. As per Canon Inc, the adoption of refillable ink tank printers has grown by 25% annually among small business owners who require color printing for marketing materials. The ability to produce vibrant colors and high resolution images makes inkjets indispensable for graphic designers and photographers. Additionally, the compact size of many inkjet models suits home offices with limited space. These attributes ensure that inkjet printers remain a preferred choice for users prioritizing quality and flexibility over sheer volume.

By Technology Insights

The server based printing technology segment led the market in 2025 and is expected to remain a fixture in institutional settings over the next few years, particularly within large enterprises and government institutions that require centralized control, security, and management of printing resources. This traditional architecture allows IT administrators to monitor usage, enforce policies, and maintain strict data governance. The dominance of server based printing technology is driven by the need for centralized management and robust security compliance in large organizations. Server based systems enable IT departments to control access, manage drivers, and monitor print jobs across extensive networks, ensuring operational efficiency and data protection. According to the National Institute of Standards and Technology, federal agencies and large corporations mandate centralized logging of all document outputs to comply with regulatory standards, such as the Health Insurance Portability and Accountability Act. According to the Department of Defense, over 90% of its printing infrastructure relies on server based architectures to maintain security protocols. This centralization facilitates the implementation of secure print release features, requiring user authentication at the device, which prevents sensitive documents from being left unattended. As per a report by Gartner, 70% of Fortune 500 companies prefer server based solutions for their ability to integrate with existing identity management systems. The reliability and predictability of server based environments reduce the risk of unauthorized access and data breaches. Furthermore, these systems support legacy applications and specialized hardware that may not be compatible with cloud platforms. The established infrastructure and deep integration with enterprise resource planning systems make migration difficult and costly. These factors ensure that server based technology remains the backbone of printing operations in security sensitive and large scale organizational environments.

On the other hand, the serverless or cloud printing segment is likely to achieve the highest CAGR of 19.2% during the forecast period in the U.S. market owing to the shift towards remote work, the demand for simplified IT infrastructure, the widespread adoption of remote work and the desire for simplified IT infrastructure that eliminates the need for on premise servers. Cloud printing allows users to print from any location using any device, without complex driver installations or network configurations. According to the Bureau of Labor Statistics, 22% of the US workforce continues to work remotely at least part of the time, creating a need for flexible printing solutions. According to Microsoft, the use of cloud based productivity tools has increased significantly among small and medium businesses, facilitating seamless integration with cloud printing services. This technology reduces the burden on IT staff by automating updates and maintenance tasks. As per IDC, 60% of new printer deployments in small businesses are now cloud enabled due to ease of setup and management. The scalability of cloud solutions allows organizations to adjust resources based on demand without significant capital investment. Furthermore, cloud printing supports mobility, enabling employees to print from smartphones and tablets, which is essential for modern workflows. The reduction in hardware costs associated with eliminating local servers makes this option financially attractive. These advantages drive the accelerated adoption of serverless cloud printing technologies across various sectors.

By Application Insights

The commercial segment held the largest share of the U.S. printer market in 2025 and is projected to lead the U.S. market in revenue for the foreseeable future, due to the extensive printing needs of businesses ranging from small enterprises to large corporations. This segment includes offices, retail stores, healthcare facilities, and professional service firms that rely on printers for daily operations. The dominance of the commercial segment is attributed to the operational necessity of printing in document intensive industries, such as legal, finance, and healthcare. These sectors generate substantial volumes of contracts, invoices, records, and reports that require reliable and high quality printing solutions. According to the American Bar Association, law firms alone account for a significant portion of commercial printing expenditure due to the requirement for physical case files and court submissions. According to the Healthcare Financial Management Association, hospitals and clinics print millions of patient records and billing statements annually, despite digital health initiatives. The need for immediate physical documentation in customer facing roles, such as retail receipts and shipping labels, further sustains demand. As per the U.S. Postal Service, over 7.1 billion packages are shipped annually, each requiring printed labels, driving commercial printer sales. Businesses prioritize durability and speed, leading to the adoption of enterprise grade laser and multifunction devices. The integration of printing with workflow automation software enhances efficiency, making it a critical component of commercial operations. The sheer scale of business activities in the U.S. ensures that the commercial segment remains the primary driver of printer market revenue.

However, the residential segment is on the rise and is likely to see consistent upward momentum over the next few years by showcasing a CAGR of 13.4% during the forecast period. The permanence of remote work and the increasing tendency of households to maintain home offices are propelling the expansion of the residential segment in the U.S. market. As more Americans work from home, the demand for personal printing solutions for documents, school assignments, and personal projects has stabilized at a higher level. According to the Census Bureau, approximately 20% of employed Americans worked from home in the last year, creating a sustained base of residential users. According to the National Center for Education Statistics, parents frequently print educational materials for children, contributing to household printer usage. The availability of affordable and compact inkjet models makes it easier for families to incorporate printers into their homes. As per the Consumer Electronics Association, residential printer sales have remained steady with a focus on multifunction devices that offer scanning and copying capabilities. The trend towards homeschooling and online learning further reinforces the need for home printing. Additionally, the rise of DIY projects and hobbies involving printed materials, such as photos and crafts, adds to residential demand. These lifestyle changes ensure that the residential segment continues to expand as printing becomes an integral part of the home environment.

COUNTRY LEVEL ANALYSIS

The U.S. had the leading share of 33.7% of the global market share in 2025 and is expected to remain the world's most influential printer market for the next several years. This leading position is supported by a robust economy, a large corporate sector, and high technological adoption rates. The U.S. maintains its dominant position in the printer market due to its advanced technological infrastructure and high density of corporate entities that require extensive document management solutions. The presence of numerous multinational corporations and small businesses creates a vast installed base of printers. According to the Small Business Administration, there are 34 million small businesses in the U.S., each contributing to the demand for office equipment. According to the Bureau of Economic Analysis, real business investment in equipment increased by 0.3% in the first quarter of 2024, supporting the replacement and upgrade cycles of printing hardware. The country's well developed logistics and retail networks ensure wide availability of printers and consumables. As per the U.S. International Trade Commission, the domestic production of high end printing equipment contributes significantly to the manufacturing sector. The emphasis on innovation and technology adoption drives the uptake of smart and cloud connected printers. Furthermore, the regulatory environment encourages compliance through documented records, sustaining the need for physical output in key industries. The combination of economic strength, industrial diversity, and technological readiness ensures that the U.S. remains the pivotal market for global printer manufacturers seeking growth and stability.

COMPETITIVE LANDSCAPE

The competition in the U.S. printer market is intense and characterized by established global brands competing on technology reliability and service quality. Major players leverage their extensive distribution networks and brand recognition to maintain dominance while niche manufacturers target specific segments with specialized solutions. Product differentiation is crucial as companies compete on features such as cloud connectivity security protocols and print speed. The shift towards subscription based supply models has created new competitive dynamics where customer retention becomes as important as hardware sales. Price competition remains fierce in the entry level segment prompting manufacturers to bundle value added services. Innovation in sustainable materials and energy efficiency serves as a key differentiator for environmentally aware consumers. The rise of remote work has intensified focus on mobile printing capabilities and easy setup processes. Mergers and acquisitions are common as firms seek to expand their software portfolios and intellectual property. Regulatory compliance regarding data security and environmental standards adds complexity to competitive strategies. Companies must continuously adapt to technological changes and consumer behavior shifts to retain market relevance. This dynamic environment drives constant innovation and strategic realignment among industry participants seeking sustainable growth.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. printer market are

- Brother Industries Ltd

- Roland DG Corp

- Ricoh Co Ltd

- Xerox Holdings Corp

- Toshiba Corporation

- FUJIFILM Holdings Corp

- Canon Inc

- Panasonic Holdings Corp

- Seiko Epson Corp

Top Players in the Market

- HP Inc remains a dominant force in the U.S. printer market by offering a comprehensive portfolio of inkjet and laser devices for home and enterprise users. The company focuses on integrating advanced security features and cloud connectivity into its hardware to meet modern workplace demands. Recent actions include expanding its Instant Ink subscription service which ensures consistent revenue and customer loyalty through automated supply delivery. HP has also invested heavily in sustainable manufacturing practices using recycled plastics in new models. These initiatives enhance brand reputation among environmentally conscious consumers. By leveraging artificial intelligence for predictive maintenance HP reduces downtime for business clients. The company continues to innovate with high speed multifunction printers that support hybrid work environments. Their strategic emphasis on software solutions and managed print services strengthens their ecosystem lock in. This holistic approach allows HP to maintain strong relationships with corporate clients while adapting to evolving digital workflow requirements in the competitive landscape.

- Canon U S A Inc contributes significantly to the U.S. printer market through its renowned imageRUNNER and PIXMA product lines catering to both commercial and residential segments. The company is known for superior optical technology and high quality color reproduction capabilities. Recent efforts involve strengthening partnerships with healthcare and education sectors by providing specialized printing solutions for medical imaging and academic materials. Canon has launched new energy efficient models that comply with strict environmental regulations. They have also enhanced their cloud printing platforms to facilitate seamless remote access for distributed workforces. The introduction of advanced security protocols protects sensitive data in corporate environments. Canon actively promotes recycling programs for toner cartridges reducing electronic waste. Their focus on innovation in large format printing supports architectural and engineering firms. By prioritizing customer service and technical support Canon builds long term trust. These strategies enable the company to differentiate itself through quality and reliability ensuring sustained relevance in a mature market.

- Brother International Corporation serves the U.S. printer market with robust and cost effective laser and inkjet solutions particularly favored by small and medium businesses. The company emphasizes durability and low total cost of ownership in its product design. Recent actions include expanding its line of mobile friendly printers that support wireless printing from smartphones and tablets. Brother has introduced high yield toner options to reduce frequent replacements for heavy users. They have also integrated stronger cybersecurity measures to protect networked devices from threats. The company focuses on simplifying setup and maintenance processes to enhance user experience. Brother actively engages in community outreach and educational programs promoting digital literacy. Their commitment to sustainability is evident in reduced packaging materials and energy saving modes. By targeting niche segments such as home offices and retail logistics Brother captures diverse demand. These targeted strategies help the company maintain a loyal customer base seeking reliable and affordable printing infrastructure.

Top Strategies Used by Key Market Participants

Key players in the U.S. printer market primarily employ product innovation and service diversification strategies to maintain competitiveness. Companies invest heavily in research and development to create smart connected devices with enhanced security features. This approach addresses growing concerns about data privacy in networked environments. Brands also focus on subscription based models for supplies ensuring recurring revenue streams and customer retention. By offering automated ink or toner delivery services they reduce consumer friction and enhance convenience. Strategic partnerships with cloud service providers enable seamless integration with digital workflows appealing to remote workers. Sustainability initiatives including eco friendly materials and recycling programs attract environmentally conscious buyers. Manufacturers also emphasize total cost of ownership benefits to appeal to budget sensitive businesses. Marketing efforts highlight ease of use and mobile connectivity to align with modern lifestyle trends. Continuous improvement in supply chain efficiency ensures product availability despite global disruptions. These multifaceted strategies allow companies to adapt to shifting consumer preferences and technological advancements while sustaining growth in a mature market sector.

MARKET SEGMENTATION

This research report on the U.S. printer market is segmented and sub-segmented into the following categories.

By Type

- Laser

- Inkjet

- LED Printer

- Others

By Technology

- Serverless/Cloud

- Server

By Output Type

- Monochrome

- Color

By Application

- Residential

- Commercial

- Educational Institutions

- Enterprises

- Government

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1.What is driving the growth of the U.S. printer market?

The growth of the U.S. printer market is driven by rising demand for home office printing, increasing adoption of wireless and multifunction printers, and technological advancements in printing solutions.

2.Which type of printers are most popular in the U.S. market?

Inkjet and laser printers are the most popular printer types in the U.S. due to their wide usage in homes, offices, educational institutions, and commercial sectors.

3.How are multifunction printers influencing the U.S. printer industry?

Multifunction printers are gaining traction because they combine printing, scanning, copying, and faxing features into a single device, improving efficiency and reducing operational costs.

4.What role does wireless connectivity play in the U.S. printer market?

Wireless connectivity enables users to print directly from smartphones, tablets, and cloud platforms, increasing convenience and supporting remote work environments.

5.Which sectors contribute significantly to printer demand in the United States?

Corporate offices, educational institutions, healthcare facilities, government organizations, and residential users are major contributors to printer demand in the U.S.

6.How is the shift toward remote work impacting the printer market?

The growing remote and hybrid work culture has increased demand for compact, affordable, and high performance home office printers across the United States.

7.What are the major challenges faced by the U.S. printer market?

High maintenance costs, rising digitalization, reduced paper usage, and cybersecurity concerns associated with connected printers are key challenges for the market.

8.Which printer technology is witnessing strong adoption in the U.S.?

Laser printing technology is witnessing strong adoption in commercial settings due to its faster printing speed, efficiency, and lower cost per page.

9.How are eco friendly trends affecting the U.S. printer market?

Manufacturers are increasingly developing energy efficient printers, recyclable cartridges, and sustainable printing solutions to meet environmental regulations and consumer preferences.

10.Who are the key participants in the U.S. printer market?

Major companies operating in the U.S. printer market include HP Inc., Canon Inc., Seiko Epson Corporation, Brother Industries, Ltd., and Xerox Holdings Corporation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com