U.S. Salty Snacks Market Size, Share, Trends, and Growth Analysis Report, Segmented by Product Type, Flavor, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

$81 BnMarket Estimate, 2026

$85.50 BnMarket Forecast, 2034

$131.71 BnCAGR, 2026–2034

5.55%U.S. Salty Snacks Market Report Summary

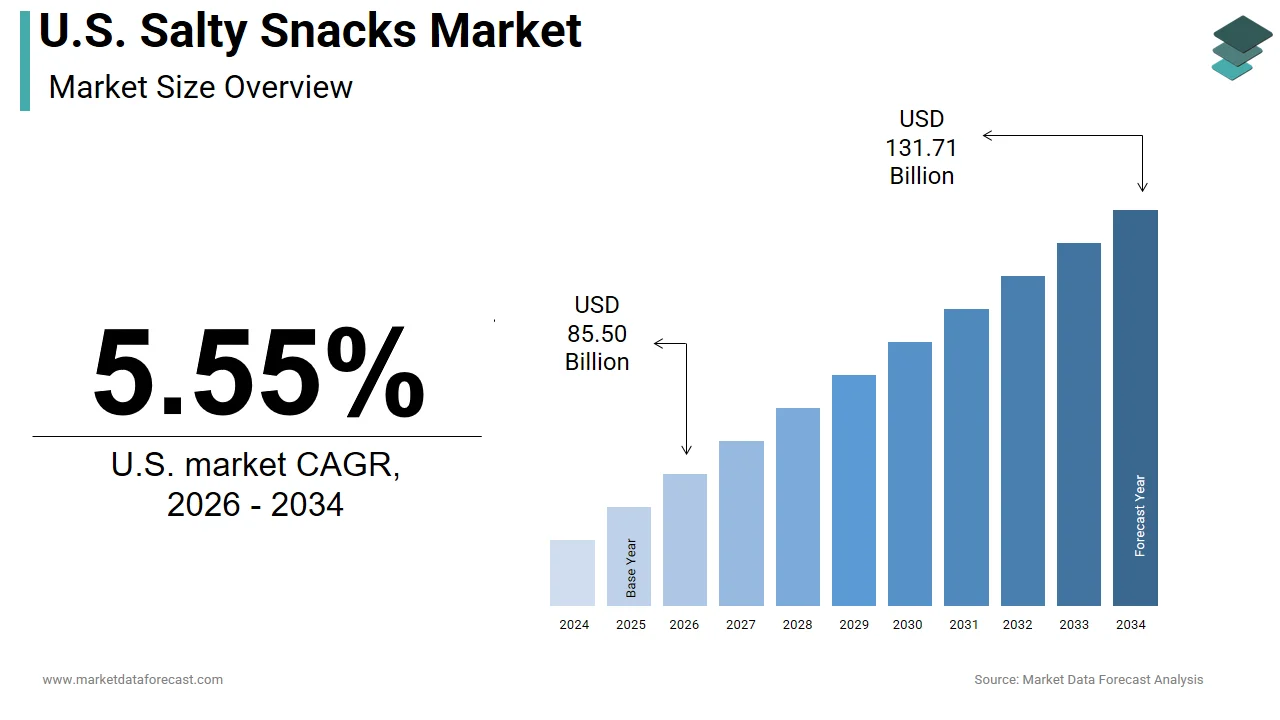

The U.S. salty snacks market was valued at USD 81 billion in 2025, is estimated to reach USD 85.50 billion in 2026, and is projected to reach USD 131.71 billion by 2034, growing at a CAGR of 5.55% from 2026 to 2034. Market growth is driven by increasing consumer demand for convenient ready-to-eat snack products, rising preference for flavored snack varieties, and expanding product innovation across healthier and premium snack categories. Salty snacks such as chips, popcorn, pretzels, nuts, and savory mixes continue to gain popularity due to evolving snacking habits, busy lifestyles, and strong retail availability. Growing demand for clean-label, protein-rich, and low-calorie snack options is further supporting market expansion across the United States.

Key Market Trends

- Rising consumer preference for flavored and premium salty snack varieties.

- Increasing demand for healthier, low-fat, and protein-rich snack options.

- Growing popularity of on-the-go and convenience snacking habits.

- Expansion of innovative seasoning blends and ethnic flavor profiles.

- Increasing focus on clean-label ingredients and sustainable packaging solutions.

Segmental Insights

- Based on product type, the chips segment dominated the U.S. salty snacks market in 2025 by accounting for 46.5% market share, driven by strong consumer preference, extensive product variety, and continuous flavor innovation.

- Based on flavor, the flavored salty snacks segment held a substantial share in 2025, supported by increasing demand for bold, spicy, and globally inspired flavor combinations among consumers.

- Based on distribution channel, the supermarkets and hypermarkets segment led the market by capturing 54.5% share in 2025, driven by broad product availability, strong promotional activities, and convenient consumer access.

Regional Insights

- The United States maintained dominance in the North American salty snacks market in 2025 by accounting for 82.1% share, driven by strong consumer spending on packaged snacks, extensive retail distribution networks, and continuous innovation in snack product development. Rising demand for healthier snacking alternatives and premium snack offerings continues to support long-term market growth across the country.

Competitive Landscape

The U.S. salty snacks market is characterized by intense competition among multinational food manufacturers and snack brands focusing on flavor innovation, healthier formulations, and product diversification. Market participants are emphasizing expansion of baked and organic snack portfolios, development of clean-label products, and strategic retail partnerships to strengthen market positioning. Acquisitions, new product launches, and investments in sustainable packaging and ingredient sourcing are shaping competitive dynamics across the market.

Prominent companies operating in the U.S. salty snacks market include PepsiCo Inc., The Kellogg Company, General Mills Inc., Mondelez International, The Kraft Heinz Company, Conagra Brands Inc., Calbee Inc., Frito-Lay, Intersnack Group GmbH & Co. KG, Blue Diamond Growers, Hain Celestial Group, Campbell Soup Company, UTZ Brands Inc., Snyder's-Lance Inc., Amplify Snack Brands, and Kettle Foods Inc.

U.S. Salty Snacks Market Size

The U.S. salty snacks market was valued at USD 81 billion in 2025, is estimated to reach USD 85.50 billion in 2026, and is projected to reach USD 131.71 billion by 2034, growing at a CAGR of 5.55% from 2026 to 2034.

Salty snacks are a broad spectrum of savory, ready-to-eat food products, including potato chips, tortilla chips, pretzels, popcorn, and extruded snacks, that serve as integral components of American dietary habits. These products are characterized by their high sodium content, crunchy texture, and convenience, making them popular choices for casual consumption, social gatherings, and on-the-go eating. The market is deeply embedded in the cultural fabric of the United States, where snacking has evolved from an occasional treat to a regular meal replacement or supplement. According to the Bureau of Labor Statistics Consumer Expenditure Survey, the average American household actually dedicates between 16% and 23% of its total grocery budget to the combined categories of non-alcoholic beverages and snacks/miscellaneous foods, highlighting a massive economic footprint. The proliferation of single-serve packaging and vending machine accessibility has further normalized impulse purchases. Consumer preferences are shifting toward bold flavors and ethnic inspirations, reflecting the diverse culinary landscape of the country. Additionally, the rise of health consciousness has prompted manufacturers to innovate with baked alternatives and reduced-fat formulations. The market is highly competitive with established giants and niche artisanal brands vying for shelf space. Regulatory scrutiny regarding labeling and nutritional content continues to shape product development strategies. This dynamic environment requires constant adaptation to changing consumer tastes and health trends, ensuring the market remains vibrant and responsive to societal shifts.

MARKET DRIVERS

Increasing Demand for Convenience and On-the-Go Consumption

The escalating demand for convenience and on-the-go consumption is a primary driver for the US salty snacks market. This is because modern lifestyles prioritize speed and efficiency in meal choices. Busy schedules among working professionals, students, and families have reduced the time available for traditional sit-down meals, leading to a reliance on portable and easy-to-eat options. According to the International Food Information Council, 70% of Americans snack at least once a day. While hunger or treating oneself are the top motivators, the easy availability and convenience of snack foods remain critical factors in this daily habit. The expansion of the gig economy and remote work has further blurred the lines between meal times, encouraging continuous grazing throughout the day. Retailers respond by placing salty snacks in high-traffic areas such as checkout counters and gas stations to capture impulse buys. Single-serve packs and resealable bags cater to portion control and freshness needs, enhancing appeal for commuters and travelers. The versatility of salty snacks allows them to be consumed in various settings, from offices to vehicles, making them indispensable for busy individuals. Manufacturers innovate with durable packaging that withstands movement and temperature changes, ensuring product integrity. This alignment with the fast-paced nature of contemporary life ensures sustained growth in the salty snacks segment as consumers seek effortless satisfaction without compromising on taste or enjoyment.

Innovation in Bold and Ethnic Flavor Profiles

The continuous innovation in bold and ethnic flavor profiles greatly fuels the growth of the US salty snacks market. Consumers are increasingly seeking adventurous and diverse taste experiences. The multicultural demographic of the United States has influenced mainstream palates, leading to a surge in demand for snacks inspired by global cuisines such as Mexican, Asian, and Mediterranean traditions. As per the Specialty Food Association, sales of ethnic inspired snacks grew by 8 percent annually as shoppers look for authentic and intense flavors that elevate the snacking experience. Flavors like sriracha, kimchi, harissa, and Tajin have gained popularity, appealing to younger demographics who view food as a form of exploration and self-expression. Social media platforms amplify this trend by showcasing unique snack combinations and challenging taste tests, which drive viral interest and trial. Manufacturers collaborate with celebrity chefs and culinary experts to create limited-edition flavors that generate buzz and urgency. The ability to offer novel taste sensations differentiates brands in a saturated market and commands premium pricing. Retailers dedicate shelf space to international aisles featuring these innovative products, catering to diverse community preferences. This focus on flavor diversity transforms salty snacks from simple commodities into exciting culinary discoveries. Consequently, the emphasis on bold and ethnic profiles sustains market expansion and encourages frequent repurchase among adventurous eaters.

MARKET RESTRAINTS

Health Concerns Related to High Sodium and Fat Content

Health concerns related to high sodium and fat content are a major restraint on the US salty snacks market. Consumers are becoming more aware of the negative impacts of excessive intake on cardiovascular health and weight management. Traditional salty snacks are often perceived as unhealthy due to their high levels of saturated fats and salt, which contribute to hypertension and obesity. According to the Centers for Disease Control and Prevention, nearly half of all adults in the United States have hypertension or high blood pressure, prompting many to limit sodium intake to less than 2300 milligrams per day. Per the American Heart Association, excessive intake of sodium and saturated fats from processed snacks significantly increases the risk of heart disease and stroke. However, despite these health warnings, overall consumer purchasing volumes for the category continue to grow steadily. Despite reformulation efforts, some mainstream brands struggle to lower sodium and fat levels without compromising taste and texture, which are critical for consumer satisfaction. Nutritionists and healthcare providers advise patients to choose whole food alternatives, such as nuts and fruits, over processed salty snacks. This perception limits the appeal of traditional chips and pretzels among fitness enthusiasts and those managing chronic conditions. Regulatory initiatives such as front-of-package labeling warnings further discourage consumption of high-sodium products. The need to balance flavor profile with nutritional integrity creates a formulation dilemma for producers. Thus, health concerns regarding sodium and fat content restrict the growth potential of conventional salty snacks and drive demand for healthier alternatives.

Rising Ingredient and Production Costs

Rising ingredient and production costs are also a serious hindrance to the US salty snacks market. This squeezes profit margins and forces price increases that may dampen consumer demand. Key raw materials such as potatoes, corn, and vegetable oils are subject to volatility due to weather conditions, supply chain disruptions, and geopolitical tensions. According to the United States Department of Agriculture, extreme weather events, including droughts and floods, have reduced crop yields, leading to higher prices for agricultural commodities. According to the Bureau of Labor Statistics, the Producer Price Index for food manufacturing rose by roughly 4% to 4.5% over the past year, highlighting a continuing, albeit more moderate, upward pressure on overall business production expenses. Energy costs associated with frying, baking, and packaging also contribute to higher operational expenditures for manufacturers. These increased costs are often passed on to consumers in the form of higher retail prices, which can lead to trade-downs to private label brands or reduced purchase volumes. Small and medium-sized brands face greater challenges in absorbing these costs compared to large corporations with diversified supply chains. The reliance on imported ingredients such as spices and specialty oils exposes manufacturers to currency fluctuations and trade tariffs. Geopolitical conflicts and logistical bottlenecks can disrupt the flow of essential components, leading to production delays. Manufacturers must invest in hedging strategies and long-term contracts to mitigate risks, but these measures require significant financial resources. Consequently, cost inflation remains a critical hurdle that constrains market growth and operational efficiency in the salty snacks industry.

MARKET OPPORTUNITIES

Expansion into Plant-Based and Vegan Snack Options

The expansion into plant-based and vegan snack options offers a substantial opportunity for the US salty snacks market. This growth is driven by a rising number of individuals adopting plant-based diets. Consumers are seeking dairy-free and meat-free alternatives that align with their ethical and environmental values, driving innovation in vegetable-based chips and legume snacks. According to the Plant Based Foods Association, U.S. retail sales of plant-based foods experienced a slight contraction in 2023 due to elevated inflation, though long-term data show the total market value has expanded by nearly 80% over the last five years. Manufacturers leverage ingredients such as chickpeas, lentils, kale, and sweet potatoes to create nutritious and flavorful alternatives to traditional potato chips. The inclusion of protein-rich legumes appeals to health-conscious buyers looking for satiety and nutritional benefits. Retailers dedicate shelf space to plant-based options, recognizing their growth potential and high margin possibilities. Marketing campaigns emphasize sustainability and ethical sourcing, resonating with environmentally conscious consumers who associate plant-based diets with lower carbon footprints. Collaborations with popular vegan influencers help promote new products and build brand loyalty. The versatility of plant-based ingredients allows for diverse flavor profiles and textures, expanding their application beyond traditional formats. This trend aligns with broader wellness movements, offering a pathway for market differentiation and revenue growth. American dietary preferences are constantly evolving. By catering to these changes, manufacturers can capture a significant share of the expanding plant-based sector.

Development of Functional Snacks with Added Benefits

The development of functional snacks with added health benefits provides a promising prospect for the US salty snacks market. This appeals to consumers who seek nutrition alongside indulgence. Functional snacks are fortified with vitamins, minerals, probiotics, or adaptogens to provide specific health advantages such as improved digestion, immunity, or stress relief. According to the Global Wellness Institute, the functional food market is projected to grow significantly as consumers prioritize preventive health measures through their dietary choices. Per the International Food Information Council, nearly two-thirds of consumers look for foods and snacks that deliver specific functional benefits beyond basic nutrition, heavily driving the demand for high-protein and gut-health-fortified snacks. Manufacturers incorporate ingredients like turmeric for inflammation, fiber for digestive health, and ashwagandha for stress management into salty snack formulations. These innovations transform traditional snacks into wellness tools, attracting health-conscious individuals who want to optimize their daily intake. Retailers support this trend by featuring functional snacks in health and wellness sections, highlighting their unique benefits. Partnerships with nutritionists and healthcare professionals help validate claims and build credibility. The ability to offer targeted health solutions allows brands to command premium prices and build loyal followings. This diversification strategy reduces reliance on traditional indulgent snacks and opens new market segments. Consequently, the integration of functional benefits drives engagement and expands the appeal of salty snacks to a broader audience seeking holistic well-being.

MARKET CHALLENGES

Intense Competition from Private Label Brands

Intense competition from private-label brands is a major challenge to the US salty snacks market. This erodes market share and pressures margins for national brands. Retailers such as Walmart, Kroger, and Costco have developed high-quality store-brand snacks that offer comparable taste and ingredients at significantly lower prices. According to the Private Label Manufacturers Association, private label sales in the grocery sector have grown steadily, with consumers increasingly trusting store brands for staple items like chips and pretzels. National brands struggle to justify price premiums when private labels improve their packaging and formulation quality. The lack of differentiation in basic salty snacks makes it difficult for established brands to maintain loyalty based solely on heritage or recognition. Retailers prioritize their own brands on shelves, giving them prominent placement and promotional support, which limits visibility for national competitors. Small and artisanal brands face even greater challenges in competing with the economies of scale enjoyed by large retailers. The perception that private labels offer better value forces national brands to invest heavily in marketing and innovation to retain customers. Price wars can lead to reduced profitability across the sector, impacting investment in research and development. Thus, the rise of powerful private label alternatives threatens the dominance of traditional salty snack manufacturers and necessitates strategic adaptation to maintain relevance.

Regulatory Pressure on Labeling and Marketing Practices

Regulatory pressure on labeling and marketing practices is a significant barrier to the US salty snacks market. This is propelled by governments and consumer advocacy groups demanding greater transparency and accountability. Agencies such as the Food and Drug Administration are scrutinizing claims related to natural ingredients, low-sodium content, and health benefits to prevent misleading information. According to the Federal Trade Commission, companies face increasing legal risks if their marketing materials exaggerate nutritional values or imply unproven health outcomes. As per the Center for Science in the Public Interest, there is growing calls for stricter regulations on front-of-package labeling to clearly indicate high levels of sodium, sugar, and saturated fats. Compliance with these evolving standards requires manufacturers to invest in rigorous testing and reformulation, which can be costly and time-consuming. Failure to adhere to guidelines can result in fines, product recalls, and damage to brand reputation. Consumers are becoming more skeptical of marketing claims, relying on third-party certifications and independent reviews to verify product quality. The complexity of navigating different state and federal regulations adds to the operational burden for national brands. Additionally, restrictions on advertising to children limit promotional opportunities for certain snack categories. Balancing creative marketing with regulatory compliance requires careful planning and legal oversight. Hence, regulatory pressures compel manufacturers to adopt more transparency.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Flavor, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Product Type Insights

The chips segment led the US salty snacks market and captured a 46.5% share in 2025. This leading position of the segment was attributed to its universal appeal, affordability, and deep integration into American snacking culture. In addition, this category includes potato chips, tortilla chips, and vegetable chips, which are consumed across all demographics and occasions. As per the United States Department of Agriculture, Americans consume over 1.5 billion pounds of potato chips annually, highlighting the massive scale of demand. The versatility of chips allows them to be paired with dips served at social gatherings or eaten as standalone treats, making them a staple in households and food service establishments. Manufacturers benefit from established supply chains for potatoes and corn, ensuring consistent raw material availability and cost efficiency. The wide variety of flavors, textures, and formats, from thin and crispy to thick and kettle cooked, caters to diverse consumer preferences. Retailers allocate significant shelf space to chips due to their high turnover rates and impulse purchase potential. Innovation within this segment focuses on healthier alternatives, such as baked chips and those made from alternative vegetables like kale and beetroot, to address health concerns. The cultural significance of chips during sporting events and holidays further sustains their dominance. Therefore, chips remain the cornerstone of the salty snack industry due to their widespread acceptance and essential role in casual dining.

On the other hand, the nuts and seeds segment is expected to exhibit a noteworthy CAGR of 7.2% from 2026 to 2034 due to the increasing consumer focus on health and nutrition. Unlike traditional fried snacks, nuts and seeds are perceived as nutrient-dense options rich in protein, healthy fats, fiber, and essential vitamins. According to data from the USDA Economic Research Service, per capita consumption of tree nuts in the United States has surged by nearly 50% over the last fifteen years, as health-conscious shoppers increasingly seek out plant-based satiety and functional dietary benefits. As per the Harvard T H Chan School of Public Health, regular consumption of nuts is associated with reduced risk of cardiovascular disease and type 2 diabetes, encouraging health-conscious individuals to incorporate them into their diets. The rise of plant-based and keto diets has further amplified demand for nuts and seeds as primary sources of energy and protein. Manufacturers innovate with roasted salted and flavored varieties to enhance taste while maintaining nutritional integrity. Single-serve packaging appeals to busy consumers looking for convenient and portable healthy snacks. The premium positioning of nuts and seeds allows for higher profit margins, attracting investment from major snack companies. Retailers expand their natural and organic sections to accommodate diverse nut and seed offerings, including almonds, walnuts, pumpkin seeds, and sunflower seeds. So, the combination of health benefits, dietary trends, and product innovation drives the rapid expansion of the nuts and seeds segment.

By Flavor Insights

The flavored salty snacks segment dominated the US market and accounted for a substantial share in 2025. Factors such as consumer desire for diverse and exciting taste experiences that go beyond basic saltiness are driving the dominance of this segment. This segment includes a wide array of profiles, such as barbecue, sour cream, and onion cheese, and spicy variations, which cater to adventurous palates. According to the International Food Information Council, while flavor remains the absolute top driver for 85% of food purchases, specific retail trends show that approximately 40% of snackers actively prioritize novelty and bold, unconventional flavor profiles to satisfy sensory curiosity. The influence of global cuisines has introduced popular flavors like sriracha, kimchi, and Tajin, appealing to younger demographics who view food as a form of exploration. Social media platforms amplify trends by showcasing unique flavor combinations and challenges driving viral interest and trial. Manufacturers collaborate with celebrity chefs and brands to create limited-edition flavors that generate buzz and urgency. Retailers dedicate shelf space to international and specialty aisles featuring these innovative products, catering to diverse community preferences. The ability to offer novel taste sensations differentiates brands in a saturated market and commands premium pricing. Flavored snacks also encourage repeat purchases as consumers seek to explore the full range of offerings. Thus, the emphasis on flavor diversity sustains market leadership and encourages frequent repurchase among adventurous eaters.

However, the plain salty snacks segment is predicted to witness the highest CAGR of 5.9% during the forecast period, owing to the rising demand for clean-label and minimally processed products. Consumers increasingly seek snacks with simple ingredient lists free from artificial flavors, colors, and preservatives, aligning with health and wellness trends. Market retail data demonstrates that sales of clean-label, low-sodium, and unsalted snack alternatives grew by roughly 7%, aligning with Organic Trade Association insights that show consumers are increasingly prioritizing transparency, minimal processing, and organic ingredients in their snack choices. National survey data from organizations like the Consumer Reports National Research Center reveal that approximately half of all U.S. consumers intentionally avoid artificial colors, flavors, and preservatives, prioritizing a 'clean label' consisting of authentic base ingredients. The perception that plain snacks are healthier due to lower sodium and additive content appeals to fitness enthusiasts and parents managing children's diets. Manufacturers respond by highlighting sourcing quality and preparation methods, such as air popping or baking, to enhance natural flavors without extra seasoning. The versatility of plain snacks allows them to be paired with homemade dips or used in cooking recipes, increasing their utility. Retailers expand their organic and natural sections to accommodate these straightforward options, catering to discerning buyers. The shift toward mindful eating and ingredient awareness drives the adoption of plain variants. Consequently, the combination of health consciousness and clean label preferences accelerates the growth of the plain salty snack segment.

By Distribution Channel Insights

The supermarkets and hypermarkets segment held the majority share 54.5% of the US salty snacks market in 2025. This supremacy of the segment was credited to its extensive reach, comprehensive product assortments, and one-stop shopping convenience. These retail outlets allow consumers to purchase snacks alongside other grocery items, facilitating routine household provisioning. The tactile experience of examining packaging and reading labels builds consumer confidence and trust in product quality. Established relationships between manufacturers and retailers ensure consistent stock levels and widespread geographic coverage. Loyalty programs and weekly flyers drive traffic and encourage bulk purchases of snack bags. The presence of dedicated aisle space for snacks allows for diverse product assortments ranging from budget-friendly to premium options. Older demographics who prefer traditional shopping methods rely heavily on supermarkets for their regular needs. Retailers also offer private label options that compete directly with national brands, enhancing choice. So, supermarkets remain the dominant channel due to their convenience, accessibility, and ability to drive volume sales through physical engagement.

But the online retail segment is estimated to register the fastest CAGR of 10.8% between 2026 and 2034. This growth is propelled by the convenience of home delivery and access to niche and specialty products. E-commerce platforms allow consumers to browse extensive catalogs, compare prices, and read reviews before purchasing, which enhances decision-making. Subscription services offered by online retailers ensure automatic replenishment of favorite snacks, enhancing customer retention and lifetime value. Direct-to-consumer brands leverage social media marketing to reach targeted audiences effectively, bypassing traditional retail markups. The pandemic accelerated the shift to online grocery shopping as consumers sought to minimize physical contact and prioritize safety. Logistics improvements have reduced shipping times and costs, making online purchases more attractive for bulk items. Personalized recommendations based on browsing history further enhance the shopping experience. Consequently, online retail continues to expand rapidly, capturing market share from traditional offline retailers by offering unparalleled convenience and selection.

REGIONAL ANALYSIS

U.S. Salty Snacks Market Analysis

The United States was the top performer in the North American salty snacks market and accounted for a 82.1% share in 2025. This expansion of the country’s market was driven by its large population, high consumption rates, and robust retail infrastructure. The market status is characterized by intense competition among established legacy brands and emerging artisanal producers who cater to diverse dietary preferences. According to United States Department of Agriculture data, the United States is the world's largest corn producer and the fifth-largest potato producer, with a dedicated portion of the potato crop (approximately 59 million cwt) processed annually for chips and shoestrings. The prevalence of snacking as a meal replacement or supplement ensures steady demand regardless of economic fluctuations. High disposable income allows consumers to experiment with premium and organic varieties, driving innovation in the sector. The widespread adoption of e-commerce platforms has expanded access to niche and specialty snacks from across the country. Regulatory frameworks regarding food safety and labeling ensure high standards of quality and transparency. Consumer trends toward health and wellness influence product development with increased demand for baked and low-sodium options. The mature retail landscape, including supermarkets, warehouse clubs, and convenience stores, ensures broad distribution and availability. Consequently, the United States remains the primary engine of growth and innovation in the continental salty snacks industry, setting trends that influence global markets.

COMPETITIVE LANDSCAPE

The competition in the US salty snacks market is intense and characterized by the presence of established multinational corporations and numerous private label brands vying for consumer attention. Market leaders differentiate themselves through brand heritage, product quality and innovative formulations that cater to specific dietary needs. The rise of private label offerings from major retailers poses significant pressure on national brands to maintain value propositions and justify premium pricing. Consumers are increasingly discerning and demanding transparency in ingredient sourcing and nutritional content, which raises the barrier for entry. Digital marketing and social media engagement have become critical tools for building brand loyalty and connecting with younger audiences. Price competition remains fierce, particularly in the standard chip segment, where cost sensitivity is high. Companies invest heavily in research and development to create unique flavor profiles and clean-label products. Regulatory compliance and adherence to food safety standards are essential for maintaining credibility. The market is fragmented with opportunities for niche artisanal brands to thrive alongside mass market giants. Strategic acquisitions and partnerships continue to reshape the landscape as companies seek to consolidate resources and expand their reach.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. salty snacks market include

- PepsiCo Inc.

- The Kellogg Company

- General Mills Inc.

- Mondelez International

- The Kraft Heinz Company

- Conagra Brands Inc.

- Calbee Inc.

- Frito-Lay

- Intersnack Group GmbH & Co. KG

- Blue Diamond Growers

- Hain Celestial Group

- Campbell Soup Company

- UTZ Brands Inc.

- Snyder's-Lance Inc.

- Amplify Snack Brands

- Kettle Foods Inc.

TOP PLAYERS IN THE MARKET

- Frito-Lay North America dominates the US salty snacks landscape with its iconic portfolio, including Lay's, Doritos, and Cheetos. The company leverages extensive distribution networks to ensure product availability across all retail channels. Recent actions include significant investments in sustainable packaging initiatives aiming to reduce plastic waste and enhance recyclability. Frito-Lay has also expanded its product line with baked and reduced-sodium options to address health-conscious consumer demands. The company utilizes advanced data analytics to optimize supply chain efficiency and minimize operational costs. By focusing on innovation in flavors and textures, Frito-Lay maintains strong brand loyalty. Strategic marketing campaigns featuring popular celebrities and digital engagement strategies help connect with younger demographics. These efforts solidify its position as a leader by balancing tradition with modern dietary preferences and environmental responsibility.

- The Kellogg Company, now operating as Kellanova holds a significant position in the US salty snacks market through brands like Pringles and Cheez-its. The company focuses on global expansion and product innovation to drive growth and maintain competitiveness. Recent actions include the spinoff of its North American cereal business to concentrate resources on snacking and international markets. Kellanova has introduced new Pringles flavors inspired by global cuisines to attract adventurous eaters. The company emphasizes sustainability by sourcing ingredients responsibly and reducing carbon emissions in manufacturing. Investments in digital marketing and e-commerce platforms enhance direct consumer engagement. By prioritizing agile operations and targeted brand strategies, Kellanova strengthens its market presence. These initiatives help the company adapt to changing consumer tastes while delivering consistent quality and value to shoppers across diverse retail environments.

- Mondelez International Inc contributes significantly to the US salty snacks market with popular brands such as Ritz Crackers and Triscuit. The company emphasizes premiumization and health-focused innovations to meet evolving consumer preferences. Recent actions include the acquisition of complementary snack brands to diversify its portfolio and expand market reach. Mondelez has launched organic and whole-grain variations of its core products to appeal to health-conscious shoppers. The company invests in sustainable cocoa and wheat sourcing programs to support ethical supply chains. Digital transformation initiatives improve customer insights and personalized marketing efforts. By focusing on mindful snacking trends, Mondelez positions its products as enjoyable yet responsible choices. Strategic partnerships with retailers ensure prominent shelf placement and promotional visibility. These actions reinforce its competitive stance by aligning with modern wellness values and maintaining high product standards.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the US salty snacks market employ several strategic initiatives to maintain competitiveness and drive growth. Product innovation is a primary strategy with companies developing healthier formulations, such as baked low-sodium and organic options to meet evolving consumer preferences. Investment in sustainable sourcing and eco-friendly packaging helps brands appeal to environmentally conscious shoppers and differentiate themselves. Strategic marketing campaigns leveraging digital platforms and influencer partnerships enhance brand visibility and engage younger demographics. Expansion into premium and artisanal segments allows companies to capture higher margins and attract gourmet enthusiasts. Optimization of supply chain operations ensures cost efficiency and consistent product availability across retail channels. Private label competition drives national brands to emphasize quality and heritage to justify price premiums. These multifaceted approaches help key participants adapt to changing dietary trends and economic conditions while sustaining business success.

MARKET SEGMENTATION

This research report on the U.S. salty snacks market has been segmented and sub-segmented into the following categories.

By Product Type

-

- Chips

- Popcorn

- Pretzels

- Nuts & Seeds

- Others

By Flavor

-

- Plain

- Flavored

By Distribution Channel

-

- Supermarkets / Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Others

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. salty snacks market?

The U.S. salty snacks market includes potato chips, corn chips, pretzels, popcorn, meat snacks, cheese snacks, and other savory snack foods consumed across the United States for taste and comfort.

Why is the U.S. salty snacks market growing?

The U.S. salty snacks market is growing due to snacking culture, stress relief consumption, flavor innovation, convenience, and consumers seeking comfort foods despite economic pressures.

Who buys products from the U.S. salty snacks market?

Millennials, Gen Z, parents, remote workers, and consumers seeking comfort, stress relief, and boredom relief drive purchases in the U.S. salty snacks market across all age groups.

What types of snacks are in the U.S. salty snacks market?

The U.S. salty snacks market includes potato chips, corn chips, pretzels, popcorn, meat jerky, cheese snacks, veggie chips, pork rinds, snack mixes, and puffed or multi-grain snacks.

How does flavor impact the U.S. salty snacks market?

Flavor is crucial to the U.S. salty snacks market, with new flavors, spicy options, and limited-edition seasonal varieties driving consumer interest and purchase decisions most strongly.

What challenges face the U.S. salty snacks market?

Challenges in the U.S. salty snacks market include inflation, price sensitivity, health concerns, sodium regulation, demand for healthier options, and competition from better-for-you snacks.

Which demographic consumes the most from the U.S. salty snacks market?

Millennials represent the largest demographic in the U.S. salty snacks market, followed by parents and work-from-home employees who consume salty snacks for comfort and stress relief.

How does health consciousness affect the U.S. salty snacks market?

Health consciousness shapes the U.S. salty snacks market through demand for reduced sodium, organic ingredients, high protein, no artificial additives, and minimally processed snack options.

What role does comfort food play in the U.S. salty snacks market?

Comfort food is central to the U.S. salty snacks market, as consumers choose salty snacks for relaxation, stress relief, craving satisfaction, and emotional comfort rather than hunger.

Is the U.S. salty snacks market competitive?

Yes, the U.S. salty snacks market is highly competitive with major brands, private label products, flavor innovation, value pricing, and diversification into healthier snack categories.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com