U.S. Structural Steel Market Size, Share, Trends & Growth Forecast Report By Product, By Application, and By Country (California, Texas, Florida, New York, Illinois & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

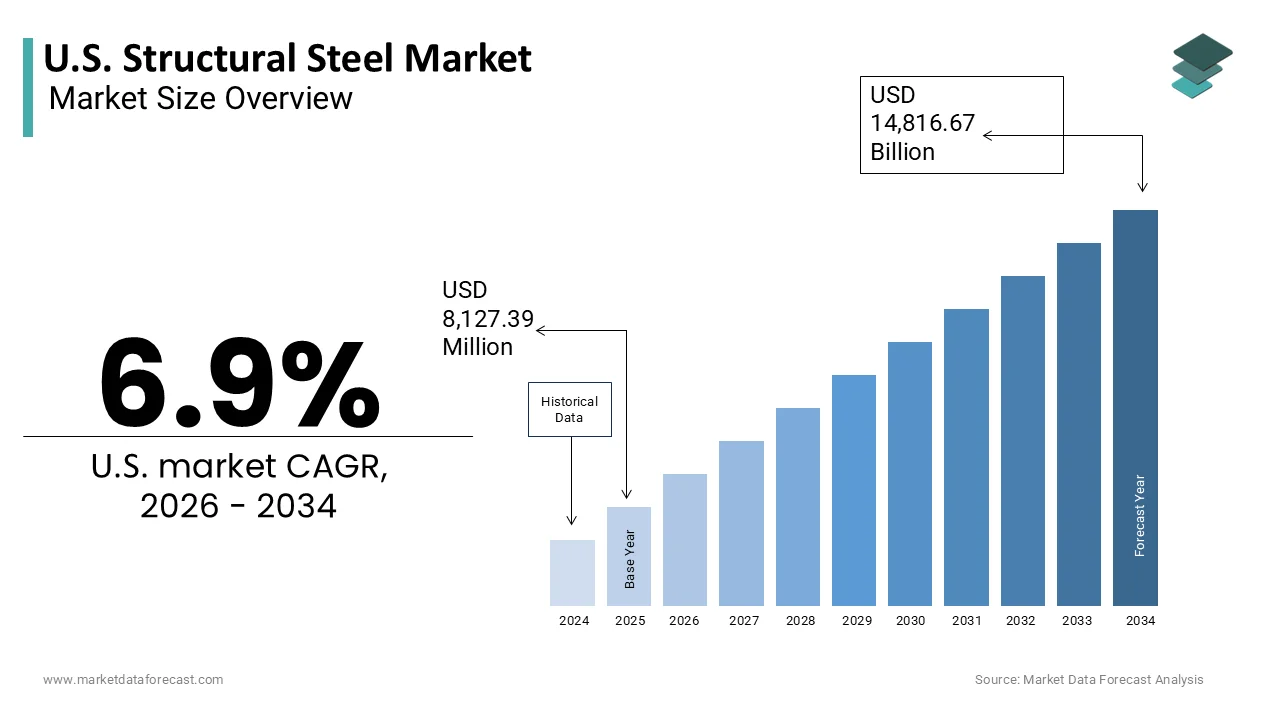

Market Size, 2025

$8.13 BnMarket Estimate, 2026

$8.69 BnMarket Forecast, 2034

$14.82 BnCAGR, 2026–2034

6.9%U.S. Structural Steel Market Size

The U.S. Structural Steel Market is projected to grow from USD 8,127.39 million in 2025 to USD 8,688.18 million in 2026 and reach USD 14,816.67 million by 2034, registering a CAGR of 6.9% during the forecast period from 2026 to 2034.

The structural steel is the fabrication and erection of steel beams, columns, and trusses used in commercial, industrial, and institutional construction. The intersection of raw material supply and requiresengineering services by requiring precise adherence to architectural specifications and safety codes. As per the American Institute of Steel Construction, the average cost of structural steel represents approximately 10% to 15% of total construction costs for large commercial projects, highlighting its significant financial impact on development budgets. Regulatory standards set by the American Society of Civil Engineers dictate rigorous performance criteria for seismic resistance and wind load management, particularly in coastal and high-risk zones. The integration of Building Information Modeling has transformed design processes, allowing for greater precision in component fabrication and reduced waste during assembly. Labor dynamics play a crucial role, with skilled welders and ironworkers forming the backbone of project execution.

MARKET DRIVERS

Resurgence in Industrial Construction Fuels Demand for Heavy Structural Sections

The rapid expansion of the industrial construction sector, driven by the reshoring of manufacturing and tm in e-commerce logistics, which is majorly propelling the growth of the United States structural steel market. Companilarge-scaleeasingly investing in large scale distribution centers and advanced manufacturing column-free spaces that require wide column free spaces, long spans best achieved through long span structural steel systems. The Inflation Reduction Act has further accelerated this trend by providing tax incentives for domestic semiconductor and battery production facilities, many of which are currently under construction in the Midwest and South. These mega projects demand thousands of tons of heavy wide flange beams and hollow structural sections to support heavy machinery and high ceiling requirements. The speed of erection associated with prefabricated steel components allows developers to meet tight schedules, a factor in the fast paced logistics industry. Furthermore, the durability of steel ensures low maintenance costs over the lifecycle of the long-term facility, appealing to long term investors.

High-Risertical Expansion Drives High Rise Steel Framework Adoption

The continued trend of urbanization and land scarcity in major metropolitan areas is driving the high-rise use of structural steel for high rise residential and mixed-use developments, which is additionally amplifying the growth of the United States. Structural steel offers superior strength-to-weight ratios compared to concrete by allowing for taller structures with smaller footprints and faster construction timelines. According to the Council on Tall Buildings and Urban Habitat, there were 45 skyscrapers completed in the United States in 2025, with steel or composite steel concrete structures accounting for nearly 60% of these projects. Cities like New York, Chicago, and Miami continue to see dense vertical growth as populations concentrate in urban cores by creating demand for luxury apartments and office towers that utilize steel frames for their flexibility and open floor plans. The modern designs favor cantilevered elements and irregular geometries that are easier to achieve with steel fabrication than with traditional cast-in-place concrete. The ability to erect steel structures in all weather conditions also reduces project delays, a significant advantage in regions with harsh winters or rainy seasons. Developers value the predictability of steel schedules, which helps in managing financing costs and leasing timelines. Additionally, the retrofitting of existing urban infrastructure often involves steel additions or reinforcements, further expanding the market scope.

MARKET RESTRAINTS

Volatility in Raw Material Prices Disrupts Project Budgeting

The fluctuations in the prices of steel scrap, iron ore, and energy inputs for structural steel fabricators and their clients are limiting the growth of the United States structural steel market. The cost of raw materials can swing dramatically due to global supply chain disruptions, trade policy changes, and shifts in international demand, making it difficult to lock in fixed price contracts for long-duration construction projects. The volatility erodes profit margins for fabricators, who may be locked into agreements before material costs spike, leading to disputes and potential project cancellations. As per industry surveys, nearly 40% of construction firms reported delaying bid submissions due to unpredictable material pricing, slowing down the overall pace of new project initiations. The reliance on imported semi-finished steel products also exposes the market to currency exchange risks and tariff implications, further complicating cost forecasting. Cllarge-scale hesitation to commit to large scale developments when the final cost of the structural frame is undecided, leading to a freeze in decision making. This financial instability discourages investment in speculative construction projects, particularly in the commercial office sector, where returns are already under pressure. Manufacturers struggle to pass on sudden cost increases without losing competitive bids, creating a squeeze on operational viability.

Acute Shortage of Skilled Labor Hinders Production Capacity

The persistent shortage of skilled welders, ironworkers, and detailers is additionally inhibiting the growth of the United States structural steel market. According to the Associated General Contractors of America, many construction firms reported difficulty in filling craft worker positions in 2025, with welding and metalworking being among the hardest roles to staff. This labor deficit leads to extended project timelines and increased labor costs as companies compete for a limited pool of qualified personnel. Training new workers requires significant time and resources, and the complexity of modern structural connections demands higher levels of technical proficiency than in the past. Delays in fabrication due to labor shortages can cascade into broader construction schedules, causing penalties and strained client relationships. The inability to scale up production quickly in response to a surge in demand limits revenue potential for fabricators. Furthermore, safety concerns arise when less experienced workers are pressed into service, potentially leading to accidents and regulatory scrutiny.

MARKET OPPORTUNITIES

Adoption of Modular Construction Techniques Opens New Avenues

The rising popularity of modular and prefabricated construction methods to expand its valusite-builtion beyond traditional site built projects is to expand the growth of the United States structural steel market. Modular construction involves assembling building sections off-site in controlled factory environments, a process that heavily relies on the precision and strength of steel frames. Steel is the ideal material for modular units due to its dimensional accuracy and ability to withstand transportation stresses without deformation. The modular steel buildings can be completed up to 30% faster than conventional structures by offering substantial savings on financing and labor costs, as per the research. This method also aligns with sustainability goals by reducing material waste and site emissions, appealing to environmentally conscious developers. Fabricators who invest in automated cutting and welding technologies can capitalize on this trend by producing high-volume standardized modules for multi-story residential and hotel projects. The ability to integrate mechanical, electrical, and plumbing systems into steel modules during fabrication further enhances efficiency. This shift towards industrialized construction allows steel suppliers to move up the value chain, offering integrated solutions rather than just raw materials.

Integration of Digital Twin Technology Enhances Design Efficiency

The integration of digital twin technology and advanced Building Information Modeling software to improve design accuracy and operational efficiency is another factor to promote the growth of the United States structural steel market. Digital twins create virtual replicas of physical steel structures, allowing engineers to simulate performance under various loads and environmental conditions before fabrication begins. This technology enables seamless collaboration between architects, engineers, and fabricators by ensuring that complex geometries are translated accurately into buildable cloud-based The firms utilizing cloud based BIM platforms reported an improvement in project delivery time, better coordination, and real-time data sharing. The ability to optimize steel usage through algorithmic design reduces material waste and lowers overall project costs, enhancing the competitiveness of steel against alternative materials. Digital twins also facilitate ongoing maintenance by providing owners with detailed data on structural health and load history, extending the lifecycle of the asset. This technological advancement positions structural steel as a smart, data-rich building material, attracting tech savvy developers and institutional investors.

MARKET CHALLENGES

Supply Chain Fragility Impacts Timely Material Availability

The fragility of global and domestic supply chains, which is affecting the timely availability of raw materials and finished components is likely to be a challenge for the growth of the United States structural steel market. Disruptions in logistics networks, port congestion, and rail capacity constraints can delay the delivery of steel beams and plates, causing costly setbacks for construction projects operating on tight schedules. According to the Logistics Management Institute, lead times for structural steel deliveries extended by an average of four weeks in 2025 compared to historical norms, due to bottlenecks in transportation and inventory management. This unpredictability forces contractors to hold larger inventories, tying up capital and increasing storage costs. As per industry feedback, just-in-time delivery models, which are critical for urban construction sites with limited storage space, have become increasingly difficult to maintain. Dependence on specific mills for specialized sections creates single points of failure, where any production issue at one facility can ripple through the entire supply network. Geopolitical tensions and trade policies further complicate sourcing strategies, limiting options for alternative suppliers. The lack of transparency in tier two supply chains makes it difficult to anticipate disruptions caused by raw material shortages or energy outages. These logistical challenges undermine the reliability of structural steel as a construction material, prompting some developers to consider alternative systems with more predictable supply lines. Mitigating these risks requires significant investment in supply chain diversification and digital tracking tools, adding to operational complexities.

Stringent Environmental Regulations Increase Compliance Costs

The implementation of stringent environmental regulations regarding carbon emissions and industrial pollution for structural steel manufacturers and fabricators is also expected to slow down the growth of the United States structural steel market. Governments at both federal and state levels are imposing stricter limits on greenhouse gas emissions from heavy industry, compelling companies to invest in cleaner technologies and sustainable practices. The new guidelines issued in 2025 require steel producers to reduce carbon intensity by 20% over the next decade, which is substantial capital expenditure on electric arc furnace upgrades and carbon capture systems, as per the report. These compliance costs are often passed down the supply chain, increasing the final price of structural steel and potentially reducing its competitiveness against lower carbon alternatives like mass timber. As per regulatory analysis, facilities that fail to meet emission standards face hefty fines and operational restrictions, creating financial risk for non-compliant entities. The push for green building certifications also demands detailed environmental product declarations, requiring manufacturers to track and report the carbon footprint of every beam produced. This administrative burden adds complexity to operations and requires specialized expertise in sustainability reporting. Smaller fabricators may struggle to afford the necessary upgrades, leading to market consolidation and reduced competition. The transition to low carbon steel production is technologically challenging and capital intensive, slowing down the pace of adaptation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Texas, Florida, New York, Illinois, the rest of the United States |

| Market Leaders Profiled | Nucor Corporation, Steel Dynamics, Inc., United States Steel Corporation, Commercial Metals Company (CMC), ArcelorMittal North America, Gerdau S.A., EVRAZ North America, SSAB Americas, Liberty Steel Group, Valmont Industries, Inc., Canam Group Inc., Vulcraft (Nucor Corporation) |

SEGMENTAL ANALYSIS

By Product Insights

High-sectional steel dominates the United States structural steel market due to its indispensable role in constructing large scale commercial and industrial infrastructure that requires superior load bearing capacity. This segment includes wide flange beams, heavy columns, and large channels that form the primary skeleton of skyscrapers, bridges, and manufacturing plants. The dominance is driven by the ongoing boom in data center construction and logistics warehouses, which demand long-span spaces supported by long span steel structures. According to the American Institute of Steel Construction, high sectional steel accounts for approximately 60% of total structural steel tonnage used in nonresidential projects, reflecting its critical importance in modern architecture. The material’s ability to support heavy vertical loads while minimizing column footprint allows for flexible interior layouts, a key requirement for office and retail spaces. The resurgence of bridge infrastructure projects, defined by federal high-strength requirements, boosts demand for high-strength steel, which provides the durability needed for transportation networks. Manufacturers benefit from economies of scale in producing standardized heavy sections, ensuring a consistent supply for mega projects.

The light sectional steel segment is projected to expand at a CAGR of 6.,5% throughout the forecast period with the increasing adoption in residential construction and light commercial applications. The shift towards sustainable and resilient housing solutions, as light gauge steel offers resistance to fire, pests, and moisture compared to traditional wood framing is also fuelling the growth of the segment. The precision of factory-produced steel components reduces on site waste and labor time, addressing the chronic shortage of skilled carpenters. The versatility of light sectional steel allows for complex architectural designs and easy integration with insulation and utility systems. Additionally, the recyclability of steel aligns with green building certifications, attracting environmentally conscious developers. The expansion of modular housing projects further accelerates demand, as light steel frames are ideal for off-site assembly.

By Application Insights

The non-residential application segment was the largest by holding a significant share of the United States' structural steel market share in 2025 due to the extensive use of steel in commercial, industrial, and institutional buildings. The robust investment in infrastructure, including airports, hospitals, schools, and corporate headquarters, which require the strength and flexibility of structural steel is also fuelling the growth of the segment. The trend towards larger industrial facilities for e-commerce and advanced manufacturing drives demand for heavy steel frameworks that can support automated equipment and high ceilings. The durability and fire resistance of steel make it the preferred choice for high-traffic institutions and long-term commercial venues by ensuring long term safety and lower insurance costs. Government initiatives to modernize public infrastructure further bolster this segment, with billions allocated for bridge repairs and transit hubs. The ability of steel to facilitate rapid construction schedules is crucial for commercial developers aiming to minimize financing costs and accelerate revenue generation.

The residential application segment is expected to witness a fastest CAGR of 5.8% from 2026 to 2034, with the increasing adoption of steel framing in single-family housing and custom single family homes. The need for durable and sustainable building materials that can withstand long-term weather events and reduce long term maintenance costs. The rising cost and volatility of lumber prices have made steel a more attractive alternative for builders looking to stabilize budgets. The use of light gauge steel in residential construction has expanded beyond coastal regions to inland markets, driven by greater awareness of its benefits. The precision of steel components allows for tighter building envelopes, improving energy efficiency and meeting stricter environmental codes. The growth of modular home manufacturing also contributes to this trend, as steel frames are ideal for prefabricated units that require high structural integrity during transport. Additionally, consumer preference for modern industrial aesthetics in home design has boosted the use of exposed steel elements.

COMPETITIVE LANDSCAPE

The competition in the United States structural steel market is characterized by a mix of large integrated producers and specialized regional fabricators vying for dominance in diverse construction segments. Intense rivalry exists due to the commoditized nature of standard structural shapes, prompting firms to differentiate through service quality, delivery speed, and technical support. Major players leverage economies of scale to offer competitive pricing while investing in advanced manufacturing technologies to improve product consistency and reduce lead times. The market features moderate barriers to entry due to high capital requirements for milling equipment and stringent quality certifications, which protect established incumbents from new competitors. Price volatility in raw materials adds complexity to competitive dynamics by forcing companies to adopt sophisticated hedging strategies to maintain margins. Customer loyalty plays a crucial role as builders prioritize reliability and consistent supply over minor price differences. Innovation in sustainable production methods provides avenues for differentiation beyond traditional metrics.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Structural Steel Market include

- Nucor Corporation

- Steel Dynamics, Inc.

- United States Steel Corporation

- Commercial Metals Company (CMC)

- ArcelorMittal North America

- Gerdau S.A.

- EVRAZ North America

- SSAB Americas

- Liberty Steel Group

- Valmont Industries, Inc.

- Canam Group Inc.

- Vulcraft (Nucor Corporation)

TOP LEADING PLAYERS IN THE MARKET

- Nucor Corporation stands as a leading force in the United States structural steel market by leveraging its extensive network of electric, high-quality facilities to produce high quality beams and columns. The company focuses on sustainable manufacturing practices, utilizing recycled scrap metal to reduce environmental impact while maintaining cost efficiency. Recent investments in advanced rolling mills have enhanced their ability to produce specialized large-scale sections required for large scale infrastructure projects. Nucor actively collaborates with fabricators to ensure the timely delivery of materials, which is strengthening supply chain reliability for critical construction timelines. The firm’s commitment to innovation includes adopting digital technologies for quality control and production optimization.

- Steel Dynamics Inc contributes significantly to the structural steel sector through its integrated approach to steel production and fabricatiostate-of-the-artcompany operates state of the art facilities that produce a diverse range of structural shapes tailored for bridge, building, and industrial applications. Recent expansions in its Texas and Alabama plants have increased capacity for heavy structural sections, allowing it to meet growing demand from infrastructure projects. Steel Dynamics emphasizes rapid turnaround times and precise engineering support, which appeals to contractors managing tight schedules. The firm also invests in rehigh-strength, low-alloy to create high-strength, low-alloy steels that offer superior performance in extreme conditions.

- Gerdau S.A. maintains a strong presence in the United States structural steel market byproviding a comprehensivee portfolio of long steel products, including beams, channels, and angles. The company leverages its global expertise and local manufacturing capabilities to serve diverse sectors such as energy, transportation, and commercial construction. Recent initiatives include upgrading its micro mill technology to enhance production flexibility and reduce carbon emissions by aligning with sustainability goals of modern developers. Gerdau focuses on building long-term relationships with distributors and fabricators to ensure seamless material flow to job sites. The firm also provides value-added technical assistance and value added services that help clients optimize steel usage and reduce waste.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States structural steel market primarily employ vertical integration strategies to control production costs and ensure consistent material availability for clients. Companies invest heavily in technological advancements such as automated rolling mills and digital quality control systems to enhance product precision and operational efficiency. Strategic expansion of high-growth facilities in high growth regions allows firms to reduce logistics costs and improve delivery speeds for local projects. Participants also focus on sustainability initiatives by adopting electric arc furnace technologies and recycling programs to meet environmental regulations and long-term building standards. Long term partnerships with major construction firms and fabricators help secure stable demand and mitigate market volatility risks. Additionally, manufacturers prioritize developing high-strength alloys and customized sections that address specific engineering challenges.

MARKET SEGMENTATION

This research report on the U.S. structural steel market is segmented and sub-segmented into the following categories.

By Product

- High Sectional Steel

- Light Sectional Steel

By Application

- Non-Residential

- Residential

By Country

- California

- Texas

- Florida

- New York

- Illinois

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com