U.S Subscription Video On Demand Market Size, Share, Trends & Growth Forecast Report Segmented By Content Type (Movies, TV Shows, Documentaries), Device Type, End Use, And Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis And Forecast, 2026 To 2034

U.S. Subscription Video On Demand Market Report Summary

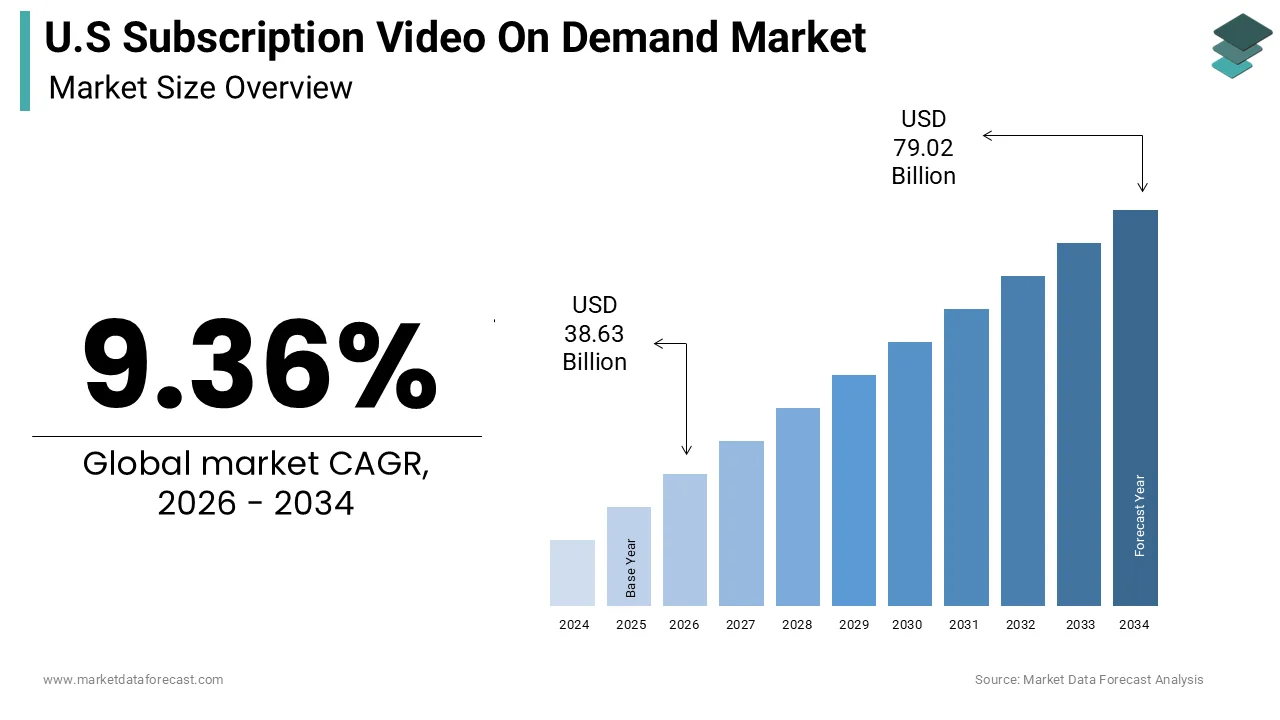

The United States subscription video on demand (SVOD) market was valued at USD 35.32 billion in 2025 and is projected to reach USD 79.02 billion by 2034, growing from USD 38.63 billion in 2026 at a CAGR of 9.36% during the forecast period. Market growth is driven by increasing internet penetration, rising adoption of smart devices, and growing consumer preference for on-demand digital entertainment. The expansion of original content, personalized streaming experiences, and bundled subscription services is further accelerating the growth of the U.S. SVOD market.

Key Market Trends

- Rising demand for original and exclusive streaming content

- Increasing adoption of smart TVs and connected devices

- Growth in ad-supported subscription models and bundled services

- Expansion of AI-driven content recommendations and personalization

- Increasing popularity of mobile streaming and multi-device viewing

Segmental Insights

- Based on content type, the TV shows segment dominated the U.S. subscription video on demand market in 2025 by accounting for 35.5% of the regional market share, driven by binge-watching culture and serialized content popularity.

- Based on device type, the smart TVs segment led the market in 2025 by capturing 44.1% of the total market share, supported by increasing smart home adoption and connected entertainment systems.

- Based on end use, the individual end-user segment held the largest share in 2025, driven by rising personal streaming subscriptions and digital entertainment consumption.n

Regional Insights

- United States accounted for 40.2% of the global subscription video on demand market share in 2025, making it the leading regional market due to strong streaming infrastructure and high consumer adoption.

Competitive Landscape

- The U.S. SVOD market is highly competitive, with companies focusing on original programming, user engagement, and global content expansion. Market players are investing heavily in exclusive content libraries, live streaming, and AI-powered personalization to strengthen subscriber retention.

- Prominent players in the U.S. subscription video on demand market include Netflix Inc, Amazon Prime Video, The Walt Disney Company, Warner Bros. Discovery, Paramount Global, Apple Inc, Comcast Corporation, Hulu LLC, Peacock TV, and YouTube Premium.

U.S Subscription Video On Demand Market Size

The U.S. subscription video on demand market size was calculated to be USD 35.32 billion in 2025 and is anticipated to be worth USD 79.02 billion by 2034, from USD 38.63 billion in 2026, growing at a CAGR of 9.36% during the forecast period.

Subscription Video On Demand (SVOD) is a streaming service model where users pay a recurring monthly or annual fee to gain unlimited, on-demand access to a library of video content. This model has fundamentally reshaped entertainment consumption by prioritizing viewer autonomy and on-demand accessibility over scheduled broadcasting. The sector is characterized by intense competition among legacy media conglomerates and technology giants who leverage proprietary content to drive subscriber acquisition and retention. As per a study, 83 percent of American adults report using streaming services, indicating deep market penetration and cultural integration. Furthermore, the Federal Communications Commission notes that broadband access remains high, with over 95 percent of households having access to fixed high-speed internet (100/20 Mbps), which is essential for high-definition streaming. The shift toward mobile viewing is also significant as smartphones and tablets become primary devices for content consumption outside the home. Regulatory discussions regarding net neutrality and data privacy continue to influence operational strategies for providers. The market is currently navigating a transition phase where growth is shifting from pure subscriber accumulation to profitability and average revenue per user optimization. This environment reflects a sophisticated consumer base that demands high-quality original programming, seamless user experience, and flexible pricing options in an increasingly saturated digital ecosystem.

MARKET DRIVERS

Proliferation of High Quality Original Content

The proliferation of high-quality original content is pushing the United States subscription video-on-demand market forward. This creates unique value propositions that distinguish platforms from competitors and justify subscription costs. Consumers are increasingly willing to pay for exclusive access to critically acclaimed series and films that are not available elsewhere. As per sources, while original programming remains a key engagement driver, acquired library content accounted for the largest share of total streaming minutes in 2024, with top titles like Bluey reaching over 55 billion viewing minutes. Platforms invest billions of dollars annually in production to secure talent and create flagship shows that generate cultural buzz and social media conversation. This strategy fosters brand loyalty and reduces churn as subscribers remain active to follow ongoing narratives. The emphasis on diverse storytelling and niche genres allows services to cater to specific demographic segments, enhancing their appeal. Award recognition, such as Emmys and Oscars, further validates the quality of streaming originals, attracting prestige-oriented viewers. The ability to release entire seasons at once supports binge-watching behaviors, which increase platform stickiness. Therefore, the continuous pipeline of premium original content acts as a critical magnet for subscriber acquisition and retention in a competitive landscape.

Convenience and Personalization Through Advanced Algorithms

Convenience and personalization through advanced algorithms fuel the growth of the United States subscription video-on-demand market. This enhances user experience and facilitates content discovery in vast libraries. Streaming platforms utilize sophisticated machine learning models to analyze viewing habits and recommend titles tailored to individual preferences, reducing the effort required to find enjoyable content. As per the sources, Global Institute personalization can deliver five to eight times the return on investment on marketing spend and lift sales by 10 percent or more, highlighting its economic impact. Features such as multiple user profiles, watch lists, and seamless cross-device synchronization allow subscribers to engage with content on their own terms and schedules. The ability to pause, resume, and download content for offline viewing adds to the flexibility that modern consumers expect. Algorithmic recommendations also help platforms promote lesser-known titles, optimizing the utilization of their content libraries. The intuitive user interfaces and minimal friction in navigation contribute to higher satisfaction levels compared to traditional cable services. This technological advantage creates a sticky ecosystem where users feel understood and valued. Hence, the combination of ease of use and intelligent curation drives sustained engagement and reduces the likelihood of subscription cancellation.

MARKET RESTRAINTS

Market Saturation and Subscription Fatigue

Market saturation and subscription fatigue are significant restraints to the United States subscription video-on-demand market. This limits the potential for new subscriber growth and increases churn rates. As the number of streaming services proliferates, consumers face decision fatigue and financial strain, leading them to rotate subscriptions rather than maintain multiple simultaneous accounts. As per a survey, a growing percentage of consumers, now roughly 41%, report canceling services because the content is not perceived to be worth the cost, indicating a shift toward more selective viewing habits. The fragmentation of content across numerous platforms forces users to manage multiple bills and interfaces, which diminishes the convenience factor that initially drove adoption. Many households have reached a ceiling in terms of the number of services they are willing to pay for simultaneously. This behavior results in volatile subscriber bases where users subscribe only to specific shows and cancel immediately after viewing. The lack of bundled options in the early stages of this fragmentation exacerbated the issue, although recent bundling efforts aim to address it. Thus, the saturation of the market creates a challenging environment for providers to achieve stable long-term growth without offering compelling, unique value or competitive pricing.

Rising Subscription Costs and Price Sensitivity

Rising subscription costs and price sensitivity hamper the expansion of the United States subscription video-on-demand market. This erodes the perceived value proposition and prompts consumers to seek cheaper alternatives. As platforms shift their focus from growth to profitability, they have implemented multiple price increases and introduced advertising-supported tiers that alter the user experience. As per the Bureau of Labor Statistics, the inflation rate has impacted household budgets, leading consumers to scrutinize discretionary spending, including entertainment subscriptions. Frequent price hikes can trigger backlash and mass cancellations, particularly among budget-conscious demographics such as students and young families. The introduction of ads into previously ad-free tiers is perceived by many loyal subscribers as a reduction in value, leading to dissatisfaction. Competitors offering lower-priced or free ad-supported services attract these price-sensitive users, creating pressure on premium providers to justify their higher fees. The transparency of pricing allows for easy comparison shopping, making it difficult for platforms to raise prices without losing customers. Additionally, the availability of pirated content or shared accounts provides low-cost alternatives for those unwilling to pay full price. Consequently, the tension between the need for revenue growth and consumer affordability constraints limits the pricing power of streaming services.

MARKET OPPORTUNITIES

Introduction of Advertising Supported Tiers

The introduction of advertising-supported tiers offers a significant opportunity for the United States subscription video-on-demand market. This expands the addressable audience to include price-sensitive consumers and creates new revenue streams. These lower-cost options allow platforms to attract users who are unwilling or unable to pay premium subscription fees, thereby reducing churn and increasing overall reach. As per a study, digital video ad spending is projected to grow substantially as advertisers recognize the targeting capabilities and engaged audiences of streaming platforms. Advertising tiers enable providers to monetize a broader user base while offering a more affordable entry point for consumers. Advanced data analytics allow for precise ad targeting based on viewing behavior and demographics, increasing the value proposition for advertisers. This model also provides a fallback option for subscribers who might otherwise cancel due to price increases. The integration of interactive and shoppable ads offers innovative engagement opportunities that traditional television cannot match. Diversifying revenue sources beyond subscription platforms can achieve greater financial stability and invest in content without relying solely on subscriber fees. Therefore, the strategic implementation of ad-supported tiers opens new avenues for growth and profitability in a maturing market.

Expansion into Live Sports and Events

The expansion into live sports and events provides a promising prospect for the United States subscription video-on-demand market. This attracts dedicated fan bases and reduces churn through exclusive real-time content. Live sports remain one of the few content categories that drive habitual viewing and immediate engagement, making them a valuable asset for streaming platforms. As per the Sports Business Journal, rights deals for major leagues are increasingly moving to streaming services, reflecting the shift in consumer viewing habits. Securing exclusive rights to popular sports leagues allows providers to differentiate themselves and justify premium pricing. The ability to stream live events on multiple devices enhances accessibility for fans who may not be near a television. Interactive features such as real-time statistics, multiple camera angles, and social integration enrich the viewing experience and foster community engagement. Live events also provide unique advertising opportunities, including dynamic ad insertion, which allows for targeted commercials during breaks. The exclusivity of live sports content creates a barrier to entry for competitors and encourages long-term subscriptions. Streaming platforms can secure a loyal and engaged audience by investing in live sports infrastructure and partnerships. Such an audience deeply values immediacy and exclusivity.

MARKET CHALLENGES

Password Sharing and Account Security

Password sharing and account security are a major challenge to the United States subscription video-on-demand market. This undermines revenue potential and complicates user management strategies. Many subscribers share their login credentials with friends and family outside their households, effectively reducing the number of paid accounts required to serve a larger audience. As per Netflix's internal estimates, over 100 million households accessed content through shared accounts, prompting a global crackdown that added millions of new paying subscribers by 2025. While some providers have implemented measures to restrict sharing, such as limiting the number of simultaneous streams or verifying household location,s these efforts often face consumer backlash and technical workarounds. Balancing enforcement with user convenience is difficult, as overly strict policies may drive legitimate customers to cancel subscriptions. Additionally, account sharing poses security risks,s including unauthorized access and data breaches, which can damage brand reputation. The lack of standardized identity verification methods across platforms makes it challenging to detect and prevent fraudulent usage effectively. Providers must invest in sophisticated detection algorithms and customer education campaigns to address this issue without alienating users. The ethical ambiguity surrounding sharing among close relatives further complicates policy implementation. Password sharing will continue to erode profitability and distort subscriber metrics. This will persist until effective and user-friendly solutions are developed.

Content Licensing and Rights Fragmentation

Content licensing and rights fragmentation hinder the expansion of the United States subscription video-on-demand market. This creates a disjointed user experience and increases the cost of content acquisition. As media companies launch their own proprietary streaming services, they often withdraw licensed content from third-party platforms to populate their own libraries. As per the Harvard Business Review, this fragmentation forces consumers to subscribe to multiple services to access their favorite shows and movies, leading to frustration and increased costs. The complexity of negotiating and managing rights across different regions and platforms adds to operational burdens for providers. Exclusive content deals drive up acquisition cost,s making it difficult for smaller players to compete with well-funded giants. The constant rotation of content libraries makes it hard for users to rely on any single platform for consistent access to specific titles. This instability can lead to subscriber dissatisfaction and churn as users seek more reliable sources of entertainment. Additionally, the legal complexities of international rights hinder global expansion strategies for US-based platforms. Consequently, the fragmented rights landscape creates inefficiencies and consumer friction that threaten the long-term sustainability of the subscription model.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.36% |

| Segments Covered | By Content Type, Device Type, End Use, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Netflix Inc., Amazon Prime Video, The Walt Disney Company, Warner Bros. Discovery, Paramount Global, Apple Inc., Comcast Corporation, Hulu LLC, Peacock TV, YouTube Premium |

SEGMENTAL ANALYSIS

By Content Type Insights

The TV shows segment held the majority share of the 35.5% of the United States Subscription Video On Demand market in 2025. This supremacy of the segment is credited to the serialized nature of content that fosters long-term viewer engagement and habitual viewing patterns. Unlike movies, which are typically one-time experiences, television series encourage subscribers to maintain their subscriptions over extended periods to follow ongoing storylines and character arcs. The main driver for this domination is the strategy employed by major platforms to release entire seasons or weekly episodes, which creates sustained buzz and social media conversation. This format allows for deeper world-building and character development, which resonates strongly with audiences seeking immersive entertainment. The ability to binge-watch multiple episodes in a single session has become a cultural phenomenon, further cementing the appeal of TV shows. Additionally, the diversity of genres, ranging from drama and comedy to science fiction, ensures broad demographic appeal. Platforms invest heavily in original series as they serve as key differentiators in a crowded market. The recurring revenue model aligns perfectly with the continuous consumption habits associated with television series. Therefore, the structural advantage of serialized storytelling and its ability to drive retention establish TV shows as the dominant content type.

The documentaries segment is expected to exhibit a noteworthy CAGR of 12.4% during the forecast period due to increasing consumer interest in true crime, social issues, and educational content. This genre has evolved from niche programming to mainstream entertainment, attracting diverse audiences who seek informative yet engaging narratives. According to a study, streaming platforms have increased their investment in documentary and unscripted content, which now accounts for a significant portion of their original catalogs, though some organizations emphasize the need for equitable sustainability for filmmakers within this model. The primary factor driving this growth is the rise of high-profile documentary series that spark public discourse and viral marketing opportunities. True crime documentaries in particular have captured the imagination of viewers, leading to high completion rates and strong word-of-mouth promotion. The lower production costs compared to scripted dramas allow platforms to experiment with diverse topics and formats, reducing financial risk. Furthermore, the educational value of documentaries appeals to families and lifelong learners, expanding the addressable market beyond traditional entertainment seekers. Streaming services often use documentaries to fulfill regulatory requirements for local or educational content in certain jurisdictions. The accessibility of archival footage and the ability to produce compelling stories without large casts or sets also contribute to the proliferation of this genre. Thus, the combination of cultural relevance, cost efficiency, and audience curiosity drives the rapid expansion of the documentary segment.

By Device Type Insights

The smart TVs segment dominated the United States Subscription Video On Demand market and accounted for a 44.1% share in 2025. This dominance of the segment is driven by its superior viewing experience, large screen size, and integration into the primary living room entertainment setup. Consumers prefer watching movies and television series on larger displays, which offer better picture quality and immersive sound compared to mobile devices or laptops. As per the Consumer Technology Association (CTA), smart TV penetration in United States households has reached approximately 82 percent, ensuring that the majority of subscribers have direct access to streaming applications on their primary display. A key accelerator for this leadership is the communal nature of television viewing, where families and friends gather to watch content together. Smart TVs eliminate the need for external streaming devices such as set-top boxes or gaming consoles, as most modern televisions come with built-in operating systems and app stores. The convenience of using a single remote control to navigate between live television and streaming services enhances user experience. Additionally, the advancement in display technologies such as four resolution and high dynamic range, Smart TVs are the ideal platform for premium content. Manufacturers continue to improve user interfaces and voice control features, making navigation more intuitive. The central role of television in home entertainment culture ensures its continued dominance. Providers optimize their platforms for big screen experiences, recognizing that this device drives the highest engagement and viewing duration. So, the visual superiority and convenience of Smart TVs establish them as the primary device for streaming consumption.

The tablets segment is predicted to witness the highest CAGR of 10.6% from 2026 to 203,4 owing to its portability, versatility, and suitability for personal viewing. Tablets offer a balance between the large screen of a laptop and the mobility of a smartphone, making them ideal for watching content in various settings, such as bed, kitchen, or during travel. As per sources, tablet ownership among American adults has plateaued at approximately 53 percent, with no significant difference in ownership rates across age groups, unlike smartphones, which see near-universal adoption among younger demographics. The primary factor accelerating this growth is the improvement in tablet display quality and battery life, which supports longer viewing sessions without frequent charging. The rise of remote work and hybrid learning has increased the amount of time individuals spend on tablets for both productivity and leisure, creating more opportunities for streaming consumption. Streaming platforms have optimized their applications for tablet interfaces, providing enhanced features such as offline downloads and multi-window capabilities. The ease of holding a tablet for extended periods makes it a preferred choice for binge-watching series or watching movies in relaxed positions. Additionally, the availability of affordable tablet models has expanded the user base to include children and seniors. The integration with smart home ecosystems allows tablets to serve as control hubs for other devices, further enhancing their utility. Consequently, the convenience and adaptability of tablets drive their rapid adoption as a secondary but increasingly important streaming device.

By End-use Insights

The individual end-user segment was the largest in the United States Subscription Video On Demand market and occupied a substantial share in 2025. This prominence of the segment is supported by the direct-to-consumer business model that targets households and personal viewers. This segment dominates because streaming services are primarily designed for personal entertainment, offering personalized recommendations and user profiles tailored to individual preferences. As per Digital TV Research, the number of subscription video on demand (SVOD) subscriptions in the United States and Canada reached approximately 409 million in 2023, with widespread adoption averaging roughly four services per household. The main reason for this leadership is the affordability and flexibility of monthly subscription plans, which allow individuals to choose services based on their specific content interests without long-term contracts. The ease of signing up and canceling services empowers consumers to manage their entertainment budgets effectively. The proliferation of original content catering to diverse tastes ensures that there is something for every individual viewer. Marketing efforts are heavily focused on acquiring individual subscribers through digital channels and social media campaigns. The ability to share accounts within families further enhances the value proposition for individual users. Additionally, the shift from cable television to streaming has been largely driven by individual choices to cut the cord in favor of more customizable options. Therefore, the focus on personalization, affordability, and convenience establishes individual users as the primary revenue source for streaming platforms.

The commercial end-user segment is estimated to register the fastest CAGR of 15.8% over the forecast period. This rapid expansion of the segment is fueled by the increasing use of streaming services in hospitality, healthcare, and corporate environments. Businesses are leveraging streaming platforms to provide entertainment and information to customers, patients, and employees, enhancing their service offerings and environment. As per AHLA (formerly HTNG) standards and Oracle Hospitality reports (2025), hotel chains are increasingly integrating casting and streaming services into guest rooms to meet the expectations of modern travelers who prefer accessing their own content over traditional cable packages. The primary factor driving this growth is the demand for personalized and on-demand entertainment in public and semi-public spaces. Hospitals use streaming services to provide patients with comforting content during stays, improving patient satisfaction scores. Corporate offices utilize streaming platforms for training videos, internal communications, and employee lounges, fostering a modern workplace culture. Licensing agreements for commercial use are becoming more streamlined, allowing businesses to legally access content at scale. The ability to manage multiple accounts and devices through centralized dashboards simplifies administration for commercial users. Additionally, the integration of streaming with digital signage and advertising platforms opens new revenue opportunities for businesses. Thus, the expansion of streaming applications beyond residential use into diverse commercial sectors drives the rapid growth of this segment.

REGIONAL ANALYSIS

The United States led the global Subscription Video On Demand market and captured a 40.2% share in 2025. This growth of the US market is supported by its advanced digital infrastructure, high disposable income, and mature media consumption habits. The country’s market status is characterized by intense competition among major global players who continuously innovate to capture viewer attention and spending. As per the Motion Picture Association, the United States is home to the highest number of subscription video-on-demand services globally, fostering a dynamic and fragmented landscape. The widespread adoption of high-speed broadband and smart devices facilitates seamless access to streaming content across the nation. Cultural factors such as the strong tradition of television viewing and the early adoption of digital technologies have accelerated the transition from linear to on-demand media. Regulatory frameworks regarding copyright and net neutrality shape the operational environment, ensuring fair competition and content protection. The presence of major production studios in Hollywood provides a steady supply of high-quality original content that attracts both domestic and international subscribers. The United States serves as a trendsetter for technological innovations in streaming, such as interactive content and personalized algorithms. The continuous investment in digital marketing and customer experience enhancements by key players ensures sustained growth. The combination of economic strength, technological leadership, and cultural influence solidifies the United States' position as the dominant force in the global Subscription Video On Demand industry.

COMPETITION OVERVIEW

The competition in the United States Subscription Video On Demand market is intense and characterized by the presence of large global aggregators, specialized niche platforms, and direct supplier channels. Major players compete on price, inventory breadth, and user experience, striving to offer the most convenient and cost-effective booking solutions. Differentiation is achieved through proprietary technology such as artificial intelligence-driven recommendations and seamless mobile interfaces that enhance customer satisfaction. The rise of alternative accommodations has intensified rivalry between traditional hotel-focused agencies and home-sharing platforms. Direct booking initiatives by airlines and hotel chains pose a significant challenge to intermediaries, prompting agencies to add value through bundled packages and loyalty rewards. Price transparency allows consumers to easily compare options, forcing companies to maintain competitive rates while managing thin margins. Customer retention is a key focus area with firms investing heavily in loyalty programs and personalized marketing to foster brand allegiance. Regulatory compliance and data security are critical factors influencing consumer trust and operational stability. The market sees continuous innovation in payment solutions and customer support technologies. Strategic acquisitions and partnerships are common as companies seek to expand their reach and capabilities. This dynamic landscape requires constant adaptation and investment to sustain growth and profitability.

KEY MARKET PLAYERS

A few major players of the U.S Subscription Video on Demand market include

- Netflix Inc

- Amazon Prime Video

- The Walt Disney Company

- Warner Bros. Discovery

- Paramount Global

- Apple Inc

- Comcast Corporation

- Hulu LLC

- Peacock TV

- YouTube Premium

Leading Players in the US SVOD Market

- Netflix Inc remains a pioneering force in the United States subscription video-on-demand market by offering an extensive library of films, television series, and documentaries. The company leverages sophisticated algorithms to personalize content recommendations, enhancing user engagement and retention. Recent actions include the successful rollout of an advertising-supported subscription tier, which attracts price-sensitive consumers and diversifies revenue streams. Netflix has also intensified its crackdown on password sharing to convert unauthorized users into paying subscribers, thereby boosting account growth. The platform continues to invest heavily in original local and international content to differentiate its offerings from competitors. By focusing on high production values and diverse genres, Netflix maintains its position as a preferred entertainment destination. Its global infrastructure ensures seamless streaming quality across various devices. These strategic initiatives strengthen its market presence by balancing subscriber growth with profitability while adapting to evolving consumer preferences and competitive pressures in the digital media landscape.

- Amazon.com Inc contributes significantly to the United States Subscription Video On Demand market through its Prime Video service, which is bundled with the broader Amazon Prime membership. This integration provides substantial value to subscribers, encouraging loyalty and reducing churn rates across the ecosystem. Recent actions involve the introduction of advertisements within the standard Prime Video tier, allowing the company to generate additional advertising revenue while keeping subscription prices stable. Amazon has also secured exclusive rights to major live sports events such as Thursday Night Football, attracting a wider audience beyond traditional movie and series viewers. The company leverages its technological prowess to enhance streaming quality and user interface experience. Investments in original content production continue to expand its library with critically acclaimed series and films. By combining e-commerce benefits with premium entertainment, Amazon creates a unique value proposition. These efforts solidify its position as a major competitor by leveraging its vast resources and existing customer base to drive engagement and revenue growth in the streaming sector.

- The Walt Disney Company plays a pivotal role in the United States subscription video-on-demand market with its flagship streaming service Disney+, which hosts content from Disney, Pixar, Marvel, Star Wars, and National Geographic. The company leverages its powerful intellectual property portfolio to attract families and fans of franchise content. Recent actions include the integration of Hulu content into the Disney+ platform for bundle subscribers, creating a more comprehensive entertainment hub. Disney has also focused on achieving profitability in its streaming division by implementing price increases and introducing ad-supported tiers. The company continues to produce high-budget original series and films that drive subscriber acquisition and retention. Strategic partnerships with telecommunications providers offer bundled deals that enhance accessibility and value. By capitalizing on its beloved brands and expanding its content offerings, Disney strengthens its competitive stance. These initiatives ensure sustained relevance and growth in a crowded market by appealing to diverse demographic segments through trusted and popular entertainment franchises.

Top Strategies Used by Key Market Participants

Key players in the United States Subscription Video On Demand market primarily focus on leveraging artificial intelligence to personalize user experiences and optimize search results for higher conversion rates. Companies are increasingly integrating alternative accommodations such as vacation rentals into their platforms to diversify inventory and appeal to broader consumer preferences. Strategic partnerships with airlines and hotel chains enable direct connectivity, ensuring real-time availability and competitive pricing for customers. Investment in mobile technology enhances accessibility and facilitates seamless last-minute bookings through intuitive applications. Loyalty programs are expanded and integrated across multiple brands to encourage repeat business and increase customer lifetime value. Marketing efforts emphasize sustainable travel options and unique experiences to align with evolving consumer values. Data analytics are utilized to refine targeting strategies and improve operational efficiency. These combined approaches help companies maintain competitive advantages and drive growth in a dynamic digital environment.

MARKET SEGMENTATION

This research report on the U.S subscription video on demand market has been segmented and sub-segmented based on content type, device type, end use & region.

By Content Type

- Movies

- TV Shows

- Documentaries

By Device Type

- Tablets

- Laptops

- Smart TVs

By End Use

- Individual

- Commercial

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What factors are driving the growth of the U.S. SVOD market?

The market is growing due to increasing internet penetration, rising smartphone usage, demand for on-demand entertainment, and the popularity of original streaming content.

2. What are the major content trends in the U.S. SVOD industry?

Popular trends include exclusive original series, regional content, live streaming integration, interactive programming, and AI-based personalized recommendations.

3. Which devices are commonly used to access SVOD services?

Consumers commonly access SVOD platforms through smart TVs, smartphones, tablets, laptops, gaming consoles, and streaming devices.

4. What role does artificial intelligence play in SVOD platforms?

AI helps platforms deliver personalized content recommendations, improve user experience, optimize streaming quality, and analyze viewer behavior.

5. How is mobile streaming affecting the SVOD market?

Mobile streaming increases content accessibility and supports higher user engagement, especially among younger consumers and users in remote locations.

6. What challenges are faced by SVOD service providers?

Major challenges include high content production costs, intense competition, subscriber churn, content piracy, and changing consumer preferences.

7. What is the impact of 5G technology on video streaming services?

5G technology improves streaming speed, reduces buffering, and enables high-quality video experiences such as 4K and live streaming.

8. How are advertising-supported subscription models evolving?

Many SVOD providers are introducing lower-cost ad-supported plans to attract price-sensitive consumers and generate additional advertising revenue.

9. What opportunities exist for new entrants in the SVOD market?

New entrants can focus on niche content categories, regional programming, sports streaming, and innovative user experiences to gain market share.

10. What is the future outlook for the U.S. subscription video on demand market?

The market is expected to witness steady growth due to increasing digital entertainment consumption, technological advancements, and rising demand for personalized content experiences.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com