U.S. Tablet PC Market Size, Share, Trends & Growth Forecast Report By Operating System, By Distribution Channel, By End User, and By Country (California, Texas, Florida, New York, Illinois & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

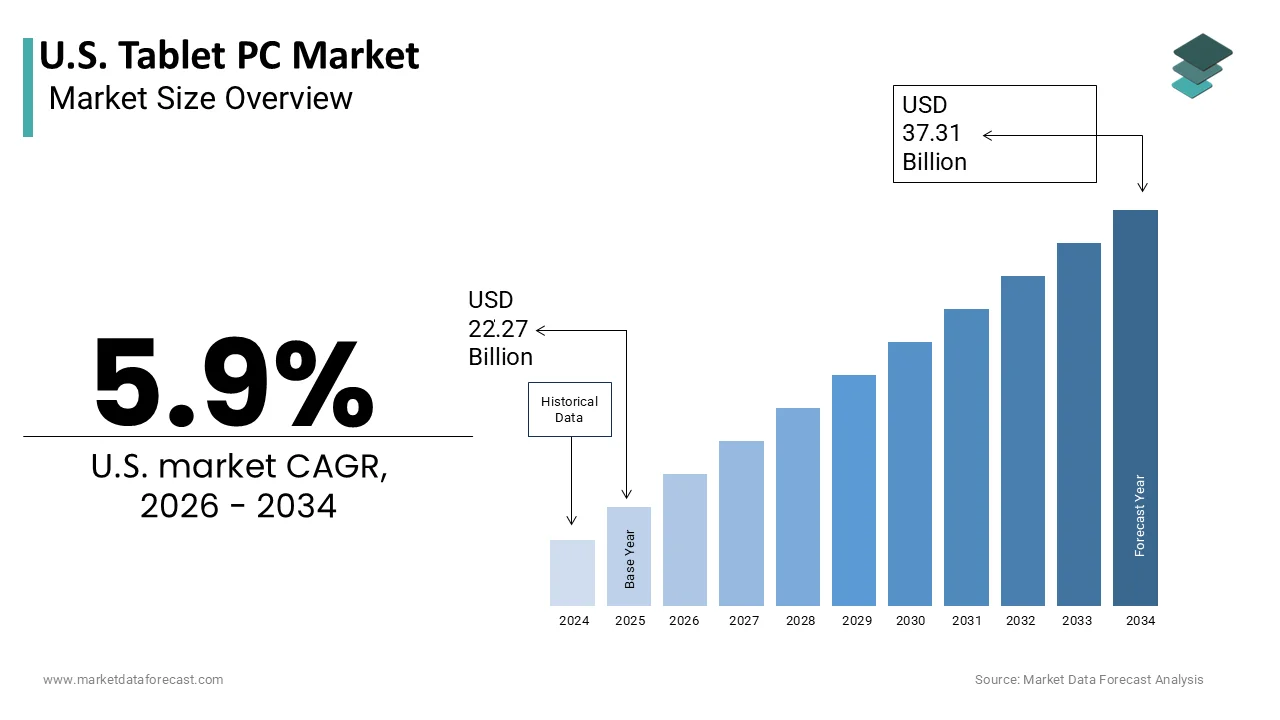

$22.27 BnMarket Estimate, 2026

$23.58 BnMarket Forecast, 2034

$37.31 BnCAGR, 2026–2034

5.9%U.S. Tablet PC Market Size

The U.S. Tablet PC Market was valued at USD 22.27 billion in 2025 and is estimated to reach USD 23.58 billion in 2026. The market is projected to grow to USD 37.31 billion by 2034, registering a CAGR of 5.9% from 2026 to 2034.

The tablet PC is a portable computing device characterized by touchscreen interfaces and versatile form factors that bridge the gap between smartphones and laptops. These devices serve roles in education, enterprise, healthcare, and consumer entertainment sectors, offering mobility without compromising device power. According to the National Center for Education Statistics, approximately 50 million students were enrolled in prekindergarten through grade 12 and postsecondary institutions in recent years, creating a massive base for educational technology adoption. Furthermore, the Bureau of Labor Statistics indicates that telework arrangements remain prevalent, with roughly 35% of employed individuals working from home at least part of the time, which sustains demand for secondary computing devices for home offices. The aging population also contributes to offering intuitive interfaces for digital literacy among seniors. As per the United States Census Bureau, individuals aged 65 and older constitute over 17% of the total population, representing a growing demographic that utilizes tablets for health monitoring and offering information. The integration of advanced processors and artificial intelligence capabilities has further enhanced productivity features, making tablets viable primary devices for creative professionals. Retailers and manufacturers focus on ecosystem integration, ensuring seamless connectivity with other smart devices.

MARKET DRIVERS

Pervasive Adoption in K-12 and Higher Education Systems

The extensive integration of tablet PCs into educational curricula is largely attributed to the growth of the United States tablet PC market. Schools and universities increasingly adopt digital learning platforms requiring robust and portable hardware for students and faculty. This infrastructure supports the widespread adoption of devices for interactive classrooms, remote learning, and standardized testing. The shift towards personalized learning experiences necessitates individual student access to computing devices,s fostering consistent replacement and upgrade cycles. As per the research, approximately 95% of teens report having access to a smartphone or computer at home, indicating a high level of digital saturation that extends to tablet usage for academic purposes. Educati,,onal institutions prioritize tablets due to their durability, long battery life, and touch interface, which enhances engagement for younger learners. State and federal funding initiatives, such as the Emergency Connectivity Fund, have historically subsidized device purchases, ensuring equitable access for low-income students. This institutional demand creates a stable revenue stream for manufacturers who tailor devices with rugged cases and educational software suites. The transition from physical textbooks to digital resources further amplifies the tablet as an essential educational tool.

Expansion of Remote Work and Hybrid Enterprise Models

The enduring presence of remote and hybrid work models in the corporate sector, as professionals seek flexible computing solutions, is driving the growth of the United States tablet PC market. Tablets offer the portability required for mobile employees, while providing sufficient processing power for video conferencing,g document editing, ng and client presentations. Enterprises increasingly issue tablets as secondary devices to complement laptops, ps allowing employees to maintain productivity during travel or in informal settings. The integration of enterprise-grade security features and compatibility with productivity suites make tablets viable for business operations. Corporate investments in digital transformation initiatives often include tablet deployments for field workers, retail staff, and healthcare enterprise-grade users who require real-time data access. The ability to use tablets as lightweight alternatives for meetings reduces physical strain and enhances convenience. Furthermore, the rise of bring your own device policies encourages professionals to purchase high-end tablets for personal use that seamlessly integrate with corporate networks. This dual utility drives premium segment growth as users seek devices with advanced connectivity and performance capabilities.

MARKET RESTRAINTS

Market Saturation and Extended Device Lifecycles

The increasing longevity of tablet devices by limiting the frequency of replacement purchases is hindering the growth of the United States tablet PC market. Modern tablets are built with durable materials and powerful processors that remain functional for several years, reducing the urgency for upgrades. This durability means that consumers do not need to replace their devices as frequently as they did in the early stages of market adoption. Additionally, the high initial penetration rate in US households means that most potential buyers already own a functional device. Manufacturers face challenges in convincing existing users to upgrade when their current devices still meet basic needs such as web browsing and media consumption. The lack of compelling new features in mid-range models further exacerbates this issue, as incremental improvements do not justify the cost of a new purchase. Economic uncertainty also leads consumers to delay discretionary spending on electronics, prioritizing essential expenditures instead. This combination of hardware durability, high ownership rates, and modest innovation cycles suppresses unit sales volume.

Competition from Large-Screen Smartphones and Lightweight Laptops

The intense competition from large-screen smartphones and increasingly lightweight laptops is additionally leveraging the growth of the United States tablet PC market. Modern smartphones with screens exceeding 6.7 inches offer sufficient display area for media consumption and light productivity, reducing the need for a separate tablet device. The smartphone shipments in the US remain robust,t with flagship models featuring larger displays capturing significant consumer attention. These devices provide constant connectivity and portability that tablets cannot match, making them the preferred choice for on-the-go usage. Simultaneously, the evolution of ultrabooks and convertible laptops offers superior typing experiences and multitasking capabilities at similar price points to premium tablets. Consumers often perceive laptops as more versatile for serious work on-the-go to physical keyboards and full operating systems. This functional overlap forces tablets into a niche role rather than a primary computing device for many users. The cannibalization effect is particularly evident in the mid-range segment, where consumers must choose between a capable laptop and a tablet.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Enhanced Productivity Features

The integration of artificial intelligence and advanced productivity features by transforming these devices into powerful creative and professional tools is setting up new opportunities for the growth of the United States tablet PC market. Manufacturers are embedding AI-driven capabilities, such as natural language processing, image enhancement, and automated task management, into tablet operating systems. The incorporation of AI assistants in Windows-based tablets enhances user efficiency by predicting actions and optimizing performance based on usage patterns. These features appeal to professionals seeking streamlined workflows and creative individuals requiring sophisticated editing tools. The development of powerful chipsets capable of handling machine learning tasks locally ensures privacy and speed. Software developers are creating optimized applications that leverage these hardware capabilities, offering unique experiences not available on traditional laptops. The ability to run desktop-class applications on tablets further bridges the gap between mobile and desktop computing. Enterprise users benefit from AI-enhanced security features that detect anomalies and protect sensitive data. This technological evolution positions tablets as indispensable tools for knowledge workers and creators.

Growth in Healthcare and Industrial Field Applications

The expansion of tablet usage in healthcare and industrial field operations by addressing specific professional needs for mobility and data access is also expected to escalate the growth of the United States tablet PC market. In healthcare tablets, facilitate electronic health record access, patient monitoring,g and telemedicine consultations, ns improving care delivery efficiency. Ruggedized tablets designed for industrial environments enable workers in manufacturing logistics and construction to acquire real-time data, manage inventory, and perform inspections. The adoption o,f enterprise mobile devices in the warehousing and transportation sectors continues to rise, driven by the need for operational visibility and accuracy. These specialized tablets feature enhanced real-time barcodes, scanners,s and long battery lives suited for demanding conditions. The ability to customize software for specific industry workflows adds value beyond consumer applications. Healthcare providers benefit from portable devices that reduce administrative burdens and improve patient engagement. Industrial firms leverage tablets to optimize supply chain operations and reduce downtime through predictive maintenance apps.

MARKET CHALLENGES

Supply Chain Volatility and Component Shortages

The supply chain volatility and persistent component shortages are likely to pose a major challenge for the growth of the United States tablet PC market. The production of tablets relies on complex global supply chains for semiconductors, display panels, and batteries, which are susceptible to disruptions. Fluctuations in chip availability have historically impacted the production schedules of consumer electronics manufacturers, leading to delayed product launches. Geopolitical tensions and trade restrictions that further complicate sourcing strategies give increasing costs and uncertainty. The reliance on specific regions for manufacturing creates vulnerabilities to natural disasters and labor disputes. Supply-side constraints force companies to manage inventory carefully and often pass increased costs to consumers,s potentially dampening demand. Logistics hurdles, such as port congestion and shipping delays, exacerbate the issue affecting timely delivery to retailers. The shortage of specialized components like advanced display drivers limits the ability to produce high end mo, dels at scale. Manufacturers must invest in diversified supply chains and strategic stockpiling to mitigate risks, but these measures increase operational expenses. The unpredictability of supply conditions hampers long-term planning and the product roadmap.

Security Vulnerabilities and Data Privacy Concerns

The security vulnerabilities and data privacy concerns, particularly in the enterprise and healthcare sectors, are also impeding the growth of the United States tablet PC market. As tablets become integral to professional workflows, they store and transmit sensitive information, making them attractive targets for cyberattacks. The open nature of some operating systems and third-party applications creates entry points for malware and data breaches. Enterprises struggle to enforce consistent security policies across a diverse device fleet, especially in bring your own device environments. Mobile devices often lack the robust endpoint protection found in traditional computers, leaving them vulnerable to exploitation. Privacy regulations, such as the California Consumer Privacy Act, impose strict requirements on data handling, requiring manufacturers and developers to implement rigorous compliance measures. Failure to address these concerns can result in legal liabilities and reputational damage. Users are increasingly aware of privacy risks and may hesitate to adopt tablets for sensitive tasks if trust is compromised. Manufacturers must invest heavily in security features, such as biometric authentication,n encryption, and regular software updates. However, balancing security with user convenience remains difficult. The evolving threat landscape requires constant vigilance and innovation in security protocols.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Operating System, Distribution Channel, End-User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Texas, Florida, New York, and the rest of the United States |

| Market Leaders Profiled | Apple Inc., Samsung Electronics Co., Ltd., Microsoft Corporation, Lenovo Group Limited, Amazon.com, Inc., ASUSTeK Computer Inc., Acer Inc., HP Inc., Dell Technologies Inc., Huawei Technologies Co., Ltd., Xiaomi Corporation, Google LLC |

SEGMENTAL ANALYSIS

By Operating System Insights

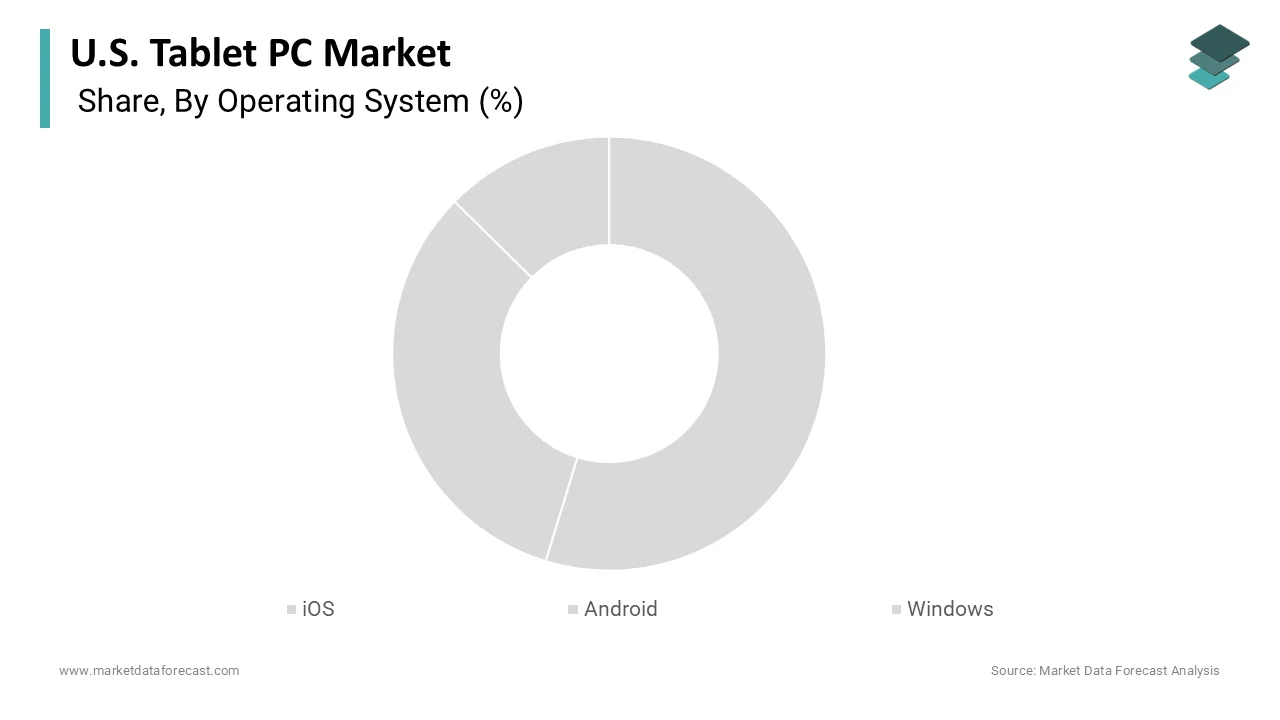

The iOS operating system segment was the largest by holding 34.6% of the US tablet PC market share in 2025, with the strong ecosystem integration and high consumer loyalty associated with Apple devices. The iPad brand has become synonymous with tablets in the American consciousness, creating a powerful network effect that encourages continued adoption. The seamless connectivity between iPhones,s Macs, and iPads, which allows users to share data and continue tasks across devices effortlessly, is elevating the growth of the segment. The App Store offers a vast library of optimized applications specifically designed for the larger tablet interface providing su,perio, r user experiences compared to competitors. Educational institutions also favor iOS devices due to their ease of management through Apple School Manager and robust security features. The longevity of software support for older iPad models ensures that devices remain functional and secure for many years, enhancing their value proposition. Consumers perceive iPads as premium products with high resale values, which justifies the initial investment. The consistent release of new features, such as Stage Manager and Apple Pencil support,t further differentiates iOS tablets from Android and Windows alternatives.

The Windows operating system segment is projected to register the fastest CAGR of 5.4% during the forecast period due to the increasing demand for hybrid devices that combine tablet portability with laptop productivity. Microsoft Surface devices and other Windows-based tablets are gaining traction among professionals who require the full desktop application compatibility in a portable form factor. The shipments of detachable tablets running Windows have shown steady growth as remote work trends persist and users seek versatile computing solutions. The integration of artificial intelligence features in Windows 11, such as Copilot, enhances productivity and appeals to enterprise users looking to optimize workflows. As per Microsoft, the adoption of Windows on ARM architecture is improving battery life and performance,e making Windows tablets more competitive with traditional x86 laptops. Corpo, rate IT departments prefer Windows tablets for their manageability and compatibility with existing enterprise software infrastructure. The ability to run legacy applications without emulation on issues is a significant advantage over iOS and Android platforms. Additionally, the rise of hybrid work models drives demand for devices that can serve as both primary laptops and secondary tablets. Manufacturers are introducing innovative form factors, such as dual-screen and foldable devices running Windows, to capture niche markets. The growing emphasis on security and compliance in regulated industries further boosts Windows adoption.

By Distribution Channel Insights

The online sales segment was the largest by holdindual-screendual-screene United States tablet PC market share in 2025, with the convenience of extensive product selection and competitive pricing. Consumers prefer purchasing electronics online due to the ability to compare specifications, reviews,s and find the best deals without visiting physical stores. The e-commerce sales of electronics and appliances have grown significant,l y,, with online channels capturing a substantial portion of retail transactions. Major platforms, such as Amazon, Best Buy, and Apple Store, offer vast inventories of tablets from various brands by allowing consumers to find specific models and configurations easily. The availability of detailed product information and customer feedback helps buyers make informed decisions by reducing the perceived risk of online purchasing. Home delivery services eliminate the logistical challenge of transporting bulky items, ms which is particularly appealing to urban residents. As per the National Retail Federation, retailers have invested heavily in logistics and last-mile delivery capabilities, ensuring faster and more reliable shipping options. Promotional events, such as Prime Day and Black Friday, further drive online sales through significant discounts and bundled offers. The integration of augmented reality tools on solast-milerms allows users to visualize products, thus enhancing confidence in purchase decisions. The ease of return policies offered by major online retailers also mitigates concerns about product suitability.

The online sales channel is expected to grow at the fastest CAGR of 12.2% during the forecast period, with the continuous expansion of digital infrastructure and changing consumer behaviors. The proliferation of high-speed internet and mobile devices has made online shopping more accessible to a broader demographic, including older adults. The rise of social media and influencer marketing drives traffic to online retail platforms where targeted advertising influences purchasing decisions. Manufacturers are increasingly adopting direct-to-consumer models, bypassing traditional intermediaries to offer exclusive deals and personalized experiences. The integration of artificial intelligence in recommendation engines enhances product discovery, leading to higher conversion rates. Subscription services and trade-in programs offered exclusively online encourage repeat purchases and brand loyalty. The flexibility of payment options, such as buy now pay later services, makes high-end tablets more high-end for younger consumers. Additionally, the ability to access global brands and niche products not available in local stores attracts tech enthusiasts.

By End-User Insights

The individual users segment was the largest by holding 44.3%high-endUS tablet PC market share in 2025, with the versatility of tablets for entertainment, communication, and personal productivity. Consumers utilize tablets for media consumption, gaming, social networking, and light work tasks, making them essential household devices. The affordability of entry level table, ts makes them accessible to a broad demographic, including students, seniors, and families. Tablets serve as ideal devices for children, due to their durability and parental control features, fostering early digital literacy. Seniors also adopt entry-level strategies for staying connected with family members, accessing health information,n and engaging in cognitive exercises. The intuitive touch interface lowers the barrier to entry for non-technical users. Individual users frequently upgrade devices to access new features and improved performance, causing replacement cycles. The popularity of streaming services and mobile gaming further incentivizes the purchase of high-performance tablets with large displays and long battery life. Personalization options, such as cases and accessories, enhance the user experience and emotional connection to the device.

The schools and colleges segment is likely to grow at the fastest CAGR high-performance6 to 2034 due to the accelerated digital transformation in education. Educational institutions are increasingly integrating tablets into curricula to facilitate interactive learning, remote education, and administrative efficiency. Programss, such as the Emergency Connectivity Fund, have provided billions of dollars to support the purchase of devices and internet access for students in need. Tablets offer portable and engaging platforms for accessing digital textbooks,tbooks educational apps, a nd collaborative tools. Higher education institutions utilize tablets for note-taking, research, and virtual laboratories,s enhancing the academic experience. The shift towards hybrid learning models requires flexible devices that support both in-person and remote instruction. Schools are investing in device management systems to ensure note-taking, content filtering, and protecting students online. The longevity and durability of modern educational tablets reduce the total cost of ownership for schools. Teacher training programs focus on integrating technology into pedagogy, further driving effective usage.

COMPETITIVE LANDSCAPE

The competition in the US tablet PC market is intense and characterized by the dominance of established technology giants alongside emerging challengers seeking niche opportunities. Apple maintains a leading position through its strong ecosystem and premium branding, while Samsung and Microsoft compete vigorously with diverse Android and Windows offerings.s Price competition is evident in the mid -range anentry-levelel segments, where manufacturers offer value-driven devices to attract budget-conscious consumers. Enterprise and education sectors represent critical battlegrounds where vendors compete on manageability, security, and bulk pricing agreements. Retailers and online platforms play significant roles in shaping consumer preferences through promotions and exclusive bundles. The shift towards hybrid work and digital learning sustains demand for versatile devices that support productivity and collaboration. Companies also focus on sustainability and durability to appeal to environmentally aware buyers and reduce electronic waste. Intellectual property disputes and patent licensing agreements occasionally influence competitive dynamics.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Tablet PC Market include

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Microsoft Corporation

- Lenovo Group Limited

- Amazon.com, Inc.

- ASUSTeK Computer Inc.

- Acer Inc.

- HP Inc.

- Dell Technologies Inc.

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- Google LLC

TOP LEADING PLAYERS IN THE MARKET

- Apple Inc dominates the US tablet PC market through its iconic iPad lineup, which sets the industry standards for performance, design, and ecosystem integration. The company continuously innovates by introducing powerful custom silicon,n such as the M series chips, that bring desktop-class capabilities to portable devices. The launch of the iPad Pro with ultra retina display technology and enhanced artificial intelligence features tailored for creative professionals. Apple strengthens its position by expanding services like Apple Arcade and iCloud, which increase user stickiness and device utility. The company also focuses on sustainability initiatives using recycled materials in manufacturing to appeal to environmentally conscious consumers.

- Samsung Electronics Co., Ltd. maintains a strong presence in the US tablet PC market by offering a diverse range of Android-based tablets catering to various consumer segments. The Galaxy Tab series is renowned for its vibrant displays, versatile S Pen functionality, and robusmultitaskingCo, Ltd.b abilities Samsung recently strengthened its market position by integrating advanced Android-based intelligence features into its One UI software,e enhancing productivity and user experience. The company actively partners with major carriers and retailers to ensure widespread availability and promotional support for its latest models. Samsung also emphasizes cross-device connectivity, allowing seamless interaction between Galaxy smartphones, tablets, and laptops.

- Microsoft Corporation contributes significantly to the US tablet PC market through its Surface lineup, which bridges the gap between traditional laptops and PCs. The company targets enterprise users, students, teams, and creative professionals with devices that run full Windows operating systems, enabling complete desktop application compatibility. The introduction of Surface Pro models equipped with neural processing units to support local artificial intelligence workloads and improved battery efficiency. Microsoft strengthens its position by bundling productivity software such as Microsoft 365 with hardware purchases, creating added value for business and educational customers. The company also enhances security features and manageability tools for IT administrators,s making Surface devices attractive for corporate deployments.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the US tablet PC market primarily focus on product differentiation through advanced hardware specifications and unique software ecosystems to attract diverse consumer segments. Companies invest heavily in research and development to integrate artificial intelligence capabilities, es enhancing productivity and user personalization. Strategic partnerships with educational institutions and enterprise clients help secure bulk contracts and establish long-term usage patterns. Manufacturers emphasize ecosystem integration, ensuring seamless connectivity between tablet smartphones and laptops to increase brand loyalty. Pricing strategies vary from premium positioning for high-end models to competitive pricing for entry-level devices to capture broader market share. Marketing efforts highlight versatility, creativity, and mobility,y appealing to remote workers, students, and content creators. Supply chain optimization and local manufacturing initiatives reduce costs and mitigate logistical risks. Continuous software updates and security enhancements maintain device relevance and protect user data. These multifaceted strategies enable participants to sustain competitiveness and adapt to evolving technological trends in the dynamic US appliance landscape.

MARKET SEGMENTATION

This research report on the U.S. tablet pc market is segmented and sub-segmented into the following categories.

By Operating System

- iOS

- Android

- Windows

- Others

By Distribution Channel

- Online Sales

- Offline Sales

By End-User

- Individual Users

- Schools and Colleges

- Enterprises

- Healthcare Institutions

- Government Organizations

- Others

By Country

- California

- Texas

- Florida

- New York

- Illinois

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com