U.S. Waste Management Market Size, Share, Trends & Growth Forecast Report By Waste Type, By Service, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Waste Management Market Size

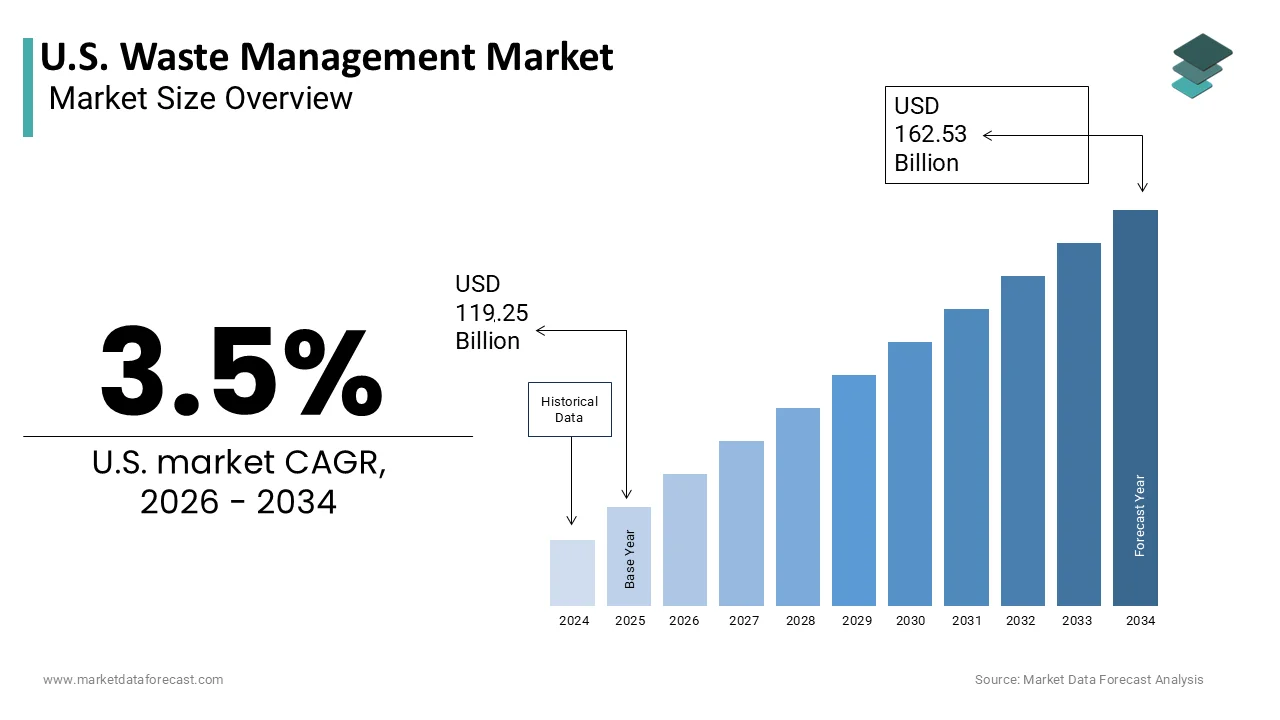

The U.S. Waste Management Market was valued at USD 119.25 billion in 2025, is estimated to reach USD 123.43 billion in 2026, and is projected to reach USD 162.53 billion by 2034, growing at a CAGR of 3.5% from 2026 to 2034.

According to the U.S. Environmental Protection Agency, the nation generates approximately 265 million tons of municipal solid waste annually, reflecting the substantial volume managed by this sector. Furthermore, as per the U.S. Census Bureau, the nation’s population reached approximately 334.9 million in 2023, driving consistent demand for waste services across expanding urban and suburban areas. The composition of waste has shifted significantly, with plastics and organic materials constituting a larger proportion of the waste stream. As per the U.S. Environmental Protection Agency, approximately 32.1% of municipal solid waste is recycled or composted, indicating significant potential for improvement in diversion rates. Landfill capacity remains a concern as many existing sites approach closure, necessitating investment in new facilities and alternative treatment technologies. The integration of advanced sorting technologies and data analytics is transforming operational efficiency, allowing for better tracking and optimization of waste flows. These dynamics define a market that is evolving from simple disposal to sophisticated resource management, driven by regulatory pressure, technological innovation, and growing environmental awareness among consumers and businesses alike.

MARKET DRIVERS

Stringent Environmental Regulations and Landfill Diversion Mandates Drive Service Adoption

Strict environmental regulations and ambitious landfill diversion mandates are primarily driving the growth of the U.S. waste management market. Federal and state laws increasingly restrict the types of waste allowed in landfills and set specific targets for waste reduction and material recovery. According to the U.S. Environmental Protection Agency, 9 states have implemented various types of organic waste landfill bans, requiring separate collection and processing for composting or anaerobic digestion. As per the National Conference of State Legislatures, 7 states have currently enacted packaging extended producer responsibility laws, which shift the financial burden of recycling packaging materials from taxpayers to manufacturers. This regulatory shift drives investment in specialized collection infrastructure and processing facilities capable of handling diverse material streams. As per the U.S. Environmental Protection Agency, food waste management methods such as composting and anaerobic digestion saw a 37% increase in throughput between 2020 and 2023. Furthermore, local governments are adopting zero-waste goals that require comprehensive waste audits and tailored management strategies. These policies encourage the adoption of single-stream recycling systems, which simplify participation for residents and increase capture rates. The pressure to meet diversion targets also stimulates innovation in waste sorting technologies such as optical sorters and artificial intelligence-driven robots. Consequently, the regulatory landscape acts as a powerful catalyst for market growth, forcing stakeholders to expand service offerings and improve operational efficiency to meet legal requirements and avoid penalties.

Rapid Urbanization and Population Growth Increase Waste Generation Volumes

The continuous trend of urbanization and steady population growth in the U.S. is further contributing to the waste management market growth in the U.S. As more people concentrate in urban areas, the density of waste production rises, requiring efficient and frequent collection services to maintain sanitation and public health. According to the U.S. Census Bureau, the urban population accounts for over 80% of the total populace, creating high demand for municipal solid waste services in metropolitan regions. Data from the Bureau of Labor Statistics shows that household spending on waste removal services has increased in line with population growth, reflecting the essential nature of these utilities. The expansion of commercial activities in urban centers further contributes to waste volumes, with businesses generating significant amounts of packaging, paper, and organic waste. As per the U.S. Environmental Protection Agency, the commercial, institutional, and industrial sectors contribute approximately 50% of the total municipal solid waste stream. This substantial volume requires robust infrastructure, including transfer stations and large-scale recycling facilities, to manage logistics effectively. Furthermore, the construction boom in growing cities generates considerable construction and demolition debris, which requires specialized handling and recycling services. The need to manage these diverse waste streams efficiently drives investment in fleet modernization and route optimization software. Consequently, the demographic and economic expansion in urban areas sustains strong demand for comprehensive waste management solutions, ensuring consistent revenue growth for service providers.

MARKET RESTRAINTS

High Operational Costs and Fuel Price Volatility Constrain Profit Margins

Elevated operational costs and the volatility of fuel prices represent significant restraints on the U.S. waste management market by squeezing profit margins and limiting investment capacity. Waste collection and transportation are heavily dependent on diesel-fueled trucks, making fuel expenses a major component of operational budgets. According to the U.S. Energy Information Administration, diesel prices reached a national average of $4.21 per gallon in early 2024, creating significant cost pressures for heavy-duty vehicle operators. Data from the American Trucking Associations indicates that fuel accounts for approximately 20% to 30% of total operating expenses for heavy-duty vehicles, impacting the financial stability of waste management firms. Furthermore, the cost of labor has risen due to shortages of qualified drivers and equipment operators, forcing companies to increase wages to retain staff. As per the Bureau of Labor Statistics, wages for refuse and recyclable material collectors increased by approximately 5.4% annually in recent reporting periods. Maintenance costs for heavy machinery and collection vehicles also add to the financial burden, particularly as emissions standards require more expensive engine technologies. The combination of these rising costs limits the ability of companies to invest in new technologies or expand services without raising fees. However, rate increases are often regulated by local municipalities, creating a rigid pricing environment. Consequently, these financial pressures act as a brake on market expansion, forcing operators to focus on efficiency improvements rather than growth initiatives.

Limited Landfill Capacity and Site Approval Delays Restrict Disposal Options

The diminishing availability of landfill capacity and the prolonged process for approving new sites are further hampering the U.S. market expansion. Many existing landfills are approaching their permitted capacity, and finding suitable locations for new facilities is increasingly difficult due to environmental concerns and community opposition. According to the Environmental Research and Education Foundation, the number of active municipal solid waste landfills in the U.S. decreased by over 75% between 1986 and 2023, which is leaving approximately 1,600 active sites. Data from the Environmental Protection Agency indicates that the average distance waste must travel to reach a landfill has increased, leading to higher transportation costs and carbon emissions. The permitting process for new landfills can take five to ten years, involving extensive environmental impact assessments and public hearings. As per the National Waste and Recycling Association, community resistance, often referred to as NIMBYism, significantly delays or blocks new projects regardless of technical merit. This scarcity of disposal space forces waste managers to rely on long-haul transfers to distant facilities, which is economically and environmentally unsustainable. Furthermore, stricter regulations on landfill leachate and methane emissions increase the cost of operating existing sites. Consequently, the lack of adequate disposal infrastructure constrains the market, forcing greater reliance on recycling and waste-to-energy alternatives, which may not yet be fully scalable or economically viable in all regions.

MARKET OPPORTUNITIES

Expansion of Waste-to-Energy Technologies Offers Sustainable Revenue Streams

The expansion of waste-to-energy technologies is a significant opportunity for the U.S. waste management market. This approach reduces landfill dependence while generating renewable energy, aligning with national sustainability goals. According to the U.S. Energy Information Administration, 60 waste-to-energy plants were operating in the U.S. in 2022, processing nearly 30 million tons of municipal solid waste. Data from the U.S. Department of Energy indicates that waste-to-energy plants reduce the volume of waste sent to landfills by up to 90%, offering a highly efficient disposal solution. The growing demand for renewable energy sources encourages utilities and municipalities to partner with waste management firms to develop new facilities. As per the U.S. Department of Energy, the waste-to-energy market is projected to grow from $40.7 billion in 2025 to $43.85 billion in 2026, at a compound annual growth rate of 7.8%. Advanced technologies, such as gasification and pyrolysis, allow for the conversion of diverse waste streams, including plastics and biomass, into valuable synthetic fuels. These innovations expand the applicability of waste-to-energy beyond traditional incineration. Furthermore, the production of refuse-derived fuel provides an alternative energy source for industrial processes, reducing reliance on fossil fuels. By integrating waste-to-energy solutions, waste management companies can diversify their revenue streams and enhance their environmental credentials. This strategic shift positions the industry as a key contributor to the circular economy and energy security.

Integration of Smart Waste Management Systems Enhances Operational Efficiency

The integration of smart waste management systems offers a substantial opportunity for the U.S. market. This technology enables dynamic scheduling, reducing unnecessary trips and lowering fuel consumption. According to the U.S. Department of Energy, the smart waste management market is expected to grow from $2.95 billion in 2025 to $3.38 billion in 2026, at a compound annual growth rate of 14.4%. As per the data from the Environmental Protection Agency, optimized collection schedules can decrease greenhouse gas emissions by minimizing vehicle idle time and mileage. Sensors installed in waste containers transmit real-time data to central platforms, allowing operators to prioritize full bins and adjust frequencies based on actual demand. As per the U.S. Department of Energy, smart waste solutions are projected to grow to $5.81 billion by 2030, at a compound annual growth rate of 14.5%. Furthermore, data analytics provide insights into waste generation patterns, helping planners design better recycling programs and educate residents. The integration of these systems also improves customer service by providing accurate billing based on usage rather than flat rates. Additionally, smart technology facilitates better compliance with recycling guidelines by identifying contamination sources. By adopting these digital tools, waste management companies can enhance operational transparency and reduce environmental impact. This technological evolution creates new value propositions for clients and positions providers as innovative partners in urban sustainability efforts.

MARKET CHALLENGES

Labor Shortages and Workforce Aging Impact Service Reliability

The persistent shortage of skilled labor and the aging workforce are major challenges to the U.S. waste management market by affecting service reliability and increasing operational risks. The industry faces difficulties in recruiting and retaining truck drivers, equipment operators, and facility workers due to perceived job hazards and competitive wage pressures in other sectors. According to the Bureau of Labor Statistics, the median age of refuse and recyclable material collectors is 43.1 years, indicating a demographic that is slightly older than the general workforce median. Data from the Solid Waste Association of North America reveals that difficulty in filling entry-level positions has led to service delays and overtime costs. The physical demands of the job and safety concerns further deter younger workers from entering the field. As per the Bureau of Labor Statistics, the waste collection industry employs approximately 68,300 specialized collectors, yet vacancy rates remain high in several metropolitan areas. The lack of automation in many collection routines means that labor shortages directly impact service frequency and quality. Furthermore, the cost of training new employees adds to operational burdens while turnover remains high. Consequently, the workforce crisis threatens the stability of waste collection services, forcing companies to invest heavily in recruitment incentives and safety improvements. Until the industry can attract a new generation of workers or accelerate automation adoption, labor constraints will remain a critical vulnerability.

Contamination in Recycling Streams Reduces Material Value and Processing Efficiency

High levels of contamination in recycling streams are further challenging the expansion of the U.S. waste management market by reducing the value of recovered materials and complicating processing operations. When non-recyclable items, such as food residue, plastics, and hazardous waste, are mixed with recyclables, it degrades the quality of the output and increases processing costs. According to the U.S. Environmental Protection Agency, contamination levels in some inbound recycling streams can reach as high as 25% or more, complicating the recovery of usable materials. Data from the Environmental Protection Agency indicates that contaminated batches are frequently sent to landfills instead of being recycled, undermining diversion goals and wasting resources. The presence of contaminants damages sorting equipment and increases maintenance requirements for material recovery facilities. As per the U.S. Environmental Protection Agency, high contamination rates have significantly increased the cost of processing a ton of recycling, making programs less economically viable for operators. Furthermore, global markets for recycled materials have become stricter regarding quality standards, reducing export opportunities for contaminated loads. Domestic processors struggle to handle low-grade materials, leading to stockpiling or disposal. Consumer confusion about what can be recycled exacerbates the problem despite education efforts. Consequently, contamination erodes the profitability of recycling programs and hinders the development of a robust circular economy. Addressing this issue requires significant investment in public education and advanced sorting technologies, which strain municipal and corporate budgets.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Waste Type, Service, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Waste Management, Inc., Republic Services, Inc., Waste Connections, Inc., Clean Harbors, Inc., Casella Waste Systems, Inc., GFL Environmental Inc., Stericycle, Inc., Recology Inc., Advanced Disposal Services, Inc., Covanta Holding Corporation, Veolia North America, FCC Environmental Services |

SEGMENTAL ANALYSIS

By Waste Type Insights

The municipal solid waste segment dominated the market in 2025 and is likely to maintain its dominant position in the U.S. market during the forecast period, as consistent household consumption and urban growth drive core service volumes. This segment encompasses everyday items discarded by the public, such as packaging, food scraps, yard trimmings, furniture, and electronics. The high consumption patterns of the American population, coupled with a culture of convenience that relies heavily on single-use products, are further contributing to the dominance of the municipal solid waste segment in the U.S. market. According to the U.S. Environmental Protection Agency, approximately 292.4 million tons of municipal solid waste were generated in the most recent comprehensive reporting year. This vast quantity requires extensive collection infrastructure and disposal capacity, making it the largest revenue generator for waste management firms. Data from the Census Bureau indicates that the U.S. population exceeded 335 million people, with over 80% living in urban areas where waste generation per capita is highest. The density of urban living necessitates frequent and organized collection services to maintain public health and sanitation standards. As per the American Public Works Association, municipal waste collection accounts for a significant portion of city budgets, reflecting its critical importance. Furthermore, the diversity of materials within municipal solid waste streams creates opportunities for recycling and recovery programs, although contamination remains a challenge. The consistent and predictable nature of residential waste generation ensures stable demand for waste management services regardless of economic fluctuations. These factors collectively establish municipal solid waste as the cornerstone of the industry, driving the majority of operational activity and investment in collection and processing infrastructure.

However, the e-waste segment in the U.S. is likely to experience rapid expansion during the forecast period owing to the increasing ownership of smartphones, laptops, tablets, and wearable devices, which are frequently replaced due to obsolescence or damage. According to the Consumer Technology Association, annual U.S. retail sales for consumer electronics exceeded $485 billion in 2023, with millions of devices eventually entering the waste stream. Data from the Environmental Protection Agency estimates that only approximately 15% to 20% of e-waste is currently recycled, highlighting a massive gap between generation and proper disposal. The presence of valuable materials, such as gold, silver, and copper, in electronic devices creates economic incentives for specialized recycling services. As per the Institute of Scrap Recycling Industries, the value of recovered materials from e-waste contributes significantly to the economy, driving investment in advanced sorting and recovery technologies. Furthermore, stringent regulations regarding the disposal of hazardous components, like batteries and leaded glass, are forcing manufacturers and consumers to seek certified recycling options. The rise of extended producer responsibility laws also shifts the burden of e-waste management to manufacturers, encouraging the development of take-back programs. These dynamics position e-waste as a high velocity segment that requires specialized handling and offers significant growth potential for waste management companies capable of managing complex material streams.

By Service Insights

The collection service segment led the market and accounted for the largest share of the U.S. market in 2025. The growth of the collection service segment in the U.S. market is attributed to the mandatory nature of waste removal for public health and sanitation, which ensures consistent demand regardless of economic conditions. According to the Bureau of Labor Statistics, employment in the waste collection industry remains stable, with over 68,300 specialized collectors ensuring regular pickup schedules. Data from the Environmental Protection Agency indicates that nearly all households in urban and suburban areas have access to curbside collection services, reflecting the ubiquity of this segment. The logistical complexity of collecting waste from millions of dispersed locations requires significant infrastructure investment in fleets and routing software. As per the American Public Works Association, collection costs typically account for 50% to 70% of total municipal waste management budgets, highlighting their financial significance. Furthermore, the frequency of collection, whether weekly or biweekly, creates recurring revenue streams for service providers. The integration of automated collection trucks has improved efficiency, but the labor-intensive nature of the service maintains its prominence. Additionally, the expansion of separate collection streams for recycling and organics increases the volume of collection activities. These factors collectively establish collection as the backbone of the waste management industry, driving the majority of operational interactions and customer relationships.

On the other side, the waste-to-energy service segment is estimated to showcase a promising CAGR of 13.4% during the forecast period in the U.S. market, owing to the increasing pressure to divert waste from landfills while simultaneously meeting renewable energy targets. According to the U.S. Energy Information Administration, waste-to-energy facilities in the U.S. process nearly 30 million tons of waste annually, generating enough electricity to power approximately 2 million homes. Data from the Department of Energy indicates that waste-to-energy reduces the volume of waste sent to landfills by up to 90%, offering a highly efficient disposal solution. The growing demand for sustainable energy sources encourages utilities and municipalities to partner with waste management firms to develop new facilities. As per the U.S. Department of Energy, investments in waste-to-energy infrastructure are projected to grow from $40.7 billion in 2025 to $43.85 billion in 2026, at a compound annual growth rate of 7.8%. Advanced technologies, such as plasma gasification, allow for the conversion of diverse waste streams, including plastics and biomass, into valuable synthetic fuels. These innovations expand the applicability of waste-to-energy beyond traditional incineration. Furthermore, the production of refuse-derived fuel provides an alternative energy source for industrial processes, reducing reliance on fossil fuels. By integrating waste-to-energy solutions, waste management companies can diversify their revenue streams and enhance their environmental credentials, positioning this segment for rapid expansion.

COUNTRY LEVEL ANALYSIS

U.S. Waste Management Market Analysis

The U.S. waste management sector is likely to lead North American market activity for the next few years, as it advances toward national recycling targets and integrates sophisticated digital waste tracking systems. The U.S. stands as the largest and most mature market for waste management globally. This dominant position is underpinned by a highly developed infrastructure, strict environmental regulations, and a large population that generates substantial waste volumes. The market status in the region is characterized by a mix of private and public sector involvement, with major corporations providing services to municipalities and industrial clients. A primary driving factor for this leadership is the comprehensive regulatory framework established by the Environmental Protection Agency, which mandates safe disposal and promotes recycling. According to the U.S. Environmental Protection Agency, the nation generates approximately 292 million tons of municipal solid waste annually, creating a vast addressable market for waste management services. Furthermore, the high level of urbanization, with over 80% of the population living in cities, necessitates efficient and organized waste collection systems. Data from the Census Bureau shows that the U.S. population continues to grow, driving consistent demand for waste services across expanding metropolitan areas. The presence of leading waste management companies fosters continuous innovation in recycling technologies and waste-to-energy solutions. As per the Department of Energy, the waste-to-energy market is projected to reach $43.85 billion by 2026, as states implement stricter landfill diversion mandates. Additionally, the widespread adoption of single-stream recycling has simplified participation for residents, increasing capture rates. These structural and behavioral factors solidify the U.S. as the central hub for waste management innovation and market activity in the region.

COMPETITIVE LANDSCAPE

The competition in the U.S. waste management market is intense and characterized by a mix of large national corporations and numerous local independent operators. Major players compete based on service reliability, price efficiency,y and environmental sustainability. National firms leverage their scale to offer comprehensive solutions, ns including recycling and waste-to-energy services. Local operators often differentiate themselves through personalized customer service and flexibility in niche markets. The high capital requirements for infrastructure, such as landfills and transfer stations,s create significant barriers to entry, thereby protecting established players. Various regulatory pressures regarding emissions and recycling mandates force all participants to invest continuously in technology and compliance. Price competition remains fierce in dense urban areas where multiple providers vie for municipal contracts. Strategic acquisitions are common as companies seek to consolidate fragmented markets and expand their geographic reach. The shift toward circular economy principles also drives competition in recycling innovation and resource recovery. Ultimately, tely's success depends on the ability to balance operational efficiency with sustainable practices while maintaining strong community relationships and regulatory compliance in a highly scrutinized industry.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. waste management market include

- Waste Management, Inc.

- Republic Services, Inc.

- Waste Connections, Inc.

- Clean Harbors, Inc.

- Casella Waste Systems, Inc.

- GFL Environmental Inc.

- Stericycle, Inc.

- Recology Inc.

- Advanced Disposal Services, Inc.

- Covanta Holding Corporation

- Veolia North America

- FCC Environmental Services

TOP LEADING PLAYERS IN THE MARKET

- Waste Management Inc is the largest provider of comprehensive waste management and environmental services in North America. The company serves residential, commercial, industrial i, al and municipal customers throughout the ... Recent actions to strengthen its market position include significant investments in renewable natural gas projects, ts which convert landfill methane into clean energy. Waste Management has also expanded its recycling capabilities by upgrading material recovery facilities with advanced sorting technology. The company focuses on sustainability initiatives such as increasing landfill diversion rates and reducing carbon emissions. By leveraging its extensive network of landfills and transfer stations, Ons Waste Management ensures efficient service delivery. These strategic moves enhance operational efficiency and reinforce its leadership in the evolving waste management landscape while meeting growing environmental standards.

- Republic Services Inc is a leading provider of non-hazardous solid waste collection, transfer, recycling,g and disposal services. The company operates a vast network of collection companies,ompanies transfer stations, material recovery facilities, and landfills across the U.S.. Recent actions to strengthen its market position include the acquisition of smaller regional waste haulers to expand its geographic footprint. Republic Services has also invested heavily in automation and digital tools to optimize collection routes and improve customer experience. The company prioritizes sustainability by developing solar farms on closed landfills and enhancing recycling programs. These initiatives reduce environmental impact and create new revenue streams. By focusing on operational excellence and sustainable practices, Republic Services maintains a strong competitive position and delivers consistent value to shareholders and communities.

- Advanced Disposal Services Inc provides solid waste collection and disposal services primarily in the United States. The company offers a range o,f services including residential curbside collection commercial wast,e commercial waste management, and landfill operations. Recent actions to strengthen its market position include the integration of advanced routing software to increase efficiency and reduce fuel consumption. Advanced Disposal has also focused on expanding its recycling and organics processing capabilities to meet regulatory demands. The company emphasizes customer service by offering flexible billing options and responsive support. By investing in modern fleet technology and sustainable waste solutions,s Advanced Disposal enhances its operational reliability. These efforts help the company compete effectively in a fragmented market and drive growth through improved service quality and environmental stewardship.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the U.S. waste management market primarily employ consolidation and technological innovation to maintain competitive advantages. Companies actively acquire smaller regional providers to expand their service territories and achieve economies of scale. This strategy increases market density and reduces operational costs per unit. Firms also invest heavily in automation and digital platforms to optimize collection routes and enhance customer engagement. Sustainability initiatives such as renewable energy generation from landfill gas and advanced recycling technologies are central to long-term growth. These efforts align with regulatory requirements and consumer expectations for environmental responsibility. Additionally, companies focus on diversifying revenue streams by expanding into specialized waste streams like construction debris and organic materials. These multifaceted strategies enable participants to navigate regulatory complexities and sustain profitability in a mature industry.

MARKET SEGMENTATION

This research report on the U.S. waste management market is segmented and sub-segmented into the following categories.

By Waste Type

- Municipal Solid Waste

- Industrial Waste

- Hazardous Waste

- E-Waste

- Construction & Demolition Waste

- Biomedical Waste

By Service

- Collection

- Transportation

- Disposal

- Recycling

- Waste-to-Energy

- Muncipal

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com