U.S. Coffee Market Size, Share, Trends, and Growth Analysis Report, Segmented By Product Type (Whole Bean, Ground Coffee, Instant Coffee, Coffee Pods, Capsules), Packaging Type, Distribution Channel & Region (New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado), Industry Forecast From 2026 to 2034

U.S. Coffee Market Size

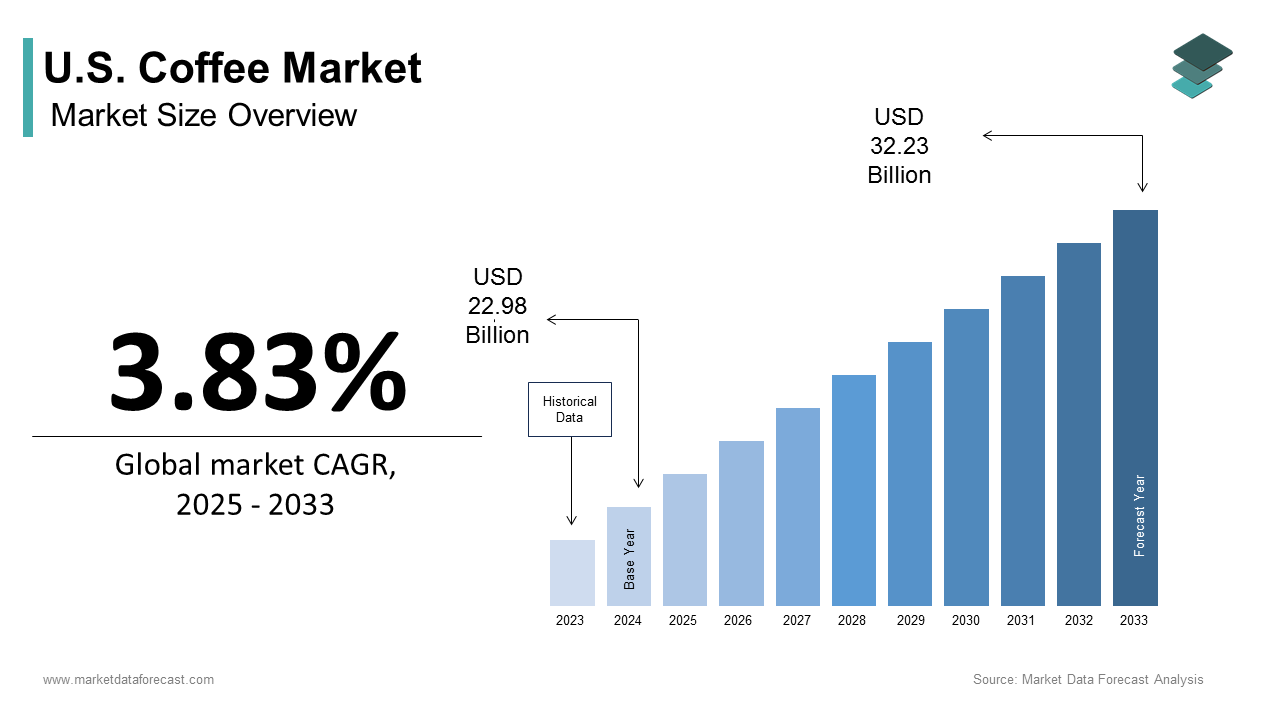

The U.S. coffee market size was valued at USD 23.86 billion in 2025 and is anticipated to reach USD 24.77 billion in 2026 and USD 33.46 billion by 2034, growing at a CAGR of 3.83% during the forecast period from 2026 to 2034.

The coffee is a cultural infrastructure, woven into the rhythms of work, social ritual, and identity formation across generations. According to the National Coffee Association, 65% of Americans drink coffee daily, consuming an average of 3.1 cups per day, equivalent to over 400 million cups served nationwide every single day. Specialty coffee now accounts for nearly half of all retail sales, with consumers willing to pay premiums for single-origin beans, direct-trade certifications, and transparent roasting profiles.

MARKET DRIVERS

Labor Shortages and the Rise of Coffee as a Workplace Necessity

The coffee has become a non-negotiable anchor in the modern workplace, not for productivity alone, but as a psychological and social tether, which is driving the growth of the US coffee market. According to the Society for Human Resource Management, 78% of U.S. employers now provide free or subsidized coffee in the office, citing its role in employee retention, morale, and informal collaboration. Simultaneously, labor shortages in hospitality have intensified reliance on coffee as a low-touch, high-impact amenity.

Climate Anxiety and Consumer Demand for Ethical Sourcing

The climate volatility in key producing regions has shifted coffee from a commodity to a cause is compelling consumers to align purchases with environmental and social values, which is enhancing the growth of the US coffee market. A 2023 consumer survey by McKinsey revealed that 67% of millennials and Gen Z buyers would pay up to 40% more for coffee labeled “climate-resilient” or “farmer-paid-a-living-wage.” Brands like Counter Culture and Stumptown now publish real-time farm-level data via blockchain, which is showing rainfall patterns, harvest dates, and income distribution to individual cooperatives.

MARKET RESTRAINTS

Supply Chain Fragility and Climate-Driven Production Volatility

The supply chain remains perilously exposed to climatic shocks in origin countries, where extreme weather events have disrupted harvest cycles with increasing frequency, which is impeding the growth of the US coffee market. Meanwhile, political instability in Colombia and fungal outbreaks like coffee leaf rust (Hemileia vastatrix) have further strained production, where USDA estimates show that 22% of global coffee farms suffered yield losses exceeding 30% between 2020 and 2023. These disruptions cascade through U.S. roasteries, many of which operate on thin margins and lack long-term futures contracts.

Regulatory Pressure on Single-Use Packaging and Waste Disposal

The environmental scrutiny has turned the coffee industry’s most convenient formats into liabilities is also hindering the growth of the US coffee market. Over 16 billion disposable coffee cups are used annually in the U.S., fewer than 1% of which are recycled due to polyethylene linings. Cities including San Francisco, Seattle, and New York have enacted bans on non-compostable cups, mandating compostable materials or reusable systems with penalties reaching $1,000 per violation.

MARKET OPPORTUNITIES

Fermented and Functional Coffee Beverages as Next-Generation Wellness Products

Coffee is evolving beyond stimulation into bioactive wellness, with fermented, probiotic-infused, and adaptogen-blended beverages emerging as high-margin categories, which is expected to bolster the growth of the US coffee market. Companies like Kombucha Coffee Co. and Houndstooth Roasters now produce cold-brew coffees inoculated with Lactobacillus strains by enhancing digestibility and gut health benefits. Adaptogens such as lion’s mane mushroom, reishi, and ashwagandha are being infused into espresso shots to mitigate stress and enhance cognitive clarity, targeting professionals seeking alternatives to stimulant-heavy energy drinks. These products command premium pricing ($8–$12 per 12 oz), bypassing traditional coffee’s commoditized pricing structure.

Domestic Roasting and Regional Bean Cultivation Initiatives

A quiet revolution is underway in domestic cultivation and processing, which is additionally to enhance the growth of the US coffee market. Hawaii’s Kona region has long been a niche player, but new experimental farms in California, Florida, and Puerto Rico are testing heat-tolerant Arabica varieties bred by the USDA’s Agricultural Research Service under its “Climate-Resilient Coffee Project.” The USDA has allocated $18 million in grants since 2022 to expand these initiatives, aiming to reduce import dependency and create rural economic anchors.

MARKET CHALLENGES

Generational Shifts in Consumption Habits Among Younger Demographics

The younger cohorts are moving away from traditional coffee rituals, which is quite a challenging factor for the growth of the US coffee market. According to the Pew Research Center, only 51% of Gen Z adults drink coffee daily, down from 68% among Millennials at the same age and significantly below the 74% rate among Baby Boomers. Many cite health concerns around acidity, jitteriness, or sleep disruption, while others prefer tea, sparkling water, or adaptogenic tonics.

Wage Inflation and the Unsustainable Economics of Labor-Intensive Craft Preparation

The artisanal coffee model depends on skilled baristas, precise equipment, and time-intensive preparation, all of which are becoming financially untenable is likely to degrade the growth of the US coffee market. The median wage for baristas rose 38% between 2020 and 2023, per the Bureau of Labor Statistics, yet retail prices have not kept pace: the average price of a specialty latte increased by only 12% over the same period. The result is a paradox: the more consumers value quality, the harder it becomes for those delivering it to survive.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.83% |

| Segments Covered | By Product Type, Packaging Type, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado |

| Market Leaders Profiled | Starbucks Corporation, The J.M. Smucker Company, Keurig Dr Pepper Inc., Nestlé USA, Peet’s Coffee, Dunkin’ Brands, Lavazza North America, Caribou Coffee Company, Community Coffee Company, Eight O’Clock Coffee Company, Kraft Heinz Company, Death Wish Coffee Company, Intelligentsia Coffee. |

SEGMENTAL ANALYSIS

By Product Type Insights

The ground coffee segment was the largest and held 52.3% of the US coffee market share in 2025, with its balance of convenience, affordability, and familiarity by offering a middle ground between the ritual of whole bean grinding and the simplicity of single-serve pods. A 2023 survey by YouGov, 41% of Americans cite “ease of use” as their primary reason for choosing ground coffee over other forms, while 37% value its lower per-ounce cost compared to pods or specialty beans. Major retailers like Costco, Walmart, and Kroger drive volume through private-label offerings priced 20–30% below branded alternatives.

The Coffee Pods and Capsules segment is growing lucratively with an expected CAGR of 9.8% during the forecast period, with the integration of premiumization and personalization into single-serve formats. The rise of subscription models, where consumers receive curated weekly rotations of roast profiles, has turned pod consumption into a discovery experience by appealing to younger, tech-savvy buyers who seek variety without complexity.

By Packaging Type Insights

The rigid packaging segment was the largest and held 61.2% of the US coffee market share in 2025. Over 78% of specialty coffee sold in the U.S. uses rigid packaging with one-way degassing valves, a feature developed by industry pioneers like Stumptown and Peet’s to extend freshness beyond six weeks, as validated by sensor-based shelf-life testing from the Institute of Food Technologists. Retailers such as Whole Foods and Trader Joe’s mandate rigid packaging for their premium lines because it signals quality, durability, and resealability attributes consumers associate with authenticity. Moreover, rigid packaging enables branding through tactile design, embossing, and color differentiation, which are essential for differentiation in crowded shelves.

The single-serve segment is projected to expand at a CAGR of 13.2% during the forecast period with the proliferation of non-pod, portable formats designed for on-the-go consumption: stand-up pouches with resealable zippers, vacuum-sealed sachets for travel, and multi-serving foil-lined bags optimized for cold brew concentrate or instant coffee powder. Additionally, flexible packaging supports innovative product formats such as nitrogen-infused coffee shots and powdered mushroom lattes, products incompatible with rigid containers.

By Distribution Channel Insights

The Off-Trade Channel segment was the largest by capturing a significant share of the US coffee market in 2025. Amazon alone accounts for 28% of all online coffee purchases, with subscription services driving repeat loyalty. E-commerce growth, accelerated by pandemic-era habits, now contributes $5.2 billion annually in coffee sales, with subscription boxes delivering curated beans directly to doorsteps. The off-trade channel’s scale, reach, and integration with loyalty programs make it the indispensable backbone of coffee consumption, where routine meets accessibility, and flavor is commodified at scale.

The On-Trade Channel segment is anticipated to witness a CAGR of 11.5% during the forecast period, with the resurgence of experiential consumption and the transformation of cafés from service points into community hubs. Independent cafés, which grew by 14% between 2020 and 2023, are driving innovation through third-wave aesthetics, barista-led education, and seasonal micro-lot releases. Meanwhile, hybrid models of coffee shops inside bookstores, co-working spaces, and pharmacies are expanding footprints in urban and suburban corridors where consumers seek “third places” beyond home and office.

REGIONAL ANALYSIS

California Market Analysis

California was the top performer of the US coffee market with a 17.6% share in 2025. The state leads in single-origin sourcing, with 89% of its coffee retailers offering traceable farm-to-cup narratives, and hosts the highest density of certified Q-graders, professional coffee tasters per capita in the country. California’s progressive regulatory environment also shapes national standards was the first state to mandate disclosure of added sugars in flavored coffee syrups and to ban single-use coffee lids statewide.

New York Market Analysis

New York was positioned second by capturing 13.3% of the US coffee market share in 2025. New Yorkers consume an average of 4.3 cups per day, the highest in the nation, according to a Columbia University behavioral study, which often involves drinking multiple varieties across work, commute, and social settings. New York also leads in artisanal craftsmanship: iconic institutions like Irving Farm and Café Grumpy maintain rigorous sourcing standards and train baristas in advanced extraction techniques that influence global trends.

KEY MARKET PLAYERS

A few of the dominating players in the U.S. Coffee Market include

- Starbucks Corporation

- The J.M. Smucker Company

- Keurig Dr Pepper Inc.

- Nestlé USA

- Peet’s Coffee

- Dunkin’ Brands

- Lavazza North America

- Caribou Coffee Company

- Community Coffee Company

- Eight O’Clock Coffee Company

- Kraft Heinz Company

- Death Wish Coffee Company

- Intelligentsia Coffee

MARKET SEGMENTATION

This research report on the U.S. coffee market is segmented and sub-segmented into the following categories.

By Product Type

- Whole Bean

- Ground Coffee

- Instant Coffee

- Coffee Pods

- Capsules

By Packaging Type

- Flexible

- Rigid

- Single-Serve

By Distribution Channel Insights

- On-Trade

- Off-Trade Channel

By Region

- New York

- Massachusetts

- Pennsylvania

- Illinois

- Ohio

- Michigan

- Texas

- Florida

- Georgia

- California

- Washington

- Colorado

Frequently Asked Questions

1. What are the main factors driving the U.S. coffee market?

Key drivers include the rise of specialty coffee, growth in ready-to-drink (RTD) coffee, increased home brewing, and a strong café culture across urban areas.

2. Which coffee segment is the most popular in the U.S.?

Brewed coffee remains the most consumed type, while cold brew and RTD coffee are experiencing rapid growth, especially among younger consumers.

3. Who are the major players in the U.S. coffee market?

Leading companies include Starbucks Corporation, The J.M. Smucker Company, Keurig Dr Pepper Inc., Nestlé USA, and Dunkin’ Brands.

4. What are the latest trends shaping the coffee market in the U.S.?

Major trends include rising cold brew and nitro coffee consumption, growth in plant-based and functional coffee, and increasing focus on sustainability and ethical sourcing

5. How is e-commerce impacting coffee sales in the U.S.?

E-commerce enables direct-to-consumer sales, subscription-based deliveries, and access to premium and international coffee brands, significantly boosting sales volume.

6. What are the key distribution channels for coffee in the U.S.?

Major channels include supermarkets, coffee shops and cafés, online platforms, convenience stores, and specialty roasters.

7. How are health and wellness trends influencing coffee consumption?

Consumers are opting for low-sugar, plant-based, and functional coffee products with added ingredients like collagen, protein, or adaptogens.

8. How do seasonal trends affect coffee sales in the U.S.?

Coffee consumption increases during colder months, but cold brew and iced coffee maintain strong sales even in warmer seasons, showing year-round demand.

9. What role does innovation play in the coffee industry?

Innovation drives new product launches like RTD coffee cans, single-serve pods, sustainable packaging, and functional blends that cater to changing consumer preferences.

10. What is the growth outlook for the U.S. coffee market?

The market is expected to grow at a CAGR of around 4–5% in the coming years, driven by specialty coffee trends, RTD innovation, and strong cafe culture.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com