US Cold storage Market Research Report Segmented By Temperature Type (Chilled, Frozen), Application (Fruits & vegetables, Dairy, Fish, meat & seafood & Pharmaceuticals), Warehouse Type (Private & semi-private), & Country Analysis on Size, Value, Growth, Trends, Forecast Research Report 2026 to 2034

Market Size, 2025

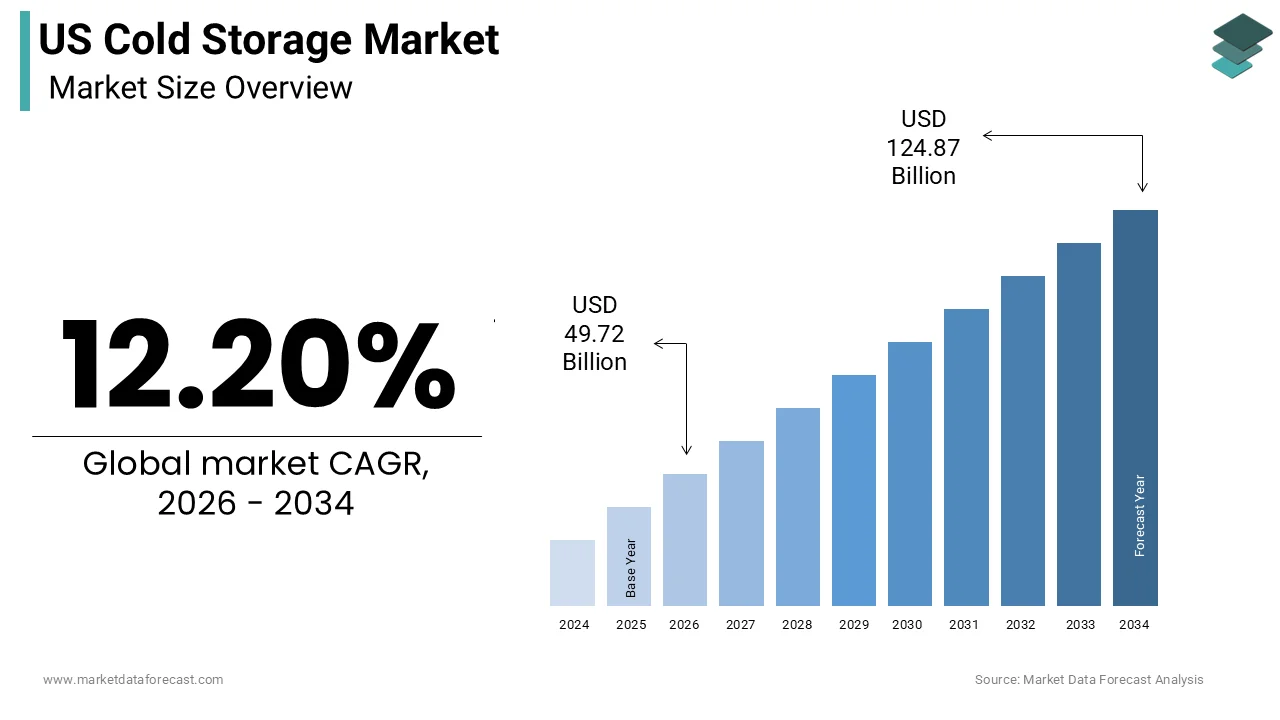

$44.31 BnMarket Estimate, 2026

$49.72 BnMarket Forecast, 2034

$124.87 BnCAGR, 2026–2034

12.20%Executive Summary: US Cold Storage Market

- Market Scope: Comprehensive market analysis covering construction types, temperature segments, application channels, regional leadership frameworks, and temperature-controlled logistics metrics for the US cold storage sector.

- Market Valuation: Valued at USD 44.31 billion (2025), estimated at USD 49.72 billion (2026), and projected to reach USD 124.87 billion by 2034, registering a robust CAGR of 12.20% (2026–2034).

- Primary Growth Drivers: Rapid e-commerce grocery expansion, last-mile delivery networks, surging demand for pharmaceutical/biologics cold storage, automation investments, and sustainable energy practices. Market challenges include high energy costs and infrastructure expenses, while opportunities lie in production store integration, chilled storage expansion, and specialized biopharmaceutical distribution.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment Position | Fastest-Growing Segment |

|---|---|---|

| By Construction / Temperature | Bulk storage facilities (held 39.5% share in 2025) & Frozen storage (led with 61.4% share in 2025) | Production stores (highest CAGR of 8.5%) & Chilled storage (fastest CAGR of 9.2% for fresh perishables/pharma) |

| By Application / Region | Processed foods (occupied 24.1% share in 2025) & United States (dominates North America with 85.7% share) | Pharmaceuticals application (fastest CAGR of 10.5% driven by biologics and vaccine distribution) |

Major Market Players & Market Structure

Market Structure: Highly competitive US cold chain logistics landscape centering on advanced cooling technologies, facility modernization, strategic acquisitions, automated tracking systems, and specialized blast freezing capabilities.

Key Companies: Americold Logistics, LLC (Americold Realty Trust), Lineage Logistics Holdings LLC, AGRO Merchants Group North America, Burris Logistics, Cloverleaf Cold Storage, Henningsen, Nordic Logistics LLC, Preferred Freezer Services, Wabash National, and United States Cold Storage Inc.

US Cold Storage Market Size

The US Cold Storage Market size was calculated to be USD 44.31 billion in 2025 and is anticipated to be worth USD 124.87 billion by 2034, from USD 49.72 billion in 2026, growing at a CAGR of 12.20% during the forecast period.

Cold storage refers to a specialized, temperature- and humidity-controlled facility used to preserve perishable goods. This market is critical for the integrity of the food supply chain, pharmaceutical distribution, and chemical storage, ensuring that products remain safe and effective from production to consumption. The definition extends beyond simple refrigeration to include advanced monitoring systems, automated handling, and energy-efficient technologies that minimize spoilage and waste. As per the United Nations Environment Programme (UNEP) and the FAO, approximately 12% of all food produced globally is lost directly due to a lack of effective refrigeration, highlighting the vital role of robust cold chain storage solutions. In the United States, the Food and Drug Administration mandates strict temperature controls for pharmaceuticals and biologics, driving investment in compliant facilities. The Centers for Disease Control and Prevention (CDC) mandates "chilling" food promptly at 40°F or below as a core safety pillar to mitigate foodborne pathogens, which collectively cause an estimated 48 million illnesses in the United States every year. The market is characterized by a shift toward multi-temperature zones and blast freezing capabilities to accommodate diverse product requirements. Increasing urbanization and the rise of e-commerce grocery shopping have further amplified the need for strategically located distribution centers. The integration of Internet of Things sensors allows for real-time tracking of temperature fluctuations, ensuring accountability and quality assurance. This technological evolution transforms cold storage from a passive utility into an active component of supply chain resiliency,e supporting both economic efficiency and consumer safety in a rapidly changing logistical landscape.

MARKET DRIVERS

Expansion of E-Commerce Grocery and Last Mile Delivery

The rapid expansion of e-commerce grocery shopping and the demand for efficient last-mile delivery are primary drivers for the United States cold storage market. Consumers increasingly prefer the convenience of online ordering and home delivery for fresh and frozen foods, necessitating a robust network of temperature-controlled fulfillment centers. As per the United States Census Bureau, total e-commerce sales have seen sustained expansion, growing by roughly 9.4% year-over-year by the end of 2024 to account for over 16% of all domestic retail sales, anchoring a permanent shift toward digital grocery and last-mile logistics. This trend requires cold storage facilities to be located closer to urban centers to facilitate quick delivery times while maintaining product integrity. Traditional warehouses are being retrofitted or replaced with modern facilities equipped with automated sorting systems and multiple temperature zones to handle varied inventory. The complexity of managing small individual orders rather than bulk shipments increases the need for precise inventory control and rapid turnover. Retailers are investing heavily in cold chain infrastructure to reduce delivery windows and enhance customer satisfaction. The ability to offer same-day or next-day delivery for perishable items has become a competitive differentiator in the retail sector. This driver stimulates the construction of new facilities and upgrades to existing ones, ensuring that the cold storage network can support the high volume and speed required by modern consumers. The integration of cold storage with last-mile logistics creates a seamless flow of goods, reducing spoilage and improving overall supply chain efficiency.

Growth in Pharmaceutical and Biologics Distribution

The growing demand for temperature-controlled storage of pharmaceuticals and biologics is propelling the growth of the United States cold storage market. The development of complex drugs, vaccines, and gene therapies requires stringent temperature management to maintain efficacy and safety. According to the Food and Drug Administration (FDA) approval data, biological therapies and advanced therapeutics continue to experience a sustained surge, consistently making up over 25% of all newly approved molecular entities annually and generating high demand for specialized cold storage infrastructure. Many of these products require ultra-low temperature storage ranging from minus 20 degrees Celsius to minus 80 degrees Celsius, which standard refrigeration cannot provide. The distribution of vaccines, particularly those for infectious diseases, necessitates a reliable cold chain to prevent degradation during transport and storage. Healthcare providers and distributors are investing in compliant facilities that meet Good Distribution Practice standards to ensure regulatory adherence. The rise of personalized medicine and clinical trials further amplifies the need for flexible and secure storage options. Pharmaceutical companies prioritize partners who can offer validated temperature monitoring and emergency backup systems to mitigate risks. This driver ensures steady growth in the healthcare segment of the cold storage market as the industry continues to innovate and expand its portfolio of temperature-sensitive treatments. The critical nature of these products makes reliability and precision paramount, driving continuous improvement in storage technologies and protocols.

MARKET RESTRAINTS

High Energy Consumption and Operational Costs

High energy consumption and associated operational costs are a major restraint for the United States cold storage market. Refrigeration systems require continuous power to maintain low temperatures, resulting in significant electricity usage and expense. As per the U.S. Energy Information Administration (EIA) and industry energy tracking, commercial refrigeration is highly energy-intensive, accounting for roughly 50% of total electricity consumption in supermarkets and up to 70% to 80% of total electrical loads in cold storage warehouses. Fluctuating energy prices directly impact profitability, forcing operators to pass costs onto customers or reduce margins. The need for redundant systems to prevent spoilage during power outages further increases capital and maintenance expenditures. Older facilities with inefficient insulation and outdated compressors are particularly vulnerable to high energy bills, making retrofitting a financial burden. Small and medium-sized operators often struggle to compete with larger players who can leverage economies of scale to negotiate better energy rates. The pressure to reduce carbon footprints adds another layer of complexity as companies invest in renewable energy sources or energy-efficient technologies, which require substantial upfront investment. These financial constraints can limit expansion plans and slow the adoption of advanced technologies. High operational costs will remain a persistent barrier to growth and profitability in the cold storage industry. This will continue to be the case until more cost-effective and sustainable cooling solutions become widely available.

Regulatory Compliance and Safety Standards

Strict regulatory compliance and safety standards are a significant hindrance to the United States cold storage market. This imposes rigorous requirements on facility design and operation. Agencies such as the Food and Drug Administration and the United States Department of Agriculture enforce detailed guidelines for temperature monitoring, sanitation, and pest control. As per the Food Safety Modernization Act, facilities must implement comprehensive preventive controls and maintain detailed records of temperature logs and handling procedures. Non-compliance can result in severe penalties, product recalls, and reputational damage. The complexity of these regulations varies by product type and jurisdiction, requiring operators to navigate an intricate legal landscape. Regular audits and inspections demand significant administrative resources and staff training. The need for validated equipment and calibrated sensors adds to capital expenses. Smaller operators may lack the expertise or financial capacity to meet these stringent standards, limiting their market participation. The constant evolution of regulations requires continuous adaptation and investment in compliance programs. This regulatory burden increases operational complexity and costs, potentially discouraging new entrants and slowing innovation. The fear of non-compliance can lead to conservative business practices hindering the adoption of new technologies or processes that might otherwise improve efficiency. Thus, regulatory rigor acts as a brake on rapid market expansion and flexibility.

MARKET OPPORTUNITIES

Adoption of Automation and Robotics Technology

The adoption of automation and robotics technology offers a substantial opportunity for the United States cold storage market. This enhances efficiency and reduces labor dependency. Automated storage and retrieval systems ASRS and robotic pickers can operate in extreme temperatures where human labor is limited and costly. As per the Association for Advancing Automation (A3), the integration of autonomous mobile robots (AMRs) in warehousing has been shown to reduce operational throughput costs by up to 25% while simultaneously mitigating order error rates and enhancing workplace safety. Cold storage facilities can leverage these technologies to optimize space utilization and accelerate order fulfillment. Automation minimizes exposure to cold environments, improving worker safety and reducing turnover. The integration of artificial intelligence allows for predictive maintenance and optimized energy usage, further lowering operational costs. Companies that invest in smart warehouses can offer faster and more reliable service, attracting high-value clients in retail and pharmaceuticals. The scalability of automated systems enables facilities to handle fluctuating demand without significant increases in staffing. This technological shift also supports the growth of e-commerce by enabling the rapid processing of small orders. The opportunity lies in modernizing existing facilities and designing new ones with automation in mind. Cold storage providers can differentiate themselves by embracing robotics to achieve superior service quality and operational efficiency. Doing so drives long-term competitiveness and growth in a technologically advanced market.

Integration of Renewable Energy and Sustainable Practices

The integration of renewable energy and sustainable practices provides a clear path for the growth of the United States cold storage market. This helps to align with environmental goals and cost reduction strategies. Facilities can install solar panels, wind turbines, and geothermal systems to power refrigeration units, reducing reliance on fossil fuels. The Environmental Protection Agency (EPA) highlights that because commercial and industrial electricity consumption accounts for a massive portion of national greenhouse gases, businesses transitioning to renewable energy can drastically shrink their carbon footprints and bolster corporate social responsibility profiles. Green building certifications such as LEED attract environmentally conscious clients and investors. The use of natural refrigerants with low global warming potential replaces harmful hydrofluorocarbons, complying with emerging regulations. Energy recovery systems capture waste heat from refrigeration processes for use in heating offices or water, providing additional efficiency gains. Sustainable practices also include improved insulation and LED lighting to minimize energy waste. These initiatives not only lower utility bills but also mitigate risks associated with carbon taxes and energy price volatility. Marketing sustainability efforts can strengthen brand reputation and customer loyalty. The opportunity extends to partnerships with utility companies for demand response programs where facilities adjust energy usage during peak times for financial incentives. Cold storage providers should lead in sustainability to become responsible supply chain partners. Consequently, they will capture a growing segment of eco-aware businesses.

MARKET CHALLENGES

Labor Shortages and Workforce Safety Concerns

Labor shortages and workforce safety concerns are significant challenges to the United States cold storage market. This affects operational continuity and efficiency. Workinsub-zero zero environments is physically demanding and poses health risks such as hypothermia and frostbite, leading to high turnover rates. As per the Bureau of Labor Statistics, the warehousing and storage sector faces a persistent labor gap with thousands of unfilled positions nationwide. Attracting and retaining skilled workers for cold storage roles is difficult due to harsh working conditions and competitive job markets. Companies must invest in protective gear, heating breaks, and safety training to protect employees, increasing operational costs. The aging workforce exacerbates the shortage as younger generations seek less physically taxing employment. Automation helps mitigate this issue, but requires skilled technicians for maintenance and operation who are also in short supply. The inability to staff facilities adequately can lead to delays, errors, and increased spoilage rates. Safety incidents can result in lawsuits and regulatory fines, further straining resources. Addressing these challenges requires innovative human resource strategies and investment in ergonomic technologies. The industry must balance automation with human labor to ensure resilience. The cold storage sector will continue to face critical obstacles to growth and service reliability. These workforce issues will only be resolved once working conditions improve and labor pools expand.

Infrastructure Aging and Maintenance Complexities

Aging infrastructure and maintenance complexities are a serious obstacle to the United States cold storage market. This is because many facilities were built decades ago with outdated technology. Older buildings often suffer from poor insulation, inefficient refrigeration systems, and inadequate electrical capacity, leading to higher energy costs and frequent breakdowns. As industrial facilities scale, maintaining aging legacy refrigeration and HVAC systems requires navigating specialized parts shortages and a widening technical talent gap, as modern service technicians are increasingly trained on digital and automated systems rather than obsolete infrastructure. Retrofitting these facilities with modern equipment is costly and disruptive to operations. The risk of temperature excursions due to equipment failure threatens product integrity and client trust. Emergency repairs in cold environments are difficult and expensive, requiring specialized contractors. The lack of real-time monitoring in older systems makes it hard to detect issues before they escalate. Upgrading infrastructure requires significant capital investment, which may be prohibitive for smaller operators. The transition to new refrigerants mandated by environmental regulations further complicates maintenance as older systems are incompatible. These challenges hinder the ability of older facilities to compete with modern automated warehouses. The industry faces a dilemma of either investing heavily in upgrades or risking obsolescence. Managing the lifecycle of aging assets while maintaining service levels is a complex task that requires strategic planning and financial resilience.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 12.20% |

| Segments Covered | By Construction Type, Temperature, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Americold Logistics, LLC, Lineage Logistics Holdings LLC, AGRO Merchants Group North America, Burris Logistics, Cloverleaf Cold Storage, Henningsen, Nordic Logistics LLC, Preferred Freezer Services, and Wabash National |

SEGMENTAL ANALYSIS

By Construction Type Insights

In 2025, the bulk storage facilities segment held the majority share of 39.5% of the United States cold storage market because of its ability to accommodate massive volumes of agricultural produce and retail inventory efficiently. These large-scale warehouses are strategically located near production hubs or major distribution centers, allowing for the consolidation of goods before they enter the supply chain. As per the United States Department of Agriculture (USDA), the country produces hundreds of millions of tons of agricultural products annually, including nearly 400 million tons of grain and corn alone, a significant portion of which demands rapid post-harvest cooling and long-term bulk storage to prevent spoilage and secure the food supply. Bulk storage units provide the necessary cubic footage to handle seasonal surges in commodities such as potatoes, apples,s and frozen vegetables. The economies of scale associated with these facilities lower the cost per pallet for storage, making them attractive to large food processors and retailers. The design of bulk storage allows for high-density stacking and efficient use of vertical space, maximizing storage capacity within a fixed footprint. This segment benefits from long-term contracts with major agribusinesses, ensuring stable revenue streams. The infrastructure supports heavy-duty material handling equipment, facilitating rapid loading and unloading operations. The dominance of this segment is further reinforced by its critical role in national food security, enabling the preservation of harvests for year-round consumption. The ability to store vast quantities of essential goods ensures that bulk storage remains the backbone of the cold chain infrastructure, supporting both domestic consumption and export activities.

Furthermore, the domination of the bulk storage segment is further driven by its strategic positioning near key transportation hubs such as ports, railways, and highways. Proximity to these logistics nodes minimizes transit time and reduces the risk of temperature excursions during transfer. As per the American Association of Port Authorities, maritime ports in the United States handled over 2 billion tons of cargo in 2024, much of which included perishable imports and exports requiring immediate cold storage. Bulk storage facilities located near these entry points serve as critical intermediaries ensuring that imported goods such as seafood, fruits, and meats are stored under optimal conditions before distribution. This location advantage facilitates seamless intermodal transfers, reducing handling costs and improving supply chain efficiency. Retailers and distributors prefer these facilities because they offer quick access to major markets, enabling faster replenishment of store shelves. The integration of bulk storage with transportation networks supports just-in-time inventory models, which are essential for modern retail operations. The concentration of these facilities in logistics clusters creates synergies with other supply chain services such as customs clearance and packaging. This logistical connectivity enhances the value proposition of bulk storage, making it indispensable for international trade and domestic distribution. The strategic alignment with transportation infrastructure ensures that this segment continues to lead the market by providing reliable and efficient storage solutions for high-volume goods.

But the production stores segment is predicted to witness the highest CAGR of 8.5% from 2026 to 2034 due to the increasing integration of storage capabilities directly within manufacturing and processing facilities. Companies are adopting this model to streamline operations, reduce handling time,s and maintain product quality from production to storage. Driven by strict regulatory standards and risk mitigation, a growing number of food manufacturers are investing heavily in on-site production store infrastructure to drastically minimize the transit distance products travel immediately after processing, reducing contamination risks and temperature fluctuations. This vertical integration allows for better control over inventory management and production scheduling. Production stores enable manufacturers to hold finished goods until they are ready for shipment, optimizing warehouse space and reducing reliance on third-party logistics providers. The trend toward automation in processing plants extends to storage areas where automated guided vehicles and robotic systems manage inventory with precision. This synergy between production and storage enhances operational efficiency and reduces labor costs. The ability to monitor product quality in real time from the production line to the storage unit ensures compliance with safety standards. This segment grows as more companies recognize the benefits of consolidating operations to improve supply chain resilience. The reduction in transit time and handling steps leads to lower energy consumption and carbon emissions, aligning with sustainability goals. The shift toward integrated production stores reflects a broader industry move toward efficiency and quality control.

In addition, the rapid expansion of the production stores segment is also fueled by the growing demand for just-in-time inventory management practices in the food and beverage industry. Manufacturers seek to minimize inventory holding costs while ensuring timely delivery to customers. According to lean logistics frameworks recognized by the Council of Supply Chain Management Professionals (CSCMP), major food producers balance just-in-time (JIT) strategies with strategic cold storage indexing to enhance supply chain flexibility, buffer against raw material volatility, and optimize shelf life. Production stores facilitate this approach by providing immediate storage capacity adjacent to processing lines, allowing for quick retrieval and shipment. This proximity enables manufacturers to respond rapidly to changes in demand without maintaining excessive stock levels. The reduced need for long-distance transportation from separate warehouses lowers logistics costs and environmental impact. Production stores support customized order fulfillment, allowing manufacturers to package and ship products according to specific customer requirements quickly. The integration of advanced software systems enables real-time tracking of inventory levels and production status, enhancing decision-making. This agility is crucial in a market characterized by fluctuating consumer preferences and short product life cycles. The ability to maintain lean inventory while ensuring product availability drives the adoption of production stores. This segment offers a competitive advantage by improving responsiveness and reducing operational inefficiencies. The trend toward localized and integrated storage solutions ensures sustained growth for production stores in the coming years.

By Temperature Insights

The frozen storage segment remained in the lead in the United States cold storage market by capturing a 61.4% share in 2025. Its ability to preserve products for extended periods without significant degradation in quality has contributed to the leading position of this segment. Freezing inhibits microbial growth and enzymatic activity, ensuring that food items remain safe and nutritious for months or even years. According to retail data tracked by the American Frozen Food Institute (AFFI) and industry partners, the U.S. frozen food market commands over $74 billion in retail sales annually, sustained by a permanent consumer shift toward convenient, portion-controlled, and long-lasting meal options. This segment accommodates a wide range of products, including meat, seafood, vegetables, and prepared meals. The stability of frozen goods allows for efficient inventory management and reduces the frequency of restocking. Retailers and food service providers rely on frozen storage to maintain consistent supply levels regardless of seasonal variations in production. The ability to store large quantities of frozen products supports bulk purchasing and cost savings. Frozen storage facilities are designed to maintain temperatures below-188 degrees Celsius, ensuring product integrity. The widespread acceptance of frozen foods as a convenient and healthy option drives the continued dominance of this segment. The infrastructure for frozen storage is well established, with specialized equipment and expertise widely available. The reliability of frozen preservation makes it the preferred choice for many supply chain participants seeking to minimize waste and maximize shelf life.

Moreover, the top position of this segment is further supported by the strong consumer preference for convenience foods that require minimal preparation time. Modern lifestyles, characterized by busy schedules and dual-income households, have increased the demand for ready-to-eat and easy-to-prepare meals. Frozen storage enables the distribution of these products across vast geographic areas, ensuring availability in remote and urban markets alike. The variety of frozen options has expanded to include gourmet meals, organic ingredients, and ethnic cuisines appealing to diverse tastes. Retailers dedicate significant shelf space to frozen categories, recognizing their high turnover rates and profit margins. The consistency in quality and taste of frozen products builds consumer trust and loyalty. The ability to portion control and reduce food waste at home also appeals to environmentally conscious shoppers. Frozen storage supports the innovation of new product formats such as air-fried snacks and plant-based alternatives. The enduring popularity of convenience foods ensures that frozen storage remains a critical component of the cold chain. The segment benefits from continuous product development and marketing efforts that highlight the benefits of frozen nutrition.

However, the chilled storage segment is estimated to register the fastest CAGR of 9.2% during the forecast period, owing to the rising consumer demand for fresh and perishable goods. Shoppers are increasingly prioritizing fresh fruits, vegetables, dairy, and meat over processed alternatives, seeking higher nutritional value and better taste. Chilled storage maintains temperatures between 0 and 4 degrees Celsius, preserving the freshness and texture of sensitive products. This segment supports the farm-to-table movement and the growth of organic food markets, which rely on rapid distribution to maintain quality. The short shelf life of chilled products requires efficient logistics and precise temperature control, driving investment in advanced refrigeration technologies. Retailers are expanding their fresh food sections to meet consumer expectations, increasing the need for chilled warehousing. The growth of meal kit services and fresh food delivery platforms further amplifies demand for chilled storage. These services require dedicated facilities to handle high volumes of perishable ingredients with strict temperature requirements. The ability to deliver fresh products quickly and safely is a key competitive advantage. The trend toward healthier eating habits ensures sustained growth for chilled storage. The segment benefits from innovations in packaging and monitoring that extend shelf life and reduce spoilage.

Furthermore, the swift expansion of this segment is also driven by the expansion of pharmaceutical cold chain requirements for vaccines, biologics, and medications. Many medical products require strict temperature control within the chilled range to maintain efficacy and safety. Healthcare providers and distributors invest in specialized chilled warehouses equipped with redundant cooling systems and real-time monitoring to prevent deviations. The distribution of insulin, antibiotics, and certain cancer treatments relies heavily on chilled logistics. Regulatory standards such as Good Distribution Practice mandate rigorous documentation and validation of storage conditions. The complexity of pharmaceutical supply chains requires dedicated chilled storage areas separate from food products to prevent cross-contamination. The growth of personalized medicine and clinical trials further increases the need for flexible and secure chilled storage solutions. Pharmaceutical companies prioritize partners who can offer validated environments and emergency response protocols. This driver ensures steady growth in the healthcare segment of chilled storage. The critical nature of these products makes reliability paramount. The integration of advanced tracking technologies enhances visibility and accountability. The expansion of the pharmaceutical sector ensures that chilled storage remains a high-growth area.

By Application Insights

The processed foods segment was the largest and occupied a 24.1% share of the United States cold storage market in 2025. Factors such as the high-volume consumption of packaged meals and ready-to-eat products have supported the prominence of this segment. This category includes frozen dinners, pizzas, appetizers, and desserts that require consistent temperature control to maintain quality and safety. As per the Consumer Brands Association, processed food sales account for a significant portion of household grocery expenditure,s with frozen items representing a large share. The convenience and affordability of processed foods appeal to a broad demographic, driving steady demand for cold storage services. Manufacturers produce these items in large batches, requiring substantial storage capacity before distribution. The standardized nature of processed foods allows for efficient stacking and handling in warehouses. Retailers rely on a consistent supply of these products to meet consumer demand. The long shelf life of frozen processed foods reduces the risk of spoilage and waste. The segment benefits from established distribution networks and brand loyalty. The ability to store large volumes of processed foods supports promotional campaigns and seasonal peaks. The dominance of this segment is reinforced by the continuous innovation in product formulations and packaging. The integration of processed foods into daily diets ensures that cold storage remains essential. The segment supports the efficiency of the overall food supply chain.

Moreover, the spearheading of the processed foods segment is further driven by the efficiency it brings to supply chain management. Standardized packaging and predictable demand patterns allow for optimized inventory control and logistics planning. According to modern supply chain analytics and IoT validation metrics, implementing optimized thermal management and automated monitoring architectures systematically reduces operational throughput costs and cold-chain energy waste by 15% to 30% for commercial food distributors. The ability to forecast demand accurately enables better utilization of storage space and transportation resources. Processed foods often have longer lead times, allowing for smoother coordination between production and distribution. The use of automated systems in processing and storage facilities enhances throughput and reduces labor requirements. The consistency in product dimensions facilitates high-density storage, maximizing warehouse capacity. The segment benefits from economies of scale in transportation and handling. The reliability of processed food supply chains supports retail operations and customer satisfaction. The integration of technology, such as radio frequency identification tags, improves tracking and visibility. The efficiency gains achieved in this segment drive its continued leadership. The ability to manage large volumes effectively ensures stability. The segment supports the overall resilience of the food system.

On the other hand, the pharmaceuticals segment is anticipated to witness the fastest CAGR of 10.5% between 2026 and 2034. This quick surge of the segment is fuelled by stringent regulatory compliance and safety standards. The storage of vaccines, biologics, and other temperature-sensitive medications requires precise control and monitoring to ensure efficacy. Healthcare providers and distributors invest heavily in specialized facilities that meet these requirements. The complexity of pharmaceutical supply chains necessitates dedicated storage areas with redundant systems. The risk of product degradation due to temperature excursions is high, making reliability critical. The segment benefits from high-value contracts and long-term partnerships. The growth of biologics and personalized medicine increases the demand for specialized storage. The ability to provide validated environments is a key differentiator. The segment supports the integrity of the healthcare system. The focus on patient safety drives continuous improvement. The regulatory landscape ensures sustained growth. The segment requires high levels of expertise and investment.

In addition, the rapid growth of the pharmaceutical segment is also propelled by the expansion of biologics and vaccine distribution. The development of new treatments for chronic diseases and infectious agents requires robust cold chain infrastructure. As per the Centers for Disease Control and Prevention, the distribution of vaccines has increased significantly in recent years. Biologics often require chilled or frozen storage depending on the formulation. The complexity of these products demands specialized handling and storage conditions. The growth of clinical trials and personalized medicine further amplifies demand. Pharmaceutical companies prioritize partners who can offer secure and compliant storage solutions. The segment benefits from high barriers to entry, limiting competition. The critical nature of these products ensures steady demand. The integration of advanced monitoring technologies enhances visibility. The segment supports innovation in healthcare. The focus on quality and safety drives growth. The expansion of the pharmaceutical sector ensures long-term viability. The segment requires continuous investment in technology and training.

REGIONAL ANALYSIS

The United States dominated the North American cold storage market and accounted for a 85.7% share in 2025. This dominance of the US market was driven by its vast agricultural output, advanced logistics infrastructure, and high consumer demand for perishable goods. The market status is characterized by a mature yet evolving landscape where technological innovation and sustainability drive growth. A key driving factor is the extensive network of highways and railways that facilitates the efficient distribution of temperature-controlled goods across the country. As per the United States Department of Transportation, the nation boasts over 4 million miles of roads and 140000 miles of rail tracks, enabling seamless connectivity between production hubs and consumption centers. A further significant driver is the robust regulatory framework enforced by agencies such as the Food and Drug Administration, which mandates strict temperature controls for food and pharmaceuticals. This regulatory environment ensures high standards of safety and quality, prompting continuous investment in compliant facilities. The presence of major retail chains and e-commerce giants further stimulates demand for cold storage services. The adoption of automation and renewable energy technologies enhances operational efficiency and sustainability. The cultural emphasis on convenience and fresh food supports the growth of both frozen and chilled segments. The combination of infrastructure regulation and consumer trends ensures that the United States remains the largest and most influential market for cold storage in the region, setting standards that influence global practices. The maturity of the market drives continuous innovation and optimization.

COMPETITION OVERVIEW

The competition in the United States cold storage market is intense and characterized by a mix of large real estate investment trusts and specialized logistics providers vying for dominance. Established players leverage extensive networks and capital resources to expand capacity, while smaller firms focus on niche services and regional expertise. Price competition is moderate as service quality and reliability often dictate customer selection. Manufacturers continuously invest in technology to automate operations and improve energy efficiency. The rise of e-commerce has increased demand for faster and more flexible cold chain solutions. This dynamic landscape forces all participants to remain agile and responsive to changing consumer preferences. Collaborations with technology firms help enhance digital capabilities and tracking precision. The constant need for infrastructure upgrades ensures that the market remains vibrant and competitive. Consumers benefit from improved service levels and reduced spoilage rates. The focus on sustainability and innovation drives differentiation among competitors.

Top Strategies Used by Key Market Participants

Key players in the United States cold storage market primarily employ technological integration and strategic expansion to maintain a competitive advantage. Companies frequently invest in automation and robotics to enhance operational efficiency and reduce labor costs. This strategy improves accuracy and speed in handling perishable goods. Expansion through mergers and acquisitions allows firms to broaden their geographic reach and consolidate market presence. Sustainability initiatives such as energy-efficient refrigeration and renewable energy adoption are critical for reducing environmental impact and operational expenses. Digital transformation efforts focus on providing real-time visibility and data analytics to customers. These combined strategies enable participants to address complex supply chain demands and sustain growth in a dynamic industry.

Leading Players in the US Cold Storage Market

- Lineage Logistics stands as a pivotal entity in the United States cold storage market by operating one of the largest networks of temperature-controlled warehouses globally. The company focuses on integrating advanced technology with physical infrastructure to enhance supply chain efficiency and reduce food waste. Recent actions include significant investments in automation technologies such as robotic picking systems and artificial intelligence-driven inventory management. Lineage has expanded its footprint through strategic acquisitions of regional providers to strengthen its national coverage. The company also prioritizes sustainability by implementing energy-efficient refrigeration systems and solar power initiatives. By leveraging data analytics, Lineage optimizes storage utilization and improves customer service levels. Its commitment to innovation and operational excellence ensures it remains a preferred partner for major food producers and retailers seeking reliable and scalable cold chain solutions.

- Americold Realty Trust plays a critical role in the United States cold storage market as a leading owner and operator of independent temperature-controlled warehouses. The company provides essential infrastructure for the food supply chain, serving producers, manufacturers, and retailers across the nation. Recent strategies involve modernizing existing facilities with state-of-the-art cooling technologies and expanding capacity in key logistics hubs. Americold has focused on enhancing its digital platform to offer customers real-time visibility into inventory and shipment status. The trust actively pursues growth through joint ventures and development projects in high-demand markets. By emphasizing customer-centric services and operational reliability, Americold strengthens its competitive position. Its extensive network and financial stability allow for continuous investment in infrastructure improvement,s ensuring consistent performance and adherence to strict safety standards.

- United States Cold Storage Inc contributes significantly to the market by providing comprehensive cold chain logistics services, including storage, transportation, and value-added processing. The company specializes in handling diverse product categories such as seafood, meat, and dairy with precision and care. Recent efforts include upgrading its fleet of refrigerated trucks and implementing advanced tracking systems to ensure product integrity during transit. US Cold Storage has invested in expanding its blast freezing capabilities to meet the growing demand for frozen goods. The company emphasizes regulatory compliance and quality assurance to build trust with healthcare and food industry clients. By offering integrated solutions that streamline the supply chain, US Cold Storage enhances efficiency for its partners. Its focus on technological advancement and service customization allows it to adapt to evolving market needs and maintain a strong reputation for reliability.

MARKET SEGMENTATION

This research report on the US cold storage market has been segmented and sub-segmented based on construction type, temperature, application & region.

By Construction Type

- Production Stores

- Bulk Storage

- Ports

By Temperature

- Frozen

- Chilled

By Application

- Dairy Products

- Processed Foods

- Meat and Seafood

- Fruits and Vegetables

- Pharmaceuticals

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What is driving the growth of the US cold storage market?

The market is driven by increasing demand for frozen and refrigerated food products, the rise of e-commerce grocery delivery, growth in the pharmaceutical cold chain (especially biologics and vaccines), and the need for advanced temperature-sensitive logistics. Changing consumer habits, such as a preference for frozen prepared meals and packaged foods, have further boosted demand.

2. What are the major segments in the US cold storage market?

The market is segmented by temperature range (refrigerated, frozen, deep frozen), by end use (food, pharmaceuticals, biotechnology), and by facility type (public warehousing, private and contract cold storage operators). Frozen food storage currently holds a significant share due to widespread consumption of frozen products.

3. Which industries consume the most cold storage services?

The food and beverage industry is the largest consumer of cold storage services, particularly for items like meat, seafood, dairy, fruits, and vegetables. The pharmaceutical and healthcare sectors also represent a growing segment due to increased demand for temperature-controlled storage of vaccines, biologics, and diagnostic materials.

4. How is e-commerce influencing the US cold storage market?

E-commerce growth, especially in grocery and meal delivery services, has expanded the need for strategically located cold storage facilities near urban centers. Faster delivery expectations and fulfillment requirements have encouraged investment in cold storage capacity and last-mile distribution hubs.

5. What role does technology play in the cold storage market?

Advanced technologies such as IoT sensors, automated storage and retrieval systems (AS/RS), real-time temperature monitoring, and AI-enabled warehouse management systems are improving operational efficiency, traceability, and energy management. These innovations make cold storage operations more reliable and cost-effective.

6. What challenges does the US cold storage market face?

Key challenges include high energy costs, stringent regulatory compliance (FDA, USDA, FSMA), capital-intensive infrastructure investments, and maintaining temperature integrity during transport. Workforce shortages and fluctuating demand patterns can also complicate capacity planning.

7. How does sustainability impact the cold storage industry?

Sustainability initiatives focus on reducing energy consumption through efficient insulation, LED lighting, renewable energy sources, and advanced refrigeration technologies. Companies are also exploring carbon footprint reduction strategies to meet environmental goals and regulatory expectations.

8. What are the primary distribution channels for cold storage services?

Cold storage services are distributed through public warehousing providers, dedicated private facilities owned by food processors or retailers, and third-party logistics (3PL) companies offering contract cold storage solutions tailored to specific temperature needs.

9. Who are the major players in the US cold storage market?

Key companies operating in the market include Lineage Logistics, Americold Realty Trust, United States Cold Storage (USCS), Preferred Freezer Services, and Burris Logistics. These firms compete based on capacity, geographic coverage, and technology adoption.

10. What is the future outlook of the US cold storage market?

The US cold storage market is expected to grow steadily due to expanding frozen food consumption, e-commerce grocery delivery, pharmaceutical cold chain requirements, and investment in sustainable, technology-enabled facilities. Strategic location expansion and automation will continue to shape market dynamics.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com