U.S. Power Tools Market Size, Share, Trends, and Growth Analysis Report - Segmented By Mode of Operation (Electric, Pneumatic, Others (Hydraulic)), Tool Type, Application & Region (New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado), Industry Forecast From 2026 to 2034

U.S. Power Tools Market Summary

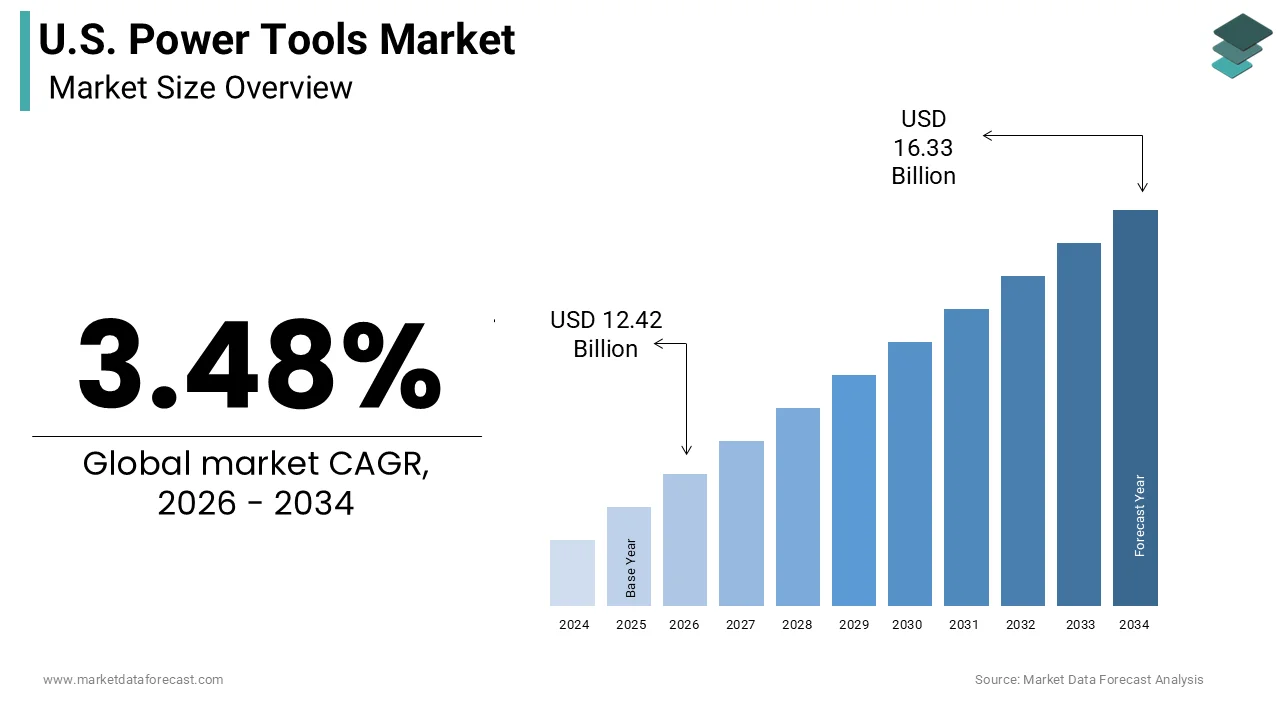

The U.S. power tools market was valued at USD 12 billion in 2025, is anticipated to reach USD 12.42 billion in 2026, and is projected to reach USD 16.33 billion by 2034, growing at a CAGR of 3.48% during the forecast period from 2026 to 2034. The growth of the U.S. power tools market is driven by rising adoption of cordless and electric-powered tools, expanding construction and manufacturing industries, increasing demand for DIY home improvement projects, and technological advancements in tool efficiency and battery performance.

Key Market Trends

- Growing shift toward battery-operated and cordless power tools for greater flexibility and portability.

- Increasing use of smart and connected tools with integrated sensors and IoT capabilities for precision and monitoring.

- Rising popularity of DIY culture among U.S. homeowners, boosting residential tool demand.

- Expansion of industrial automation and infrastructure projects fueling the demand for heavy-duty electric tools.

- Growing focus on ergonomic designs and sustainable materials to enhance user safety and comfort.

Segmental Insights

- Based on mode of operation, the electric-powered tools segment held a prominent share of the U.S. power tools market in 2025, supported by rapid advancements in lithium-ion battery technology and the widespread use of cordless tools across professional and consumer segments.

- Based on tool type, the drilling and fastening tools segment dominated the market, accounting for 47.3% of the U.S. power tools market share in 2025, driven by their essential role in construction, automotive, and assembly applications.

- Based on application, the industrial segment held a significant share of the market in 2025, fueled by strong demand from the automotive, aerospace, and manufacturing sectors for efficient and high-precision power tools.

Competitive Landscape

The U.S. power tools market is highly competitive, with companies emphasizing product innovation, battery efficiency, and smart connectivity to gain market share. Strategic initiatives such as mergers, new product launches, and expansion of e-commerce distribution networks are also key growth strategies. Prominent players dominating the market include Atlas Copco AB, Emerson Electric Co., Enerpac Tool Group, Hilti Corporation, Ingersoll Rand, Koki Holdings Co., Ltd, Makita Corporation, Robert Bosch GmbH, Stanley Black & Decker Inc., and Techtronic Industries Co. Ltd.

U.S. Power Tools Market Size

The U.S. power tools market size was calculated to be USD 12 billion in 2025 and is anticipated to be worth USD 16.33 billion by 2034, from USD 12.42 billion in 2026, growing at a CAGR of 3.48% during the forecast period.

The power tools are sale of motorized equipment used for construction manufacturing and home improvement applications. The integrated with the broader construction and DIY ecosystems serving both professional contractors and amateur enthusiasts. According to the United States Census Bureau total construction spending has consistently exceeded 1.8 trillion dollars annually reflecting sustained demand for mechanized tools across residential and commercial projects. The employment in the construction sector remains robust with hundreds of thousands of new jobs added in recent years driving the need for efficient and portable equipment. Regulatory frameworks established by the Occupational Safety and Health Administration influence design standards and safety features prompting manufacturers to innovate in ergonomics and protective mechanisms. The definition of the market extends beyond hardware to include accessories batteries and digital connectivity solutions that enhance productivity. The interplay between housing renovation trends industrial automation and technological adoption defines the current operational landscape. Stakeholders are increasingly focusing on sustainability and durability to meet evolving client expectations. The integration of smart technologies, such as Bluetooth connectivity and torque control is beginning to influence purchasing decisions among tech savvy professionals.

MARKET DRIVERS

Surge in Home Improvement and Residential Renovation Activities

The surge in home improvement and residential renovation activities, as homeowners invest in upgrading and maintaining their properties is surging the growth of the United States power tools market. The aging housing stock in the country necessitates regular repairs and modernization, which drives consistent demand for DIY and professional grade tools. Spending on home improvements reached record levels in recent years with millions of households undertaking projects ranging from kitchen remodels to deck constructions. The pandemic induced shift towards remote work has further amplified this trend as individuals seek to enhance their living spaces for comfort and functionality. The majority of homeowners plan to continue investing in maintenance and upgrades reflecting a long term commitment to property value preservation. The availability of online tutorials and social media content has empowered amateurs to tackle complex tasks increasing the purchase of versatile power tools such as circular saws and impact drivers. Retailers have responded by expanding their offerings of user friendly and compact models suitable for small scale projects. The cultural emphasis on homeownership and curb appeal ensures that power tools remain essential household items.

Expansion of Construction Infrastructure and Industrial Projects

The expansion of construction infrastructure and industrial projects by creating substantial demand for heavy duty and professional grade equipment is additionally propelling the growth of the United States power tools market. Federal and state investments in transportation utilities and public facilities require extensive use of powerful tools for drilling cutting and fastening applications. The Bipartisan Infrastructure Law has allocated billions of dollars for road bridge and broadband development creating a multi-year pipeline of construction activity. These large-scale projects necessitate reliable and high performance tools that can withstand rigorous daily use in challenging environments. The backlog of commercial and industrial construction projects ensures steady procurement of equipment by contracting firms. The growth of the manufacturing sector particularly in semiconductor and electric vehicle production also contributes to demand for precision power tools in factory settings. Professional contractors prioritize durability and battery compatibility leading to brand loyalty and repeat purchases. Manufacturers are responding by developing specialized tools for specific industrial applications such as concrete grinding and metal fabrication. The emphasis on productivity and safety in professional settings drives the adoption of advanced features like brushless motors and electronic controls. This institutional demand provides a robust revenue stream for manufacturers and distributors.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

The volatility in raw material prices and supply chain disruptions by affecting production costs and availability. The industry relies heavily on steel copper plastics and rare earth metals for batteries which are subject to global commodity price fluctuations. The producer price index for metals and metal products has shown considerable variance reflecting the instability of input costs. Trade tensions and geopolitical conflicts have further exacerbated supply chain disruptions leading to delays in component sourcing and increased logistics expenses. Manufacturing indices indicate persistent challenges in obtaining parts, such as semiconductors and motor components. These disruptions force manufacturers to either absorb higher costs, which reduces profitability or pass them on to consumers, which may dampen demand. Small and medium sized distributors are particularly vulnerable as they lack the bargaining power to negotiate favorable terms with suppliers. The unpredictability of lead times complicates inventory management and order fulfillment for retailers. Consumers may face stockouts or delayed deliveries during peak seasons affecting satisfaction and sales. The reliance on overseas manufacturing for certain components increases exposure to international trade policies.

High Cost of Advanced Cordless Systems and Batteries

The high cost of advanced cordless systems and batteries by limiting accessibility for budget conscious consumers and small businesses is degrading the growth of United States power tools market. Cordless power tools equipped with high-capacity lithium-ion batteries and brushless motors command premium prices compared to their corded counterparts. The initial investment for a complete cordless tool kit, including multiple batteries and chargers can exceed several hundred dollars creating a barrier for entry level users. The additional cost of replacement batteries, which degrade over time adds to the total cost of ownership making these systems less attractive for occasional users. The price sensitivity remains a key factor in purchasing decisions with many consumers opting for lower cost corded alternatives or used equipment. Professional contractors may hesitate to switch entire fleets to new battery platforms due to the significant capital expenditure required. The complexity of proprietary battery ecosystems locks users into specific brands reducing flexibility and increasing long term costs. Economic uncertainty and inflationary pressures further exacerbate this issue by reducing disposable income for non-essential upgrades. Manufacturers face challenges in balancing advanced features with affordability to capture a broader market segment.

MARKET OPPORTUNITIES

Integration of Smart Technology and IoT Connectivity

The integration of smart technology and Internet of Things connectivity to enhance productivity and user experience is creating new opportunities for the growth of the United States power tools market. Smart power tools equipped with sensors and Bluetooth connectivity allow users to monitor performance adjust settings and track usage via smartphone applications. According to the Consumer Technology Association, the adoption of connected devices in the construction industry is growing rapidly driven by the need for data driven decision making and efficiency. Professional contractors can use these features to ensure consistent torque application prevent over tightening and maintain quality standards. The digital tools enable better project management and accountability by providing real time data on tool utilization and maintenance needs. Manufacturers are developing ecosystems where tools communicate with each other and central databases to optimize workflow and reduce downtime. The ability to remotely diagnose issues and schedule repairs enhances service efficiency and customer satisfaction. Smart tools also offer enhanced safety features such as automatic shut off when hazardous conditions are detected. The integration with building information modeling software allows for precise execution of complex tasks. This technological evolution transforms power tools from simple mechanical devices into intelligent assets.

Growth in Renewable Energy and Electric Vehicle Infrastructure

The growth in renewable energy and electric vehicle infrastructure to expand into specialized installation and maintenance sectors is another attribute fuelling the growth of the United States power tools market. The transition towards clean energy requires extensive installation of solar panels wind turbines and charging stations, which demand specific power tools for mounting and wiring. The federal incentives for renewable energy projects are driving a surge in construction activity across the country. Installers require durable and portable tools capable of working in diverse outdoor environments and at heights. The rapid expansion of residential and commercial solar installations creates a steady demand for drills drivers and cutting tools designed for metal and composite materials. The build out of electric vehicle charging networks also necessitates electrical work and concrete drilling for station placement. Manufacturers can capitalize on this trend by developing tool kits tailored for green energy technicians with features, such as insulated handles and precision controls. The emphasis on sustainability aligns with corporate social responsibility goals attracting environmentally conscious buyers. Partnerships with renewable energy firms provide channels for bulk sales and brand visibility. This emerging sector diversifies revenue streams and reduces dependence on traditional construction cycles. The specialized nature of these applications allows for higher margins and brand differentiation.

MARKET CHALLENGES

Counterfeit Products and Intellectual Property Theft

The counterfeit products and intellectual property theft by undermining brand reputation and consumer safety is one of the challenges for the growth of the United States power tools market. The proliferation of fake tools that mimic established brands floods online marketplaces and unauthorized retail channels offering inferior quality at lower prices. According to the International Trademark Association counterfeit goods cause significant financial losses for legitimate manufacturers and pose serious safety risks to users due to substandard materials and construction. These counterfeit products often lack proper safety certifications and can malfunction causing injuries or property damage. As per the United States Patent and Trademark Office, enforcement against intellectual property infringement is complex and resource intensive particularly in the digital commerce space. Consumers who inadvertently purchase fake tools may associate negative experiences with the genuine brand eroding trust and loyalty. The difficulty in distinguishing authentic products from sophisticated fakes complicates purchasing decisions for buyers. Manufacturers must invest heavily in anti counterfeiting technologies and legal actions to protect their interests. The presence of counterfeit goods also distorts market pricing and undermines the value of genuine innovations. This illicit trade diverts revenue away from research and development hindering industry progress.

Environmental Regulations and Battery Disposal Issues

The environmental regulations and battery disposal issues by increasing compliance costs and operational complexity is also to pose as a significant barrier for the growth of the United States power tools market. The widespread use of lithium ion batteries in cordless tools raises concerns about environmental impact and waste management. The improper disposal of batteries can lead to soil and water contamination requiring strict handling and recycling protocols. State and federal regulations mandate responsible recycling practices, which increase operational expenses for manufacturers and retailers. The infrastructure for battery collection and processing is still developing creating logistical challenges for widespread compliance. Manufacturers face pressure to design tools with easily removable and recyclable batteries which may require redesigning existing product lines. The cost of establishing take back programs and partnering with recycling facilities adds to the total cost of ownership. The push for sustainable manufacturing processes also requires significant capital investment in cleaner technologies and materials. Consumers are increasingly aware of environmental issues and may prefer brands with strong sustainability credentials. The complexity of navigating varying state regulations creates administrative burdens for national operators.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.48% |

| Segments Covered | By Mode of Operation, Tool Type, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Stanley Black & Decker, Robert Bosch GmbH, Makita Corporation, Hilti Corporation, Techtronic Industries Co. Ltd., Emerson Electric Co., Ingersoll Rand, Atlas Copco AB, Apex Tool Group, Koki Holdings Co., Ltd. |

SEGMENTAL ANALYSIS

By Mode of Operation Insights

The electric segment was accounted in holding 47.4% of the United States power tools market share in 2025 with their versatility ease of use and widespread availability for both residential and professional applications. The rapid advancement in battery technology, which has made cordless electric tools comparable in power to traditional corded and pneumatic alternatives. The sales of cordless power tools have surged, as lithium-ion batteries offer longer runtimes and faster charging capabilities. The convenience of operating without air compressors or hydraulic hoses makes electric tools ideal for diverse work environments from home workshops to construction sites. The majority of construction and manufacturing tasks, now utilize electric drills drivers and saws due to their portability and reduced setup time. The elimination of exhaust fumes and noise pollution associated with gas powered tools that further enhances their appeal in indoor and urban settings. Manufacturers have expanded their product lines to include brushless motors which improve efficiency and durability. The integration of smart features such as torque control and connectivity is predominantly found in electric models. This technological edge ensures that electric tools remain the preferred choice for a broad spectrum of users. The extensive retail distribution network for electric tools also supports their market leadership.

The pneumatic power tools segment is likely to register a CAGR of 5.8% from 2026 to 2034 with the increasing demand for high power to weight ratio tools in industrial and automotive manufacturing sectors. The pneumatic tools are essential for assembly lines, where continuous high torque and durability are required without the risk of overheating. The automotive repair and body shop industries rely heavily on pneumatic impact wrenches sanders and spray guns for their consistent performance and longevity. The pneumatic tools are often preferred in hazardous environments where electrical sparks could pose a safety risk. The lower initial cost of pneumatic tools compared to advanced cordless electric models makes them attractive for large scale industrial procurement. Improvements in air compressor efficiency and portable air supply systems have enhanced the usability of pneumatic equipment in field applications. The robustness of pneumatic mechanisms allows them to withstand harsh conditions and heavy usage with minimal maintenance. Industrial automation trends also favor pneumatic actuators and tools for their precision and reliability. The expansion of the manufacturing sector particularly in aerospace and automotive industries drives the adoption of specialized pneumatic equipment.

By Tool Type Insights

The drilling and fastening tools segment was the largest by holding a dominant share of the United States power tools market in 2025 with their fundamental role in construction assembly and DIY projects. The drilling and fastening operations are among the most frequent tasks performed in residential construction and renovation. Cordless drills and impact drivers are staple tools for both professional contractors and homeowners due to their versatility and ease of operation. The high volume of housing starts and infrastructure projects ensures consistent demand for these essential tools. The development of compact and lightweight models has expanded their applicability in tight spaces and overhead tasks. Manufacturers continuously innovate with features such as adjustable clutches and LED lights to enhance user experience. The availability of diverse bits and accessories further extends the functionality of drilling and fastening tools. The replacement cycle for these high usage items is relatively short driving repeat purchases. The integration of brushless technology has improved battery life and performance making them more attractive to users.

The sawing and cutting tools segment is expected to witness a fastest CAGR of 6.5% during the forecast period with increasing complexity of construction materials and the demand for precision cutting. The rising popularity of cordless circular saws, miter saws, and reciprocating saws that offer portability and accuracy. The shift towards prefabricated construction components requires precise cutting tools for efficient assembly on site. The growth of the woodworking hobbyist community also contributes to demand for high quality table saws and jigsaws. The sales of premium cutting tools have increased as consumers invest in home improvement projects requiring detailed craftsmanship. Advances in blade technology and motor efficiency have enhanced cutting speed and quality reducing material waste. The introduction of track saws and plunge cut models has revolutionized carpentry workflows appealing to professionals seeking superior results. The expansion of the renewable energy sector also drives demand for cutting tools used in solar panel and wind turbine installation. Manufacturers are focusing on safety features such as electric brakes and kickback protection to meet regulatory standards.

COMPETITION OVERVIEW

The competition in the United States power tools market is characterized by intense rivalry among global giants and specialized manufacturers who compete on innovation quality and brand loyalty. The market structure is moderately consolidated with key players holding significant influence over pricing and technological trends. Competitive intensity is driven by the rapid advancement of cordless technology and the integration of smart features into traditional tools. Regulatory compliance regarding safety and environmental standards serves as a baseline requirement but excellence in performance becomes a key differentiator. Established players leverage their extensive distribution networks and strong brand recognition to maintain market presence. Price competition is fierce in the consumer segment while professional sectors focus on durability and total cost of ownership. The rise of direct to consumer sales channels disrupts traditional retail models forcing companies to adapt. The focus on sustainability and ergonomic design is becoming increasingly important for attracting diverse user groups.

KEY MARKET PLAYERS

A few major players of the U.S power tools market include

- Stanley Black & Decker

- Robert Bosch GmbH

- Makita Corporation

- Hilti Corporation

- Techtronic Industries Co. Ltd

- Emerson Electric Co

- Ingersoll Rand

- Atlas Copco AB

- Apex Tool Group

- Koki Holdings Co., Ltd

Leading Players in the U.S Power Tools Market

- Stanley Black and Decker Inc is a dominant force in the United States power tools market with a diverse portfolio including DeWalt Craftsman and Milwaukee brands. The company leverages its extensive distribution network to serve both professional contractors and DIY consumers effectively. Stanley Black and Decker strengthens its market position by investing heavily in digital innovation and connected tool technologies. The company recently focused on supply chain optimization and cost reduction initiatives to improve operational efficiency. It also expands its product lines with advanced cordless solutions powered by high performance lithium ion batteries. These strategic actions reinforce its reputation for durability and innovation while addressing the evolving needs of the construction and industrial sectors.

- Techtronic Industries Co Ltd is a leading manufacturer in the US power tools market known for its Ryobi and Milwaukee brands which cater to distinct consumer segments. The company focuses on delivering innovative cordless solutions that offer superior power and runtime for professional and home users. Techtronic Industries strengthens its market position through continuous research and development in battery technology and motor efficiency. The company recently expanded its manufacturing capabilities in the United States to reduce lead times and enhance supply chain resilience. It also invests in digital platforms that provide users with tool tracking and management features. These efforts enable Techtronic Industries to maintain a competitive edge and drive growth in the dynamic power tools sector.

- Bosch Power Tools is a prominent player in the United States market recognized for its high quality engineering and innovative design in professional grade equipment. The company offers a wide range of corded and cordless tools for construction woodworking and metalworking applications. Bosch strengthens its market position by introducing advanced features such as connectivity and precision control in its product lineup. The company recently launched new brushless motor technologies that enhance performance and extend tool lifespan. It also focuses on sustainability by developing eco friendly manufacturing processes and packaging solutions. Bosch prioritizes customer support and training programs to build loyalty among professional users. These strategies allow Bosch to maintain a strong presence and meet the demanding standards of the US power tools industry.

Top Strategies Used by Key Market Participants

Key players in the United States power tools market primarily employ strategies such as product innovation brand diversification and supply chain optimization to strengthen their market position. Companies frequently invest in developing advanced cordless technologies with improved battery life and power output to meet professional demands. This approach allows them to differentiate their offerings and command premium pricing in competitive segments. Strategic acquisitions of complementary brands help firms expand their product portfolios and access new customer bases. By focusing on digital connectivity features companies enhance user experience through tool tracking and data analytics. Additionally, manufacturers emphasize sustainability by adopting eco friendly materials and energy efficient production methods. Direct to consumer sales channels are also expanded to improve margin and customer engagement. These combined strategies enable market participants to maintain competitiveness and drive growth in a mature industry landscape.

MARKET SEGMENTATION

This research report on the U.S. power tools Market has been segmented and sub-segmented based on the following categories.

By Mode of Operation

- Electric

- Pneumatic

- Others (Hydraulic)

By Tool Type

- Drilling & Fastening Tools

- Material Removal Tools

- Sawing and Cutting Tools

- Demolition Tools

- Others (Routing Tools)

By Application

- Do-It-Yourself (DIY)

- Industrial

By Region

- New York

- Massachusetts

- Pennsylvania

- Illinois

- Ohio

- Michigan

- Texas

- Florida

- Georgia

- California

- Washington

- Colorado

Frequently Asked Questions

1. What factors are driving the growth of the U.S. power tools market?

Key growth drivers include rising residential and commercial construction activities, increasing adoption of cordless and smart tools, expansion in DIY and home improvement projects, and growing manufacturing and automotive sectors.

2. What are the major challenges facing the U.S. power tools market?

Challenges include High initial costs of advanced tools, Battery performance limitations in cordless tools, Intense price competition among brands, and Raw material price volatility

3. Which types of power tools are most popular in the U.S.?

The most widely used tools include drills, saws, grinders, sanders, wrenches, nailers, and impact drivers, with cordless drills holding the largest market share.

4. What technological trends are shaping the U.S. power tools market?

Emerging trends include Battery innovation (lithium-ion and solid-state batteries), integration of IoT and Bluetooth for tool tracking and safety, brushless motor technology for higher efficiency, and ergonomic and lightweight designs

5. What is the difference between corded and cordless power tools?

Corded tools require a direct power source and offer consistent performance, while cordless tools are battery-powered, providing portability and flexibility ideal for mobile or remote work environments.

6. Who are the leading players in the U.S. power tools market?

Major companies include Stanley Black & Decker, Bosch, Makita, Hilti, Milwaukee Tool, DEWALT, Ryobi, and Snap-on, among others.

7. Which end-user industries contribute most to market demand?

Primary end-users include construction, automotive, manufacturing, woodworking, aerospace, and residential consumers (DIY and renovation enthusiasts).

8. How are sustainability and eco-friendly initiatives influencing the market?

Manufacturers are focusing on energy-efficient motors, recyclable batteries, and sustainable packaging, aligning with U.S. environmental standards and consumer preferences for eco-conscious tools.

9. What distribution channels are dominant in the U.S. power tools market?

The market operates through offline retail stores (Home Depot, Lowe’s, Ace Hardware) and online platforms (Amazon, brand websites), with e-commerce growth accelerating post-pandemic.

10. What are the future opportunities in the U.S. power tools market?

Future growth opportunities lie in Smart and connected power tools, Battery-swapping and fast-charging innovations, Rental services and tool-as-a-service models, and Expansion of modular tool systems for professionals.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com