- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$5 BnMarket Estimate, 2026

$5.33 BnMarket Forecast, 2034

$8.89 BnCAGR, 2026–2034

6.6%Executive Summary: Ventilator Market

- Market Scope: Comprehensive global ventilator market analysis covering device mobility, interface types, end-user settings, regional leadership frameworks, and critical-care technology metrics.

- Market Valuation: Valued at USD 5.0 billion (2025 base year), estimated at USD 5.33 billion (2026), and projected to reach USD 8.89 billion by 2034, registering a steady CAGR of 6.6% (2026–2034).

- Primary Growth Drivers: Increasing respiratory diseases, aging populations, critical-care admissions, premature births, expanding ICU capacity, and technological advancements in microprocessor-controlled ventilation. Advanced systems integrate sophisticated sensors for air pressure, flow rate, leakage detection, and remote monitoring capabilities.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Mobility & Type | Intensive-Care Ventilators (dominated mobility segment with >60% market share in 2025) | Portable, Transport, & Advanced Microprocessor-Controlled Ventilators |

| By Interface & Delivery | Invasive Ventilation (led by interface in 2025), alongside considerable Non-Invasive share | Non-Invasive Ventilation (NIV) Systems & Smart Hybrid Interfaces |

| By End User | Hospitals & Clinics (held the largest end-user share in 2025) | Home Care Settings & Ambulatory Care Facilities (ranked second, registering highest CAGR) |

| By Region / Country | North America (led global market with a 35% share in 2025), followed by Europe & Asia-Pacific | Asia-Pacific & Emerging Regional Critical-Care Infrastructure Hubs |

Major Market Players & Market Structure

Market Structure: Highly competitive global critical-care medical device landscape featuring leading healthcare technology enterprises competing intensely on AI-enabled monitoring, remote-control capabilities, improved battery life, miniaturized components, and advanced critical-care ventilation technologies.

Key Companies: Koninklijke Philips N.V., ResMed Inc., Medtronic plc, Becton, Dickinson and Company, Getinge AB, Drägerwerk AG & Co. KGaA, Smiths Group plc, Hamilton Medical AG, GE Healthcare, Fisher & Paykel Healthcare, Air Liquide, Asahi Kasei Corporation, and Allied Healthcare Products.

Global Ventilator Market Size

The size of the global ventilator market was worth USD 5 billion in 2025. The global market is anticipated to grow at a CAGR of 6.6% from 2026 to 2034 and be worth USD 8.89 billion by 2033 from USD 5.33 billion in 2026.

MARKET DRIVERS

Growth Driven by Respiratory Diseases & Aging Population

The increasing prevalence of respiratory diseases and the growing aging population worldwide are key drivers propelling the growth of the global ventilator market. The burden of respiratory diseases is rising due to various causes, such as smoking, obesity, and behavioral changes. Also, lung and respiratory disorders, such as chronic obstructive pulmonary disease (COPD) and bronchial asthma, consistently need ventilators as they cause postoperative problems among patients. The increasing incidence of these target indications raises the affected patient's hospital admission and readmitted rates as they may need regular ventilation assistance. Besides, with an uptick in the aging population, there has been a corresponding increase in cardiovascular disease, stroke, and diabetes. The need for prompt medical attention distinguishes these cases.

Critical Care & Technological Advancements

An increase in critical care unit cases is a major factor accelerating the ventilator market growth. The ventilation system gives artificial or mechanical respiration to a patient suffering from a chronic condition. Also, growing people's discretionary incomes and their ability to pay more for specialized healthcare systems have facilitated the development and upgrading of healthcare infrastructure and treatment facilities. As a result, it also brings momentum to the market. Technological developments, growing healthcare costs, and an increasing number of intensive care beds in developing markets also drive the development of the global ventilator industry. The industry is similarly influenced by a high rate of premature births, rising demand for medical care in the senior community, and government efforts to improve the development of ventilators. However, the shortage of qualified healthcare personnel, the lack of consistent terminology for various ventilation types, and the high costs associated would significantly restrict business development.

Technological advancements in ventilators are boosting the growth rate of the global market.

Technological advancements in microprocessor-controlled ventilation, integrated with the challenge of new ventilation types, have created a multidisciplinary healthcare team with a range of ways to transform critically ill ventilation treatment for patients. Advanced ventilators are ready for all specifications and have multiple checks and balances. Patient-specific parameters, such as air pressure, air volume, and flow rate, and general parameters such as air leakage, mechanical loss, power failure, battery replacement, oxygen tanks, and remote control are fitted with sensors and monitors.

Factors such as preterm birth, rapid growth in population, rising lung diseases, and an increased number of ICU beds are promoting the ventilator market growth worldwide. The growth in chronic illness among children and the diseases related to the heart and lungs due to lifestyle changes has also increased the demand for ventilators. The growth in the number of home therapists has also led to an increase in demand for ventilators. Countries like India, China, and Brazil have led a rise in the need for ventilators in these countries. These countries have increased their healthcare budgets, and there is a significant share of the development of ventilators in these budgets.

MARKET RESTRAINTS

Unfavorable reimbursement scenarios in case ventilators limit the growth of the global market.

The ventilators are very complex to use, and only trained professionals should be allowed to use them; due to the lack of such professionals worldwide, ventilators are restricted. Physicians have also shown a lack of transition to ventilators, which can be challenging. Ventilator costs are high worldwide, making them inaccessible to the poor, thus limited in reach. The improper functioning of alarms, inappropriate heating or humidification of the inspired gas, and improper ventilation cycle are minor complications during ventilation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type Of Interface, End-Users, Mobility, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Philips, ResMed, Medtronic, Becton, Dickinson and Company, Getinge, Dräger, Smiths Group, Hamilton Medical, G.E. Healthcare, Fisher & Paykel, Air Liquide, Asahi Kasei, and Allied Healthcare Products, and Others. |

SEGMENTAL ANALYSIS

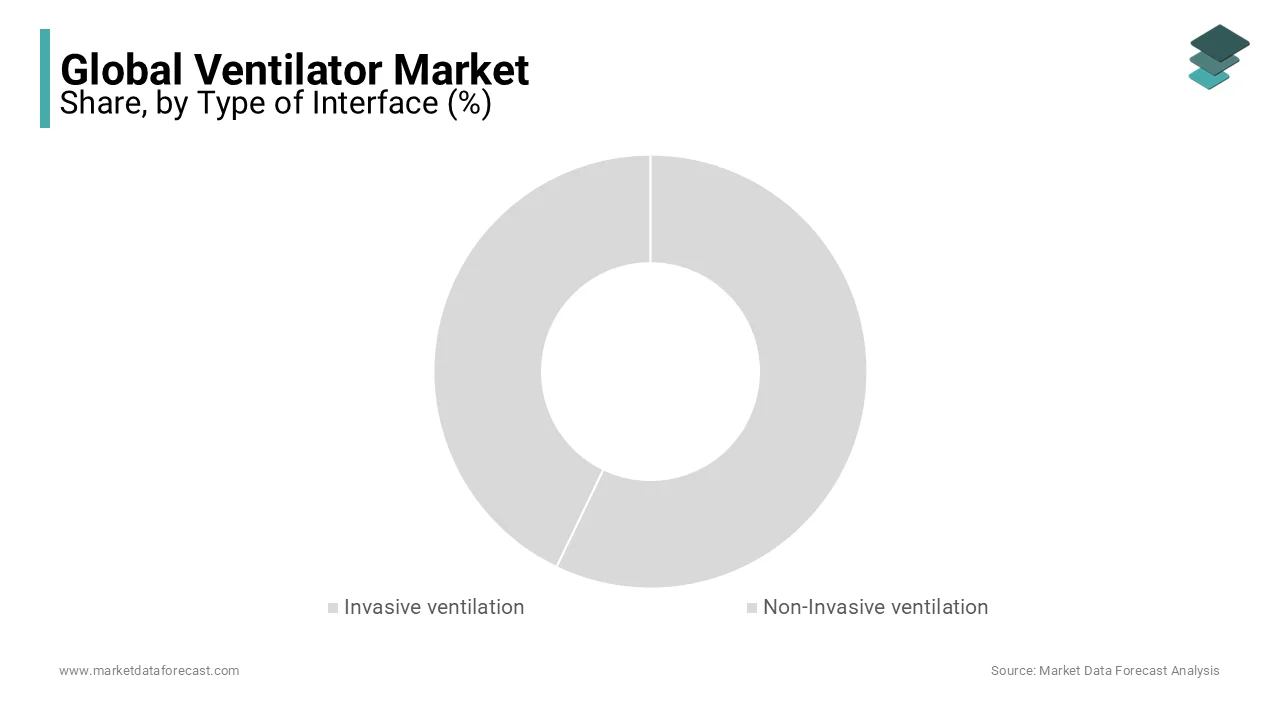

By Type of Interface Insights

The invasive segment led the ventilator market in 2025 and is expected to register a prominent CAGR during the forecast period. Mechanical ventilation is termed Invasive Ventilation. Invasive ventilatory support is provided via either an endotracheal tube or a tracheostomy tube. Wide applications in respiratory diseases, neurological diseases, and sleeping disorders are the primary factors supporting the growth of the invasive ventilation segment.

The non-invasive ventilation segment accounted for a considerable share of the worldwide market in 2025 and is predicted to witness a healthy CAGR during the forecast period. Non-invasive ventilation is the one where support is not provided via the endotracheal tube or tracheostomy tube. Non-invasive ventilation is breathing support through a face mask or nasal mask. Air pressure is administered depending on whether the person is breathing in or out. NIV is used due to the reason that it can avoid spreading the infection. It is second in market share and is expected to increase rapidly.

By End-users Insights

The hospitals and clinics segment occupied the major share of the worldwide market in 2025 and is predicted to continue to be the dominating segment in the global market throughout the forecast period. Hospitals and clinics are the largest end-users of ventilators because ventilators are expensive and difficult to procure. However, especially during COVID-19 times, hospitals have increased their inventory of ventilators to treat patients with severe conditions.

The home care segment is the second-largest ventilator market and is expected to register the highest CAGR. The increased awareness of ventilator technology among patients and doctors, and increased healthcare budgets by personnel have driven this segment's growth.

Ambulances are the third largest, but are expected to rise at a reasonable growth rate due to increased budgets for quality healthcare from private and public institutions.

Emergency medical services are also expected to have a reasonable growth rate due to increased emergency medical cases.

By Mobility Insights

The intensive-care segment is expected to hold the leading share of the global ventilator market during the forecast period. Intensive-care ventilators have the largest market share and are expected to increase as more hospitals and other healthcare institutions are built.

Although they are second in market share, portable ventilators are expected to have a promising CAGR. Portable ventilators are used in cases where ambulances and home care are needed.

REGIONAL ANALYSIS

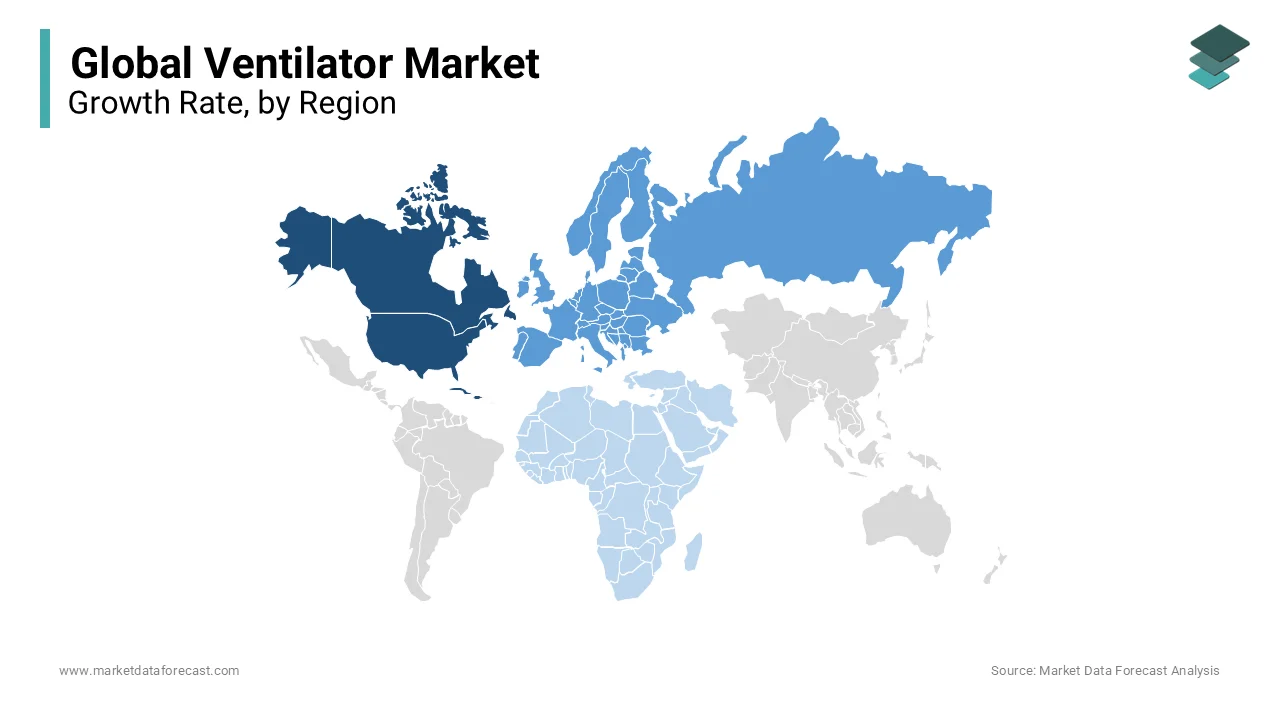

North America Ventilator Market Analysis

North American had the largest share in the global ventilator market in 2025, as the quality of health facilities is much better than in other countries. The hospitals are more advanced, and the significant players in the ventilator market see massive potential and invest more in research and development.

Europe Ventilator Market Analysis

Europe had the second-largest share worldwide in 2025, as the government allocated a fair share for the healthcare industry in its budget. Increased smoking, a rising population, and high healthcare expenditure drive market growth.

Asia-Pacific Ventilator Market Analysis

Asia-Pacific had the third-largest share in the global market in 2025. It is expected to grow at a reasonable rate due to the increase in population in China and India. Also, the healthcare budgets and facilities are significantly less compared to the North American and European markets.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global ventilators market include

- Koninklijke Philips N.V. (Netherlands)

- ResMed Inc. (U.S.)

- Medtronic plc (Ireland)

- Becton, Dickinson and Company (U.S.)

- Getinge AB (Sweden)

- Drägerwerk AG & Co. KGaA (Germany)

- Smiths Group plc (U.K.)

- Hamilton Medical AG (Switzerland)

- GE Healthcare (U.S.)

- Fisher & Paykel Healthcare Corporation Limited (New Zealand)

- Air Liquide (France)

- Asahi Kasei Corporation (Japan)

- Allied Healthcare Products, Inc. (U.S.)

MARKET SEGMENTATION

This market research report on the global ventilator market has been segmented and sub-segmented based on the type of interface, end-users, mobility, and region.

By Type of Interface

- Invasive ventilation

- Non-Invasive ventilation

By End-users

- Hospitals and clinics

- Ambulances

- Home care

- Emergency Medical Services

By Mobility

- Intensive care

- Portable ventilators

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa