Global Wood Chips Market Size, Share, Trends & Growth Forecast Report By Product Type (Hardwood, Softwood and Manual), Variety Type (Forest Chips, Wood Residue Chips and Recycled Chips), Application (Household Furnishing, Combined Heat and Power (CHP)) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis 2024 to 2033

Global Wood Chips Market Size

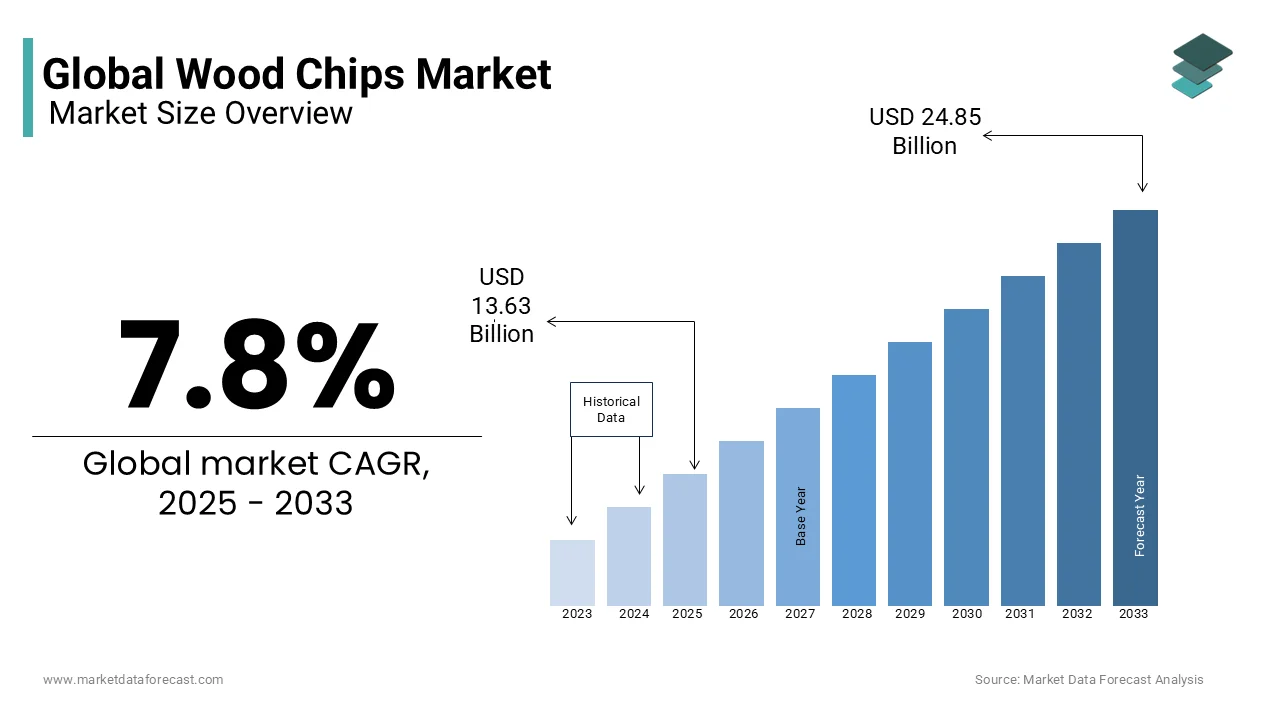

The global wood chips market is estimated to grow from USD 12.64 billion in 2024 to USD 24.85 billion in 2033, representing a CAGR of 7.8%.

The wood chips are chipped lignocellulosic biomass derived from forest residues, logging by-products, and dedicated energy plantations, primarily utilized for energy generation, pulp production, and soil amendment. These processed wood fragments, typically ranging from 10 to 50 mm in size, serve as a feedstock in industrial and residential applications where renewable, carbon-neutral alternatives to fossil fuels are prioritized. As per the Food and Agriculture Organization of the United Nations, approximately 1.8 billion cubic meters of roundwood were harvested globally in 2022, with over 34% allocated to industrial wood processing, generating substantial residual biomass suitable for chipping.

MARKET DRIVERS

Expansion of Biomass-Based Energy Generation

The global shift toward renewable energy as a feedstock in biomass power plants is substantially prompting the growth of the wood chips market. According to the International Energy Agency, bioenergy accounted for over 55% of total renewable energy consumption in the power, heat, and transport sectors in 2023, with solid biomass predominantly wood chips and pellets, which is representing the largest share. The Finland operates over 1,200 biomass-fueled combined heat and power (CHP) facilities, with wood chips constituting 70% of their fuel input, according to Statistics Finland. The European Commission has projected that biomass will contribute 32% of the EU’s renewable energy mix by 2030 under its REPowerEU initiative, further institutionalizing wood chips as a strategic energy resource.

Growth in the Pulp and Paper Industry’s Raw Material Demand

The expansion of the pulp and paper industry is leveraging the demand for raw materials, which is additionally enhancing the growth of the wood chips market. As per the Confederation of European Paper Industries, the EU produced 84 million tonnes of paper and board in 2023, requiring an estimated 120 million cubic meters of wood fiber, much of which is supplied in chipped form. In Canada, the world’s second-largest producer of market pulp, over 40% of harvested roundwood is converted into wood chips for export and domestic mill use, according to Natural Resources Canada. The industry’s preference for uniform, contaminant-free chips ensures consistent pulping efficiency and fiber quality.

MARKET RESTRAINTS

Stringent Regulations on Forest Harvesting and Sustainability Certification

The increasing regulatory scrutiny over forest management practices is restraining the growth of the wood chips market. The European Union’s revised Renewable Energy Directive (RED II) mandates that biomass feedstocks comply with strict sustainability criteria, including proof of legal origin and maintenance of carbon stock levels. As per the European Environment Agency, 38% of forest harvesting in Eastern Europe between 2016 and 2021 exceeded sustainable yield thresholds, triggering import restrictions on non-compliant wood chips. In Canada, the Forest Stewardship Council (FSC) certifies only 42% of managed forests, limiting the volume of certified chips available for eco-sensitive markets, according to the Canadian Council of Forest Ministers. Moreover, countries like Indonesia and Myanmar have imposed export bans on raw wood materials to curb deforestation, indirectly affecting chip availability.

Seasonal and Geographic Limitations in Supply Chain Efficiency

The logistical viability of wood chip transportation is heavily influenced by seasonal weather patterns and geographic remoteness, which is also hampering the growth of the wood chips market. Wood chips have a high moisture content often exceeding 50% when freshly chipped by making them prone to spoilage, mold, and spontaneous combustion during storage and transit, as noted by the U.S. Department of Energy. In northern latitudes, winter snowfall and frozen ground can halt harvesting operations for up to four months annually, according to Natural Resources Canada. Conversely, heavy rainfall in tropical regions like Southeast Asia disrupts road access to logging sites, delaying chipping and transport.

MARKET OPPORTUNITIES

Development of Torrefied Wood Chips for High-Energy Applications

The torrefaction is a thermal treatment process that upgrades wood chips into a coal-like, energy-dense biofuel, which is attributed in leveraging new opportunities for the growth of the wood chips market. The process, conducted at 200–300°C in an oxygen-limited environment, increases the calorific value of wood chips from 18–20 MJ/kg to over 25 MJ/kg while enhancing hydrophobicity and grindability, as demonstrated in research by the Netherlands’ Energy Research Centre (ECN). In Japan, where coal co-firing regulations mandate 5% biomass blending in power plants by 2030, torrefied wood chips are being piloted at units operated by JERA and Tohoku Electric. According to Japan’s Agency for Natural Resources and Energy, the country aims to import 3 million tonnes of upgraded biomass annually by 2030, creating a premium market for treated chips.

Integration into Urban Green Infrastructure and Landscaping

The escalating municipal landscaping and urban forestry programs as a sustainable ground cover and soil conditioner is also to amplify the growth of the wood chips market. As per the U.S. Environmental Protection Agency, over 68 million tons of yard trimmings, including chipped wood, were generated in 2022, with more than half diverted to mulching and land application. Cities like Portland and Vancouver have implemented urban wood recovery programs, converting storm-damaged trees into landscaping chips, reducing landfill burden and enhancing green space resilience. According to the Federal Ministry for the Environment, 90% of public parks use wood chip mulch to suppress weeds, retain moisture, and reduce irrigation needs.

MARKET CHALLENGES

Competition from Alternative Biomass Feedstocks

The intensifying competition from non-woody biomass sources such as agricultural residues, energy crops, and municipal organic waste is a quiet challenging factor for the growth of the wood chips market. According to the International Renewable Energy Agency, rice husks, sugarcane bagasse, and straw accounted for nearly 28% of global bioenergy feedstock use in 2023, particularly in Asia and Latin America. In India, sugarcane bagasse supplies over 3,000 MW of power annually, as reported by the Ministry of New and Renewable Energy, offering a low-cost, locally available alternative. Similarly, in Thailand, cassava rhizome waste and palm kernel shells are increasingly used in biomass boilers due to their high calorific value and lower collection costs. These materials often require less preprocessing than wood chips and are generated in proximity to processing facilities, reducing transport burdens.

Carbon Accounting Disputes and Emissions Controversies

The classification of wood chips as carbon-neutral energy sources is increasingly contested due to temporal carbon debt and supply chain emissions is also to impede the growth of the wood chips market. While the Intergovernmental Panel on Climate Change (IPCC) includes biomass in its carbon accounting frameworks, it acknowledges that carbon neutrality depends on sustainable regrowth timelines. A 2023 study published in Nature Communications found that replacing fossil fuels with wood chips can result in a carbon payback period of 20 to 100 years, depending on forest type and harvesting intensity. In the southeastern United States, large-scale sourcing for export pellet and chip production has led to the conversion of native hardwood forests into pine plantations, as documented by the Southern Environmental Law Center.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| CAGR | 7.8% |

| Segments Covered | By Product Type, Variety Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Cogent Fibre, Enviva Pellets, St. Boniface Pallet, American Wood Resources, EVOWORLD GmbH, Mitsui & Co., Ltd., Oji Holdings, Rentech, Axpo Group, Great Northern Timber, and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The softwood segment dominated the global wood chips market by capturing 54.3% of the share in 2024 with the widespread availability of coniferous forests in boreal and temperate regions, particularly across Canada, Scandinavia, and Russia. Softwood species such as pine, spruce, and fir are preferred in pulp and paper manufacturing due to their long cellulose fibers, which enhance paper strength and durability. According to Natural Resources Canada, over 78% of the country’s roundwood harvest used for industrial processing consists of softwood, much of which is chipped for export or domestic mill supply. In Sweden, softwood chips account for nearly 85% of biomass fuel used in district heating systems, as documented by the Swedish Forest Industries Federation.

The hardwood segment is projected to expand at a CAGR of 5.3% from 2025 to 2033, owing to the rising demand in specialty applications such as biomass torrefaction, landscaping, and high-grade pulp for packaging. Hardwood species like oak, birch, and eucalyptus are increasingly favored in Asia and Europe for their faster growth cycles and suitability for engineered wood products. In Japan, eucalyptus-based wood chips imported from Brazil and Portugal are being used in co-firing trials at thermal power plants due to their lower ash content and improved combustion efficiency, as reported by the Institute of Energy Economics, Japan. Additionally, municipal urban wood recovery programs in the U.S. are converting storm-felled hardwood trees into mulch and biochar feedstock, reducing landfill use.

By Variety Type Insights

The forest chips segment held 48.2% of the wood chips market share in 2024. These chips are produced directly from roundwood or whole trees harvested specifically for energy or industrial use, particularly in regions with dedicated short-rotation coppice plantations. In Finland, forest chips sourced from thinnings and small-diameter trees supply over 6 million cubic meters of biomass annually to CHP plants, according to Statistics Finland. The Finnish government supports this supply chain through subsidies under its KELA program, which incentivizes forest owners to participate in energy wood harvesting.

The recycled chips segment is anticipated to grow at a CAGR of 6.2% from 2025 to 2033. These chips are derived from post-consumer wood waste, demolition debris, and discarded pallets, reflecting a shift toward circular economy models in construction and urban management. The Netherlands has implemented a national ban on untreated wood waste in landfills since 2021, which is compelling municipalities and contractors to channel wood debris into recycling facilities, as enforced by the Ministry of Infrastructure and Water Management. Additionally, in California, the Department of Resources Recycling and Recovery (CalRecycle) reports that urban wood recycling programs diverted 3.2 million tons of wood waste from landfills in 2023, a 12% increase from the previous year.

By Application Insights

The Combined Heat and Power (CHP) application segment was accounted in holding a prominent share of the wood chips market in 2024 with the integration of biomass-fueled CHP systems into national energy infrastructures, particularly in Northern and Central Europe. These facilities simultaneously generate electricity and thermal energy, achieving energy efficiencies exceeding 85%, far surpassing conventional power plants. In Austria, forest-based biomass, primarily in the form of wood chips, fuels 80% of community heating systems in rural municipalities, as reported by the Austrian Biomass Association. The European Commission’s Renewable Energy Directive mandates that member states increase renewable heat usage, further institutionalizing wood chips as a strategic fuel.

The household furnishing segment is likely to witness a CAGR of 5.8% from 2025 to 2033 owing to the rising use of wood chips in engineered wood products such as medium-density fiberboard (MDF), particleboard, and laminated veneer lumber used in furniture and interior design. In India, the engineered wood market expanded by 14% in 2023, as reported by the Indian Plywood Manufacturers’ Association, fueled by modular kitchen and ready-to-assemble furniture trends. Wood chips, especially from fast-growing eucalyptus and rubberwood, serve as the primary raw material in these composites. In Vietnam, over 1.8 million cubic meters of rubberwood chips were processed annually for export-oriented furniture production, according to the Vietnam Timber and Forest Product Association.

REGIONAL ANALYSIS

Europe was the largest contributor of the global wood chips market with 41.2% of the share in 2024 due to its advanced bioenergy infrastructure and strong policy support for renewable heating. The region’s dominance is anchored in Nordic and Central European countries, where sustainable forest management and district heating networks are deeply integrated. Sweden alone produced over 12 million cubic meters of forest chips in 2023, primarily for CHP and industrial heat, as documented by the Swedish Energy Agency. The European Green Deal and REPowerEU initiative have accelerated investments in biomass co-firing and carbon-neutral heating, with Germany allocating EUR 3 billion in subsidies for biomass boiler retrofits by 2027. However, sustainability concerns persist—Greenpeace has reported illegal logging in Romania’s old-growth forests, prompting the EU to tighten biomass sourcing criteria.

North America wood chips market held 28.3% of the share in 2024. The United States and Canada are major producers and exporters of wood chips, particularly to European and Asian bioenergy markets. According to the U.S. Forest Service, over 50 million dry tons of wood residue were converted into chips in 2023, primarily from logging and sawmill by-products. In British Columbia, forest management regulations require utilization of at least 90% of harvested timber, promoting chipping of residuals for energy and pulp. The Southeastern U.S. has become a global hub for wood pellet production, with Georgia-Pacific and Enviva operating large-scale chipping and export terminals. As per the U.S. Energy Information Administration, biomass accounted for 5.3% of total U.S. renewable energy generation in 2023, with wood chips playing a central role in industrial cogeneration and co-firing applications.

Asia Pacific wood chips market is anticipated to grow with a prominent CAGR in the next coming years with rapid industrialization and urbanization driving demand in China, Japan, and South Korea. China is the largest importer of wood chips in the region, sourcing over 15 million cubic meters annually from Australia, Indonesia, and New Zealand for its paper and board industry, as reported by the China Forestry and Paper Association. According to Japan’s Agency for Natural Resources and Energy, the country imported 2.1 million tons of wood chips in 2023, a 17% increase from 2022. In India, urban wood recovery initiatives in cities like Pune and Chennai are converting construction waste into chips for panelboard manufacturing.

Latin America wood chips market growth is likely to grow with Brazil and Chile emerging as key producers due to their expansive eucalyptus and pine plantations. Brazil is the world’s largest producer of eucalyptus pulp, requiring over 100 million cubic meters of chipped wood annually, as stated by the Brazilian Tree Industry Association (IBÁ). The country’s fast-growing eucalyptus clones, which reach harvestable size in just 7–8 years, provide a consistent and high-yield feedstock. Chile exports over 3 million cubic meters of radiata pine chips annually, primarily to China and Japan, according to the Chilean Forestry Institute.The

Middle East & Africa wood chips market growth is expected to remain steady in the coming years. South Africa is the primary producer, generating over 1.2 million cubic meters of wood chips annually from commercial pine and eucalyptus plantations, as reported by the South African Forestry Company Limited (SAFCOL). These chips are used in pulp mills and brick kilns, where biomass is replacing coal to reduce emissions.

KEY PLAYERS IN THE MARKET AND COMPETITIVE LANDSCAPE

Companies playing a major role in the global wood chips market include Cogent Fibre, Enviva Pellets, St. Boniface Pallet, American Wood Resources, EVOWORLD GmbH, Mitsui & Co., Ltd., Oji Holdings, Rentech, Axpo Group and Great Northern Timber.

The competitive landscape of the wood chips market is defined by geographic specialization, resource access, and compliance with environmental standards. Multinational forestry companies dominate supply to industrial hubs in Asia and Europe, while regional processors focus on localized biomass energy and pulp needs. Competition is increasingly shaped by the ability to deliver certified, low-moisture, and contaminant-free chips that meet stringent import regulations. Emerging players in Latin America and Africa are challenging established suppliers by offering cost-advantaged feedstocks, though logistical constraints limit scalability.

Top Players in the Wood Chips Market

Suzano S.A. has significantly expanded its footprint in the Asia Pacific wood chips market through strategic export initiatives and sustainability certifications. As one of the world’s largest producers of eucalyptus pulp, the Brazilian company supplies high-quality hardwood chips to major paper manufacturers in China, India, and South Korea. In 2023, Suzano strengthened its logistics network by securing long-term port capacity at the Port of Itapoá, enabling faster shipment of wood chips to Asian markets. The company has also partnered with Japanese trading houses such as Itochu and Mitsubishi Corporation to co-develop low-carbon supply chains compliant with Japan’s biomass co-firing regulations. Suzano’s FSC-certified plantations and vertically integrated production model ensure traceability and consistent chip quality by making it a preferred supplier for eco-conscious industrial buyers across the region.

West Fraser Timber Co. Ltd. plays a pivotal role in supplying wood residue chips to the Asia Pacific market, leveraging its extensive sawmill operations in Canada and the southern United States. The company processes logging residuals and sawmill by-products into uniform wood chips, which are exported to Japan, South Korea, and Thailand for use in pulp mills and biomass power plants. In 2023, West Fraser upgraded its chipping and drying facility in Hinton, Alberta, to enhance moisture control and transportation efficiency. It also secured a multi-year supply agreement with a leading Thai paperboard manufacturer, reinforcing its presence in Southeast Asia.

Nippon Paper Industries Co., Ltd. is a dominant force in Japan’s domestic wood chips market and a key influencer in regional supply dynamics. The company operates integrated pulp and paper mills that rely heavily on imported and domestically sourced wood chips, particularly from sustainable plantations in New Zealand and Australia. In 2024, Nippon Paper launched a biomass co-firing project at its Oji mill, utilizing processed wood chips to replace 10% of coal consumption, aligning with Japan’s carbon neutrality goals. The company has also invested in advanced chipping and sorting technologies to improve feedstock efficiency.

Top Strategies Used by Key Market Participants

Key players in the wood chips market are prioritizing vertical integration, securing control over forest plantations, chipping operations, and logistics to ensure supply chain resilience. Companies are investing in advanced drying and screening technologies to meet moisture and contamination standards for export markets. Strategic partnerships with energy utilities and paper mills are being forged to lock in long-term off-take agreements. Sustainability certification such as FSC and PEFC is increasingly leveraged to access environmentally regulated markets in Europe and Asia. Additionally, firms are expanding port infrastructure and shipping alliances to reduce transit times. Innovation in torrefaction and chip densification is being explored to enhance energy density and transport efficiency, strengthening competitiveness in high-value bioenergy applications.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Suzano S.A. secured a long-term shipping agreement with Maersk Line to enhance wood chip export capacity from Brazil to Chinese pulp mills that ensures consistent delivery schedules and reduces transit-related moisture degradation, thereby strengthening its position in the Asia Pacific industrial feedstock market.

- In May 2023, West Fraser Timber commissioned a new automated chipping and drying facility in Louisiana, increasing output by 18% and improving chip uniformity for export to South Korean biomass power plants by reinforcing its role as a high-efficiency supplier in the trans-Pacific wood chip trade.

- In September 2023, Nippon Paper Industries launched a forest thinning initiative in Nagano Prefecture, sourcing underutilized cedar and cypress trees to produce low-cost wood chips for domestic paper production, which is supporting rural forest management while securing a sustainable feedstock supply.

- In February 2024, Suzano partnered with Itochu Corporation to co-develop a low-carbon wood chip supply chain to Japan, incorporating blockchain-based traceability and emissions tracking by enhancing compliance with Japan’s biomass sustainability certification scheme.

- In April 2024, West Fraser Timber expanded its port storage capacity at the Port of Vancouver, enabling year-round export of dried wood chips to Southeast Asian markets, reducing shipping delays and improving moisture control, thereby strengthening its reliability as a key supplier in the Asia Pacific region.

MARKET SEGMENTATION

This research report on the global wood chips market has been segmented and sub-segmented based on product type, variety type, application, and region.

By Product Type

- Hardwood

- Softwood

- Manual

By Variety Type

- Forest Chips

- Wood Residue Chips

- Recycled Chips

By Application

- Household Furnishing

- Combined Heat and Power (CHP)

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the Wood Chips Market growth rate during the projection period?

The Global Wood Chips Market is expected to grow with a CAGR of 7.80% between 2025-2033.

2. What can be the total Wood Chips Market value?

The Global Wood Chips Market size is expected to reach a revised size of USD 24.85 billion by 2033.

3.Name any three Wood Chips Market key players?

Enviva Pellets, St. Boniface Pallet, and American Wood Resources are the three Wood Chips Market key players.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com