Mexico Cards And Payments Market Size, Share, Trends & Growth Forecast Report By Cards (Debit Cards, Credit Cards, Prepaid Cards), By Payment Terminals (POS And ATM's), By Payment Instruments (Credit Transfers, Direct Debit, Cheques And Payment Cards), Transaction Value, Volumes, Historical Trends, Analysis And Forecasts 2025 to 2033

Mexico Cards and Payments Market Size

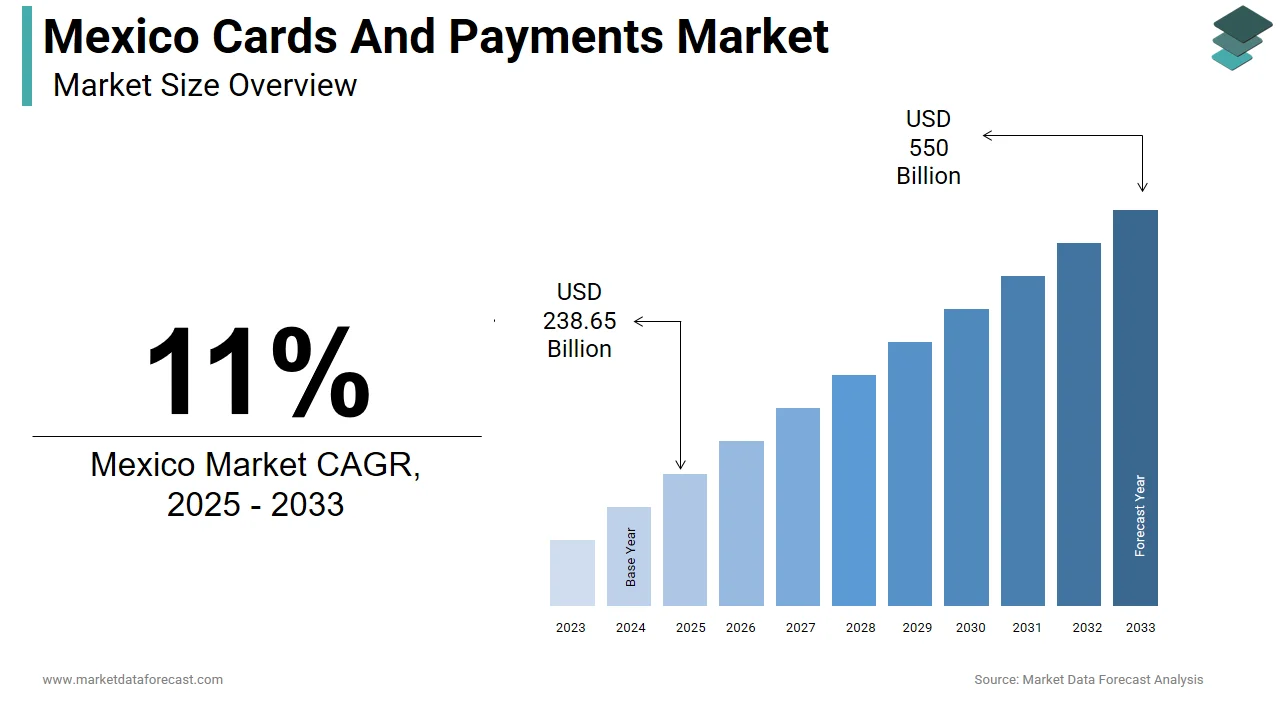

The Mexico cards and payments market size was valued at USD 215 billion in 2024. This market is expected to grow at a CAGR of 11% from 2025 to 2033 and be worth USD 550 billion by 2033 from USD 238.65 billion in 2025.

MARKET DRIVERS

Rapid Growth of E-commerce and Digital Transactions

The surge in e-commerce has been a key driver for card and digital payment adoption in Mexico. This growth has necessitated secure and efficient digital payment solutions, especially credit and debit cards. In 2023, approximately 65% of all online transactions were conducted using cards, while alternative methods like digital wallets accounted for an additional 20%, per BBVA Research. Platforms such as PayPal, Mercado Pago, and Apple Pay have expanded their presence, which is offering localized services that cater to diverse consumer preferences. Mastercard reported a 33% year-on-year increase in cross-border card spending among Mexican consumers, driven largely by access to global marketplaces like Amazon and Shein.

Government Initiatives Promoting Financial Inclusion and Cashless Payments

The Mexican government has implemented policies aimed at reducing cash dependency and enhancing financial inclusion, directly supporting the growth of the cards and payments sector. Banxico’s National Strategy for Financial Inclusion (ENIF) set a target to increase the proportion of adults using formal financial services from 65% in 2021 to 80% by 2024. According to the World Bank's Global Findex Database (2021), 46% of adults in Mexico still rely on cash for daily transactions, highlighting the significant potential for digital payment expansion.

MARKET RESTRAINTS

Persistent High Reliance on Cash Across Demographics

Cash remains dominant in Mexico among lower-income and older demographics despite growing digital adoption. According to the World Bank's Global Findex Database (2021), 52% of adults in Mexico still use cash for most of their daily transactions. A 2023 survey by Banxico found that only 38% of micro-merchants accepted card payments, largely due to high transaction fees and limited technological infrastructure. This gap restricts the reach of digital payment systems and slows nationwide transformation efforts. Moreover, cultural habits play a role approximately 44% of respondents in a BBVA Research study cited distrust in digital systems as a reason for preferring cash. Older generations and rural populations are particularly hesitant to adopt electronic alternatives. Additionally, informal economic activity, which accounts for nearly 26% of GDP according to OECD estimates, further reinforces cash dependency and limits the scope of formal payment instruments.

Regulatory Complexity and Fragmentation in Payment Systems

Mexico’s evolving regulatory environment presents challenges for both traditional banks and fintechs aiming to scale their operations. The National Banking and Securities Commission (CNBV) oversees banking institutions, while the Secretariat of Finance and Public Credit (SHCP) regulates non-bank payment platforms, creating overlapping jurisdictions. Furthermore, licensing timelines for fintech firms remain lengthy, averaging 12–18 months, deterring foreign investment and slowing product launches.

Interoperability issues also persist QR code-based payment systems such as CoDi and those offered by private banks often do not work seamlessly across platforms, causing confusion for users and merchants alike. These structural inefficiencies hinder innovation and create friction in the broader digital payments ecosystem.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services

The BNPL segment is emerging as a major opportunity in Mexico, catering to younger, digitally savvy consumers seeking flexible financing options. This growth is driven by partnerships between fintechs and major retailers to offer interest-free installment plans. Companies like Klarna, Affirm, and local players such as Konfio and Kueski are expanding rapidly, with Konfio alone processing over MXN 15 billion in annual gross merchandise volume by Q4 2023. Younger consumers, particularly those aged 18–35, account for nearly 65% of BNPL users, as they seek alternatives to traditional credit cards due to high interest rates or lack of access to formal credit. Financial regulators are working closely with industry stakeholders to develop a balanced regulatory framework that encourages innovation while protecting consumers, which is suggesting a favorable policy climate ahead.

Integration of AI and Blockchain in Fraud Detection and Security

As digital payments expand, so too does the need for robust fraud detection mechanisms. Financial institutions in Mexico are increasingly adopting AI-driven analytics and blockchain technology to enhance security and reduce risk. According to a 2023 report by IBM Security, AI-powered fraud detection systems have reduced fraudulent card transactions by up to 40% in the last two years, saving the industry over MXN 12 billion annually. Blockchain technology is being tested by several banks and fintech firms for identity verification and transaction traceability. For example, Banorte partnered with ConsenSys to pilot a blockchain-based KYC system in 2023, streamlining customer onboarding and reducing fraud risks. These innovations are attracting international attention. In 2023, Mexico attracted $150 million in venture capital funding for fintech startups focused on secure payment solutions, reflecting a 42% year-over-year increase, per PitchBook data.

MARKET CHALLENGES

Cybersecurity Threats and Data Privacy Concerns

With the rapid digitization of payments, cybersecurity threats have become a critical challenge in Mexico. According to the National Cybersecurity Coordination Center (CNCSC), the number of cyberattacks targeting financial institutions rose by 40% in 2023 compared to the previous year. Credit card fraud alone accounted for over 35,000 complaints filed with Profeco (Federal Consumer Protection Agency) in 2023, with losses exceeding MXN 18 billion ($1.1 billion). Phishing attacks targeting mobile banking apps affected over 1.2 million users during the same period, per a report by Kaspersky Lab. Fintech startups and smaller banks face particular challenges in implementing robust cybersecurity measures due to limited resources and expertise. Many rely on third-party vendors for fraud detection, which can lead to vulnerabilities if not properly managed.

High Entry Barriers for Foreign Fintech Companies

Foreign fintech firms encounter significant entry barriers when attempting to operate in Mexico’s cards and payments market, limiting international competition and innovation. Mexico’s regulatory framework requires extensive localization, including adherence to strict licensing requirements set by the National Banking and Securities Commission (CNBV). For example, foreign companies must partner with local banks or obtain a specialized fintech license, which can take up to 18 months to process. According to a 2023 report by ProMéxico, only 10% of foreign fintech firms successfully entered the market within their first year of application, compared to over 35% in Brazil.

Moreover, language barriers, conservative business culture, and entrenched domestic players make market penetration difficult. Even global giants like Stripe and Adyen have faced slow adoption due to reluctance from Mexican merchants accustomed to domestic payment processors.

Banks also dominate customer relationships, which is leaving little room for neobanks or alternative payment providers to scale quickly. These structural and regulatory hurdles create a challenging environment for foreign entrants, potentially stifling the pace of digital transformation in the sector.

MARKET KEY HIGHLIGHTS

- The growth of electronic payments across the country and reduced the dependence on cash as a result of being part of UN’s Better Than Cash Alliance, which uses mobile phones for digital payments.

- The growing adoption of alternative payments led to the introduction of new products by banking firms like Banamex Wallet, launched by Banamex in collaboration with MasterCard allowing Android users to add their MasterCard details to the wallet and pay for transactions, and Bancomer's mobile wallet BBVA Wallet allowing NFC payments at merchant locations that accept contactless payments.

- Secured payment solutions are being given more significance to avoid fraudulent transactions. For instance, the Identity Check Mobile solution by MasterCard requires scanning the fingerprint or a selfie of the user to authenticate the transaction, and OT Motion Code technology, developed by Mexican payment processing services provider Promocion y Operacin SA (PROSA) along with Oberthur Technologies, involves changing CVV code at regular intervals.

KEY MARKET PARTICIPANTS

Top players in the Mexican cards and payments market include

- BBVA Bancomer

- Banco Santander

- BanCoppel

- Citibanamex

- Banorte

- Nacional Financiera

- HSBC

MEXICO CARDS AND PAYMENTS MARKET NEWS

- Payment cards are accepted by only 14% of the merchants in Mexico, constraining the market growth. Various banking and financial institutions are implementing new strategies to increase this percentage. Mastercard started the Cashless Makeover Mexico program in January 2018 to encourage the acceptance of payment cards and its Masterpass by small and medium enterprises. A deal was made earlier in May 2017 between Mastercard and the government of Mexico to encourage card transactions, under the supervision of the Ministry of Economic Development (SEDECO).

- The use of prepaid cards for transportation is expected by the Mexican government to support digital payments. Prepaid Metro cards were introduced by Mastercard in November 2017, integrating with the Metro Collective Transportation System. This card includes both the Mastercard balance and Metro balance, which can be used for retail purchases and buying metro tickets respectively. Similarly, for bus transport, the closed-loop prepaid card called Cytibus was launched in January 2018. This card at the time of its inception was accepted in only 150 buses with a loading facility at 30 OXXO stores, which is now increased to almost 500 buses and 220 OXXO stores.

- In March 2018, a Fintech law was introduced in the country to control the growing financial technology companies in the region. This law offers basic fintech companies’ requirements, along with accurate regulations governing issues like payment options, cryptocurrencies and public funding. It also allows open banking, a concept that enables financial institutions to share consumer information via a public API

MARKET SEGMENTATION

This research report on the Mexican Cards and Payments market has been segmented and sub-segmented based on the following categories.

By Cards

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards

Frequently Asked Questions

1. What is the size of the Mexico cards and payments market?

The Mexico cards and payments market reached USD 238.65 billion in 2025, projected to hit USD 550 billion by 2033. Growth reflects digital transformation.

2. What drives growth in the Mexico cards and payments market?

Neobanks and prepaid expansion propel the Mexico cards and payments market. E-commerce boosts contactless adoption significantly.

3. Who are key players in the Mexico cards and payments market?

Leaders in the Mexico cards and payments market include BBVA, Citibanamex, Mercado Pago, Visa, and Mastercard. They drive digital issuance.

4. What is the CAGR of the Mexico cards and payments market?

The Mexico cards and payments market forecasts 11% CAGR through 2033, fueled by wallet integration and inclusion programs.

5. Which payment types dominate the Mexico cards and payments market?

Debit cards lead volume in the Mexico cards and payments market, with credit growing via retail and aggregators.

6. What trends shape the Mexico cards and payments market?

Aggregators and QR payments trend in the Mexico cards and payments market amid e-commerce surge.

7. How competitive is the Mexico cards and payments market?

Fintechs challenge banks in the Mexico cards and payments market with innovative prepaid solutions.

8. What role does debit play in the Mexico cards and payments market?

Debit shows 14.3% value growth in the Mexico cards and payments market for everyday spending.

9. Are neobanks key in the Mexico cards and payments market?

Neobanks boost inclusion in the Mexico cards and payments market via accessible card issuance.

10. How does e-commerce affect the Mexico cards and payments market?

E-commerce accelerates digital adoption in the Mexico cards and payments market across platforms.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com