Global Aerial Imaging Market Size, Share, Trends, & Growth Analysis Report, Segmented By Platform (UAV/Drone, Helicopter, Fixed-Wing Aircraft), Imaging Type (Oblique Imaging, Vertical Imaging), Application (Conservation & Research, Urban Planning, Surveillance & Monitoring, Energy & Resource Management, Disaster Management, Geospatial Mapping), End-Use (Oil & Gas, Archaeology & Civil Engineering, Agriculture & Forestry, Military & Defense, Energy, Government), & Region, Industry Forecast From 2026 to 2034

Global Aerial Imaging Market Size

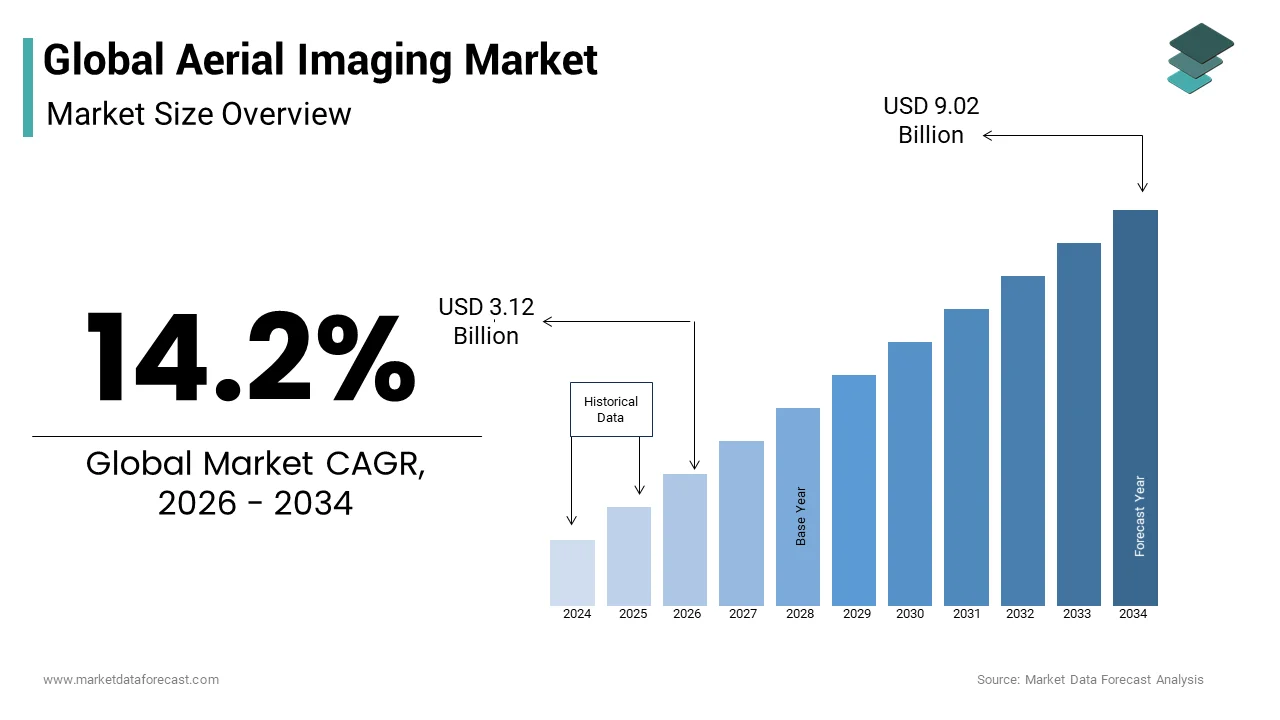

The global aerial imaging market was valued at USD 2.39 billion in 2024 and is anticipated to reach USD 2.73 billion in 2025 to USD 7.90 billion by 2033, growing at a CAGR of 14.2% during the forecast period from 2025 to 2033.

Current Intro/Definition Of The Aerial Imaging Market

Aerial imaging is the process of capturing photographs or sensor data of the Earth's surface from an elevated perspective. This domain provides critical visual and spectral information used for mapping surveying monitoring and inspection across diverse industries such as agriculture construction defense and environmental management. The technology has evolved from simple photographic documentation to sophisticated multispectral and hyperspectral analysis enabling detailed insights into land use crop health and infrastructure integrity. According to NASA's Earth Science Data Systems (ESDS), the agency ingests and processes over 100 terabytes of Earth science data daily, reflecting the massive scale of contemporary satellite and remote sensing data generation. As per the Federal Aviation Administration (FAA), there are more than 350,000 registered commercial drones active within the United States, providing extensive domestic infrastructure for low-altitude aerial imaging and enterprise surveying operations. The integration of artificial intelligence and machine learning algorithms has further enhanced the value proposition by automating feature extraction and anomaly detection from vast image datasets. Data from the European Space Agency indicates that the Copernicus program provides free and open access to petabytes of earth observation data which serves as a foundational resource for commercial aerial imaging applications. This convergence of advanced sensor technology regulatory evolution and computational power establishes aerial imaging as a pivotal component of modern digital infrastructure and decision making processes globally.

MARKET DRIVERS

Rapid Adoption of Precision Agriculture and Crop Monitoring

The rapid adoption of precision agriculture practices drives the growth of the aerial imaging market. This is driven by the need to optimize crop yields and reduce resource waste. Farmers increasingly rely on multispectral and thermal imagery captured by drones to assess plant health soil moisture levels and pest infestations with high spatial resolution. According to the Food and Agriculture Organization of the United Nations global food production must increase by 60 percent by 2050 to feed a growing population necessitating efficient farming techniques. Environmental metrics aggregated by the Association of Equipment Manufacturers (AEM) demonstrate that widespread adoption of precision agriculture technologies can optimize input efficiency, offering potential yield increases up to 20% and reducing chemical fertilizer applications by up to 15%. Furthermore the ability to detect early signs of disease or stress allows for timely intervention preventing significant losses. As per sources the use of normalized difference vegetation index derived from aerial images has become standard practice for large scale farm management in North America and Europe. This data driven approach enables farmers to make informed decisions regarding irrigation planting and harvesting thereby enhancing profitability and sustainability. The increasing availability of affordable drone platforms and user friendly analytics software further accelerates the integration of aerial imaging into mainstream agricultural operations.

Expansion Of Infrastructure Development And Urban Planning Initiatives

The expansion of infrastructure development and urban planning initiatives significantly fuels the growth of the global aerial imaging market. This is due to the need for accurate topographic data and progress monitoring. Governments and private developers utilize high resolution orthomosaics and 3D models generated from aerial surveys to design roads bridges and residential complexes with greater precision. the G20’s Global Infrastructure Hub (GI Hub) project that international infrastructure investment demands will reach $94 trillion by 2040, establishing a massive operational window for downstream surveying and geospatial visualization companies. DroneDeploy shows that construction firms integrating specialized aerial drone imagery for job site mapping can achieve up to a 50% reduction in tracking errors and accelerate timeline scheduling by 20%. Additionally municipal authorities employ aerial data for zoning compliance traffic analysis and disaster response planning ensuring efficient urban management. As per sources, the integration of building information modeling with aerial photogrammetry allows for real time comparison between planned and actual construction progress. This capability enhances accountability and reduces cost overruns in large scale projects. The growing emphasis on smart city development further amplifies the need for continuous aerial monitoring to manage utilities transportation networks and public spaces effectively. Consequently, the construction and urban planning sectors remain key drivers of aerial imaging market growth.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Airspace Restrictions

Stringent regulatory frameworks and airspace restrictions hamper the expansion of the aerial imaging market. This is particularly true for unmanned aerial vehicle operations in populated areas. Governments worldwide have implemented strict rules regarding flight altitude no fly zones and pilot certification to ensure public safety and national security. According to Federal Aviation Administration (FAA) Part 107 guidelines, commercial operators must secure explicit individual regulatory waivers to fly Beyond Visual Line of Sight (BVLOS), representing a complex vetting process for expanding enterprise drone programs. Data from the European Union Aviation Safety Agency indicates that compliance with new drone regulations requires significant investment in remote identification systems and geo fencing technology increasing operational costs. Furthermore varying regulations across different countries create challenges for multinational companies seeking to standardize their aerial imaging services. Drone Analyst reveal that ongoing compliance uncertainty and rigid flight restrictions represent the largest structural hurdle for over half of surveyed drone operators, bottlenecking corporate scaling initiatives. Privacy concerns also lead to local ordinances restricting data collection over private properties further complicating deployment strategies. These legal and bureaucratic hurdles slow down market entry and innovation forcing companies to navigate a fragmented regulatory landscape that hinders the seamless integration of aerial imaging technologies into various industries.

High Initial Investment And Operational Costs

High initial investment and ongoing operational costs pose significant barriers to entry for small and medium sized enterprises looking to adopt aerial imaging technologies, which impedes the expansion of the global market. Acquiring high quality drones equipped with advanced sensors such as LiDAR multispectral cameras and thermal imagers requires substantial capital expenditure. SkyWatch indicates that procuring professional-grade RTK enterprise drone setups routinely requires capital investments of $10,000 to $50,000 per unit, independent of ongoing cloud data processing subscription expenditures. Furthermore the need for skilled personnel to operate equipment and process complex geospatial data adds to the labor costs. Data from the Bureau of Labor Statistics shows that specialized roles such as photogrammetrists and GIS analysts command higher salaries due to the technical expertise required. Additionally insurance premiums for commercial drone operations have risen as liability risks increase further straining budgets. Strategic surveys published by Drone Analyst show that approximately 40% of enterprise organizations list initial scaling costs and software stack fees as the primary reason for postponing aerial imaging integration. The total cost of ownership including battery replacements software updates and data storage also contributes to financial pressure. These economic constraints limit the accessibility of advanced aerial imaging tools to larger corporations with deeper pockets leaving smaller players at a competitive disadvantage and slowing overall market penetration.

MARKET OPPORTUNITIES

Integration With Artificial Intelligence And Automated Analytics

The integration of artificial intelligence and automated analytics offers a transformative opportunity for the aerial imaging market. This enhances data processing speed and accuracy. AI algorithms can automatically identify objects detect changes and classify land cover types from vast amounts of imagery reducing the need for manual interpretation. Research indicates that integrating computer vision and automated image analysis into data pipelines can reduce claims and data processing times by up to 80 percent, driving rapid decision-making. Data from NVIDIA indicates that deep learning models trained on aerial datasets achieve over 95 percent accuracy in detecting infrastructure defects such as cracks in bridges or leaks in pipelines. Furthermore, predictive analytics powered by machine learning can forecast trends such as crop yield fluctuations or urban expansion patterns providing valuable insights for stakeholders. Research shows that the demand for AI-driven geospatial analytics and GeoAI platforms has expanded rapidly as enterprises scale up autonomous feature extraction from raw aerial arrays. This technological synergy enables new business models such as subscription based monitoring services where clients receive regular automated reports. By leveraging AI, companies can offer higher-value services with lower labor costs. This opens new revenue streams and expands the applicability of aerial imaging across diverse sectors, including insurance, energy, and environmental conservation.

Growth In Environmental Monitoring And Climate Change Mitigation

The growing focus on environmental monitoring and climate change mitigation provides substantial prospects for the aerial imaging market. This is driven by governments and organizations seeking data-driven solutions to address ecological challenges. Aerial imagery provides critical information for tracking deforestation monitoring glacier retreat and assessing carbon sequestration in forests and wetlands. According to the Intergovernmental Panel on Climate Change remote sensing is essential for verifying national greenhouse gas inventories and monitoring land use changes. Data from the Global Forest Watch platform shows that satellite and aerial data help detect illegal logging activities in real time enabling faster response from authorities. Furthermore aerial surveys are used to monitor wildlife populations and assess the impact of natural disasters such as floods and wildfires. Sources confirm that the international demand for high-frequency, low-latency Earth Observation data for climate and ESG compliance modeling has expanded significantly. Carbon credit markets also rely on accurate aerial measurements to verify offset projects creating a new economic incentive for data collection. Aerial imaging providers can tap into a rapidly expanding market segment by supporting sustainability goals and regulatory compliance. This market growth is primarily driven by global environmental priorities and corporate social responsibility initiatives.

MARKET CHALLENGES

Data Management And Storage Complexities

Data management and storage complexities are a significant challenge for the aerial imaging market. This is because of the massive volume of high-resolution images and point clouds generated by modern sensors. A single drone flight can produce hundreds of gigabytes of raw data which requires robust infrastructure for storage processing and retrieval. The International Data Corporation (IDC) show the global datasphere scaling to 175 zettabytes, driven significantly by the proliferation of unstructured visual assets like aerial photography, LiDAR, and satellite maps. Managing this deluge of information requires scalable cloud solutions and high performance computing resources which can be costly and technically demanding. A study reveals that cloud-based hosting, redundancy, and data lifecycle retention pipelines for high-resolution imagery sets can represent up to 30 percent of ongoing technology expenditures. Furthermore ensuring data security and privacy while complying with regulations such as GDPR adds another layer of complexity. The Cloud Security Alliance (CSA) stress that protecting high-fidelity industrial visual maps is critical, as breaches of enterprise data repositories can trigger severe legal liabilities and compromise sensitive telemetry infrastructure. The lack of standardized data formats also hinders interoperability between different software platforms making it difficult to integrate aerial data with other enterprise systems. These technical and logistical challenges require continuous investment in IT infrastructure and expertise straining resources for many aerial imaging providers.

Limited Battery Life and Flight Endurance

Limited battery life and flight endurance heavily restrict the operational efficiency of unmanned aerial vehicles, which slows down the expansion of the aerial imaging market. Consequently, these limitations impact their use as the primary platforms for low-altitude aerial imaging. Most commercial drones have flight times ranging from 20 to 40 minutes requiring frequent battery swaps and ground interruptions during large area surveys. The National Renewable Energy Laboratory (NREL) underscores that current lithium-based battery configurations face rigid chemical energy-density thresholds, limiting multi-rotor flight endurance during continuous high-wind or heavy-payload missions. DJI Enterprise notes that sub-zero ambient temperatures can significantly degrade lithium cell performance, mandating internal self-heating configurations to safeguard flight time and avoid abrupt power depletion. This constraint increases the time and labor required to complete mapping missions affecting project timelines and costs. According surveys, cell endurance and limited flight times continue to be identified by roughly 70 percent of field operators as a principal technical barrier to scaling remote sensing services. While advancements in hydrogen fuel cells and solar powered drones are emerging they are not yet widely adopted due to high costs and technical immaturity. The need for multiple drones and pilots to cover large areas also increases logistical complexity. Flight endurance is a persistent bottleneck for aerial imaging operations. It currently restricts the productivity and scalability of these missions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 14.2% |

| Segments Covered | By Platform, Imaging Type, End User, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | PrecisionHawk, Getmapping, Cooper Aerial Surveys, Kucera International, DJI, GeoVantage, Fugro, DroneDeploy, 3D Robotics, Airobotics, Digital Aerial Solutions, Nearma, Eagle View Technologies, and Google. |

SEGMENTAL ANALYSIS

By Platform Insights

The unmanned aerial vehicles or drones segment dominated the aerial imaging market and accounted for a substantial share in 2025. This dominance of the segment was driven by its cost effectiveness operational flexibility and ability to capture high resolution data at low altitudes. The widespread availability of consumer and enterprise-grade drones drives the domination of this segment. Unlike manned aircraft, these devices require almost no physical infrastructure. According to recent data from the Federal Aviation Administration (FAA), there are more than 800,000 total registered drones active within the United States, with commercial enterprise aircraft accounting for over 350,000 systems of that multi-use fleet. A study demonstrates that deploying autonomous unmanned aircraft systems can cut geographic data-gathering overhead by roughly 50 percent compared to conventional manned survey flights, reducing adoption barriers for smaller enterprises. Furthermore, drones can operate in confined spaces and hazardous environments such as inspecting power lines or monitoring active construction sites without risking human safety. As per the Association for Unmanned Vehicle Systems International the versatility of drone platforms allows for the integration of diverse sensors including LiDAR multispectral and thermal cameras enabling multifaceted data acquisition. The ease of deployment and rapid turnaround time for data processing further solidify the position of drones as the primary platform for modern aerial imaging applications.

On the other hand, the other platform types segment is estimated to register the fastest CAGR of 12.5% during the forecast period. This rapid expansion of the segment is fueled by advancements in stratospheric balloon technology and the proliferation of small satellite cubesats which offer persistent wide area monitoring capabilities. Novaspace show that the global fleet of active Earth observation satellites has more than doubled in recent years, driving massive increases in global revisit frequency and lowering imaging turnaround latencies. Data from World View Enterprises shows that stratospheric balloons can remain airborne for weeks capturing ultra high resolution imagery at a fraction of the cost of satellite launches. These platforms bridge the gap between the detailed but limited coverage of drones and the broad but lower resolution coverage of traditional satellites. As per research, the declining cost of launching small satellites has democratized access to space based imaging enabling new business models for real time global monitoring. The ability of these alternative platforms to provide continuous surveillance over large geographic areas drives their accelerated adoption in sectors such as defense agriculture and climate science.

By Application Insights

In 2025, the geospatial mapping segment held the majority share of 35.7% of the aerial imaging market because of its fundamental role in creating accurate base maps for navigation land management and urban planning. The increasing demand for high-precision topographic data is further driving the dominance of this segment. Consequently, this data is heavily utilized to support infrastructure development and property delineation. According to the United States Geological Survey national mapping programs rely heavily on aerial imagery to update geographic information systems with current land cover and elevation data. A study reveals that high-resolution, aerial-derived orthomosaics serve as the primary foundational base-map layer across the vast majority of municipal, regional, and national government geographic databases. Furthermore the integration of photogrammetry software with drone data has streamlined the map creation process allowing for centimeter level accuracy in shorter timeframes. As per the International Society for Photogrammetry and Remote Sensing the automation of feature extraction from aerial images has significantly reduced the manual labor required for map production. This efficiency combined with the critical need for up to date spatial information ensures that geospatial mapping remains the cornerstone of the aerial imaging industry.

However, the environmental monitoring segment is anticipated to witness the fastest CAGR of 14.2% from 2026 to 2034 owing to urgent global concerns regarding climate change deforestation and biodiversity loss. Governments and non governmental organizations are increasingly utilizing aerial data to track ecosystem health measure carbon stocks and detect illegal logging activities. According to the Intergovernmental Panel on Climate Change remote sensing is essential for verifying national greenhouse gas inventories and monitoring land use changes Global Forest Watch shows that satellite and aerial data help detect forest loss in near real time enabling faster response from conservation authorities. Furthermore aerial imaging is used to monitor water quality glacier retreat and coastal erosion providing critical insights for climate adaptation strategies. Novaspace indicate that commercial demand for high-revisit Earth observation datasets for environmental, social, and governance (ESG) compliance and climate metrics has accelerated significantly. The ability to assess large inaccessible areas without physical intrusion makes aerial imaging an indispensable tool for environmental scientists and policymakers driving the rapid growth of this segment.

By End User Insights

The construction segment led the aerial imaging market and captured a 30.5% share in 2025. This leading position of the segment was attributed to the need to improve project efficiency, reduce costs, and enhance safety on complex construction sites. Such market share is due to the extensive use of drones for site surveying, progress monitoring, and volume calculations. DroneDeploy show that implementing automated aerial drone mapping instead of traditional ground methods allows construction teams to reduce initial site surveying timelines by roughly 50 percent. Data from Autodesk indicates that the integration of building information modeling with aerial photogrammetry allows for real time comparison between planned and actual construction progress helping to identify deviations early. Furthermore drones enable safe inspection of hard to reach areas such as high rise facades and bridge undersides reducing the risk of accidents for workers. Sources reveal that more than 60 percent of large-scale construction enterprises have integrated drone technology into their standard workflows for site documentation and safety reviews. The tangible return on investment through improved productivity and risk mitigation ensures that construction remains the primary driver of aerial imaging adoption.

But the agriculture segment is likely to experience the fastest CAGR of 15.8% between 2026 and 2034. This quick surge of the segment is fuelled by the widespread adoption of precision farming techniques to optimize crop yields and resource usage. Farmers are increasingly relying on multispectral and thermal imagery to assess plant health soil moisture and pest infestations with high spatial resolution. According to the Food and Agriculture Organization of the United Nations global food production must increase by 60 percent by 2050 necessitating efficient farming practices supported by data. The Association of Equipment Manufacturers (AEM) indicate that adopting precision agriculture tools allows farms to maximize input efficiencies, driving prospective crop yield boosts of up to 20% and chemical input reductions of up to 15%. Furthermore, the ability to detect early signs of disease allows for timely intervention preventing significant losses. As per sources companies the use of normalized difference vegetation index derived from aerial images has become standard practice for large scale farm management. This data driven approach enhances profitability and sustainability driving the rapid growth of aerial imaging in the agricultural sector.

REGIONAL ANALYSIS

North America Market Analysis

North America was the top performer in the global aerial imaging market and accounted for a 38.1% share in 2025. This supremacy of the North American was driven by early technology adoption robust regulatory frameworks and significant investment in research and development. The market status in this region is characterized by a mature drone ecosystem and widespread integration of aerial data into government and commercial workflows. According to data tracking from the Federal Aviation Administration (FAA), there are over 300,000 registered commercial drones operating in the United States airspace, highlighting a massive domestic infrastructure for aerial data collection. Data from the United States Geological Survey shows that federal agencies extensively use aerial imagery for natural resource management disaster response and infrastructure monitoring. Furthermore the presence of major technology companies and startups fosters innovation in sensor technology and data analytics. As highlighted during the Commercial UAV Expo, North American enterprise sectors are aggressively advancing the commercial implementation of UAS technologies for autonomous structural inspection and precision agriculture workflows.The strong intellectual property protection and venture capital funding further support the growth of the aerial imaging industry in this region.

Europe Market Analysis

Europe was the next prominent region in the global aerial imaging market and captured a 28.6% share in 2025. This growth of the European market was supported by stringent environmental regulations and strong government support for digital transformation. The market status in this region is defined by the European Union’s Copernicus program which provides free and open access to earth observation data fostering innovation in downstream services. According to the European Union Aviation Safety Agency harmonized drone regulations across member states have simplified cross border operations encouraging market expansion. Driven by initiatives from the European Space Agency (ESA), Europe maintains strong technical leadership in specialized sensor analytics and environmental observation via the Copernicus Sentinel satellite program to optimize global agriculture resilience. Furthermore the emphasis on sustainable urban planning and infrastructure maintenance drives demand for high resolution aerial surveys. As per sources, Europe is a hub for satellite based aerial imaging technologies contributing significantly to global earth observation capabilities. The focus on privacy and data security also shapes the development of compliant aerial imaging solutions in the region.

Asia Pacific Market Analysis

Asia Pacific is the fastest growing region in the global aerial imaging market due to rapid urbanization large scale infrastructure projects and increasing adoption of precision agriculture. Massive investments in smart city initiatives and digital economy strategies, particularly across China, India, and Japan, are the primary drivers of market growth in this region. According to the Asian Development Bank infrastructure investment needs in Asia are estimated to reach 26 trillion USD by 2030 creating substantial demand for aerial surveying and monitoring services. The Civil Aviation Administration of China (CAAC) confirms massive domestic escalation in the low-altitude economy, with registered civil drone systems exceeding 1.27 million aircraft across thousands of operations. Furthermore governments in Southeast Asia are utilizing aerial data for disaster management and forest conservation efforts. As per sources, the adoption of drone technology in agriculture is accelerating in India and Australia to address labor shortages and improve productivity. The combination of demographic growth and technological leapfrogging positions Asia Pacific as a key engine for future market expansion.

Latin America Market Analysis

Latin America grew steadily in the global aerial imaging market owing to the need for efficient natural resource management and agricultural optimization. The regional market shows growing adoption of drone technology in large scale farming operations particularly in Brazil and Argentina. According to the Inter American Development Bank digital technologies are being increasingly used to enhance productivity in the agricultural sector which is a major contributor to regional GDP. Data from local agritech startups shows that multispectral imaging is helping farmers monitor soybean and corn crops more effectively reducing input costs. Furthermore mining and oil and gas companies are utilizing aerial inspections to improve safety and compliance in remote locations. As per research, regulatory frameworks are evolving to support commercial drone operations although challenges remain in terms of infrastructure and skilled personnel. The potential for growth is significant as economic conditions improve and awareness of aerial imaging benefits increases among key industries.

Middle East And Africa Market Analysis

The Middle East and Africa region holds a notable share of the global aerial imaging market due to mega infrastructure projects and security surveillance needs. The market status in this region is characterized by high value government contracts and ambitious smart city developments particularly in the Gulf Cooperation Council countries. According to the Saudi Arabian government Vision 2030 initiatives include extensive use of geospatial data for urban planning and tourism development. Data from the United Arab Emirates shows that aerial imaging is integral to the construction of iconic projects such as Expo City and various renewable energy installations. In Africa the focus is on using aerial data for agricultural extension services and wildlife conservation. In alignment with the African Union (AU) Agenda 2063, the AU promotes satellite remote sensing frameworks to drive climate adaptation, establish early drought warnings, and safeguard multi-national agricultural food security programs. While market size is smaller compared to other regions the strategic importance of aerial imaging for national development and security ensures continued investment and growth opportunities.

COMPETITIVE LANDSCAPE

The competition in the Aerial Imaging Market is characterized by the presence of established aerospace giants alongside agile technology startups who strive to differentiate themselves through innovation and specialized applications. Major players leverage their extensive manufacturing capabilities and global distribution networks to offer comprehensive hardware and software ecosystems. Meanwhile niche firms focus on developing proprietary algorithms for specific industries such as precision agriculture or infrastructure inspection. The market is highly dynamic with rapid technological advancements in sensor miniaturization and autonomous flight systems driving continuous product evolution. Competitive dynamics are influenced by regulatory compliance data security standards and the ability to provide actionable insights rather than just raw images. Strategic alliances between hardware manufacturers and software developers are increasingly common to deliver integrated solutions. Price competition remains intense in the consumer segment while enterprise clients prioritize reliability and support. This intense rivalry fosters rapid innovation and improves the overall quality and accessibility of aerial imaging technologies for diverse global applications.

KEY MARKET PLAYERS

Some noteworthy players operating in the global aerial imaging market include

- PrecisionHawk

- Getmapping

- Cooper Aerial Surveys

- Kucera International

- DJI

- GeoVantage

- Fugro

- DroneDeploy

- 3D Robotics

- Airobotics

- Digital Aerial Solutions,

- Nearma

- Eagle View Technologies

Top Players In The Market

- DJI Holdings is a dominant force in the global aerial imaging market renowned for its comprehensive portfolio of consumer and enterprise drones. The company provides high resolution imaging platforms equipped with advanced gimbals and sensors that cater to industries such as agriculture construction and public safety. Recent actions include the launch of the Matrice 350 RTK which offers enhanced flight time and modular payload capabilities for professional users. DJI has also expanded its software ecosystem with AI powered analytics tools that automate data processing and feature extraction. These initiatives strengthen its market position by delivering integrated hardware and software solutions that improve operational efficiency and data accuracy for commercial clients worldwide while maintaining technological leadership through continuous innovation.

- Trimble Inc contributes significantly to the global aerial imaging market by integrating drone captured data with its robust geospatial and building information modeling software suites. The company focuses on providing end to end workflows that transform raw aerial imagery into actionable insights for surveying engineering and construction projects. Recently Trimble strengthened its position by acquiring specialized photogrammetry software developers to enhance its reality capture capabilities. They have also introduced cloud based collaboration platforms that allow teams to access and analyze aerial data in real time from any location. These strategic moves enable Trimble to offer seamless interoperability between field data collection and office based design processes thereby enhancing productivity and decision making for infrastructure and land development professionals globally.

- Planet Labs PBC plays a pivotal role in the global aerial imaging market by operating the largest constellation of earth observation satellites that provide daily global coverage. The company delivers high frequency medium resolution imagery that complements low altitude drone data for large scale monitoring applications in agriculture forestry and defense. Recent actions include the successful deployment of its Pelican satellite series which offers improved spectral resolution and data downlink speeds. Planet has also partnered with major cloud providers to integrate its data feeds directly into artificial intelligence and machine learning pipelines. These efforts enhance the accessibility and utility of their imagery allowing customers to detect changes and trends more rapidly. Planet combines space-based persistence with advanced analytics. This dual capability strengthens its position as a key provider of comprehensive geospatial intelligence solutions.

Major Strategies Used By Key Market Participants

Key players in the Aerial Imaging Market primarily focus on vertical integration and strategic partnerships to maintain their competitive edge. Companies invest heavily in research and development to create advanced sensors and artificial intelligence algorithms that enhance data accuracy and processing speed. Collaborations with cloud computing providers facilitate scalable storage and analysis solutions for massive geospatial datasets. Additionally manufacturers emphasize user friendly software interfaces to lower the barrier to entry for non technical users. Expanding service offerings to include managed data analytics and consulting helps capture higher value segments. These strategies enable companies to address diverse industry needs while ensuring reliable and efficient delivery of aerial imaging solutions across global markets.

RECENT MARKET NEWS

- In May 2023, DJI launched the Matrice 350 RTK commercial drone platform, introducing an IP55 protection rating, up to 55 minutes of flight time, and multi-payload support to expand its presence in industrial mapping and surveying workflows.

- In May 2023, Trimble Inc. expanded its geospatial reality capture portfolio by launching the Trimble X9 3D laser scanning system, engineered to deliver shorter scan times and higher accuracy for surveying, engineering, and construction professionals.

MARKET SEGMENTATION

This research report on the global aerial imaging market has been segmented and sub-segmented based on the platform, imaging type, application, and region.

By Platform

- UAV/Drone

- Helicopter

- Fixed-wing Aircraft

By Imaging Type

- Oblique Imaging

- Vertical Imaging

By Application

- Conservation & Research

- Urban Planning

- Surveillance & Monitoring

- Energy & Resource Management

- Disaster Management

- Geospatial Mapping

By End User

- Oil & Gas

- Archaeology & Civil Engineering

- Agriculture & Forestry

- Military & Defense

- Energy

- Government

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

Why is the aerial imaging market experiencing rapid growth across industries?

The market is growing rapidly due to increasing adoption of drones, advancements in geospatial technologies, rising demand for high-resolution mapping, and expanding applications across commercial and government sectors.

What is aerial imaging and how is it used in modern data collection?

Aerial imaging involves capturing photographs and geospatial data from aircraft, drones, satellites, or helicopters to support mapping, monitoring, surveying, and analytical applications.

Which industries are driving the highest demand for aerial imaging solutions?

Construction, agriculture, defense, mining, urban planning, energy, environmental monitoring, and disaster management sectors are driving the highest demand.

How does aerial imaging improve decision-making for businesses and governments?

It provides accurate visual data, real-time monitoring capabilities, detailed geographic insights, and improved situational awareness for planning and operational decisions.

What technologies are transforming the aerial imaging market?

Drone-based imaging systems, LiDAR technology, artificial intelligence, machine learning, hyperspectral imaging, and cloud-based geospatial analytics are transforming the market.

Why are drones becoming a preferred platform for aerial imaging applications?

Drones offer cost-effective deployment, high operational flexibility, rapid data collection, and access to areas that may be difficult to survey using conventional methods.

Which aerial imaging application segment holds the largest market share?

Mapping and surveying applications hold a significant share due to increasing infrastructure development, land management projects, and urban planning initiatives.

How is artificial intelligence enhancing aerial imaging capabilities?

AI enables automated image analysis, object detection, change monitoring, predictive insights, and faster processing of large volumes of aerial data.

What challenges could affect the growth of the aerial imaging market?

Regulatory restrictions, data privacy concerns, adverse weather conditions, high equipment costs, and airspace management complexities could affect market growth.

Which regions are expected to lead the global aerial imaging market?

North America remains a major market due to technological advancements, while Europe and Asia Pacific are witnessing strong growth driven by infrastructure development and drone adoption.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com