Global Aircraft De-Icing Market Size, Share, Trends & Growth Forecast Report By Operation Mode, By De-Icing Method, and By Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) – Industry Analysis and Forecast, 2026 to 2034

Global Aircraft De-Icing Market Report Summary

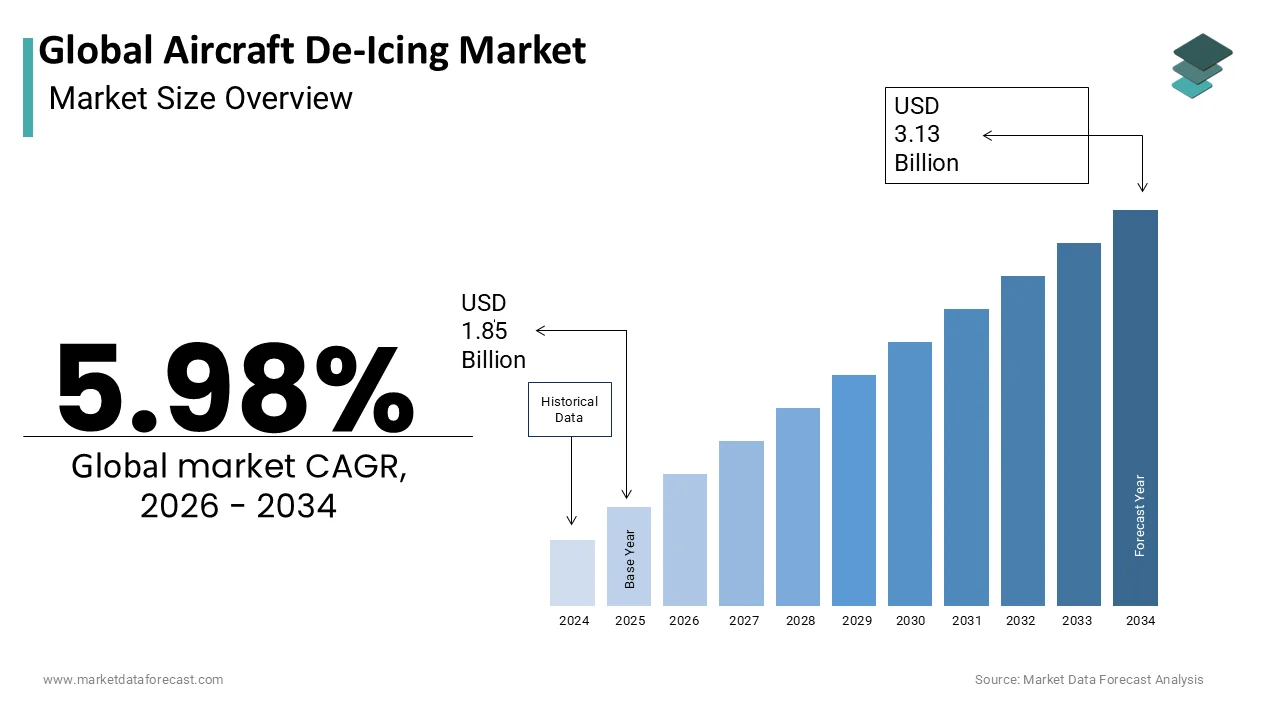

The Global Aircraft De-Icing Market was valued at USD 1.85 billion in 2025 and is projected to reach USD 3.13 billion by 2034, growing from USD 1.97 billion in 2026 at a CAGR of 5.98% during the forecast period. Growth is driven by strict aviation safety mandates prohibiting takeoff with surface ice, rising air traffic in cold-climate hubs, and expanding winter operations infrastructure. Increasing adoption of automation and eco-friendly fluids is further shaping market development.

Key Market Trends

- Rising demand for bio-based and biodegradable de-icing fluids

- Growing adoption of automated and robotic de-icing systems

- Expansion of dedicated de-icing pads and fluid storage at major airports

- Increasing use of ice-detection sensors and avionics-integrated in-flight systems

- Growing environmental compliance pressure driving closed-loop fluid recovery

Segmental Insights

- Based on operation mode, ground spray operations dominated the market in 2025, driven by regulatory mandates requiring complete removal of frozen contaminants before takeoff.

- Based on de-icing method, Type IV fluid held the leading share in 2025, supported by its extended holdover time in severe freezing precipitation.

- In-flight systems is the fastest-growing operation mode segment, projected at a CAGR of 7.1%, driven by advances in ice-detection sensors and avionics integration.

Regional Insights

- North America led the market in 2025 by holding 33.3% of the global market share, supported by mature winter infrastructure and high commercial air traffic volume.

- Europe holds a significant share, driven by stringent environmental regulations pushing adoption of bio-based fluids and closed-loop recovery systems.

- Asia Pacific is a prominent market supported by expanding cold-climate hub traffic and infrastructure investment.

- Latin America contributes notably due to growing air cargo and passenger traffic.

- Middle East and Africa is expected to witness considerable growth during the forecast period, driven by expanding aviation infrastructure and fleet modernization.

Competitive Landscape

The market is highly competitive, with manufacturers focusing on product efficacy, environmental compliance, and technical support. Companies are investing in sustainable fluid formulations and strategic partnerships with airport authorities to offer holistic winter operations solutions.

Prominent players in the market include Clariant AG, Kilfrost Limited, The Dow Chemical Company, BASF SE, Cryotech Deicing Technology, LyondellBasell Industries N.V., Integrated Deicing Services (IDS), JBT Corporation (John Bean Technologies), Global Ground Support LLC, Textron GSE (TUG Technologies), Vestergaard Company A/S, and UTC Aerospace Systems (Collins Aerospace).

Global Aircraft De-Icing Market Size

The Global Aircraft De-Icing Market is projected to grow from USD 1.85 billion in 2025 to USD 1.97 billion in 2026 and reach USD 3.13 billion by 2034, registering a CAGR of 5.98% during the forecast period from 2026 to 2034.

Aircraft de-icing is designed to remove ice, snow, and frost from aircraft surfaces before takeoff, ensuring aerodynamic integrity and flight safety. This critical operational segment utilizes glycol-based fluids, such as propylene glycol and ethylene glycol, along with heated application systems to melt frozen contaminants and provide anti-icing protection during ground hold periods. The necessity of these procedures is dictated by strict aviation regulations that prohibit takeoff with any accumulation of ice on critical surfaces. According to the Federal Aviation Administration, even a thin layer of ice as rough as sandpaper can reduce lift by 30% and increase drag by up to 40%, potentially leading to catastrophic stall conditions. Furthermore, as per National Transportation Safety Board historical accident data, icing-related incidents have been a contributing factor in numerous commercial aviation disasters, underscoring the absolute nature of de-icing protocols. The International Civil Aviation Organization mandates that all member states enforce rigorous winter operations standards, requiring certified de-icing facilities at airports experiencing freezing precipitation. With global air traffic projected to double over the next two decades, according to the International Air Transport Association, the frequency of winter operations in northern hemisphere hubs will intensify. This regulatory framework, combined with the physical realities of atmospheric physics, creates an immutable demand for effective de-icing solutions across commercial, cargo, and general aviation sectors worldwide.

MARKET DRIVERS

Stringent Regulatory Mandates and Safety Compliance Requirements

The uncompromising regulatory environment governing aviation safety is primarily boosting the expansion of the aircraft de-icing market. Aviation authorities globally enforce zero-tolerance policies regarding ice accumulation on aircraft surfaces before departure. According to the European Union Aviation Safety Agency, operators must ensure that aircraft are free of frozen contaminants through visual inspections or approved detection methods before every flight in winter conditions. Failure to comply results in severe penalties, which is grounding of fleets and potential revocation of operating certificates. The Federal Aviation Administration requires that all de-icing activities adhere to specific holdover time guidelines, which dictate how long a treated aircraft remains protected under prevailing weather conditions. These regulations necessitate the use of certified Type I, Type II, Type III, and Type IV fluids, each engineered for specific viscosity and freeze-point requirements. As per the International Civil Aviation Organization Annex 6 standards, international commercial air transport mandates that operators establish comprehensive winter operation programs, including staff training and equipment maintenance. The legal liability associated with icing-related accidents drives airlines and airport authorities to invest heavily in high-quality de-icing fluids and advanced application technologies. This regulatory pressure ensures that de-icing is not merely an operational choice but a mandatory compliance activity, creating a stable and inelastic demand base regardless of economic fluctuations in the broader aviation sector.

Increasing Air Traffic Volume in Cold Climate Regions

North America, Northern Europe, and parts of Asia are likely to see sustained demand for de-icing infrastructure as these regions continue to prioritize flight reliability during increasingly busy winter seasons, which is likely to aid the aircraft de-icing market expansion. The substantial growth in passenger and cargo air traffic in regions prone to severe winter weather significantly amplifies the requirement for de-icing services. Northern hemisphere markets, including North America, Northern Europe, and parts of Asia, experience extended winter seasons with frequent snowfall and freezing rain events. According to the International Air Transport Association, total global air passenger numbers are expected to reach 8.2 billion by 2037, with a significant portion of this growth occurring in cold-climate hubs such as Chicago, Toronto, Frankfurt, and Beijing. These airports operate year-round, necessitating robust de-icing infrastructure to maintain schedule reliability during winter months. According to the Federal Aviation Administration, weather-related delays account for approximately 15% of all flight delays in the United States, with winter storms being a major contributor. To mitigate these disruptions, airlines increase their reliance on efficient de-icing operations to minimize turnaround times. Furthermore, the expansion of cargo logistics networks driven by e-commerce requires uninterrupted air freight services regardless of weather conditions. As per the Airports Council International, many major airports are expanding their de-icing pads and fluid storage capacities to accommodate larger fleets and higher flight frequencies. This operational scaling directly correlates with increased consumption of de-icing fluids and utilization of mechanical removal equipment, driving sustained market expansion in geographies with harsh winter climates.

MARKET RESTRAINTS

Environmental Regulations and Chemical Discharge Restrictions

Strict environmental regulations concerning the discharge of glycol-based de-icing fluids pose a significant restraint on the aircraft de-icing market. Propylene glycol and ethylene glycol, while effective at melting ice, are organic compounds that consume large amounts of oxygen when they decompose in water bodies, leading to hypoxic conditions that harm aquatic life. According to the Environmental Protection Agency, airports in the United States must obtain National Pollutant Discharge Elimination System permits to manage stormwater runoff containing de-icing chemicals. Compliance with these permits requires expensive infrastructure, such as retention basins, filtration systems, and biological treatment facilities, which increase operational costs for airport authorities. The European Union Water Framework Directive similarly imposes stringent limits on the concentration of organic pollutants in surface waters, forcing airports in countries like Germany and Sweden to invest heavily in closed-loop recovery systems. As per the Canadian Council of Ministers of the Environment, several provinces have implemented bans on the use of ethylene glycol due to its higher toxicity compared to propylene glycol. These regulatory pressures limit the choice of available chemicals and necessitate costly waste management protocols. Smaller regional airports often struggle to afford the required environmental mitigation infrastructure, leading to operational bottlenecks or reduced service capabilities during winter storms. This environmental compliance burden acts as a financial and operational brake on market expansion, particularly for facilities with limited capital resources.

High Operational Costs and Fluid Price Volatility

The substantial financial burden associated with de-icing operations is further hindering the global market expansion. De-icing fluids are petroleum-derived products, making their prices highly susceptible to fluctuations in global crude oil markets. According to data from the U.S. Energy Information Administration, energy-related input costs can significantly impact the final price of chemical formulations, which can vary considerably during periods of market instability. A single wide-body aircraft may require up to 1,000 gallons of de-icing fluid during heavy snow events, costing thousands of dollars per operation. For airlines operating on thin margins, these recurring winter expenses can severely impact profitability. Additionally, the maintenance and deployment of specialized de-icing vehicles equipped with heated booms and precision nozzles require significant capital investment and skilled personnel. The Air Transport Action Group notes that ground handling costs, including de-icing, represent a growing percentage of total airline operating expenses. In response, some carriers may choose to cancel flights or reroute aircraft to avoid de-icing charges rather than absorb the cost. This economic pressure discourages excessive use of premium Type IV anti-icing fluids and encourages operators to seek cheaper alternatives or delay departures until temperatures rise. Such cost-avoidance behaviors limit the total volume of fluids consumed and restrain the overall revenue potential of the de-icing market.

MARKET OPPORTUNITIES

Development of Bio-Based and Environmentally Friendly DDe-IcingFluids

The urgent need for sustainable aviation solutions presents a significant opportunity for the aircraft de-icing market expansion. Traditional glycol-based fluids face increasing scrutiny due to their environmental impact, creating a market gap for eco-friendly alternatives derived from renewable sources such as corn, sugar beets, or agricultural byproducts. According to the American Chemistry Council, research into acetate-based and other biodegradable de-icing agents has accelerated, with several prototypes demonstrating comparable performance to conventional glycols in terms of freeze-point depression and viscosity. These bio-based fluids offer the advantage of rapid biodegradation, reducing the burden on airport wastewater treatment systems and lowering compliance costs. The European Commission Green Deal initiative encourages the aviation sector to adopt cleaner technologies, providing potential subsidies and tax incentives for airports that transition to environmentally benign de-icing solutions. As per the National Research Council of Canada, ongoing studies focus on enhancing the stability and holdover times of organic acid-based fluids, making them viable for commercial use. Early adopters of these green technologies can differentiate themselves as sustainability leaders, attracting environmentally conscious airlines and passengers. Furthermore, regulatory bodies are likely to favor operators who proactively reduce their ecological footprint, potentially easing permitting processes for new infrastructure. This shift toward green chemistry represents a high-growth avenue for manufacturers who can successfully scale production of effective and affordable bio-based de-icing agents.

Integration of Automated and Robotic De-Icing Systems

The integration of automation and robotics into de-icing operations offers a promising opportunity for global market expansion. Traditional manual de-icing using truck-mounted booms is labor-intensive, time-consuming, and exposes workers to hazardous chemicals and extreme weather conditions. According to the International Air Transport Association, automating the de-icing process can reduce turnaround times, improving schedule reliability and reducing fuel burn associated with ground holding. Emerging technologies include autonomous robotic arms equipped with sensors and artificial intelligence algorithms that can detect ice thickness and apply the precise amount of fluid needed. The Federal Aviation Administration is currently evaluating certification standards for automated de-icing systems, paving the way for commercial deployment. As per the Swedish Transport Agency, trials of robotic de-icing units at Stockholm Arlanda Airport have demonstrated significant reductions in fluid usage and improved consistency of application. These systems can operate continuously without fatigue, ensuring uniform coverage even in complex aircraft geometries. Airlines and airports facing labor shortages and rising wage costs view automation as a strategic solution to maintain operational capacity during peak winter periods. The initial high investment in robotic infrastructure is offset by long-term savings in labor, fluid, and maintenance costs. This technological evolution positions early adopters to achieve superior operational metrics and cost efficiencies in the competitive aviation landscape.

MARKET CHALLENGES

Unpredictable Weather Patterns Due To Climate Change

The increasing unpredictability of weather patterns driven by climate change poses a major challenge to the aircraft de-icing market growth. Historically, winter weather followed relatively predictable seasonal trends, allowing airports to stockpile fluids and schedule staff accordingly. However, according to the National Oceanic and Atmospheric Administration, the frequency of extreme weather events, such as sudden freeze-thaw cycles, heavy wet snow, and ice storms, has increased in recent years. These erratic conditions make it difficult for airport authorities to accurately forecast de-icing demand, leading to either costly overstocking or dangerous shortages of critical fluids. The Intergovernmental Panel on Climate Change warns that mid-latitude regions may experience more volatile winter weather, including rapid temperature fluctuations that create challenging icing conditions known as clear ice, which is harder to detect and remove. Such unpredictability strains logistical supply chains as just-in-time delivery models fail during sudden surges in demand. Furthermore, unusually warm spells followed by immediate freezes can catch operators off guard, resulting in flight cancellations and safety risks. As per the World Meteorological Organization, the variability in precipitation types requires de-icing teams to constantly switch between different fluid types and application methods, increasing operational complexity. This climatic instability undermines the efficiency of traditional winter operation plans and forces airports to maintain higher safety margins and inventory buffers, thereby increasing operational costs and logistical burdens.

Logistical Complexities in Fluid Storage and Distribution

Managing the storage, transportation, and distribution of large volumes of de-icing fluids is further challenging the global market expansion. De-icing fluids are bulky, viscous liquids that require specialized storage tanks, heating systems, and pumping infrastructure to prevent freezing and maintain usability. According to the Airports Council International, many older airports lack adequate storage capacity, forcing them to rely on frequent deliveries from external suppliers, which is risky during severe weather when roads may be impassable. The transportation of these chemicals is regulated as hazardous materials, requiring compliant vehicles and trained drivers, further complicating the supply chain. As per the Department of Transportation, spills during transport or transfer can result in severe environmental fines and operational shutdowns. Additionally, the shelf life of certain de-icing additives is limited, requiring careful inventory rotation to prevent degradation. The spatial constraints at busy airports often limit the expansion of storage facilities, leading to congestion and inefficiencies in fluid distribution to de-icing pads. During peak winter storms, the simultaneous demand from multiple airlines can overwhelm distribution networks, causing delays in vehicle refilling and aircraft servicing. These logistical bottlenecks can cascade into widespread flight delays and cancellations, affecting the entire aviation network. Overcoming these infrastructure limitations requires substantial capital investment and coordinated planning among stakeholders, which is often difficult to achieve in fragmented airport environments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Operation Mode, De-Icing Method, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Operation Mode Insights

The ground spray operations segment dominated the market by holding the highest share of the global market in 2025. The dominance of the round spray segment in the global market can be credited to its established reliability and comprehensive coverage capabilities, as well as the strict regulatory mandate requiring thorough pre-flight inspections and complete removal of frozen contaminants before takeoff. According to the Federal Aviation Administration, aviation authorities globally enforce a "clean aircraft concept" which dictates that no ice, snow, or frost can remain on critical aerodynamic surfaces. Ground spray operations utilize heated fluids and physical application methods that guarantee the complete melting and removal of existing ice layers. This method allows ground crews to visually inspect the aircraft during the process, ensuring absolute compliance with safety protocols. The Society of Automotive Engineers notes that ground-based application provides the necessary thermal energy and mechanical force to break the adhesion bond between ice and the aircraft fuselage. Furthermore, ground spray systems can be precisely calibrated to deliver the exact volume of fluid required based on the specific aircraft geometry and ambient temperature. This level of control is impossible to achieve with passive or in-flight systems, which rely on aerodynamic forces. The legal liability associated with icing-related accidents compels airlines and airport operators to rely exclusively on proven ground spray methods for initial de-icing. This regulatory and safety imperative ensures that ground spray remains the undisputed foundation of winter aviation operations worldwide.

However, the in-flight systems segment represents the fastest-growing segment in the aircraft de-icing market and is predicted to record 7.1% growth during the forecast period owing to the continuous advancement in ice detection sensors and avionics integration technologies. According to the International Air Transport Association, modern commercial aircraft are increasingly equipped with sophisticated ice detection systems that utilize infrared lasers and microwave sensors to identify ice accumulation in real time. These advanced sensors provide pilots with immediate and highly accurate data regarding the thickness and location of ice on the wings and fuselage. This technological leap enables the automated activation of in-flight anti-icing systems precisely when needed rather than relying on conservative manual estimates. The integration of these sensors with the aircraft's central computer allows for optimized fluid deployment, minimizing waste and maximizing aerodynamic efficiency. Boeing Commercial Airplanes states that next-generation aircraft designs are heavily focused on fly-by-wire systems that automatically adjust control surfaces and activate thermal anti-icing mechanisms based on sensor input. This seamless integration reduces pilot workload and ensures continuous protection during extended flights through freezing precipitation. As airlines upgrade their fleets with these advanced avionics suites, the demand for compatible in-flight systems grows exponentially. The shift toward highly automated and sensor-driven flight operations is fundamentally accelerating the adoption of in-flight de-icing technologies across the global commercial aviation sector.

By De Icing Method Insights

The type IV fluid segment held the leading share of the global market in 2025 due to its superior holdover time capabilities in severe freezing precipitation and the unique rheological properties of Type IV fluids, which allow them to adhere to aircraft surfaces and provide extended protection. According to the Society of Automotive Engineers, Type IV fluids are thickened with polymers that create a viscous layer on the wings and fuselage. This thickened layer prevents the fluid from running off the aircraft surfaces during the takeoff roll, ensuring that the anti-icing protection remains intact until the aircraft reaches a safe altitude. The Federal Aviation Administration mandates the use of Type IV fluids for aircraft expecting significant ground hold times in heavy snow or freezing rain. This regulatory requirement forces airlines to procure massive volumes of Type IV fluid during the winter season. The ability of Type IV fluid to absorb incoming precipitation and dilute without freezing is critical for preventing ice adhesion. The European Union Aviation Safety Agency notes that Type IV fluids can provide holdover times exceeding 3 hours under moderate freezing conditions, which is essential for managing flight delays. Without this extended protection, airlines would be forced to return to the de-icing pad multiple times, causing massive schedule disruptions. The unmatched performance of Type IV fluid in extreme weather conditions solidifies its position as the most widely consumed and relied-upon de-icing method in the global aviation industry.

On the other side, the weeping wing fluid segment is anticipated to grow at a CAGR of 8.14% during the forecast period owing to the significant reduction in overall fluid consumption and chemical runoff associated with this technology. According to the Environmental Protection Agency, traditional ground spray methods require thousands of gallons of glycol-based fluid per aircraft, which creates massive environmental compliance challenges for airports. Weeping wing technology utilizes porous panels embedded in the leading edges of the wings that continuously release a microscopic layer of anti-icing fluid. This precise delivery mechanism uses up to 80% less fluid compared to conventional spray methods. The National Aeronautics and Space Administration states that the reduction in fluid volume drastically lowers the biological oxygen demand in airport wastewater treatment systems. Airports facing strict environmental regulations and high disposal costs are actively seeking ways to minimize their chemical footprint. Weeping wing systems address this critical pain point by providing effective anti-icing protection with minimal environmental impact. Furthermore, the reduction in fluid weight contributes to improved fuel efficiency during the initial climb phase. The International Council on Clean Transportation notes that even minor weight reductions on commercial aircraft translate to significant carbon emission savings over the lifespan of the fleet. The dual benefit of environmental compliance and operational efficiency is driving rapid adoption of weeping wing fluid technologies among environmentally conscious airlines and airport authorities.

COUNTRY LEVEL ANALYSIS

North America Aircraft De Icing Makret Analysis

North America accounted for 33.3% of the global market share in 2025 and is likely to maintain its market dominance for the next few years as it continues to upgrade its massive winter infrastructure network, a highly mature and extensive infrastructure network designed to handle severe and prolonged winter weather conditions. The primary driving factor for this dominance is the massive volume of commercial air traffic operating out of major hubs in the United States and Canada, which experience frequent and heavy snowfall. According to the Federal Aviation Administration, the United States processes a significant volume of commercial flights daily during peak winter months, requiring millions of gallons of de-icing fluid annually. The region benefits from decades of investment in dedicated de-icing pads, centralized fluid storage, and advanced recovery systems. Furthermore, the strict regulatory environment enforced by the Federal Aviation Administration and Transport Canada mandates rigorous winter operations protocols, ensuring consistent and high-volume consumption of de-icing products. The presence of major global de-icing fluid manufacturers and ground handling companies headquartered in the region further solidifies its market leadership. The continuous modernization of airport infrastructure and the adoption of automated de-icing technologies at major hubs like Chicago, Toronto, and Denver demonstrate the region's commitment to maintaining operational efficiency. The combination of harsh winter climates, massive air traffic volume, and robust regulatory frameworks ensures that North America remains the undisputed leader in the global aircraft de-icing market.

Europe Aircraft De Icing Makret Analysis

Europe is expected to see steady growth in the coming years as it focuses on integrating sustainable technology into its existing airport network. The primary driving factor for the European market is the stringent environmental regulations imposed by the European Union regarding the discharge of glycol-based chemicals into local water systems. According to the European Union Aviation Safety Agency, airports across the continent are mandated to implement closed-loop fluid recovery systems and advanced biological treatment facilities to minimize ecological impact. This regulatory pressure has driven significant innovation in the development of bio-based de-icing fluids and highly efficient automated application systems. Major aviation hubs in Germany, Sweden, and the United Kingdom are global leaders in environmental compliance, investing heavily in state-of-the-art wastewater treatment infrastructure. Furthermore, the European market is characterized by a high concentration of premium de-icing services offered by specialized ground handling companies that prioritize safety and sustainability. As per the International Air Transport Association, European airlines are increasingly adopting advanced, automated de-icing solutions to optimize operations and reduce chemical usage.

COMPETITIVE LANDSCAPE

The competition in the aircraft de-icing market is characterized by intense rivalry among established chemical giants and specialized aviation service providers. Major players leverage their extensive distribution networks and brand recognition to maintain dominance while innovators disrupt the landscape with sustainable alternatives. The market features a mix of commodity glycol products and premium specialized fluids, creating a diverse competitive environment. Companies differentiate themselves through product efficacy, environmental compliance,e and technical support rather than price alone. Strategic alliances between chemical manufacturers and airport infrastructure developers are becoming increasingly common as stakeholders seek to offer holistic winter operations solutions. The entry of biotechnology firms into the de-icing space has further intensified competition by blurring the lines between traditional chemicals and green innovations. Regulatory hurdles act as a barrier to entry for smaller firms but also ensure high standards of biotechnology safety. Intellectual property protection plays a crucial role in sustaining competitive advantages as companies patent unique fluid formulations and application technologies. Overall, the market remains dynamic with continuous innovation driving shifts in competitive positioning and customer preferences across the global aviation sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Global Aircraft De-Icing Market include

- Clariant AG

- Kilfrost Limited

- The Dow Chemical Company

- BASF SE

- Cryotech Deicing Technology

- LyondellBasell Industries N.V.

- Integrated Deicing Services (IDS)

- JBT Corporation (John Bean Technologies)

- Global Ground Support, LLC

- Textron GSE (TUG Technologies)

- Vestergaard Company A/S

- UTC Aerospace Systems (Collins Aerospace)

TOP LEADING PLAYERS IN THE MARKET

- The Dow Chemical Company maintains a prominent position in the global aircraft de-icing market through its extensive portfolio of high-performance glycol-based fluids. The company produces Type I and Type IV anti-icing fluids that are widely recognized for their reliability and adherence to international safety standards. Dow recently expanded its production capabilities in North America to ensure consistent supply during peak winter seasons and mitigate logistical bottlenecks. This strategic expansion enhances the company's ability to meet surging demand from major airports and airlines globally. The company also invests heavily in research and development to create more environmentally sustainable formulations that reduce biological oxygen demand in wastewater. By collaborating with airport authorities on fluid recovery initiatives, Dow strengthens its reputation as a responsible industry leader. These actions reinforce its commitment to operational excellence and environmental stewardship while securing long-term contracts with key aviation stakeholders across multiple continents.

- Innospec LLC serves as a critical supplier in the aircraft de-icing market by offering specialized aviation fluids and comprehensive ground support services. The company is known for its Kilfrost brand, which provides advanced anti icing solutions trusted by airlines and ground handling operators worldwide. Innospec recently launched innovative low viscosity fluids designed to improve application efficiency and reduce fluid consumption during severe weather events. This anti-icing addresses the growing need for cost effective and environmentally compliant de icing operations. The company, low-viscosity, strengthened its distribution network in Europe and Asia to provide faster delivery and technical support to international clients. By partnering with major airport infrastructure providers, Innospec ensures seamless integration of its products into existing de icing systems. These strategic moves enhance customer loyalty and expand the company global footprint while demonstrating its dedication to advancing aviation safety and operational efficiency through continuous technological improvement.

- Clariant Ade-icing contributes significantly to the global aircraft de-icing market by providing the company's specialty chemicals and sustainable aviation solutions. The company offers a range of de-icing fluids that meet strict international certifications and environmental regulations. Clariant recently introduced bio-based de-icing agents derived from renewable resources, which significantly lower the ecological impact of winter operations. This innovation aligns with the aviationindustry'sy growing focus on sustainability and carbon reduction goals. The company also enhanced its technical service teams to provide customized training and consultation to airport operators on optimal fluid usage and waste management. By establishing strategic partnerships with aircraft original equipment manufacturers, Clariant ensures its products are compatible with next-generation anti-icing systems. These efforts solidify its position as a forward-thinking leader in the market while addressing the dual challenges of operational safety and environmental responsibility in global aviation.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the aircraft de-icing market primarily employ strategies focused on product innovation and environmental sustainability to maintain a competitive advantage. Companies invest heavily in research and development to create bio-based and biodegradable fluids that comply with stringent environmental regulations. Strategic partnerships with airport authorities and ground handling companies help integrate advanced de-icing technologies into existing infrastructure. Mergers and acquisitions are common tactics used to expand geographic reach and diversify product portfolios. Digitalization is another major strategy where firms develop smart monitoring systems to optimize fluid usage and reduce waste. Compliance with international safety standards remains central to operational strategies, ensuring trust and reliability among users. Additionally,y companies focus on expanding their technical support services to provide training and consultation to clients. These multifaceted approaches enable market participants to address evolving regulatory requirements and capture growing demand for efficient and eco-friendly de-icing solutions.

MARKET SEGMENTATION

This research report on the global aircraft de-icing market is segmented and sub-segmented into the following categories.

By Operation Mode

- Ground Spray Operations

- In-Flight Systems

By De-Icing Method

- Type I Fluid

- Type II Fluid

- Type III Fluid

- Type IV Fluid

- Weeping Wing Fluid

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1.What are the main product types?

The main product types include de-icing fluids, de-icing equipment, and de-icing services.

2.Which segment leads the market?

De-icing fluids and de-icing equipment are core segments, with fluids widely used at airports and equipment critical for ground operations.

3. Which region leads the market?

North America is the largest regional market, supported by heavy winter operations and strong airport infrastructure

4. Who are the major players?

Major players include B/E Aerospace, John Bean Technologies, Global Ground Support, SDI Aviation, Collins Aerospace, BASF, Clariant, Kilfrost, Dow, and Vestergaard.finance.yahoo+1

5. What are the main challenges?

The main challenges are environmental concerns around fluid runoff, high operational costs, and meeting strict safety and regulatory standards.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com