Global Aircraft Engine Blades Market Size, Share, Trends, & Growth Forecast Report Segmented, By Blade Type (Compressor Blades, Turbine Blades, And Fan Blades), Application (Commercial, Military, and General Aviation), Material (Titanium, Nickel Alloy, Composites, Aluminum Alloy, and Other Materials), & Region (North America, Europe, Asia-Pacific, Latin America, Middle East And Africa), Industry Analysis From 2026 to 2034

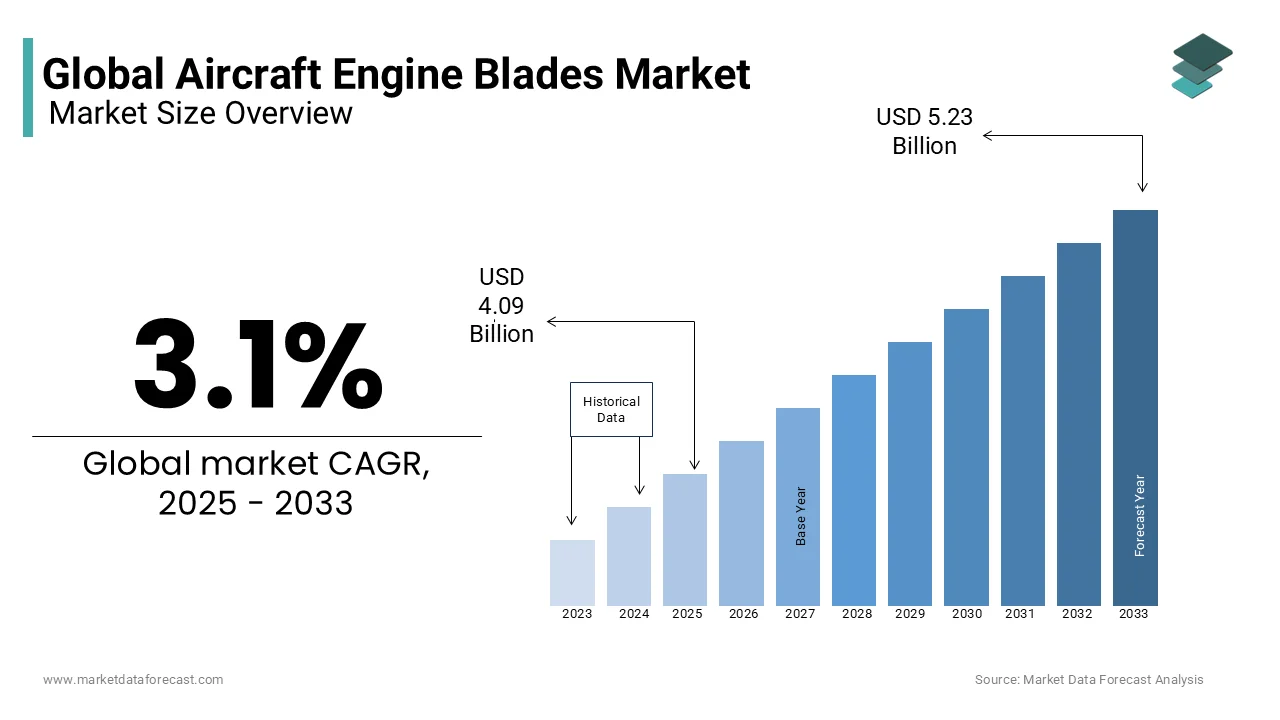

Market Size, 2025

$4.09 BnMarket Estimate, 2026

$4.22 BnMarket Forecast, 2034

$5.38 BnCAGR, 2026–2034

3.1%Global Aircraft Engine Blades Market Size

The global aircraft engine blades market was valued at USD 4.09 billion in 2025 and is anticipated to reach USD 4.22 billion by 2026 from USD 5.38 billion in 2034, growing at a CAGR of 3.1% during the forecast period from 2026 to 2034.

Aircraft engine blades are the core aerodynamic components within gas turbine propulsion systems, engineered to convert high velocity combustion gases into rotational thrust while withstanding extreme thermal and mechanical stress. These precision forged and cast elements operate at rotational velocities exceeding 15000 revolutions per minute and endure turbine inlet temperatures surpassing 1600 degrees Celsius. The operational reliability of these components directly dictates overall aircraft performance and safety compliance. According to IATA's 2024-2025 data, global commercial aviation accommodates approximately 102,000 to 106,000 scheduled flights daily (based on ~37–39 million annual flights). As per the Federal Aviation Administration, modern jet engines incorporate multiple blade stages ranging from fan assemblies to high pressure turbine sections, with each stage requiring distinct alloy formulations and cooling architectures. As described in FAA Airframe & Powerplant (A&P) Handbooks, modern jet engines incorporate multiple blade stages ranging from fan assemblies to high-pressure turbine sections. The European Aviation Safety Agency (EASA) mandates scheduled structural inspections and Non-Destructive Inspection (NDI) protocols. "Continuous structural health monitoring" (SHM) is currently recognized as a developing technology or "future alternative" (Acceptable Means of Compliance). NASA research initiatives demonstrate that single crystal nickel superalloys exhibit significantly superior creep resistance compared to conventional polycrystalline alternatives. These technological advancements align with stringent airworthiness directives that prioritize passenger safety and environmental compliance. The continuous evolution of computational fluid dynamics and finite element analysis enables manufacturers to optimize airfoil geometries and internal cooling channels with micron level precision. Regulatory bodies continuously update maintenance intervals based on accumulated flight hours and cycle counts to guarantee structural integrity.

MARKET DRIVERS

Expanding Commercial Fleet Deployment Drives Component Replacement Requirements

The continuous expansion of global commercial airline networks necessitates the integration of new propulsion systems, and the systematic replacement of aging turbine assemblies is a major factor boosting the growth of the aircraft engine blades market. According to the Airbus Global Market Forecast (GMF) 2024–2043, commercial aircraft manufacturers anticipate the delivery of 42,430 new passenger and freighter aircraft over the 20-year period to accommodate rising mobility demands and fleet modernization initiatives. Modern turbofan engines incorporate thousands of rotating and stationary blade elements distributed across the fan, compressor, and turbine stages, establishing a direct correlation between airframe procurement and component manufacturing volume. As per IATA data, global airline passenger volume reached approximately 4.41 billion in 2023, reflecting a robust post-pandemic recovery trajectory that reached 94.1% of pre-pandemic (2019) operational baselines. This sustained utilization pattern accelerates wear induced degradation across high pressure turbine stages, compelling operators to schedule proactive blade inspections and replacements before reaching mandatory cycle limits. European commercial carriers operate a massive active fleet of narrowbody and widebody jets with average fleet ages ranging from 10 to 12 years depending on the airline category, which naturally increases the frequency of maintenance-driven engine overhauls. The European Union Aviation Safety Agency (EASA) enforces strict Airworthiness Directives (ADs) that mandate life-limit thresholds and specific inspection intervals for engine blades, which vary significantly by engine architecture, component type, and operational stresses. These operational parameters generate consistent procurement cycles for original equipment manufacturers and certified repair facilities, ensuring steady component demand irrespective of short term economic fluctuations.

Regulatory Mandates for Fuel Efficiency Accelerate Advanced Blade Adoption

Aviation authorities worldwide have implemented stringent emission reduction frameworks that compel engine manufacturers to optimize thermodynamic efficiency through advanced blade architectures, and thereby contribute to the expansion of the aircraft engine blades market. According to the International Civil Aviation Organization (ICAO), the baseline for the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) is set at 85% of 2019 emissions levels for the 2024–2035 compliance phases, requiring airlines to offset international emissions that exceed this target. Modern high-bypass ratio engines achieve overall fuel burn reductions of 15% to 20% compared to previous-generation platforms, driven by a combination of higher propulsive efficiency and improved thermal efficiency from advanced single-crystal turbine blades with intricate internal cooling channels. NASA aerodynamic and materials research indicates that advanced airfoil designs incorporating serpentine cooling passages and thermal barrier coatings allow engines to operate at significantly higher gas temperatures while keeping underlying turbine blade metal temperatures within safe structural limits. These continuous structural and aerodynamic refinements enable next-generation aircraft engines to deliver a 15% to 20% reduction in fuel consumption and CO2 emissions compared to the fleets they replace, directly translating into substantial operational cost savings and compliance with environmental directives. European regulators enforce the Fit for 55 legislative package, which mandates an economy-wide target to reduce net greenhouse gas emissions by at least 55% by 2030 relative to 1990 baselines, implementing specific mechanisms for aviation such as phasing out free EU ETS allowances and introducing Sustainable Aviation Fuel (SAF) mandates. This regulatory pressure compels airlines to retrofit existing fleets with next generation blade assemblies that minimize aerodynamic losses and maximize combustion energy conversion. Manufacturers consequently prioritize research investments in ceramic matrix composite materials and directional solidification casting techniques.

MARKET RESTRAINTS

Complex Material Certification Processes Extend Production Timelines

The development and validation of next generation turbine blade materials involve rigorous structural testing protocols that significantly constrain manufacturing scalability, and therefore hamper the growth of the aircraft engine blades market. As detailed in FAA Type Certification guidelines, the validation of critical rotating parts involves rigorous high-cycle fatigue, thermal shock, and foreign object damage testing. However, the FAA mandates specific compliance and safety margins rather than an arbitrary "36-month minimum" timeframe, though the overall design approval process for an engine often takes several years. As per EASA Certification Specifications for Engines (CS-E), single-crystal nickel-based superalloys must undergo exhaustive material characterisation and substantiation testing to prove uniform mechanical property limits under extreme stress, but the regulatory framework evaluates performance safety factors. These exhaustive validation procedures demand extensive laboratory infrastructure and specialized testing equipment, which restricts the ability of secondary suppliers to enter the production ecosystem. The investment casting yield rate for high-pressure, complex hollow turbine blades can face substantial rejection rates—frequently scraping lower margins during early production runs—primarily due to internal ceramic core shifting, cooling channel deviations, and unwanted grain boundaries. Manufacturers must subsequently implement precision machining and thermal barrier coating applications that further extend lead times by 8 to 12 months per production batch. This extended certification and fabrication cycle limits rapid inventory replenishment capabilities and constrains manufacturers from responding swiftly to sudden procurement surges. The stringent quality assurance frameworks ultimately prioritize operational safety over production velocity.

Geopolitical Concentration of Critical Alloy Elements Constrains Supply Stability

The production of high-performance turbine blades relies heavily on specialized refractory metals that exhibit limited global availability and concentrated extraction networks, which hinders the expansion of the aircraft engine blades market. According to the USGS Mineral Commodity Summaries, estimated world primary mine production of rhenium was approximately 62.6 metric tons (62,600 kilograms) in 2023, with Chile alone accounting for nearly 48% of the global output, followed by Poland and the United States. As per the European Commission critical raw materials assessment, cobalt supply chains remain highly centralized, with the Democratic Republic of Congo accounting for 70 percent of worldwide extraction volumes. These geographic concentrations introduce significant procurement vulnerabilities, particularly when trade restrictions or export quotas disrupt material flow trajectories. The alloying requirements for advanced single-crystal nickel-based turbine blades typically demand 2% to 6% rhenium by weight (e.g., second and third-generation alloys) and 3% to 12% cobalt by weight to inhibit creep and maintain structural integrity under extreme thermal conditions. Market price volatility for highly concentrated minor metals like rhenium and cobalt can experience dramatic year-over-year spikes, with rhenium chemical and metal prices surging 70% to 90% depending on specific aerospace demand cycles, compelling manufacturers to absorb unpredictable raw material cost fluctuations. European defense and commercial aerospace sectors maintain strategic material reserves to mitigate short term disruptions, yet these stockpiles only provide temporary buffer capacity. The persistent supply chain fragility surrounding these essential metallurgical inputs restricts manufacturing scalability.

MARKET OPPORTUNITIES

Additive Manufacturing Integration Enables Rapid Prototyping and Weight Optimization

The implementation of powder bed fusion and directed energy deposition technologies offers transformative potential for turbine blade fabrication cycles and geometric complexity, which is expected to propel the global aircraft engine blades market. According to the National Aeronautics and Space Administration, additive manufacturing processes can drastically reduce component production lead times by two to ten times while bypassing the traditional tooling constraints of conventional casting methods. : As per General Electric research and production data, 3D-printed titanium aluminide low-pressure turbine blades offer a significant 50% weight reduction compared to traditional nickel-based alloys without compromising structural integrity. This manufacturing paradigm shift enables engineers to implement topology optimized internal cooling networks that precisely match thermal stress distributions across rotating airfoils. European aerospace consortiums have validated laser metal fusion techniques for turbine components, leveraging precision post-processing techniques to achieve strict aerospace dimensional tolerances and surface finish requirements. The integration of machine learning algorithms further accelerates powder parameter optimization, reducing trial iterations and improving material deposition consistency. Commercial airlines operating in regions with stringent weight penalties stand to gain immediate operational advantages through reduced fuel burn and extended maintenance intervals. Certification pathways for additively manufactured rotating components are maturing. Consequently, manufacturers can transition these parts to full-scale production environments.

Sustainable Aviation Fuel Compatibility Demands Enhanced Material Resilience

The aviation industry transition toward alternative fuel compositions creates unprecedented requirements for turbine blade metallurgical stability and chemical resistance, which opens the door for the expansion of the aircraft engine blades market. According to the International Air Transport Association, sustainable aviation fuel accounted for approximately 0.2% of global jet fuel consumption in 2023, requiring a massive global production ramp-up to meet mid-century aviation decarbonization goals. As per ASTM International fuel specification D7566, synthetic paraffinic kerosene must be blended with conventional jet fuel to maintain a minimum aromatic content, ensuring proper elastomer seal expansion within aircraft fuel systems. Turbine blades engineered for conventional jet fuel require targeted surface treatments and alloy modifications to withstand increased water vapor formation and reduced soot deposition. European research institutions have developed advanced thermal barrier coatings that improve high-temperature oxidation resistance by 25% while successfully keeping thermal conductivity restricted to low, insulating levels below 2.0 W/m·K. These material innovations ensure consistent structural performance across varying fuel compositions without requiring complete engine redesigns. Airlines implementing 50% sustainable aviation fuel blends experience a 50% to 70% reduction in exhaust carbon particulate emissions compared to standard conventional jet fuel. Manufacturers who proactively adapt blade metallurgy will secure long term service contracts with carriers pursuing environmental compliance certifications.

MARKET CHALLENGES

Accelerated Thermal Barrier Coating Degradation Complicates Maintenance Protocols

Prolonged exposure to extreme combustion environments induces progressive delamination and microscopic cracking within protective surface layers that shield underlying superalloy substrates, which limits the growth of the aircraft engine blades market. High-temperature materials research demonstrates that thermal barrier coating (TBC) degradation accelerates when bond coat oxidation generates a critical thermally grown oxide (TGO) layer thickness between 3 and 5 micrometers, leading to microscopic delamination. Federal Aviation Administration maintenance oversight documentation mandates strict, non-destructive inspection intervals for high-pressure turbine sections to capture localized coating spallation before base-metal erosion occurs. These degradation patterns compromise thermal insulation effectiveness, allowing base metal temperatures to exceed safe operational thresholds and accelerating creep deformation mechanisms. Maintenance facilities must implement advanced non destructive evaluation techniques, including thermography and ultrasonic phased array scanning, to detect subsurface coating detachment before catastrophic failure occurs. European airline operators face substantial logistical costs from thermal barrier coating restoration, which represents a highly technical and capital-intensive portion of a high-pressure turbine component overhaul cycle. The development of advanced segmented ceramics and self-healing oxide layers represents a highly critical evolutionary step in aerospace engineering, with next-generation iterations progressively entering commercial engine platforms to support higher operating temperatures. Operators currently face escalating maintenance frequency requirements that disrupt fleet scheduling and necessitate precise inventory management strategies to prevent operational delays.

Specialized Workforce Shortages Impede Precision Manufacturing Capacity Expansion

Shortage of specialized workforce impedes the expansion of the precision manufacturing capacity, which negatively impacts the aircraft engine blades market. The fabrication of next generation turbine components demands highly trained metallurgical engineers and advanced machining technicians who possess expertise in complex solidification processes and dimensional metrology. According to data from European labor and industrial bodies, the advanced aerospace manufacturing sector faces critical recruitment shortfalls, particularly within specialized precision machining and computerized component-milling roles. Due to highly stringent quality control frameworks and proprietary metallurgical processes, structural technicians specializing in precision turbine components undergo multi-year qualification pathways before achieving full line-release certification. Educational institutions struggle to align curriculum development with rapidly evolving manufacturing technologies, creating a persistent gap between academic graduates and industry competency standards. European advanced manufacturers navigate specialized workforce attrition, which is influenced by demographic shifts including retirement patterns among senior specialists and competing compensation packages from adjacent high-technology engineering fields. The integration of automated grinding systems and robotic inspection platforms partially mitigates labor constraints, yet these systems still require expert supervision for process calibration and anomaly resolution. Consequently, production scalability remains tightly coupled with human capital availability, limiting manufacturers from rapidly expanding output volumes.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.1% |

| Segments Covered | By Type, Application, Material & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Key Market Players | GE Aviation, CFM International, Rolls-Royce Holdings Plc, Albany International Corporation, Collins Aerospace, Arconic Inc., MTU Aero Engines, Pratt & Whitney, CFAN Company, GKN Aerospace, and Safran Aircraft Engines |

SEGMENTAL ANALYSIS

By Type Insights

The turbine blades segment dominated the aircraft engine blades market and accounted for a 58.6% share in 2025. This segment’s dominance was driven by the critical positioning of turbine blades within the hottest sections of gas turbine engines where operational temperatures exceed 1600 degrees Celsius and rotational stresses demand exceptional material performance. Turbine blades operate within combustion gas streams that reach temperatures surpassing the melting point of their base alloys, necessitating advanced cooling architectures and thermal barrier coatings. According to NASA research publications, modern high-pressure turbine blades incorporate advanced serpentine internal cooling channels and film-cooling holes to keep metal temperatures hundreds of degrees below the melting point of the superalloy. As per Federal Aviation Administration oversight guidelines, turbine blade inspection intervals are strictly regulated by engine-specific Life Limited Part (LLP) limits and operational parameters to catch thermal degradation early. These demanding conditions create consistent replacement demand across commercial and military fleets. European engine maintenance facilities report that turbine blade refurbishment and material replacement constitute one of the single most capital-intensive aspects of standard hot-section overhaul cycles. The integration of single-crystal nickel superalloys has revolutionized gas turbine longevity, vastly extending time on wing and creep resistance compared to traditional polycrystalline alternatives. Airlines operating in high ambient temperature regions experience accelerated coating degradation that further increases replacement frequency. This thermal intensity ensures turbine blades remain the highest value segment within engine blade portfolios.

Furthermore, the manufacturing complexity and material intensity of turbine blades generate substantially higher unit values compared to compressor or fan blade equivalents. According to aerospace manufacturing cost analyses, individual high-pressure turbine blades are among the most expensive components in a turbofan core due to complex internal cooling geometries and advanced single-crystal casting. As per aviation maintenance cost analyses, high-pressure turbine blade replacement represents a primary driver of material costs during narrowbody engine shop visits. European MRO facilities manage tight turbine blade repair turnarounds, where complex chemical stripping, specialized coating reapplication, and geometric validation dictate the engine's critical path. The adoption of ceramic matrix composite materials in next generation engines is elevating unit costs further while improving thermal efficiency. Defense procurement programs prioritize turbine blade availability due to mission critical performance requirements. These economic factors consolidate turbine blades as the revenue dominant segment despite lower unit volumes compared to compressor stages.

Turbine blades segment is also rapidly growing, with a projected CAGR of 7.2% from 2026 to 2034 due to intensifying thermal demands and fleet modernization initiatives across global aviation sectors. Advanced turbofan architectures targeting double-digit fuel burn reductions rely on next-generation turbine blades capable of operating under significantly increased overall pressure ratios and turbine inlet temperatures. According to CFM International technical updates, upgraded high-pressure turbine airfoils and durability kits have been progressively rolled out across the LEAP engine family to optimize time on wing in harsh operating environments. As per European Union Aviation Safety Agency framework guidelines, new turbine blade designs must undergo stringent, multi-phase cyclic, thermal, and containment testing profiles to secure official airworthiness certification. These rigorous validation processes ensure performance reliability while creating sustained procurement pipelines for qualified suppliers. Airlines retrofitting existing fleets with durability kits report measurable reductions in unscheduled removals. The transition toward sustainable aviation fuel compatibility introduces modified combustion characteristics that necessitate blade material adaptations. Manufacturers investing in directional solidification casting capacity are positioning to capture growing demand from both OEM production and aftermarket channels.

Moreover, the maturation of new generation engine fleets is triggering concentrated shop visit activity that elevates turbine blade replacement volumes. According to global aviation MRO forecasts, surging aircraft utilization and deep maintenance backlogs are driving a substantial increase in global turbine blade demand through the turn of the decade. As per advanced aerospace manufacturing and inspection practices, transient thermography techniques are increasingly utilized to non-destructively detect subsurface thermal barrier coating delamination before structural failure occurs. These predictive maintenance protocols optimize replacement timing while ensuring fleet availability. European carriers report that turbine blade inventory management represents a critical component of operational planning due to extended lead times for certified replacements. The integration of digital twin monitoring systems enables operators to track blade degradation in real time. This data driven approach supports proactive procurement strategies that sustain aftermarket growth trajectories independent of new aircraft delivery schedules.

By Application Insights

The commercial airplanes segment held the majority share of 65.2% of the aircraft engine blades market in 2025. This supremacy of the segment was credited to the scale of global passenger and cargo aviation operations that drive consistent engine component demand. Commercial aircraft manufacturers project long-term aviation expansion, with the Airbus Global Market Forecast predicting the delivery of over 42,000 new aircraft over the next two decades to support fleet growth and fleet replacement initiatives. Each modern narrowbody jet incorporates multiple engine blade stages with turbine and compressor sections requiring distinct alloy formulations and manufacturing processes. As per global air transport data, commercial aviation networks manage upwards of 90,000 to 100,000 daily flights globally, establishing continuous fleet utilization cycles that drive the high volume of engine blade aftermarket maintenance. European airline fleets average 11 years of operational age, positioning many aircraft within peak maintenance windows that generate steady aftermarket demand. The proliferation of low cost carrier networks across emerging markets expands route density and increases engine cycle accumulation. These operational dynamics ensure commercial aviation remains the foundational demand driver for aircraft engine blades across both original equipment and service channels.

In addition, aviation authorities enforce rigorous airworthiness directives that mandate blade inspection and replacement at defined flight hour or cycle intervals. According to Federal Aviation Administration regulatory mandates, high-pressure turbine airfoils are subject to tight life limits and regular cycles of non-destructive inspection to monitor structural and metallurgical integrity. As per the European Union Aviation Safety Agency documentation, commercial operators must maintain comprehensive blade tracking systems that monitor individual component history and remaining service life. These compliance requirements generate predictable procurement patterns that support stable market demand. Airlines operating in high temperature or high altitude environments experience accelerated coating degradation that necessitates more frequent replacements. The adoption of predictive maintenance technologies enables operators to optimize inspection scheduling while ensuring regulatory adherence. This structured maintenance framework consolidates commercial aviation as the dominant application segment within the aircraft engine blades market.

Military Airplanes Segment

Military airplanes segment is predicted to witness the highest CAGR of 7.6% during the forecast period. This expansion is propelled by heightened defense modernization initiatives and increased operational tempo across global armed forces. Military aviation forces worldwide are upgrading legacy aircraft platforms with next generation propulsion systems that demand advanced blade technologies. According to the United States Department of Defense procurement records, F 35 fighter deliveries reached record levels in 2025, locking in multi year turbine blade requirements from certified suppliers. As per the European Defence Agency capability development plan, member states are investing in adaptive cycle engine research that requires blades capable of handling variable bypass ratios and extreme thermal cycling. These programs prioritize material performance over cost considerations, enabling manufacturers to deploy single crystal superalloys and ceramic matrix composites without commercial budget constraints. The integration of stealth coatings and reduced infrared signature requirements introduces additional manufacturing complexity that elevates unit values. Defense contracts typically include long term sustainment provisions that ensure stable demand visibility beyond initial production lots.

Also, military aircraft frequently operate under high stress mission profiles that include rapid throttle transitions, low altitude flight, and aggressive maneuvering. Military maintenance data shows that combat aircraft turbine blades endure far more rapid and severe thermal-transient cycles than commercial passenger aircraft engines due to aggressive tactical operating profiles. As per the North Atlantic Treaty Organization logistics reports, deployed forces require expedited blade replacement capabilities to maintain mission readiness in forward operating locations. These operational demands compress inspection intervals and increase spare parts consumption across military fleets. The adoption of condition based maintenance systems enables commanders to optimize blade utilization while ensuring safety margins. This funding trajectory supports sustained procurement of high performance engine blades across fighter, transport, and rotorcraft platforms.

By Material Insights

The titanium alloys segment led the aircraft engine blades market and captured a 38.7% share in 2025 because of the material's optimal balance of strength, weight, and corrosion resistance for compressor and fan blade applications. Titanium alloys deliver specific strength characteristics that enable blade designers to minimize rotational mass while maintaining structural integrity under centrifugal loads. According to metallurgical research publications, titanium aluminide intermetallics offer a 50% weight reduction compared to conventional nickel superalloys, maintaining critical structural stability in lower-temperature turbine stages. As per Federal Aviation Administration certification standards, titanium compressor airfoils undergo highly rigorous high-cycle and low-cycle fatigue testing to establish strict lifing limits under representative operational conditions. These performance attributes support fuel efficiency targets by reducing engine rotational inertia and improving throttle response. European engine manufacturers report that titanium content in modern turbofan cores averages 25 percent by weight, with fan and low pressure compressor stages relying heavily on these alloys. The material's inherent corrosion resistance reduces maintenance requirements in marine and coastal operating environments. These technical advantages consolidate titanium alloys as the foundational material choice for front section engine components.

Furthermore, the aerospace industry has developed mature titanium processing capabilities that enable high volume blade production with consistent quality. These production efficiencies support competitive pricing for high volume commercial programs while maintaining margins for defense applications. European manufacturers have invested in digital forging technologies that improve grain flow alignment and reduce post machining requirements. The integration of additive manufacturing for titanium preforms is further enhancing design flexibility and material utilization. This established ecosystem enables rapid scaling to meet fluctuating demand without compromising certification standards or delivery schedules.

The composites segment is estimated to register the fastest CAGR of 9.4% between 2026 and 2034 owing to advancing technology readiness and expanding application envelopes within engine architectures. Ceramic matrix composites deliver thermal capabilities that exceed conventional metal alloys, enabling turbine blades to operate at temperatures approaching 1300 degrees Celsius without extensive cooling air extraction. According to NASA and aerospace research publications, Ceramic Matrix Composite (CMC) turbine components drastically reduce or entirely eliminate traditional cooling air requirements compared to nickel superalloys, significantly improving engine thermal efficiency. Advanced materials development programs show that Silicon Carbide (SiC) fiber-reinforced ceramic matrix composites demonstrate exceptional oxidation resistance, allowing components to survive harsh, high-temperature combustion environments. These performance gains support next generation engine programs targeting double digit fuel burn reductions. Airlines operating CMC equipped engines report measurable improvements in specific fuel consumption during long haul missions. The material's lower density also contributes to overall engine weight reduction that enhances aircraft payload capacity. Manufacturers investing in CMC coating and joining technologies are positioning to capture growing demand from efficiency focused engine programs.

Moreover, advanced manufacturing techniques are reducing production costs and lead times for composite engine blades, enabling broader commercial adoption. These efficiencies support competitive pricing for high performance applications while maintaining certification compliance. European research consortia have validated laser based deposition techniques for silicon carbide composites that achieve dimensional tolerances within 25 micrometers. The integration of machine learning algorithms optimizes process parameters and reduces trial iterations during qualification. This manufacturing evolution enables rapid prototyping and iterative design refinement that accelerates technology maturation cycles. Airlines benefit from improved blade durability and reduced maintenance frequency as composite applications expand across engine architectures.

REGIONAL ANALYSIS

North America Market Analysis

North America remained the top performer in the aircraft engine blades market and occupied a 33.2% share in 2025. The demand for these blades was driven by the concentration of major engine original equipment manufacturers, advanced materials research institutions, and certified production facilities within the United States and Canada. According to the Federal Aviation Administration operational statistics, the United States aviation system processes over 44000 commercial flights daily, establishing intense engine utilization patterns that drive consistent blade replacement demand. As per the United States Department of Defense procurement records, military modernization programs including F 35 production and next generation adaptive cycle engine development generate sustained turbine blade requirements. The region benefits from established supply chains for critical alloys including titanium and nickel superalloys, with domestic sponge production and refining capabilities ensuring material security. European aerospace partnerships further strengthen technology exchange and certification alignment across transatlantic programs. The integration of predictive maintenance technologies and digital twin monitoring systems positions North American operators at the forefront of blade lifecycle management. Government investments in advanced manufacturing initiatives support capacity expansion for high performance blade production. These structural advantages consolidate North America's market leadership while enabling technology export to emerging aviation ecosystems globally.

Europe Market Analysis

Europe was positioned second in the aircraft engine blades market and captured a 27.6% share in 2025. This position of the European market was propelled by the region's strong aerospace manufacturing base, advanced materials research capabilities, and regulatory leadership in aviation safety and environmental standards. According to the European Union Aviation Safety Agency certification database, European engine programs including the Open Fan and UltraFan initiatives drive innovation in blade aerodynamics and thermal management architectures. As per the European Commission critical raw materials assessment, the region maintains strategic partnerships for titanium and nickel alloy supply that support production stability for major engine manufacturers. The concentration of specialized foundries and precision machining facilities in Germany, France, and the United Kingdom enables high quality blade manufacturing with stringent quality control protocols. Research institutions across the European Union collaborate on ceramic matrix composite development and additive manufacturing techniques that advance next generation blade technologies. Airlines operating within European airspace benefit from harmonized maintenance regulations that optimize inspection intervals and replacement scheduling. The region's commitment to sustainable aviation fuel adoption introduces modified combustion characteristics that necessitate blade material adaptations. These factors position Europe as a technology leader while ensuring steady demand across commercial and defense aviation segments.

Asia Pacific Market Analysis

Asia Pacific is the fastest growing region in the aircraft engine blades market due to rising aircraft deliveries, fleet modernization initiatives, and expanding domestic manufacturing capabilities across China, India, and Southeast Asian nations. According to the Civil Aviation Administration of China traffic statistics, passenger volumes continue to recover toward pre pandemic levels, supporting increased engine utilization and component replacement demand. The region benefits from growing maintenance repair and overhaul infrastructure that supports localized blade inspection and refurbishment services. Government initiatives including China's Made in China 2025 and India's Make in India programs promote domestic aerospace component production, reducing import dependency for critical engine parts. Emerging aerospace hubs in South Korea and Japan contribute advanced materials research and precision manufacturing expertise to regional supply chains. Airlines operating in high temperature and high humidity environments experience accelerated coating degradation that increases replacement frequency. These dynamics position Asia Pacific as the primary growth engine for the global aircraft engine blades market through the forecast period.

Middle East And Africa Market Analysis

The Middle East and Africa region plays a key role in the aircraft engine blades market owing to the its strategic position as a global aviation hub, with major carriers operating extensive long haul fleets that generate consistent engine component demand. The region's harsh operating environment characterized by high ambient temperatures and sand ingestion necessitates specialized blade coatings and maintenance protocols that elevate aftermarket service demand. Local maintenance facilities in Dubai, Abu Dhabi, and Doha have developed advanced inspection and repair capabilities that support regional fleet operators. Government investments in aerospace industrial zones promote technology transfer and local content development for engine component manufacturing. These factors ensure steady market participation while enabling gradual capability expansion across the value chain.

Latin America Market Analysis

Latin America is likely to grow notably in the aircraft engine blades market during the forecast period due to the region's developing aviation infrastructure, growing middle class mobility demand, and expanding cargo logistics networks. According to the Latin American and Caribbean Air Transport Association traffic reports, passenger volumes continue to recover toward pre pandemic levels, supporting increased engine utilization across commercial fleets. The region benefits from strategic geographic positioning that supports cargo hub operations connecting North America, Europe, and Africa, generating consistent engine cycle accumulation. Local maintenance facilities in Brazil, Mexico, and Colombia have developed certified capabilities for blade inspection and minor repairs, reducing dependence on overseas service providers. Government initiatives promoting tourism and trade expansion support fleet renewal programs that create new blade procurement opportunities. Airlines operating in high altitude airport environments experience modified engine performance characteristics that influence maintenance scheduling and component replacement strategies. These dynamics position Latin America as a stable growth market with potential for accelerated expansion as economic conditions improve and aviation infrastructure investments materialize.

COMPETITIVE LANDSCAPE

The aircraft engine blades market features moderate consolidation with established original equipment manufacturers and specialized component suppliers competing across technology, quality, and service dimensions. Major players leverage deep integration across design, materials science, and certified manufacturing to secure long term supply agreements with airframers and airline customers. Competition centers on production reliability, certification capability, and lifecycle performance of blade components rather than price alone. Emerging participants focus on niche capabilities including composite blade manufacturing, localized production, and flexible supply models to access specific value chain segments. Technology differentiation through advanced cooling architectures, thermal barrier coatings, and additive manufacturing processes creates barriers to entry that favor incumbents. Supply chain resilience and material security represent critical competitive factors given the concentration of critical alloy production in limited geographic regions. Aftermarket service networks provide additional competitive advantage through blade inspection, repair, and refurbishment capabilities that extend component service life. Regulatory compliance and airworthiness certification requirements further reinforce the position of established players with proven quality systems. Future market dynamics will be shaped by advancements in material performance, sustainability requirements, and evolving engine architecture specifications that demand continuous innovation from all participants.

KEY MARKET PLAYERS

Some prominent players in the global aircraft engine blades market are

- GE Aviation

- CFM International

- Rolls-Royce Holdings Plc

- Albany International Corporation

- Collins Aerospace

- Arconic Inc.

- MTU Aero Engines

- Pratt & Whitney

- CFAN Company

- GKN Aerospace

- Safran Aircraft Engines

Top Players In The Market

- GE Aerospace maintains a prominent position in the aircraft engine blades market through its leadership in turbofan engine programs including the GE9X and CFM LEAP families. The company invests substantially in advanced materials research including ceramic matrix composites and additive manufacturing techniques that enhance blade performance and durability. GE Aerospace collaborates with airline customers to develop predictive maintenance solutions that optimize blade inspection intervals and replacement scheduling. The company's focus on fuel efficiency and emission reduction aligns with global aviation sustainability targets, driving demand for next generation blade architectures. Continuous innovation in cooling channel design and thermal barrier coatings extends component service life while improving engine thermal efficiency. These capabilities position GE Aerospace as a technology leader serving both commercial and defense aviation markets globally.

- RTX Corporation contributes significantly to the aircraft engine blades market through its Pratt and Whitney division which supplies propulsion systems for commercial and military aircraft platforms. The company specializes in geared turbofan technology that reduces fuel consumption and noise while requiring advanced blade designs for optimal performance. RTX invests in digital manufacturing technologies that improve blade casting yield and dimensional accuracy. The company collaborates with materials suppliers to develop next generation superalloys and composite structures that withstand extreme operating conditions. RTX's global service network provides blade inspection and repair capabilities that support fleet operators worldwide. These strengths enable RTX Corporation to maintain competitive positioning across diverse aviation segments while advancing propulsion technology for future aircraft programs.

- Safran Aircraft Engines plays a critical role in the aircraft engine blades market through its partnership in CFM International and independent engine programs serving commercial and defense customers. The company achieves major milestones in composite fan blade technology for next generation open rotor architectures. Recent developments include investments in advanced casting facilities that expand production capacity for high pressure turbine blades. Safran focuses on sustainable aviation fuel compatibility and emission reduction technologies that influence blade material selection and design parameters. The company collaborates with research institutions to develop ceramic matrix composites and additive manufacturing processes that enhance blade performance. Safran's global maintenance network provides blade refurbishment services that extend component service life and reduce operator costs. These capabilities position Safran Aircraft Engines as an innovation leader serving evolving aviation market requirements across multiple geographic regions.

Top Strategies Used By The Key Market Participants

Key participants in the aircraft engine blades market pursue strategic initiatives focused on technology advancement, capacity expansion, and supply chain resilience. Leading companies invest substantially in research and development for advanced materials including ceramic matrix composites and single crystal superalloys that enable higher operating temperatures and improved fuel efficiency. Manufacturers expand production facilities through capital investments that increase casting capacity and machining capabilities for high performance blade components. Strategic partnerships with materials suppliers ensure reliable access to critical alloys including titanium and nickel while mitigating geopolitical supply risks. Companies integrate digital manufacturing technologies including additive processes and artificial intelligence optimization that improve yield rates and reduce production lead times. Aftermarket service expansion through certified repair networks enhances customer retention and generates recurring revenue streams. Sustainability initiatives align blade development with emission reduction targets through lightweight designs and thermal efficiency improvements. These coordinated strategies enable market participants to maintain competitive positioning while addressing evolving aviation industry requirements.

RECENT MARKET NEWS

- In March 2026, GE Aerospace invested 33 million dollars in its Greenville facility to expand high pressure turbine blade manufacturing capacity and deploy advanced production technologies. This investment is anticipated to allow GE Aerospace to increase output volumes and strengthen the Aircraft Engine Blades Market presence.

- In June 2025, Safran Aircraft Engines achieved major milestones in the technological readiness of large diameter composite fan blades developed for the Open Fan propulsion program. This advancement is anticipated to allow Safran to accelerate next generation engine development and strengthen the Aircraft Engine Blades Market presence.

MARKET SEGMENTATION

This research report on the global aircraft engine blades market has been segmented and sub-segmented into the following categories.

By Type

- Fan Blades

- Compressor Blades

- Turbine Blades

By Application

- Commercial Airplanes

- Military Airplanes

- General Aviation

By Material

- Titanium

- Nickel Alloys

- Composites

- Aluminum Alloys

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What are aircraft engine blades?

They are precision-engineered rotating components that compress air and generate thrust inside aircraft engines.

What is driving the aircraft engine blades market growth?

Rising global air travel, fleet modernization, and demand for fuel-efficient engines are the main growth drivers.

Which aircraft types use engine blades?

Commercial, military, business jets, helicopters, and UAV engines all rely on advanced blade systems.

What materials are used in engine blades?

Titanium alloys, nickel-based superalloys, and ceramic matrix composites are commonly used for high strength and heat resistance.

Why are turbine blades critical in jet engines?

They convert hot gas energy into mechanical power that drives the engine’s compressor and fan.

What is the difference between compressor and turbine blades?

Compressor blades compress incoming air, while turbine blades extract energy from hot exhaust gases.

How does lightweight blade design benefit airlines?

Lighter blades improve fuel efficiency, reduce emissions, and lower operating costs.

What role does additive manufacturing play in blade production?

3D printing enables complex cooling channels, faster prototyping, and weight-optimized blade designs.

Which sector consumes the most aircraft engine blades?

The commercial aviation sector dominates due to large fleet size and frequent engine overhauls.

How often are aircraft engine blades replaced?

Blades are replaced during scheduled maintenance cycles based on flight hours and thermal stress limits.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com