Global Aircraft Tire Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Radial Tire, Bias Tire), Distribution Channel, Aircraft Type, And Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2026 To 2034)

Global Aircraft Tire Market Size

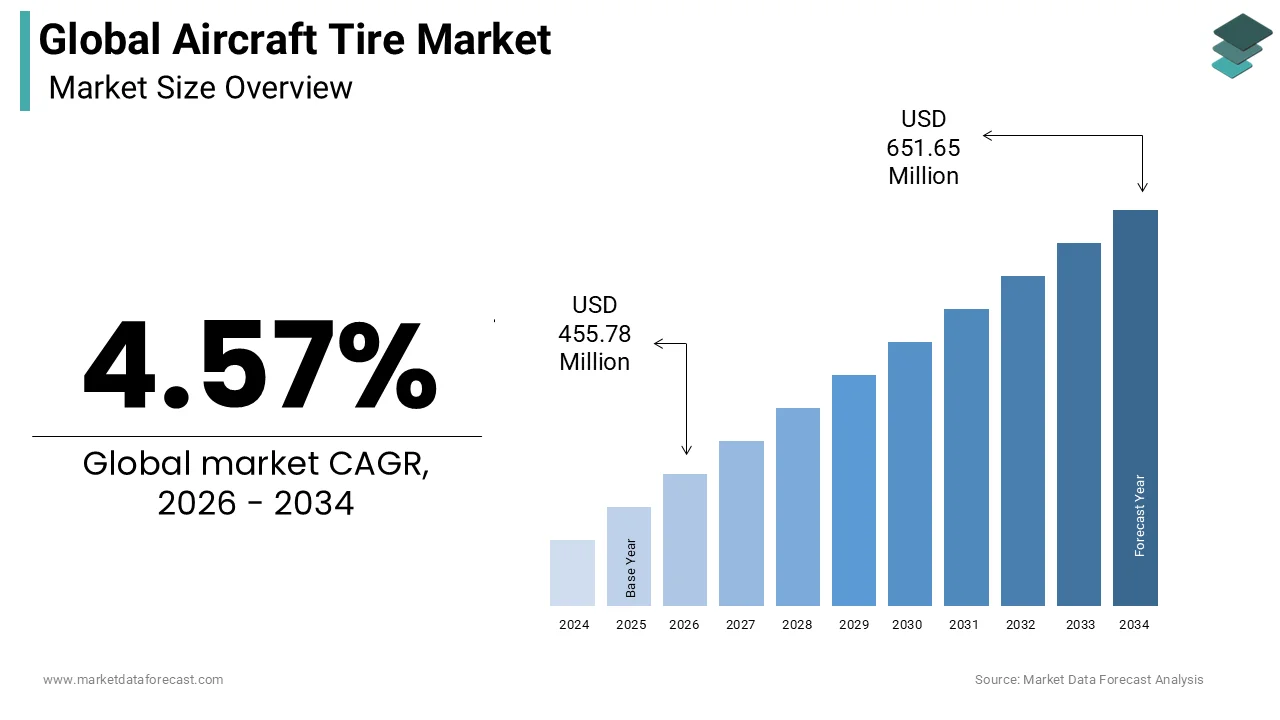

The global aircraft tire market size was calculated at USD 435.86 million in 2025 and is anticipated to reach USD 651.65 million by 2034, from USD 455.78 million in 2026, growing at a CAGR of 4.57% during the forecast period.

Aircraft tires are high-performance pneumatic tires designed to withstand the extreme mechanical and thermal stresses associated with aviation operations. These critical components serve as the primary interface between the aircraft and the runway during takeoff, landing, and taxiing, requiring exceptional durability, heat resistance, and load-bearing capacity. Unlike automotive counterparts, aircraft tires must endure rapid acceleration forces, sudden deceleration from high speeds, and significant vertical loads upon touchdown, often exceeding 50 tons for wide-body aircraft. According to the International Civil Aviation Organization, global air passenger traffic reached 9.4 billion in 2024, reflecting a robust recovery that directly correlates with increased flight cycles and subsequent tire wear rates. The European Union Aviation Safety Agency mandates rigorous certification standards for all aviation components, ensuring that tires meet strict safety protocols regarding burst pressure and tread integrity. Furthermore, the increasing adoption of sustainable aviation practices has prompted manufacturers to explore eco-friendly materials and re-treading technologies to minimize environmental impact. The market is characterized by a high barrier to entry due to the complex engineering requirements and stringent regulatory approvals necessary for certification. As airlines prioritize operational efficiency and safety, the demand for advanced tire technologies that offer extended service life and reduced maintenance intervals continues to shape the strategic direction of this specialized industrial sector.

MARKET DRIVERS

Expansion of Global Commercial Fleet Drives Replacement Demand

The global commercial aircraft fleet is expected to see steady expansion over the next few years, further driving demand for replacement tires, which is a key market driver. According to the Boeing Commercial Market Outlook, the global commercial airplane fleet is projected to nearly double from its current size by 2044, driven by rising passenger demand in emerging economies. Each new aircraft entering service requires a full set of main and nose landing gear tires, which are subject to regular replacement based on flight cycles rather than just calendar time. High-frequency short-haul operations typical of low-cost carriers accelerate tire wear significantly, as each takeoff and landing cycle imposes substantial thermal and mechanical stress on the rubber compounds. For instance, a narrow-body aircraft operating multiple daily sectors may require tire changes every few months, depending on runway conditions and braking intensity. This relentless operational tempo ensures a steady and predictable demand for replacement tires across the global network. Furthermore, the aging profile of existing fleets in mature markets necessitates frequent maintenance interventions, including tire replacements, to maintain airworthiness standards. As airlines expand their route networks and increase flight frequencies to capture post-pandemic travel demand, the cumulative effect of increased flight hours directly translates into higher volume requirements for durable and reliable aircraft tires, sustaining robust market growth.

Stringent Safety Regulations Mandate Regular Inspection and Replacement

Strict regulatory frameworks imposed by international aviation authorities mandate rigorous inspection schedules and mandatory replacement criteria for aircraft tires, which further contribute to the aircraft tire market expansion. According to the Federal Aviation Administration, operators must adhere to specific maintenance manuals that dictate tire removal based on tread depth, wear patterns, and age limits, regardless of visible condition. These regulations are designed to prevent catastrophic failures such as blowouts during high-speed takeoffs or landings, which could compromise aircraft safety. For example, tires must be removed if the tread depth falls below specified minimums or if there are signs of sidewall cracking or cord exposure. Additionally, the International Civil Aviation Organization requires periodic non-destructive testing to detect internal structural weaknesses that may not be visible externally. Compliance with these stringent standards forces airlines and maintenance, repair, and overhaul providers to procure new tires proactively rather than waiting for complete failure. The regulatory environment also emphasizes the importance of using certified original equipment manufacturer parts, which limits the use of inferior alternatives and ensures a stable demand for high-quality products. As safety standards evolve to address newer aircraft designs and heavier payloads, the frequency and complexity of tire inspections increase, further reinforcing the necessity for regular procurement of compliant aircraft tires to maintain operational legality and safety.

MARKET RESTRAINTS

Volatility in Raw Material Prices Impacts Manufacturing Costs

The volatility in prices of key raw materials such as natural rubber, synthetic rubber, and carbon black that constitute the majority of production costs is hindering the expansion of the aircraft tire market. According to the World Bank commodity price indices, natural rubber prices have historically experienced high volatility, with annual price fluctuations often exceeding 30% due to supply chain disruptions and climatic variations in major producing regions like Southeast Asia. These price swings directly affect the profit margins of tire manufacturers who operate under long-term fixed price contracts with airlines and original equipment manufacturers. Synthetic rubber, derived from petroleum products, is equally susceptible to crude oil price volatility, adding another layer of financial uncertainty to the manufacturing process. When raw material costs rise sharply, manufacturers struggle to pass these increases on to customers immediately due to competitive pressures and contractual obligations, leading to compressed profitability. Furthermore, the specialized nature of aircraft tire compounds requires high-purity materials that are less commoditized and more expensive than standard automotive grades. This dependency on volatile input costs makes financial planning difficult and can delay investment in research and development or capacity expansion. Consequently, manufacturers must employ sophisticated hedging strategies and supply chain diversification to mitigate these risks, but the inherent instability of raw material markets remains a persistent constraint on industry growth and pricing stability.

High Certification Barriers Limit New Market Entrants

The aircraft tire market is also constrained by exceptionally high barriers to entry, primarily driven by the rigorous and time-consuming certification processes required by aviation regulatory bodies. According to the European Union Aviation Safety Agency, obtaining type certification for a new aircraft tire design is a multi-year process that involves extensive testing, including burst pressure endurance runs and high-speed dynamic simulations. These tests require specialized facilities and significant capital investment, which discourages new players from entering the market. The certification process ensures that tires can withstand extreme conditions, such as high temperatures generated during braking and heavy loads during landing, but it also creates a moat around established manufacturers who already have certified product lines. New entrants must not only prove technical competence but also demonstrate a robust quality management system and traceability protocols that meet international standards. This lengthy approval timeline means that innovation cycles are slow, and companies cannot quickly introduce new products to capture emerging opportunities. Additionally, airlines prefer to stick with proven suppliers to minimize risk and simplify maintenance logistics, further entrenching the position of incumbent players. The high cost and complexity of certification thus act as a significant restraint on market competition, limiting the number of qualified suppliers and potentially keeping prices elevated due to a lack of competitive pressure from new innovators.

MARKET OPPORTUNITIES

Adoption of Sustainable and Eco-Friendly Tire Technologies

The growing emphasis on sustainability within the aviation industry presents a significant opportunity for the aircraft tire market. According to the International Air Transport Association, the aviation industry has committed to achieving net-zero carbon emissions by 2050, driving interest in all aspects of the supply chain, including ground support components. Traditional aircraft tires rely heavily on petroleum-based synthetic rubbers, but innovations are introducing bio-based alternatives such as dandelion rubber and rice husk silica, which reduce the carbon footprint of production. These sustainable materials offer comparable performance characteristics while appealing to airlines seeking to enhance their environmental credentials. Furthermore, the development of tires designed for easier re-treading and recycling supports the circular economy model, reducing waste and resource consumption. Manufacturers who invest in green chemistry and sustainable sourcing can differentiate themselves in a competitive market and secure contracts with environmentally conscious carriers. Regulatory incentives and corporate sustainability goals are increasingly favoring suppliers who can demonstrate tangible reductions in environmental impact. This shift towards sustainability opens new revenue streams and fosters long-term partnerships with airlines aiming to meet their climate targets. By pioneering eco-friendly solutions, manufacturers can position themselves as leaders in the next generation of aviation technology, capturing value from the industry's green transition.

Integration of Smart Tire Monitoring Systems

The integration of smart monitoring systems into aircraft tires offers a promising opportunity for the aircraft tire market expansion. According to a SITA report, over 60% of airports are investing in smart technologies to improve asset management and safety. Smart tires equipped with embedded sensors can transmit real-time data on pressure, temperature, and tread wear to maintenance crews, allowing for proactive interventions before failures occur. This technology reduces the risk of unscheduled groundings and optimizes tire usage by ensuring they are replaced only when necessary rather than on fixed schedules. For airlines, this translates into significant cost savings through reduced fuel consumption as properly inflated tires lower rolling resistance and improve safety through early detection of potential issues. The data collected from smart tires can also be integrated into broader aircraft health monitoring systems, providing a holistic view of landing gear performance. Manufacturers who partner with technology firms to develop these intelligent solutions can offer value-added services beyond the physical product, creating recurring revenue streams through data analytics and software subscriptions. As digitalization accelerates in aviation, the demand for connected components will grow, enabling manufacturers to capture a larger share of the maintenance and service market while enhancing customer loyalty through superior operational insights.

MARKET CHALLENGES

Supply Chain Disruptions Affect Production Timelines

The aircraft tire market faces significant challenges due to ongoing supply chain disruptions that affect the availability of critical raw materials and components. According to the Institute for Supply Management, global manufacturing lead times have remained extended due to logistical bottlenecks and geopolitical tensions impacting trade routes. These disruptions delay the delivery of essential inputs such as steel cords, fabric plies, and chemical additives, causing production slowdowns and inventory shortages. For aircraft tire manufacturers who operate on just-in-time principles to minimize holding costs, any delay in the supply chain can halt production lines and result in missed delivery deadlines for airline customers. The concentration of raw material sourcing in specific geographic regions exacerbates this vulnerability, as local disruptions can have global repercussions. Additionally, the shortage of skilled labor in manufacturing facilities further compounds the problem, limiting the ability to ramp up production when supplies become available. These supply chain inefficiencies increase operational costs and erode customer confidence as airlines face uncertainty in receiving timely replacements. To mitigate these risks, manufacturers are exploring nearshoring and diversifying supplier bases, but the complexity of the aviation supply chain makes complete resilience difficult to achieve. This persistent instability remains a major challenge affecting the reliability and responsiveness of the aircraft tire market.

Technical Complexity of Re-treading Processes

The technical complexity and regulatory scrutiny associated with re-treading aircraft tires are further challenging the expansion of the global aircraft tire market. According to the Federal Aviation Administration, retreaded tires must meet the same stringent safety standards as new tires, requiring precise inspection and manufacturing processes to ensure structural integrity. The retreading process involves removing the worn tread and bonding a new one to the existing casing, which requires specialized equipment and highly trained technicians. Any deviation in the bonding process or failure to detect hidden damage in the casing can lead to catastrophic failures during operation. This high level of technical difficulty limits the number of qualified retreading facilities and increases the cost of service compared to simple replacement. Furthermore, airlines are often hesitant to use retreaded tires on new aircraft types due to perceived risks, preferring new tires for maximum safety assurance. The variability in casing quality from different manufacturers also complicates the retreading process, as each brand may require specific handling procedures. These technical and perceptual barriers restrict the widespread adoption of retreading despite its economic and environmental benefits. Manufacturers must continuously invest in training and quality control to maintain certification and customer trust, making retreading a challenging but necessary segment of the aircraft tire lifecycle management.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.57% |

| Segments Covered | By Type, Distribution Channel, Aircraft Type, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, the Middle East and Africa, And Latin America |

| Market Leaders Profiled | Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Dunlop Aircraft Tyres, Sentury Tire, Qingdao Doublestar Tire Industrial, Petlas Tire Corporation, Specialty Tires of America, Wilkerson Company, Aviation Tires & Treads, Condor Tyres, Monster Tires, Shenzhen Zhongtian Tire, Air T Inc., Desser Aerospace |

SEGMENTAL ANALYSIS

By Type Insights

The radial tire segment dominated the market by capturing the leading share of the aircraft tire market in 2025. The dominance of the radial tire segment in the global market can be credited to its superior performance characteristics, including enhanced durability, lower rolling resistance, and improved fuel efficiency compared to bias ply alternatives. According to Michelin, a leading manufacturer, radial tires can reduce fuel consumption by up to 5% per flight cycle because their flexible sidewalls and rigid tread belts minimize heat generation and energy loss during taxiing and takeoff. This fuel saving is critical for airlines operating high-frequency short-haul routes where marginal gains in efficiency translate into millions of dollars in annual savings. Furthermore, radial tires offer a longer service life with the ability to withstand more landings before requiring retreading or replacement, which significantly lowers the total cost of ownership for operators. The structural integrity of radial tires also provides better handling stability during crosswind landings and wet runway conditions, enhancing overall safety margins. As environmental regulations tighten and airlines strive to meet sustainability targets, the adoption of radial technology has become standard for modern commercial fleets. The widespread availability of radial tires for both narrow-body and wide-body aircraft ensures that this segment remains the preferred choice for major carriers seeking to optimize operational economics while maintaining rigorous safety standards across their global networks.

On the other side, the bias tire segment is experiencing steady growth and is estimated to register a CAGR of 4.04% during the forecast period, owing to its continued relevance in general aviation, military, and older legacy aircraft fleets. For instance, there are hundreds of thousands of piston engine and turboprop aircraft in operation globally, many of which are designed to use bias ply tires due to their simpler construction and lower initial cost. Bias tires are preferred for smaller aircraft because they offer robust sidewall protection against debris on unpaved runways and require less sophisticated maintenance procedures, which is ideal for remote or rural airfields. The military sector also maintains a significant demand for bias tires for transport and tactical aircraft that operate in austere environments where durability and ease of repair are prioritized over fuel efficiency. Furthermore, the aftermarket for vintage and classic aircraft relies exclusively on bias ply technology, as these tires are often the only certified option for maintaining historical authenticity and airworthiness. This specialized demand ensures that while bias tires are being phased out in mainstream commercial aviation, they remain essential for specific operational segments. The affordability and ruggedness of bias ply construction make them indispensable for operators who do not require the high speed and heavy load capabilities of radial tires, thereby sustaining a consistent growth trajectory in this niche market.

By Distribution Channel Insights

The aftermarket segment led the market by accounting for the major share of the global market in 2025. The growth of the aftermarket segment in the global market is attributed to the high frequency of tire replacements required throughout the operational lifecycle of an aircraft. According to aviation maintenance standards, a typical commercial aircraft tire may need to be replaced or retreaded every 200 to 400 flight cycles, depending on runway conditions and braking intensity. With global flight volumes exceeding 35 million annually, the cumulative demand for replacement tires creates a massive and recurring revenue stream for aftermarket providers. Airlines and maintenance, repair, and overhaul organizations prioritize the aftermarket channel because it offers greater flexibility in sourcing, competitive pricing, and faster delivery times compared to original equipment manufacturer channels. The aftermarket also includes a robust retreading industry, which extends the life of tire casings and reduces waste, aligning with sustainability goals. Furthermore, the diverse needs of different aircraft types and operating environments require a wide variety of tire specifications that are readily available through aftermarket distributors. This accessibility ensures that operators can maintain optimal fleet readiness without being constrained by the production schedules of primary manufacturers. The sheer volume of maintenance events and the critical nature of tire availability for flight operations solidify the aftermarket as the dominant distribution channel in the global aircraft tire market.

On the other hand, the original equipment manufacturer segment is estimated to showcase a CAGR of 5.1% during the forecast period, owing to the robust production rates of new commercial aircraft and the increasing complexity of integrated landing gear systems. For instance, Boeing plans to ramp up production to 53 units per month for the 737 MAX by the end of 2026, creating a surge in demand for factory-fitted tires. OEMs benefit from long-term exclusive contracts with airframers such as Airbus and Boeing, which guarantee a steady volume of tire sales for every new aircraft rolling off the assembly line. These partnerships often involve collaborative engineering efforts where tire manufacturers work closely with aircraft designers to develop customized solutions that optimize performance and weight. The trend toward more integrated landing gear systems, where tires are pre-mounted and balanced at the factory, further strengthens the OEM channel as it simplifies the initial setup for airlines. Additionally, the introduction of new aircraft models with unique tire specifications requires OEM involvement to ensure proper certification and compatibility. As global aircraft deliveries accelerate to meet post-pandemic demand, the OEM segment is poised for rapid growth driven by the direct correlation between production volumes and tire installations.

By Aircraft Type Insights

The narrow-body aircraft segment led the market by holding the highest share of the global market in 2025. The growth of the narrow-body aircraft segment in the global market can be attributed to the sheer volume of single-aisle aircraft in operation globally and their high utilization rates. According to Airbus data, there are over 15000 A320 family aircraft in service worldwide, making it the most numerous commercial jet category. These aircraft typically operate on short to medium haul routes with multiple daily flights, resulting in frequent takeoffs and landings that accelerate tire wear. The high-cycle nature of narrow-body operations means that tires are replaced more often compared to wide-body aircraft, which fly fewer but longer sectors. This high turnover rate generates consistent and substantial demand for replacement tires in the aftermarket. Furthermore, the widespread use of narrow-body aircraft by low-cost carriers who prioritize rapid turnaround times and high asset utilization further amplifies tire consumption. The standardization of tire sizes across major narrow-body models such as the Boeing 737 and Airbus A320 allows for economies of scale in manufacturing and distribution. This uniformity simplifies inventory management for airlines and maintenance providers, ensuring a steady flow of products through the supply chain. The dominance of narrow-body aircraft in global fleets ensures that this segment remains the primary driver of volume in the aircraft tire market.

However, the wide-body aircraft segment is experiencing the fastest growth and is expected to exhibit a CAGR of 6.06% during the forecast period, owing to the recovery of long-haul international travel and the introduction of next-generation large aircraft. According to the International Air Transport Association, long-haul passenger traffic is recovering robustly as business and leisure travelers resume intercontinental journeys. Wide-body aircraft such as the Boeing 777X and Airbus A350 utilize larger and more complex tire assemblies that command higher prices due to their advanced engineering and material requirements. These tires must support significantly heavier loads and withstand higher landing speeds, necessitating the use of premium radial technologies and specialized rubber compounds. The increasing average stage length of flights also means that wide-body tires are subjected to prolonged periods of high temperature and stress, requiring superior heat dissipation properties. As airlines expand their long-haul networks to connect emerging markets in Asia and the Middle East, the demand for wide-body aircraft is rising sharply. This growth is further supported by the freighter conversion market, where retired passenger wide bodies are repurposed for cargo operations, requiring robust and durable tires to handle heavy payloads. The combination of higher unit value and increasing fleet size makes the wide-body segment the fastest-growing area in the aircraft tire market.

REGIONAL ANALYSIS

North America Aircraft Tire Market Analysis

North America dominated the market by capturing the highest share of the global market in 2025. The dominance of North America in the global market is attributed to its expansive aviation infrastructure. The United States holds the largest share of the North American aircraft tire market, driven by its massive domestic aviation network and high flight frequencies. According to the Federal Aviation Administration, the United States manages over 900 million passengers annually, creating immense demand for tire replacements. The presence of major airlines such as Delta, American, and United, which operate large fleets of narrow-body aircraft, ensures a consistent and high volume of aftermarket tire consumption. The region is also home to leading tire manufacturers and retreading facilities, which benefit from advanced infrastructure and skilled labor pools. Strict safety regulations enforced by the Federal Aviation Administration mandate regular tire inspections and replacements, driving compliance-based demand. Furthermore, the strong general aviation sector in the United States contributes significantly to the bias tire segment, as private and business aircraft require frequent maintenance. The mature nature of the market means that focus is shifting toward sustainability and efficiency, with airlines adopting radial tires and re-treading programs to reduce costs and environmental impact. The robust economic environment and high disposable income levels support strong leisure and business travel demand, ensuring sustained growth for the aircraft tire market in North America.

Europe Aircraft Tire Market Analysis

Europe had 24.4% of the global market share in 2025. Germany is poised to remain a critical innovation hub for the European aircraft tire market in the coming years. Germany serves as the central hub for the European aircraft tire market, characterized by strict environmental regulations and a dense network of international hubs. According to Eurostat, European airports handled over 1.1 billion passengers in 2024, reflecting a strong recovery in cross-border travel. The market in Germany is driven by major carriers like Lufthansa, which operate extensive fleets of wide-body and narrow-body aircraft requiring high-quality radial tires. The European Union Green Deal mandates significant reductions in carbon emissions, prompting airlines to adopt fuel-efficient radial tires and participate in circular economy initiatives such as tire re-treading. The region is also a leader in aerospace manufacturing, with Airbus facilities in France and Germany driving OEM demand for new aircraft tires. Strict safety and environmental standards imposed by the European Union Aviation Safety Agency ensure that only high-performance and compliant tires are used in the region. The well-developed maintenance, repair, and overhaul infrastructure in Europe supports a vibrant aftermarket sector with specialized providers offering advanced re-treading and inspection services. The focus on sustainability and operational efficiency ensures that the European market remains a key driver of innovation and quality in the global aircraft tire industry.

Asia Pacific Aircraft Tire Market Analysis

The Asia-Pacific is anticipated to record a promising CAGR in the global market during the forecast period, owing to the unprecedented fleet expansion and rising middle-class travel demand. According to the Civil Aviation Administration of China, the nation plans to increase the total number of civil airports to 450 by 2035 to accommodate its rapidly growing passenger traffic. This infrastructure boom requires the procurement of thousands of new aircraft, each equipped with fresh sets of tires, creating substantial OEM demand. Chinese airlines such as China Southern and Air China are expanding their international networks, increasing the utilization of wide-body aircraft and driving demand for high-performance radial tires. The region is also seeing a surge in low-cost carriers, which operate high-frequency short-haul routes, leading to accelerated tire wear and robust aftermarket activity. Local manufacturing capabilities are improving with domestic tire producers gaining certification and market acceptance, reducing reliance on imports. The government's support for the aviation sector as a strategic industry ensures continued investment in fleet modernization and infrastructure development. The combination of massive fleet growth, increasing flight frequencies, and rising consumer spending ensures that the Asia Pacific will remain the primary engine of growth for the global aircraft tire market in the coming decades.

Latin America Aircraft Tire Market Analysis

Latin America is estimated to showcase a healthy CAGR in the global market during the forecast period due to the gradual modernization and privatization of airport infrastructure. According to the Brazilian Airport Infrastructure Company, recent concession agreements for major airports have unlocked significant capital for infrastructure upgrades and fleet expansion. The market in Brazil is driven by major carriers like LATAM and Gol, which operate large fleets of narrow-body aircraft on domestic routes with high flight frequencies. The tropical climate and varied runway conditions in the region place additional stress on tires, increasing the need for durable and robust products. The aftermarket segment is particularly strong as airlines seek cost-effective solutions to manage maintenance expenses amidst economic volatility. Retreading services are widely used to extend tire life and reduce costs, aligning with the budget constraints of many regional operators. The growth of tourism and business travel in countries like Mexico and Colombia is also contributing to increased flight volumes and tire demand. Although the market faces economic challenges, the ongoing privatization trend and the need for operational efficiency provide a stable foundation for market growth. The focus on cost optimization and durability ensures steady demand for both new and retreaded aircraft tires in the region.

United Arab Aircraft Tire Market Analysis

The United Arab Emirates is expected to solidify its role as a key aviation hub, driving consistent demand for premium tire solutions in the Middle East and Africa over the next few years. The UAE is known for its ultra-modern aviation hubs and long-haul connectivity. According to the General Civil Aviation Authority, the UAE is home to Dubai International Airport, one of the busiest in the world for international passenger traffic, requiring an extensive and highly efficient fleet of wide-body aircraft. These aircraft operate long-haul routes with heavy payloads, placing significant demands on tire performance and durability. The extreme ambient temperatures in the region accelerate tire aging and wear, necessitating the use of high-quality heat-resistant radial tires. Major carriers like Emirates and Etihad Airways invest heavily in premium tires to ensure safety and reliability on their global networks. The region is also a major hub for air cargo, driving demand for freighter aircraft tires, which must withstand heavy loads and frequent operations. The focus on luxury and premium service means that airlines prioritize high-performance components to minimize disruptions and maintain schedule integrity. The ambitious expansion plans of Saudi Arabia under Vision 2030 are also creating new opportunities for tire suppliers as the kingdom develops its aviation infrastructure. The combination of high traffic volumes, extreme operating conditions, and strategic growth initiatives ensures that the Middle East and Africa remain a critical market for advanced aircraft tire solutions.

COMPETITION OVERVIEW

Competition in the aircraft tire market is characterized by a highly consolidated landscape dominated by a few multinational corporations with extensive technical expertise and certification portfolios. High barriers to entry due to stringent safety regulations and complex manufacturing requirements protect incumbent players from new competitors. Leading companies differentiate themselves through superior product performance, innovative materials, and comprehensive service networks, including retreading and logistics support. Price competition is moderate as airlines prioritize safety and reliability over cost savings for such critical components. However, vendors compete aggressively on the total cost of ownership metric,s offering long-term service contracts and predictive maintenance solutions to secure loyalty. The shift toward sustainable aviation drives rivalry in developing eco-friendly tires and recycling technologies. Strategic alliances with airframers ensure early access to new platform specifications, creating a moat around established suppliers. Regional players focus on niche segments like general aviation or specific geographic markets where local support offers a competitive advantage. Overall, the market remains stable with innovation and service quality serving as the primary battlegrounds for maintaining leadership positions among top-tier manufacturers who continuously invest in technology to meet evolving industry demands.

KEY MARKET PLAYERS

A few major players of the global aircraft tire market include

- Michelin

- Bridgestone Corporation

- Goodyear Tire & Rubber Company

- Dunlop Aircraft Tyres

- Sentury Tire

- Qingdao Doublestar Tire Industrial

- Petlas Tire Corporation

- Specialty Tires of America

- Wilkerson Company

- Aviation Tires & Treads

- Condor Tyres

- Monster Tires

- Shenzhen Zhongtian Tire

- Air T Inc

- Desser Aerospace

Top Strategies Used by the Key Market Participants

Key players in the aircraft tire market prioritize research and development to create advanced rubber compounds that enhance durability and fuel efficiency for airline operators. Strategic partnerships with original equipment manufacturers enable companies to integrate tires into new aircraft designs from the initial engineering phase. Expansion of global retreading networks helps participants capture value from the aftermarket segment while promoting sustainability through circular economy practices. Investment in smart tire technologies allows manufacturers to offer predictive maintenance services that reduce unscheduled groundings and optimize asset utilization. Focusing on sustainable materials and eco-friendly production processes addresses regulatory pressures and meets the growing demand for green aviation solutions globally.

Leading Players in the Global Market

- Michelin stands as a global leader in aviation mobility, providing high-performance radial and bias tires for commercial, military, and general aviation aircraft. The company leverages its advanced rubber compound technology to deliver superior durability and fuel efficiency for airline operators worldwide. Recent strategic initiatives include the expansion of its sustainable tire portfolio using bio-sourced materials to meet environmental mandates. Michelin actively collaborates with major airframers to co-develop next-generation landing gear solutions that optimize weight and performance. Their commitment to circular economy principles is evident in robust retreading programs that extend tire life cycles significantly. By focusing on innovation and sustainability, Michelin reinforces its reputation for engineering excellence and reliability in the critical aviation sector, ensuring long-term partnerships with global carriers.

- Bridgestone Corporation contributes significantly to the aircraft tire market through its comprehensive range of high-quality radial tires designed for diverse operational conditions. The company utilizes proprietary nanotechnology to enhance tread wear resistance and heat dissipation capabilities, ensuring safety during high-stress landings. Recent actions to strengthen its position include investing in smart tire technologies that monitor pressure and temperature in real time for predictive maintenance. Bridgestone also expands its global service network to provide rapid support and retreading services to airlines, minimizing downtime. The company focuses on reducing environmental impact by developing eco-friendly manufacturing processes and recyclable materials. These efforts demonstrate Bridgestone’s dedication to technological advancement and customer-centric solutions in the competitive global aviation industry.

- Goodyear Tire and Rubber Company plays a pivotal role in the aircraft tire market by supplying durable and reliable tires for a wide spectrum of aircraft types. The company specializes in advanced radial designs that offer excellent handling stability and reduced rolling resistance for improved fuel economy. Recent efforts to bolster its market presence involve launching new product lines specifically engineered for next-generation narrow-body and wide-body aircraft. Goodyear actively partners with maintenance providers to streamline supply chain logistics and ensure the timely availability of replacement tires. The company emphasizes rigorous quality control and testing protocols to meet stringent international safety standards. By prioritizing product innovation and operational efficiency, Goodyear maintains a strong competitive edge and supports the safe and efficient operations of airlines globally.

MARKET SEGMENTATION

This research report on the global aircraft tire market has been segmented and sub-segmented based on type, distribution channel, aircraft type, and region.

By Type

- Radial tire

- Bias tire

By Distribution Channel

- Aftermarket

- OEM

By Aircraft Type

- Narrow-body

- Wide-body

- Regional jet

- Others

By Region

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

Frequently Asked Questions

1. What factors are driving the growth of the aircraft tire market?

Rising air passenger traffic, increasing aircraft deliveries, growing defense spending, and frequent tire replacement requirements are key growth drivers.

2. Which aircraft type generates the highest demand for aircraft tires?

Commercial aircraft account for the largest share due to their high fleet size and frequent flight operations.

3. What materials are commonly used in aircraft tires?

Aircraft tires are manufactured using natural rubber, synthetic rubber, nylon cord, aramid fibers, and reinforced steel components.

4. What is aircraft tire retreading?

Retreading is the process of replacing the worn tread on an aircraft tire, extending its service life while reducing operating costs.

5. What challenges does the aircraft tire market face?

High manufacturing costs, strict aviation safety regulations, and supply chain disruptions are significant challenges.

6. How do military aircraft contribute to market demand?

Military aircraft require specialized high-performance tires for demanding operational conditions, supporting market growth.

7. Who are the major players in the Global Aircraft Tire Market?

Leading companies include Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Dunlop Aircraft Tyres, and Desser Aerospace.

8. What technological advancements are shaping the aircraft tire industry?

Innovations include lightweight tire materials, enhanced tread compounds, improved durability, and advanced tire monitoring technologies.

9. What is the future outlook for the Global Aircraft Tire Market?

The market is expected to grow steadily, supported by increasing aircraft production, rising air travel, expanding MRO activities, and continuous advancements in tire technology.

10. What role do MRO services play in the aircraft tire market?

Maintenance, Repair, and Overhaul (MRO) providers ensure timely inspection, retreading, and replacement of aircraft tires, driving aftermarket demand.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com