Global Airport Security Market Size, Share, Trends & Growth Forecast Report By Security System, By Airport Size, By Application, and By Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) – Industry Analysis and Forecast, 2026 to 2034

Global Airport Security Market Summary

Market Size & Growth

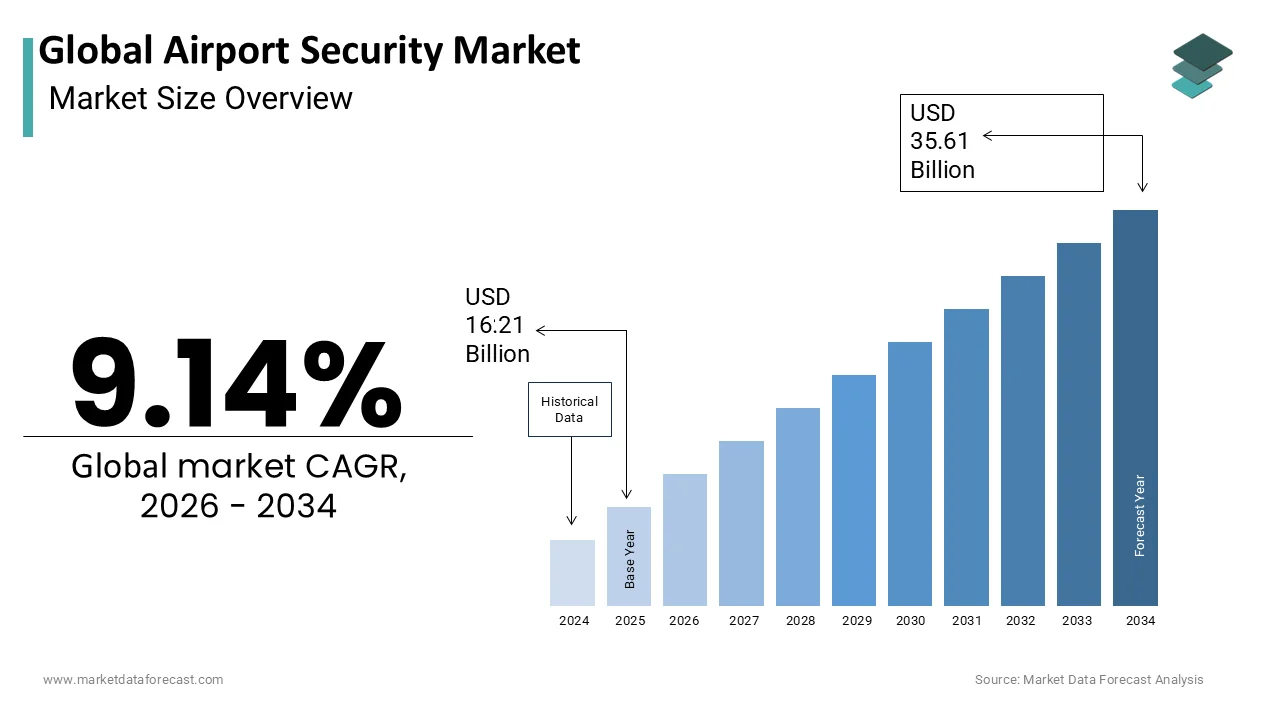

- The global airport security market was valued at USD 16.21 billion in 2025.

- Expected to reach USD 17.69 billion in 2026 and USD 35.61 billion by 2034, growing at a CAGR of 9.14% from 2026 to 2034.

- North America led the market in 2025; the access control and biometrics segment is the fastest-growing, at a CAGR of 12.5% from 2026 to 2034.

Key Market Segments

- By security system: Screening and Scanning Systems, Access Control and Biometrics, Surveillance Systems, Perimeter Security Systems, Cybersecurity Systems, Others

- By geography: North America leads; Asia Pacific is the fastest-growing region

- By airport size: More than 15 Million Passengers Annually held the largest share in 2025; airports below this threshold post the highest CAGR of 11.8%

- By application: Terminal held the largest share in 2025; Airside is the fastest-growing, at a CAGR of 10.9% from 2026 to 2034

Key Drivers

- Global passenger traffic hit 4.8 billion in 2024 (IATA), straining legacy terminal screening capacity.

- Escalating threats of drone incursions and cyberattacks, combined with ICAO Annex 17 and EASA mandates, are forcing continuous security upgrades.

- Expansion of biometric "One ID" systems is cutting passenger processing times by up to 50% (ACI).

Key Players

Smiths Detection Group Ltd., OSI Systems, Inc. (Rapiscan Systems), Leidos Holdings, Inc., Thales Group, NEC Corporation, Bosch Security Systems, Honeywell International Inc., Siemens AG, L3Harris Technologies, Inc., Teledyne FLIR LLC, Axis Communications AB, SITA.

Global Airport Security Market Size

The Global Airport Security Market is projected to grow from USD 16.21 billion in 2025 to USD 17.69 billion in 2026 and reach USD 35.61 billion by 2034, registering a CAGR of 9.14% during the forecast period from 2026 to 2034.

Airport security refers to the comprehensive measures, protocols, and technologies used to protect passengers, staff, aircraft, and airport facilities from crime, terrorism, and unlawful interference. This integrates physical screening systems, biometric identification, cybersecurity solutions, and perimeter surveillance to ensure compliance with international safety standards. As global air travel rebounds post-pandemic, the imperative for robust security measures has intensified. According to the International Civil Aviation Organization (ICAO), global passenger traffic reached approximately 4.53 billion in 2024, officially surpassing pre-pandemic levels. The International Civil Aviation Organization mandates strict adherence to Annex 17 standards, compelling airports worldwide to upgrade their security infrastructure. According to ACI Europe, the European airport network welcomed a record 2.6 billion passengers in 2025, heightening operational demands on airport terminal security.

Furthermore, the rise in asymmetric threats, including drone incursions and cyber vulnerabilities, has expanded the scope of airport security beyond traditional checkpoints. A study notes a drastic rise in the complexity of cyber threats targeting airspace users and infrastructure, with sectoral incidents climbing well over 100% in recent tracking cycles. This evolving threat landscape demands continuous innovation in detection technologies and operational protocols. The market is thus characterized by a shift towards integrated, intelligent security solutions that balance stringent safety requirements with passenger convenience and operational efficiency.

MARKET DRIVERS

Rising Global Passenger Traffic and Capacity Constraints

The exponential growth in global air passenger volumes drives the growth of the airport security market. This compels airports to adopt advanced screening technologies to manage throughput without compromising safety. The International Air Transport Association (IATA) confirmed that global passenger volumes hit a record 4.8 billion in 2024, quickly outstripping legacy airport terminal processing frameworks. This surge in traffic necessitates faster, more efficient screening processes to prevent bottlenecks and maintain operational fluidity. Traditional security checkpoints often struggle to handle peak-hour volumes, leading to long wait times that negatively impact passenger experience and airline scheduling. As per Airports Council International (ACI), the rollout of rigorous new biometric border tracking technologies has increased traveler processing bottlenecks by up to 70% at major international terminals. These technologies enable passengers to keep liquids and laptops in bags, significantly reducing processing time per passenger. Additionally, the expansion of low-cost carriers and the opening of new routes in emerging markets have diversified passenger demographics, requiring security systems that can handle varied threat profiles and higher volumes. The International Civil Aviation Organization emphasizes that security infrastructure must scale proportionally with passenger growth to maintain safety standards. Consequently, airports are prioritizing capital expenditure on next-generation screening equipment that offers higher detection accuracy and faster processing rates. This demand for scalability and efficiency directly fuels the adoption of innovative security solutions, driving market growth as airports strive to balance capacity constraints with stringent regulatory compliance and passenger satisfaction metrics.

Escalating Threat Landscape and Regulatory Mandates

The evolving nature of security threats and stringent regulatory frameworks further propels the expansion of the airport security market. This forces continuous upgrades in detection and surveillance capabilities. Terrorist organizations increasingly exploit unconventional methods, including improvised explosive devices concealed in everyday items and cyberattacks on critical aviation infrastructure. In addition, regulatory bodies such as the International Civil Aviation Organization and the European Union Aviation Safety Agency have introduced stricter mandates requiring airports to implement multi-layered security protocols. These regulations mandate the deployment of advanced imaging technology, explosive trace detection systems, and behavioral analysis tools to identify potential threats before they reach secure areas.

Furthermore, the rise in drone incursions near airport perimeters has prompted the integration of counter-unmanned aircraft systems into security frameworks. These regulatory pressures and threat dynamics compel airports to invest heavily in modernizing their security infrastructure. The need to comply with international standards while addressing emerging threats ensures sustained demand for innovative security solutions, making regulatory compliance and threat mitigation pivotal drivers of market expansion.

MARKET RESTRAINTS

High Capital Expenditure and Budgetary Constraints

The substantial capital investment required for deploying advanced airport security systems is a major restraint on the airport security market. This is particularly true for smaller regional airports and those in developing economies. Implementing state-of-the-art screening technologies such as computed tomography scanners, biometric gates, and integrated surveillance networks involves high upfront costs that strain limited budgets. Airports Council International (ACI) highlights that high capital procurement and integration costs for next-generation screening lanes place a severe financial burden on airport operators. For many airports, especially those handling lower passenger volumes, these costs represent a prohibitive financial burden that delays or prevents necessary upgrades. Additionally, the rapid pace of technological obsolescence means that investments made today may require replacement within five to seven years, further exacerbating financial pressures. Airports Council International (ACI) emphasizes that significant capital shortfalls serve as the primary barrier preventing secondary airports from modernizing security equipment. This financial limitation is particularly acute in emerging markets where government funding for aviation infrastructure is often prioritized for terminal expansions or runway improvements rather than security enhancements. Moreover, the ongoing operational costs associated with staffing, maintenance, and software updates add to the total cost of ownership, making it difficult for airports to justify large-scale investments. The disparity in financial resources between major international hubs and smaller regional facilities creates an uneven adoption landscape, slowing overall market growth. Advanced security solutions remain too expensive for many global airports to implement right now. Until technology costs drop or better financing models emerge, this high capital expenditure will hinder widespread adoption.

Privacy Concerns and Regulatory Compliance Complexities

Growing public concern over data privacy and the complex regulatory landscape surrounding biometric and surveillance technologies hamper the expansion of the airport security market. The increasing deployment of facial recognition, behavioral analysis, and passenger data tracking systems has sparked intense debate regarding individual privacy rights and data protection. Regulations such as the General Data Protection Regulation in Europe impose strict requirements on data collection, storage, and usage, compelling airports and technology providers to navigate a complex compliance framework. Non-compliance can result in substantial fines and reputational damage, discouraging some airports from adopting advanced biometric solutions. The regulatory fragmentation creates uncertainty for technology vendors and airport operators, who must ensure that their systems meet diverse legal standards in multiple countries.

Furthermore, public resistance to intrusive screening methods can lead to operational disruptions and negative media coverage, undermining the perceived benefits of enhanced security. The balance between security efficacy and privacy preservation remains delicate, with passenger trust being a critical factor in the successful implementation of new technologies. Privacy concerns will continue to hinder the rapid adoption of innovative security solutions, limiting market potential in key regions. This stagnation will persist until clear global standards for data privacy in aviation security are established and public acceptance improves.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Machine Learning

The integration of artificial intelligence and machine learning into airport security systems offers a significant opportunity for enhancing threat detection accuracy and operational efficiency, which is likely to boost the growth of the global market. These technologies enable real-time analysis of vast amounts of data from video feeds, sensor networks, and passenger screening processes, allowing for the identification of anomalies and potential threats with greater precision. Organizations like the U.S. Transportation Security Administration (TSA) verify that integrating AI algorithms with next-generation screening hardware significantly reduces false alarm rates while simultaneously increasing overall threat detection accuracy. Machine learning algorithms can continuously learn from new data, adapting to evolving threat patterns and improving performance over time. This capability is particularly valuable in identifying sophisticated threats such as concealed explosives or behavioral indicators of malicious intent that traditional systems might miss.

Furthermore, AI-powered systems can optimize resource allocation by predicting peak traffic periods and adjusting staffing levels accordingly, enhancing overall operational efficiency. The ability to process and analyze data from multiple sources simultaneously enables a more holistic approach to security, integrating physical and cyber defense mechanisms. Technology providers are increasingly focusing on developing modular AI solutions that can be seamlessly integrated into existing infrastructure, lowering barriers to adoption. As airports seek to enhance security while improving the passenger experience, the demand for intelligent, adaptive security systems is expected to grow substantially. This technological evolution offers a transformative opportunity for market players to deliver value through improved safety, efficiency, and scalability, positioning AI and machine learning as key drivers of future market expansion.

Expansion of Biometric Identification Systems

The widespread adoption of biometric identification systems provides a clear path for the expansion of the airport security market. This streamlines passenger processing and enhances identity verification accuracy. Biometric technologies such as facial recognition, fingerprint scanning, and iris detection enable seamless, contactless verification of passenger identities, reducing reliance on physical documents and minimizing human error. IATA and tech partners reveal that hundreds of major airports worldwide have introduced biometric identity checkpoints to accommodate international "One ID" digital travel credentials. These systems significantly reduce processing times at check-in, security checkpoints, and boarding gates, improving overall passenger experience and operational efficiency. As per the Airports Council International, airports using biometric verification reported a 50 percent reduction in average processing time per passenger, leading to shorter queues and higher throughput. The integration of biometrics with existing security infrastructure allows for continuous identity verification throughout the passenger journey, enhancing security by ensuring that the person screened is the same individual who boards the aircraft.

Furthermore, biometric systems support compliance with international travel regulations by providing reliable identity verification that meets stringent security standards. The growing acceptance of digital travel credentials and the development of interoperable biometric platforms facilitate cross-border travel, creating additional demand for standardized solutions. Technology providers are investing in scalable, privacy-compliant biometric solutions that can be customized for different airport sizes and operational needs. As global travel continues to recover and expand, the demand for efficient, secure, and convenient passenger processing solutions will drive significant growth in the biometric segment of the airport security market, offering lucrative opportunities for innovation and market penetration.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Integrated Systems

The increasing integration of digital technologies into airport security infrastructure introduces significant cybersecurity vulnerabilities that pose a major challenge to the global market. Modern security systems rely heavily on interconnected networks, cloud computing, and Internet of Things devices, creating multiple entry points for potential cyberattacks. These attacks can disrupt security operations, compromise sensitive passenger data, and even disable critical screening equipment, posing serious safety risks. CISA and independent tech analysts show that critical infrastructure data breaches cost millions of dollars per incident, factoring in severe recovery expenses and regulatory fines. The complexity of securing heterogeneous systems from multiple vendors further complicates cybersecurity efforts, as inconsistencies in security protocols and patch management create weaknesses that attackers can exploit. Additionally, the shortage of skilled cybersecurity professionals in the aviation sector limits the ability of airports to effectively monitor and respond to threats. The International Civil Aviation Organization has emphasized the need for robust cybersecurity frameworks, but implementation remains inconsistent across different regions and airport sizes. Ensuring the resilience of security systems against evolving cyber threats requires continuous investment in advanced defense mechanisms, regular security audits, and comprehensive staff training. Until airports can effectively address these vulnerabilities, cybersecurity risks will remain a persistent challenge. Consequently, these lingering issues could undermine confidence in integrated security solutions and hinder market growth.

Workforce Shortages and Training Deficiencies

Acute shortages of skilled security personnel and inadequate training programs are a serious impediment to the effective operation of these security systems, which negatively impacts the expansion of the airport security market. The demanding nature of security work, coupled with relatively low compensation and high stress levels, has led to significant turnover rates and recruitment difficulties across the industry. The International Civil Aviation Organization (ICAO) Assembly highlights a severe global shortage of skilled aviation personnel, causing systemic terminal congestion and recruitment strain. This shortage impacts the ability of airports to maintain adequate staffing levels at security checkpoints, leading to longer wait times and increased operational pressures on existing employees. Furthermore, the rapid introduction of advanced technologies requires continuous training to ensure that personnel can operate new equipment effectively and interpret complex data outputs. However, many airports lack comprehensive training programs that keep pace with technological advancements, resulting in suboptimal utilization of security investments. The International Civil Aviation Organization highlights that inadequate training contributes to inconsistent security performance and increased vulnerability to threats. Addressing these workforce challenges requires coordinated efforts between governments, airports, and technology providers to improve working conditions, offer competitive compensation, and develop standardized training curricula. Workforce shortages and training deficiencies must be resolved to restore the optimal functioning of airport security systems. Until then, these deficits limit the effectiveness of new technology and threaten overall market stability and growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Security System, Airport Size, Application, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America Europe Asia-Pacific Latin America Middle East & Africa |

| Market Leaders Profiled | Smiths Detection Group Ltd., OSI Systems, Inc. (Rapiscan Systems), Leidos Holdings, Inc., Thales Group, NEC Corporation, Bosch Security Systems, Honeywell International Inc., Siemens AG, L3Harris Technologies, Inc., Teledyne FLIR LLC, Axis Communications AB, SITA. |

SEGMENTAL ANALYSIS

By Security System Insights

The screening and scanning systems segment dominated the airport security market and accounted for a substantial share in 2025. This dominance of the segment was driven by mandatory regulatory requirements for advanced imaging technology and computed tomography scanners at major global hubs. They play a critical role in passenger and baggage inspection. Also, the U.S. Transportation Security Administration (TSA) states that hundreds of advanced Computed Tomography (CT) scanners have been deployed at major airports nationwide, steadily phasing out legacy X-ray machinery. The International Civil Aviation Organization mandates strict screening protocols that necessitate continuous upgrades toX-rayy and millimeter wave technologies to identify concealed explosives and weapons. In addition, the high volume of passengers processed through these checkpoints ensures consistent demand for replacement parts and system upgrades.

Furthermore, the integration of artificial intelligence into scanning systems enhances detection accuracy, reducing false alarms and improving throughput. The Airports Council International reported that airports utilizing advanced scanning systems experienced a 30 percent increase in passenger processing efficiency, reinforcing the economic justification for these investments. The sheer scale of global air travel, with billions of passengers undergoing screening annually, sustains the leading market share of this segment as airports prioritize safety compliance and operational efficiency through robust screening infrastructure.

But the access control and biometrics segment is expected to exhibit a noteworthy CAGR of 12.5% from 2026 to 2034 due to the increasing adoption of seamless travel initiatives and the need for enhanced identity verification throughout the passenger journey. IATA and tech providers indicate that hundreds of airports globally have activated facial-recognition systems to support paperless travel. The desire to reduce physical touchpoints and minimize queue times drives airports to invest in facial recognition and iris scanning technologies that verify passenger identity at multiple checkpoints without manual document checks. As per the Airports Council International, biometric systems reduced average boarding times by 40 percent at participating airports, providing a compelling operational benefit that accelerates adoption. Additionally, government initiatives promoting digital travel credentials facilitate the integration of biometric data with border control systems, creating a unified security framework. The International Civil Aviation Organization supports the development of standardized biometric protocols to ensure interoperability across different jurisdictions, further encouraging investment. The rising concern over identity fraud and unauthorized access to secure areas also contributes to this growth, as biometric solutions offer superior accuracy compared to traditional methods. Technological advancements are lowering implementation costs and improving privacy compliance. Consequently, the access control and biometrics segment is poised for sustained rapid expansion as airports seek to balance security rigor with passenger convenience.

By Airport Size Insights

The Airport Size More than 15 Million Passengers Annually segment led the airport security market and captured a significant share in 2025. This leading position of the segment was attributed to the complex security infrastructure required to manage high passenger volumes. These major international hubs face intense pressure to maintain stringent security standards while ensuring efficient passenger flow, necessitating significant investments in advanced screening and surveillance technologies. International transport networks highlight that mega-hubs handling over 15 million passengers annually dominate capital expenditure on advanced security deployments. The International Civil Aviation Organization imposes rigorous security mandates on large hubs, requiring multi-layered defense systems including perimeter surveillance, explosive detection, and cybersecurity measures. Compliance updates to European Commission screening regulations require continental airport networks to collectively commit billions of Euros to install advanced Standard 3 screening hardware. The high frequency of international flights at these airports also demands sophisticated border control and customs integration, further driving demand for comprehensive security solutions. Additionally, the presence of multiple terminals and extensive airside operations requires coordinated security management systems that can monitor vast areas in real time. The financial resources available to these large airports enable them to adopt cutting-edge technologies such as artificial intelligence-driven analytics and automated screening lanes, setting a benchmark for security standards. The continuous expansion of terminal facilities and the addition of new routes contribute to ongoing capital expenditure on security infrastructure, solidifying the leading position of this segment in the global market.

However, the airport size segment is predicted to witness the highest CAGR of 11.8% during the forecast period owing to increasing government focus on regional connectivity and the modernization of smaller airports to meet international security standards. The expansion of low-cost carrier networks into secondary cities has increased passenger traffic at these smaller facilities, necessitating upgrades to basic screening equipment and access control systems. Furthermore, the harmonization of global security standards requires smaller airports to implement minimum security measures, including X-ray scanners and metal detectors, which were previously optional or outdated. The introduction of modular and scalable security solutions tailored for smaller operations has lowered entry barriers, enabling these airports to upgrade efficiently. The growing awareness of security threats even in less busy airports has prompted authorities to enforce stricter compliance, driving demand for essential security equipment. As regional travel continues to expand and regulatory pressures mount, this segment will experience rapid growth. This expansion is further fueled by smaller airports catching up with global security benchmarks.

By Application Insights

The terminal segment was the largest in the airport security market and occupied a commanding share in 2025. This supremacy of the segment was supported by the concentration of passenger processing activities and critical security checkpoints within this area. Terminals house the primary screening lanes, immigration counters, and baggage handling systems that require robust security measures to protect passengers and staff. Airports Council International (ACI) confirms that passenger terminal buildings and baggage screening setups comprise a massive share of total airport capital investments. The International Civil Aviation Organization mandates comprehensive screening of all passengers andcarry-onn baggage within the terminal, driving continuous investment in X-ray machines, metal detectors, and explosive trace detection systems. The high density of people in terminal areas also necessitates advanced surveillance systems and access control mechanisms to prevent unauthorized entry into secure zones.

Furthermore, the integration of retail and dining facilities within terminals increases the complexity of security management, requiring coordinated monitoring of public and restricted areas. The recent push for seamless travel experiences has led to the deployment of biometric gates and automated screening lanes within terminals, further boosting investment in this segment. The critical nature of terminal operations in ensuring overall airport safety and compliance with international regulations ensures that this segment remains the largest contributor to market revenue, driven by constant technological refresh cycles and capacity expansions.

On the other hand, the airside segment is estimated to register the fastest CAGR of 10.9% between 2026 and 2034. Factors such as increasing concerns over perimeter security and aircraft protection are propelling the rapid growth of this segment. This growth is also fueled by the rising incidence of drone incursions and unauthorized access attempts near runways and taxiways, prompting airports to invest in specialized detection and neutralization systems. Technical handbooks from the International Civil Aviation Organization (ICAO) outline non-interfering drone risk assessment models to help airports deploy detection technology without disrupting navigation communications. As per the Federal Aviation Administration, major airports in the United States allocated significant budgets for perimeter fencing upgrades and sensor network installations to improve situational awareness on the airside. Additionally, the protection of ground support equipment and fuel storage facilities from sabotage or theft requires robust access control and surveillance solutions tailored for outdoor environments. The expansion of airport infrastructure, including new runways and taxiways, also creates demand for integrated security systems that can monitor large open areas effectively. The increasing automation of airside operations, such as autonomous baggage carts and refueling vehicles, introduces new cybersecurity vulnerabilities that require specialized protection measures. These factors collectively contribute to the rapid growth of the airside security segment as airports prioritize the safeguarding of critical operational assets and flight safety.

COUNTRY LEVEL ANALYSIS

North America Airport Security Market Analysis

North America was the top performer in the global airport security market and accounted for a substantial share in 2025. This prominence of the region’s market was driven by mature infrastructure and stringent regulatory frameworks. The region benefits from substantial government funding and a high level of awareness regarding aviation security threats. According to the Transportation Security Administration, the United States alone processed over 900 million passengers in 2025, necessitating continuous upgrades to security equipment at hundreds of airports. The Federal Aviation Administration mandates strict compliance with security standards, driving consistent demand for advanced screening technologies and cybersecurity solutions. ACI-NA highlights that North American airports rely heavily on multi-billion-dollar Federal Aviation Administration (FAA) capital grants to deploy next-generation computed tomography (CT) scanners and advanced biometrics. The presence of major technology providers in the region fosters innovation and rapid adoption of new security solutions.

Furthermore, the high volume of domestic and international travel ensures steady utilization of security systems, supporting recurring revenue streams for maintenance and upgrades. The region also leads in the integration of artificial intelligence into security operations, enhancing threat detection capabilities and operational efficiency. Collaborative efforts between government agencies and private sector stakeholders facilitate the development of standardized security protocols, ensuring uniform protection across the continent. The strong economic base and commitment to aviation safety sustain North America's leading role in the global market, with ongoing investments aimed at addressing emerging threats and improving the passenger experience through technological advancement.

Europe Airport Security Market Analysis

Europe was the next prominent region in the global airport security market in 2025 because of rigorous regulatory standards and a dense network of international airports. The European Union Aviation Safety Agency enforces comprehensive security directives that require member states to implement advanced screening and surveillance measures. Eurostat and ACI Europe confirm that while internal EU flights clear 900 million travelers annually, the total European airport network managed 2.6 billion passengers in 2025, driving severe pressure for high-volume security throughput. The European Organisation for the Safety of Air Navigation emphasizes the importance of cybersecurity in aviation, prompting airports to invest in protective measures against digital threats. As per the International Air Transport Association, European carriers and airports collaborated on initiatives to standardize biometric travel processes, facilitating smoother cross-border movements while enhancing security. The region is also at the forefront of adopting sustainable security technologies, with many airports exploring energy-efficient screening equipment. The Schengen Area's open borders require robust external border controls, driving investment in automated border control gates and facial recognition systems at entry points.

Furthermore, the threat of terrorism and asymmetric attacks remains a priority, leading to continuous updates in security protocols and equipment. The presence of established security manufacturers and research institutions in Europe supports innovation and the development of cutting-edge solutions. These factors collectively sustain Europe's strong market position, with a focus on balancing security efficacy with passenger rights and environmental considerations.

Asia Pacific Airport Security Market Analysis

Asia Pacific is a rapidly growing region in the airport security market due to expanding air travel and infrastructure development. The region is witnessing a surge in the construction of new airports and the expansion of existing facilities to accommodate rising passenger numbers. The International Air Transport Association (IATA) projects that the Asia-Pacific region will remain aviation’s primary long-term growth engine, pacing at an average annual growth rate of roughly 3.8%. Governments in countries such as China, India, and Japan are prioritizing aviation security as part of their national safety strategies, leading to increased procurement of advanced screening and surveillance systems. The Civil Aviation Administration of China (CAAC) achieved its 14th Five-Year Plan aviation target, expanding its infrastructure network to over 270 civil transport airports heavily reliant on AI security screening. The adoption of biometric systems is accelerating in the region, with major hubs implementing facial recognition for seamless passenger processing. The diverse economic landscape means that while developed markets focus on technological upgrades, emerging markets are investing in basic security infrastructure to comply with global norms. The rise in the middle-class population and disposable income contributes to higher travel frequencies, increasing the load on security checkpoints. Regional cooperation initiatives aim to harmonize security standards, facilitating smoother international travel. These dynamics position Asia Pacific as a key growth engine for the global airport security market, with substantial opportunities for technology providers and service integrators.

Latin America Airport Security Market Analysis

Latin America is a developing region in the global airport security market owing to gradual modernization and increasing regulatory alignment with international standards. The region is experiencing steady growth in air travel, prompting airports to upgrade their security infrastructure to handle higher passenger volumes and meet safety requirements. According to the International Air Transport Association, Latin American passenger traffic grew by 6 percent in 2025, driven by economic recovery and increased tourism. Governments in countries such as Brazil and Mexico are investing in airport expansions and security enhancements to support this growth. The adoption of biometric technologies is gaining traction, with several major airports implementing facial recognition for border control and boarding processes. However, budgetary constraints and varying levels of technical expertise pose challenges to the widespread adoption of advanced solutions. Regional collaborations aim to improve security standards and share best practices among member countries. The increasing awareness of cyber threats is also prompting airports to invest in digital security measures. While the market size is smaller compared to other regions, the growth potential is significant as economies stabilize and travel demand rises. Strategic partnerships with global technology providers are helping local airports access innovative solutions, fostering gradual but steady market expansion in Latin America.

Middle East and Africa Airport Security Market Analysis

The Middle East and Africa region holds a noteworthy position in the global airport security market due to major hub developments and increasing focus on aviation safety. Countries in the Gulf Cooperation Council are investing heavily in world-class airport infrastructure to maintain their status as global transit hubs. IATA and Airports Council International (ACI) demonstrate that Middle Eastern aviation hubs handle hundreds of millions of passengers annually, heavily driven by international hub-and-spoke transfer traffic. The General Authority of Civil Aviation in Saudi Arabia and the General Civil Aviation Authority in the United Arab Emirates enforce strict security regulations, driving demand for advanced screening and surveillance technologies. As per the Airports Council International, major airports in Dubai and Doha implemented comprehensive biometric systems in 2025 to enhance passenger experience and security efficiency. In Africa, the African Union's initiative to improve continental connectivity is leading to airport upgrades and security enhancements in key nations such as South Africa and Kenya. The continent faces unique challenges related to resource allocation and technical capacity, but international partnerships are facilitating technology transfer and training. The rising threat of terrorism in certain regions necessitates robust perimeter security and intelligence sharing mechanisms. The region's focus on becoming a global aviation leader ensures continued investment in state-of-the-art security solutions, positioning it as an important market for future growth and innovation in airport security technologies.

COMPETITIVE LANDSCAPE

The competition in the airport security market is intense and characterized by the presence of established multinational corporations alongside specialized technology providers. Major players compete based on technological innovation, product reliability, and comprehensive service offerings. The market sees frequent launches of advanced screening systems incorporating artificial intelligence and machine learning capabilities. Companies strive to differentiate themselves through superior detection accuracy and faster processing times. Strategic partnerships with airlines and airport authorities are crucial for securing large-scale contracts. The entry of new players with niche solutions adds pressure on incumbents to continuously innovate. Price competition remains moderate as quality and compliance with strict regulatory standards take precedence. Geographic expansion into emerging markets offers significant growth opportunities but requires adaptation to local regulations. Cybersecurity concerns have intensified competition in the digital security segment, prompting investments in robust protective measures. Mergers and acquisitions are common strategies used to consolidate market position and acquire specialized technologies. The dynamic nature of security threats ensures that competition remains focused on delivering adaptable and future-ready solutions. Customer loyalty is driven by proven performance and ongoing support services. Overall, the market landscape is shaped by a balance of technological leadership, regulatory compliance,e and strategic agility among key participants.

KEY MARKET PLAYERS

Some of the companies that are playing a dominant role in the Global Airport Security Market include

- Smiths Detection Group Ltd.

- OSI Systems, Inc. (Rapiscan Systems)

- Leidos Holdings, Inc.

- Thales Group

- NEC Corporation

- Bosch Security Systems

- Honeywell International Inc.

- Siemens AG

- L3Harris Technologies, Inc.

- Teledyne FLIR LLC

- Axis Communications AB

- SITA

TOP LEADING PLAYERS IN THE MARKET

- Smiths Detection is a global leader in threat detection and security screening technologies for aviation. The company specializes in advanced X-ray systems, computed tomography scanners, and explosive trace detection devices. Smiths Detection actively collaborates with international regulatory bodies to ensure its solutions meet evolving safety standards. Recently,y the company launched next-generation cargo screening systems that enhance throughput while maintaining high detection accuracy. Their focus on innovation drives continuous improvement in passenger experience and operational efficiency at major airports worldwide. By integrating artificial intelligence into their screening platforms, Smiths Detection enables faster and more accurate threat identification. This technological advancement supports airports in managing increasing passenger volumes without compromising security integrity. The company also invests heavily in research and development to address emerging threats such as concealed explosives and cyber vulnerabilities. Their comprehensive portfolio and global service network strengthen their position as a trusted partner for airport authorities seeking reliable and cutting-edge security solutions.

- Thales Group provides integrated security solutions encompassing biometric identity management, surveillance,e and access control systems. The company leverages its expertise in aerospace and defense to deliver robust airport security infrastructure. Thales recently expanded its biometric boarding solutions across multiple international hubs, facilitating seamless passenger journeys. Their technology enables secure and contactless verification using facial recognition and digital travel credentials. Thales emphasizes cybersecurity resilience,e ensuring that security systems remain protected against digital threats. The company partners with airlines and airport operators to create interoperable ecosystems that enhance both safety and convenience. By focusing on end-to-end identity management, Thales helps reduce processing times and improve overall airport efficiency. Their commitment to sustainability also drives the development ofenergy-efficientt security equipment. Thales continues to innovate in data analytics and machine learning to predict and prevent security breaches. These efforts solidify their role as a key enabler of modern secure and efficient air travel experiences globally.

- Leidos offers specialized security engineering services and advanced technology solutions for aviation infrastructure. The company focuses on integrating physical and cyber security measures to protect critical airport assets. Leidos recently deployed enhanced perimeter surveillance systems utilizing radar and optical sensors to detect unauthorized drone activity. Their expertise in systems integration allows for seamless connectivity between various security components, including screening checkpoints and command centers. Leidos works closely with government agencies to develop customized security architectures that address specific regional threats. The company also provides comprehensive training programs for security personnel,l ensuring effective operation of complex systems. By emphasizing operational readiness and risk mitigation,n Leidos supports airports in maintaining high security standards. Their innovative approach includes the use of predictive analytics to optimize resource allocation and response strategies. Leidos continues to expand its footprint through strategic collaborations and technology upgrades that enhance situational awareness. This holistic approach ensures that airports are well equipped to handle current and future security challenges effectively.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the airport security market primarily focus on technological innovation and strategic partnerships to maintaa in competitive advantage. Companies invest heavily in research and development to create advanced screening technologies such as computed tomography and artificial intelligence-driven analytics. These innovations enhance detection accuracy and improve passenger throughput. Strategic acquisitions allow firms to expand their product portfolios and enter new geographic markets. Collaborations with regulatory bodies ensure compliance with evolving international security standards. Integration of biometric and cybersecurity solutions addresses the growing need for comprehensive protection. Companies also prioritize customer support and maintenance services to build long-term relationships with airport authorities. Emphasis on sustainability leads to the development of energy-efficient security equipment. Digital transformation initiatives enable real-time monitoring and data-driven decision-making. These strategies collectively drive market growth and enhance the overall security posture of global aviation infrastructure.

MARKET SEGMENTATION

This research report on the global airport security market is segmented and sub-segmented into the following categories.

By Security System

- Screening and Scanning Systems

- Access Control and Biometrics

- Surveillance Systems

- Perimeter Security Systems

- Cybersecurity Systems

- Others

By Airport Size

- More than 15 Million Passengers Annually

- 5 to 15 Million Passengers Annually

- Less than 5 Million Passengers Annually

By Application

- Terminal

- Airside

- Landside

- Cargo Area

By Country

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. Which technology is leading the market?

Cybersecurity is emerging as a leading and fast-growing area because airports rely more on connected digital systems.

2. Which segment leads by location?

Terminal security is a major segment because passenger screening and access control are concentrated there.

3. Which equipment or system types are important?

Important systems include CCTV and video analytics, biometrics, access control, screening systems, perimeter protection, and RFID-based tracking.

4. Which region leads the market?

North America and Asia Pacific are both major regions, with North America holding a strong market share and Asia Pacific showing faster growth in several reports.

5. Who are the major players?

Major players include Thales, Smiths Detection, Leidos, Rapiscan Systems, Honeywell, IBM, Axis Communications, Siemens, and Collins Aerospace.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com