Global Anesthesia CO2 Absorbent Market Size, Share, Trends & Growth Forecast Report By Product (Medisorb, Amsorb, Litholyme, Soda-Lime, Dragersorb, Others), Type (Premium, Traditional), End-Use, Form and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From2026 to 2034

Market Size, 2025

$97.1 MnMarket Estimate, 2026

$104.7 MnMarket Forecast, 2034

$194 MnCAGR, 2026–2034

7.98%Global Anesthesia CO2 Absorbent Market Report Summary

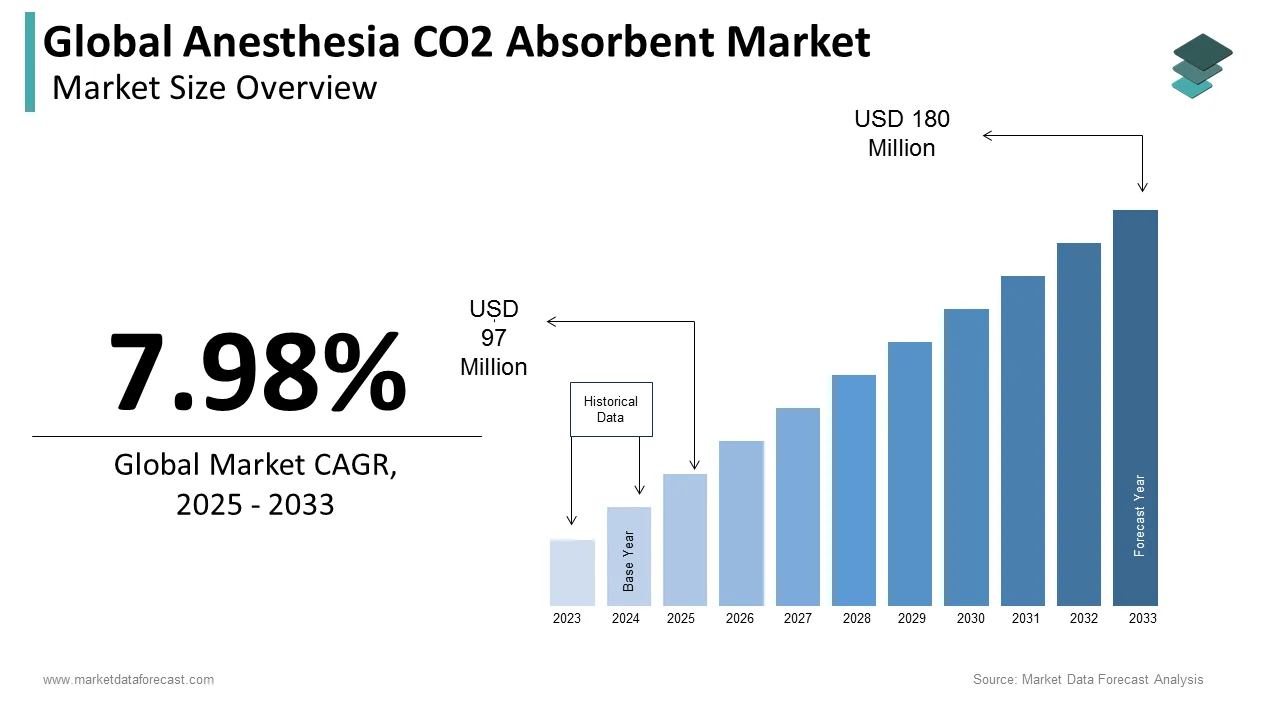

The global anesthesia CO2 absorbent market was valued at USD 97 million in 2025, is estimated to reach USD 104.74 million in 2026, and is projected to reach USD 194 million by 2034, growing at a CAGR of 7.98% from 2026 to 2034. Market growth is driven by the increasing number of surgical procedures, rising demand for safe anesthesia delivery systems, and growing awareness of patient safety in operating rooms. CO2 absorbents play a critical role in removing carbon dioxide from exhaled gases during anesthesia, ensuring efficient ventilation and minimizing complications. Advancements in absorbent formulations, increasing healthcare infrastructure, and the expansion of surgical services are further supporting market growth globally.

Key Market Trends

- Increasing number of surgical procedures worldwide.

- Rising demand for safe and efficient anesthesia systems.

- Growing focus on patient safety and operating room efficiency.

- Advancements in CO2 absorbent materials and formulations.

- Expansion of hospital infrastructure and surgical facilities.

Segmental Insights

- Based on product, the soda-lime segment dominated the global anesthesia CO2 absorbent market by capturing 58.3% share in 2025, driven by its widespread use and cost-effectiveness.

- Based on type, the traditional segment led the market with 64.4% share in 2025, supported by its established clinical usage and reliability.

Regional Insights

The global anesthesia CO2 absorbent market is witnessing steady growth across major regions due to increasing surgical demand and healthcare advancements.

- North America led the market in 2025 with 38.5% share, supported by advanced healthcare infrastructure and high surgical volumes.

- Europe followed with 29.6% share in 2025, driven by strong healthcare systems and patient safety standards.

- Asia-Pacific is emerging as a rapidly growing region due to expanding healthcare infrastructure and increasing awareness of anesthesia safety.

Competitive Landscape

The global anesthesia CO2 absorbent market is moderately competitive, with the presence of established medical device and healthcare product companies. Market players are focusing on improving product efficiency, enhancing safety profiles, and expanding their global presence. Innovation in absorbent materials and strategic partnerships is shaping competitive dynamics across the market.

Prominent companies operating in the global anesthesia CO2 absorbent market include Smiths Medical Inc., Armstrong Medical Ltd, Micropore Inc, Lowenstein Medical Ltd, Atrasorb, Drägerwerk AG, GE Healthcare, Allied Healthcare Products, Vyaire Medical Inc., Intersurgical Ltd., Meridian Medical Technologies, Molecular Products Group, and CareFusion.

Global Anesthesia CO2 Absorbent Market Size

The size of the global anesthesia CO2 Absorbent market was worth USD 97 million in 2025. The global market is anticipated to grow at a CAGR of 7.98% from 2026 to 2034 and be worth USD 194 million by 2034 from USD 104.74 million in 2026.

An anesthesia CO2 absorbent is a chemical substance used in anesthesia breathing circuits to remove carbon dioxide from a patient's exhaled breath. This process allows for rebreathing of anesthetic gases, which conserves expensive volatile agents, reduces environmental pollution, and prevents the patient from inhaling dangerous levels of CO2 (hypercapnia). These absorbents, typically composed of calcium hydroxide mixed with indicators and catalysts like soda lime or baralyme, are critical for maintaining physiological homeostasis and preventing hypercapnia in anesthetized individuals. The definition extends to include next-generation formulations designed to minimize the production of toxic byproducts such as Compound A and carbon monoxide when interacting with volatile anesthetics. According to a landmark study published in The Lancet (Weiser et al., 2015), an estimated 312.9 million major surgical procedures were performed globally in 2012. This volume has likely increased in the subsequent decade, creating a fundamental and recurring demand for essential consumables in operating theaters worldwide. The market operates under strict regulatory oversight from bodies like the Food and Drug Administration and the European Medicines Agency to ensure chemical stability and patient safety. Organizations such as the Anesthesia Patient Safety Foundation (APSF) emphasize the elimination of anesthesia-related complications. This dual focus drives the demand for advanced consumables, including high-purity CO2 absorbents, which are critical for preventing the formation of toxic byproducts and maintaining airway safety. The sector is increasingly focused on eco-friendly alternatives that reduce hazardous waste disposal costs associated with spent canisters. Unlike general medical supplies, these products require precise particle sizing and moisture content control to optimize gas flow and absorption efficiency. This niche yet vital market serves as the backbone of safe inhalational anesthesia, bridging chemical engineering with critical care medicine.

MARKET DRIVERS

Escalating Global Volume of Surgical Procedures Requiring General Anesthesia

The relentless increase in the global volume of surgical interventions drives the growth of the anesthesia CO2 absorbent market. These procedures necessitate the use of general anesthesia and closed-circuit breathing systems. As populations age and the prevalence of chronic diseases rises, the number of elective and emergency surgeries requiring intubation and gas anesthesia grows correspondingly. Research indicates that global surgical volume must increase significantly to meet healthcare needs, with the most substantial growth required in low- and middle-income countries. Every procedure utilizing a circle system requires the regular replacement of CO2 absorbent canisters, typically every 12 to 24 hours of use or when the color indicator changes, creating a consistent consumption cycle. Multiple studies show that in the United States alone, tens of millions of inpatient and outpatient surgeries are performed annually, with each procedure requiring multiple units of essential medical consumables. Furthermore, the expansion of ambulatory surgery centers, which perform millions of minor procedures annually, has decentralized surgical care while maintaining the need for reliable anesthesia delivery systems. The aging demographic, as highlighted by European population statistics, is driving higher rates of orthopedic, cardiac, and oncological surgeries that rely heavily on inhalational anesthesia. This direct correlation between surgical frequency and absorbent usage ensures a robust and inelastic demand trajectory that scales linearly with healthcare infrastructure development worldwide.

Stringent Safety Regulations Mandating Advanced Non-Toxic Formulations

The tightening of global safety regulations fuels the expansion of the anesthesia CO2 absorbent market. These regulations mandate the use of advanced CO2 absorbents free from strong bases like potassium hydroxide and sodium hydroxide. Traditional soda lime formulations were found to react with desflurane and sevoflurane to produce Compound A, a nephrotoxic agent, and carbon monoxide, posing severe risks to patient safety, especially during low-flow anesthesia. As per guidelines issued by the Food and Drug Administration, manufacturers are increasingly required to label and formulate absorbents that eliminate these dangerous byproducts, pushing hospitals to upgrade to newer generation products like Amsorb or LoFloSorb. The European Society of Anaesthesiology has also published consensus statements recommending the exclusive use of absorbents without strong alkali hydroxides to prevent airway fires and toxicity. Studies indicate that the adoption of safer absorbent formulations helps prevent the elevation of renal stress markers in patients by eliminating the production of toxic degradation products during surgery. Consequently, healthcare facilities are actively replacing legacy stockpiles with compliant alternatives to mitigate liability and adhere to best practice standards. This regulatory push forces a market-wide turnover of inventory, driving sales of higher-value, safety-certified absorbents. The imperative to protect patients from iatrogenic harm transforms regulatory compliance into a powerful commercial engine, compelling distributors and hospitals to prioritize advanced chemical compositions over cost-saving traditional options.

MARKET RESTRAINTS

High Operational Costs Associated with Frequent Replacement Cycles

The substantial operational cost burden imposed on healthcare facilities restricts the growth of the anesthesia CO2 absorbent market. This is largely caused by the frequent need to replace CO2 absorbent canisters, particularly in high-volume surgical centers. Unlike durable medical equipment, these absorbents are single-use consumables that must be discarded once exhausted, generating recurring expenses that strain hospital budgets, especially in resource-constrained environments. Financial reviews of perioperative departments confirm that supply costs represent a substantial portion of the total operating room budget, prompting scrutiny of all consumable categories, though specific expenditure percentages for anesthesia disposables vary by facility and case mix. In large tertiary care hospitals performing hundreds of surgeries weekly, the volume of spent canisters requires significant logistical management and disposal fees, further inflating the total cost of ownership. The price volatility of raw materials such as calcium hydroxide and indicator dyes exacerbates this issue, leading to unpredictable procurement costs. Clinical and supply chain studies indicate that facilities are increasingly adopting low-flow anesthesia techniques and indicator-based replacement protocols to optimize absorbent use and reduce waste; while this saves costs and reduces environmental impact, it requires vigilant monitoring to prevent absorbent desiccation and ensure patient safety. Furthermore, the lack of standardized pricing across different regions creates disparities in access, with developing nations often forced to utilize lower-quality or recycled alternatives. This economic pressure discourages the widespread adoption of premium, safer formulations in cost-sensitive markets, limiting the overall market value growth despite rising surgical volumes.

Environmental Concerns Regarding Hazardous Waste Disposal

The growing environmental scrutiny and regulatory complexity surrounding the disposal of spent CO2 absorbents constrain the expansion of the anesthesia CO2 absorbent market. These are often classified as hazardous chemical waste due to their alkaline nature and potential contamination with anesthetic gases. The disposal process requires specialized handling to prevent soil and water contamination, imposing strict protocols that many healthcare facilities find cumbersome and expensive to implement. According to waste management guidelines, standard calcium hydroxide-based CO₂ absorbents are typically classified as non-hazardous solid waste, allowing hospitals to dispose of them via standard medical or municipal waste streams without incurring the high costs and regulatory burdens associated with hazardous chemical waste. The carbon footprint associated with the manufacturing, transportation, and incineration of single-use plastic canisters filled with chemical granules is increasingly scrutinized by sustainability officers within health systems. Data from the Healthcare Without Harm initiative and recent lifecycle assessments suggest that the medical sector contributes significantly to global greenhouse gas emissions, with the supply chain (manufacturing and disposal of single-use devices) and waste anesthetic gases both being notable contributors. This environmental burden drives some institutions to seek alternative anesthesia techniques such as total intravenous anesthesia (TIVA) to bypass the need for absorbents entirely, thereby reducing market demand. Additionally, the lack of effective recycling programs for spent canisters means that tons of chemical waste end up in landfills annually, drawing negative public attention. Biodegradable or regenerative solutions are not yet commercially viable. Therefore, the environmental liability of traditional absorbents remains a persistent drag on market expansion and social license.

MARKET OPPORTUNITIES

Development of Regenerable and Eco-Friendly Absorbent Technologies

Research and commercialization of regenerative CO2 absorbent systems and eco-friendly formulations provide a transformative opportunity for the anesthesia CO2 absorbent market. These technologies are crucial for addressing both cost and environmental constraints. Innovations such as reusable canisters filled with regenerable sorbents or bio-based granules that decompose safely could revolutionize the economic and ecological landscape of anesthesia care. Recent research, including studies from institutions like MIT, indicates that emerging Metal Organic Frameworks (MOFs) and advanced zeolites are being engineered to capture carbon dioxide with high stability. Newer innovations specifically focus on electrochemical release mechanisms to avoid the high energy costs associated with traditional thermal (heating) regeneration, enabling more efficient reuse cycles. This technology could reduce the volume of hazardous waste generated by hospitals, aligning with global sustainability goals. Furthermore, the development of plant-based indicators and biodegradable casing materials offers a pathway to completely green anesthesia circuits. Patent activity and R&D in the medical device sector are increasingly focusing on sustainable anesthesia technologies, including regenerable gas scrubbers and capture systems. This trend is driven by the industry's push to reduce the carbon footprint of volatile anesthetic gases. Hospitals facing pressure to reduce their carbon footprint are eager pilots for such technologies, willing to invest in upfront capital for long-term savings. Companies that successfully bring these sustainable solutions to market will gain a first-mover advantage, capturing share from traditional manufacturers unable to adapt. This shift represents not just a product upgrade but a paradigm change in how anesthesia consumption is managed globally.

Expansion of Ambulatory Surgery Centers in Emerging Economies

The rapid proliferation of Ambulatory Surgery Centers (ASCs) in emerging economies offers a lucrative prospect for the anesthesia CO2 absorbent market expansion. These facilities are increasingly adopting modern anesthesia delivery systems, which require reliable CO2 absorbents. Healthcare infrastructure is developing rapidly in regions like the Asia-Pacific and Latin America. Consequently, there is a decisive shift from inpatient to outpatient care for minor and moderate procedures, aiming to improve efficiency and reduce costs. Research indicates that the number of Ambulatory Surgery Centers (ASCs) is expanding globally, with significant growth projected in developing nations across the Asia-Pacific region. This expansion is creating new, decentralized points of consumption for anesthesia and surgical supplies, driven by the demand for cost-effective outpatient care. These centers often prioritize compact, efficient anesthesia machines that rely on circle systems to minimize gas usage, thereby driving steady demand for high-quality absorbents. The rising middle class in countries like India and Brazil is fueling demand for elective surgeries such as cataract removal and endoscopies, which frequently utilize general anesthesia. Multiple studies confirm a structural shift where hospitals are increasingly outsourcing surgical services to specialized outpatient clinics and ASCs. These facilities are consolidating their supply chains, moving toward centralized procurement strategies to leverage bulk purchasing power and reduce operational costs. By tailoring packaging sizes and distribution models to the specific needs of smaller ASCs, manufacturers can penetrate this high-growth segment. The standardization of care protocols in these new facilities also creates an opening for educating providers on the benefits of premium, safe absorbents, fostering brand loyalty early in the market lifecycle.

MARKET CHALLENGES

Risk of Channeling and Inconsistent Absorption Efficiency

The technical risk of channeling within absorbent canisters, where gas flows through paths of least resistance rather than permeating the entire granule bed, limits the growth of the anesthesia CO2 absorbent market. This phenomenon leads to ineffective scrubbing and potential patient hypercapnia. This phenomenon occurs due to improper packing of granules, settling during transport, or variations in particle size distribution, compromising the safety of the anesthesia circuit. Clinical guidance from organizations like the Anesthesia Patient Safety Foundation emphasizes that the primary risks associated with CO₂ absorbents are desiccation-related chemical reactions, specifically the production of carbon monoxide and Compound A, as well as fire hazards. Inadequate CO₂ removal due to channeling is recognized as a cause of hypercapnia and respiratory acidosis, particularly during low-flow anesthesia. Manufacturers struggle to maintain perfect uniformity in granule shape and hardness across massive production batches, with even minor deviations causing significant performance drops. Laboratory assessments indicate that channeling is a performance risk primarily associated with low-flow anesthetic techniques, where reliance on the absorbent's efficiency is highest. This phenomenon is typically linked to loose canister packing or settling of granules rather than being a widespread defect across a specific percentage of commercial brands under high-flow conditions. This inconsistency forces clinicians to frequently monitor end-tidal CO2 levels with heightened vigilance, increasing cognitive load during surgery. The challenge is compounded by the variety of anesthesia machine models and canister designs, which interact differently with specific granule geometries. Ensuring absolute reliability requires rigorous quality control measures that drive up production costs, yet the consequence of failure is severe patient harm. Channeling remains a critical safety hurdle that undermines confidence in absorbent reliability. This issue will persist until automated packing technologies and smarter granule engineering eliminate this variability.

Supply Chain Vulnerabilities for Critical Raw Materials

The fragility of the global supply chain for critical raw materials such as calcium hydroxide, silica, and specific pH indicators impedes the expansion of the anesthesia CO2 absorbent market. These materials are susceptible to geopolitical disruptions and mining restrictions. The production of high-grade anesthesia absorbents relies on a limited number of suppliers for these chemical precursors, creating a bottleneck that can halt manufacturing during crises. The reliance on single-source suppliers for proprietary indicator dyes further exacerbates this vulnerability, as any disruption in chemical synthesis can halt entire production lines. The recent global logistics crisis demonstrated how quickly freight delays could deplete hospital stocks of essential anesthesia consumables, forcing facilities to ration supplies or delay elective surgeries. Recent industry surveys regarding hospital procurement reveal that supply chain reliability and vendor resilience have emerged as leading priorities for sourcing officers, often outweighing unit cost considerations in response to global logistics disruptions. Additionally, stringent import regulations on chemical substances in various countries add layers of complexity to cross-border trade, delaying replenishment. Diversifying the supplier base is difficult due to the rigorous certification processes required for medical-grade chemicals. The market remains exposed to external shocks that threaten the continuity of safe anesthesia delivery. This will continue until the supply chain becomes more resilient and localized.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Type, End-Use, Form & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leader Profiled | GE Healthcare, Allied Healthcare Products, Vyaire Medical Inc., Intersurgical Ltd |

SEGMENTAL ANALYSIS

By Product Insights

The Soda-Lime segment was the largest segment in the global anesthesia CO2 absorbent market and accounted for a 58.3% share in 2025. This prominence of the segment is supported by its long history of clinical use, widespread availability, and cost-effectiveness compared to newer proprietary formulations, making it the default choice for many healthcare facilities globally. One key reason for the growth of Soda-Lime is its deep integration into existing hospital infrastructure and its significantly lower procurement cost, which appeals to budget-conscious healthcare administrators. For decades, anesthesia machines worldwide have been calibrated and tested specifically for use with standard soda lime granules, creating a massive installed base that resists switching to alternative products without compelling safety mandates. According to research, traditional soda lime remains the dominant choice for carbon dioxide absorption in community hospitals, primarily driven by its lower acquisition cost compared to advanced, premium formulations. The raw materials required for production, primarily calcium hydroxide and sodium hydroxide, are abundant and inexpensive, allowing manufacturers to offer these products at a fraction of the price of premium alternatives. Comparative pricing data confirms that generic soda lime canisters are significantly less expensive than proprietary, advanced absorbents such as Amsorb or Litholyme, which incorporate chemical additives to prevent compound production or color reversion. In developing regions where healthcare budgets are tightly constrained, this price differential is the decisive factor in purchasing decisions. Furthermore, the familiarity of surgical staff with the color change indicators and handling characteristics of soda lime reduces training needs and operational friction. Until regulatory bodies universally mandate the phase-out of strong alkali hydroxides, the economic advantage and entrenched usage patterns of soda lime will ensure its continued market dominance despite known safety limitations. Also, this segment is boosted by the robust and ubiquitous supply chain network dedicated to soda lime, ensuring consistent availability even in remote or resource-limited settings. Unlike specialized absorbents that may rely on limited manufacturing sites or complex distribution channels, soda lime is produced by numerous chemical companies across every major continent, minimizing the risk of stockouts. The World Health Organization identifies carbon dioxide absorbents like soda lime as priority medical devices for safe surgery; however, surgical facilities in low- and middle-income countries frequently face supply chain challenges that impact the consistent availability of these essential items. The standardization of packaging sizes and canister compatibility across different anesthesia machine brands further cements its position as the universal standard. Manufacturers have optimized production lines for decades, achieving economies of scale that new entrants cannot easily match. Hospitals managing just-in-time inventory often rely on the widespread availability of generic soda lime, which benefits from a broad base of regional manufacturers, whereas proprietary blends may be subject to more constrained supply chains or sole-source dependencies. The ability to source this product locally in many regions also reduces transportation costs and carbon footprint, adding to its appeal. This logistical resilience ensures that, regardless of global supply chain disruptions, soda lime remains the most accessible option for maintaining continuous surgical operations, reinforcing its status as the market leader.

The Amsorb segment is likely to experience the fastest CAGR of 9.2% over the forecast period. This swift growth of the segment is fuelled by increasing awareness of patient safety risks associated with traditional absorbents and the subsequent shift toward non-toxic, calcium hydroxide-only formulations. A main factor pushing the growth rate of Amsorb is its unique chemical composition, which eliminates potassium hydroxide and sodium hydroxide, thereby preventing the formation of Compound A and carbon monoxide during anesthesia. These toxic byproducts, generated when traditional absorbents interact with volatile agents like sevoflurane and desflurane, pose significant risks of renal toxicity and cardiac stress, particularly during low-flow anesthesia techniques. Studies in the journal Anesthesiology and related research indicate that Amsorb prevents the formation of measurable Compound A during low-flow sevoflurane anesthesia, offering superior safety compared to strong alkali-containing soda lime. As regulatory agencies and professional societies increasingly emphasize patient safety, hospitals are proactively replacing legacy stocks with these safer alternatives to mitigate liability and improve outcomes. Various European clinical guidelines and anesthesia experts are increasingly moving towards or recommending alkali-free absorbents to enhance patient safety by eliminating toxic by-products, rather than relying on a specific, quantified percentage of protocols. The growing prevalence of low-flow anesthesia, favored for its cost savings and environmental benefits, further amplifies the need for safe absorbents since toxin concentration is higher in closed circuits. This clinical imperative drives hospitals to upgrade their supplies regardless of the higher unit cost, prioritizing patient welfare over short-term savings. As evidence mounts regarding the dangers of traditional formulations, the adoption of Amsorb accelerates across both developed and emerging markets. Additionally, the segment is helped by the formal endorsement of advanced absorbents like Amsorb by major medical regulatory bodies and the inclusion of their use in updated clinical practice guidelines. Health authorities in North America and Europe are issuing stronger warnings about the risks of carbon monoxide poisoning and airway fires linked to desiccated traditional absorbents, effectively pushing the market toward safer options. As per guidance documents from the Food and Drug Administration, manufacturers are encouraged to label products clearly regarding their potential to generate toxic compounds, influencing hospital formulary decisions. The Joint Commission and other accreditation organizations are increasingly scrutinizing anesthesia safety protocols, prompting facilities to adopt best-in-class materials to maintain their accredited status. Evidence from medical literature indicates a growing trend of hospital quality improvement teams updating purchasing policies to adopt absorbents free from strong base agents, such as calcium hydroxide-based products, to avoid caustic waste and increase safety. Furthermore, insurance providers and malpractice carriers are beginning to offer favorable terms to facilities that demonstrate adherence to the highest safety standards, including the use of non-toxic absorbents. This regulatory and financial pressure creates a powerful incentive for rapid market conversion. Guidelines are trickling down from top-tier academic centers to community hospitals, causing a surge in demand for Amsorb and similar premium products. Consequently, this has made it the fastest-growing segment in the industry.

By Type Insights

The Traditional type segment led the anesthesia CO2 absorbent market and occupied a share of 64.4% in 2025. This leading position of the segment is attributed to the vast number of healthcare facilities in developing nations and smaller clinics that prioritize cost containment over advanced safety features. A major reason for the domination of traditional absorbents is the severe economic constraints faced by healthcare systems in developing regions, where budget allocations for surgical supplies are minimal. In many parts of Asia, Africa, and Latin America, hospitals operate on thin margins and must prioritize essential life-saving equipment over premium consumables, making traditional soda lime the only viable option. The price gap between traditional and premium absorbents is substantial, with traditional options costing up to 50 percent less per unit, a difference that translates into significant annual savings for high-volume surgical centers. Governments in these regions often centralize procurement to leverage bulk pricing, further entrenching the market position of traditional suppliers who can meet large volume demands at rock-bottom prices. The lack of strict enforcement of safety regulations regarding toxic byproducts in these jurisdictions also reduces the pressure to switch to expensive alternatives. Until economic conditions improve and international aid programs specifically target anesthesia safety upgrades, the sheer volume of procedures in these cost-sensitive markets will ensure that traditional absorbents remain the dominant type globally. One more point that adds strength is the widespread presence of legacy anesthesia machines and the entrenched operational habits of medical staff who are accustomed to traditional absorbent characteristics. Many older anesthesia workstations, still in active service in thousands of hospitals worldwide, were designed and validated specifically for use with standard soda lime, and there is hesitation to introduce new formulations without extensive re-validation. Surgical teams often resist changing products due to perceived differences in granularity, dust production, or color change kinetics, fearing that unfamiliar variables could compromise workflow efficiency. Manufacturers of traditional absorbents capitalize on this stability by offering consistent packaging and familiar branding that reinforces user loyalty. The absence of immediate adverse events in many cases also leads to a false sense of security, delaying the transition to safer modern alternatives. This combination of hardware compatibility and human resistance to change creates a formidable barrier to entry for premium types, securing the dominant market share for traditional solutions.

The Premium type segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 8.5% between 2026 and 2034 due to the rising standard of care in developed nations and the increasing adoption of low-flow anesthesia techniques that require superior absorbent performance. A top factor behind the segment’s expansion is the global shift toward low-flow and minimal-flow anesthesia techniques, which maximize the efficiency of anesthetic gas usage but increase the risk of toxic byproduct accumulation if inferior absorbents are used. In low-flow systems, the rebreathing of gases is extensive, meaning any Compound A or carbon monoxide generated by the reaction between volatile agents and strong alkalis becomes highly concentrated, posing a direct threat to patient safety. Research shows that the adoption of low-flow techniques has increased in the last five years as hospitals seek to reduce costs and environmental impact. This trend necessitates the use of high-performance absorbents like Amsorb or Litholyme that guarantee safety even under extreme rebreathing conditions. Premium manufacturers are actively marketing their products as essential enablers of green anesthesia, aligning with sustainability goals while addressing safety concerns. As more anesthesiologists are trained in these efficient techniques, the demand for compatible premium absorbents rises in tandem. The technical superiority of these products in maintaining gas purity over extended periods makes them indispensable for modern anesthesia practices, driving their accelerated growth rate. Added support for this segment comes from the growing awareness of medical liability and the increasing frequency of litigation related to anesthesia complications, which prompts healthcare providers to invest in the safest available technologies. Hospitals and surgical centers are becoming increasingly risk-averse, recognizing that the marginal cost savings of traditional absorbents are negligible compared to the potential financial and reputational damage of a lawsuit involving patient harm from toxic byproducts. The financial incentive encourages administrators to upgrade their formularies to include only the highest safety-rated products. Furthermore, patient advocacy groups are demanding greater transparency and safety in surgical care, pressuring hospitals to adopt best practices. The premium segment benefits from this cultural shift toward zero-harm healthcare, where cost is secondary to outcome assurance. As the legal landscape evolves to hold providers to higher standards of care, the migration from traditional to premium absorbents accelerates, fueling the segment's rapid expansion.

REGIONAL ANALYSIS

North America Anesthesia CO2 Absorbent Market Analysis

North America was the top performer in the global anesthesia CO2 absorbent market and captured a 38.5% share in 2025. The region's dominance is propelled by its advanced healthcare infrastructure, high volume of surgical procedures, and a stringent regulatory environment that prioritizes patient safety above cost considerations. The United States serves as the primary engine of growth, driven by a high density of ambulatory surgery centers and tertiary care hospitals that rapidly adopt premium absorbent technologies. The presence of leading manufacturers and a robust distribution network ensures quick access to the latest innovations like Amsorb and Litholyme. Regulatory bodies such as the Food and Drug Administration actively issue safety communications regarding the risks of traditional absorbents, accelerating the market shift toward non-toxic alternatives. Furthermore, the high prevalence of malpractice litigation drives facilities to invest in the safest available products to mitigate legal risks. The region also leads in the adoption of low-flow anesthesia techniques, which require premium absorbents for safe operation. Despite higher product costs, the focus on value-based care and patient outcomes ensures that North America remains the largest and most sophisticated market for advanced CO2 absorbents, setting trends that influence global practices.

Europe Anesthesia CO2 Absorbent Market Analysis

Europe was the next prominent market for anesthesia CO2 absorbents and accounted for a 29.6% share in 2025. The growth of the European market is driven by a strong emphasis on environmental sustainability and harmonized safety standards across the European Union. The region presents a mature market where regulatory directives drive the transition from traditional to premium products. The country’s market has the influence of the European Medicines Agency and national health services that prioritize green anesthesia initiatives to reduce the carbon footprint of surgical care. Countries like Germany, France, and the United Kingdom are leading the adoption of eco-friendly and non-toxic formulations, supported by government-funded healthcare systems that can absorb higher upfront costs for long-term safety benefits. A study indicates that the aging population in Europe is driving an increase in complex surgical interventions, further boosting demand for reliable anesthesia supplies. The implementation of strict waste disposal regulations also favors premium absorbents that often come with better disposal guidelines or reduced hazardous classification. Furthermore, cross-border trade within the EU facilitates the rapid dissemination of new products and safety guidelines. Europe is becoming a critical hub for premium CO2 absorbents and sustainable anesthesia solutions, driven by a regional trend toward high-safety standards. However, cost containment remains a concern in some Eastern European nations.

Asia-Pacific Anesthesia CO2 Absorbent Market Analysis

The Asia-Pacific region is expanding rapidly in the global anesthesia CO2 absorbent market due to the massive healthcare infrastructure development in China, India, and J,apan and a growing awareness of anesthesia safety. While traditionally dominated by low-cost options, the region is witnessing a swift transition toward premium products in urban centers. China and India are at the forefront of this transformation, driven by government initiatives to upgrade medical facilities and reduce surgical complications in their vast populations. According to sources, China is investing billions in expanding its surgical capacity, with a specific focus on adopting international safety standards that favor premium absorbents. In India, the rising middle class and increasing medical tourism are pushing private hospitals to differentiate themselves by offering world-class safety protocols, including the use of non-toxic CO2 absorbents. Japan, with its super-aged society, maintains a high standard of care and early adoption of advanced medical technologies, driving steady demand for premium products. The proliferation of modern anesthesia machines capable of low-flow techniques in new hospitals creates a natural demand for compatible premium absorbents. Although rural areas still rely heavily on traditional soda lime due to cost, the rapid urbanization and increasing regulatory oversight in major economies are accelerating the market shift, positioning Asia-Pacific as the primary growth engine for the future.

Latin America Anesthesia CO2 Absorbent Market Analysis

Latin America occupies a notable position in the global market, which is driven primarily by Brazil and Mexico, where healthcare reforms and a growing private sector are beginning to unlock the potential for premium anesthesia products. The region benefits from increasing surgical volumes but faces challenges related to economic volatility and uneven access to advanced supplies. Brazil is the dominant force in the region, boasting the most sophisticated healthcare system in Latin America and a growing number of JCI-accredited hospitals that adhere to international safety standards. The private healthcare sector, which serves a significant portion of the population, is particularly aggressive in adopting advanced technologies to attract patients. In Mexico, proximity to the United States facilitates the flow of medical trends and products, with many border hospitals mirroring US safety protocols. However, public hospitals often struggle with budget constraints that limit them to traditional soda lime. Despite these disparities, the growing awareness among anesthesiologists about the risks of traditional absorbents is driving a grassroots movement toward safer alternatives. As economic stability improves and insurance coverage expands, the penetration of premium products in Latin America is expected to accelerate significantly.

Middle East and Africa Anesthesia CO2 Absorbent Market Analysis

The Middle East and Africa region is anticipated to grow in the global anesthesia CO2 absorbent market during the forecast period. However, this growth is constrained by infrastructure deficits and varying levels of economic development. The region represents a long-term frontier where gradual investments in healthcare safety could unleash substantial demand. South Africa and the Gulf states serve as the anchors of advancement in the region, with state-of-the-art medical cities in Saudi Arabia and the UAE importing the latest anesthesia technologies and premium consumables. In South Africa, the private healthcare sector maintains rigorous standards comparable to Europe, driving steady demand for premium products. However, the broader African continent faces significant challenges, with the World Health Organization estimating that many facilities still rely on outdated equipment and basic traditional absorbents due to cost and availability issues. Efforts by international NGOs to improve surgical safety are slowly introducing better products to remote areas, but progress is incremental. As political stability improves and healthcare spending rises in key nations, the Middle East and Africa are expected to transition from a marginal player to a meaningful contributor to the global market, particularly for premium segments in elite medical centers.

COMPETITIVE LANDSCAPE

The competition in the anesthesia CO2 absorbent market is characterized by a distinct divide between established manufacturers of traditional soda lime and innovative firms promoting premium non-toxic alternatives. While traditional players compete aggressively on price and volume, leveraging their entrenched presence in cost-sensitive regions and public hospitals, premium manufacturers differentiate themselves through clinical safety data and regulatory endorsements. The market is witnessing a gradual shift as increasing awareness of anesthesia-related complications drives hospitals to prioritize safety over initial procurement costs. Large medical device conglomerates use their bundled offerings of machines and consumables to lock in customers, creating high barriers for standalone absorbent suppliers. However, specialized companies retain a strong foothold by focusing exclusively on absorbent innovation and cultivating deep relationships with clinical stakeholders. Price wars are less common in the premium segment, where value is derived from risk mitigation and extended usage life. The competitive landscape is further shaped by regional regulatory variations, with stricter safety mandates in North America and Europe forcing faster adoption of advanced products compared to developing nations. Ultimately, the battle for market share is increasingly fought on the grounds of scientific evidence, environmental sustainability, and the ability to provide comprehensive support services to healthcare providers.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global anesthesia CO2 Absorbent market include

- Smiths Medical Inc.

- Armstrong Medical Ltd

- Micropore Inc

- Lowenstein Medical Ltd

- Atrasorb

- Dragerwerk AG

- GE Healthcare

- Allied Healthcare Products

- Vyaire Medical Inc.

- Intersurgical Ltd.

- Meridian Medical Technologies

- Molecular Products Group

- CareFusi on

TOP PLAYERS IN THE MARKET

- Drägerwerk AG & Co. KGaA stands as a global leader in medical and safety technology with a significant footprint in the anesthesia CO2 absorbent sector through its proprietary DrägerSorb brand. The German company leverages its extensive manufacturing of anesthesia workstations to create a seamless ecosystem where its machines and absorbents are optimized for joint performance. Recent actions include the expansion of its production facilities in Europe to ensure a stable supply chain for its calcium hydroxide-based granules that do not produce carbon monoxide. Dräger has also intensified its focus on sustainability by developing packaging solutions that reduce medical waste volume. The firm actively collaborates with hospitals to provide training on low-flow anesthesia techniques, which maximize the efficiency of their absorbents. By integrating digital monitoring capabilities into its anesthesia devices, Dräger enhances the safety profile of its consumables. This holistic approach strengthens their market position by offering customers a reliable and integrated solution for safe inhalational anesthesia delivery worldwide.

- Molecular Products Limited is a pioneering force in the market, renowned for inventing Amsorb, the first CO2 absorbent free from strong alkali hydroxides like potassium and sodium hydroxide. This British company revolutionized patient safety by eliminating the risk of Compound A formation and carbon monoxide production during anesthesia. Their contribution to the global market involves setting the benchmark for non-toxic absorbent formulations that are now widely recommended by safety organizations. Recent actions include scaling up manufacturing capacity to meet the surging demand from North American and European hospitals transitioning away from traditional soda lime. Molecular Products has also engaged in strategic partnerships with major anesthesia machine manufacturers to ensure compatibility and endorsement of their unique formulation. The company continues to invest in research to further improve the absorption capacity and lifespan of its granules. They have maintained a strict focus on clinical safety and evidence-based benefits. As a result, they have secured a loyal customer base among anesthesiologists who prioritize patient welfare over cost.

- Meridian Medical Technologies, a subsidiary of Pfizer Inc, plays a crucial role in the market as the manufacturer of Litholyme, a popular lithium hydroxide-based CO2 absorbent known for its high efficiency and safety profile. The company utilizes its vast pharmaceutical distribution network to ensure widespread availability of its absorbent products across diverse healthcare settings globally. Recent actions involve optimizing their supply chain logistics to reduce lead times and prevent stockouts in critical care facilities. Meridian has also launched educational campaigns targeting hospital procurement teams to highlight the long term cost benefits of using longer-lasting premium absorbents despite higher upfront costs. They are actively working on reducing the environmental impact of their product lifecycle through improved recycling programs for spent canisters. The firm leverages the scientific credibility of its parent company to validate the safety claims of Litholyme through continuous clinical studies. This commitment to quality and reliability allows Meridian to maintain a strong competitive edge in the premium segment of the anesthesia consumables market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the anesthesia CO2 absorbent market primarily employ product differentiation strategies by developing advanced formulations that eliminate toxic byproducts such as Compound A and carbon monoxide to ensure superior patient safety. Companies frequently invest in research and development to create absorbents with longer lifespans and higher absorption capacities, which reduce the frequency of changes and lower overall operational costs for hospitals. Another major strategy involves forming strategic partnerships and bundling agreements with anesthesia machine manufacturers to ensure their absorbents are recommended or pre-installed with new equipment. Market participants are also focusing on expanding their global distribution networks to penetrate emerging markets where surgical volumes are rising rapidly. Educational initiatives targeting anesthesiologists and hospital administrators about the risks of traditional soda lime and the benefits of premium alternatives are widely used to drive adoption. Additionally, firms are adopting sustainability practices by introducing eco-friendly packaging and waste reduction programs to align with the growing environmental concerns of healthcare institutions. These combined strategies help companies build brand loyalty and secure long-term contracts in a competitive landscape.

MARKET SEGMENTATION

This research report on the global anesthesia CO2 absorbent market has been segmented and sub-segmented based on product, type, end-use, form & region.

By Product

- Medisorb

- Amsorb

- Litholyme

- Soda-Lime

- Dragersorb

- Others

By Type

- Premium

- Traditional

By End-User

- Clinics

- Hospitals

- Others

By Form

- Powdered Form

- Granular Form

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. Which are the dominant product types in the global anesthesia CO2 absorbent market?

Soda lime and medisorb dominate the global anesthesia CO2 absorbent market due to their effectiveness in absorbing CO2 during anesthesia with wide hospital usage

2. What factors are driving growth in the global anesthesia CO2 absorbent market?

Growth drivers include rising surgeries worldwide, aging populations, chronic disease prevalence, and innovations in safer, eco-friendly CO2 absorbent formulations

3. How do advancements influence the global anesthesia CO2 absorbent market?

Innovations such as improved absorbent lifespan, reduced dust emissions, and enhanced exhaustion indicators boost efficiency and safety in the global anesthesia CO2 absorbent market

4. What role do hospitals play in the global anesthesia CO2 absorbent market?

Hospitals are the largest end-users in the global anesthesia CO2 absorbent market, accounting for major consumption due to high surgical patient volumes

5. How important is environmental sustainability in the global anesthesia CO2 absorbent market?

Eco-friendly anesthesia CO2 absorbents reduce harmful byproducts and align with hospital sustainability goals, gaining traction in the global anesthesia CO2 absorbent market

6. What challenges does the global anesthesia CO2 absorbent market face?

Challenges include regulatory compliance, high costs of premium absorbents, and varying regional safety standards in the global anesthesia CO2 absorbent market

7. How has COVID-19 affected the global anesthesia CO2 absorbent market?

COVID-19 initially slowed elective surgeries, impacting demand but subsequently increased focus on patient safety, boosting the global anesthesia CO2 absorbent market recovery

8. What regional trends are prominent in the global anesthesia CO2 absorbent market?

North America leads in market share, while Asia Pacific shows fastest growth due to expanding healthcare infrastructure and rising surgical procedures

9. What key companies lead the global anesthesia CO2 absorbent market?

Companies like CareFusion (BD), Dräger, and Smiths Medical lead the global anesthesia CO2 absorbent market with innovative product offerings and broad distribution

10. How do innovations improve patient safety in the global anesthesia CO2 absorbent market?

Innovations reduce toxic byproducts and improve CO2 removal efficiency during anesthesia, enhancing patient safety in the global anesthesia CO2 absorbent market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com