Asia Pacific Automotive AC Compressor Market Size, Share, Trends & Growth Forecast Report By Vehicle Type (Passenger Cars, HCVs, LCVs), By Compressor Type (Variable Displacement, Fixed Displacement, Electric Compressor), By Drive Type (Conventional, Electric), By Sales Channel (OEM, Aftermarket), and Country (India, China, Japan, South Korea, Australia, Rest of APAC) – Industry Analysis From 2026 to 2034.

Market Size, 2025

$2.46 BnMarket Estimate, 2026

$2.58 BnMarket Forecast, 2034

$3.77 BnCAGR, 2026–2034

4.85%Asia Pacific Automotive AC Compressor Market Size

The size of the Asia Pacific automotive AC compressor market was worth USD 2.46 billion in 2025. The Asia Pacific market is anticipated to grow at a CAGR of 4.85% from 2026 to 2034 and be worth USD 3.77 billion by 2034, up from USD 2.58 billion in 2026.

The automotive air conditioning (AC) compressor is a critical component in vehicle climate control systems, responsible for circulating refrigerant and maintaining cabin comfort. In the Asia Pacific region, the market for automotive AC compressors has evolved significantly due to rising consumer demand for enhanced vehicle interiors, increasing vehicle production, and growing awareness of thermal comfort in passenger vehicles as well as commercial transport.

The region’s hot and humid climatic conditions across countries like India, Indonesia, Thailand, and Vietnam further amplify the necessity for efficient cooling solutions in automobiles. As per the International Energy Agency, the number of air-conditioned vehicles registered in Southeast Asia has grown steadily, driven by both domestic consumption and export-oriented manufacturing bases.

Moreover, regulatory bodies such as Japan’s Ministry of Land, Infrastructure, Transport and Tourism and Australia’s Department of Climate Change, Energy, Environment and Water have emphasized energy efficiency and environmental compliance in automotive HVAC systems. This has led to increased adoption of advanced compressor technologies, including variable displacement and electric compressors, particularly in hybrid and electric vehicles.

In addition, the expansion of automotive manufacturing hubs in China and India has positioned the Asia Pacific region as a major contributor to global automotive AC compressor demand.

MARKET DRIVERS

Rising Vehicle Production and Sales Across the Region

One of the primary drivers of the Asia Pacific automotive AC compressor market is the substantial growth in vehicle production and sales, particularly in emerging economies such as India, Indonesia, and Vietnam. According to the International Organization of Motor Vehicle Manufacturers (OICA), Asia Pacific accounted for a large share of global automotive production in 2023, with China alone producing more than 28 million vehicles that year. This surge in automotive output directly translates into higher demand for AC compressors, as nearly all modern vehicles—ranging from passenger cars to commercial trucks—are equipped with air conditioning systems. In India, the Society of Indian Automobile Manufacturers (SIAM) reported that domestic vehicle sales reached over 4.2 million units in FY2023, marking a significant increase compared to previous years. Additionally, governments in several ASEAN countries have introduced policies promoting local manufacturing and investment in automotive infrastructure. For example, Thailand’s Board of Investment recorded an influx of USD 2.5 billion in new automotive sector investments in 2023, supporting both traditional and electric vehicle assembly plants

Increasing Demand for Electric and Hybrid Vehicles with Advanced Thermal Management Systems

The rapid adoption of electric and hybrid vehicles in the Asia Pacific region is another key driver influencing the automotive AC compressor market. Unlike conventional internal combustion engine (ICE) vehicles, EVs and HEVs rely on electric compressors for cabin cooling and battery thermal management, creating a distinct demand segment within the industry. These vehicles require high-efficiency, low-energy compressors capable of operating without engine-driven mechanical systems. Japanese automakers such as Toyota and Honda have also accelerated their electrification programs, incorporating advanced variable-speed compressors in hybrid models. South Korea and Singapore are also witnessing strong momentum in electric mobility, prompting local suppliers to develop compact, lightweight compressors compatible with battery-powered architectures. As the shift toward electrification intensifies, so does the demand for innovative compressor technologies across the Asia Pacific market.

MARKET RESTRAINTS

Stringent Environmental Regulations Affecting Refrigerant Choices

A significant restraint affecting the Asia Pacific automotive AC compressor market is the tightening of environmental regulations concerning refrigerants used in vehicle air conditioning systems. Governments across the region are enforcing stricter limits on greenhouse gas emissions, particularly targeting hydrofluorocarbon (HFC) refrigerants due to their high global warming potential (GWP). According to the United Nations Environment Programme (UNEP), several Asia Pacific countries—including China, India, and South Korea—are actively phasing out R-134a in favor of lower-GWP alternatives such as R-1234yf or natural refrigerants like CO₂. This transition necessitates modifications in AC compressor design and compatibility, increasing development costs for manufacturers. Japan’s Ministry of the Environment has mandated that all new vehicles must use low-GWP refrigerants by 2025, compelling automakers and compressor suppliers to adapt quickly.

Volatility in Raw Material Prices and Supply Chain Disruptions

Another critical constraint impacting the Asia Pacific automotive AC compressor market is the fluctuation in raw material prices and ongoing supply chain disruptions. Key materials such as aluminum, steel, copper, and synthetic refrigerants have experienced significant price volatility in recent years, primarily due to geopolitical tensions, trade restrictions, and pandemic-related logistical bottlenecks. In response, companies had to either absorb these increases or pass them on to automakers, affecting overall profitability. Furthermore, supply chain instability continues to disrupt operations across the region. Also, these constraints force companies to maintain higher inventory levels and buffer stocks, reducing operational flexibility and increasing capital expenditure.

MARKET OPPORTUNITIES

Growth in Aftermarket and Replacement Demand for AC Components

A major opportunity emerging in the Asia Pacific automotive AC compressor market is the rising demand from the aftermarket and replacement segments. With the expanding vehicle parc and aging fleet, there is a growing need for maintenance, repair, and replacement of AC systems, particularly in countries with large numbers of pre-owned vehicles. Also, the rise in disposable incomes and improved access to financing options in countries like Indonesia and the Philippines is encouraging vehicle owners to upgrade their existing AC systems for better efficiency and comfort. Also, independent workshops and third-party service providers are increasingly sourcing high-quality, cost-effective AC compressors from regional manufacturers, opening new revenue streams beyond original equipment manufacturer (OEM) contracts.

Expansion of Cooling Solutions in Commercial and Heavy-Duty Vehicles

The growing demand for air conditioning in commercial and heavy-duty vehicles presents a promising opportunity for the Asia Pacific automotive AC compressor market. Traditionally, only premium commercial vehicles featured full climate control systems, but evolving consumer expectations and government mandates are now pushing for standardization across fleets. With urbanization and e-commerce expansion driving freight and logistics activities across the region, the need for comfortable and efficient driver environments is expected to further fuel the adoption of advanced AC compressors in commercial transportation.

MARKET CHALLENGES

Integration of Electric Compressors in EV Platforms with Limited Standardization

One of the foremost challenges facing the Asia Pacific automotive AC compressor market is the integration of electric compressors into electric vehicle (EV) platforms, where standardization remains limited. Unlike traditional mechanical compressors driven by internal combustion engines, electric compressors must be compatible with varying voltage systems, cooling requirements, and vehicle architectures across different EV models. Like, EV platforms developed by Chinese, Japanese, and Korean automakers often feature proprietary thermal management designs, making it difficult for compressor manufacturers to offer universal solutions. This lack of standardization increases development time and costs, particularly for smaller suppliers seeking to enter the EV market. Apart from these, electric compressors must operate efficiently without drawing excessive power from the vehicle’s battery, which can impact driving range.

Intensifying Competition from Domestic and Global Players

The Asia Pacific automotive AC compressor market is experiencing heightened competition from both established global players and rapidly growing domestic manufacturers. Multinational corporations such as Denso, Sanden, and Mahle dominate through technological leadership and long-standing relationships with major automakers. However, local firms in China, India, and Southeast Asia are aggressively expanding their production capacities and improving product quality to capture market share. Many of these regional players are leveraging localized production and lower labor costs to undercut international brands, making it challenging for global firms to maintain profit margins. Furthermore, the consolidation of automotive suppliers and the formation of joint ventures among tier-1 vendors are reshaping the competitive landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Vehicle Type, Compressor Type, Drive Type, Sales Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Continental AG, Hanon Systems, Toyota Industries Corporation, Mitsubishi Heavy Industries Ltd., Subros Ltd, Mahle GmbH, Denso Corporation, Sanden Corporation, Valeo SA, and BorgWarner Inc. |

SEGMENTAL ANALYSIS

By Vehicle Type Insights

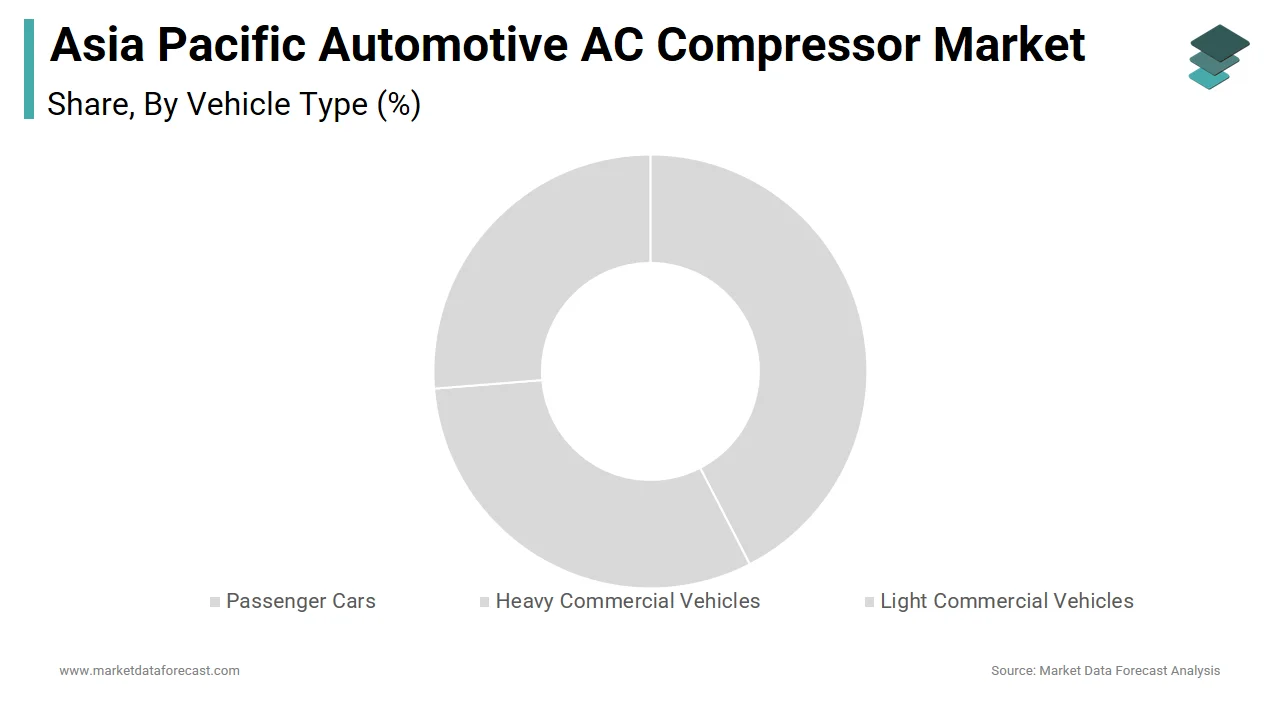

The passenger cars segment dominated the Asia Pacific automotive AC compressor market by accounting for 62.4% of total demand in 2025. This dominance is primarily driven by the sheer volume of passenger vehicle production and sales across the region, particularly in China, India, and Southeast Asia. Additionally, rising disposable incomes and urbanization have significantly boosted vehicle ownership rates. The Ministry of Road Transport and Highways of India reported that domestic passenger car sales exceeded 3.1 million units in FY2023, reflecting sustained consumer demand for comfort-oriented features such as air conditioning. Moreover, governments in several countries are mandating climate control systems in new vehicles to enhance occupant safety and comfort.

The Light commercial vehicles (LCVs) represent the fastest-growing segment in the Asia Pacific automotive AC compressor market, projected to expand at a CAGR of 7.9%. This rise is primarily attributed to the rapid expansion of e-commerce, logistics, and last-mile delivery services across the region. Also, LCV production in Southeast Asia increased, driven by strong demand from transport companies seeking modern, driver-friendly fleets. In response to evolving customer expectations, automakers are increasingly offering air-conditioned cabins even in entry-level LCVs. Furthermore, regulatory bodies in Australia and Japan have introduced guidelines encouraging better working conditions for commercial drivers, indirectly boosting the adoption of AC-equipped LCVs.

By Compressor Type Insights

The variable displacement compressors held the largest share of the Asia Pacific automotive AC compressor market by capturing 48.9% of total demand in 2025. Their widespread adoption is attributed to their ability to adjust cooling capacity based on ambient conditions, thereby improving fuel efficiency and reducing engine load. These compressors are extensively used in mid-to-high-end passenger vehicles, particularly in Japan, South Korea, and China, where fuel economy regulations are stringent. Variable displacement compressors are now standard in nearly all new gasoline and diesel-powered sedans and SUVs sold in the country. Also, automakers are integrating these compressors with advanced climate control systems to enhance user experience and energy efficiency. Moreover, environmental mandates aimed at reducing carbon emissions have further reinforced their adoption.

Electric compressors are emerging as the fastest-growing segment in the Asia Pacific automotive AC compressor market, expected to grow at a CAGR of 13.2%. This surge is primarily driven by the exponential growth of electric and hybrid vehicle production across the region. China leads this transition. Unlike traditional mechanical compressors, electric variants operate independently of the engine, making them essential components in battery-powered vehicles for both cabin cooling and battery thermal management. Japanese automakers such as Toyota and Honda have also accelerated their electrification strategies, incorporating high-efficiency electric compressors in their hybrid and plug-in hybrid models. Besides, South Korean manufacturers like Hyundai and Kia have introduced new EV platforms requiring compact, lightweight compressors capable of delivering consistent performance without draining the battery excessively.

By Drive Type Insights

The conventional drive type commanded the Asia Pacific automotive AC compressor market. This segment includes vehicles powered by internal combustion engines (ICEs), which continue to form the bulk of the region's automotive fleet despite growing electrification efforts. These vehicles rely on mechanically driven AC compressors connected to the engine via a belt or clutch mechanism, ensuring consistent cooling performance under varying operating conditions. In addition, the affordability and widespread availability of spare parts and servicing infrastructure for conventional AC systems make them highly attractive to consumers in emerging economies. Moreover, government policies in several countries still focus on improving fuel efficiency rather than outright banning ICE vehicles, allowing this segment to maintain its stronghold.

The electric drive type is the quickly surging segment in the Asia Pacific automotive AC compressor market, expanding at a CAGR of 14.1%. This rapid growth is primarily fueled by the aggressive push toward electric mobility, supported by government incentives, charging infrastructure development, and increasing consumer awareness. China continues to lead the EV revolution, with the China Association of Automobile Manufacturers noting that EV production crossed 9 million units in 2023. These vehicles require electric AC compressors that function independently of the engine, ensuring efficient thermal management for both the cabin and the battery pack. Similarly, South Korea and Japan are witnessing strong momentum in electric mobility, with automakers like Hyundai, Kia, and Toyota introducing new EV platforms designed for superior energy efficiency.

By Sales Channel Insights

The OEM (Original Equipment Manufacturer) channel possessed the largest share of the Asia Pacific automotive AC compressor market by accounting for 68.1% of total sales in 2025. This dominance is because nearly all new vehicles in the region are factory-fitted with air conditioning systems, necessitating direct procurement from compressor manufacturers. Similarly, Japanese automakers such as Toyota and Honda integrate AC compressors sourced from tier-1 suppliers like Denso and Sanden into their mass-produced models. India has also seen a surge in OEM demand, with the Society of Indian Automobile Manufacturers (SIAM) reporting that air conditioning has become a standard feature even in budget hatchbacks and subcompact SUVs. This trend reflects shifting consumer preferences and competitive product differentiation strategies among automakers.

The aftermarket segment is the fastest-growing sales channel in the Asia Pacific automotive AC compressor market, projected to expand at a CAGR of 9.3%. This growth is primarily driven by the rising number of aging vehicles on the road and increasing consumer preference for cost-effective repair and maintenance solutions. This trend is mirrored in China, where a key year-on-year growth in the automotive aftermarket sector. Moreover, rising disposable incomes and improved access to financing options in Southeast Asian countries like Indonesia and the Philippines are encouraging vehicle owners to upgrade their existing AC systems for enhanced efficiency and comfort. Independent workshops and third-party service providers are increasingly sourcing high-quality, compatible compressors from regional manufacturers and creating new revenue streams beyond OEM contracts.

KEY MARKET PLAYERS

Some of the noteworthy companies in the APAC automotive AC compressor market profiled in this report are Continental AG, Hanon Systems, Toyota Industries Corporation, Mitsubishi Heavy Industries Ltd., Subros Ltd, Mahle GmbH, Denso Corporation, Sanden Corporation, Valeo SA, and BorgWarner Inc.

COUNTRY LEVEL ANALYSIS

China was at the forefront of the Asia Pacific automotive AC compressor market by contributing 40.9% of regional demand in 2025. As the world’s largest automotive manufacturer, China produces millions of passenger and commercial vehicles annually, each equipped with air conditioning systems. Rising consumer expectations and government-mandated comfort features have made AC systems standard even in budget vehicles.

In addition, China’s electric vehicle boom is further driving demand for advanced electric compressors.

India’s demand is driven by rising vehicle production, expanding middle-class purchasing power, and increasing penetration of air conditioning in entry-level vehicles. The Ministry of Road Transport and Highways mandated improved driver comfort standards, encouraging automakers to equip commercial vehicles with climate control systems.

Additionally, the growing aftermarket for AC components is supporting demand, particularly among the large base of pre-owned vehicle owners seeking repairs and upgrades.

Japan is a technologically advanced market with premium demand, which is distinguished by its focus on high-efficiency, variable displacement, and electric compressors tailored for premium and hybrid vehicles. With one of the most mature automotive industries globally, Japan places a strong emphasis on fuel efficiency, emissions reduction, and occupant comfort. Also, nearly all new vehicles sold in the country are equipped with advanced climate control systems, including multi-zone air conditioning and intelligent thermal management. Japanese automakers such as Toyota and Honda have pioneered the integration of electric compressors in hybrid and plug-in hybrid models.

South Korea is characterized by its growing emphasis on electric mobility and high-tech thermal management solutions. With Hyundai and Kia aggressively expanding their EV portfolios, the demand for electric compressors has surged. In addition to OEM demand, South Korea is investing heavily in after-sales service infrastructure. It’s strategic shift toward electrification and digital vehicle platforms positions it as a key growth market for advanced AC compressor technologies in the Asia Pacific region.

Thailand is serving as a key manufacturing hub for both domestic and export-oriented vehicle production. Major brands such as Toyota, Honda, and Isuzu operate large-scale plants in the country, all of which integrate air conditioning systems into their vehicle lineups.

TOP LEADING PLAYERS IN THE MARKET

Denso Corporation (Japan)

Denso is a global leader in automotive air conditioning systems and holds a dominant position in the Asia Pacific automotive AC compressor market. The company supplies high-efficiency compressors for both conventional and electric vehicles, with strong partnerships across Japanese, Korean, and Chinese automakers. Denso's expertise lies in developing advanced thermal management solutions that enhance energy efficiency and occupant comfort.

Sanden Holdings Corporation (Japan)

Sanden is a key player known for its innovative variable displacement and electric compressors tailored for diverse vehicle platforms. With a strong presence in Japan, China, and Southeast Asia, Sanden supports major automakers by providing reliable, high-performance cooling systems. The company invests heavily in R&D to stay ahead of evolving industry demands, particularly in hybrid and electric mobility applications.

Mahle GmbH (Germany, with major operations in China and India)

Mahle maintains a significant footprint in the Asia Pacific region through its extensive manufacturing and distribution network. The company offers a wide range of compressors designed for fuel-efficient and electric vehicles, catering to OEMs and aftermarket channels. Mahle’s strategic collaborations with local suppliers and commitment to sustainability reinforce its competitive edge in the regional market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Expansion into High-Growth Markets through Local Manufacturing and Partnerships

Leading companies are strengthening their regional presence by setting up local production facilities and forming strategic alliances with domestic players. These moves allow them to reduce logistics costs, comply with local regulations, and better serve growing industrial sectors such as water treatment and mining.

Product Innovation and Customization for Diverse Applications

To meet the evolving needs of different industries, key players are investing in research and development to create specialized polyacrylamide variants. This includes developing low-residue, high-purity, and bio-compatible formulations that cater to sensitive applications like drinking water purification and pharmaceutical processing.

Focus on Sustainability and Eco-Friendly Polymer Development

Amid rising environmental concerns, manufacturers are adopting green chemistry principles and enhancing product safety profiles. This includes improving purification techniques to minimize acrylamide residue and exploring hybrid or biodegradable alternatives to maintain competitiveness in environmentally conscious markets.

COMPETITION OVERVIEW

The competition in the Asia Pacific automotive AC compressor market is intense, characterized by a mix of global Tier-1 suppliers and rapidly emerging regional manufacturers. Established players such as Denso, Sanden, and Mahle dominate through technological leadership, long-term relationships with automakers, and continuous innovation in thermal management systems. However, domestic firms in China, India, and Southeast Asia are aggressively expanding their capabilities, leveraging cost advantages and localized supply chains to capture market share.

Market participants are increasingly focusing on electric and hybrid vehicle technologies, where differentiation depends on energy efficiency, compact design, and integration with smart climate control systems. As regulatory standards tighten across the region, companies must continuously adapt their offerings to align with environmental compliance requirements while maintaining performance benchmarks.

Additionally, competition extends beyond product quality to include after-sales service, technical support, and customization capabilities. With rising consumer expectations and increasing demand from both OEM and aftermarket segments, companies must innovate swiftly and scale efficiently to maintain a strong foothold in this dynamic and evolving market landscape.

RECENT MARKET DEVELOPMENTS

- In March 2024, Denso Corporation announced the launch of a new line of ultra-compact electric compressors specifically designed for battery electric vehicles (BEVs), targeting the growing EV market in China and South Korea.

- In June 2024, Sanden Holdings expanded its manufacturing facility in Thailand to increase production capacity for variable displacement compressors, aiming to strengthen its supply chain and meet rising demand from ASEAN automakers.

- In September 2024, Mahle GmbH formed a joint venture with an Indian automotive component manufacturer to develop cost-effective, high-efficiency compressors tailored for entry-level passenger cars and commercial vehicles in the Indian market.

- In November 2024, Hanon Systems opened a new R&D center in Shanghai focused on next-generation thermal management solutions, including advanced refrigerants and electric compressor integration for EV platforms in the Asia Pacific region.

- In January 2025, Valeo partnered with a leading Japanese electronics firm to co-develop intelligent climate control systems that optimize compressor performance based on real-time cabin and battery conditions, enhancing energy efficiency in hybrid and electric vehicles.

MARKET SEGMENTATION

This Asia Pacific automotive AC compressor market research report is segmented and sub-segmented into the following categories.

By Vehicle Type

- Passenger Cars

- Heavy Commercial Vehicles

- Light Commercial Vehicles

By Compressor Type

- Variable Displacement

- Fixed Displacement

- Electric Compressor

By Drive Type

- Conventional

- Electric

By Sales Channel

- OEM

- Aftermarket

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

1. What factors are driving the Asia Pacific automotive AC compressor market?

The Asia Pacific automotive AC compressor market is driven by rapid growth in vehicle production, rising demand for passenger cars with air conditioning, government initiatives supporting electric vehicles, and technological advancements in compressor efficiency and design

2. What challenges does the Asia Pacific automotive AC compressor market face?

The Asia Pacific automotive AC compressor market faces challenges such as volatile raw material prices, supply chain disruptions, high initial costs for advanced compressors, and the need to comply with strict environmental regulations and emission standards

3. What opportunities exist in the Asia Pacific automotive AC compressor market?

Opportunities in the Asia Pacific automotive AC compressor market include the expansion of electric and hybrid vehicle segments, increased investment in manufacturing, adoption of variable displacement and electric compressors, and growth in aftermarket services and remanufacturing

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com