Asia Pacific Automotive Operating System Market Size, Share, Growth, Trends, And Forecast Research Report, Segmented By OS, Commercial vehicle, EV Application and Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From (2025 to 2033)

Asia Pacific Automotive Operating System Market Size

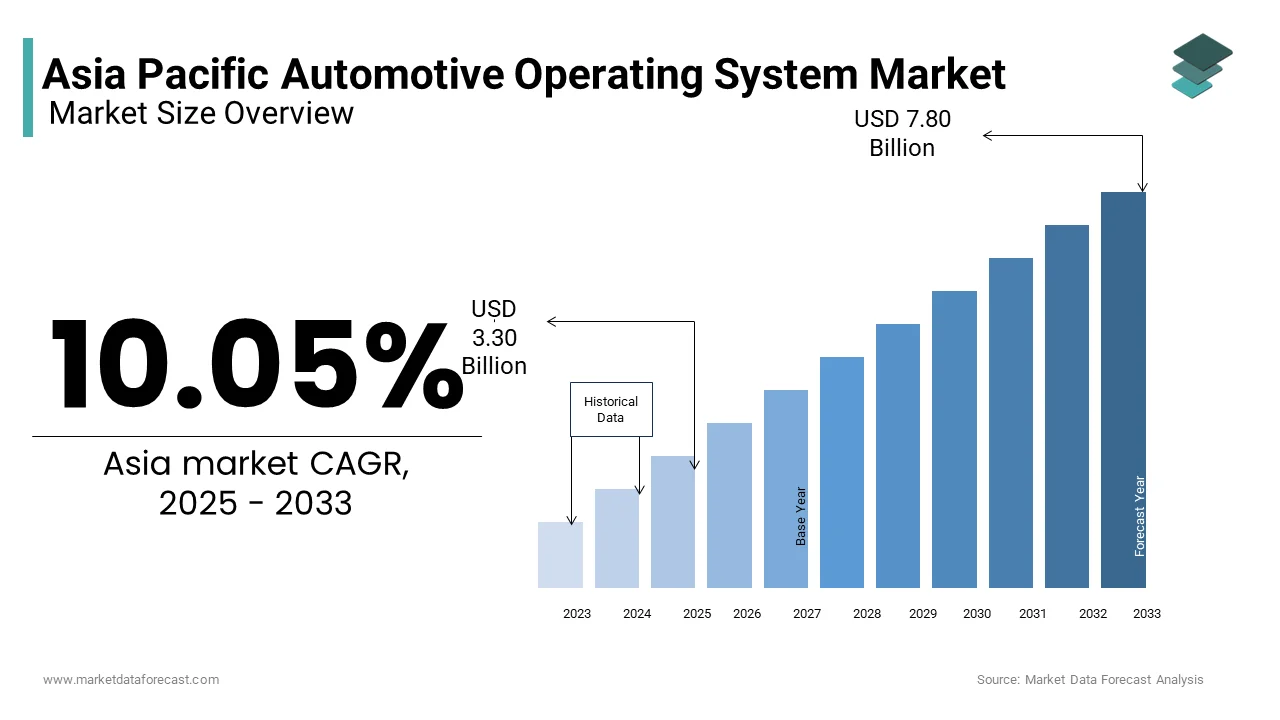

The Asia Pacific automotive operating system market is anticipated to jump from USD 3.30 billion in 2024 to USD 7.80 billion by 2033, growing at a CAGR of 10.05%.

An automotive operating system (OS) is a specialized software platform designed to manage vehicle functions, support infotainment systems, enable driver assistance features, and facilitate connectivity with external devices and networks. As vehicles become increasingly digitized and autonomous, automotive operating systems have evolved from being mere control mechanisms to becoming central to the driving experience, safety, and vehicle intelligence.

In addition, as per the Asian Development Bank, the region accounted for nearly 60% of global automotive production in recent years, driven by manufacturing hubs like China, Japan, and South Korea. These developments provide a strong foundation for embedding sophisticated operating systems into new vehicle models.

The increasing adoption of electric vehicles (EVs), smart mobility solutions, and over-the-air (OTA) updates has further intensified interest in automotive OS development across the region. Governments in several APAC nations are promoting indigenous R&D initiatives to reduce reliance on foreign software platforms and build homegrown digital ecosystems within the automotive sector.

Therefore, the Asia Pacific automotive operating system market is transitioning and is setting the stage for sustained innovation and investment.

MARKET DRIVERS

Surge in Demand for Connected and Autonomous Vehicles

The rising demand for connected and autonomous vehicles is primarily driving the Asia Pacific automotive operating system market. These vehicles rely on robust, secure, and scalable operating systems to manage complex functionalities such as real-time navigation, driver assistance, and remote diagnostics.

In China, the Ministry of Industry and Information Technology has been actively supporting the development of intelligent transportation systems, resulting in a significant increase in semi-autonomous and fully autonomous vehicle trials. According to the China Association of Automobile Manufacturers, more than 3 million connected cars were sold in China in 2023, many of which operated on embedded automotive OS platforms like Alibaba’s YunOS and QNX-based systems.

Similarly, in Japan, major automakers are integrating proprietary and third-party operating systems into their next-generation models to support vehicle-to-everything (V2X) communication and AI-powered driving assistants. South Korea is also witnessing increased collaboration between tech firms and automotive manufacturers to develop localized operating systems tailored for smart mobility applications.

Expansion of Electric Vehicle Manufacturing and Software Integration

The rapid expansion of electric vehicle (EV) manufacturing across the Asia Pacific is another key factor propelling the growth of the automotive operating system market. Unlike traditional internal combustion engine vehicles, EVs require highly integrated software platforms to manage battery performance, energy efficiency, and user interfaces, making automotive OS a critical component.

China leads this trend, as it remains the world’s largest EV market. According to the China Association of Automobile Manufacturers, over 9 million electric vehicles were produced in China in 2023, with companies like BYD and NIO developing proprietary operating systems to enhance vehicle intelligence and customer engagement.

Similarly, in India, the government’s push for electrification under the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme has spurred domestic automakers to integrate advanced software systems into EVs. EV sales in India grew in 2023, necessitating more sophisticated onboard operating environments.

Japan and South Korea are also investing heavily in EV software ecosystems. Companies like Panasonic and Hyundai are partnering with global tech firms to embed automotive operating systems that support OTA updates, voice-controlled dashboards, and predictive maintenance features. So, this shift toward software-defined vehicles is significantly boosting the role and relevance of automotive operating systems across the Asia Pacific.

MARKET RESTRAINTS

Fragmented Regulatory Frameworks Across APAC Countries

The fragmented regulatory environment across different countries, which complicates compliance and slows down software standardization, is a major restraint affecting the Asia Pacific automotive operating system market. Each nation imposes unique requirements regarding data privacy, cybersecurity, and software certification, making it difficult for international vendors to deploy uniform automotive OS solutions. In China, the Cyberspace Administration mandates strict data localization rules, requiring all vehicle-generated data to be stored within the country. According to the Chinese Academy of Cybersecurity and Law, these regulations have delayed the rollout of certain foreign-developed automotive operating systems in the local market.

Likewise, India has introduced stringent data protection laws under the Digital Personal Data Protection Act, compelling automotive software providers to ensure compliance with data handling protocols before deployment. As per the Data Security Council of India, several multinational automotive OS vendors have had to modify their platforms to meet Indian standards, adding time and cost to product launches. Also, in Southeast Asia, ASEAN member states have yet to harmonize vehicle software regulations, leading to inconsistent implementation across markets like Thailand, Malaysia, and Indonesia.

These inconsistencies will continue to hinder the widespread adoption of standardized automotive operating systems across the Asia Pacific.

High Development and Integration Costs for Custom Automotive OS Platforms

The high cost associated with developing and integrating custom operating systems tailored for specific vehicle models or brands is also restraining the growth of the Asia Pacific automotive operating system market. Unlike consumer electronics, automotive operating systems must meet rigorous safety, reliability, and longevity standards, which increases both research and deployment expenses.

In Japan, automotive manufacturers such as Nissan and Mazda face considerable financial barriers when designing proprietary operating systems for next-generation electric and hybrid models. According to the Japan Automobile Research Institute, automotive software development costs have risen over the past five years due to the need for functional safety certifications like ISO 26262 and ASPICE. Similarly, in Australia, where local manufacturing is minimal, but EV imports are rising, automotive OS developers struggle with retrofitting foreign systems onto imported vehicles, leading to compatibility issues and increased customization costs.

MARKET OPPORTUNITY

Growth of Smart Mobility and Shared Transportation Ecosystems

The rapid expansion of smart mobility and shared transportation services is one of the most promising opportunities for the Asia Pacific automotive operating system market. Ride-hailing platforms, car-sharing services, and autonomous mobility-on-demand systems rely heavily on intelligent, cloud-connected operating environments that support real-time monitoring, fleet management, and enhanced user experiences.

Singapore is actively promoting smart mobility initiatives, encouraging ride-sharing and autonomous public transport projects. According to the Infocomm Media Development Authority (IMDA), Singaporean startups and tech firms are collaborating with automotive OS developers to create embedded platforms that support dynamic route optimization, driver analytics, and in-vehicle commerce.

In India, ride-hailing companies like Ola and Uber are integrating customized automotive operating systems into their fleets to enhance driver-passenger interaction, optimize fuel efficiency, and ensure regulatory compliance. As per the Federation of Automobile Dealers Associations (FADA), fleet operators are among the fastest adopters of connected vehicle operating systems, particularly in Tier 1 cities.

Meanwhile, in China, state-backed smart city programs are facilitating the deployment of connected and autonomous taxis equipped with proprietary operating systems developed by companies like Baidu and Huawei.

Increasing Demand for Over-the-Air (OTA) Updates and Remote Diagnostics

The increasing demand for over-the-air (OTA) updates and remote diagnostics in modern vehicles presents a significant opportunity for the Asia Pacific automotive operating system market. Consumers and automakers alike are recognizing the value of software-driven enhancements that allow for real-time upgrades without requiring physical visits to service centers.

In Japan, automotive OEMs such as Toyota and Subaru have integrated OTA capabilities into their latest vehicle models, enabling seamless software improvements related to performance, security, and user interface. South Korean automakers are following suit, with companies like Hyundai and Kia incorporating OTA-compatible operating systems into their electric and hybrid lineups. In Australia, the rise of premium EV imports and many of which come with OTA-enabled operating systems, has created new avenues for local dealerships and aftermarket service providers to offer continuous software support.

MARKET CHALLENGES

Complexity in Ensuring Functional Safety and Compliance with Global Standards

The complexity involved in ensuring functional safety and compliance with global standards such as ISO 26262 and AUTOSAR is also a challenging factor confronting the Asia Pacific automotive operating system market. Unlike consumer-grade operating systems, automotive OS must undergo extensive validation processes to guarantee reliability, fault tolerance, and fail-safe operations. This extended timeline results from rigorous testing procedures mandated by international safety norms, which are essential for export-oriented manufacturers targeting European and North American markets.

Japanese automakers face similar hurdles, particularly in integrating third-party automotive operating systems with in-house vehicle architectures while maintaining compliance with ASIL (Automotive Safety Integrity Level) requirements. These complexities cause a delay in time to market and also increase development costs.

Intense Competition from Proprietary and Open-Source Operating Systems

Intense competition from both proprietary and open-source platforms, creating a fragmented landscape where differentiation is difficult, is another serious challenge for the Asia Pacific automotive operating system market. Major global players such as Google (Android Automotive), BlackBerry (QNX), and Linux-based AGL (Automotive Grade Linux) are vying for dominance alongside emerging domestic alternatives from China and India.

In China, major automakers are adopting Huawei’s HarmonyOS Automotive and Baidu’s Apollo OS for in-car infotainment and autonomous driving functions, as per the China Electronics Chamber of Commerce. These homegrown platforms are backed by strong government support and ecosystem partnerships, posing a direct challenge to Western operating systems.

Similarly, in India, Mahindra and Tata Motors are exploring partnerships with domestic software developers to create indigenous automotive operating systems, reducing dependency on foreign platforms and aligning with national self-reliance goals. As per the Automotive Component Manufacturers Association of India (ACMA), local automakers are prioritizing indigenous software stacks to avoid licensing fees and ensure long-term scalability.

This competitive landscape is making market entry and sustainability increasingly challenging without strategic alliances or deep technical expertise.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| CAGR | 10.05% |

| Segments Covered | By OS, Commercial Vehicle, EV Application, And Region. |

| Various Analyses Covered | Global, Regional, Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of APAC |

| Market Leaders Profiled | Blackberry Limited, Huawei Technologies Co., Ltd., Automotive Grade Linux, Microsoft Corporation, Apple Inc., Alphabet Inc., Green Hills Software, Nvidia Corporation, Siemens, Red Hat, Inc., Wind River Systems, Inc |

SEGMENTAL ANALYSIS

By OS Insights

The QNX segment commanded the largest share of the Asia Pacific automotive operating system market and captured 37.5% of total revenue in 2024. The growth of the QNX segment is primarily attributed to its widespread use in mission-critical vehicle applications such as instrument clusters, infotainment systems, and ADAS modules, where real-time performance and functional safety are paramount. South Korea’s automotive industry also demonstrates strong QNX adoption, particularly among companies like Hyundai and Kia that prioritize software reliability and security. Also, BlackBerry QNX has maintained a strong foothold in Australia and New Zealand, where commercial fleets and premium imports demand certified safe and secure operating platforms.

The Android automotive OS segment is emerging as the fastest-growing segment in the Asia Pacific automotive operating system market and is projected to expand at a CAGR of 15% from 2025 to 2033. This rapid growth of the segment is driven by increasing consumer demand for seamless smartphone integration, voice-controlled navigation, and app-based infotainment features directly embedded into vehicle dashboards. In South Korea, automakers such as Hyundai and Genesis have adopted Android Automotive OS for their latest EV lineups, enabling built-in Google Assistant, Maps, and Play Store access.

China is another key growth engine for Android Automotive, with local EV manufacturers including XPeng, NIO, and BYD integrating the platform to enhance digital cockpit experiences. India is also witnessing increased Android Automotive adoption, particularly among mid-sized electric SUVs and sedans targeting younger, tech-savvy consumers.

By Commercial Vehicle Insights

The light commercial vehicles (LCVs) segment constitutes the top-performing category in the Asia Pacific automotive operating system market by accounting for 42.1% of total revenue in 2024. The dominance of the LCV segment is primarily driven by the rising digitization of logistics, delivery services, and fleet management solutions that require advanced telematics and onboard diagnostics powered by automotive operating systems.

In India, LCVs play a critical role in urban freight, e-commerce deliveries, and last-mile logistics, prompting manufacturers to embed intelligent operating systems for route optimization and fuel efficiency tracking. China's logistics sector has also seen a surge in LCVs featuring embedded automotive operating systems for remote diagnostics and driver monitoring. Japan and South Korea are leveraging LCVs in smart mobility-as-a-service (MaaS) and shared transportation programs, further boosting demand for automotive OS integration.

On the other hand, the heavy commercial vehicles (HCVs) segment, including trucks and long-haul transporters, is emerging as the fastest-growing segment in the Asia Pacific automotive operating system market and is likely to expand at a CAGR of 13.2%. The acceleration of the HCV segment is fueled by the increasing deployment of electronic logging devices (ELDs), predictive maintenance tools, and autonomous driving support systems in large freight and cargo vehicles.

In China, HCV manufacturers are integrating automotive operating systems to support smart highways and automated logistics corridors under the Ministry of Transport’s Intelligent Transportation Systems initiative. India is also witnessing a shift toward digital HCV operations, with state transport corporations mandating ELD installation in inter-city buses and goods carriers. In Australia, heavy transport operators are adopting OS-enabled telematics for real-time GPS tracking and emissions reporting.

By EV Application Insights

The battery management segment represented the dominant application in the Asia Pacific automotive operating system market by capturing 55.4% of total revenue in 2024. The lead position of the battery management segment is primarily due to the critical role battery management systems (BMS) play in ensuring electric vehicle performance, longevity, and safety.

In China, where over 9 million electric vehicles were produced in 2023, automotive OS vendors are deeply embedding BMS functionalities into vehicle control units to optimize energy distribution and thermal regulation. Japan’s EV manufacturers, including Nissan and Mitsubishi, have been actively integrating automotive operating systems into battery control modules to enhance efficiency and reduce degradation. India’s growing EV ecosystem is also prioritizing battery management, particularly among startups developing indigenous software stacks for lithium-ion packs used in two-wheelers and compact EVs.

On the contrary, the charging management segment is emerging as the fastest-growing application area for automotive operating systems in the Asia Pacific and is projected to expand at a CAGR of more than 16% in the coming years. This growth charging management segment is driven by the proliferation of public and private charging infrastructure, coupled with increasing demand for smart, interoperable EV charging solutions.

In China, the Ministry of Transport has mandated standardized communication protocols for EV charging stations. South Korea is witnessing a similar trend, with companies like Hyundai and SK Innovation investing in automotive OS-based charging interfaces that support bidirectional power flow and grid-connected EVs. In India, the Department of Heavy Industry has encouraged automakers to integrate charging management OS in FAME II-certified EVs to improve interoperability and user experience.

COUNTRY-LEVEL ANALYSIS

China Automotive Operating System Market Analysis

China remained at the forefront of the Asia Pacific automotive operating system market by contributing 30.2% of total regional revenue in 2023. As the world’s largest automobile manufacturer and EV producer, China’s automotive industry is increasingly focused on developing and integrating advanced operating systems into both domestic and export-bound vehicles. The government’s push for indigenous software ecosystems has encouraged automakers to move away from foreign OS dependencies. Besides, the Ministry of Industry and Information Technology has initiated national-level collaborations between automotive manufacturers and software developers to promote standardized automotive OS development.

Japan Automotive Operating System Market Analysis

Japan secured a significant portion of the Asia Pacific automotive operating system market. The country’s automotive industry is known for its technological sophistication, with leading OEMs such as Toyota, Honda, and Suzuki investing heavily in embedded operating systems that support vehicle autonomy, connectivity, and safety features. Japanese automakers prioritize functional safety and system stability, often opting for customized versions of QNX and Android Automotive OS to meet domestic and global standards.

India Automotive Operating System Market Analysis

India rapidly expanded in the Asia Pacific automotive operating system market. It continues to be driven by a combination of rising EV adoption, digital infrastructure investment, and government-led automotive modernization initiatives. While traditionally lagging in software integration, India is now witnessing a transformation as domestic automakers embrace digital cockpit systems and connected vehicle platforms. This shift is largely influenced by consumer demand for smart features and government policies encouraging digital upgrades in the automotive sector. The Indian government’s Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme has played a crucial role in accelerating the use of automotive operating systems in electric mobility. Moreover, India’s thriving software engineering ecosystem is enabling domestic startups to develop indigenous automotive OS solutions tailored for local conditions.

South Korea Automotive Operating System Market Analysis

South Korea is distinguished by its high penetration of smart and connected vehicle applications. The country’s automotive and technology industries work closely together, resulting in the rapid adoption of advanced infotainment, ADAS, and OTA update-capable vehicles. Companies are integrating OS platforms that support seamless connectivity, driver assistance, and AI-enhanced vehicle controls. South Korean tech firms such as Samsung and LG have entered the automotive OS domain by offering embedded platforms for digital instrument clusters, head units, and autonomous driving modules. Furthermore, the Korean government has established smart mobility corridors and pilot zones for autonomous vehicle testing, encouraging the use of standardized automotive operating systems.

Australia Automotive Operating System Market Analysis

Australia is an emerging landscape in the Asia Pacific automotive operating system market, with a growing emphasis on fleet management, smart mobility, and autonomous driving technologies. Although not a major manufacturing hub, Australia is emerging as a key market for automotive OS integration, particularly in commercial fleets and electric mobility services. The Australian government has also supported the adoption of advanced automotive operating systems through its Intelligent Transport Systems (ITS) roadmap, which encourages the use of connected and autonomous vehicle technologies. In addition, premium car imports from Germany and the U.S., which often feature embedded automotive operating systems, are growing in popularity among affluent consumers.

COMPETITVE LANDSCAPE

- The Asia Pacific automotive operating system market is marked by intense competition between global technology firms, regional software developers, and automotive original equipment manufacturers (OEMs) striving to shape the future of connected and autonomous vehicles. While multinational corporations like Google, BlackBerry, and Huawei bring established platforms and global expertise, local players are rapidly advancing indigenous alternatives that cater to unique regulatory, cultural, and infrastructure conditions across the region.

- Competition is not only centered around technological capabilities but also on how well an operating system integrates with vehicle subsystems, supports over-the-air updates, and complies with evolving safety and cybersecurity standards. Japanese and Korean automakers prioritize functional safety and system stability, favoring certified real-time operating systems like QNX. In contrast, Chinese and Indian markets show growing interest in open-source and customizable platforms that offer scalability and lower licensing costs.

- Market differentiation is further driven by strategic alliances, localized R&D investments, and ecosystem-building efforts that extend beyond the vehicle itself, encompassing charging networks, fleet management, and AI-powered diagnostics. As the automotive industry moves toward software-defined architectures, the battle for dominance in the Asia Pacific automotive operating system space is shifting from mere functionality to comprehensive integration, user experience personalization, and long-term software sustainability.

KEY MARKET PLAYERS

These are the market players that are dominating the Asia Pacific automotive operating system market, including.

- Blackberry Limited

- Huawei Technologies Co., Ltd.

- Automotive Grade Linux

- Google LLC (Android Automotive OS)

- Microsoft Corporation

- Apple Inc

- Alphabet Inc.

- Green Hills Software

- Nvidia Corporation

- Siemens

- Red Hat, Inc

- Wind River Systems, Inc

Top Players In the Market

- Huawei has emerged as a leading force in the Asia Pacific automotive operating system market with its HarmonyOS Automotive platform. Designed to support seamless connectivity, digital cockpits, and intelligent mobility features, HarmonyOS Automotive enables automakers to build software-defined vehicles tailored for electric and autonomous driving ecosystems. The company plays a crucial role in reducing regional dependency on Western-originated OS platforms by offering a homegrown alternative backed by strong government and industry support.

- BlackBerry’s QNX Software division remains a dominant player in the Asia Pacific automotive operating system landscape due to its focus on real-time performance, functional safety, and cybersecurity. QNX-based operating systems are widely used in mission-critical applications such as ADAS, instrument clusters, and infotainment units across Japan, South Korea, and Australia. The platform's ISO 26262 certification makes it a preferred choice among automakers requiring high reliability and compliance with global safety standards, reinforcing its lead position in industrialized APAC markets.

- Google’s Android Automotive OS is gaining momentum in the Asia Pacific region due to its consumer-friendly interface, deep integration with mobile ecosystems, and compatibility with AI-driven voice assistants. Automakers such as Hyundai, MG Motor, and certain Chinese EV brands have adopted Android Automotive to enhance user experience and streamline digital services within vehicles.

Top Strategies Used By Key Market Participants

- One major strategy employed by key players in the Asia Pacific automotive operating system market is deep collaboration with local automakers and Tier 1 suppliers, allowing OS vendors to embed their platforms directly into vehicle production lines rather than relying on aftermarket solutions. These partnerships help ensure compatibility, reduce development cycles, and improve long-term integration success.

- Another critical approach involves customization for regional requirements, including language localization, regulatory compliance, and integration with domestic mobility ecosystems. Companies are tailoring their automotive operating systems to align with country-specific data privacy laws, driver behavior patterns, and smart city initiatives, enhancing adoption in both developed and emerging markets across the region.

- Lastly, leading players are focusing on expanding open-source or modular OS frameworks, enabling developers and manufacturers to adapt and scale solutions according to specific vehicle needs. This strategy fosters innovation, reduces licensing costs, and encourages ecosystem growth, particularly in fast-developing EV and commercial vehicle segments where cost-effectiveness and flexibility are paramount.

RECENT MARKET NEWS

- In January 2024, Huawei announced a partnership with a leading Chinese electric vehicle manufacturer to integrate its HarmonyOS Automotive platform into next-generation EV models, aiming to enhance in-vehicle connectivity and digital cockpit capabilities while reducing reliance on foreign operating systems.

- In March 2024, BlackBerry signed a collaboration agreement with a Japanese automaker to supply QNX-based automotive operating systems for next-generation ADAS and autonomous driving modules, reinforcing its position in the high-safety segment of the APAC market.

- In June 2024, Google expanded its Android Automotive OS footprint by entering a licensing deal with a major South Korean automaker, enabling deeper integration with Google Assistant, Maps, and Play Store services across new passenger vehicle models.

- In September 2024, a prominent Indian software startup secured funding to develop a localized automotive operating system tailored for EVs, focusing on low-cost, high-efficiency deployment in domestic two-wheeler and three-wheeler mobility solutions.

- In November 2024, a consortium of Australian and New Zealand-based mobility tech firms launched a joint venture to develop a regional automotive OS framework aimed at supporting smart fleet management and autonomous logistics applications, strengthening the region’s software independence and digital mobility ambitions.

MARKET SEGMENTATION

This research report on the Asia Pacific automotive operating system market is segmented and sub-segmented into the following categories.

By Operating System Type

- QNX

- Linux

- Windows

- Android

- Others

By ICE Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

By EV Application

- Charging Management Systems

- Battery Management Systems

By Application

- ADAS & Safety Systems

- Autonomous Driving

- Body Control & Comfort Systems

- Communication Systems

- Connected Services

- Infotainment Systems

- Engine Management & Powertrain

- Vehicle Management & Telematics

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is the Asia Pacific automotive operating system market?

It refers to software platforms that control vehicle functions such as infotainment, connectivity, safety systems, EV controls, and autonomous features.

Why is the Asia Pacific automotive operating system market becoming important?

Modern cars rely heavily on software for performance, safety, driver assistance, and seamless digital connectivity.

What factors are driving growth in the Asia Pacific automotive operating system market?

EV adoption, connected car expansion, stricter safety norms, and the shift toward software-defined vehicles.

Which countries lead the Asia Pacific automotive operating system market?

China, Japan, South Korea, and India dominate due to strong automotive production and rapid tech adoption.

What types of systems are used in the Asia Pacific automotive operating system market?

Linux-based OS, Android Automotive, QNX, AUTOSAR systems, and custom OEM software platforms.

How do electric vehicles influence the Asia Pacific automotive operating system market?

EVs rely on software for battery management, charging optimization, thermal control, and real-time performance monitoring.

What challenges affect the Asia Pacific automotive operating system market?

Cybersecurity risks, system integration complexity, high software maintenance needs, and compatibility issues.

Why are software-defined vehicles shaping the Asia Pacific automotive operating system market?

Automakers now deliver features, updates, and performance improvements through software rather than mechanical upgrades.

Why are tech companies entering the Asia Pacific automotive operating system market?

Vehicles require advanced computing, AI functions, cloud access, and intuitive interfaces — strengths of major tech firms.

What is the future outlook for the Asia Pacific automotive operating system market?

The market is set for strong growth as EVs expand, autonomous driving advances, and OEMs build fully software-led mobility ecosystems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com